Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 27.74 Billion |

| Market Size (2026) | USD 28.9 Billion |

| Market Size (2031) | USD 35.49 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Paper Packaging Market Analysis by Mordor Intelligence

The Russia paper packaging market size was valued at USD 27.74 billion in 2025 and estimated to grow from USD 28.9 billion in 2026 to reach USD 35.49 billion by 2031, at a CAGR of 4.19% during the forecast period (2026-2031). Russia paper packaging market growth rests on three pillars: a state-led drive for import substitution, fast-rising e-commerce volumes, and regulatory measures that redirect demand from plastics to fiber-based formats. Brand owners are moving more procurement to domestic converters to hedge geopolitical risk, while local producers rush to close technology gaps and secure raw-material supply chains. Investments in new board machines, such as Kama Karton’s folding boxboard line, signal confidence that domestic mills can meet quality expectations traditionally served by imports. Demand also benefits from the food-processing sector’s continuing modernization and a 45% jump in e-commerce turnover to ₽19.9 trillion in 2024, which fundamentally lifted corrugated-case orders. At the same time, currency swings keep input costs volatile, and slow progress in waste-paper collection hampers recycled-fiber penetration, tempering upside potential.

Key Report Takeaways

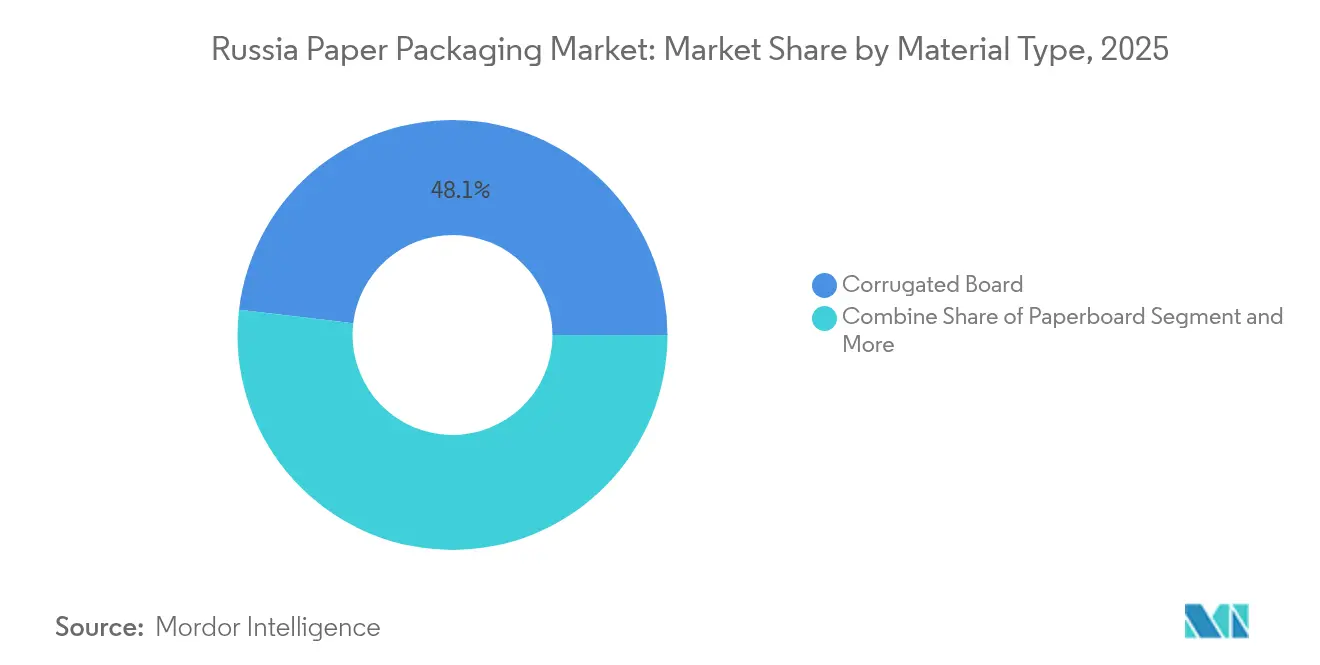

- By material type, corrugated board led with a 48.12% Russia paper packaging market share in 2025, while kraft paper is projected to post the fastest 7.18% CAGR to 2031.

- By product type, rigid formats accounted for 57.62% of the Russia paper packaging market in 2025; flexible formats are expected to grow at 5.78% CAGR through 2031.

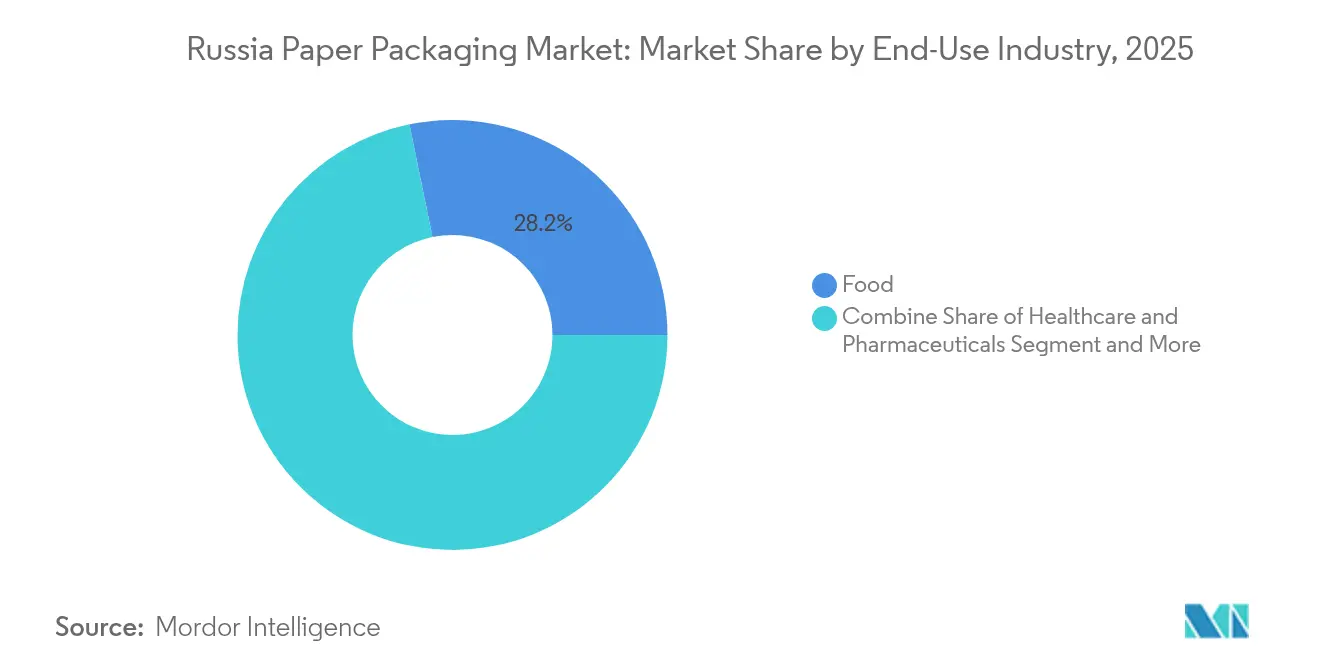

- By end-use, food held 28.21% revenue share in 2025, whereas healthcare and pharmaceuticals are forecast to expand at 6.49% CAGR to 2031.

- By distribution channel, direct sales captured 54.12% of the Russia paper packaging market in 2025, yet indirect channels will record a 5.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Domestic Food-Processing Sector Boosting Folding Carton Demand | +1.2% | National, concentrated in Central and Southern regions | Medium term (2-4 years) |

| Import-Substitution Policy Accelerating Investment in Local Board Mills | +1.8% | National, emphasis on Northwestern and Siberian regions | Long term (≥ 4 years) |

| Federal Plastic-Ban Roadmap Driving Shift to Fiber Retail Bags | +0.9% | National, early implementation in major cities | Short term (≤ 2 years) |

| Direct-to-Consumer E-commerce Growth Raising Corrugated Demand | +1.1% | National, concentrated in urban centers | Medium term (2-4 years) |

| Beverage Aseptic Carton Recycling Mandates Enhancing Liquid Carton Use | +0.7% | National, focus on metropolitan areas | Medium term (2-4 years) |

| Arctic Rail/Northern Sea Route Projects Stimulating Heavy-Duty Kraft Sacks | +0.6% | Arctic regions, Northern Sea Route corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Domestic Food-Processing Sector Boosting Folding Carton Demand

Turnover in Russia’s food-service and processing complex rose 12.1% to RUB 5.3 trillion in 2024, translating directly into higher folding-carton consumption.[1]INFOLine, “Russian Food-Service Market 2025,” infoline.spb.ru Brand owners require retail-ready carton designs that preserve freshness and support track-and-trace compliance now in force for packaged water. Government subsidies for plant modernization encourage converters to supply premium, coated substrates that withstand automated filling lines. The recently installed folding-boxboard machine at Kama Karton adds domestic capacity in this high-specification grade. As consumers trade up to quality packaged meals, converters can push value-added graphics and barrier coatings, supporting higher margins in the Russia paper packaging market.

Import-Substitution Policy Accelerating Investment in Local Board Mills

Resolution No. 1875, effective December 2024, grants national-treatment advantages in public procurement, guaranteeing order flow to locally made packaging. The rule has already stimulated multi-billion-ruble mill upgrades, including Segezha Group’s integrated CLT panel and sack-kraft lines. Mills able to match European quality grades win long-term supply contracts, while equipment suppliers report larger order pipelines despite currency risk. Over time, a deeper domestic asset base reduces reliance on imported board and cushions the Russia paper packaging market against external shocks.

Federal Plastic-Ban Roadmap Driving Shift to Fiber Retail Bags

A prohibition on three plastic-pack formats begins in 2025, forcing retailers to switch to paper bags for high-volume checkout applications 1-ofd.ru. Environmental fees on imported packaging further skew economics in favor of local converters. Producers able to guarantee burst strength and moisture resistance are experiencing order backlogs. Short-run bag makers scramble for kraft-paper supply, widening spreads over export prices and underpinning revenue growth across the Russia paper packaging market.

Direct-to-Consumer E-Commerce Growth Raising Corrugated Demand

Online retail jumped 45% year on year to ₽19.9 trillion, lifting corrugated-case shipments across fulfilment centers. Marketplace operators now represent 65% of e-commerce revenue and standardize ship-ready packaging specifications, enabling high-volume box runs. Cross-border online sales, already ₽241 billion, add extra-strength export cartons to the mix. With parcel densities rising, converters invest in lightweight, high-compression flute profiles that lower logistics costs while safeguarding goods. Stable e-commerce expansion anchors long-term corrugated demand inside the Russia paper packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Log-Supply Instability in North-West & Siberia | -0.8% | Northwestern and Siberian regions | Medium term (2-4 years) |

| Ruble Volatility Lifting Imported Chemicals & Equipment Costs | -1.1% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Under-developed Post-Consumer Collection for Recycled Fiber | -0.6% | National, acute in rural areas | Long term (≥ 4 years) |

| Capital-Intensive Paper-Machine Re-tooling Slows Modernisation | -0.9% | National, concentrated in older industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ruble Volatility Lifting Imported Chemicals and Equipment Costs

Essential bleaching agents, sizing chemicals, and precision machine components remain largely sourced abroad, leaving converters exposed when the ruble weakens. Import bills swell immediately because hedging instruments are limited, delaying critical upgrades and constraining product-quality gains. Indian chemical exports alone are projected to reach USD 2.4 billion by 2026, underscoring continued dependence on overseas inputs. [2]Chemexcil, “Export Potential of Indian Chemical Products on the Russian Market,” chemexcil.inElevated capex and opex siphon resources that could otherwise expand capacity in the Russia paper packaging market.

Under-Developed Post-Consumer Collection for Recycled Fiber

Only 4.4% of Russia’s total waste is utilized, leaving converters starved of affordable recovered paper feedstock. [3]Wilson Center, “Contentious Politics of Waste Management in Russia,” wilsoncenter.org Low recovery rates inflate virgin-fiber demand and erode sustainability credentials increasingly valued by brand owners. Rural logistics remain uneconomic, and electronic-waste volumes processed fell from 79,616 tons in 2019 to 11,569 tons in 2023, highlighting systemic collection shortfalls. [4]MDPI, “Effectiveness of Waste Management Systems,” mdpi.com Without coordinated policy and infrastructure, recycled-paper uptake across the Russia paper packaging market will lag international norms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Corrugated Board Dominance Faces Kraft-Paper Challenge

Corrugated board captured a 48.12% Russia paper packaging market share in 2025 and remains indispensable for shipping, e-commerce, and fast-moving consumer-goods logistics. The Russia paper packaging market size tied to corrugated applications reached USD 13.35 billion in 2025 and is projected to climb at 3.9% annually through 2031. Continuous flute-profile optimization lowers grammage without sacrificing stacking strength, and automated die-cutting supports just-in-time delivery models. Meanwhile, kraft paper is scaling at a 7.18% CAGR, supported by Arctic infrastructure that depends on heavy-duty sacks; Northern Sea Route cargo volumes aim for 90 million tons by 2030. The Russia paper packaging industry increasingly uses high-porosity sack-kraft to meet cement and mineral filler demand in temperatures below −30 °C.

Other grades such as folding boxboard and specialty papers address food, beverage, and electronics niches. Kama Karton’s new board machine boosts domestic supply of coated multilayer substrates, curbing imports in premium confectionery cartons. Producers balancing multi-grade portfolios spread risk across cyclical demand patterns, reinforcing resilience across the Russia paper packaging market.

By Product Type: Rigid Packaging Leads Despite Flexible Growth

Rigid formats—folding cartons and corrugated cases—achieved 57.62% share of the Russia paper packaging market in 2025, translating into USD 15.98 billion of revenue. Rigid designs provide stackability and brand billboard space that omnichannel retailers want, especially as 65% of e-commerce flows through marketplaces. The Russia paper packaging market size for rigid solutions is forecast to touch USD 19.74 billion by 2031 at a 3.1% CAGR. Producers exploit high-graphics litho-laminated corrugated and retail-ready trays to win supermarket shelf space.

Flexible paper packaging is expanding at 5.78% CAGR because barrier-coated wraps and pouches can now rival plastics on moisture and grease resistance. Upcoming bans on selected plastic formats channel retail and food-service demand toward fiber wraps. Lightweight sachets for instant beverages and portion packs for condiments illustrate where paper flexibles displace plastics. As machinery suppliers roll out high-speed form-fill-seal lines compatible with paper, converters deepen penetration in snack and dry-mix categories, enlarging addressable demand in the Russia paper packaging market.

By End-Use Industry: Food Sector Dominance Meets Healthcare Innovation

Food applications commanded 28.21% of sales in 2025, reflecting Russia’s RUB 5.3 trillion food-service ecosystem. Bakers, meat processors, and beverage fillers value paper’s breathability and shelf-visibility. Aseptic-carton recycling mandates steer liquid dairy and juice brands toward high-barrier liquid cartons, while new serialized codes for bottled water enter force in March 2025. These rules demand tamper-evident, code-friendly substrates, bolstering value across the Russia paper packaging market.

Healthcare and pharmaceuticals, although smaller, post the fastest 6.49% CAGR. Market value grew 10% in 2024, even as prescription volumes dipped, highlighting the premiumization trend. New medical-product registration rules effective March 2025 heighten labeling and barrier requirements. Serialisation and child-resistance features create space for folding cartons laminated with tamper-notify films, a niche with high margins inside the Russia paper packaging industry.

By Distribution Channel: Direct Sales Maintain Edge Over Indirect Growth

Direct sales secured 54.12% of 2025 turnover as high-volume buyers prefer mill-to-plant logistics and custom design support. Integrated converters such as Segezha Group engage in long-term agreements that cover everything from fiber sourcing to inventory management. The Russia paper packaging market size attached to direct contracts reached USD 15.01 billion in 2025.

Indirect channels—distributors and merchants—are scaling at 5.55% CAGR as smaller brand owners, regional bakeries, and online micro-sellers need low-minimum order quantities. E-commerce marketplaces facilitate multi-vendor storefronts, creating granular demand that stocking distributors can aggregate efficiently. Value-added services such as digital printing and kitting broaden indirect-channel relevance in the Russia paper packaging market.

Geography Analysis

Russia’s vast geography concentrates packaging manufacture in resource-rich yet logistically advantaged regions. The Northwestern cluster around St. Petersburg hosts integrated mills with Baltic export access; Segezha Group maintains ISO-certified plants supplying industrial sacks and consumer bags. Corrugated converters here leverage proximity to Scandinavian equipment vendors, shortening maintenance cycles. However, unstable log flow from Karelia and Arkhangelsk occasionally disrupts capacity utilization, limiting growth in the region’s portion of the Russia paper packaging market.

The Central macro-region anchors consumption. Moscow and surrounding oblasts absorb the lion’s share of folding cartons, corrugated cases, and liquid-carton sleeves needed by food, pharma, and e-commerce fulfilment hubs. Online retail expansion to ₽19.9 trillion in 2024 vaulted last-mile packaging requirements, pushing corrugated plants near Moscow to double-shift operations. Pharmaceutical packaging orders accelerate thanks to a 10% value rise in the drugs market and stronger serialization rules. The region, therefore, remains the demand nucleus for the Russia paper packaging market.

Siberia and the Far East offer the highest upside over the long term. Cargo on the Northern Sea Route reached 37.9 million tons in 2024 despite shortfalls versus government targets.The administration’s USD 40 billion infrastructure rollout plus tax revenues forecast at USD 160 billion by 2035 will require cement, chemicals, and equipment, spurring sack-kraft and heavy-duty corrugated demand. Logistics challenges persist, but state subsidies for rail spurs and ice-class cargo vessels gradually improve supply-chain reliability, positioning these territories as the future growth frontier for the Russia paper packaging market.

Competitive Landscape

Foreign exits and state policy have reshaped competitive dynamics. Mondi’s USD 87.2 million sale of Syktyvkar assets marks a decisive retreat of international majors. Domestic champions, chiefly Segezha Group and Ilim Group, now vie for share amid moderate concentration. Segezha integrates forest harvesting with sack-kraft, plywood, and corrugated, backed by RUB 3 billion invested in Russia’s first industrial CLT line. Ilim is lifting Ust-Ilimsk to design output by 2025, expanding virgin-fiber board supply.

Technology investment remains a differentiator. Kama Karton’s new ANDRITZ folding-boxboard line features dilution-control headboxes and calendering for premium print surfaces. Smaller regional mills focus on niche runs—pharmaceutical leaflet paper or barrier-lined food wraps—where agility trumps scale. Converters unable to self-generate pulp seek long-term furnish contracts to mitigate wood-price swings, but fiber availability fluctuates with harvest quotas. While the Russia paper packaging market still permits new entrants, capex intensity and raw-material integration increasingly favor players with deep balance sheets and secure forest leases.

Sustainability pressures add another competitive layer. Mills with closed-loop effluent treatment and FSC-certified forests gain procurement preference from multinational brand owners still active in Russia. At the same time, ruble swings raise debt-service costs on imported machinery, making local currency financing critical. The emerging landscape thus balances consolidation among integrated majors with specialist upstarts capitalizing on regulation-driven niches within the Russia paper packaging market.

Russia Paper Packaging Industry Leaders

Mondi Group

Ilim Group

International Paper (DS Smith)

Smurfit WestRock

Tetra Pak Russia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mandatory item-level traceability for packaged water commenced, compelling full electronic code transmission across the supply chain

- January 2025: Segezha Group launched Russia’s first industrial CLT panel line at Sokol Plant after investing over RUB 3 billion (USD 3.27 billion)

- January 2025: ANDRITZ delivered a full folding-boxboard line to Kama Karton, expanding domestic supply of premium board

- December 2024: Resolution No. 1875 introduced national-treatment advantages for Russian-made packaging in government tenders

Russia Paper Packaging Market Report Scope

Paper packaging is a cost-efficient and versatile method to protect, preserve, and transport a broad range of products. Additionally, it can be customized to meet customers' needs or product-specific requirements. Attributes like biodegradability, lightweight, and recyclability of paper packaging make it an essential component for packaging. This type of packaging is currently used for designing new and beautiful models and adding branding functions.

The Russia Paper Packaging Market By Product Type (Folding Cartons, Corrugated Boxes), End-User Industry (Food, Beverage, Healthcare, Personal Care, Household Care, Electrical Products). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Material Type

| Kraft Paper |

| Paperboard |

| Corrugated Board |

| Other Material Type |

By Product Type

| Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | |

| Other Flexible Paper Packaging | |

| Rigid Paper Packaging | Folding Carton |

| Corrugated Boxes | |

| Other Rigid Paper Packaging |

By End-Use Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Electronic |

| Other End-Use Industry |

By Distribution Channel

| Direct Sales |

| Indirect Sales |

| By Material Type | Kraft Paper | |

| Paperboard | ||

| Corrugated Board | ||

| Other Material Type | ||

| By Product Type | Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | ||

| Other Flexible Paper Packaging | ||

| Rigid Paper Packaging | Folding Carton | |

| Corrugated Boxes | ||

| Other Rigid Paper Packaging | ||

| By End-Use Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial and Electronic | ||

| Other End-Use Industry | ||

| By Distribution Channel | Direct Sales | |

| Indirect Sales | ||

Key Questions Answered in the Report

What is the current size of the Russia paper packaging market?

The market is valued at USD 28.9 billion in 2026 and is on track to hit USD 35.49 billion by 2031.

Which material type dominates the Russia paper packaging market?

Corrugated board leads with 48.12% share, driven by e-commerce and retail logistics needs.

How will the federal plastic-ban roadmap affect packaging choices?

The 2025 ban on selected plastic formats pushes retailers toward fiber-based bags and wraps, lifting demand for kraft and coated papers.

Why is the pharmaceutical segment growing faster than other end-uses?

Regulatory reforms introduce stricter serialization and safety requirements, prompting brand owners to upgrade to premium, compliant paper packaging at a projected 6.49% CAGR.

Which region offers the strongest long-term growth prospects?

Siberia and the Far East, supported by Northern Sea Route infrastructure projects, are expected to see the highest incremental demand for heavy-duty sack-kraft and corrugated solutions.

Page last updated on: