Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.54 Billion |

| Market Size (2031) | USD 4.77 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

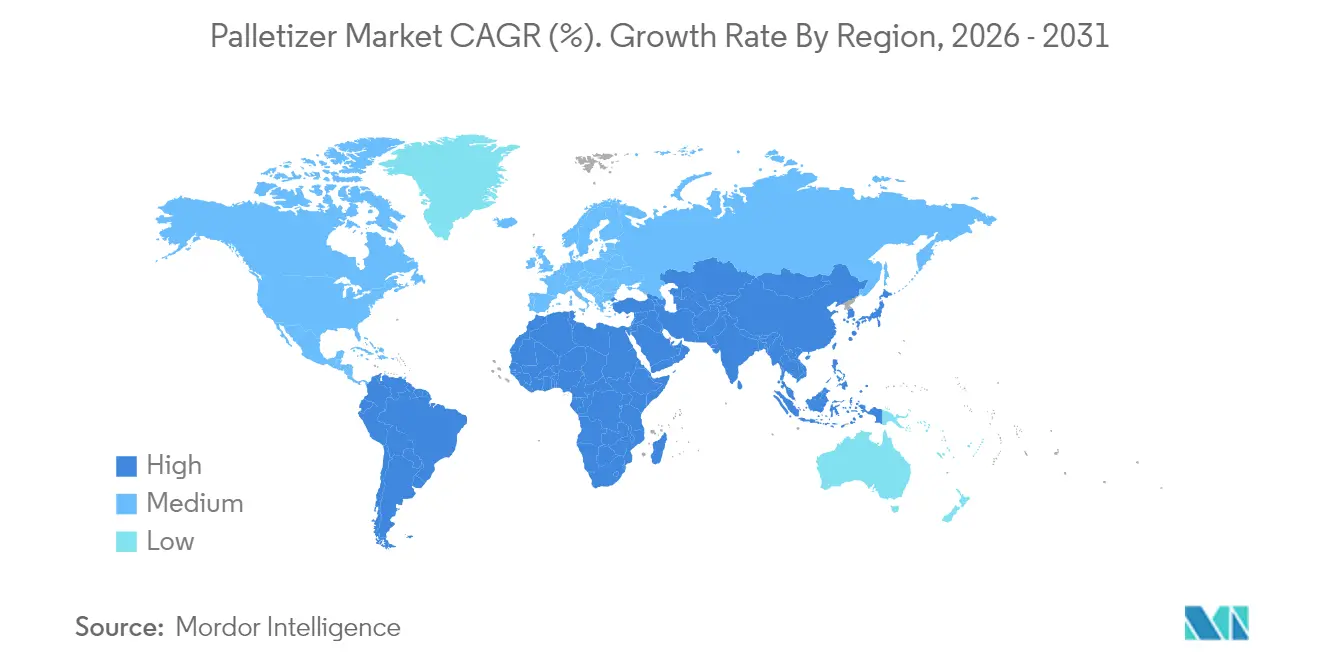

| Fastest Growing Market | Latin America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Palletizer Market Analysis by Mordor Intelligence

The palletizer market size is expected to grow from USD 3.34 billion in 2025 to USD 3.54 billion in 2026 and is forecast to reach USD 4.77 billion by 2031 at 6.12% CAGR over 2026-2031. Momentum comes from the sustained shift away from manual pallet building toward automated, software-driven systems that resolve labor shortages, optimize trailer utilization, and meet rising e-commerce throughput requirements. Growth is reinforced by the premium that mixed-SKU, AI-enabled palletizing commands, the rapid spread of rental models that lower upfront costs, and the expanding appeal of collaborative robots in space-constrained factories. Competitive intensity remains moderate: no single player holds more than 15% revenue, yet pricing pressure surfaces as regional integrators package robots with subscription or robotics-as-a-service contracts. South America registers the fastest regional expansion as reshoring and logistics upgrades intersect with government tax incentives; meanwhile APAC maintains volume leadership due to China’s scale in robot production and deployme

Key Report Takeaways

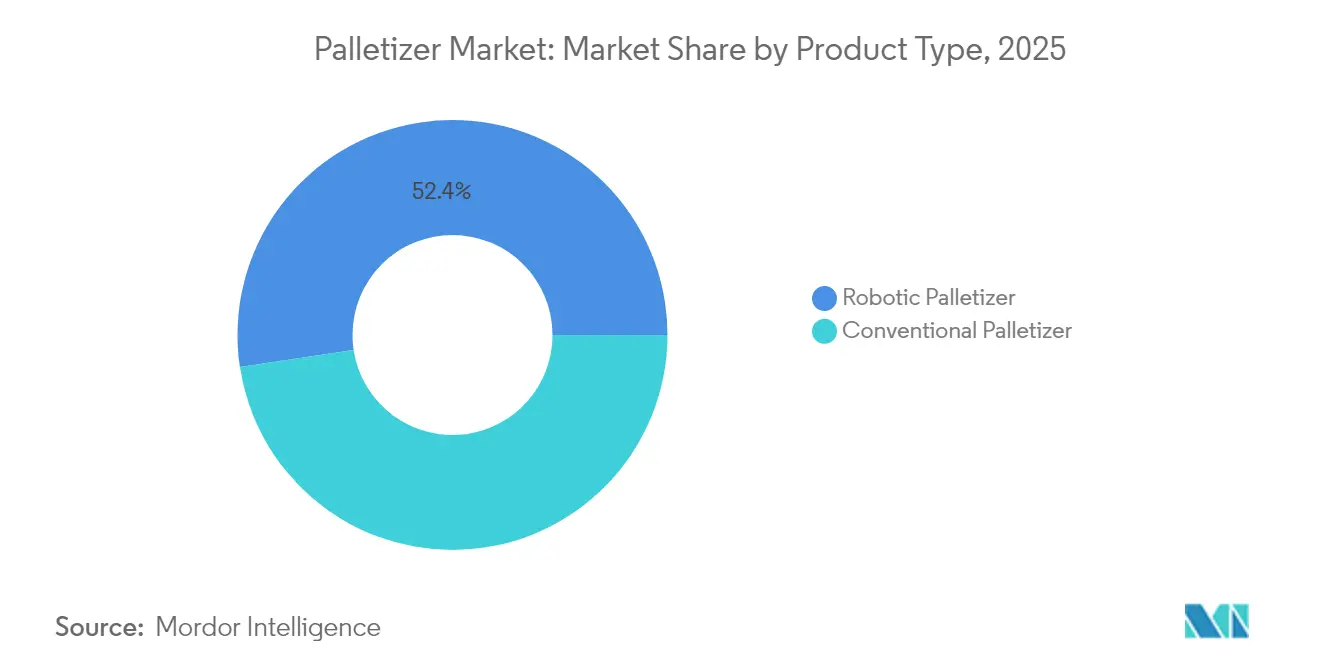

- By product type, conventional palletizers led with 47.62% revenue share in 2025, while collaborative robots are forecast to expand at a 6.09% CAGR through 2031.

- By payload capacity, medium-duty systems (50-150 kg) accounted for 40.88% of the palletizer market share in 2025; heavy-duty models (>150 kg) are projected to deliver the highest 7.18% CAGR to 2031.

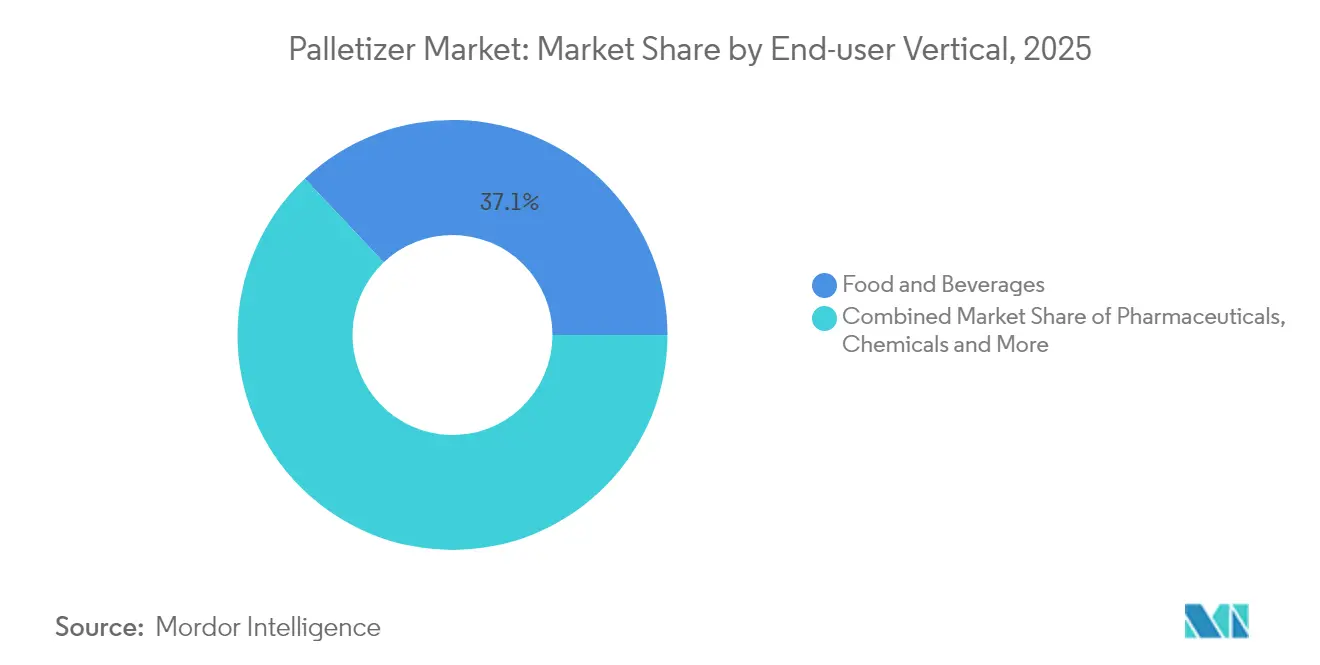

- By end-user vertical, food and beverages represented 37.06% of the palletizer market size in 2025, whereas e-commerce and 3PL facilities are advancing at a 7.55% CAGR.

- By geography, APAC captured 37.84% of 2025 revenue, yet South America shows the fastest 7.86% CAGR through 2031.

- By sales channel, direct OEM sales held 45.48% in 2025, but rental and leasing models are climbing at an 8.24% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Palletizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing e-commerce SKU complexity | +1.8% | Global, concentrated in North America & APAC | Medium term (2-4 years) |

| Labor shortages accelerating warehouse automation | +2.1% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Packaging-line ROI improvements from plug-and-play cobots | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Surge in FMCG sustainability mandates favouring robotic mixed-load palletizing | +0.9% | EU & North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing e-commerce SKU complexity

Fulfilment centres now handle volumes that exceed 180 billion cases yearly, with single sites processing more than 50,000 SKUs—ten times the diversity typical of legacy retail hubs.[1]Apptronik, “Case Picking”, Apptronik, apptronik.comFixed-pattern equipment cannot keep up, prompting adoption of AI-powered systems such as the Lucas Warehouse Optimization Suite, which lifts palletizing efficiency 15-20% by balancing weight, fragility, and stackability in real time. Premium platforms fetch 30-40% higher margins but still lower total shipping cost as optimized loads cut empty trailer space by up to 30%.

Labor shortages accelerating warehouse automation

Critical staffing gaps across 41 factory occupations in China and 15-20% vacancy rates in North American warehouses have compressed automation payback to under 18 months. Mid-market plants now automate runs of just 100 units per hour, unlocking a broader palletizer market as collaborative systems redeploy employees to safer, higher-value roles.

Packaging-line ROI improvements from plug-and-play cobots

A new class of 30 kg-payload cobots such as FANUC’s CRX-25iA eliminates up to 80% of the fencing and programming cost typical of standard industrial robots. Rental offers like Columbia/Okura’s miniPAL at USD 5,450 per month streamline trials, enabling rapid rollout without balance-sheet strain. [2]Columbia/Okura, “Columbia/Okura Launches New miniPAL® Cobot Rental Program”, MHI, og.mhi.org

Surge in FMCG sustainability mandates favouring robotic mixed-load palletizing

EU rules requiring 65% packaging recycling by 2025 spur buyers toward robots that trim voids and reduce cushioning material by 15-25%.[3]Pharma Manufacturing, “Keeping Pace with Pharma Packaging”, Pharma Manufacturing, pharmamanufacturing.com KHS’ Nature MultiPack shows how algorithmic stacking maintains stability while using 90% less adhesive khs.com. Energy-efficient drives and regenerative braking further cut carbon footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for heavy-payload robotic arms | −1.4% | Global, acute in developing markets | Short term (≤ 2 years) |

| Integration complexity with legacy MES/WMS | −0.8% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX for heavy-payload robotic arms

Installations rated above 150 kg often top USD 500,000, a hurdle for manufacturers shipping fewer than 500 pallets daily. Robotics-as-a-service pioneers such as Formic counter this barrier with USD 3,975 monthly bundles, yet tradeoffs around customisation and ownership persist.

Integration complexity with legacy MES/WMS

Connecting palletizers to heterogeneous software stacks can double project budgets and stretch timelines to 12 months. Forthcoming EU Machinery Regulation 2023/1230 tightens cybersecurity validation, raising the bar for vendors that lack deep software integration skills.[4]TÜV SÜD, “Machine Safety & the EU Machinery Directive”, TÜV SÜD, tuvsud.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conventional Systems Face Cobot Disruption

Conventional machines retained 47.62% revenue in 2025 as high-speed lines exceeding 1,000 cases per hour depend on proven layer devices. Yet the palletizer market sees collaborative units outpace at 6.09% CAGR, capturing greenfield investments in small-footprint sites that crave safety-certified, fence-free operation. Robotic articulated arms occupy the mid-performance tier, balancing throughput against changeover flexibility for mixed product portfolios. Hybrid systems, blending layer formers with robotic pickers, emerge in niche beverage and personal-care cells but remain cost-intensive.

Vendors differentiate through full-stack ecosystems: Doosan’s P-SERIES coupled with Rocketfarm’s Pally software reduces deployment time and elevates user autonomy. As customers prioritise single-source accountability over stand-alone hardware, suppliers bundling vision, simulation, and lifecycle services widen addressable opportunities inside the palletizer market.

By Payload Capacity: Heavy-Duty Applications Drive Premium Growth

Medium-duty solutions dominated with 40.88% share, reflecting consumer goods’ bias toward 50-150 kg boxes. However the palletizer market size for heavy-duty systems is slated to expand at a 7.18% CAGR as bulk shippers consolidate loads to curb labour and freight costs. Energy-efficient servo architectures and advanced safety scanners now let 180 kg cobots operate alongside staff, as seen in Bob’s Red Mill installations. These capabilities command 40-60% price uplifts compared with mid-tier peers, yet users justify the premium through reduced forklift moves and lower workers’ compensation claims.

Light-duty cells under 50 kg address pharmaceuticals and electronics, where cleanroom compliance and precision trump brute force. Vendors targeting this end of the palletizer market leverage class-10-rated enclosures and vacuum grippers to protect high-value items, maintaining a stable but slower growth profile.

By End-user Vertical: E-commerce Disrupts Traditional Hierarchies

Food and beverages remained the anchor at 37.06% of 2025 revenue, drawn to stainless-steel, wash-down-rated machinery that assures hygiene. Yet the palletizer market size for e-commerce and 3PL segments is forecast to grow 7.55% CAGR as omnichannel retailers demand robots that build mixed SKU pallets in unpredictable sequences. AI-enabled vision and gentle grippers allow cosmetics weighing 0.5 kg to be stacked beside 25 kg components without damage.

Pharmaceuticals apply distinct pressure: drug-trace regulations necessitate serialization-ready palletizers linking vision and data capture, while chemicals require ATEX-certified arms in hazardous areas. Personal-care brands boost demand for quick-changeover cells that mirror rapid product launches.

By Sales Channel: Rental Models Reshape Market Access

Direct OEM contracts still represented 45.48% revenue in 2025, favoured for large plant rollouts needing deep engineering interaction. Nonetheless, rental and leasing lines are pacing the palletizer market at an 8.24% CAGR, appealing to CFOs who prefer OPEX over CAPEX. Columbia/Okura’s miniPAL option with 3-month minimum terms de-risks pilot projects.

System integrators preserve relevance by stitching robots into broader conveyance and quality-inspection flows. Retrofits gain traction as users upgrade decade-old layer machines with AI software and safety scanners to extend asset life without full replacement.

Geography Analysis

APAC held 37.84% of 2025 revenue, with China alone installing 52% of new global robots by 2022. Domestic suppliers now secure 36% of their home market, pushing price points lower and accelerating diffusion among tier-two factories. Japan built 45% of the world’s robots and channelled USD 7.35 billion in 2024 orders into logistics, food, and pharma lines, backed by a USD 39.3 billion (USD 43.7 billion) government supply-chain fund . India’s Production-Linked Incentive schemes spark automation across automotive and generics plants, though adoption pockets remain uneven due to skill gaps.

South America records the strongest 7.86% CAGR trajectory to 2031 as Brazil’s food and auto sectors automate pallet building for export compliance. Mexico rides near-shoring trends to supply the US market with tariff-proof goods, intensifying demand for robots certified to North American safety codes. Argentina’s grain processors install palletizers that stabilise 1-tonne bulk bags for long ocean voyages despite macroeconomic volatility.

North America and Europe show measured growth driven by replacement rather than capacity additions. Upcoming Regulation (EU) 2023/1230 compels vendors to harden cybersecurity, advantaging those with certified software stacks. US reshoring programs lift the palletizer market as SMB manufacturers seek flexible cobots that accommodate frequent SKU changeovers and mitigate labour constraints in ageing rural workforces.

Regulatory Landscape

Palletizers sold into the European Union fall under Regulation (EU) 2023/1230 (Machinery Regulation), which replaces the prior Machinery Directive framework and raises the compliance bar for connected machinery, including requirements tied to safety, cybersecurity, and documentation when machines incorporate digital functions. In March 2026, Commission Implementing Decision (EU) 2026/546 updated the EU list of harmonized standards relevant to packaging machinery, shaping how palletizer OEMs and integrators demonstrate conformity for CE marking.

On the standards side, safety requirements are anchored by EN 415-4, with the 2026 edition (SIST EN 415-4:2026) addressing palletizers and depalletizers. Robot-specific safety and integration are benchmarked globally by ISO 10218-1:2025 and ISO 10218-2:2025. In the United States, industrial robot safety practice is aligned to ANSI/A3 R15.06-2025. OSHA enforcement relies on general duty obligations supported by recognized consensus standards rather than a robotics-only federal standard, keeping risk assessments, safeguarding, and training central to end-of-line palletizing deployments.

Value Chain Analysis

The palletizer value chain begins with core component suppliers, including robot arms, servo drives, sensors, safety scanners, and controls, before moving to OEMs that package mechanics, end-of-arm tooling, and software into conventional, robotic, or collaborative palletizing cells. Control and software platforms from automation majors such as Siemens and Rockwell Automation underpin many systems through PLCs and engineering environments, while robot OEMs such as ABB, FANUC, KUKA, and Yaskawa supply robot hardware that palletizer builders and integrators often standardize around. Specialized palletizing-focused players, including Fuji Robotics and Columbia/Okura, provide application-specific cell designs and tooling that reduce engineering time for common case, bag, and mixed-load patterns.

System integrators handle layout engineering, line integration with conveyors and safety systems, and connectivity to MES/WMS. Interoperability and commissioning complexity make this layer a recurring bottleneck. Distribution and aftermarket service depend heavily on local field support for spares, preventive maintenance, and uptime commitments, which increases the influence of integrators and OEM service contracts in project decisions. Technology shifts toward PLC-native control of robots, such as Comau Easy Palletizer concepts, and toward more open-architecture integration reduce reliance on proprietary controllers, but they also raise the importance of validated safety design, standardized interfaces, and reliable end-effector supply chains across diverse SKUs.

Competitive Landscape

The palletizer market is characterized by moderate fragmentation. Legacy automation majors—ABB, FANUC, KUKA—leverage global service footprints and large installed bases, but none surpass 15% revenue share. Their current strategy emphasises software platforms and vertically integrated service contracts that embed customers for complete line life cycles.

Specialist players pursue blue-ocean tactics: Formic monetises uptime through robotics-as-a-service, assuming maintenance risk and earning subscription fees. Columbia/Okura differentiates via short-term rentals that compress decision cycles and capture demand in midsize enterprises. AI-native entrants such as Ambi Robotics refine perception algorithms to solve complex item variability, targeting e-commerce nodes overlooked by traditional integrators.

M&A remains an accelerant. Krones, after posting EUR 5.29 billion (USD 5.73 billion) in 2024 revenue, is layering software and PET preform capacity through the Netstal acquisition, thereby broadening its packaging ecosystem. Industrial groups like Duravant and ProMach continue roll-ups that deliver cross-selling synergies across conveyors, depalletizers, and stretch-wrappers—extending customer lifetime value.

Palletizer Industry Leaders

ABB Ltd.

BEUMER Group GmbH & Co. KG

Yaskawa Electric Corp.

FANUC Corp.

KUKA AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Mixed-load palletizing for e-commerce and 3PL operations is a clear whitespace where AI-based perception and stacking logic reduce custom engineering and expand the range of SKUs handled per cell, consistent with the broader shift toward software-driven palletizing systems. Vendor activity in 2026 points in this direction. ABB collaborated with Jacobi Robotics to bring OmniPalletizer AI software into its ecosystem for integrator deployment, while FANUC demonstrated AI-assisted perception for adaptive palletizing at MODEX 2026, both reinforcing demand for configurable, mixed-case palletizing workflows rather than fixed-pattern equipment.

Opportunities also cluster around modernization programs where palletizing is integrated into larger logistics or plant automation projects that can justify turnkey integration and lifecycle services. Danfoss initiated an upgrade of its Central Distribution Center in Rodekro, Denmark in July 2026, with plans to automate 70-80% of palletizing activities using robotic systems. Smurfit Westrock completed a USD 136 million facility in Pleasant Prairie, Wisconsin in April 2025 with integrated robotics, indicating continued investment in end-of-line automation inside major distribution and packaging footprints. For suppliers, this favors modular palletizing cells, rentals and leasing models, and integration-ready software stacks that shorten commissioning cycles and support compliance across safety and cybersecurity requirements.

Recent Industry Developments

- April 2026: ABB announced a collaboration with Jacobi Robotics to integrate OmniPalletizer AI software into its robotics ecosystem, targeting faster deployment of AI-driven mixed-case palletizing through its integrator network. The announcement places software at the center of differentiating end-of-line systems, particularly when SKU variability makes conventional, fixed-pattern palletizing less efficient.

- April 2025: Smurfit Westrock completed a USD 136 million, 595,000-square-foot facility in Pleasant Prairie, Wisconsin, designed with integrated robotics that includes palletizing automation. The project indicates how large greenfield packaging and distribution sites are building end-of-line robotics from the start rather than relying on later retrofits.

- August 2024: Duravant acquired T-TEK Material Handling, adding material handling and related capabilities that can be bundled with palletizing and depalletizing projects. The deal supports one-stop, integrated end-of-line offerings where conveyors, handling, and robotic cells are procured together to reduce integration risk.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The palletizer market is defined as revenues generated from equipment used to automatically stack packaged products onto pallets for storage and shipment in industrial end-user facilities.

Scope exclusions: Used or refurbished units and adjacent end-of-line machines such as stretch wrappers are excluded from this sizing.

Segmentation Overview

- By Product Type

- Conventional Palletizer

- High-Level Palletizer

- Low-Level Palletizer

- Robotic Palletizer

- Cartesian/Gantry

- Articulated

- SCARA

- Collaborative (Cobot)

- Hybrid Palletizer

- Conventional Palletizer

- By Payload Capacity

- Light-Duty (<50 kg)

- Medium-Duty (50-150 kg)

- Heavy-Duty (>150 kg)

- By End-user Vertical

- Food & Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Chemicals

- E-commerce and 3PL

- Other Verticals

- By Sales Channel

- Direct OEM Sales

- System Integrators

- After-market Retrofits and Upgrades

- Rental / Leasing

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- APAC

- China

- Japan

- India

- South Korea

- Rest of APAC

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on packaging throughput, industrial output, and automation adoption, which are key demand signals for palletizers. We refer to public sources such as the US Census Bureau manufacturing statistics, USITC trade data, Eurostat industrial production series, UN Comtrade, and association materials from packaging and automation bodies where definitions are spelled out.

To connect these signals back to market value, we also review manufacturer websites, product catalogs, and public filings and presentations where shipment trends, order intake language, and regional exposure are discussed. In parallel, we use paid subscriptions for company financials and news, patent databases, and, where needed, shipment-level import/export databases to sanity check activity in key equipment categories. The desk sources mentioned are illustrative and not exhaustive, and many other references were used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure test the demand model and to fill gaps that desk sources cannot answer well, such as typical pricing bands, integration share, replacement cycles, and what is counted as a palletizer in actual customer bids. We speak with OEM-side leaders, system integration teams, distributors, and end-user operations and maintenance roles across APAC, EMEA, and the Americas so that region-specific buying patterns are reflected in the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | APAC: 48% |

| Mid tier: 44% | Functional/Unit leaders: 40% | EMEA: 30% |

| Smaller Players: 20% | Managers: 43% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where industrial packaging activity is reconstructed from end-use output and shipment trends, and then filtered by automation penetration and typical palletizing line intensity by facility type. Once the demand pool is framed, we convert it to revenue using average selling price ranges that vary by automation level, payload handling needs, and integration complexity.

To avoid relying on one set of assumptions, we add selective bottom-up checks through supplier and channel roll-ups in sampled countries, along with sanity checks on how many palletizing lines are typically installed per new or expanded site. The model is driven by practical inputs such as manufacturing production indices, packaged goods volumes, labor availability and wage pressure, installed base replacement timing, and the mix shift toward higher automation in high-throughput lines.

Forecasting is run using scenario analysis supported by multivariate regression, where the demand curve is tied to industrial output and automation investment cycles, then reviewed against what interviewees expect for lead times, budgeting behavior, and price movement. Where the cross-checks indicate missing coverage for smaller integrators or local imports, a controlled uplift is applied and then re-tested so the final number stays traceable to real activity signals.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, such as whether the implied unit demand matches typical plant expansion rates and whether the value trend aligns with quoted price ranges from the field. Outliers are flagged early, and we re-check the drivers behind them, which often come from currency timing, one-off capex cycles, or unrealistic price escalation.

Before sign-off, the model is reviewed in steps by another analyst, and any large variances trigger re-contact with select respondents to confirm what changed. Reports are refreshed annually, and interim updates are made when material events happen, such as sharp shifts in industrial production, trade flows, or automation spending. Right before delivery, a fresh pass is done to ensure the latest public data and market signals are reflected.

Mordor Intelligence's Palletizer Market Sizing Compared With Other Published Estimates

Published market estimates for palletizers can differ even when they look like they measure the same thing, because the product scope, year selection, and pricing logic are not consistent across studies. Differences also come from whether system integration value is included, how regional currency conversions are timed, and how much primary validation is used to correct desk assumptions.

A common gap driver in this market is scope creep into adjacent end-of-line equipment or into refurbished units, which changes totals without being obvious in the headline. Another driver is the treatment of turnkey projects, where some figures count only the machine, while others fold in a larger share of installed project value. The spread is mainly explained by counting only new palletizer equipment and turnkey system sales through integrators, while keeping used units and adjacent wrapping equipment outside scope, which is how the model is set up at Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.54 B (2026) | |

| Global Consultancy A | USD 3.37 B (2025) | Uses a different base year and may apply a broader machine definition without clearly separating integrator project value from equipment-only revenue, which can shift the implied pricing level year to year. |

| Industry Publisher B | USD 3.07 B (2024) | Starts from an earlier base year and appears to use more generalized growth assumptions across automation types, which can understate the recent mix shift toward higher-value automated palletizing lines in faster-growing regions. |

The table shows that year choice and what gets counted around the palletizing line are the two biggest reasons totals move apart. By keeping inclusions explicit, checking pricing and penetration with field inputs, and then validating against independent industrial activity signals, the resulting value stays balanced and repeatable even when public data is not perfect.

Key Questions Answered in the Report

What is the size of the palletizer market in 2026?

The palletizer market is valued at USD 3.54 billion in 2026.

Which region leads the palletizer market?

APAC leads, accounting for 37.84% of 2025 revenue due to China’s large-scale robot adoption.

Which product segment is growing fastest?

Collaborative palletizers are expanding at a 6.09% CAGR thanks to safety-certified, fence-free deployment.

Why are rental models important in palletizing?

Rental and leasing lower CAPEX, enabling mid-market factories to adopt automation and are rising at an 8.24% CAGR.

What payload class shows the highest growth?

Heavy-duty systems above 150 kg are projected to grow 7.18% annually as firms consolidate shipments.

How does labor shortage influence palletizer adoption?

Acute staffing gaps cut automation payback to less than 18 months, accelerating investment in robotic palletizing.

Page last updated on: