Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

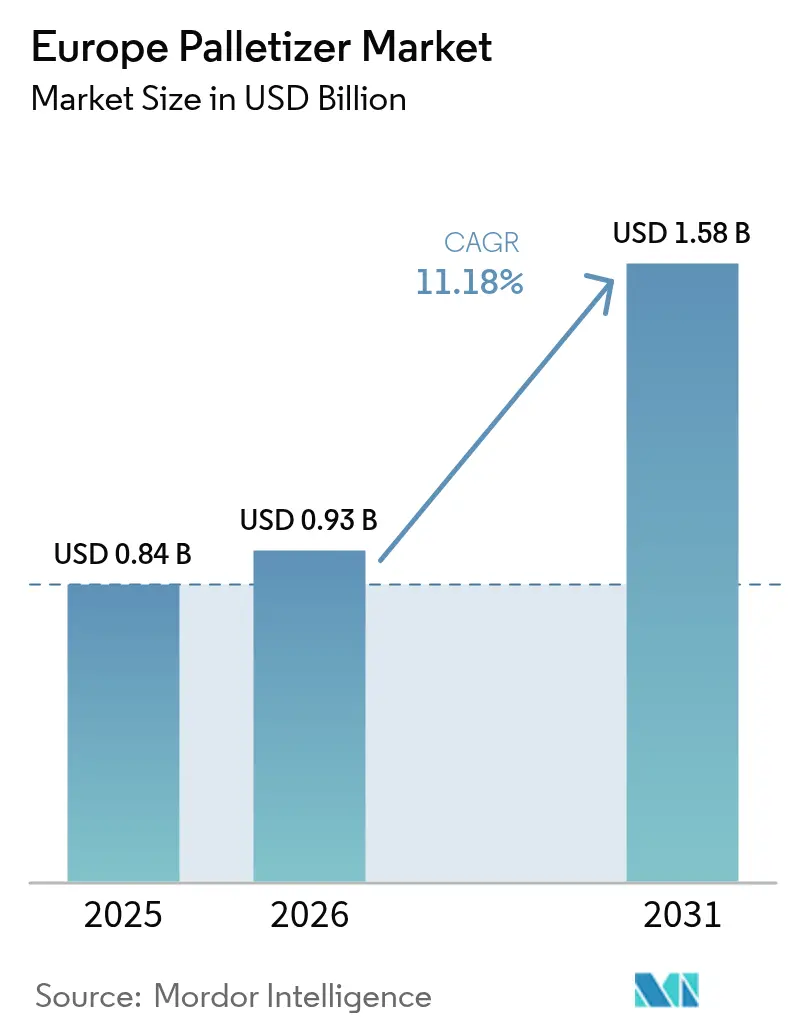

| Base Year Market Size (2025) | USD 0.84 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 11.18% CAGR |

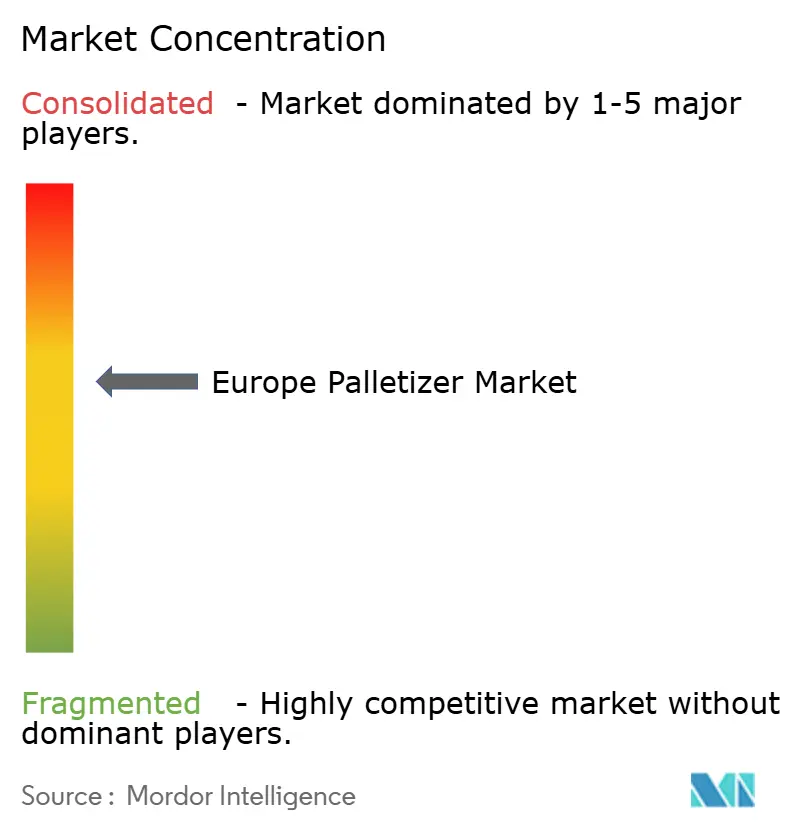

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Palletizer Market Analysis by Mordor Intelligence

The Europe Palletizer Market size is projected to expand from USD 0.84 billion in 2025 and USD 0.93 billion in 2026 to USD 1.58 billion by 2031, registering a CAGR of 11.18% between 2026 to 2031. Sustained investment is shifting end-of-line operations away from manual stacking toward fully automatic and collaborative robotic cells. High labor costs, stringent EU Machinery Regulation 2023/1230 compliance, and record e-commerce parcel volumes keep demand buoyant. Vendors that blend digital-twin commissioning with predictive-maintenance analytics are shortening payback periods to under two years, lowering the adoption barrier for mid-sized processors. At the same time, carbon-neutral logistics mandates are steering integrators toward low-energy drives and regenerative braking, embedding sustainability into capital-equipment selection. Traditional layer formers still dominate single-SKU beverage lines, yet flexibility premiums on robotic and gantry systems are accelerating their migration into brownfield sites.

Key Report Takeaways

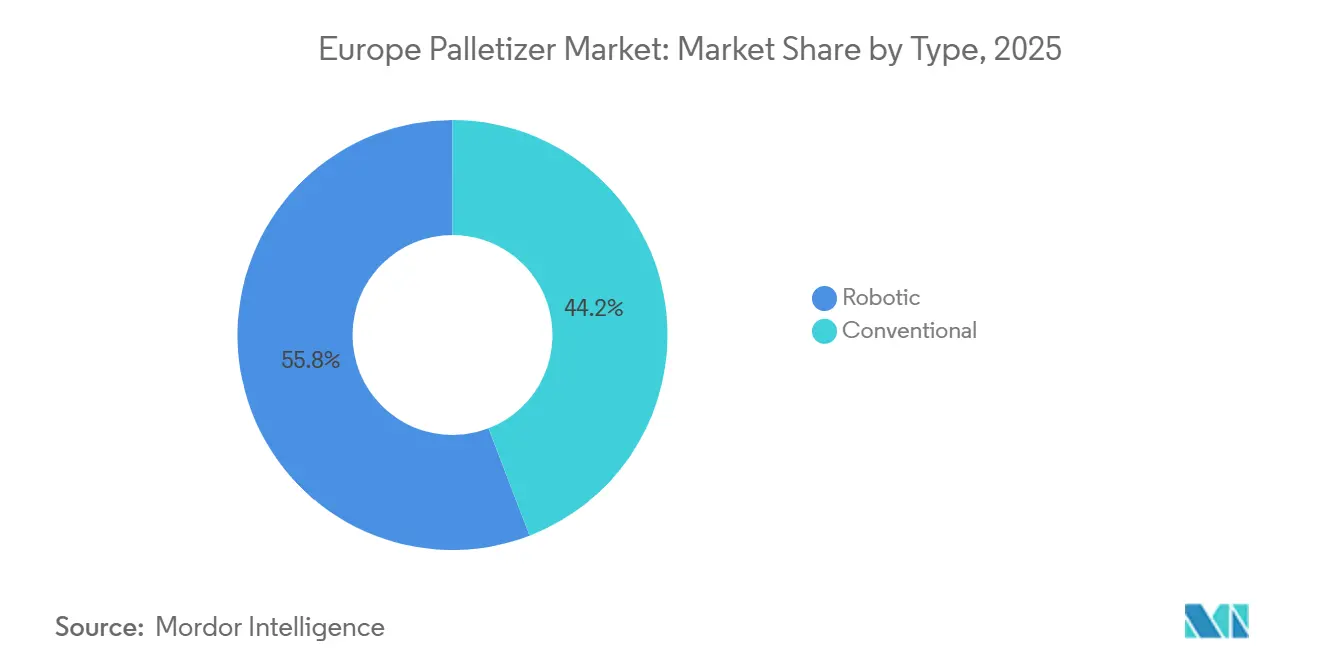

- By product type, robotic palletizers led with 55.84% revenue share in 2025, while the collaborative variant is advancing at an 11.87% CAGR through 2031.

- By end-user industry, food and beverage processors held 29.43% of the Europe palletizer market share in 2025, whereas e-commerce and logistics operations record the fastest projected CAGR at 12.62% through 2031.

- By system configuration, layer palletizers captured 40.18% of the Europe palletizer market size in 2025, yet gantry and robotic-arm system is forecast to expand at 13.01% CAGR over 2026-2031.

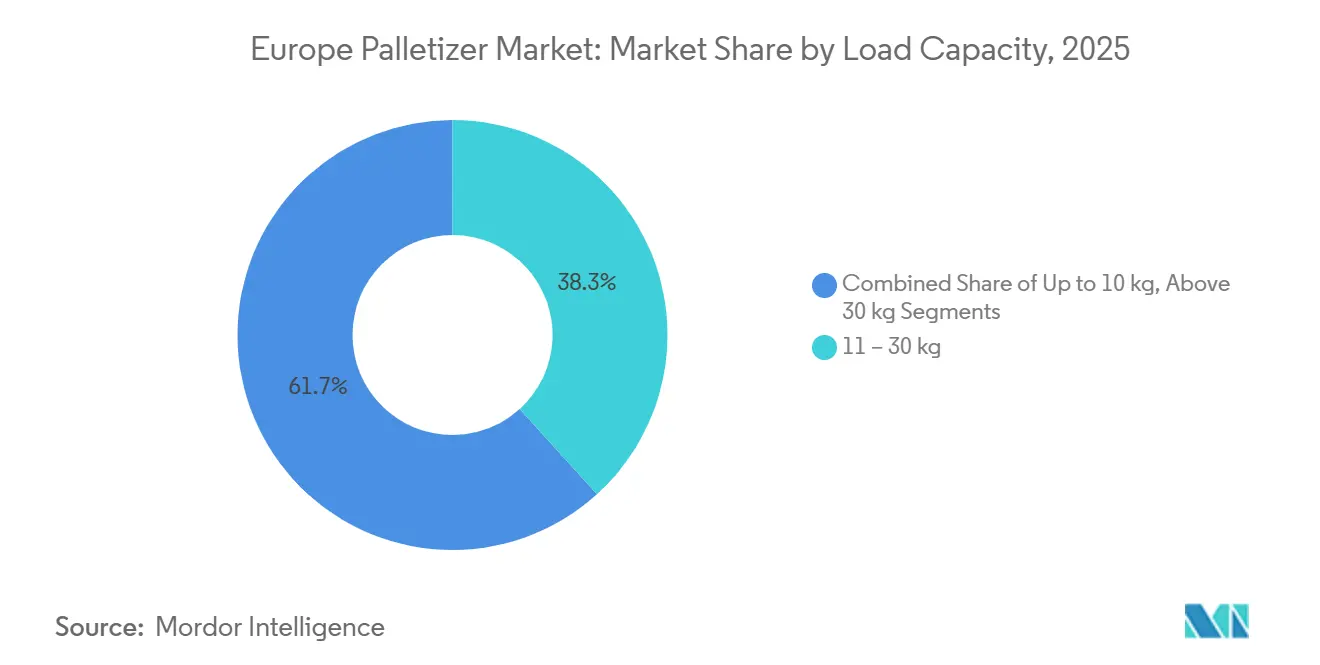

- By load capacity, the 11-30 kilogram segment accounted for 38.27% share of the Europe palletizer market size in 2025, while the up-to-10 kilogram bracket is projected to grow at 13.82% CAGR through 2031.

- By automation level, fully automatic cells represented 60.47% of the 2025 market size and remain on track for a 12.93% CAGR between 2026 and 2031.

- By country, Germany dominated the European palletizer market with a 24.51% share in 2025, and Netherlands is expected to post the fastest growth rate of 12.81% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Palletizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Automated Packaging Lines in Food and Beverage Processing | +2.8% | Germany, France, Netherlands, Italy, Spain | Medium term (2-4 years) |

| Labour Cost Escalation and Scarcity Across Western Europe | +2.5% | Germany, France, United Kingdom, Netherlands, Nordics | Short term (≤ 2 years) |

| Heightened Workplace Safety Regulations Favouring Robotic Palletizers | +1.9% | EU-27 (Germany, France, Italy, Spain leading) | Medium term (2-4 years) |

| E-commerce Boom Driving High-Throughput Warehousing Needs | +2.3% | Netherlands, Germany, United Kingdom, France, Poland | Short term (≤ 2 years) |

| Adoption of Collaborative Palletizing Cells in Mid-Sized Plants | +1.2% | Italy, Spain, France, Central Europe | Medium term (2-4 years) |

| Carbon-Neutral Logistics Hubs Demanding Energy-Efficient Palletizers | +0.9% | Netherlands, Germany, Nordics, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion Of Automated Packaging Lines In Food And Beverage Processing

European beverage fillers are matching high-speed aseptic filling and blow-molding lines with robotic palletizers that clear 36,000 bottles per hour, integrating seamlessly into manufacturing execution systems to eliminate downstream bottlenecks. Compact cells introduced in 2025 target craft brewers and regional dairies that previously relied on manual stacking, compressing floor-space needs by 40% while sustaining 98% uptime. Retrofits at detergent and snack plants delivered double-digit injury reductions within six months, strengthening the business case for modernization.[1]Packaging Europe, "Unilever Ploiești Plant Commissioning," packagingeurope.com The shift reframes palletizers as critical nodes in continuous-flow ecosystems rather than stand-alone assets, accelerating reorder cycles for next-generation equipment.

Labour Cost Escalation And Scarcity Across Western Europe

Warehouse operative wages rose 7.2% in Germany and 6.8% in France in 2024, while vacancy rates breached 12% across Benelux, prompting manufacturers to automate end-of-line tasks.[2]McKinsey and Company, "The Next Wave of Automation in Manufacturing," mckinsey.com Plants swapping two-shift crews for cobot cells now reach payback in under 18 months, as documented by bakeries and margarine processors that redeployed displaced staff to quality roles. Government upskilling grants soften social friction, further lowering resistance to capital projects. The arbitrage is greatest in the Nordics and the Netherlands where entry-level warehouse wages already exceed EUR 17 per hour (USD 19 per hour).

Heightened Workplace Safety Regulations Favouring Robotic Palletizers

EU Machinery Regulation 2023/1230 obliges ergonomic risk assessments for manual lifts above 15 kilograms, increasing compliance costs for human stacking and redirecting budgets toward robotic alternatives.[3]European Union, "Regulation (EU) 2023/1230 on Machinery," eur-lex.europa.eu EU-OSHA guidance published in 2024 explicitly endorses collaborative palletizers for repetitive lifting, citing musculoskeletal injury prevention. Early adopters report full elimination of lifting-related incidents within 12 months and avoidance of five-figure insurance surcharges. Procurement teams now list ISO 10218 force-limiting certification as a baseline filter when short-listing vendors, cementing regulation-driven demand.

E-Commerce Boom Driving High-Throughput Warehousing Needs

European parcel volumes jumped 18% in 2025, forcing third-party logistics hubs to install robotic palletizers rated above 500 layers per hour with sub-five-minute format changeovers. Flagship projects integrate autonomous mobile robots and vision-guided arms that dynamically reorder pallet patterns to maximize truck-fill density. Mixed-SKU capability is now a mandatory specification, and deployments commonly bundle cloud-based optimization algorithms that cut order-to-ship cycles by 35% . Capital commitments by global e-tailers signal that high-throughput palletizing will remain an investment priority through the decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for Fully Automatic Systems | -1.8% | Southern Europe, Central and Eastern Europe | Short term (≤ 2 years) |

| Downtime Risk Due to Complex Mechatronic Integrations | -1.2% | Germany, France, United Kingdom, Netherlands | Medium term (2-4 years) |

| Shortage of Skilled Programmers for Multi-Axis Robots | -0.9% | EU-27, particularly Eastern Europe and Iberia | Medium term (2-4 years) |

| Rising Pallet Size Diversity Complicating Standard Cell Design | -0.6% | United Kingdom, Netherlands, Nordics, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure For Fully Automatic Systems

Fully automatic cells cost EUR 250,000-500,000 (USD 282,000-565,000), levels that stretch the balance sheets of small processors in Italy and Spain where financing terms remain conservative. Many opt for semi-automatic pushers or refurbished layer formers, accepting lower throughput to conserve working capital. Vendors now experiment with subscription or leasing models at EUR 3,500 per month (USD 3,950) to democratize adoption, yet credit-risk thresholds still slow order conversion in regions where collateral coverage must exceed 150%. The capex hurdle is therefore the most immediate check on near-term growth.

Downtime Risk Due to Complex Mechatronic Integrations

Modern palletizers interlink servo drives, machine vision, and warehouse management software, creating single-point failure modes that can idle entire packaging islands. Hourly downtime costs average EUR 12,000 (USD 13,500) across the bloc, motivating buyers to favor OEMs with 24/7 remote diagnostics and four-hour field-service promises. Cloud-based condition-monitoring platforms now stream telemetry to predict bearing wear and vacuum degradation, but smaller integrators lack comparable infrastructure. Until predictive analytics and digital-twin commissioning become universal, risk-averse operators will stage modernization in phases, tempering the pace of fleet refresh cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Robotic Variants Capture Flexibility Premium

Robotic units dominated the Europe palletizer market with 55.84% revenue in 2025, reflecting their ability to palletize mixed SKUs at rapid changeover tempos that conventional layer formers cannot match. Collaborative arms priced below EUR 50,000 (USD 56,000) are breaking into mid-sized lines, and the Europe palletizer market size for cobot cells is expected to expand at an 11.87% CAGR through 2031. ABB and KUKA enhanced their high-payload portfolios in 2025, extending reach envelopes to 3.2 meters for beverage and dairy crates. Conventional systems remain competitive on single-SKU water and soft-drink lines, clocking 500 layers per hour at 30% lower capex, yet hybrid layouts pairing layer formers with side-by-side cobots are emerging in Germany and France as processors seek flexibility without wholesale replacement.

Collaborative units also satisfy ISO 10218 safety compliance without fencing, letting operators share floor space and redeploy robots between lines during short production runs. AI-enabled depalletizers launched in 2025 detect mixed patterns without pre-programming, slashing commissioning time from days to hours. These advancements are eroding the incumbent position of conventional machines in pharmaceuticals and personal care, where batch runs fragment and SKU counts proliferate.

By End-User Industry: E-Commerce Outpaces Traditional FMCG

Food and beverage producers retained 29.43% Europe palletizer market share in 2025, yet logistics providers are on course for a 12.62% CAGR as parcel hubs demand mixed-SKU builds optimized for truck loading rather than warehouse racking. Pharmaceuticals have accelerated adoption to uphold Good Distribution Practice, with robot vendors reporting double-digit inquiry growth in 2025. Cosmetics contract packagers demonstrate three-minute format swaps and nearly complete injury elimination after installing cobot cells. Chemical producers show slower uptake given ATEX certification needs, although explosion-proof gantry orders climbed 25% last year.

Logistics operators now specify vision-guided palletizers able to build route-sequenced loads, prompting integrators to merge end-of-line robots with AGVs that ferry pallets straight to dock doors, shaving 35% off order-to-ship cycles. FMCG processors still modernize, but increasingly via modular retrofits that drop cobots onto existing conveyors, preserving sunk capital.

By System Configuration: Gantry Technology Gains Ground

Layer machines captured 40.18% of 2025 installations, particularly in beverages where patterns repeat across shifts. The Europe palletizer market size for gantry and robotic-arm variants is, however, projected to rise 13.01% annually on the back of compact footprints suited to low-ceiling brownfield halls. Danish and Polish integrators unveiled sub-3-square-meter gantry cells that slot into tight corners without civil works. Modular sweep-gantry hybrids allow operators to toggle between bulk sweep and high-cycle pick modes by swapping end-effectors, making them attractive to contract packagers handling multiple clients.

Inline low-level machines are also proliferating in e-commerce centers where mezzanines cap available height, offering 570-layer-per-hour speeds with gentle handling for fragile tissue bundles. Consolidated multi-line stations connecting up to four upstream lines via spiral conveyors claim 10% higher efficiency and 40% less floor space than standalone units. The configuration mix is therefore tilting toward flexible architectures that retrofit quickly without structural reinforcements.

By Load Capacity: Light Payloads Drive Cobot Adoption

Products weighing 11-30 kilograms represented 38.27% of 2025 revenue, mirroring mainstream beverage and dairy case weights. Yet the fastest expansion lies in the up-to-10 kilogram bracket, expected to grow at 13.82% CAGR as blister packs, cosmetics tubes, and e-commerce parcels proliferate. Under-20 kilogram cobots equipped with force-limiting sensors prevent product crushing and let line operators reprogram pallet patterns via touch panels, compressing changeovers to minutes. Clean-room compliant models with stainless-steel grippers now penetrate pharmaceutical lines after passing EMA validation.

Heavier SKUs above 30 kilograms still require articulated robots rated to 500 kilograms or gantry cranes topping 3-meter reaches, with recent launches targeting beverage crates and returnable containers in Germany and France. Payload segmentation is blurring as dual-arm cobot prototypes handle both 5-gram sachets and 25-kilogram cases, letting multi-product plants amortize investment across wider order mixes.

By Automation Level: Fully Automatic Cells Dominate New Installations

Fully automatic configurations captured 60.47% of the 2025 market size and are projected to grow at a 12.93% CAGR because they integrate pallet dispensers, pad inserters, stretch wrappers, and AGV hand-off without human intervention. Operators pursuing real-time traceability embed RFID tags and synchronize pallet IDs into warehouse management systems, functionality that semi-automatic pushers cannot replicate. Modular families let users graduate from manual pallet infeed to full automation by adding destackers and outfeed conveyors over time.

Germany and the Netherlands lead the shift as labor constraints intensify, with music distributors and FMCG wholesalers already achieving sub-24-month paybacks after eliminating double-digit manual positions. Semi-automatic cells will persist in artisanal food segments and capital-tight markets where throughput falls below 7 cycles per minute, but the trajectory points decisively toward closed-loop control.

Geography Analysis

Germany accounted for 24.51% of Europe palletizer revenue in 2025, anchored by automotive, beverage, and pharma clusters across Bavaria and North Rhine-Westphalia that require 24/7 high-throughput lines. The national push toward Industry 4.0 feeds orders for robots integrated with MES dashboards, and OEMs leverage dense service footprints to secure long-term maintenance contracts. Innovation showcased at LogiMAT 2026, including omnidirectional AMRs handling 1,600 kilograms, cements Germany’s role as the bloc’s automation hub.

The Netherlands registers the fastest 12.81% CAGR to 2031 as Rotterdam’s port hinterland and the Venlo corridor build mega-fulfillment centers. Free-roaming pallet shuttles that navigate multilevel racking reduce warehouse footprints by one-quarter and appeal to site owners contending with tight land markets. Dutch hubs also pilot carbon-neutral equipment using regenerative drives, aligning with national climate targets.

France, the United Kingdom, Italy, and Spain form the next tier. France modernizes cosmetics and frozen-food lines, while the United Kingdom’s post-Brexit labor shortages accelerate investments around Birmingham and Manchester. Italian and Spanish mid-tier food plants install cobots with no fencing, taking advantage of rapid re-tooling for seasonal product runs. Central and Eastern Europe adopt robotic palletizing to increase export competitiveness, though financing remains tighter and programmer availability thinner. Russia lags due to limited access to Western robotics yet substitutes with locally integrated Asian arms for dairy and bakery applications.

Logistics-led carbon-neutral initiatives are expanding across Germany, the Netherlands, and the Nordics. Global carriers are electrifying fleets and adopting palletizers that recuperate kinetic energy, reducing electricity usage by 15%. While these trends emphasize energy-efficient designs in Western Europe, throughput and labor substitution continue to be stronger drivers in Eastern Europe.

Competitive Landscape

The top seven suppliers ABB, KUKA, FANUC, Yaskawa, KION Group, Krones, and Beumer, collectively control about 60% of sales, bundling robots, conveyors, and lifetime service agreements. Competition intensifies around vision software and digital-twin commissioning. Universal Robots collaborated with Siemens and Robotiq in 2026 to debut a UR20-based palletizer that predicts gripper wear and automatically optimizes suction points, cutting unplanned downtime by 25% in pilots. KUKA’s KR FORTEC line integrates quick-swap gripper couplings, enabling plants to switch between vacuum and mechanical tooling without recalibration.

Mid-sized specialists Premier Tech, Columbia Machine, Scott Automation, and Ehcolo post gains by rolling out modular cobot cells priced 30-40% below gates-fenced gantry systems and promising sub-two-week commissioning for brownfield sites. AI vision startups such as Sereact embed zero-shot learning that recognizes unseen cartons, driving down integration time from weeks to days and attracting fulfillment centers juggling daily SKU churn.

Regulatory compliance exerts a barrier to entry. Vendors invest in ISO 10218 and CE marking to penetrate food and pharma verticals. The October 2025 sale of ABB’s robotics arm to SoftBank reallocates capital toward electrification but retains the European service matrix, ensuring continuity for installed bases. The market therefore balances incumbent scale with insurgent agility, each contesting emerging niches like subscription-priced palletizing and AI-powered mixed-case depalletizing.

Europe Palletizer Industry Leaders

-

ABB Ltd

-

Beumer Group GmbH and Co. KG

-

KION Group AG (Dematic)

-

Krones AG

-

KUKA AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SSI SCHAEFER and Moffett Automation formed a partnership to supply free-roaming pallet shuttles for space-constrained, deep-freeze warehouses.

- January 2026: Aquila invested EUR 5 million (USD 5.6 million) in an AI vision system at its Romanian FMCG warehouse, cutting manual work by 40%.

- January 2026: Fives Intralogistics selected Agorando Technologies to automate a German fulfillment center with Caja goods-to-person robotics, targeting Q3 2026 launch.

- January 2026: Universal Robots and Robotiq unveiled a next-generation palletizing solution at CES 2026 with Siemens Digital Twin Composer, reducing commissioning time by 30%.

Europe Palletizer Market Report Scope

A palletizer is a machine used in warehouses and manufacturing facilities to automatically stack products such as boxes, bags, bottles, or cartons onto a pallet in an organized, stable pattern for storage or shipping. A palletizer receives products from a conveyor and arranges them layer by layer on a pallet based on a programmed stacking pattern. Once the pallet is full, it’s moved away and replaced with an empty one.

The Europe Palletizer Market Report is Segmented by Type (Conventional, Robotic), End-User Industry (Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Chemicals), System Configuration (Inline, Layer, Gantry/Robotic Arm), Load Capacity (Up to 10 kg, 11-30 kg, Above 30 kg), Automation Level (Semi-Automatic, Fully Automatic), and Geography (Germany, France, UK, Italy, Spain, Russia, Netherlands, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

By Type

| Conventional |

| Robotic |

By End-User Industry

| Food and Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Chemicals |

By System Configuration

| Inline Palletizers |

| Layer Palletizers |

| Gantry / Robotic Arm Palletizers |

By Load Capacity

| Up to 10 kg |

| 11 - 30 kg |

| Above 30 kg |

By Automation Level

| Semi-Automatic |

| Fully Automatic |

By Country

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Rest of Europe |

| By Type | Conventional |

| Robotic | |

| By End-User Industry | Food and Beverages |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Chemicals | |

| By System Configuration | Inline Palletizers |

| Layer Palletizers | |

| Gantry / Robotic Arm Palletizers | |

| By Load Capacity | Up to 10 kg |

| 11 - 30 kg | |

| Above 30 kg | |

| By Automation Level | Semi-Automatic |

| Fully Automatic | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe palletizer market by 2031?

The market is forecast to reach USD 1.58 billion by 2031, expanding at an 11.18% CAGR from 2026 to 2031, driven by labor scarcity, safety regulations, and e-commerce throughput demands.

Which configuration type is growing fastest in Europe?

Gantry and robotic-arm palletizers are advancing at 13.01% CAGR through 2031, outpacing layer formers due to compact footprints and flexibility in brownfield retrofits.

Why are collaborative robots gaining traction in palletizing applications?

Cobots eliminate safety fencing, allow rapid redeployment across lines, and deliver sub-two-year paybacks for mid-sized plants, making them ideal for operations with frequent SKU changes.

Which end-user segment is expanding most rapidly?

E-commerce and logistics operations are growing at 12.62% CAGR through 2031, surpassing traditional food and beverage processors as parcel volumes surge and mixed-SKU builds become standard.

What regulatory factors are accelerating adoption?

EU Machinery Regulation 2023/1230 mandates ergonomic assessments for manual lifts above 15 kilograms, while EU-OSHA guidance explicitly recommends robotic palletizers to reduce musculoskeletal injuries.

How are vendors addressing capital-expenditure concerns?

Subscription models priced at EUR 3,500 per month (USD 3,950) bundle hardware, software updates, and predictive maintenance, lowering the barrier for small and medium enterprises in Southern and Eastern Europe.

Page last updated on: