Payment Orchestration Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

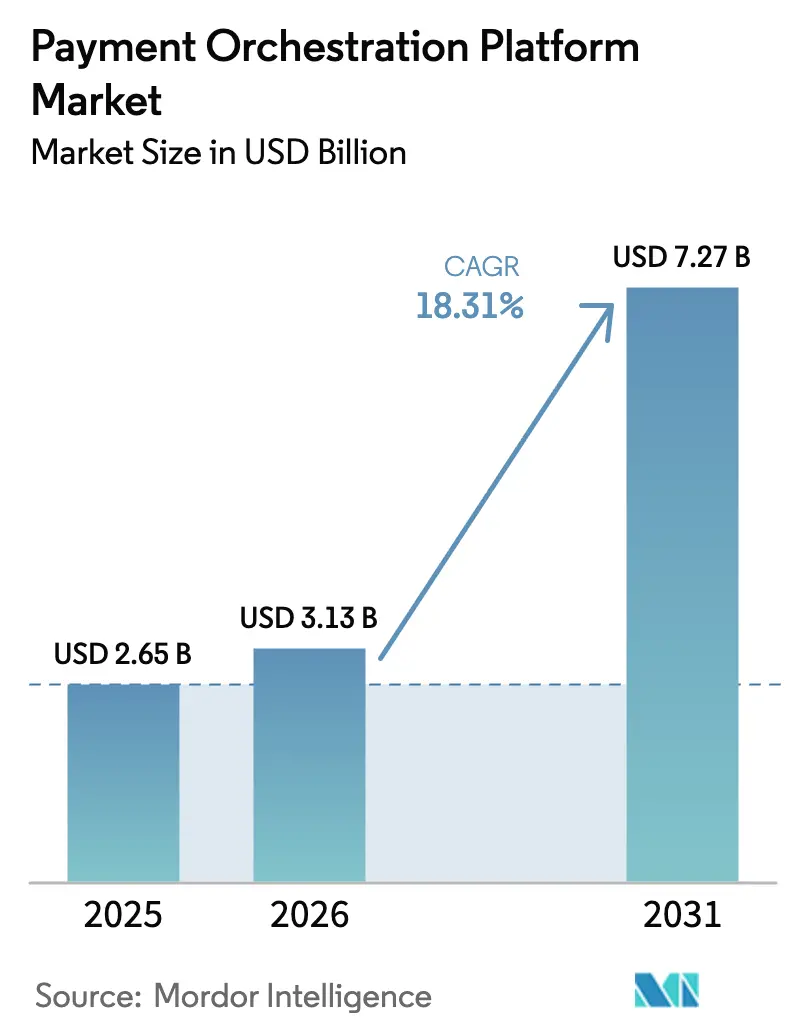

| Market Size (2026) | USD 3.13 Billion |

| Market Size (2031) | USD 7.27 Billion |

| Growth Rate (2026 - 2031) | 18.31% CAGR |

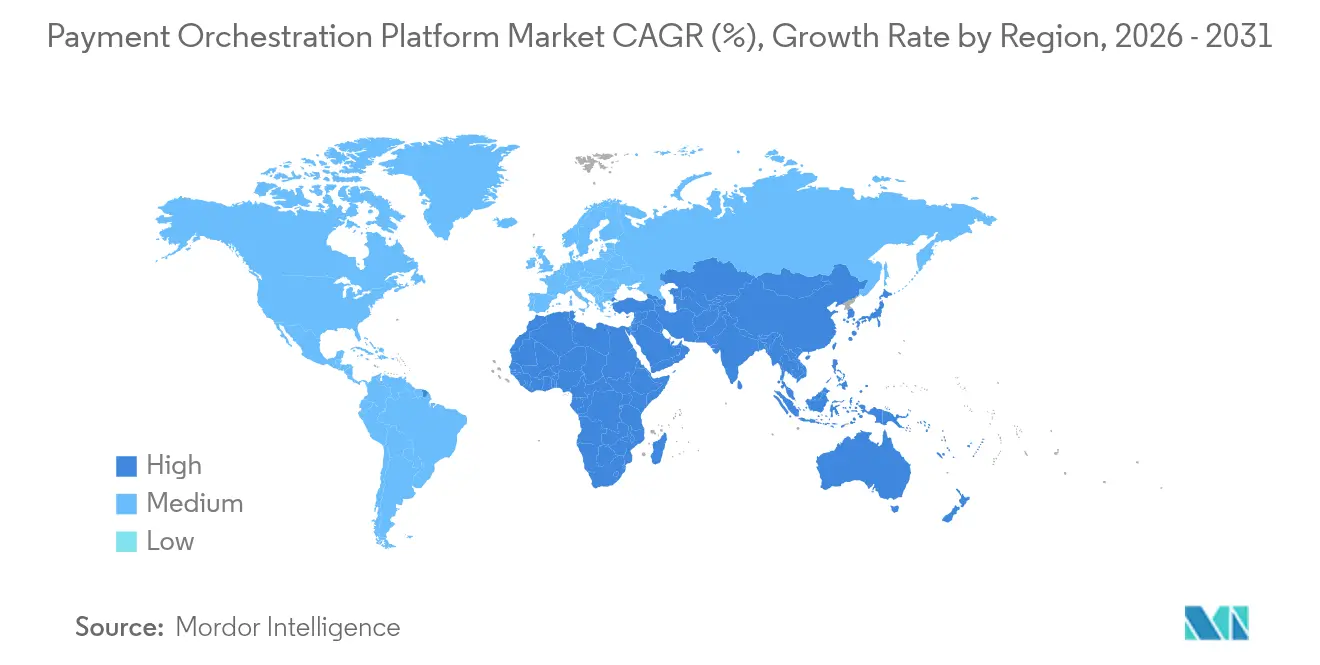

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

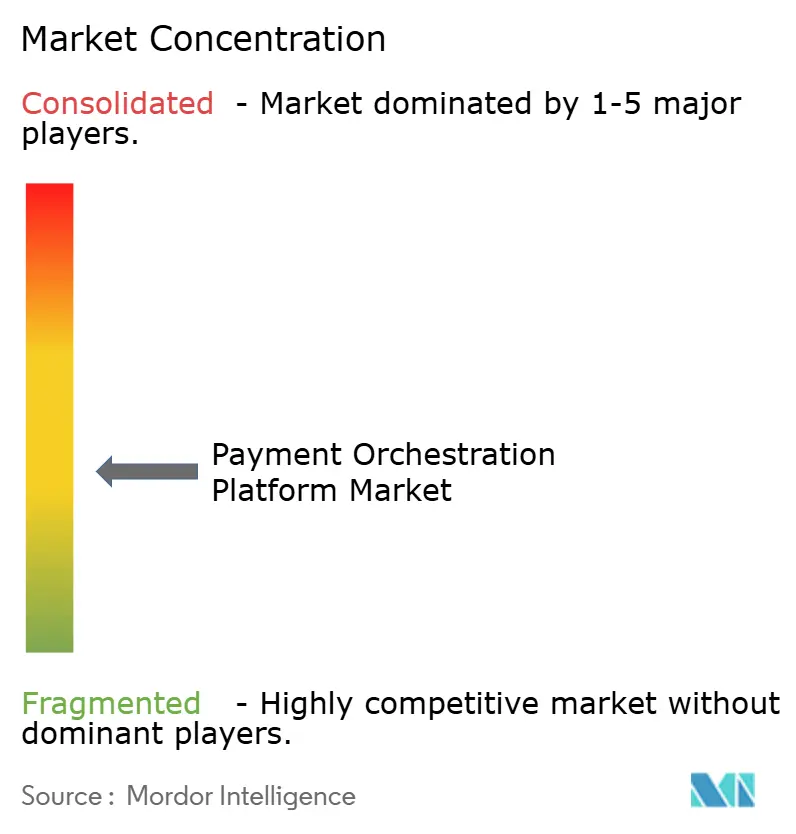

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Payment Orchestration Platform Market Analysis by Mordor Intelligence

The payment orchestration platform market size is expected to grow from USD 2.65 billion in 2025 to USD 3.13 billion in 2026, and is forecast to reach USD 7.27 billion by 2031, at an 18.31% CAGR over 2026-2031. Expansion is underpinned by the growing complexity of multi-provider payment ecosystems, rising real-time payment adoption, and merchants’ need for intelligent routing that lifts approval rates while lowering cost-per-transaction. Asia-Pacific’s vibrant fintech scene is setting the pace with a 20.4% regional CAGR, yet North America retains scale leadership, anchored by deep e-commerce penetration and early launches such as FedNow. In parallel, B2B workflows dominate volume at 55% share, though B2C deployments buoyed by frictionless checkout mandates are growing 22.3% a year. Healthcare is the fastest-growing end-user vertical, moving at a 25.1% CAGR as telehealth providers streamline billing. Competitive intensity remains high as payment processors, pure-play orchestrators, and cloud-native fintechs pursue share through acquisitions, AI-driven routing enhancements, and regional expansion.

Key Report Takeaways

- By transaction type, B2B payments held 54.40% of payment orchestration platform market share in 2025, while the B2C segment is forecast to expand at 21.63% CAGR through 2031.

- By deployment mode, cloud-based platforms captured 77.20% of the payment orchestration platform market size in 2025 and are set to grow at 19.68% CAGR to 2031.

- By organization size, large enterprises commanded 63.30% share of the payment orchestration platform market in 2025; SMEs record the fastest projected CAGR at 20.72% for 2026-2031.

- By end-user industry, retail and e-commerce led with 59.10% revenue share in 2025, whereas healthcare is advancing at a 24.4% CAGR to 2031.

- By geography, North America accounted for 37.70% of payment orchestration platform market share in 2025; Asia-Pacific is the fastest-growing region at 19.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Payment Orchestration Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| B2B Dominance in Cross-border E-commerce Remittances | +4.2% | Global, with concentration in North America, Europe, and Asia-Pacific | Medium term |

| Surge in Smart-Routing Demand Among High-Growth Fin-Tech Merchants in Asia | +3.8% | Asia-Pacific, with spillover to North America | Short term |

| Consolidation of Acquirer Landscape in Europe Driving Need for Vendor-Neutral Orchestration | +2.9% | Europe, with spillover to North America | Medium term |

| Token-Based Network Expansion (Network Tokens, SRC) Boosting Multi-PSP Integration | +2.5% | Global, with early adoption in North America and Europe | Medium term |

| Real-time-Payment Rails Adoption (FedNow, UPI, PIX) Requiring Dynamic Routing Logic | +2.1% | Global, with concentration in North America, Asia-Pacific, and Latin America | Short term |

| Marketplace Compliance (DAC-7, Inform Consumers Act) Accelerating Split-Payment Workflows | +1.9% | Europe and North America | Medium term |

| Source: Mordor Intelligence | |||

B2B Dominance in Cross-border E-commerce Remittances

Cross-border B2B payment value is set to climb 40% by 2028, fueling adoption of orchestration layers that can juggle multi-currency settlement, local compliance and blockchain-enabled rails. Stablecoins moved USD 32 trillion in 2024 and are on track to reach 20% of global cross-border flows, creating a USD 60 trillion addressable opportunity for platforms that embed tokenised liquidity. [1]BVNK, “Blockchain in Cross-Border Payments: 2025 Guide,” BVNK, bvnk.com Major institutions such as Mastercard and J.P. Morgan are piloting interoperable blockchain corridors aimed at B2B use cases, signalling that orchestration logic must now account for both fiat and on-chain rails. As transaction values rise, enterprises seek centralised control points that can optimise routing across card, account-to-account and crypto channels while enforcing consistent KYC and sanction screening.

Surge in Smart-Routing Demand Among High-Growth Fin-Tech Merchants in Asia

Asian merchants report at least a 20% uplift in approval rates after deploying AI-driven routing engines, a metric that directly converts into revenue gains. [2]Akurateco, “Worldwide Payments Orchestration Platform,” Akurateco, akurateco.com Japan’s e-commerce market alone is forecast to grow from USD 230 billion to USD 650 billion by 2032, driving demand for orchestration partners that can switch between local schemes, global cards and alternative payment methods in milliseconds. Nuvei’s acquisition of Paywiser Japan delivers direct acquiring links to major schemes, illustrating how providers are localising connectivity to capture escalating Asian volumes. With online buyers in Japan set to surpass 100 million by 2026, the capacity to learn from transaction-level data and re-route payments in real time becomes a board-level priority for merchants targeting conversion gains.

Consolidation of Acquirer Landscape in Europe Driving Need for Vendor-Neutral Orchestration

Europe’s acquirer base is shrinking through M&A, exemplified by Global Payments’ purchase of takepayments and TokenEx’s merger with IXOPAY. Merchants consequently fear over-reliance on single processors and are layering vendor-neutral orchestration to retain negotiating leverage. The European Payments Initiative’s Wero wallet adds another proprietary network that merchants must support, magnifying integration complexity. Simultaneously, draft PSD3 rules extend supervision to technical service providers, meaning orchestrators must invest in risk management modules that satisfy bank-grade oversight. For retailers scaling pan-EU checkout, the ability to plug-and-play new acquirers without code rewrites is fast becoming a prerequisite.

Token-Based Network Expansion Boosting Multi-PSP Integration

Network tokenisation has proven its commercial worth: Visa reports a 3% jump in approval rates and a 50% fraud reduction for tokenised transactions. [3]Primer, “Demystifying Network Tokens,” Primer, primer.io Merchants therefore demand orchestration engines that can propagate network tokens across every integrated PSP, not simply the incumbent gateway. Visa’s Cloud Token Framework and Mastercard’s Digital Enablement Services now enable cross-device token portability, pushing orchestration platforms to update vaults, risk scoring and routing decision trees. Adyen is already a leading third-party tokenizer, positioning itself to monetise merchant appetite for higher authorisation and lower chargeback rates. As Secure Remote Commerce reaches 80% adoption among large e-commerce sites, orchestration platforms that fail to support token routing risk obsolescence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surcharging and Interchange-Fee Caps Diluting Processor Margins for Orchestrators | -1.8% | Europe and North America | Medium term |

| EU PSD3/PSR Draft Heightening Liability for Technical Service Providers | -1.3% | Europe, with spillover to global providers serving European markets | Medium term |

| Limited 3-DS Exemptions Curbing Approval-Rate Uplift in High-Risk Sectors | -0.9% | Global | Short term |

| Scarcity of Certified Cloud HSM Capacity in LATAM | -0.7% | Latin America | Short term |

| Source: Mordor Intelligence | |||

Surcharging and Interchange-Fee Caps Diluting Processor Margins for Orchestrators

The EU’s MIF Regulation caps credit-card interchange at 0.3% and debit at 0.2%, stripping EUR 5-6 billion (USD 5.5-6.6 billion) in issuer revenue each year. As processors compress fees to stay competitive, orchestration platforms that earn variable basis-point spreads face margin squeeze. Parallel moves by the US Congress to advance the Credit Card Competition Act could replicate fee pressure in North America. Faced with diminished take rates, orchestrators are pivoting to outcome-based pricing anchored on approval-rate improvement, fraud loss reduction or working-capital savings, yet such models demand sophisticated analytics investments that raise fixed costs.

EU PSD3/PSR Draft Heightening Liability for Technical Service Providers

The draft PSD3 package places direct compliance obligations and fraud liability on technical intermediaries, including orchestration vendors. [4]LexisNexis Risk Solutions, “From PSD2 to PSD3 Regulation: What You Need to Know,” LexisNexis Risk Solutions, risk.lexisnexis.co.uk Stronger customer authentication must be adaptive and context-based; refunds for fraud must be immediate; and identity verification standards tighten. Smaller orchestrators lacking in-house regulatory teams could struggle to certify new controls across 27 EU jurisdictions, curbing their ability to scale. Larger incumbents may leverage compliance mastery as a moat, accelerating consolidation. For merchants, heightened due-diligence on provider risk is set to elongate procurement cycles and marginally temper platform adoption rates in Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: B2B Transactions Reshape Orchestration Priorities

B2B flows accounted for 54.40% of payment orchestration platform market share in 2025, reflecting enterprises’ need to rationalise multi-currency, multi-acquirer relationships. Elevated B2B non-cash growth at 14% year-on-year is translating into sustained license renewals and broader feature uptake, ensuring the payment orchestration platform market retains a strong corporate footprint. Blockchain interoperability pilots by Mastercard and J.P. Morgan signal that large treasuries now expect orchestrators to harmonise traditional rails with tokenised liquidity.

B2C implementations, in contrast, accelerate at 21.63% CAGR as digital merchants chase frictionless checkout and higher authorisation rates. Consumer endpoints increasingly demand biometric authentication, one-click token wallets and split-payment options at cart, all of which intensify routing logic. While C2C volumes remain niche, the rise of gig-economy payouts and social-commerce group purchases nudges orchestrators toward more versatile API sets. Providers that can contextualise both business and consumer flows under one analytics layer are best positioned to cross-sell additional modules and cement client stickiness.

By Deployment Mode: Cloud Flexibility Drives Market Evolution

Cloud delivery secured 77.20% of the payment orchestration platform market size in 2025 and is forecast to rise further on a 19.68% CAGR. Merchants value the single-integration model where 450-plus connectors, as offered by Akurateco, are perpetually updated without internal IT lift. Modular microservices enable feature toggling, letting merchants test-and-learn AI routing or network tokenisation without full platform re-writes.

On-premise and private-cloud instances persist in regulated verticals such as government payments and top-tier banking, yet the trend line favours hybrid architectures that retain key encryption modules behind the corporate firewall while outsourcing routing intelligence to cloud clusters. Cloud-based Hardware Security Modules, now available across the major hyperscalers, soften auditor concerns and accelerate migration. Consequently, cloud-first newcomers enjoy time-to-market advantages, while legacy processors must retrofit containerised components to sustain relevance.

By Organization Size: SMEs Drive Accelerated Adoption Curves

Large enterprises still hold 63.30% of payment orchestration platform market revenue, justified by complex multi-acquirer footprints that span countries and channels. These firms deploy orchestration to negotiate fee discounts, apply data-driven retry algorithms and centralise compliance logging. Yet SMEs constitute the fastest-growing buyer group at 20.72% CAGR, energised by lower set-up costs and simplified API kits.

Flatpay’s USD 49.5 million fund-raise exemplifies venture capital appetite for SME-centric orchestration propositions, while ISV partnerships embed routing functions inside vertical software stacks – from gym management to B2B SaaS billing. As SME card acceptance climbs from 34% toward 75%, orchestration vendors that offer pay-as-you-grow tiers, self-service onboarding and pre-configured connectors stand to capture incremental share. With churn-prone micro-merchants, retention will hinge on demonstrable cost savings and dashboard clarity rather than multi-year contracts.

By End-user Industry: Retail Dominates While Healthcare Accelerates

Retail and pure-play e-commerce merchants delivered 59.10% of 2025 revenue, ensuring that every roadmap milestone remains anchored to checkout conversion and basket-abandonment metrics. The US e-commerce sector is projected to rise 54% between 2024 and 2029, reinforcing the payment orchestration platform market as foundational infrastructure for digital storefronts. Token vaulting, one-click wallets and regional payment method roll-outs dominate feature backlogs.

Healthcare, however, records a 24.4% CAGR that is overtaking general retail growth velocity. Telehealth providers now blend HIPAA compliance with real-time eligibility checks and insurance co-pays, prompting specialists such as Gr4vy to release sector-specific orchestration modules. VisitPay’s custom deployment for R1 RCM shows how orchestration can reconcile patient identities, split insurer-patient responsibility and meet stringent audit controls. Early adopters report improved cash collection cycles and fewer denied transactions, validating healthcare as the next frontier for scale-out.

Geography Analysis

North America leads with 37.70% of payment orchestration platform market share in 2025, driven by advanced e-commerce maturity, widespread token adoption and real-time rails such as FedNow that necessitate adaptive routing logic. Legislative proposals like the Credit Card Competition Act could reshape interchange dynamics, compelling merchants to lean harder on orchestration to arbitrate network costs. Stripe, PayPal and regional upstarts funnel R&D into AI-based decision engines; PayPal, for instance, processed USD 1.68 trillion in total payment volume during 2024, underscoring the scale on which incremental approval gains translate into sizeable revenue.

Asia-Pacific posts the fastest CAGR at 19.95% for 2026-2031 and is on track to rival North American volume by decade-end. India’s UPI has normalised instant micro-payments, with cross-border instant transfers tipped to reach 42% of flows by 2028. Over 97% of enterprises in the region are MSMEs, a segment increasingly serviced by orchestrators that bundle localised acceptance and embedded financing. Providers expanding across ASEAN and Japan, such as Nuvei, emphasise direct acquiring and alternative payments that resonate with domestic buyer behaviour.

Europe wrestles with PSD3 and the Payment Services Regulation, both of which broaden liability while promoting open finance. Merchant appetite for fallback routing soared after recent acquirer mergers, furthering the payment orchestration platform market’s penetration among mid-tier retailers. Open-banking-driven account-to-account checkouts are projected to displace a share of card volume, pushing orchestrators to harmonise risk modelling across card and bank rails. Latin America, powered by Brazil’s PIX success, witnesses rising demand for orchestrators that can translate real-time mandates into frictionless cross-border settlement. Finally, the Middle East and Africa, although nascent, exhibit double-digit growth as regulators lay out fintech sandboxes and domestic instant-payment schemes.

Competitive Landscape

Competition is fragmented, blending incumbent processors, specialised orchestration vendors and emerging API-first fintechs. PayPal and Stripe together influence 67% of payment management adoption, giving them brand equity and data scale that feed superior decision networks. Adyen follows with an 8.91% slice of the payment orchestration platform market size, leveraging single-stack acquiring and its proprietary AI engine, Uplift, to justify premium pricing.

Pure-play orchestrators such as CellPoint Digital, IXOPAY and Spreedly pitch vendor-neutral independence, promising merchants negotiating leverage across gateway and acquirer contracts. CellPoint Digital’s travel-sector focus equips airlines to process up to 7.9 million transactions an hour at 99.999% uptime, a reliability benchmark that positions it as category specialist. IXOPAY combines tokenisation from TokenEx with rule-based routing, a portfolio that resonates with high-risk merchants seeking 3DS optimisation.

Artificial intelligence represents the next battleground. Visa’s purchase of Featurespace secures real-time behavioural fraud scoring, while Worldpay’s Ravelin buyout targets approval-rate optimisation through machine learning. Stripe’s alliance with OpenAI and NVIDIA embeds large-language-model tooling across the payment lifecycle, automating dispute evidence and refining issuer communications. Incumbents that can harness proprietary data at scale are likely to build durable competitive advantages, yet agile specialists remain attractive acquisition candidates for processors looking to fill capability gaps.

Payment Orchestration Platform Industry Leaders

Adyen N.V.

PayPal Holdings Inc.

Stripe Inc.

Worldline S.A.

Nuvei Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nuvei partnered with Temu to add localised card acquiring and alternative payment methods worldwide, improving customer reach while cementing Nuvei’s processor-agnostic orchestration credentials.

- March 2025: Stripe introduced a modular product catalogue that lets merchants adopt orchestration, billing or risk tools à la carte, signalling a shift toward platform unbundling that intensifies marketplace rivalry.

- February 2025: CellPoint Digital launched a travel-focused payment orchestration platform capable of handling USD 8 billion annual volume and 7.9 million transactions per hour, positioning itself as infrastructure for high-throughput verticals.

- January 2025: Nuvei’s acquisition of Paywiser Japan delivered direct scheme connectivity in a market forecast to triple e-commerce sales by 2032, illustrating strategy to embed local capabilities into its global orchestration stack.

Global Payment Orchestration Platform Market Report Scope

A payment orchestration platform (POP) consolidates integrations with different payment services, such as payment methods and PSPs, into a single platform. Using payment orchestration, merchants can route transactions across these services based on custom rules and conditions.

The payment orchestration platform market is segmented by type (B2B, B2C, other types), by end-users (BFSI, retail and e-commerce, healthcare, travel and hospitality, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| B2B |

| B2C |

| C2C |

| Cloud-Based |

| On-Premise / Private Cloud |

| Large Enterprises |

| SMEs |

| BFSI |

| Retail and E-commerce |

| Travel and Hospitality |

| Healthcare |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Type | B2B | |

| B2C | ||

| C2C | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise / Private Cloud | ||

| By Organization Size | Large Enterprises | |

| SMEs | ||

| By End-user Industry | BFSI | |

| Retail and E-commerce | ||

| Travel and Hospitality | ||

| Healthcare | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving the strong CAGR in the payment orchestration platform market?

Rapid adoption of real-time payment rails, rising cross-border B2B volumes and merchants’ need for AI-enabled smart routing together support an 18.31% CAGR through 2031.

Why are SMEs now a priority segment for orchestration vendors?

API-first architectures and pay-as-you-grow pricing lower entry barriers, letting SMEs leverage the same multi-provider optimisation previously reserved for large enterprises; SME demand is growing 20.72% a year.

How do interchange-fee caps affect orchestration platform economics?

Caps squeeze acquirer margins, prompting orchestrators to shift from per-transaction fees to outcome-based pricing that highlights approval-rate gains and cost savings.

Which region offers the fastest growth outlook?

Asia-Pacific leads with a 19.95% CAGR thanks to real-time payment systems like UPI and a large base of digitally engaged MSMEs requiring multi-rail optimisation.

What differentiates pure-play orchestrators from payment processors that offer orchestration?

Pure-plays remain vendor-neutral, enabling merchants to switch acquirers without friction and to apply universal token vaulting, whereas processors often prioritise their in-house acquiring rails.

How is network tokenisation improving approval rates?

Visa reports a 3% authorisation uplift and 50% fraud reduction when network tokens replace PANs, benefits that orchestration engines multiply by distributing tokens across every connected PSP.

Page last updated on: