Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

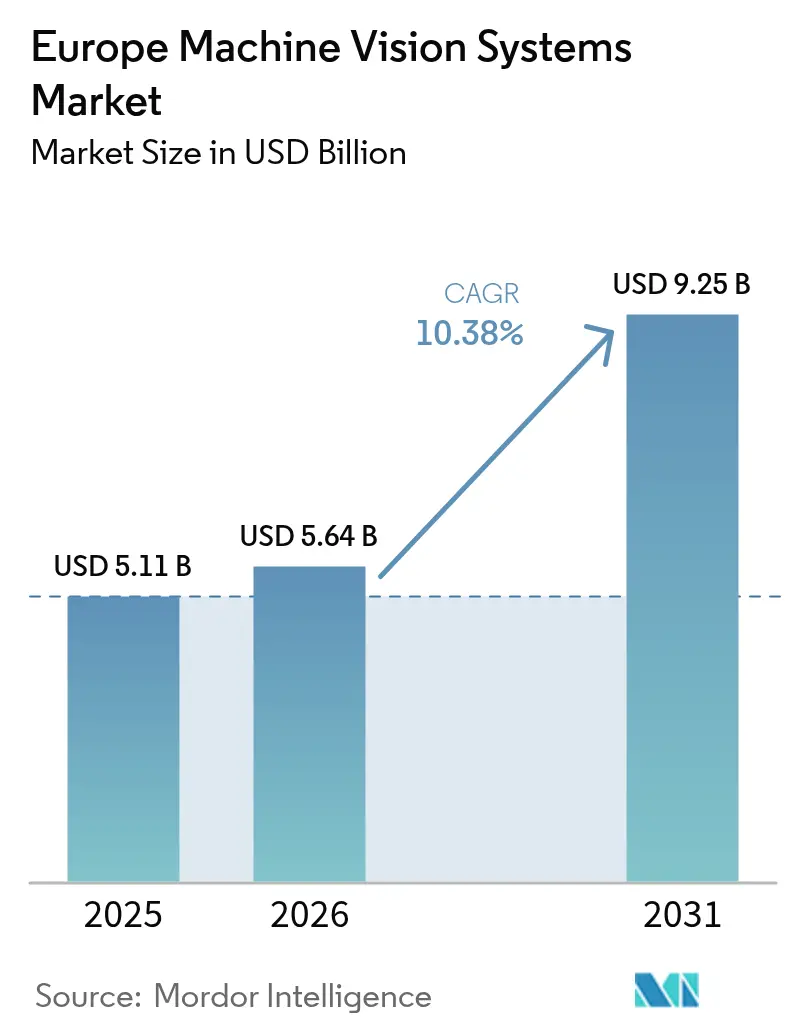

| Base Year Market Size (2025) | USD 5.11 Billion |

| Market Size (2026) | USD 5.64 Billion |

| Market Size (2031) | USD 9.25 Billion |

| Growth Rate (2026 - 2031) | 10.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Machine Vision Systems Market Analysis by Mordor Intelligence

Europe machine vision systems market size in 2026 is estimated at USD 5.64 billion, growing from 2025 value of USD 5.11 billion with 2031 projections showing USD 9.25 billion, growing at 10.38% CAGR over 2026-2031. Digitalization programs, EU sustainability rules, and labour shortages are accelerating demand for automated optical inspection across factories and warehouses. Hardware remains the largest spending category, but edge-enabled software is scaling fast as plants look for real-time analytics and AI-driven defect detection. Germany anchors regional revenue through its electric-vehicle supply chain, while Italy is expanding quickly on the strength of pharmaceutical machinery exports. Competition is moderate: global leaders and niche European specialists alike deploy deep learning and 3D vision to open new use cases and lower entry costs for small and mid-size manufacturers.

Key Report Takeaways

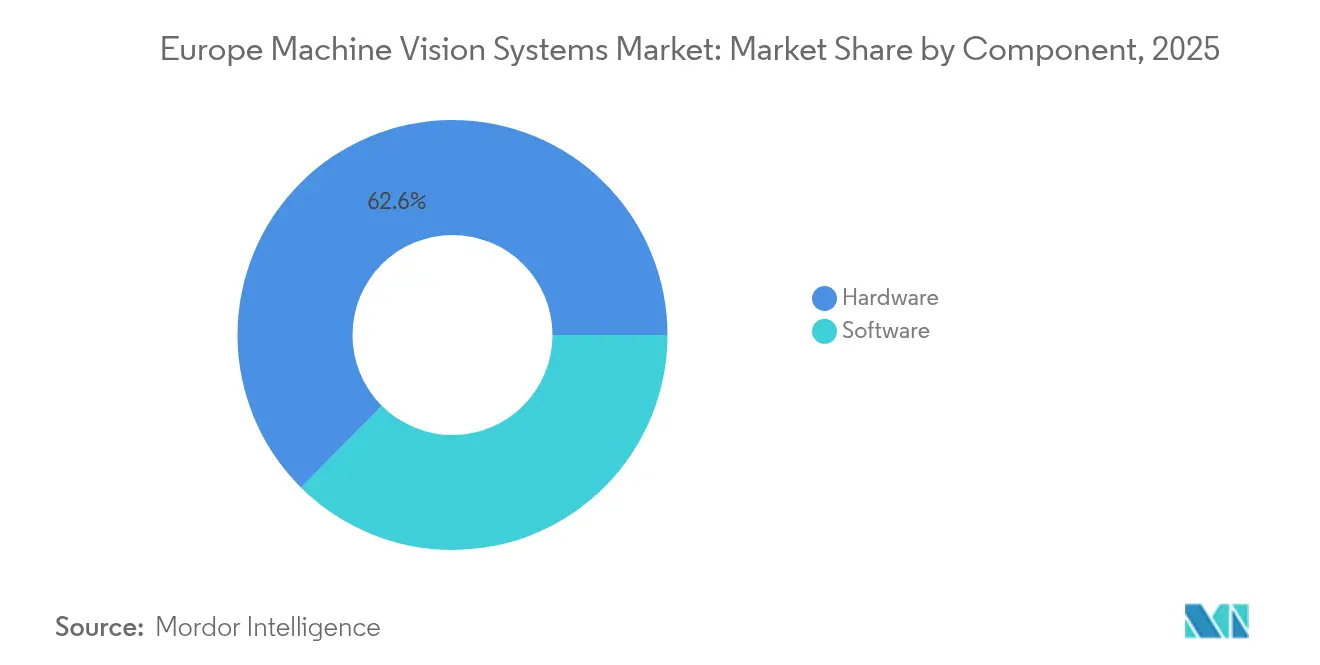

- By component, hardware captured 62.55% of Europe machine vision systems market share in 2025, whereas software is projected to grow at a 12.68% CAGR through 2031.

- By product, PC-based platforms held 56.42% of Europe machine vision systems market share in 2025; smart camera-based systems are poised for a 13.55% CAGR to 2031.

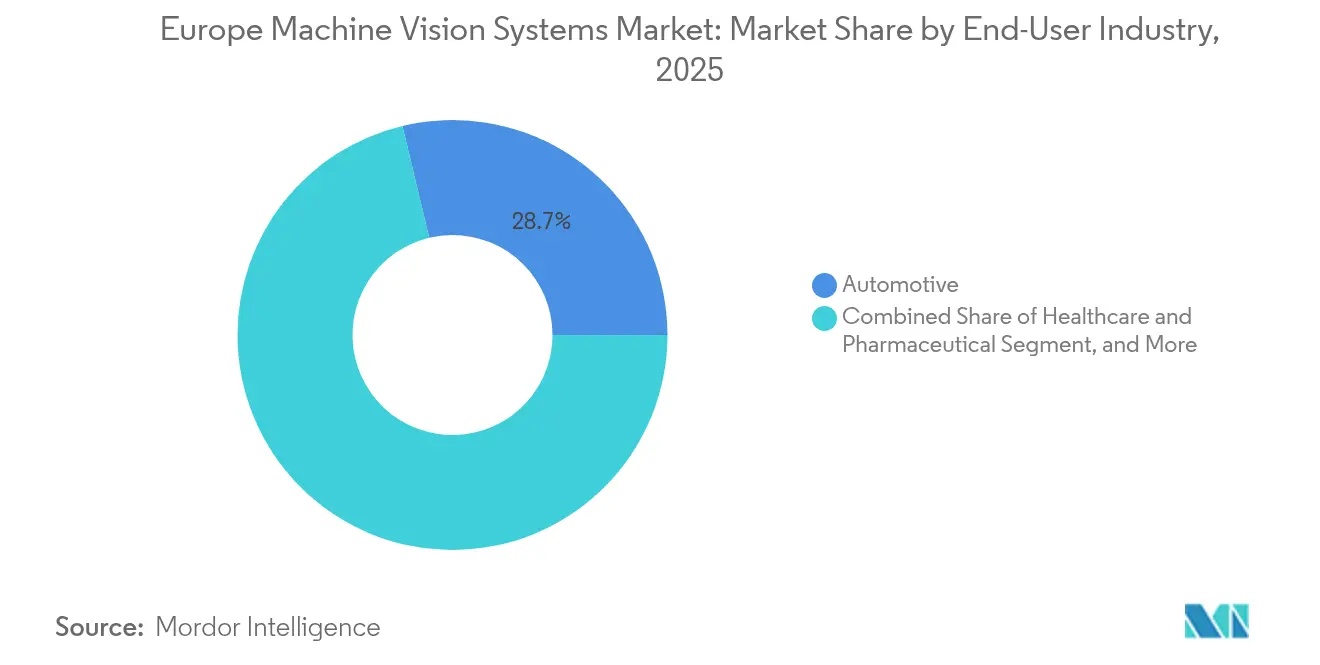

- By end-user, automotive accounted for 28.74% of Europe machine vision systems market share in 2025, while healthcare and pharmaceutical are set to expand at a 12.35% CAGR over 2026-2031.

- By application, quality inspection represented a 41.95% slice of Europe machine vision systems market size in 2025, and robotics safety and others are advancing at a 13.78% CAGR toward 2031.

- By geography, Germany contributed 27.50% of Europe machine vision systems market share in 2025; Italy is expected to log the region’s fastest 11.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Machine Vision Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Need for Quality Inspection and Automation | +2.30% | Global, strongest in Germany and Italy | Medium term (2-4 years) |

| Rising Demand for Accurate Defect Detection | +1.80% | Europe-wide, concentrated in automotive and electronics hubs | Short term (≤ 2 years) |

| Growing Adoption of Industry 4.0 and Smart Factories | +2.70% | Germany, Netherlands, Nordic countries with spillover to Eastern Europe | Long term (≥ 4 years) |

| Advancements in Camera Sensor Resolutions and Processing Speeds | +1.50% | Global with strong adoption in Western Europe | Medium term (2-4 years) |

| EU Sustainability Rules Driving Energy-Efficiency Audits | +1.20% | EU-wide, particularly Germany, France, Netherlands | Long term (≥ 4 years) |

| Edge AI Inferencing ASICs Unlocking New Use-Cases | +1.10% | Technology hubs in Germany, UK, France, Nordic region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Need for Quality Inspection and Automation

European manufacturers are turning to vision-guided inspection to offset labour shortages and satisfy stricter quality rules. Euro 7 requirements now oblige detailed emissions monitoring, pushing automakers to integrate vision-enabled diagnostics into assembly lines.[1]European Union, “Directive (EU) 2024/825 empowering consumers for the green transition,” europa.eu German supplier Dürr embedded cameras into paint-shop robotics, cutting energy use by 30% through more precise spraying.[2]Dürr, “Production Efficiency,” durr.com Pharmaceutical players such as Stevanato Group deploy AI-enhanced systems that inspect more than 600 containers per minute without human intervention. These successes encourage broader adoption across mid-sized plants seeking to safeguard yields and compliance.

Rising Demand for Accurate Defect Detection

Tolerance bands in electronics and semiconductor production continue to shrink, creating demand for sub-micron visual analytics. Belgian firm Robovision demonstrated 100 m-per-minute inspection speeds while maintaining PCB-grade accuracy.[3]Robovision, “Company News,” robovision.ai Food and beverage processors follow suit with X-ray units such as Deep Detection’s PhotonAI, which analyzes 20 million photons / mm² / s to screen for contaminants. Illumination advances from UV to multispectral help identify previously invisible flaws, widening the value proposition of machine vision in Europe.

Growing Adoption of Industry 4.0 and Smart Factories

OPC UA-enabled data exchange has become standard in German and Nordic facilities, letting vision sensors feed real-time alerts into MES and energy dashboards. VDMA reported that 81% of machinery builders reallocated resources to automation after supply chains normalized in 2024.[4]VDMA, “Pumps and Compressors for the World Market 2024,” vdma-verlag.com Autonomous picking robots like Magazino’s TORU now combine 2D and 3D cameras for 20-hour shifts in warehouses, trimming fulfilment costs for retailers. Such examples illustrate how the Europe machine vision systems market continues to underpin factory digitalization agendas.

Advancements in Camera Sensor Resolutions and Processing Speeds

3D-stacked CMOS imagers with on-sensor neural engines, typified by the J3DAI prototype, cut latency and power draw for edge inspection. CoaXPress 2.1 lifts bandwidth ceilings to 50 Gbps, enabling real-time 8K analysis. EU-funded hyperspectral projects extend wavelength coverage for agriculture and vertical farming, where a 20% yield boost was recorded in trials. These technical leaps expand addressable applications and reinforce replacement demand for legacy equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Deployment Costs for SMEs | -1.40% | Europe-wide, particularly Eastern Europe and Southern Italy | Short term (≤ 2 years) |

| Lack of Skilled Personnel for System Integration | -1.10% | Germany, Netherlands, Nordic countries with spillover effects | Medium term (2-4 years) |

| Fragmented European Harmonised Standards | -0.80% | EU-wide with varying national implementations | Long term (≥ 4 years) |

| Cyber-Security Risks in Cloud-Based Vision Analytics | -0.70% | Global with heightened concern in Germany and France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Deployment Costs for SMEs

Full-line vision installations often exceed EUR 100 000 (USD 113 000) and deter smaller factories, especially in wage-competitive regions of Eastern Europe. Smart cameras and no-code software such as MVTec MERLIC now sell for under EUR 25,000 (USD 28,250), shrinking barriers but not eliminating them. Upcoming EU consumer-protection directives on repairability may add life-cycle costs and stretch payback periods.

Lack of Skilled Personnel for System Integration

VDMA surveys rank labour shortages among the top bottlenecks for automation projects. The cross-disciplinary mix of optics, AI, and robotics skills is in short supply even around Munich and Eindhoven. Cognex has expanded training centers across 15 European sites to close the gap, yet competition from software giants keeps wage inflation high. Vendors increasingly bundle turnkey services to simplify commissioning for understaffed plants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Software Disruption

Europe machine vision systems market size for hardware reached a commanding share in 2025, when cameras, optics, and frame grabbers represented 62.55% of revenue. Vision systems cameras accounted for the bulk, aided by German makers like Basler and IDS Imaging that supply robust CMOS lines. *Europe machine vision systems market share* for hardware is expected to erode gradually as software value rises at a 12.68% CAGR. Software’s ascent stems from AI models optimized for embedded chips, vendor-agnostic platforms such as MVTec HALCON, and demand for no-code interfaces that let process engineers adjust inspection rules without coding knowledge.

Second-generation edge libraries now run sophisticated neural nets on fanless systems, lowering the total cost of ownership. Cloud analytics still plays a role for compute-heavy tasks, but GDPR compliance drives many factories to keep sensitive imagery on-premises. Cyber-hardened containers and ISO 27001 certifications have therefore become standard check-box items during procurement.

By Product: Smart Cameras Challenge PC-Based Supremacy

PC-based architectures retained 56.42% of Europe's machine vision systems market share in 2025, bolstered by GPU acceleration that handles multi-camera automotive paint inspection and wafer metrology. Smart cameras, however, are posting a 13.55% CAGR and chip away at rack-mounted solutions whenever one camera can do the job. Cost savings accrue from reduced cabling and cabinet hardware, while ARM and vision-processing units keep inference times under 10 ms.

Healthcare use cases exemplify this shift: Stevanato Group runs smart cameras to verify vial integrity at >600 units per minute and meets stringent pharma rules. Mobile robotics also benefits, as space constraints favour integrated optics and compute within a single housing. As firmware updates add new neural layers over time, smart cameras become an easily scalable entry point for SMEs testing automation waters.

By End-User Industry: Healthcare Drives Growth amid Automotive Leadership

Automotive lines remained the anchor customer base with a 28.74% share in 2025, as battery pack assembly and Euro 7 emissions checks multiply inspection stations. OEMs tap 3D vision to position prismatic cells within ±0.1 mm, while tire makers deploy vision to quantify particulate emissions. Healthcare and pharmaceutical applications lead growth at a 12.35% CAGR, propelled by 100% container inspection mandates and UDI serialization rules.

In drug injectables, AI classifiers now cut false rejects by double-digit percentages and preserve batch yields. Medical-device firms adopt vision to track micro-components during catheter assembly, ensuring traceability under EU MDR. With new biologics and personalized therapies requiring small-batch processing, demand for flexible, rapid-changeover vision lines is set to climb.

By Application: Quality Inspection Dominance Faces Robotics Disruption

Quality inspection held 41.95% of Europe's machine vision systems market size in 2025, spanning paint anomalies, PCB solder bridges, and glass container scratches. Robotics safety and other emerging uses are expanding at a 13.78% CAGR as collaborative robots spread across logistics and assembly. 3D time-of-flight sensors create protective envelopes around co-workers, allowing higher line speeds without physical cages.

Metrology benefits from sub-micron sensors and algorithmic calibration routines, meeting aerospace tolerance demands. Code reading evolved from 1D barcodes to dot-peen data matrix and even etched titanium parts in medical implants. Positioning and guidance employ SLAM fusion, enabling AGVs to adapt routes when pallets or workers alter floor geography unexpectedly.

Geography Analysis

Germany’s 27.50% share underscores its dense ecosystem of component suppliers, software firms, and integrators. Dürr uses vision to lower paint-shop energy by 30%, while MVTec’s HALCON toolkit underpins many OEM offerings. VDMA recorded 8% revenue growth for German vision vendors in 2024, with exports cushioning domestic slowdowns.

The United Kingdom grows more selectively after Brexit, focusing on aerospace and life-science niches that value AI algorithms derived from local research universities. Funding access remains uneven, nudging startups such as Vision Intelligence to hunt deals outside Europe. Customs frictions add lead-time buffers, yet strong AI talent continues to attract multinational R&D labs.

Italy posts the region’s fastest 11.55% CAGR, powered by pharmaceutical equipment exports and automotive diversification. Stevanato Group commands a global share in parenteral inspection, and SEA Vision’s track-and-trace suite secures EUDAMED compliance. Lombardy’s machinery districts collaborate closely with Swiss optics specialists, yielding competitive turnkey lines for food packaging, where energy audits fuel upgrades.

Competitive Landscape

Europe machine vision systems market remains moderately concentrated. Cognex runs facilities in 15 countries, providing localized service and training. German vendors excel in algorithm libraries, with MVTec HALCON providing platform independence that OEMs value. Basler, IDS, and Allied Vision keep hardware supply resilient through European fabs.

Acquisition momentum is strong. Zebra Technologies bought Czech 3D specialist Photoneo in 2025 to enhance bin-picking accuracy. Hitachi purchased MA Micro Automation for USD 80.8 million, expanding its medical-device inspection reach. Lear added WIP Industrial Automation to boost vision-guided robotics for seating plants. Such deals highlight priority segments: 3D, medical, and logistics.

Emerging challengers center on AI. Robovision scaled sub-3 nm semiconductor inspection and opened a U.S. office after raising USD 42 million. EdgeCortix promotes low-power ASICs that shrink inference costs. Vendors differentiate through ISO 27001 software security and GDPR-ready cloud connectors, critical factors for European buyers wary of data leaks.

Europe Machine Vision Systems Industry Leaders

Cognex Corporation

Keyence Corporation

Omron Corporation

IDS Imaging Development Systems GmbH

Teledyne DALSA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Zebra Technologies closed the acquisition of Photoneo, adding parallel structured-light 3D vision for robotics.

- November 2025: Robovision launched U.S. headquarters after a USD 42 million Series A round.

- August 2025: SICK and Endress+Hauser formed a 50/50 joint venture for process analysers and gas flowmeters.

- July 2025: Lear completed the takeover of WIP Industrial Automation to strengthen robotics and vision expertise.

Europe Machine Vision Systems Market Report Scope

According to the Automated Imaging Association, machine vision includes all industrial and non-industrial applications in which a combination of software and hardware provides operational guidance to devices in the execution of their functions based on the capture and processing of images.

The machine vision system is the substitution of the human visual sense and judgment capabilities with a video camera and computer to perform an inspection task. It is the automatic acquisition and analysis of images to obtain desired data for controlling or evaluating a specific part or activity.

Under component, hardware and software are considered under the scope. The hardware includes vision systems, cameras, optics and illumination systems, frame grabbers, and other types of hardware.

The end-user industry includes electronics and semiconductors, automotive, medical devices and pharmaceuticals, logistic and retail, food and beverages, and other end-user industries.

By Component

| Hardware | Vision Systems |

| Cameras | |

| Optics and Illumination Systems | |

| Frame Grabbers | |

| Other Hardware | |

| Software |

By Product

| PC-Based |

| Smart Camera-Based |

By End-User Industry

| Automotive |

| Electronics and Semiconductors |

| Food and Beverage |

| Healthcare and Pharmaceutical |

| Logistics and Retail |

| Other Industries |

By Application

| Quality Inspection |

| Measurement and Metrology |

| Identification and Code Reading |

| Positioning and Guidance |

| Robotics Safety and Others |

By Country

| Germany |

| United Kingdom |

| Italy |

| Rest of Europe |

| By Component | Hardware | Vision Systems |

| Cameras | ||

| Optics and Illumination Systems | ||

| Frame Grabbers | ||

| Other Hardware | ||

| Software | ||

| By Product | PC-Based | |

| Smart Camera-Based | ||

| By End-User Industry | Automotive | |

| Electronics and Semiconductors | ||

| Food and Beverage | ||

| Healthcare and Pharmaceutical | ||

| Logistics and Retail | ||

| Other Industries | ||

| By Application | Quality Inspection | |

| Measurement and Metrology | ||

| Identification and Code Reading | ||

| Positioning and Guidance | ||

| Robotics Safety and Others | ||

| By Country | Germany | |

| United Kingdom | ||

| Italy | ||

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe machine vision systems market in 2026?

The market stands at USD 5.64 billion and is projected to reach USD 9.25 billion by 2031, reflecting a 10.38% CAGR.

Which component segment is growing fastest?

Software platforms are expanding at 12.68% CAGR as factories adopt AI and edge analytics to complement existing hardware.

What drives demand in the healthcare sector?

Strict 100% inspection rules for parenteral drugs and UDI traceability requirements are propelling 12.35% CAGR growth in healthcare and pharmaceutical applications.

Why are smart cameras gaining traction?

Integrated optics and on-board processors cut cabling and cabinet costs, helping smart camera systems grow at 13.55% CAGR, especially in space-constrained or single-camera setups.

Which country shows the fastest market growth?

Italy leads with an 11.55% CAGR, buoyed by strong pharmaceutical machinery exports and wider use of vision in packaging and automotive lines.

Page last updated on: