Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 88.45 Billion |

| Market Size (2031) | USD 105.06 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

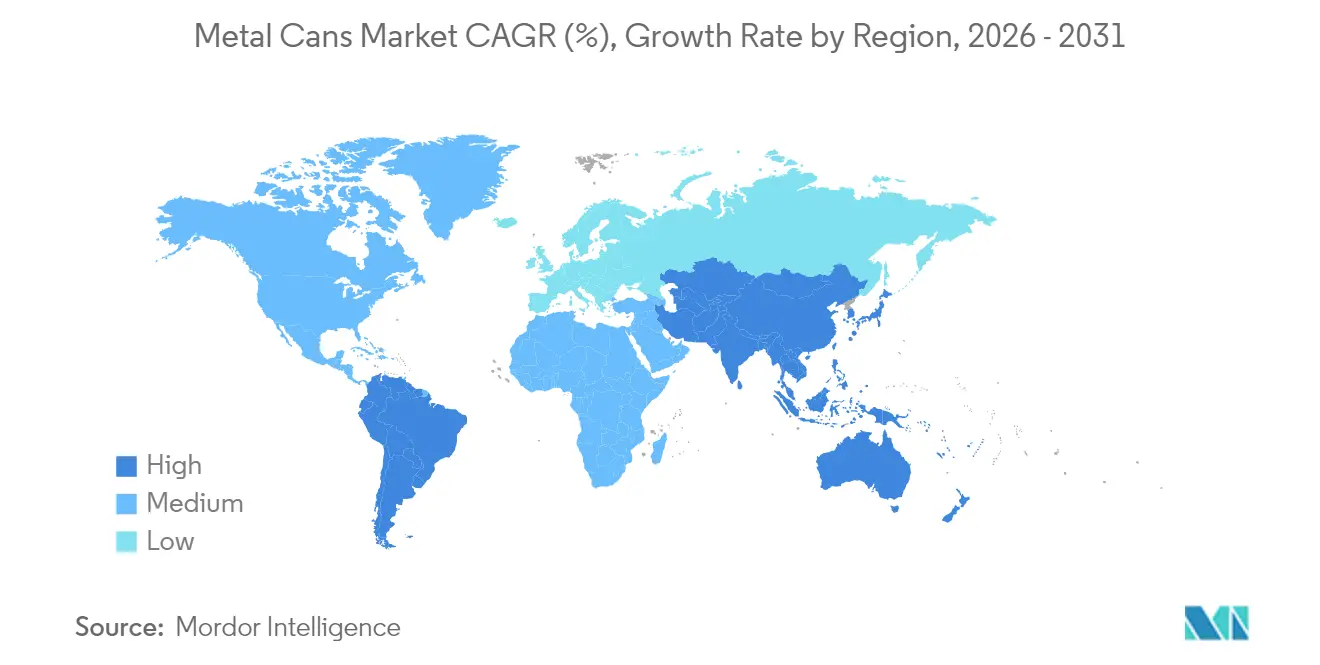

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

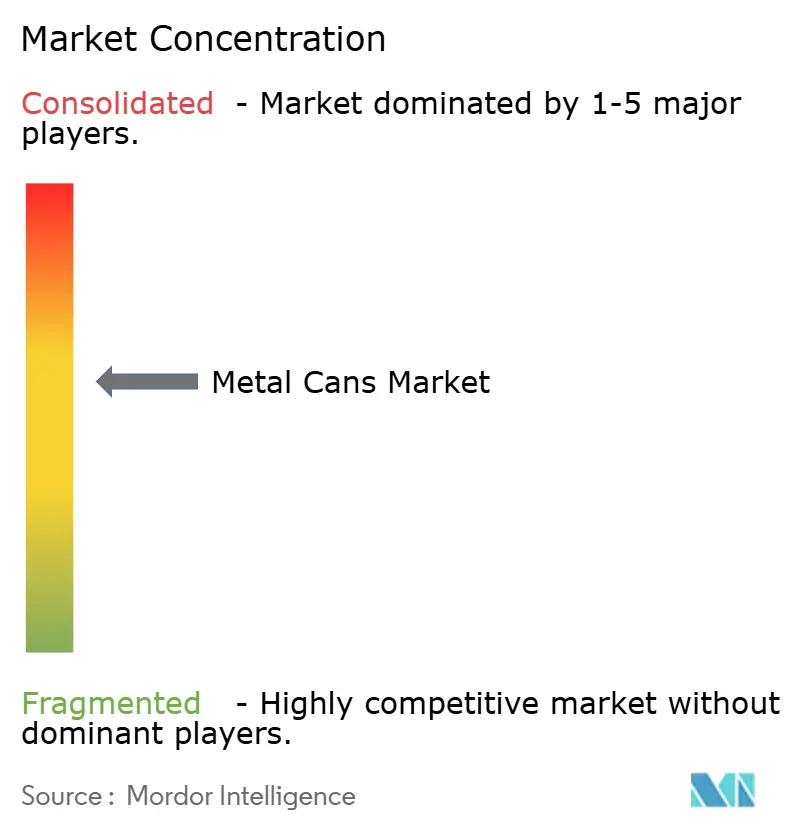

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Cans Market Analysis by Mordor Intelligence

The global metal cans market size in 2026 is estimated at USD 88.45 billion, growing from 2025 value of USD 85.44 billion with 2031 projections showing USD 105.06 billion, growing at 3.52% CAGR over 2026-2031. Current expansion reflects the shift from conventional packaging toward recyclable, circular-economy solutions. Aluminum maintains a pivotal position because it can be recycled indefinitely without degrading, and national recycling programs are rapidly scaling collection infrastructure-Japan’s 2024 aluminum can recovery rate surpassed 93%. Lightweighting technologies such as Ball Corporation’s ReAl Gen 2 alloy, introduced in 2024, are trimming material use by up to 15% and helping brand owners contain cost volatility tied to primary aluminum pricing. At the same time, deposit-return systems and extended producer-responsibility programs in Europe, North America, and parts of Asia are internalizing environmental costs, reinforcing the value proposition of the metal cans market. The beverage sector remains the cornerstone end user, yet pharmaceutical demand is gathering pace on the back of tamper-evident requirements and track-and-trace mandates, underpinning the metal cans market’s multi-segment resilience.

Key Report Takeaways

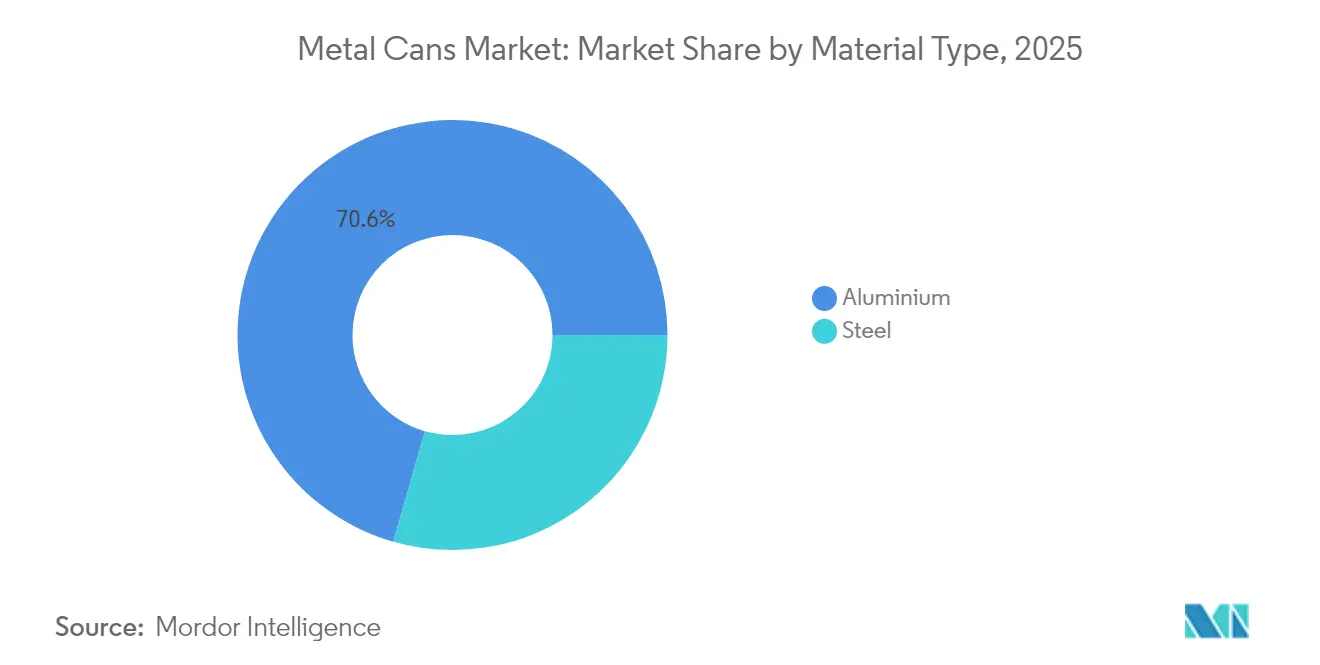

- By material type, aluminum commanded 70.56% of metal cans market share in 2025, while steel registered slower expansion despite niche retention in certain food categories.

- By can structure, two-piece formats led with 54.06% revenue share in 2025; monobloc aerosol cans posted the fastest 4.78% CAGR through 2031.

- By capacity, the 250-500 ml range accounted for 30.18% of the metal cans market size in 2025; ≤250 ml cans are on track for a 4.88% CAGR.

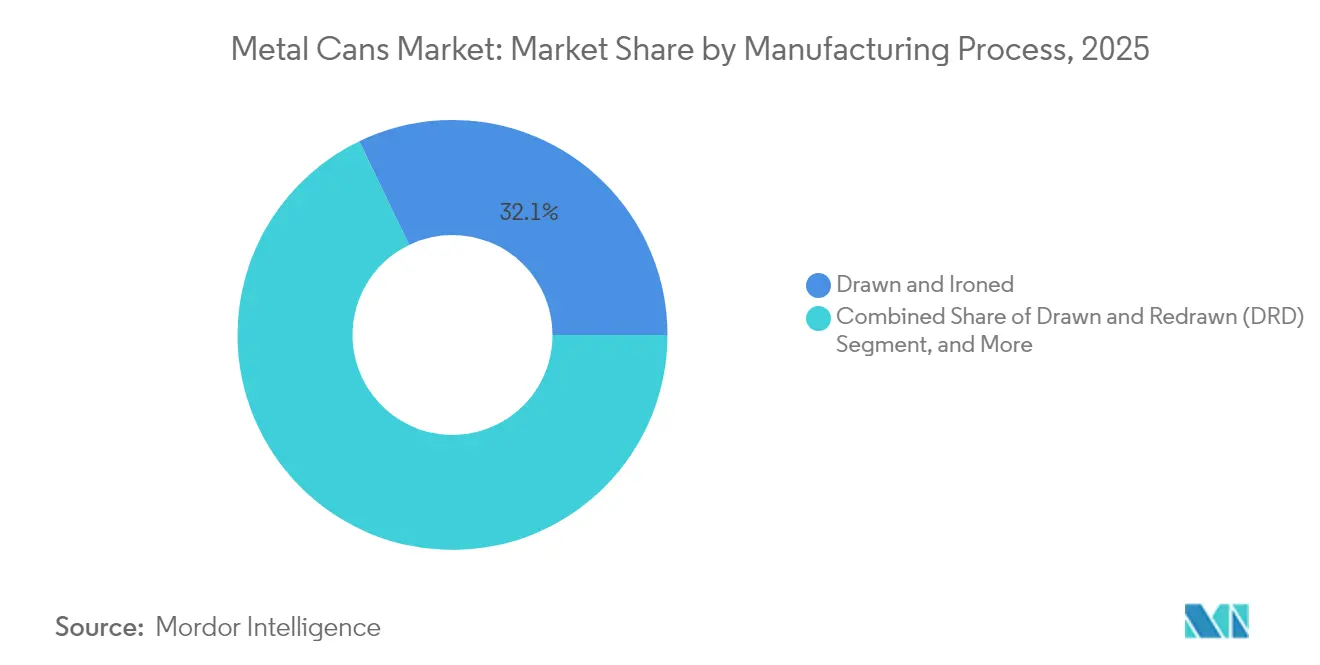

- By manufacturing process, drawn-and-ironed cans held 32.14% of the metal cans market size in 2025, whereas impact extrusion is accelerating at a 4.74% CAGR.

- By end-user industry, beverages contributed 38.01% of the metal cans market share in 2025; pharmaceuticals are advancing at a 4.95% CAGR to 2031.

- By geography, North America led with 39.72% revenue share in 2025; Asia-Pacific is projected to expand at a 5.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metal Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum price volatility accelerates lightweighting adoption | +0.8% | North America and Europe (global spillover) | Medium term (2-4 years) |

| Global DRS programs expanding refill-deposit loops | +0.6% | Europe and Asia-Pacific; emerging in North America | Long term (≥ 4 years) |

| Growth in RTD beverage launches | +0.9% | Global; strongest in Asia-Pacific | Short term (≤ 2 years) |

| Food-waste reduction initiatives | +0.4% | North America and Europe; expanding to emerging markets | Medium term (2-4 years) |

| Craft aerosol packaging for “at-home spa” | +0.3% | Premium segments in North America and Europe | Short term (≤ 2 years) |

| Smart-printing enabling supply-chain traceability | +0.2% | Developed markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aluminum Price Volatility Accelerates Lightweighting Adoption

Manufacturers are answering unpredictable aluminum costs by cutting material use instead of sacrificing margins. ReAl Gen 2, commercialized in 2024, reduces can wall thickness up to 15% while preserving top-load strength, directly offsetting commodity swings. Lighter cans also ease logistics emissions, aligning with corporate net-zero roadmaps. Premium brands willingly absorb the incremental technology cost because the aesthetic and sustainability credentials support higher shelf prices. Patent activity shows designers fine-tuning micro-alloy recipes that raise strength-to-weight ratios and enable high-speed impact extrusion. As more lines convert, the metal cans market enjoys a reinforcing cycle of lower material intensity and enhanced economic resilience.

Global DRS Programs Expanding Refill-Deposit Loops

Mandatory deposit-return systems are closing the loop on beverage containers and systematically advantaging infinitely recyclable aluminum. Europe’s updated Packaging and Packaging Waste Regulation, in force since 2024, sets aggressive material-specific targets that aluminum readily meets. Singapore and Germany post return rates above 90%, providing reliable secondary feedstock that shields manufacturers from volatile virgin supply. These loops shrink lifecycle emissions and reduce producer compliance fees, which in turn encourage brand owners to pivot toward cans in new beverage sub-segments. As infrastructure matures, DRS economics further elevate the attractiveness of the metal cans market relative to PET and flexibles.

Growth in RTD Beverage Launches

The global boom in ready-to-drink coffees, teas, cocktails, and functional beverages is sharpening demand for aluminum’s light-proof barrier and rapid chill properties. RTD coffee alone grew 23% in 2024 and overwhelmingly favored cans over glass for portability and superior artwork display. Asian urban consumers prioritizing convenience, and Western millennials seeking premium chilled cocktails, both gravitate toward sleek can formats. Smaller SKUs dovetail with portion-control trends and enable producers to test niche flavors without high glass line changeover costs. Each new RTD launch raises baseline can volumes and reinforces brand storytelling possibilities through high-definition printing.

Food-Waste Reduction Initiatives Driving Shelf-Stable Formats

Government and corporate pledges under U.N. SDG 12.3 aim to halve food waste by 2030; shelf-stable metal packaging directly supports that ambition. [1]United Nations, “Sustainable Development Goal 12: Responsible Consumption and Production,” un.org Aluminum and steel cans extend shelf life two-to-five times longer than many flexible pouches, safeguarding quality in soups, sauces, and seasonal produce. Campbell Soup’s 2024 range demonstrates how shelf-stable recipes satisfy consumer convenience while meeting retailers’ shrink-reduction KPIs. Extended ambient stability also simplifies inventory management for e-commerce channels, which favor packages that resist temperature swings and long dwell times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET and flexibles cost advantage in emerging markets | -0.7% | Asia-Pacific and Latin America (price-sensitive segments) | Short term (≤ 2 years) |

| EU BPA-migration limits on epoxy liners | -0.3% | Europe; spillover to other developed markets | Medium term (2-4 years) |

| Steel mill decarbonization costs | -0.4% | Europe and North America (global raw-material flows) | Long term (≥ 4 years) |

| E-commerce shift to “ship-in-own-container” | -0.2% | High e-commerce penetration markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PET and Flexibles Cost Advantage in Emerging Markets

Where incomes stay modest, PET bottles and pouches undercut cans by 15-25% on a delivered-cost basis, slowing metal penetration in India, Brazil, and parts of Southeast Asia. PET’s local resin output and lightweight logistics keep shelf prices low. Yet new Indian EPR rules effective 2024 have started to erode plastics’ price edge by monetizing end-of-life liabilities, encouraging retailers to trial aluminum formats for aspirational sub-brands. [2]Ministry of Environment, Forest and Climate Change, “Extended Producer Responsibility Guidelines 2024,” moef.gov.in

EU BPA-Migration Limits on Epoxy Liners

Europe’s latest bisphenol A limits have forced can makers to qualify new water-based or polymeric liners, adding as much as USD 550,000 in validation costs per SKUs. The expense temporarily cramps margins and slows launch timelines, but once approved, BPA-NI coatings deliver compliant performance and position cans as the safest choice for infant and specialty nutrition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum’s Circular Economy Advantage

Aluminum captured a commanding 70.56% metal cans market share in 2025 and is on course for a 4.35% CAGR through 2031. That dominance rests on closed-loop recycling systems that require 95% less energy than primary smelting, lowering scope 3 emissions for brand owners. Across beverages, personal care, and pharmaceuticals, marketers leverage aluminum’s printable surface and corrosion resistance to differentiate premium SKUs. In parallel, decarbonization pressures elevate aluminum versus steel, whose mills face rising carbon fees.

Steel remains essential where physical robustness overrides weight penalties-chiefly in canned meats and heat-processed meals. Yet continuing decarbonization costs are eroding its long-term price competitiveness. Producers respond by alloying tinplate with chromium to trim gauge, but substitution risk persists. For investors, the metal cans market reflects a clear material bifurcation: aluminum for growth, steel for stability.

By Can Structure: Monobloc Innovation Drives Growth

Two-piece cans preserved 54.06% share in 2025 thanks to efficient drawn-and-ironed lines that churn out billions of beverage units annually. These formats balance weight, cost, and stacking strength, underscoring their role as the backbone of the metal cans market size. On the innovation front, monobloc aerosol designs are expanding at a 4.78% CAGR, helped by personal-care brands seeking seamless shapes and advanced valves.

Impact-extruded monoblocs enable refillable cartridge systems and ultralight shells, unlocking eco-premium price points in deodorants and hair mists. Three-piece welded cans, while aging, sustain niche demand in large-volume foodservice and specialty products where customized diameters or necked ends matter more than weight. Overall, structural variety equips converters to serve diverse product viscosities, filling pressures, and shelf-life requirements.

By Capacity/Size: Premiumization Fuels Smaller Formats

The 250-500 ml category delivered 30.18% of the metal cans market size in 2025, driven by mainstream soda and beer volumes. Yet ≤250 ml slim and sleek cans represent the fastest 4.88% CAGR. These smaller formats match today’s portion-control ethos and command higher price per ounce as consumers equate compact graphics with specialty positioning. Smart-printing pilots commonly debut on 200 ml RTD coffees, illustrating how digital engagement layers onto premium SKUs.

Mid-size 500-1,000 ml cans hold steady among family beverages and pantry staples, whereas containers exceeding 1 L cater to industrial coatings, edible oils, and institutional ingredients. As e-commerce expands, shipping cost constraints spotlight weight-efficient smaller cans, further fueling the premium miniature trend inside the global metal cans market.

By Manufacturing Process: Impact Extrusion Gains Efficiency

Drawn-and-ironed technology made up 32.14% of the metal cans market size in 2025 since it scales easily for carbonated beverages. The method delivers thin walls with minimal scrap, maintaining its cost edge for high-throughput lines. Impact extrusion, however, is gaining ground at a 4.74% CAGR because it lets producers form dent-resistant, seamless walls for cosmetics, OTC sprays, and lubricants while cutting metal waste by roughly 20%.

Process engineers have refined die-lubricant mixtures and servo press controls to raise cycle speeds, narrowing the unit-cost gap with DI lines. Drawn-and-redrawn techniques survive where multi-stage deep draws create complex geometries for paint, sealants, or specialty chemicals. Collectively, process diversification equips manufacturers with a playbook to optimize strength, aesthetics, and sustainability targets.

By End-User Industry: Pharmaceutical Uptake Accelerates

Beverage fillers retained 38.01% metal cans market share in 2025 and continue to be the demand anchor, underscored by high carbonation stability and fast-chill appeal. In contrast, pharmaceuticals are the growth engine, advancing at a 4.95% CAGR as regulators tighten integrity and counterfeit controls. Serialization-ready metal packs meet 2D-barcode mandates, and aluminum’s inertness safeguards active ingredients.

Food brands leverage cans to curb spoilage, a corporate priority linked to SDG 12.3 goals. Personal-care labels exploit decoration latitude to convey spa-quality cues, while automotive fluids and paints rely on puncture resistance and chemical compatibility. These multi-industry streams reinforce volume diversity and help buffer cyclical weakness in any single sector.

Geography Analysis

North America led the global metal cans market with 39.72% revenue share in 2025. Mature soft-drink consumption, highly efficient curbside collection, and EPR statutes underpin stable can demand. Regional aluminum recycling rates hover near 75%, ensuring supply security while muting virgin-metal exposure. Recent announcements exceeding USD 200 million for new capacity in the United States and Mexico signal long-term confidence in steady, if incremental, growth.

Asia-Pacific is projected to log a 5.88% CAGR to 2031, the fastest worldwide. Urban migration, rising middle-class incomes, and surging RTD innovations keep can volumes expanding. Japan’s deposit-scheme framework recovered 93% of aluminum cans in 2024, setting a circular-economy benchmark for neighbors. China’s move from import dependence to regional export hub illustrates the strategic shift toward indigenous manufacturing and broader influence over global supply networks.

Europe balances opportunity and complexity. Stringent BPA rules force costly liner shifts, yet the same regulations elevate cans’ sustainability credentials and accelerate steel-to-aluminum substitution. The Green Deal’s circularity targets amplify recycling premiums, ultimately supporting the metal cans market despite short-term compliance drag. South America and the Middle East and Africa represent frontier demand where infrastructure gaps and price sensitivity slow adoption, but gradual EPR frameworks and digitization could lift can penetration over the forecast horizon.

Competitive Landscape

Industry structure is moderately consolidated, with a handful of multinationals controlling large swaths of capacity yet facing nimble regional challengers. Ball Corporation, Crown Holdings, Ardagh Metal Packaging, and Silgan Holdings collectively defend market positions through geographic expansion, lightweighting R&D, and digital printing rollouts. The 2024 acquisition of Helvetia Packaging by Crown bolstered premium food can portfolios in Europe.

Technology races center on reducing metal intensity, embedding smart-codes, and validating BPA-NI liners. Companies are also integrating blockchain audits to assure provenance and differentiate with traceability certifications. Smaller entrants penetrate craft beverage and personal-care niches by offering agile design services and short-run printing, challenging incumbents to enhance service levels.

Steel decarbonization costs and carbon-trading exposure are tilting the competitive field toward aluminum, prompting some converters to retrofit lines accordingly. Strategic alliances-such as Ball’s partnership with Meadow-bring cross-category expertise and broaden aluminum’s reach into sectors historically dominated by plastics. The result is an ecosystem where scale, sustainability credentials, and digital capabilities together define winning positions.

Metal Cans Industry Leaders

Ball Corporation

Crown Holdings Inc.

Ardagh Group S.A.

Silgan Holdings Inc.

CAN-PACK S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Ball Corporation published its 2024 Combined Annual and Sustainability Report highlighting achievements in aluminum recycling and circular-economy initiatives, demonstrating progress toward sustainability commitments and regulatory compliance objectives Ball Corporation.

- January 2025: Crown Holdings announced the launch of its new digital printing capabilities for beverage cans, enabling customization and limited-edition designs that support brand differentiation strategies in competitive beverage markets Crown Holdings.

- January 2025: Ball Corporation entered into a strategic alliance with Meadow involving a minority investment to commercialize MEADOW KAPSUL fully recyclable aluminum can system for personal and home care products, expanding aluminum packaging into categories traditionally served by plastic containers and creating new market opportunities in sustainable personal care applications Ball Corporation.

- January 2025: Ball Corporation and Henkel won the ADF Sustainable Innovation Award at Paris Packaging Week for developing a 150 ml lightweight impact-extruded aluminum aerosol can using Ball's proprietary ReAl Gen 2 alloy, representing Europe's lightest impact-extruded aerosol can and demonstrating advanced lightweighting capabilities Ball Corporation.

Global Metal Cans Market Report Scope

Metal cans are containers for the distribution or storage of goods. It is composed of thin metal, which is prominently driven by its growing use in food and beverage packaging. The metal can market is tracked by the revenue accumulated from the metal can sales offered by various vendors in the market.

The metal cans market is segmented by material type (aluminum and steel), end-user industry (food, beverage, cosmetics and personal care, pharmaceuticals, paint, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material Type

| Aluminium |

| Steel |

By Can Structure

| Two-Piece |

| Three-Piece |

| Monobloc Aerosol |

By Capacity / Size

| ≤250 ml |

| 250–500 ml |

| 500–1,000 ml |

| >1,000 ml |

By Manufacturing Process

| Drawn and Ironed (D&I) |

| Drawn and Redrawn (DRD) |

| Impact Extrusion |

By End-User Industry

| Food |

| Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Paints and Industrial Chemicals |

| Automotive Fluids and Lubricants |

| Other End-User Industry |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Aluminium | ||

| Steel | |||

| By Can Structure | Two-Piece | ||

| Three-Piece | |||

| Monobloc Aerosol | |||

| By Capacity / Size | ≤250 ml | ||

| 250–500 ml | |||

| 500–1,000 ml | |||

| >1,000 ml | |||

| By Manufacturing Process | Drawn and Ironed (D&I) | ||

| Drawn and Redrawn (DRD) | |||

| Impact Extrusion | |||

| By End-User Industry | Food | ||

| Beverage | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Paints and Industrial Chemicals | |||

| Automotive Fluids and Lubricants | |||

| Other End-User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global metal cans market in 2026?

The metal cans market size reaches USD 88.45 billion in 2026 and is projected to advance at a 3.52% CAGR to 2031.

Which region is growing fastest for metal packaging?

Asia-Pacific posts the quickest 5.88% CAGR, propelled by urbanization and surging RTD beverage launches.

What material dominates beverage can production?

Aluminum holds 70.56% market share thanks to its lightweight, infinitely recyclable profile and strong recycling infrastructure.

Why are pharmaceuticals increasing their use of metal cans?

Regulatory focus on tamper evident, track-and-trace capable, chemically inert packaging is steering drug companies toward aluminum formats that meet these requirements.

How are deposit-return systems affecting can demand?

Mandatory DRS schemes lock in high collection rates, supply abundant recycled feedstock, and lower compliance costs, thereby boosting the economic case for metal cans.

Which manufacturing process is gaining share?

Impact extrusion is expanding at a 4.74% CAGR because it delivers seamless walls, reduced scrap, and compatibility with refillable aerosol concepts.

Page last updated on: