Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

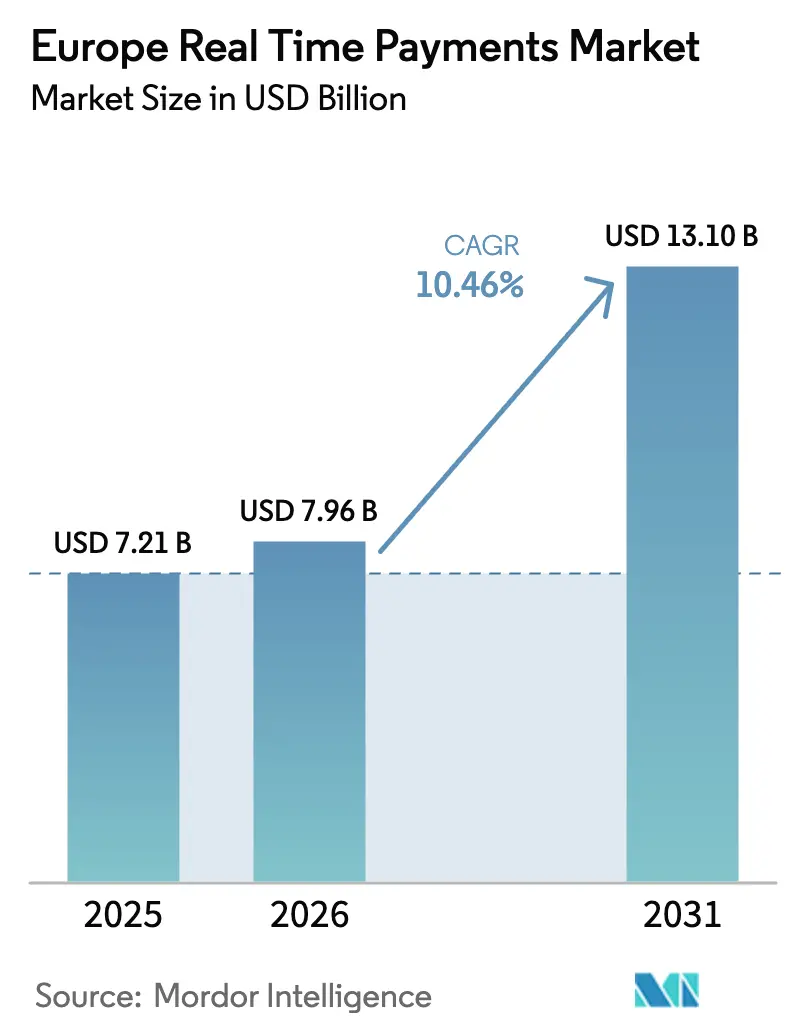

| Base Year Market Size (2025) | USD 7.21 Billion |

| Market Size (2026) | USD 7.96 Billion |

| Market Size (2031) | USD 13.1 Billion |

| Growth Rate (2026 - 2031) | 10.46% CAGR |

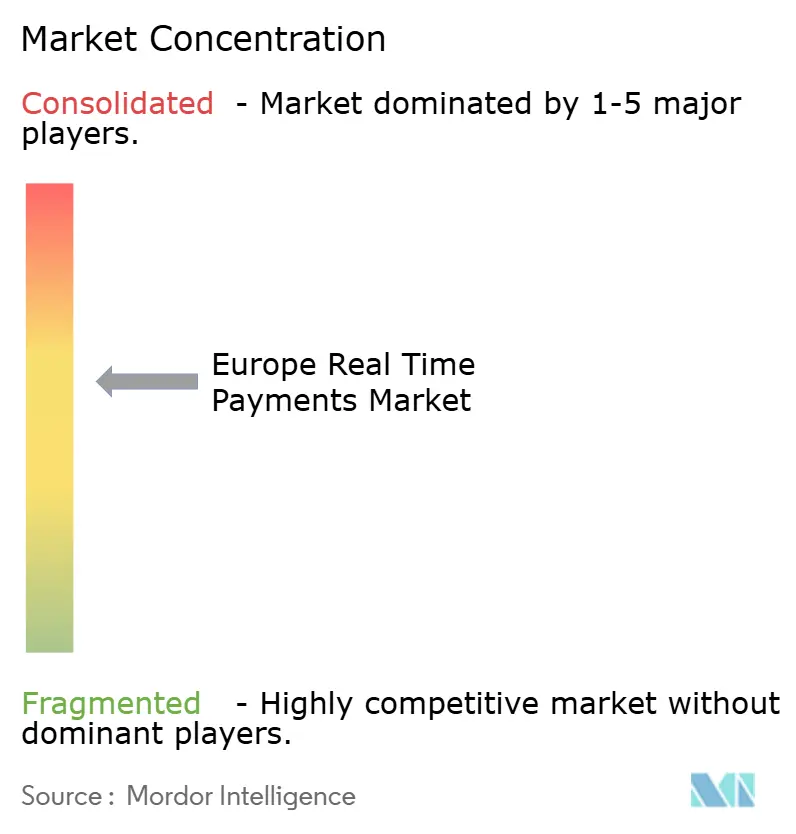

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Real Time Payments Market Analysis by Mordor Intelligence

Europe real time payments market size in 2026 is estimated at USD 7.96 billion, growing from 2025 value of USD 7.21 billion with 2031 projections showing USD 13.1 billion, growing at 10.46% CAGR over 2026-2031. Rapid regulatory harmonization—most notably the Instant Payments Regulation mandating cost-parity for euro-denominated instant transfers—has removed the EUR 2.19 (USD 2.52) average premium that previously restrained adoption. [1]European Central Bank, “TIPS Statistics 2024,” ecb.europa.eu The pricing reset forces banks to compete on service quality, triggering accelerated investment in API connectivity, risk controls and liquidity optimisation. Pan-European pilots such as the SEPA Payment Account Access (SPAA) scheme are unlocking premium data-sharing revenue streams, while large corporates fast-track ISO 20022 migration to achieve real-time cash visibility. Corporates’ need for unified, cross-border cash pooling aligns with regulators’ goal of friction-free Single Euro Payments Area infrastructure, giving the Europe real time payments market unique momentum relative to other regions. Poland’s 16.5% CAGR and the United Kingdom’s 27.8% revenue share underline the region’s blend of fast-growing challenger markets and scale-oriented incumbents, sustaining a balanced outlook for providers across software, services and clearing infrastructure.

Key Report Takeaways

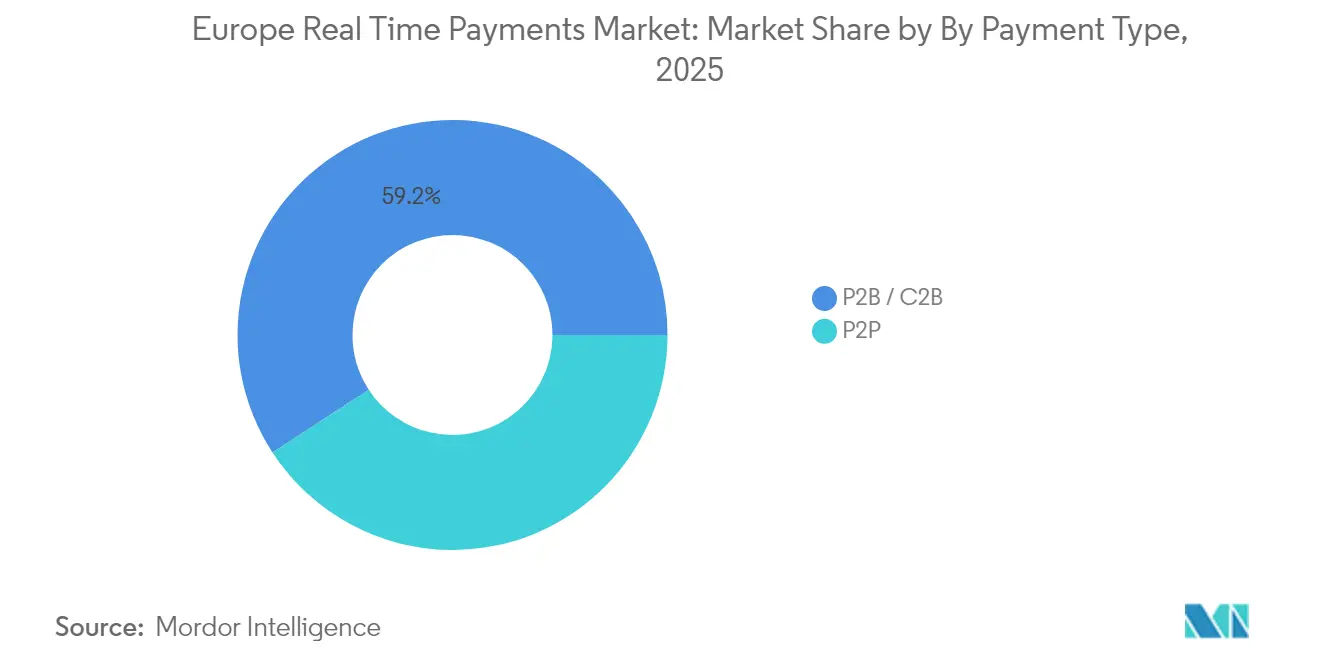

- By payment type: P2P transfers led with 40.80% of the Europe real time payments market share in 2025, whereas P2B/C2B volumes are projected to expand at a 13.59% CAGR through 2031.

- By component: Platform/Software captured 62.70% revenue in 2025; the Services segment is forecast to grow at 15.32% CAGR as institutions outsource compliance and integration.

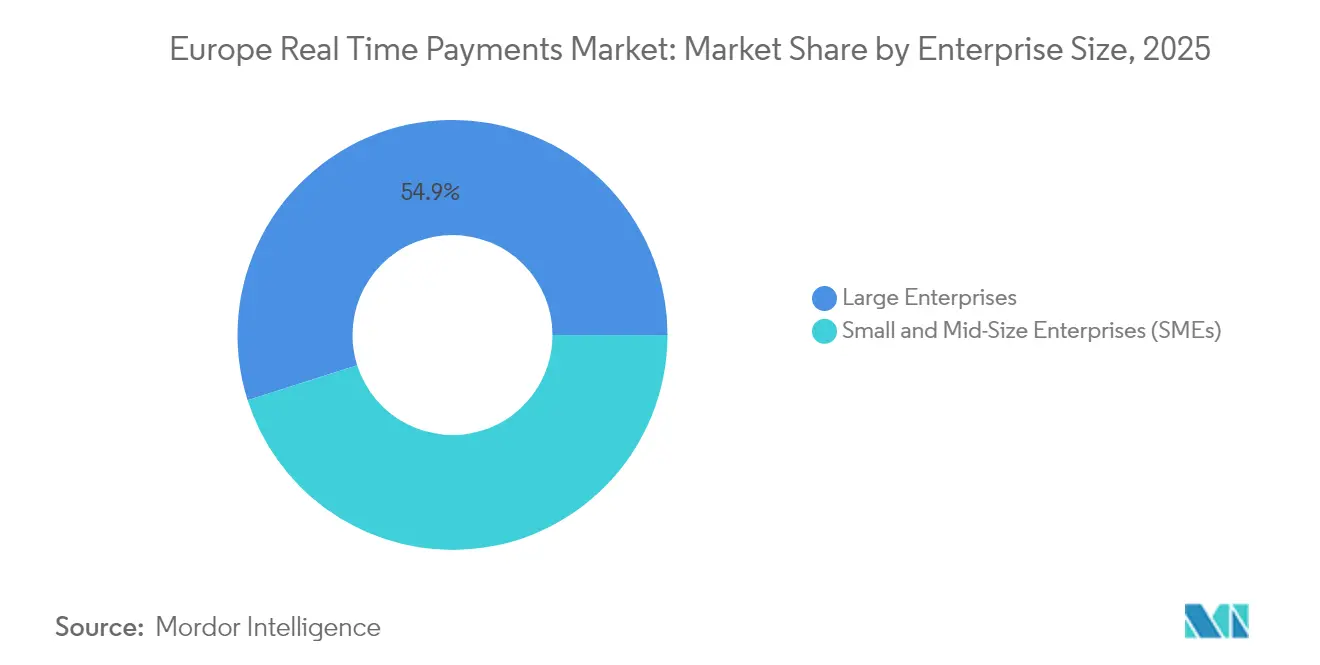

- By enterprise size: Large Enterprises held 54.90% share in 2025, while SMEs are forecast to grow at 12.18% CAGR on the back of simplified onboarding via pan-regional wallets.

- By end-user industry: Banking and Financial Services controlled 38.20% in 2025, but Retail and eCommerce is advancing at a 13.66% CAGR as merchants switch to account-to-account rails.

- By geography: The United Kingdom dominated with 27.30% share in 2025; Poland leads growth at 15.92% CAGR through 2031 on the strength of BLIK and Express Elixir adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of Pan-European Instant SEPA Mandate (SCT Inst) | +3.2% | Eurozone, extending to full SEPA area by 2027 | Medium term (2-4 years) |

| PSD3 and SPAA-Driven Open-Banking Use-Cases | +2.8% | EU-wide, with tactical pilots in Germany and Belgium | Long term (≥ 4 years) |

| Corporate Treasury Shift to ISO 20022 for Instant Liquidity | +1.9% | Global with EU early adoption focus | Short term (≤ 2 years) |

| Rise of Request-to-Pay (R2P) for Utilities and Public Sector | +1.4% | Nordic countries leading, expanding to Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adoption of Pan-European Instant SEPA Mandate (SCT Inst) Drives Market Acceleration

Mandatory SCT Inst adherence compels Eurozone banks to receive instant payments by January 2025 and dispatch them by October 2025. [2] European Payments Council, “SCT Inst Rulebook 2025,” europeanpaymentscouncil.eu Cost-parity clauses cut average instant transfer fees from EUR 2.19 to EUR 0.76, eliminating the economic barrier that had capped consumer uptake. The latest rulebook also tightens execution to 5 seconds and lifts single-transaction limits close to EUR 1 billion (USD 1.08 billion), positioning the rail for high-value corporate flows. Banks are therefore shifting investment from per-transaction pricing models to value-added overlay services such as Request-to-Pay and fraud-verified account matching. As liquidity settles in near-real time, corporates gain faster access to incoming funds, further perpetuating volume growth in the Europe real time payments market.

PSD3 and SPAA-Driven Open-Banking Use-Cases Expand Beyond Payment Initiation

SPAA’s remuneration framework finally introduces a viable economic model for premium APIs, encouraging banks to commercialise data products rather than treating open banking as a compliance cost. Dynamic Recurring Payments, pilot-tested in 2025, allow merchants to vary debits without fresh mandates, reducing rejection rates and smoothing cash flow. PSD3 harmonises licensing for Payment and Electronic Money Institutions, closing loopholes that had supported fragmented market entry. These reforms deepen integration between instant clearing rails and value-added digital services, creating new monetisation paths for banks and fintechs.

Corporate Treasury Shift to ISO 20022 for Instant Liquidity Management

ISO 20022’s structured data unlocks real-time reconciliation and richer remittance information, a capability corporates view as critical ahead of the November 2025 cross-border deadline. Early adopters report consolidated multibank cash views and reduced working-capital buffers. Airbus’s use of Swift trackers to monitor end-to-end payment status exemplifies how treasurers harness data granularity to automate cash positioning. The linkage of ISO-formatted messages to instant payment schemes eliminates information asymmetry between high-value and retail payments, reinforcing end-user demand across the Europe real time payments market.

Rise of Request-to-Pay (R2P) for Utilities and Public Sector Applications

R2P overlays digitise billing, remove paper reconciliation and embed contextual data such as energy consumption or tax identifiers. Nordic utilities show reduced late-payment ratios after adopting SEPA R2P flows, while public-sector pilots have demonstrated faster tax settlement and improved citizen satisfaction. [3]Deutsche Bank, “Pay-by-Bank Partnership Announcement,” mastercard.com By shifting customer interactions into real time, billers align receivables with operational funding cycles, further validating instant rails as the default pathway for recurring payments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented RTP Clearing Infrastructure (TIPS vs. RT1 vs. Domestic) | -2.1% | EU-wide with varying domestic implementations | Long term (≥ 4 years) |

| Payment Fraud such as Authorized Push Payment Scams | -1.8% | UK leading, expanding across EU with instant payments | Short term (≤ 2 years) |

| High AML/SCA Compliance Costs | -1.3% | Global with EU regulatory complexity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented RTP Clearing Infrastructure Creates Operational Complexity

TIPS processed 196 million payments worth EUR 122 billion (USD 132 billion) in H1 2024 with 99% completion inside 5 seconds. Yet PSPs must still fund liquidity across TIPS, RT1 and domestic schemes, tying up working capital and raising settlement risk. The ECB’s project for a single liquidity pool aims to consolidate cash buffers, but divergent implementation timelines keep liquidity siloed, disproportionately burdening smaller PSPs and tempering scale economics in the Europe real time payments market.

Payment Fraud Escalation Threatens Consumer Confidence

Authorized Push Payment scams rose sharply in 2024, prompting the European Payments Council to call fraud the primary obstacle to instant payment adoption. Liability shifts under the forthcoming Payment Services Regulation compel banks to reimburse victims, increasing compliance costs and necessitating AI-enabled pre-transaction screening. Providers must therefore balance sub-10-second processing against enhanced due-diligence, an operational tension that could restrain user experience if not addressed through advanced analytics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Commercial Volumes Redefine the Use-Case Mix

P2P transfers controlled 40.80% of 2025 volumes; however, P2B/C2B flows are forecast to grow 13.59% annually through 2031. The Europe real time payments market size for P2B transactions is expected to add USD 3.36 billion in incremental revenue between 2026 and 2031 as merchants pivot away from card interchange. Wero’s July 2024 launch in Germany and Belgium showcases the strategic sequencing from P2P to online checkout, an expansion that brings competitive pressure to global card schemes. Emerging multi-scheme routing—Spain’s Bizum, Italy’s Bancomat Pay and Portugal’s MB Way—illustrates regional collaboration designed to maintain domestic sovereignty while meeting cross-border consumer expectations. For merchants, account-to-account rails lower acceptance costs and improve settlement speed, strengthening loyalty propositions and solidifying the Europe real time payments market as a credible alternative to established card networks.

Second-order dynamics suggest a gradual re-balancing of revenue pools. Payment‐service providers able to deliver single-API access across multiple instant schemes are best positioned to capture scaled P2B volumes. As Request-to-Pay matures, utilities and public entities will shift from episodic batch collections to interactive billing, adding recurring traffic that sustains infrastructure utilisation. The Europe real time payments market therefore pivots from consumer-initiated transfers to enterprise-led cash management, accelerating monetisation potential across service layers.

By Component: Services Outpace Software as the Integration Race Intensifies

Platform/Software licences represented 62.70% of 2025 spending, but Services are forecast to grow 15.32% CAGR. Mandatory eurozone Send-capability by October 2025 drives a wave of consulting engagements and managed-service contracts, moving the Europe real time payments market size for Services from USD 2.3 billion in 2025 to USD 5.41 billion by 2031. Tier-1 banks frequently adopt “lift-and-shift” strategies—modernising legacy payment hubs while outsourcing non-differentiating functions such as ISO 20022 mapping and scheme certification. ACI Worldwide’s cloud-native deployments and IBM Z-based scaling examples prove demand for resilient, high-volume platforms complemented by expert service wrappers.

Institutions with thin IT budgets increasingly favour shared-service utilities, allowing them to meet regulatory timelines without heavy capital spend. This shift also opens cross-selling potential for analytics, fraud management and value-added overlay services. As real-time volumes rise, continuous performance tuning becomes critical, keeping specialised integrators in constant demand and reinforcing the Europe real time payments market’s service-centric revenue trajectory.

By Enterprise Size: SMEs Catch Up Through Simplified Wallet Onboarding

Large Enterprises retained 54.90% volume share in 2025, yet SME adoption is climbing at 12.18% CAGR. The Europe real time payments market share held by SMEs is projected to approach 47.80% by 2031 as regulatory cost-parity and one-click onboarding erase historical disadvantages. Unified wallets such as Wero eliminate multi-bank integration overheads, while open-banking APIs standardise pay-by-link and instant payout functions. Germany’s projected USD 9 billion open-banking revenue pool by 2030 signals how standardised connectivity translates into concrete SME demand for plug-and-play payment modules.

SMEs focus on cash-flow acceleration rather than complex treasury optimisation. Instant receipt of funds reduces reliance on overdrafts and unlocks inventory cycles. Financial institutions have responded with bundled offerings that combine identity verification, e-money accounts and settlement management, embedding value-added compliance services. As SME penetration grows, transaction diversity and volume density improve, making the Europe real time payments industry more attractive for fintech entrants.

By End-User Industry: Retail and eCommerce Leads Volume Upswing

Banking and Financial Services accounted for 38.20% of 2025 spending as institutions upgraded internal rails and customer interfaces; however, Retail and eCommerce payments are expanding at 13.66% CAGR. Smartphones facilitated 53% of European online sales in 2024, creating natural affinity with tap-to-pay and pay-by-bank checkout flows. Unified commerce strategies championed by Worldline, where every sales channel exchanges data in real time, rely on instant settlement to sync inventory, loyalty and refunds. Healthcare and Telecom remain niche adopters, using instant payouts primarily for claims and subscription billing.

Visa’s launch of AI-powered account-to-account fraud protection underscores how network vendors adapt existing risk assets to the new rail, offering merchants continuity of brand while reducing chargeback exposure. As retailers normalise instant refunds and payouts, customer experience gaps between traditional and real-time rails widen, further driving volumes inside the Europe real time payments market.

Geography Analysis

The United Kingdom maintained 27.30% of the Europe real time payments market in 2025 thanks to mature Faster Payments rails and active open-banking regulation. The National Payments Vision promotes account-to-account consumer payments, and early adopters report higher conversion and lower costs than card equivalents. Yet post-Brexit exclusion from SEPA instant schemes forces UK PSPs to manage dual technical stacks, raising operational overhead. The Financial Conduct Authority’s safeguarding and APP-scam reimbursement rules elevate compliance but reinforce user trust, sustaining volumes.

Germany and France form the industrial core. German open-banking revenues are forecast to hit USD 9 billion by 2030, underpinned by Berlin Group API standards and high smartphone penetration. TARGET2’s daily throughput of 350,000 payments worth EUR 1.7 trillion (USD 1.84 trillion) demonstrates systemic scale ready for instant overlays. France benefits from Wero’s August 2025 launch and national policy to reduce dependence on non-European schemes, steering domestic issuers toward pan-regional wallet acceptance.

Poland exemplifies high-velocity adoption, growing at 15.92% CAGR on the back of BLIK’s 20.2% transaction gain and Express Elixir’s user expansion. Government investment in digital-economy initiatives and ISO 20022 migration of core clearing systems provide long-term structural support. Spain and Italy benefit from Bizum-Bancomat Pay cooperation and TIPS connectivity but must still elevate consumer awareness to Nordic levels. Collectively these dynamics indicate sustained geographic diversification, widening the addressable base for providers active in the Europe real time payments market.

Competitive Landscape

Competition remains moderate-fragmented, shaped more by regulatory mandates than organic market cycles. Direct-connection fintechs such as Adyen posted 34.5% revenue CAGR (2019-2023), whereas heritage processors like Worldpay grew only 3% year-over-year in Q4 2023, revealing a structural advantage for single-platform architectures capable of rapid local scheme onboarding. Global Payments’ planned acquisition of Worldpay, if approved, would create the largest UK merchant acquirer with 30% share, signalling consolidation pressure among legacy firms seeking scale economies to fund compliance and innovation.

Incumbent banks pursue vertical integration: BNP Paribas extended its instant clearing capabilities to corporate treasury clients, bundling cash-forecasting analytics. Fintech entrants differentiate through specialist services—Banking Circle offers low-value cross-border instant payouts, whereas Trustly focuses on merchant A2A checkout across 30 markets. European Payments Initiative’s co-ordinated rollout of Wero underscores a strategic sovereignty agenda, giving regional banks a stake in consumer wallets and merchant checkout, thereby challenging global card networks’ dominance in the Europe real time payments market.

White-space opportunities emerge around cross-border interoperability and SME enablement. Providers building AI-driven risk engines for APP-fraud detection or offering managed liquidity services across TIPS and RT1 pools stand to capture premium pricing. The forthcoming digital euro could re-shape value pools; European pure-plays collectively added USD 23 billion in market value after positive CBDC updates, highlighting investor expectation that native players can monetise central-bank digital infrastructure more effectively than non-European rivals.

Europe Real Time Payments Industry Leaders

ACI Worldwide Inc.

Fiserv Inc.

Paypal Holdings Inc.

Mastercard Inc.

Visa Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Global Payments announced a bid for Worldpay to form the world’s largest merchant acquirer. Strategically, the move seeks transaction scale and combined scheme connectivity to match fintech agility while distributing rising AML and APP-fraud compliance costs across a larger volume base.

- April 2025: The European Central Bank upgraded its cross-border payment services, processing 4.1 million annual transactions across 200 plus jurisdictions. The enhancement embeds FX risk-management modules, positioning ECB services as a low-friction settlement layer aligned with instant-payment timelines.

- March 2025: The European Court of Auditors’ Special Report on Digital Payments highlighted EUR 1 trillion (USD 1.08 trillion) in annual EU digital payment value, recommending clearer price-intervention guidelines to ensure instant-payment access parity—a recommendation likely to accelerate fee caps in the Europe real time payments market.

- January 2025: Eurozone banks became legally obliged to receive instant credit transfers, with send-capability due by October 2025. The mandate neutralises premium pricing and obliges verification-of-payee, pushing banks toward fraud-resilient infrastructure investments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European real-time payments market as every bank-to-bank transaction, domestic or cross-border, that clears within ten seconds on a 24/7/365 basis under schemes such as SEPA Instant Credit Transfer, plus the platform, switching, fraud-monitoring, and advisory revenues generated around that flow. We, therefore, capture value from payment initiation apps, request-to-pay add-ons, and ISO 20022 conversion services that directly support instant settlement.

Scope exclusion: Batch ACH, card-to-card push transfers, and fees tied only to wholesale RTGS liquidity are omitted.

Segmentation Overview

- By Payment Type

- P2P

- P2B / C2B

- By Component

- Platform / Software

- Services (Consulting, Integration, Managed)

- By Enterprise Size

- Large Enterprises

- Small and Mid-Size Enterprises (SMEs)

- By End-User Industry

- Banking and Financial Services (BFSI)

- Retail and eCommerce

- Telecom and Media

- Healthcare

- Other End-user Industries

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Poland

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

We interviewed payment-processor product heads, treasury managers at large retailers, and fintech association leads across the UK, Germany, Poland, Spain, and the Nordics. Their inputs helped us validate scheme fees, transaction mix shifts, and likely timelines for ISO 20022 and Request-to-Pay roll-outs, bridging gaps that public data alone could not fill.

Desk Research

We start by pooling openly available tier-1 datasets, European Central Bank payments statistics, Eurostat smartphone and e-commerce indicators, European Payments Council rulebook updates, and country central-bank instant-transfer dashboards, because they quantify volumes, values, and adoption ceilings. Additional texture comes from regulatory texts (Instant Payments Regulation, PSD3 drafts), trade bodies such as UK Pay, or Sweden's Bankgirot, and academic papers discussing authorized-push-payment fraud. To size vendor revenue pools, our analysts pull filing data from D&B Hoovers, news hits from Dow Jones Factiva, and investor decks posted through Factiva's archive, which reveal pricing ranges and contract counts. Press releases, procurement portals, and patent trends supplement the picture. The list above is illustrative; many further sources were tapped for cross-checks.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction. ECB and national reports provide 2024 instant-transfer volumes, which are multiplied by average service fees and overlay software license rates to reach a 2025 revenue pool. Supplier roll-ups and sampled ASP × volume checks act as selective bottom-up tests to refine totals. Key drivers, SCT Inst reach, per-capita smartphone penetration, open-banking API call growth, fraud-loss ratios, and ISO 20022 migration progress, feed a multivariate regression that projects values through 2030. Where vendor data were sparse, we imputed volumes using penetration-rate benchmarks from peer countries before rerunning sensitivity bands.

Data Validation & Update Cycle

Outputs pass variance thresholds versus external series and peer interviews; any anomaly above 5% triggers a fresh analyst review. Reports refresh yearly, with interim edits if major regulatory or pricing shifts occur, and every delivery includes a final consistency sweep.

Why Mordor's Europe Real Time Payments Baseline Commands Reliability

Published estimates frequently diverge because firms pick different geographies, include or exclude overlay revenues, or stretch CAGR assumptions. According to Mordor Intelligence, disciplined scope setting and annual refreshes curb such drift.

Key gap drivers include narrower country baskets, reliance on transaction value rather than revenue, single-scenario forecasting, and outdated currency conversions used by some publishers, which together push their totals away from ours.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.21 B (2025) | Mordor Intelligence | - |

| USD 4.89 B (2023) | Global Consultancy A | Excludes overlay software and uses 2023 base without inflation parity |

| USD 6.49 B (2025) | Regional Consultancy B | Counts only P2P flows and six core economies, omitting Eastern Europe |

These comparisons show that, while ranges exist, Mordor's balanced blend of regulated scope, multi-variable modeling, and timely updates gives decision-makers a dependable starting point.

Key Questions Answered in the Report

How big is the Europe real time payments market in 2026?

The Europe real time payments market size is USD 7.96 billion in 2026 and is forecast to reach USD 13.1 billion by 2031 at a 10.46% CAGR.

Which segment is growing fastest?

P2B/C2B transactions represent the fastest-growing payment type, advancing at a 13.59% CAGR through 2031 as merchants migrate away from card-based fees.

Why is Poland considered a high-growth country?

Poland posts a 15.92% CAGR due to BLIK’s 20.2% transaction growth and Express Elixir’s expanding user base, supported by proactive ISO 20022 migration and government digital-economy funding.

What are the main challenges to instant-payment adoption?

Infrastructure fragmentation among TIPS, RT1 and domestic schemes and rising Authorized Push Payment fraud are the primary restraints, shaving an estimated 3.9 percentage points off projected CAGR.

How are banks monetising open-banking APIs under PSD3?

PSD3 and SPAA introduce remuneration models that let banks charge for premium data services, such as Dynamic Recurring Payments, turning compliance investments into new revenue streams.

Will the digital euro disrupt existing instant-payment providers?

Providers anticipate the digital euro could boost volumes by embedding central-bank money in retail wallets; firms with agile, API-centric architectures are best placed to integrate the new instrument rapidly.

Page last updated on: