Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

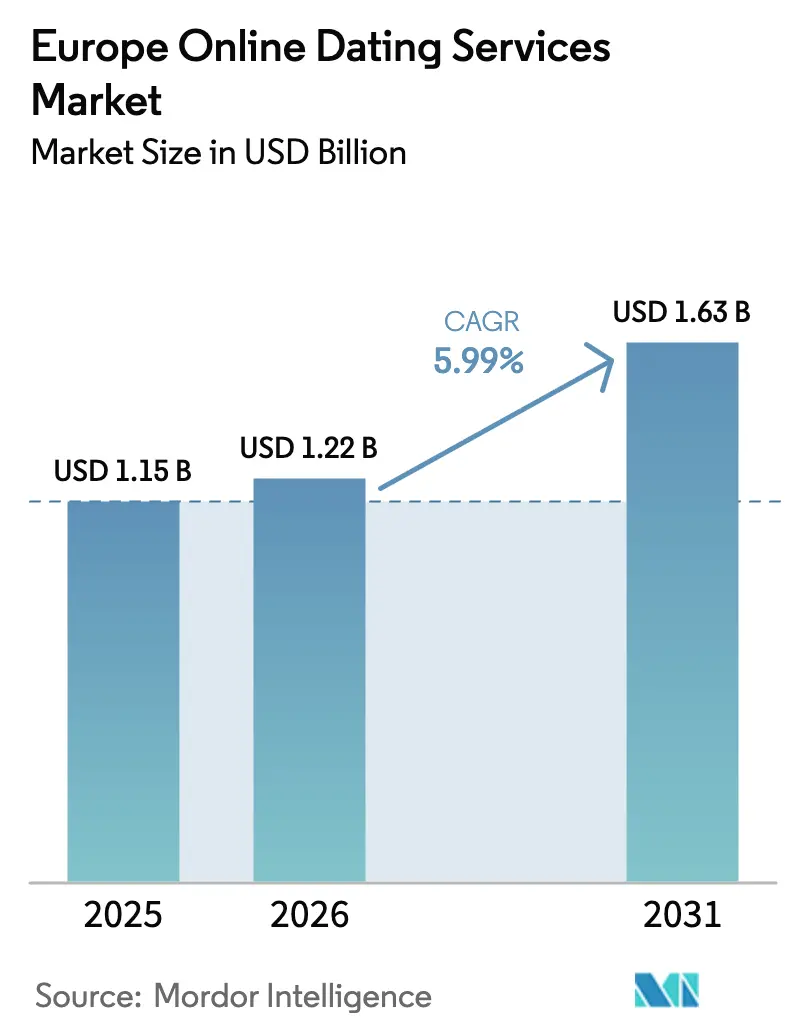

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

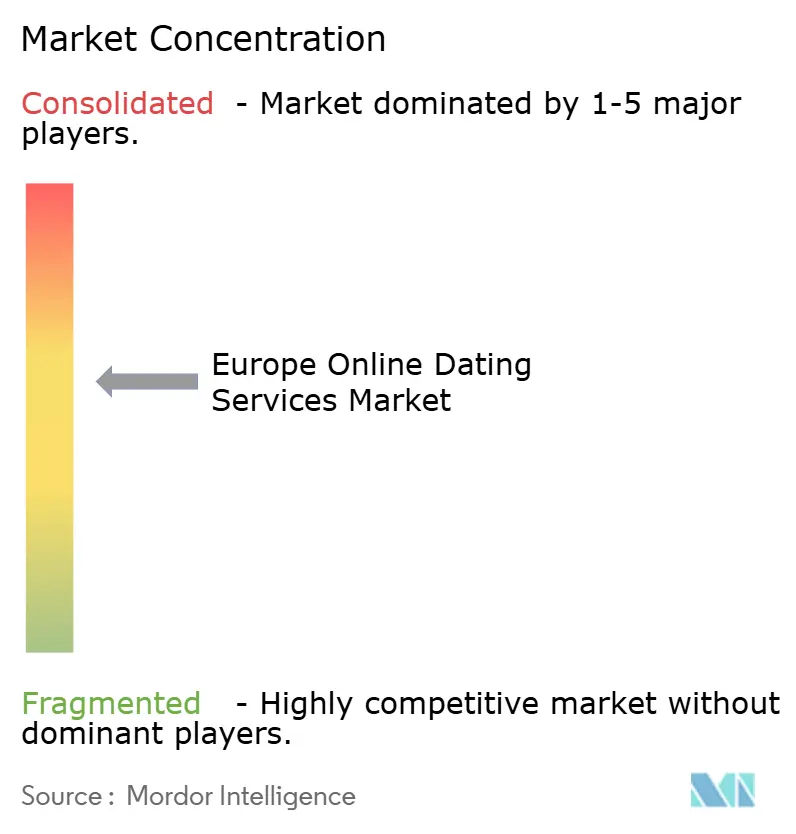

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Online Dating Services Market Analysis by Mordor Intelligence

The Europe online dating services market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.22 billion in 2026 to reach USD 1.63 billion by 2031, at a CAGR of 5.99% during the forecast period (2026-2031). This measurable rise in value signals a structural turn in how Europeans form relationships, as sharper data-privacy rules raise user trust, premium-tier spending, and long-term engagement. The General Data Protection Regulation has required tighter consent flows, yet the stronger compliance narrative has improved brand credibility among privacy-conscious millennials and Gen Z users, who now make up most paying subscribers. Match Group’s Q3 2024 revenue reached USD 895 million, with Hinge growing 36% year over year to USD 145 million, confirming that relationship-intent positioning converts better than casual models. Bumble Inc. posted USD 275 million for the same quarter, but its 7% slide in paying users to 4 million reveals subscription fatigue in saturated Western European markets.

Key Report Takeaways

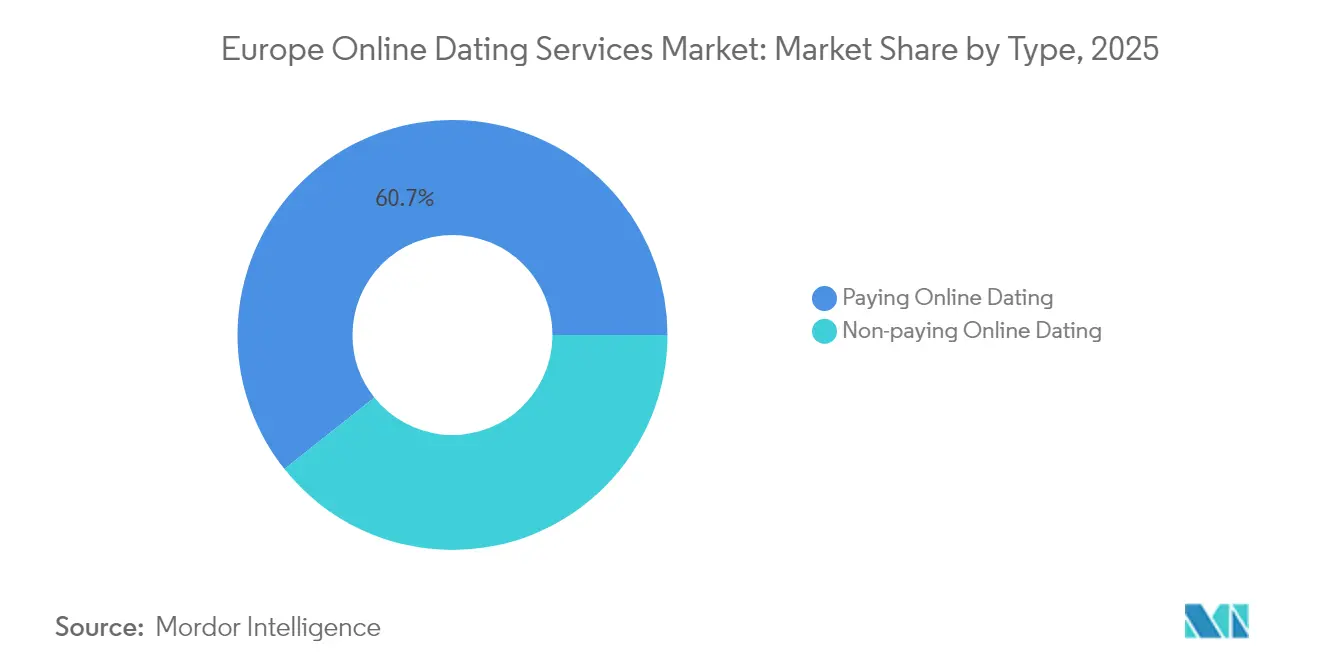

- By type, paying online dating held 60.72% of Europe online dating services market share in 2025 and is forecast to post a 7.72% CAGR through 2031.

- By device platform, mobile applications commanded 71.15% share of the Europe online dating services market size in 2025 and are projected to expand at a 7.88% CAGR.

- By age group, the 18-24 segment registered the fastest 8.64% CAGR through 2031, while the 25-34 cohort retained 39.35% share of the Europe online dating services market size in 2025.

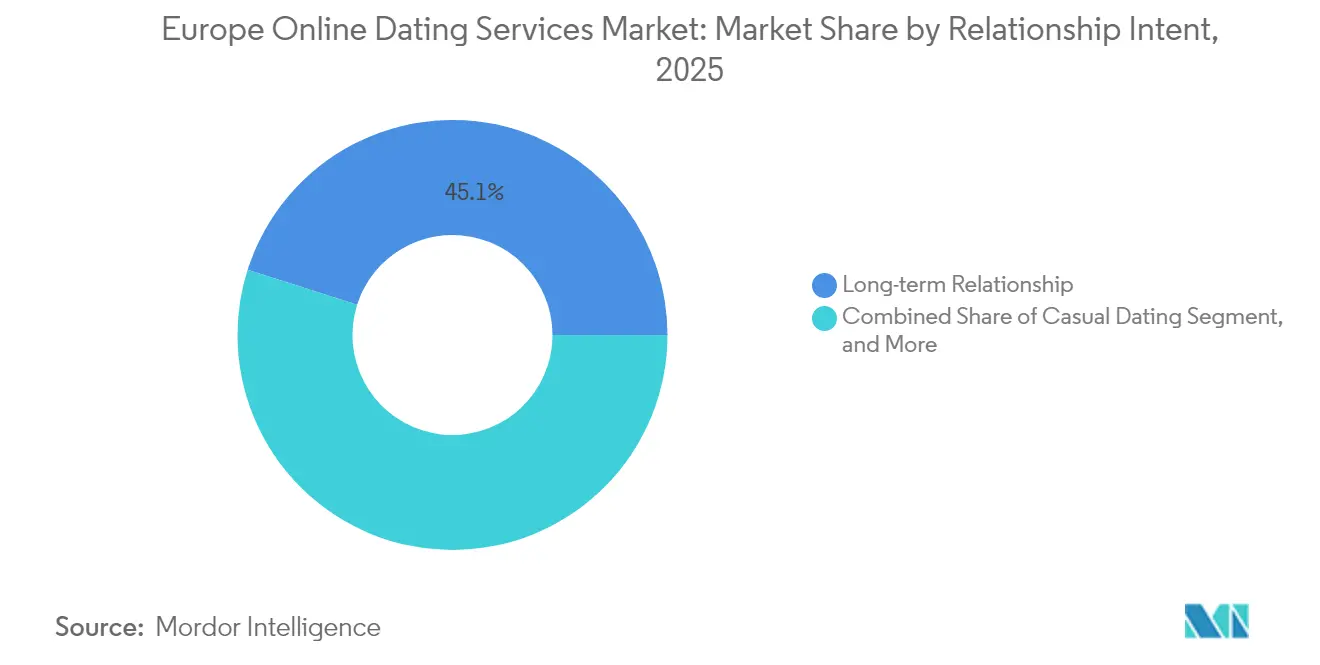

- By relationship intent, casual dating is projected to advance at an 8.35% CAGR to 2031, yet long-term seekers remain the largest segment, with a 45.10% share in 2025.

- By geography, the United Kingdom accounted for 29.95% revenue in 2025, whereas Italy is forecast to grow at a 10.25% CAGR through 2031.

- Match Group and Bumble Inc. collectively controlled roughly 60% of 2024 European revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Online Dating Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Millennial and Gen Z users embracing digital-first socialization | +1.4% | UK, Germany, France, Italy, Spain (urban centers) | Medium term (2-4 years) |

| Rising smartphone penetration and cheaper data | +1.1% | All of Europe, strongest in Italy, Spain, Eastern Europe | Short term (≤ 2 years) |

| Normalization of online dating as a social norm | +0.9% | UK, Nordics, Germany, France; extending to Southern and Eastern Europe | Long term (≥ 4 years) |

| Video dating and live streaming integration | +0.8% | UK, France, Germany, Nordics; pilots in Italy and Spain | Medium term (2-4 years) |

| AI-driven matching that boosts engagement | +1.2% | UK, Germany, France | Medium term (2-4 years) |

| Niche apps serving specific communities | +0.7% | UK, Germany, France, Nordics; rising in Italy and Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Millennial and Gen Z Users Seeking Digital-first Socialization

Millennial and Gen Z cohorts treat dating apps as primary social infrastructure rather than add-on experiences. Eurostat reported 97% daily internet usage among 16-29-year-olds in 2024, with 83% of them actively using social networks.[1]Eurostat, “Digital Economy and Society Statistics,” EC.EUROPA.EU Ofcom found that 18% of UK users aged 18-24 and 17% aged 25-34 visited dating services in May 2024.[2]Ofcom, “Online Nation 2024,” OFCOM.ORG.UK Hinge’s 36% revenue jump to USD 145 million in Q3 2024 demonstrates how intentional-dating design resonates with this audience. Delayed marriage, average first-marriage age now above 30 in Germany, France, and the UK, extends monetization windows. HER reached 15 million users, 60% of whom fall in the 18-24 bracket, underscoring youth-driven volume and engagement depth.

AI-driven Matching Algorithms Enhancing User Engagement

Artificial intelligence has moved to the front end of product differentiation, guiding compatibility predictions, conversational nudges, and personalized onboarding flows. Match Group’s AI “Matchmaker” suggests profile tweaks, while Bumble’s chat coach offers real-time tone advice. Tinder’s ID-verification rollout, which uses AI-based liveness checks, lifted matches 67% for verified users in the UK and other markets in 2024. The Schrems decision limits indefinite data aggregation, pressing platforms toward federated learning and on-device inference to stay within GDPR bounds. Incumbents with capital to retrain models enjoy an execution edge over smaller challengers.

Integration of Video Dating and Live Streaming Features Post Pandemic

Video conversation has persisted beyond lockdowns, reducing ghosting and building trust. LOVOO deployed live-video across France and Switzerland, eharmony launched 10-minute video-date scheduling Europe-wide, and Dating.com Group piloted virtual-reality dating in Germany. Roughly 40% of users tried video dating during the pandemic, and 25% continue to use it, validating infrastructure investments. Video verification also raises fraud barriers, as seen in Bumble’s Deception Detector, which blocked 95% of fake profiles and cut spam complaints 45% in its first year.

Niche Dating Apps Targeting Specific Communities Fuel Monetization

Micro-segmentation lowers acquisition costs and unlocks premium pricing. Grindr’s 14.7 million monthly active users and subscription tiers near USD 40 per month confirm scalable monetization in LGBTQ+ spaces. Feeld’s profitability with 1.5 million active users highlights sustained demand for polyamorous matchmaking. Match Group’s Archer, a gay-focused brand, tallied 1.5 million downloads in its debut year and contributed to 25% portfolio revenue growth, outweighing Tinder’s more modest expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating data-privacy concerns and breaches | -0.8% | Germany, France, Netherlands; pan-European relevance | Short term (≤ 2 years) |

| Proliferation of fake profiles and catfishing | -0.6% | UK, Germany, France, Italy, Spain | Medium term (2-4 years) |

| Urban-market saturation inflating user-acquisition costs | -0.5% | London, Paris, Berlin, Amsterdam, Stockholm, Copenhagen | Medium term (2-4 years) |

| Regulatory scrutiny on algorithmic data use | -0.7% | EU-wide enforcement led by Ireland, Italy, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Concerns over Data Privacy and Security Breaches

Norway upheld a NOK 65 million (USD 6.43 million) fine on Grindr in 2024 for sharing location and sexual-orientation data without consent. Italy’s regulator fined Nirvam EUR 200,000 (USD 232910) in February 2024 for unlawful processing of 1 million profiles. The European Data Protection Board’s October 2024 opinion declared “consent-or-pay” models incompatible with GDPR. A KU Leuven study found that 15 popular apps leaked sensitive data in 2024, six of them revealing precise location. These moves pressure platforms toward subscription-only revenue and stricter data minimization.

Proliferation of Fake Profiles and Catfishing Incidents

UK victims lost an average GBP 6,937 (USD 9253.96) per romance scam in 2024.[3] UK Action Fraud, “Romance Scam Losses 2024,” ACTIONFRAUD.POLICE.UK Tinder’s Passport and ID verification increased matches 67% for verified users, illustrating user appetite for authenticity. Bumble’s Deception Detector blocked 95% of fake accounts. Yet, deepfake technology continues to lower the costs for fraudsters, and markets with lower digital literacy remain vulnerable, thereby sustaining trust challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Premium Tiers Capture Majority Revenue

Paying services represented 60.72% of 2025 revenue and are forecast to grow at an 7.72% CAGR, buoyed by AI matching, video calls, and priority visibility bundled into subscriptions. The Europe online dating services market size attributable to paying tiers is set to outstrip freemium growth through 2031. Match retained 10 million paying Tinder users, while Hinge’s paying base climbed 38% to 1.9 million in Q3 2024. Bumble counted 4 million paying users, although the total number slipped 7%. Price hikes saw Tinder Platinum reach GBP 32.99 (USD 41) per month.

Non-paying tiers held a 39.28% share but face tighter advertising rules. The Europe online dating services market is watching the consent-or-pay debate; should regulators outlaw data-heavy ads, free tiers will shrink to basic swipes, nudging users toward subscriptions. Already, 3-5% of free users convert to paid users, yet they generate up to 90% of the platform's revenue.

By Device Platform: Mobile Dominance Reinforced by 5G and App Innovation

Mobile applications captured 71.15% of 2025 revenue and will post an 7.88% CAGR as 5G spreads and push-notification engagement deepens. The Europe online dating services market relies on mobile location discovery, camera-enabled content, and in-app billing, advantages desktop cannot match. Bumble reported USD 221 million mobile revenue versus modest web totals.

Desktop and web kept a 28.85% share, favored by older users who complete long questionnaires on larger screens. Responsive web design and progressive web apps help desktop-heavy brands avoid 30% app-store fees. Regulatory parity under the Digital Services Act removes historic compliance advantages for web-only operators, keeping both platforms in play.

By Age Group: Youth Cohorts Accelerate While Core Segment Stabilizes

Users aged 18-24 are growing at 8.64% CAGR through 2031 as Gen Z adopts app-based dating early. HER’s 15 million users are 60% in this bracket. Spending, however, lags older cohorts, prompting platforms to refine freemium funnels.

The 25-34 cohort accounted for 39.35% of 2025 revenue and remains the Europe online dating services market’s core pay-segment thanks to higher income and relationship urgency. Hinge’s USD 145 million Q3 2024 revenue underscores this demographic’s monetization power. Older groups exhibit higher average revenue per user but slower growth.

By Relationship Intent: Long-term Seekers Dominate Revenue Despite Casual Growth

Long-term seekers made up 45.10% of 2025 revenue. Hinge’s “Designed to be Deleted” mantra and eharmony’s video scheduling cater to these users, who accept 20-30% higher subscription fees and show lower churn.

Casual dating is advancing at an 8.35% CAGR, powered by urban professionals and younger demographics. Badoo’s 10% revenue growth to USD 54 million and Grindr’s instant-meetup “Right Now” tool show continuing demand. Platforms must balance high-value long-term seekers with volume-driven casual users.

By Sexual Orientation: LGBTQ+ Platforms Outpace Heterosexual Growth

Heterosexual platforms retained a 67.20% share in 2025, though growth moderates as acquisition costs rise. Tinder’s 10 million paying users remain a formidable base but expand more slowly than niche rivals.

LGBTQ+ platforms are projected to grow at an 8.03% CAGR. Grindr’s 14.7 million monthly actives and USD 2 billion valuation, along with HER’s 15 million users, illustrate robust community monetization. Match’s gay-focused Archer debuted with 1.5 million downloads, showing incumbents hedging with niche entries.

Geography Analysis

The United Kingdom held 29.95% of 2025 revenue, underpinned by high smartphone penetration and cultural acceptance of app-based dating. Ofcom tallied 4.9 million adult visitors to dating services in May 2024. Tinder’s ID verification helped increase verified matches by 67%, which is valuable in a market where romance scam losses average USD 8,700 per case. Gender imbalances, 65% male to 35% female, on many apps drive algorithmic throttling and paid boosts for visibility.

Italy is the fastest-growing geography with a 10.25% CAGR to 2031, thanks to youthful demographics and later marriage ages. Regulatory scrutiny is rising but remains lighter than in Germany or the Netherlands, allowing aggressive feature rollouts such as LOVOO’s live-video expansion.

Germany, France, and Spain form a mature cluster wrestling with the consent-or-pay debate. Advertising-funded models risk erosion, prompting pivots to subscriptions and experimental technologies, such as Dating.com Group’s VR dating in Germany.

Russia remains fragmented. Domestic players Mamba and Teamo.ru dominate after data-localization rules sidelined Western apps. Nordic countries boast 95% internet penetration and early video-dating uptake; nonetheless, saturation in Stockholm and Copenhagen is inflating acquisition costs, advantaging multi-brand incumbents like Happn.

Competitive Landscape

Match Group and Bumble Inc. command roughly 60% of European revenue, giving the Europe online dating services market a moderately concentrated profile. Match’s Q3 2024 mix USD 503 million from Tinder, USD 145 million from Hinge, and USD 204 million from evergreen brands shows insulation from single-app volatility. Bumble’s USD 275 million quarter highlights women-first branding, though a 7% dip in paying users exposes pricing limits.

Niche leaders grow faster. Grindr’s 14.7 million monthly active users validate the economics of the LGBTQ+ scale, while Feeld’s profitability proves the viability of micro-segmentation. AI safety tools create a technology moat, Bumble’s Deception Detector blocks 95% of fake profiles, while Tinder’s verification increases match rates by 67%. Smaller entrants struggle to fund comparable R&D, widening the competitive gap.

White-space opportunities lie in seamless age verification under the Digital Services Act and in federated-learning-based matching that complies with Schrems constraints. Once Dating’s one-match-per-day model and Archer’s community focus show incumbents hedging against swipe fatigue and niche insurgents. Overall, innovation pivots on AI personalization, video infrastructure, and portfolio breadth.

Europe Online Dating Services Industry Leaders

Match Group Inc.

Bumble Inc.

Badoo Ltd

FTW and Co (happn)

Meetic SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Match Group extended its AI “Matchmaker” feature across Europe, using on-device inference to comply with GDPR limits.

- February 2025: eharmony introduced video-date scheduling continent-wide, adding 10-minute calls to speed compatibility checks.

- January 2025: Bumble rolled out “Opening Moves” across Europe, allowing women to pre-set conversation starters that men must respond to.

- January 2025: Grindr launched “Roam,” enabling location-flexible browsing to monetize travel-oriented discovery.

Europe Online Dating Services Market Report Scope

Online dating is a system that enables users to connect through digital channels, introduce themselves, and discover potential partners, typically to foster deeper connections. Rising internet penetration, particularly in the region's major developing economies, as well as the rapid integration of technology, which has increased smartphone usage, are the main factors supporting the market growth of online dating services.

The Europe Online Dating Services Market Report is Segmented by Type (Non-paying Online Dating, Paying Online Dating), Device Platform (Mobile Applications, Desktop and Web Platforms), Age Group (18-24 Years, 25-34 Years, 35-44 Years, 45 Years and Above), Relationship Intent (Casual Dating, Long-term Relationship, Niche Interest Matchmaking), Sexual Orientation (Heterosexual Platforms, LGBTQ+ Platforms), and Geography (Germany, United Kingdom, France, Spain, Italy, Russia, Nordics, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| Non-paying Online Dating |

| Paying Online Dating |

By Device Platform

| Mobile Applications |

| Desktop and Web Platforms |

By Age Group

| 18-24 Years |

| 25-34 Years |

| 35-44 Years |

| 45 Years and Above |

By Relationship Intent

| Casual Dating |

| Long-term Relationship |

| Niche Interest Matchmaking |

By Sexual Orientation

| Heterosexual Platforms |

| LGBTQ+ Platforms |

By Country

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Nordics (Denmark, Sweden, Norway, Finland) |

| Rest of Europe |

| By Type | Non-paying Online Dating |

| Paying Online Dating | |

| By Device Platform | Mobile Applications |

| Desktop and Web Platforms | |

| By Age Group | 18-24 Years |

| 25-34 Years | |

| 35-44 Years | |

| 45 Years and Above | |

| By Relationship Intent | Casual Dating |

| Long-term Relationship | |

| Niche Interest Matchmaking | |

| By Sexual Orientation | Heterosexual Platforms |

| LGBTQ+ Platforms | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Nordics (Denmark, Sweden, Norway, Finland) | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe online dating services market in 2026?

The market is valued at USD 1.22 billion in 2026 and is projected to reach USD 1.63 billion by 2031.

What CAGR is expected for Europes online dating sector through 2031?

The market is forecast to grow at a 5.99% CAGR between 2026 and 2031.

Which segment holds the largest share of dating-app revenue?

Paying online dating accounted for 60.72% of 2025 revenue and is expanding faster than free options.

Which age group is growing most quickly on dating platforms?

Users aged 18-24 are growing at a 8.64% CAGR, driven by Gen Zs digital-first lifestyle.

What role do privacy regulations play in market growth?

GDPR-driven consent requirements raise compliance costs but also boost user trust, supporting premium-tier growth even as ad-funded models shrink.

Which country is forecast to be the fastest-growing European market?

Italy is projected to post a 10.25% CAGR through 2031, helped by younger demographics and later marriage trends.

Page last updated on: