Offshore Decommissioning Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.08 Billion |

| Market Size (2031) | USD 11.52 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

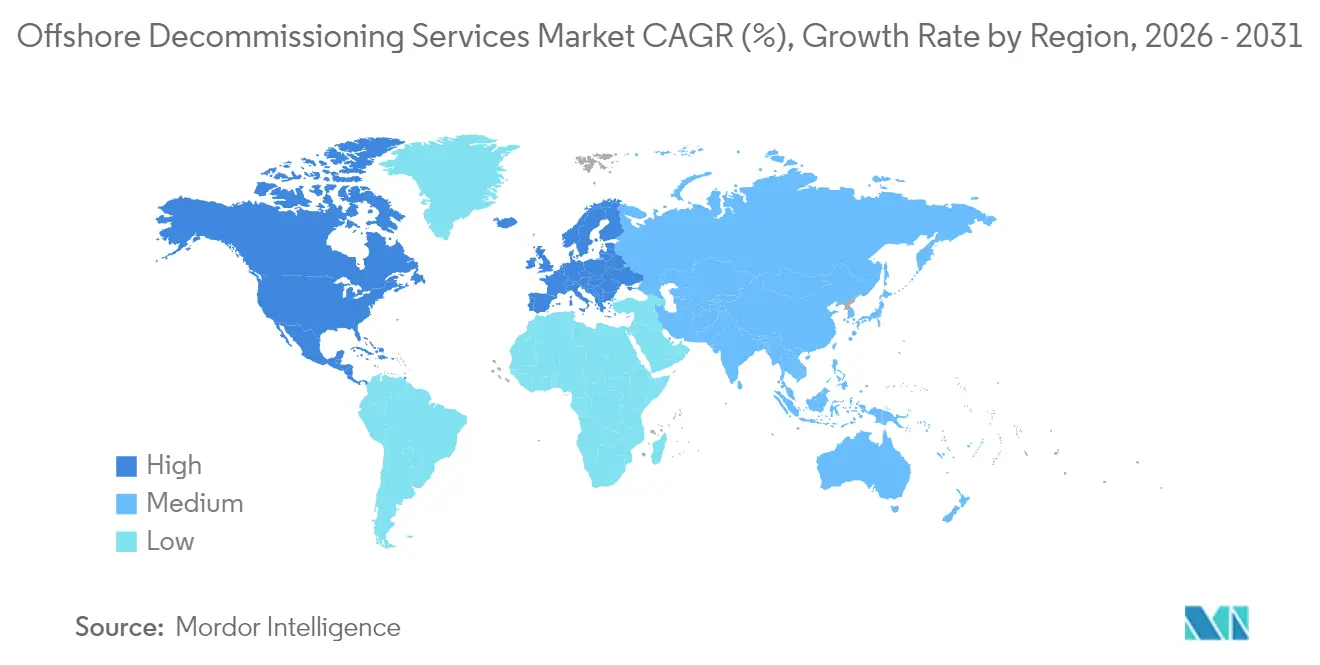

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offshore Decommissioning Services Market Analysis by Mordor Intelligence

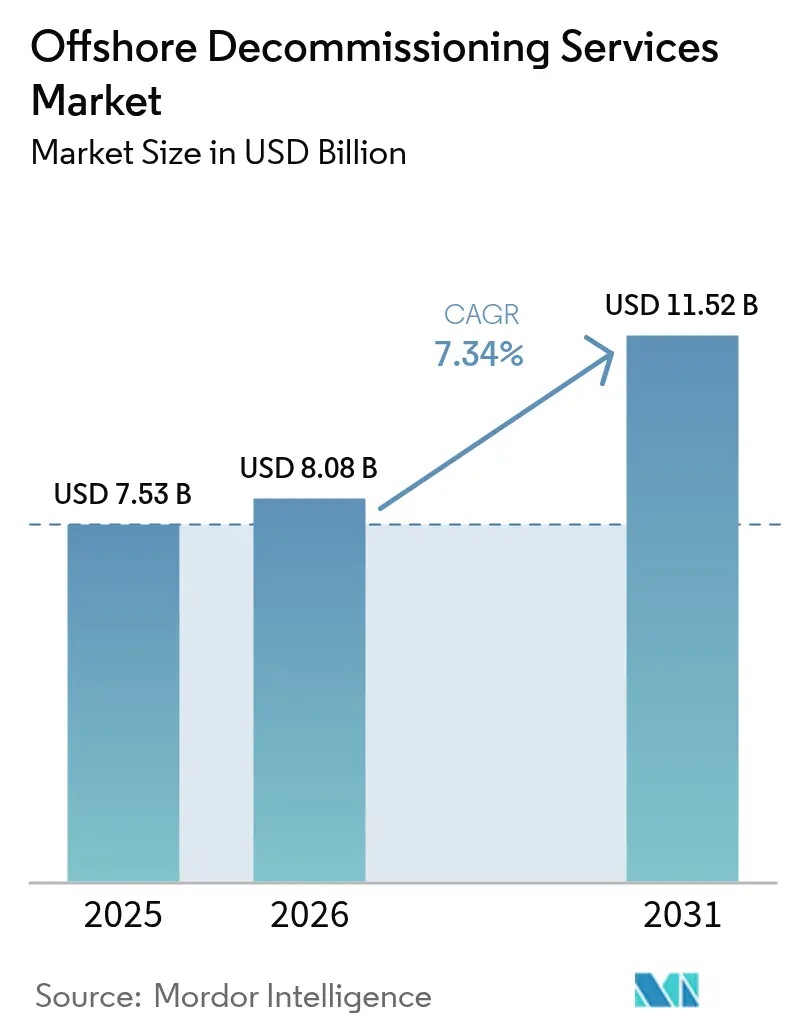

The Offshore Decommissioning Services market size is expected to grow from USD 7.53 billion in 2025 to USD 8.08 billion in 2026 and is forecast to reach USD 11.52 billion by 2031 at 7.34% CAGR over 2026-2031.

The steady retirement of aging platforms in the Gulf of Mexico (GoM) and the North Sea, along with tighter financial assurance regulations and rapid technological upgrades, collectively propel the offshore decommissioning services market. Operators are accelerating well-plugging and abandonment (P&A) programs to comply with the Bureau of Ocean Energy Management’s USD 6.9 billion bonding rule, while European producers face similar scrutiny from the North Sea Transition Authority. Cost-saving breakthroughs in robotic cutting, efficient heavy-lift vessel scheduling, and scrap steel recovery have eased historical cost barriers; yet, vessel and crew bottlenecks persist as offshore wind rebounds. Competitive dynamics are shifting toward scale: the 2025 Saipem–Subsea7 merger created a EUR 43 billion backlog champion capable of bidding for complex, multi-year campaigns.

Key Report Takeaways

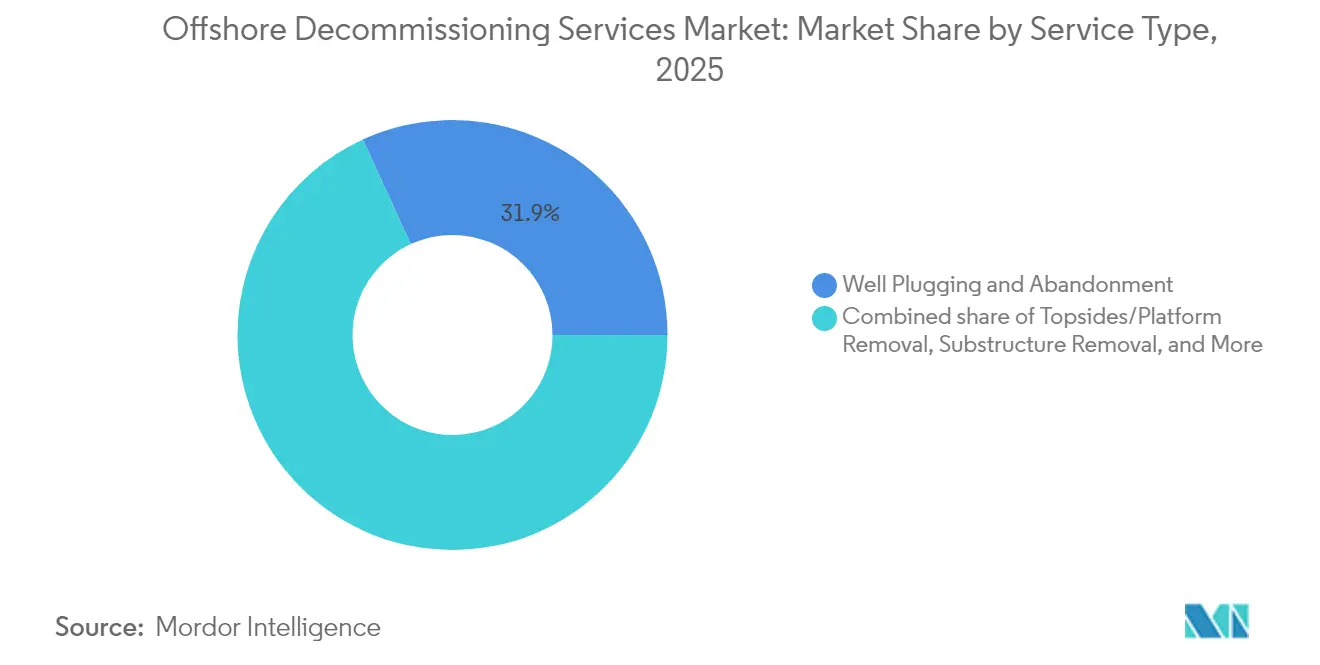

- By service type, well P&A captured 31.85% of the offshore decommissioning services market share in 2025. Topsides and platform removal is projected to expand at an 8.39% CAGR through 2031.

- By water depth, shallow-water projects accounted for 72.95% of the offshore decommissioning services market size in 2025, while ultra-deepwater work is advancing at an 8.18% CAGR.

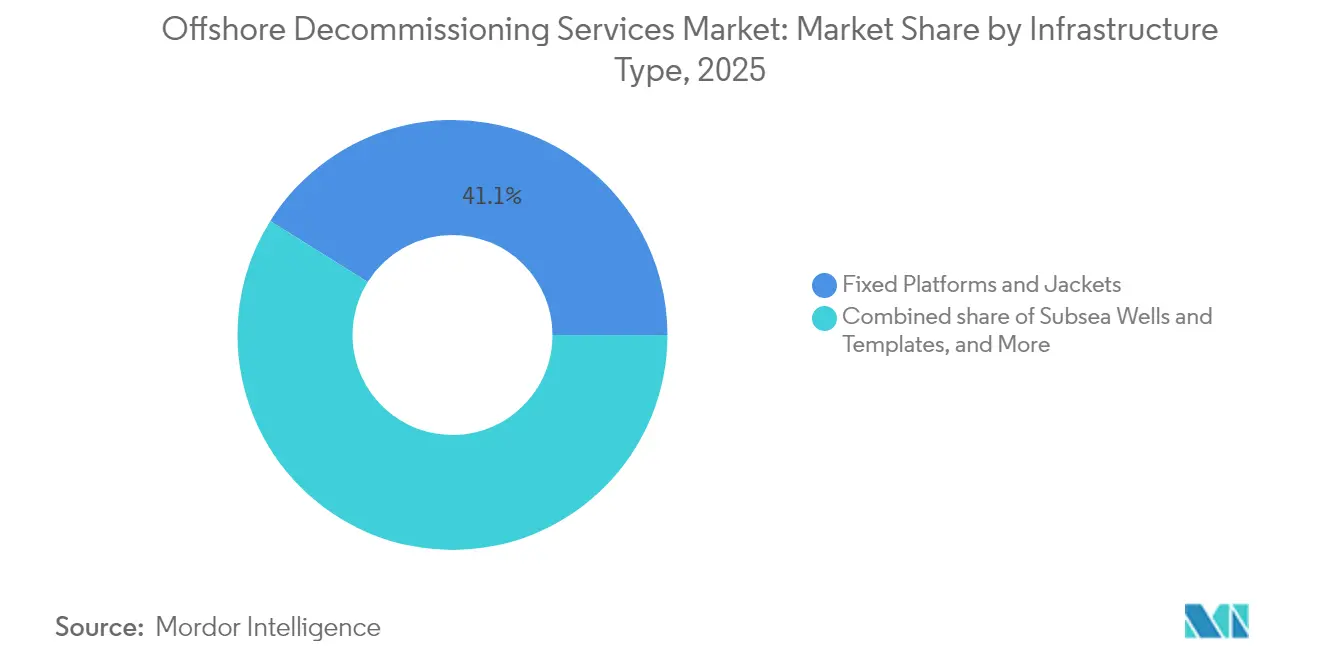

- By infrastructure type, fixed platforms and jackets commanded 41.10% of spending in 2025; subsea wells and templates represent the fastest-growing segment at an 8.78% CAGR.

- North America led with a 34.55% revenue share in 2025, whereas Europe is projected to achieve a 9.54% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Offshore Decommissioning Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates accelerating asset retirement | +2.1% | Global, primarily North America & Europe | Medium term (2-4 years) |

| Ageing North Sea & GoM infrastructure | +1.8% | North America & Europe | Long term (≥ 4 years) |

| Investor-driven P&A liability disclosures | +1.2% | Global | Short term (≤ 2 years) |

| Heavy-lift vessel over-supply after wind FID slowdown | +0.9% | Europe & Asia-Pacific | Short term (≤ 2 years) |

| Robotics and cold-cutting innovations | +0.7% | Global | Medium term (2-4 years) |

| Circular-economy revenues from scrap and reefing | +0.5% | North America & Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Leading Regulatory Mandates Accelerating Asset Retirement

Global regulators have tightened the rules that determine when and how operators must retire end-of-life infrastructure. In April 2024, the BOEM introduced a USD 6.9 billion financial assurance rule, compelling GoM leaseholders to post bonds or execute decommissioning programs within a three-year window. The measure addresses a backlog of more than 2,700 wells and 500 platforms identified as overdue. In Europe, the North Sea Transition Authority has issued schedules that penalize operators for slippage, signalling that deferral is no longer tolerated. Australia’s 2025 Offshore Resources Decommissioning Roadmap mirrors this stance, confirming that strengthened oversight is a worldwide phenomenon. Collectively, these actions pull forward spending, driving near-term growth in the offshore decommissioning services market. Operators now prefer early abandonment to avoid escalating bonding costs, improving backlog visibility for contractors.

Ageing North Sea & GoM Infrastructure Reaching Cessation-of-Production

Many fixed platforms installed before 1990 now operate at marginal rates of less than 10% of their original nameplate capacity. Shell’s retirement of the Brent Charlie platform, a single-lift extraction of 31,000 tonnes, underscored the technical scale awaiting contractors(1)Institution of Civil Engineers, “Brent Field Oil Rig Decommissioning,” ice.org.uk . In the GoM, more than 3,000 structures face similar economics, while 1,350 installations remain active in the North Sea. Depletion alongside low commodity price scenarios undermines the case for enhanced recovery, firmly tilting decisions toward abandonment. Concentration of assets in water depths below 125 m allows fleet and crew standardization, shaving mobilization costs, and accelerating project pipelines. This structural ageing profile sustains a long-duration demand stream that anchors the offshore decommissioning services market.

Increasing P&A Liability Disclosures Demanded by Investors

Institutional investors now evaluate upstream portfolios through the lens of undiscounted decommissioning liabilities. NEO Energy built its 2025 merger with Repsol’s UK assets around a dedicated USD 1.8 billion liability funding structure. Credit-rating agencies incorporate coverage ratios into scoring models, prompting operators to restate provisions upwards by up to 50%. ESG mandates require clear road maps to liability reduction; activist shareholders press companies to convert provisions into executed work scopes rather than rolling extensions. This transparency imperative aligns corporate finance with decommissioning schedules, stimulating predictable contracting opportunities and reinforcing growth prospects for the offshore decommissioning services market.

Robotics & Cold-Cutting Tech Slashing Topside Removal Time

Automation has transformed cutting and inspection workflows. Baker Hughes’ Terminator system removes wellheads in 35 minutes, compared to several hours via legacy mechanical methods, delivering 300% productivity gains(2)Baker Hughes, “Plug and Abandonment Services,” bakerhughes.com . DeepOcean’s autonomous drone verified subsea cuts at 3,000 m, halving inspection cycles. Cold cutting eliminates the need for explosives, improves worker safety, and yields cleaner steel for recycling. AI-enabled path planning optimizes blade contact angles, reducing tool wear and vessel spread downtime. The rapid adoption of these systems enhances competitiveness and further expands the addressable offshore decommissioning services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost uncertainty & funding shortfalls | −1.4% | Global | Medium term (2-4 years) |

| Frequent schedule slippage due to weather windows | −0.8% | North Sea & North America | Short term (≤ 2 years) |

| OSV & crew bottlenecks as offshore wind surges | −1.1% | Europe & Asia-Pacific | Medium term (2-4 years) |

| Asset repurposing for CCS delaying full removals | −0.6% | North Sea & GoM | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost Uncertainty & Funding Shortfalls

Deepwater well abandonment costs have risen to USD 24 million per well in parts of the GoM, a five-fold premium over shallow-water analogues. Inflation in steel-cutting consumables, mobilization fuel, and specialized crew wages pushed some projects 30–40% above early engineering estimates. Smaller independent companies lack access to project finance, forcing deferrals that swell their backlog. Bonding requirements have tightened just as credit conditions harden, intensifying pressure. These factors reduce near-term execution velocity and temper upside for the offshore decommissioning services market.

OSV & Crew Bottlenecks as Offshore Wind Surges

Norway estimates that 3,000 offshore personnel will retire by 2028, while the average workforce age is already 44.4 years. Crews migrate toward wind projects offering multi-year tenure and higher wages. Helix Energy’s 300-day Hornsea 3 trenching award demonstrates how single renewables contracts can block significant vessel capacity(3)Helix Energy Solutions Group, “Helix Robotics Solutions Trenching Contract,” helixesg.com . As wind FIDs resume after 2026, capacity strain is likely to return, restraining the growth momentum for the offshore decommissioning services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Well P&A’s Fundamental Scale Supports Growth

Well plugging and abandonment represented 31.85% of 2025 spend, anchoring the offshore decommissioning services market size, owing to the 27,000-plus wells awaiting permanent isolation in the GoM alone. The cost per shallow-water well ranges from USD 2 to USD 5 million, but deepwater P&A regularly exceeds USD 24 million, explaining the significant dollar allocation to this segment. Petrobras’ USD 170 million P&A framework with Constellation, covering 1,143 days of rig time, illustrates contractual scale. Topsides and platform removal is forecast as the fastest-expanding sub-sector at 8.39% CAGR. Single-lift campaigns, utilizing vessels such as Allseas’ Pioneering Spirit, reduce offshore exposure hours and lower project risk, thereby supporting uptake.

Pipeline and subsea-system decommissioning is gaining share as mature deepwater fields retire. The offshore decommissioning services market benefits from AI-driven toolpath optimization, which reduces cut cycles and supports safer multi-string pipeline severance. Site clearance and monitoring, though smaller, show rising growth because regulators mandate multi-year post-removal seabed surveys. Substructure removal, particularly jackets in water depths of 60-150 m, remains cost-intensive; however, it is increasingly executed through reverse-installation methods that shorten lift durations.

By Water Depth: Shallow-Water Dominance Meets Ultra-Deepwater Upside

In 2025, shallow-water projects below 125 m captured 72.95% of spending, bolstered by decades-old North Sea and GoM infrastructure and the availability of lower-cost lift spreads. Shallow work scopes enable campaign-style scheduling, maximizing vessel utilization and allowing for economies of scale across neighboring leases. Ultra-deepwater projects above 1,500 m record the strongest 8.18% CAGR. Wild Well’s DeepRange 10,000 ft-rated intervention system confirms the technology readiness for such depths. Operator budgets factor high-spec rig day rates of up to USD 500,000, translating into large contract values that expand the offshore decommissioning services market size.

Deepwater assets (125–1,500 m) occupy a middle ground; they require enhanced equipment but avoid the extreme pressures of ultra-deepwater. Weather exposure intensifies with depth as operations extend longer per well, and spread costs outperform shallow baselines by three to five times. Contractors with deepwater ROV fleets and DP3 vessels, such as TechnipFMC and Saipem, enjoy a clear advantage in this growth pocket of the offshore decommissioning services market.

By Infrastructure Type: Fixed Platforms Remain High-Value Work Scopes

Fixed platforms and jackets accounted for 41.10% of the 2025 decommissioning value, reflecting heavy steel tonnage and robust lift requirements. Single-lift removals, such as Brent Charlie, have proven viable, but multi-lift segmenting remains prevalent for smaller barges. Subsea wells and templates deliver the fastest 8.78% CAGR, supported by a wave of pre-2008 deepwater tiebacks now at the end of their life. These jobs rely on advanced ROV tooling that can detach connector frames in low-visibility, high-pressure environments, further professionalizing the offshore decommissioning services market.

Floating production systems, including FPSOs and spars, represent both removal opportunities and refurbishment prospects. Some owners evaluate redeployment to marginal fields. Pipeline and flowline scopes require fit-for-purpose trencher spreads; decisions on removal versus in-situ abandonment hinge on risk assessments and host-nation rules. The offshore decommissioning services market adapts by offering integrated engineering that compares environmental, safety, and cost outcomes before final work-scope definition.

Geography Analysis

North America retained 34.55% of 2025 revenue. The BOEM bonding rule accelerated GoM contract awards and established logistics hubs in Port Fourchon and Ingleside, enabling rapid mobilization. Mexico’s legacy Cantarell infrastructure adds incremental demand as Pemex programs early P&A on non-commercial wells. Canada’s Atlantic offshore assets are fewer, but they draw attention for the risk of iceberg mitigation during decommissioning. Together, these dynamics maintain regional primacy for the offshore decommissioning services market.

Europe is the fastest-growing region at a 9.54% CAGR. The UK’s projected GBP 59.7 billion spend through 2050 anchors activity, while Norway’s mature Ekofisk and Frigg fields continue to retire assets. Continental Europe contributes to pipeline removals in the Dutch and Danish sectors. The North Sea’s clustered asset layout favors multi-field campaign approaches, unlocking cost savings and elevating the offshore decommissioning services market share captured by integrated contractors.

Asia-Pacific offers mixed opportunities. Malaysia’s 200-plus idle wells, Australia’s Bass Strait platform retirements, and Thailand’s rapid multi-platform program executed by James Fisher exhibit early momentum. Regulatory heterogeneity complicates scheduling, yet government grants for local content spur joint-venture models. Ultra-deepwater abandonment off Western Australia’s Carnarvon Basin is pushing drilling-rig demand and raising technical benchmarks inside the offshore decommissioning services market.

Brazil leads South America. Petrobras alone intends to decommission 26 platforms and 18 gas lift manifolds by 2030, highlighted by the USD 170 million P&A contract awarded in 2025. Colombia and Trinidad plan smaller campaigns that favor regional contractors. The Middle East and Africa present nascent potential: mature Egyptian platforms in the Gulf of Suez and shallow-water Nigerian infrastructure are nearing the end of their lifespan, but many host governments are still refining their guidelines. As clarity improves, these theatres will enlarge the global offshore decommissioning services market footprint.

Competitive Landscape

The offshore decommissioning services market displays moderate fragmentation. Tier-one EPC and marine heavy-lift specialists—including Allseas, Heerema, TechnipFMC, and the merged Saipem-Subsea7 entity—dominate turnkey campaigns that require integrated lift, subsea, and P&A competency. Mid-cap specialists, such as Acteon and DeepOcean, compete through differentiated tooling or regional expertise.

Consolidation escalated in 2025 when Saipem and Subsea7 combined to form a EUR 20 billion revenue leader with a EUR 43 billion backlog, enhancing scale synergy for multi-basin programs. SLB’s acquisition of ChampionX augments production-chemistry and intervention know-how, enabling bundled P&A and late-life production optimization services(5)SLB, “SLB Completes Acquisition of ChampionX,” slb.com . TechnipFMC secured a large iEPCI award for Johan Sverdrup Phase 3, reinforcing its ability to cross-sell decommissioning solutions alongside greenfield developments.

Technology is a key differentiator. Baker Hughes’ Terminator system accelerates wellhead removal, while Helix Robotics deploys trenchers and ROVs that shorten pipeline burial timelines. Autonomous drones for subsea metrology reduce human exposure and widen operational windows. Carbon-capture repurposing opens new revenue avenues that may offset the costs of removals; Aker Solutions has positioned itself for this pivot through CCS project awards.

Pricing power rests with owners of ultra-heavy-lift assets capable of lifting 20,000 tonnes in a single lift. Competition in shallow-water scopes remains intense, pressuring margins; however, contractors offering bundled engineering, regulatory interface, and cost-certainty continue to secure repeat business. Overall, legacy fleet ownership, digital toolset, and balance-sheet strength determine success in the offshore decommissioning services market.

Offshore Decommissioning Services Industry Leaders

Aker Solutions ASA

Petrofac Ltd

TechnipFMC PLC

Heerema Marine Contractors

Allseas Group SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SLB completed its acquisition of ChampionX, targeting USD 400 million annual pretax synergies within three years.

- April 2025: Subsea7 landed a sizeable decommissioning award for Shell’s Sparta development in the GoM.

- February 2025: Subsea7 secured a USD 150–300 million pipeline decommissioning award from Saudi Aramco.

- February 2025: Valaris retired three semisubmersibles and sold jack-up Valaris 75 for USD 24 million, while landing extensions worth over USD 75 million.

- January 2025: Aker Solutions was named the preferred supplier for a CCS project, signaling diversification into repurposing opportunities.

Global Offshore Decommissioning Services Market Report Scope

The offshore decommissioning services market report include:

| Well Plugging and Abandonment |

| Topsides/Platform Removal |

| Substructure (Jacket) Removal |

| Pipeline and Subsea Infrastructure Decommissioning |

| Site Clearance and Monitoring |

| Shallow Water (Below 125 m) |

| Deepwater (125 to 1,500 m) |

| Ultra-Deepwater (Above 1,500 m) |

| Fixed Platforms and Jackets |

| Floating Production Systems (FPSO, TLP, Spar) |

| Subsea Wells and Templates |

| Pipelines and Flowlines |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germnay |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Type | Well Plugging and Abandonment | |

| Topsides/Platform Removal | ||

| Substructure (Jacket) Removal | ||

| Pipeline and Subsea Infrastructure Decommissioning | ||

| Site Clearance and Monitoring | ||

| By Water Depth | Shallow Water (Below 125 m) | |

| Deepwater (125 to 1,500 m) | ||

| Ultra-Deepwater (Above 1,500 m) | ||

| By Infrastructure Type | Fixed Platforms and Jackets | |

| Floating Production Systems (FPSO, TLP, Spar) | ||

| Subsea Wells and Templates | ||

| Pipelines and Flowlines | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germnay | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the offshore decommissioning services market?

The offshore decommissioning services market size was USD 8.08 billion in 2026 and is projected to grow to USD 11.52 billion by 2031.

Which service segment dominates spending?

Well plugging and abandonment dominates with 31.85% share in 2025 because every asset retirement requires permanent well isolation before other activities can start.

Why is Europe the fastest-growing regional market?

Europe’s 9.54% CAGR reflects North Sea regulators tightening enforcement, pushing operators to accelerate retirements and generating a sizeable pipeline of platform and subsea removals.

How do new technologies lower decommissioning costs?

Robotic cold-cutting, autonomous inspection drones and single-lift vessels cut operational hours, reduce safety risks and unlock 15–30% cost savings compared with conventional methods.

What is the biggest restraint on market growth?

High cost uncertainty—especially in deepwater projects where well abandonment can exceed USD 24 million per well—creates funding gaps and delays execution schedules.

Will CCS repurposing reduce decommissioning activity?

In the near term, pipeline and platform conversion for carbon storage can defer certain removals, but overall industry forecasts still anticipate rising decommissioning demand as assets age.

Page last updated on: