Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 19.49 Billion |

| Market Size (2026) | USD 19.92 Billion |

| Market Size (2031) | USD 22.21 Billion |

| Growth Rate (2026 - 2031) | 2.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Metal Cans Market Analysis by Mordor Intelligence

The Europe metal cans market size was valued at USD 19.49 billion in 2025 and estimated to grow from USD 19.92 billion in 2026 to reach USD 22.21 billion by 2031, at a CAGR of 2.20% during the forecast period (2026-2031). This steady climb reflects a mature yet resilient landscape in which stringent circular-economy rules, high recycling rates for aluminum and steel, and brand owner decarbonization targets jointly reinforce demand for infinitely recyclable packaging. Deposit-return systems that routinely exceed 90% collection rates, Germany’s upcoming 98% benchmark among them, underpin a dependable secondary raw-material loop that stabilizes supply. Ongoing PET-to-can conversion by craft brewers and premium ready-to-drink cocktail brands, together with e-commerce-driven aerosol demand, broadens the addressable volume base while expanding value per unit. Meanwhile, green-steel deployment and aluminum down-gauging temper emissions footprints and enable compliance with the European Commission’s requirement that all packaging be recyclable by 2030.[1]European Commission, “New Rules for a Sustainable Packaging Economy,” europa.eu Taken together, these forces keep the European metal cans market on a measured growth path despite raw-material cost volatility and substrate substitution risks.

Key Report Takeaways

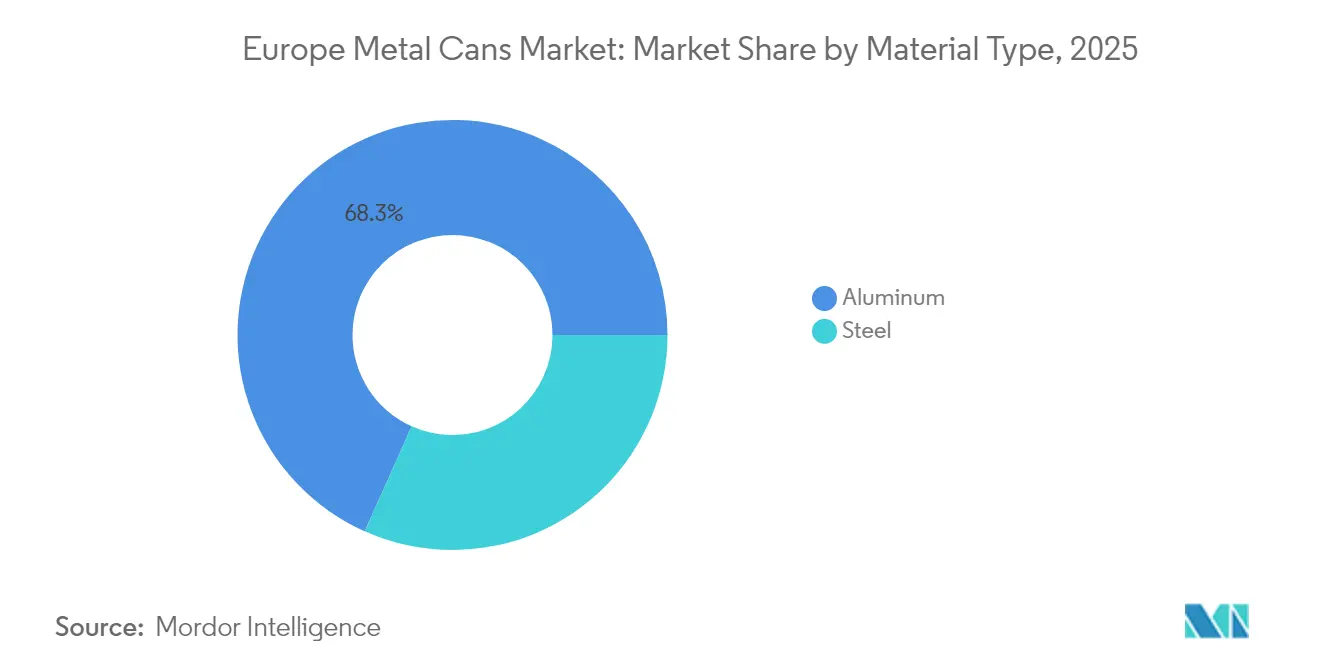

- By material type, aluminum captured 68.31% of the Europe metal cans market share in 2025.

- By end-user, the Europe metal cans market size for food is projected to grow at a 3.68% CAGR between 2026-2031.

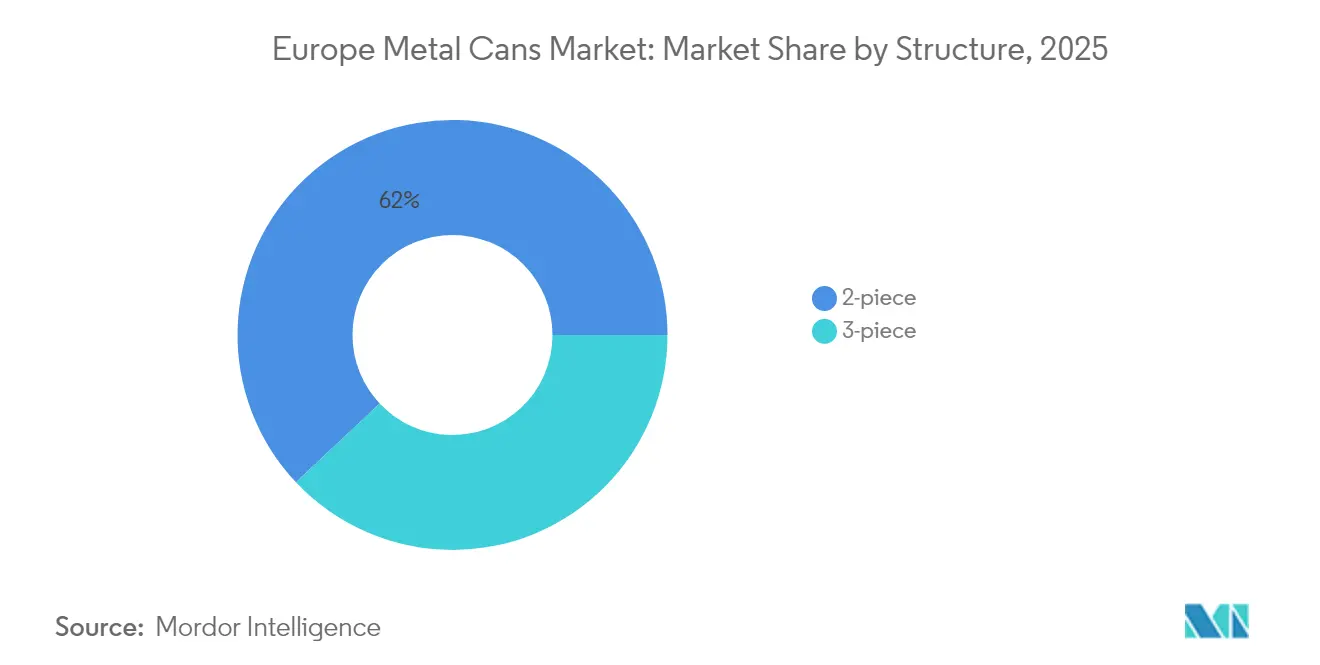

- By structure, 2-piece captured 62.02% of the Europe metal cans market size in 2025.

- By capacity, the Europe metal cans market size for up to 250 ml is projected to grow at a 3.44% CAGR between 2026-2031.

- By country, Germany captured 21.91% of the Europe metal cans market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Metal Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High recyclability rates of metal packaging | +0.4% | EU-27, UK, Switzerland, Norway | Medium term (2–4 years) |

| EU circular-economy regulations tightening in 2025–30 | +0.3% | EU-27 core, spillover to UK | Long term (≥ 4 years) |

| PET-to-can conversion by craft brewers and RTD cocktails | +0.2% | Germany, UK, France, Netherlands | Short term (≤ 2 years) |

| Steelmakers’ low-carbon alloy launches cut Scope 3 emissions | +0.2% | Germany, France, Italy, Spain | Medium term (2–4 years) |

| Deposit-return-scheme harmonization across EU-27 | +0.3% | EU-27, early gains in France, Austria | Medium term (2–4 years) |

| Aerosol can growth in e-commerce home-care refills | +0.1% | Germany, UK, France, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High recyclability rates of metal packaging

Europe’s 76% aluminum beverage-can recycling rate and 80.5% steel-pack recovery underscore an unmatched circular advantage that resonates with carbon-conscious consumers and regulators alike. The European Aluminium Packaging Group’s push to reach 100% recycled content for can ends lowers life-cycle emissions by up to 95%, creating a strong value proposition for brand owners seeking quick carbon wins. Robust deposit-return systems, Germany already collects 98% of cans—ensuring a steady feedstock that cushions against primary-metal price swings. As the European Commission targets a 23.2% circular-material-use rate by 2030, metal’s infinite recycling loop positions the Europe metal cans market ahead of plastic and glass substitutes.[2]European Environment Agency, “Circular Material Use Rate,” eea.europa.eu Producer-responsibility fees linked to recycled content further tilt cost structures in favor of metal, reinforcing long-term demand.

EU circular-economy regulations tightening in 2025–30

The Packaging and Packaging Waste Regulation that took effect in February 2025 obliges every package to be “recyclable by design” by 2030 and imposes minimum recycled-content thresholds. Metal cans, being mono-material and already compliant, gain a clear competitive edge while multi-layer plastics face redesign costs and technical hurdles. Additional requirements to trim packaging waste 15% per capita by 2040 incentivize down-gauged aluminum and thin-wall steel formats, aligning material efficiency with compliance savings. Extended-producer-responsibility levies will be harmonized, ending today’s patchwork of fees and easing cross-border logistics. Standardized labeling rules favor the simple composition of cans, which consumers can sort easily, further enhancing collection rates and reinforcing the European metal cans market.

PET-to-can conversion by craft brewers and RTD cocktails

Premium RTD cocktails are forecast to reach USD 2.43 billion by 2030, propelling a shift toward aluminum cans that offer superior light protection and a large branding canvas. Craft breweries embrace cans for lower shipping weight and oxidation resistance, fueling 4-6% annual can volume gains in European beverage channels. Aluminum’s 82% recycling rate aligns with craft brands’ authenticity narratives, attracting environmentally minded consumers. Nitro-infused cocktails and low-alcohol variants leverage can geometrics to create creamy textures that bottles cannot replicate, adding functional differentiation. Single-serve convenience resonates with younger demographics and supports the growth of smaller 200–250 mL formats within the European metal cans market.

Steelmakers’ low-carbon alloy launches cut Scope 3 emissions

Hydrogen-based direct-reduced iron and electric-arc furnaces could deliver up to 172 Mt of green steel capacity in Europe by 2030, slashing embedded carbon in steel cans. Although current production carries a 20–60% cost premium, rising EU carbon prices and green-procurement rules are narrowing the gap. Automotive willingness to pay EUR 57 extra per vehicle for clean steel signals brand acceptance of modest premiums, a mindset that is migrating to packaging. Closed-loop recycling programs that return used steel cans to mills within 60 days augment supply security and reinforce circular objectives. As these alloys proliferate, steel gains relevance in food and aerosol niches, lifting overall segment attractiveness inside the European metal cans market.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of tethered-cap aluminum bottles | -0.3% | EU-27, early adoption in Germany, Netherlands | Short term (≤ 2 years) |

| Volatility in European rolled-aluminum premiums | -0.2% | Germany, France, Italy, Spain | Medium term (2–4 years) |

| Brand owner down-gauging hitting mill utilization rates | -0.1% | Germany, UK, France, Netherlands | Medium term (2–4 years) |

| PFAS phase-out costs for epoxy can linings | -0.1% | EU-27, UK, Switzerland, Norway | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of tethered-cap aluminum bottles

The EU Single-Use Plastics Directive now requires beverage closures to stay attached, accelerating the appeal of re-sealable aluminum bottles that natively comply while distinguishing themselves from conventional cans. Coca-Cola and PepsiCo rolled out more than 400 million tethered closures in Europe by mid-2025, habituating consumers to the new ergonomics. Because bottles enable on-the-go re-closure, they siphon volume from single-serve cans in flavored water and energy-drink niches. Premium perception of slender bottle silhouettes reinforces this drift, challenging can fill-lines geared for traditional formats. Although both packages recycle well, the functional edge of bottles subtracts incremental growth from the Europe metal cans market in the near term.

Volatility in European rolled-aluminum premiums

Average 2025 European rolled-aluminum premiums near USD 2,575 per tonne, inflated by U.S. tariffs and sanctions on Russian supply, compress converter margins. European smelters cover only 11% of regional demand, exposing can makers to imported-ingot price swings. German output shrank 7% in Q1 2024, and recycled-aluminum production fell 6%, widening the supply gap. Energy-price turbulence and currency shifts amplify volatility, complicating long-term contract negotiations with fillers. While hedging mitigates some risk, sustained unpredictability tempers investment appetite, marginally dragging the CAGR for the Europe metal cans market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum leadership sustained as green steel gathers pace

Aluminum captured 68.31% of 2025 revenue thanks to its low weight, corrosion resistance, and entrenched beverage relationships, while steel is on course for a 3.11% CAGR to 2031 as hydrogen-based alloys broaden its sustainability credentials. Ball Corporation shipped 36 billion aluminum containers in EMEA during 2024, equal to a 39% share of regional can volumes, underscoring aluminum’s scale economics. In value terms, aluminum remains the linchpin of the European metal cans market; yet steel’s renaissance, powered by anticipated 172 Mt of green capacity, is widening the material choice for food and aerosol fillers looking to cut Scope 3 emissions.

Steel’s closer coupling with electric-arc furnaces slashes energy use by 30% and permits full circularity through magnetic separation, making “can-to-can in 60 days” a realistic slogan. Simultaneously, the European Aluminium Packaging Group targets 100% recycled content, reinforcing metal’s infinite recyclability narrative. Cross-material competition spurs innovation: aluminum down-gauging and easy-open ends meet steel’s improved formability and lacquer compatibility. Both substrates thus consolidate the European metal cans market by offering distinct performance ladders that satisfy diverging end-use needs.

By End-User: Beverage weight still dominant; food races ahead on innovation

Beverages retained 46.85% of 2025 turnover, propelled by craft brewing, energy drinks, and RTD cocktail momentum, whereas food cans are expected to chart a 3.68% CAGR through 2031. Europe drinks close to 93 billion canned servings yearly, anchoring filler demand for high-speed 2-piece aluminum lines that underpin the Europe metal cans market size. Crown Holdings saw beverage-can income climb 62% in 2024 on stronger contract terms and value-added ends, confirming sustained profitability.

Food cans, long criticized for dated aesthetics, are rejuvenating via glossy lithography, peel-foil membranes, and reseal features that lift shelf appeal. Their five-year shelf life combats food waste, a priority as the EU targets a 50% cut by 2030. Pet food’s switch to metal for nutrient retention and premium grain-free lines magnifies volume. Combined, these forces inject growth into a traditionally slower segment, balancing portfolio reliance that historically skewed toward beverages within the European metal cans market.

By Structure: Two-piece efficiency versus three-piece adaptability

Two-piece cans held 62.02% of 2025 output on the back of draw-and-wall-iron manufacturing speed, yet three-piece variants are tracking a 3.49% CAGR to 2031 owing to aerosol and specialty food appeal. One plant can crank out 2,000 two-piece bodies a minute, ideal for soft-drink economics. Conversely, three-piece bodies accept welded side seams and domed ends, suited to viscous foods or pressurized contents. Ball’s EUR 82 million Alucan acquisition expands its footprint in extruded aluminum aerosol technology, a signal that three-piece niches will command more strategic focus.

Resource conservation drives advances in both formats. Tata Steel Nederland’s newly commissioned food-can line maximizes material utilization while lifting output flexibility. Down-gauging mostly favors two-piece cans where wall thickness uniformity can be shaved without seam issues, but internal-lacquer upgrades benefit three-piece formats prone to weld stress. These technical nuances let fillers precisely match product needs, ensuring both structures remain pillars of the European metal cans market.

By Capacity: Mid-range formats rule; small serves gain traction

The mainstream 251–500 mL band delivered 46.05% share in 2025, reflecting European preferences for 330 mL beer and 500 mL soft drink sizes, yet sub-250 mL cans are poised for the fastest 3.44% CAGR through 2031. Single-serve indulgence aligns with premium cocktails and functional beverages, letting brands charge a higher price-per-ounce while cutting calorie counts. Deposit-return economics also favor small sizes: a fixed EUR 0.25 deposit represents a bigger relative share of product price, motivating consumer returns and boosting recycling rates.

Larger family-size containers over 500 ml lose ground to PET multipacks and glass growlers that are enjoyed in-home sharing rituals. Equipment innovation, quick-change filling valves, and modular decorators now let converters switch between 150 mL sleek cans and 473 mL standards without extended downtime, reducing unit economics barriers. Capacity right-sizing thus broadens SKU repertoires and feeds the volume cadence of the European metal cans market.

Geography Analysis

Germany’s commanding 21.91% revenue share in 2025 stemmed from high-volume beverage production and unparalleled 98% deposit-return performance that secures a closed-loop material stream. Crown’s post-acquisition integration of Helvetia Packaging unlocked extra capacity, cementing the country’s leadership. Even as primary aluminum output dipped 7% in Q1 2024, abundant scrap inflows kept can-sheet supply uninterrupted, highlighting the strategic insulation afforded by circularity.

France is gaining momentum as the fastest-growing market in the European metal cans market. Rapid harmonization of deposit schemes lifted aluminum beverage-can collection above 90%, while eco-taxes on multi-layer plastics nudged fillers toward metal alternatives. Crown’s heat-recovery upgrade at Custines improved line economics, and craft brewers embraced sleek 250 mL cans to capture premium-price points, widening addressable demand.

Elsewhere, the UK, Spain, Italy, and Poland add depth. Novelis’ Latchford expansion guarantees domestic remelt capacity post-Brexit. Crown scaled new beverage-can lines in Spain and Italy, exploiting growing soft-drink consumption. Poland, buoyed by rising disposable income, absorbs extra can volumes, while the Netherlands’ 27.5% circular-material-use rate sets a benchmark for northern neighbors. Such geographic diversity cushions the Europe metal cans market against local shocks and fosters a pan-regional growth platform.

Competitive Landscape

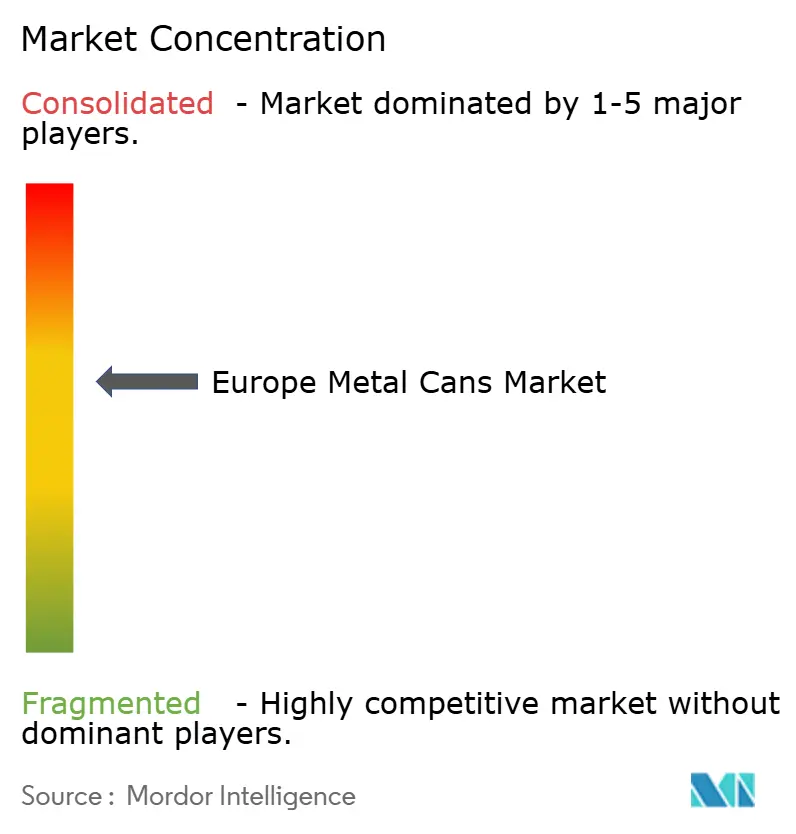

Three global suppliers, Ball, Crown, and the newly enlarged Sonoco-Eviosys platform, jointly control roughly 60% of Europe's volume, marking a moderately consolidated field. Sonoco’s EUR 3.615 billion takeover of Eviosys in December 2024 delivered 44 plants across 17 countries, promising USD 100 million capture in two years.

Ball’s 39% EMEA beverage hold is underpinned by 36 billion annual shipments and reinforced by the Alucan acquisition that expands aerosol and bottle competency in Spain and Belgium. Crown divested its European tinplate division yet posted a 62% income rise in 2024 as favorable price/mix offset lower tonnage. Technology rivalry centers on down-gauging; Neuman Aluminium’s Neucan 3.1 cuts thickness 17.2% while stitching 25% post-consumer scrap into coil, slashing CO₂ output 40%.

Coating innovators AkzoNobel and PPG accelerate PFAS-free roll-outs; more than 20% of European beverage volumes now use non-BPA systems. Emerging niche players exploit gaps in refill aerosols and decorative specialty cans, but capital intensity and stringent ISO 14855 testing limit rapid scale-up, conferring an advantage to established incumbents in the European metal cans market.

Europe Metal Cans Industry Leaders

Ball Corporation

Ardagh Group S.A.

Crown Holdings, Inc.

Silgan Holdings Inc

Can-Pack S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Ball Corporation reported Q2 2025 shipments up 4.1% globally, with EMEA operating earnings of USD 129 million on USD 1.05 billion sales.

- April 2025: Crown Holdings posted Q1 2025 diluted EPS of USD 1.65, versus USD 0.56 in 2024, and guided full-year EPS to USD 6.70–7.10.

- February 2025: The European Commission enforced the Packaging and Packaging Waste Regulation, mandating the recyclability of all packaging by 2030.

- January 2025: The EU banned Bisphenol A in food-contact materials, setting 18- to 36-month coating transition timelines.

Europe Metal Cans Market Report Scope

Metal can packaging consists of aluminum or steel containers designed to protect and preserve products, particularly food and beverages. These containers provide a durable, airtight, and lightproof barrier that prevents product deterioration from air, light, and moisture exposure. The packaging is commonly used for soft drinks, beer, energy drinks, canned foods, and cosmetic products. Metal cans offer advantages, including structural strength, transportation efficiency, and recyclability, making them an environmentally sustainable packaging solution.

The Europe metal cans market is segmented by material type (aluminum and steel), by type (food cans (vegetables, fruits, pet food, soups & condiments, and other food cans (baby food, dairy, fruit & vegetable juices, seafood, and meat and poultry cans)), beverage cans (alcoholic and non-alcoholic), aerosol cans (personal care and cosmetics, household and homecare, and other aerosol cans), and other cans), and by country (United Kingdom, Germany, France, Spain, Italy, Poland, and Rest of Europe). The market sizes and forecasts are provided in value (USD) for all the above segments.

By Material Type

| Aluminum |

| Steel |

By End-User

| Food | Vegetables |

| Fruits | |

| Pet Food | |

| Soups and Condiments | |

| Other Food Cans | |

| Beverage | Alcoholic |

| Non-Alcoholic | |

| Aerosol Cans | |

| Other End-users |

By Structure

| 2-piece |

| 3-piece |

By Capacity

| Up to 250 ml |

| 251 - 500 ml |

| More than 500 ml |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Poland |

| Rest of Europe |

| By Material Type | Aluminum | |

| Steel | ||

| By End-User | Food | Vegetables |

| Fruits | ||

| Pet Food | ||

| Soups and Condiments | ||

| Other Food Cans | ||

| Beverage | Alcoholic | |

| Non-Alcoholic | ||

| Aerosol Cans | ||

| Other End-users | ||

| By Structure | 2-piece | |

| 3-piece | ||

| By Capacity | Up to 250 ml | |

| 251 - 500 ml | ||

| More than 500 ml | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Poland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe metal cans market?

The market is valued at USD 19.92 billion in 2026 and is projected to reach USD 22.21 billion by 2031.

Which material dominates can production in Europe?

Aluminum leads with 68.31% 2025 revenue share thanks to lightweight, infinitely recyclable attributes.

Which end-use segment is growing fastest?

Food applications are forecast to rise at a 3.68% CAGR to 2031 as brands switch from PET and glass.

Why are deposit-return systems important to this market?

DRS programs secure more than 90% collection of used cans, feeding a closed-loop recycling stream that stabilizes raw-material supply.

How will EU regulations affect packaging choices?

The Packaging and Packaging Waste Regulation requires all packaging to be recyclable by 2030, favoring mono-material metal cans over composite alternatives.

What technological shift is shaping the future of steel cans?

Hydrogen-based green steel and electric-arc furnaces are cutting energy and carbon, making steel cans more attractive for low-emission supply chains.

Page last updated on: