Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

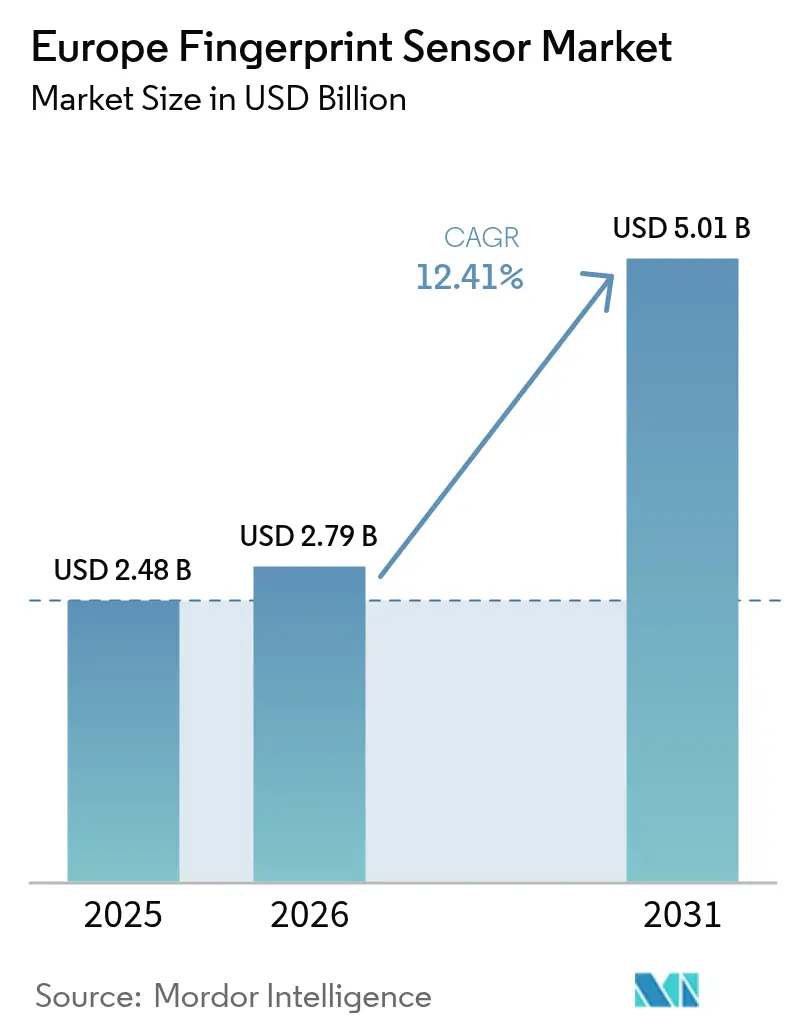

| Base Year Market Size (2025) | USD 2.48 Billion |

| Market Size (2026) | USD 2.79 Billion |

| Market Size (2031) | USD 5.01 Billion |

| Growth Rate (2026 - 2031) | 12.41% CAGR |

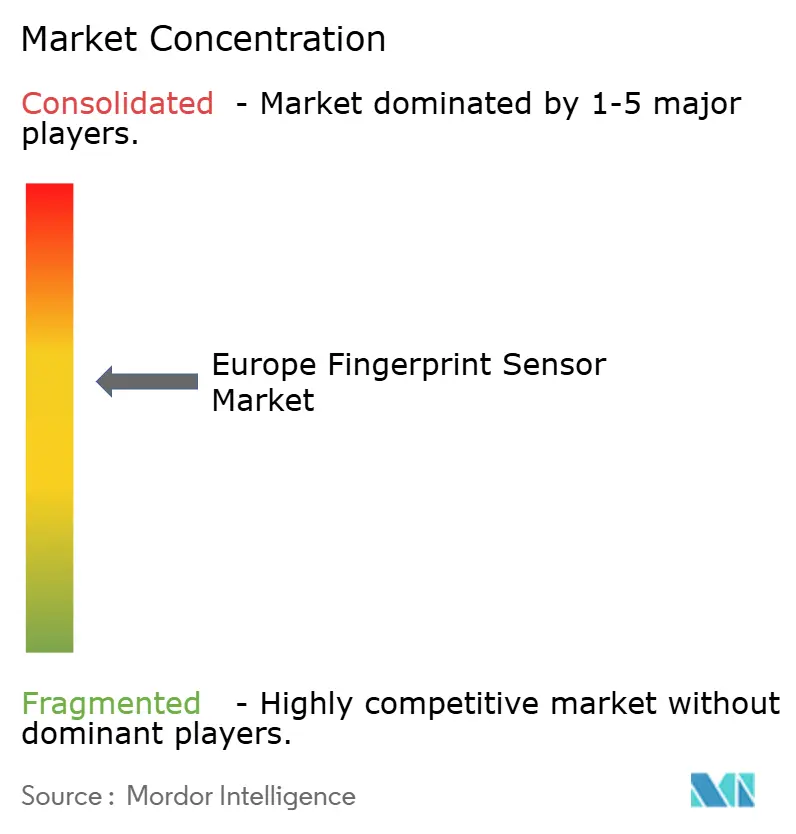

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Fingerprint Sensor Market Analysis by Mordor Intelligence

The European fingerprint sensor market size is expected to grow from USD 2.48 billion in 2025 to USD 2.79 billion in 2026 and is forecast to reach USD 5.01 billion by 2031 at 12.41% CAGR over 2026-2031. Sustained regulatory pressure, most notably the EU Digital Identity Wallet mandate, is driving an accelerated shift from password-based verification to on-device biometric authentication throughout public services, financial transactions, and connected consumer devices. Component suppliers have responded with thinner, faster, and lower-power sensor modules that align with the privacy-by-design principles under the GDPR, while systems integrators benefit from common template standards that streamline cross-border identity checks. At the same time, premium smartphone brands, banking card issuers, and automotive OEMs are converging on ultrasonic and side-mounted designs that improve user experience without compromising liveness detection. Germany’s industrial base and Italy’s post-pandemic digitization funding jointly illustrate how both mature and catch-up economies are boosting purchase volumes, even as lingering semiconductor shortages constrain near-term production output. Competitive intensity remains moderate: Nordic vendors hold certifications that resonate in government bids, whereas Asian original-design manufacturers (ODMs) keep average selling prices under pressure in the mass-market consumer segment.

Key Report Takeaways

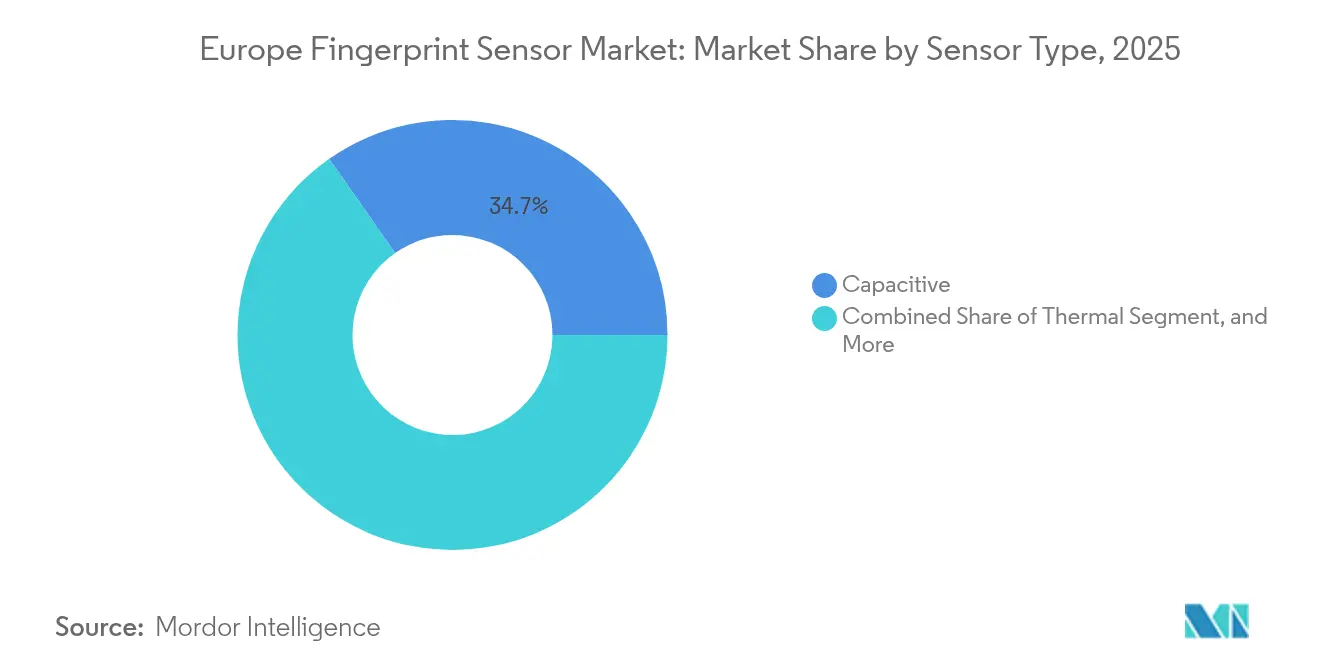

- By sensor type, capacitive technology held a 34.72% share of the European fingerprint sensor market in 2025, while ultrasonic sensors are projected to advance at a 13.12% CAGR through 2031.

- By application, smartphones and tablets accounted for a 43.22% revenue share of the European fingerprint sensor market in 2025; IoT devices and other applications are forecasted to expand at a 14.23% CAGR through 2031.

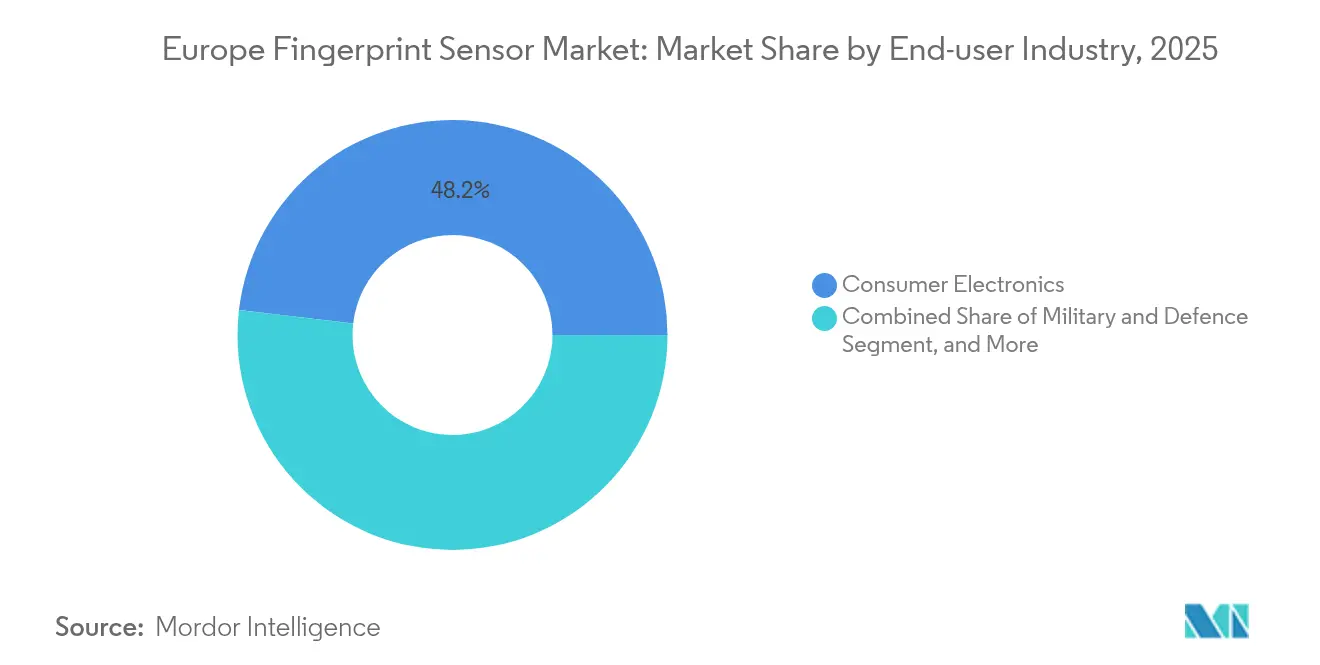

- By end-user industry, consumer electronics accounted for 48.15% of the European fingerprint sensor market size in 2025, while the government segment is projected to grow at a 13.35% CAGR across the forecast horizon.

- By sensor placement, in-display sensors commanded a 35.64% share of the European fingerprint sensor market size in 2025, while side-mounted units are registering the fastest growth at a 13.84% CAGR.

- By country, Germany led the European fingerprint sensor market with a 18.73% share in 2025, while Italy is projected to grow the fastest at a 12.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Fingerprint Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of biometric authentication in consumer electronics | +2.1% | Germany, UK, France | Medium term (2-4 years) |

| Regulatory push for stronger eID and ePassport programs | +2.8% | EU-wide, early gains in Estonia, Portugal, Bulgaria | Long term (≥ 4 years) |

| Demand for contactless payments and smartcards | +1.9% | Western Europe core, expansion to CEE | Short term (≤ 2 years) |

| Multimodal biometric fusion in border-control kiosks | +1.4% | Germany, France, Netherlands, UK | Medium term (2-4 years) |

| Ultra-thin flexible sensors for wearables and healthcare | +1.6% | Nordic countries, Germany, Switzerland | Long term (≥ 4 years) |

| EU Digital Identity Wallet standardization | +2.2% | All 27 EU member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of biometric authentication in consumer electronics

Flagship handset makers are embedding larger ultrasonic sensing areas beneath OLED panels, enabling one-tap enrollment even with wet fingers while preserving bezel-free displays.[1]IEEE, “Advanced Ultrasonic Fingerprint Sensor Technology,” ieeexplore.ieee.org Qualcomm’s 3D Sonic Max and Goodix-Vivo prototypes authenticate in under 300 ms, reinforcing a performance gap versus legacy capacitive parts. Hardware commonality in smartphones, tablets, and smartwatches enables vendors to amortize R&D costs, pushing biometric components into mid-tier devices sooner than in prior cycles. Automotive brands, such as Mercedes-Benz, have incorporated these modules into steering wheels and door pillars, extending the addressable volume beyond personal electronics.[2]Mercedes-Benz Group, “Biometric Vehicle Access Innovation,” group.mercedes-benz.com Because each installed sensor forms a gating mechanism for premium features such as mobile payments, driver profiles, and car-sharing keys, component attach rates remain resilient even during macroeconomic softness.

Regulatory push for stronger eID and ePassport programs in Europe

Revised EU Regulation 910/2014 obligations require dual fingerprint enrollment for new ID cards, prompting procurement waves across Bulgaria, Portugal, and other early movers. The programs reference ISO/IEC 19794-2 templates, rewarding suppliers with pre-certified algorithms and hardware that simplify member-state approval cycles. Estonia’s e-Residency expansion already exceeds 120,000 digital IDs, providing a recurring replacement cycle every five years that locks in service revenue. As cross-border wallet interoperability matures, ministries in smaller countries are gravitating toward similar specs to ensure mutual recognition, forming a feedback loop that boosts volumes across the full European fingerprint sensor market.

Growing demand for contactless payments and smartcards

Transaction caps for PIN-less payments were increased to EUR 50 in many EU markets following the pandemic; banks are now deploying on-card fingerprint sensors to maintain Strong Customer Authentication while preserving tap-and-go convenience. Partnerships such as Fingerprint Cards-Infineon unify the sensor, secure element, and microcontroller, creating turnkey modules for card OEMs. With more than 30 live commercial card programs in 2024, issuers are highlighting lower fraud losses and faster checkout times, which incentivize further rollouts into transport and closed-loop retail ecosystems. Visa and Mastercard certifications reduce risk for smaller banks, expanding total demand.

Integration of multimodal biometric fusion in border-control kiosks

Airports in Frankfurt, Schiphol, and Manchester have converged on kiosks that combine fingerprint, face, and document checks, reducing the per-passenger transaction time from 45 seconds to 12 seconds while maintaining 99.7% verification accuracy. Fingerprint sensors in this environment must withstand temperature fluctuations, glove residue, and thousands of daily touches. IDEMIA and other integrators prefer large-area, polymer-coated modules that retain image fidelity across millions of cycles. As air-side throughput improves, similar kiosks are now appearing at ports, rail terminals, and government offices, thereby widening the installation counts throughout the European fingerprint sensor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from face and iris recognition modalities | -1.8% | Western Europe, especially corporate access control | Short term (≤ 2 years) |

| Semiconductor component shortages | -2.3% | Automotive and IoT segments across Europe | Medium term (2-4 years) |

| Heightened privacy-by-design encryption needs | -1.5% | Germany, France, Netherlands | Long term (≥ 4 years) |

| Declining ASPs amid ODM commoditisation | -1.7% | Consumer electronics channels region-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from face and iris recognition modalities

Contactless preferences that surged during COVID-19 prompted enterprises to retrofit doors and turnstiles with facial readers costing below EUR 500 per endpoint, substantially less than fingerprint-based kits after installation labor.[3]European Union Agency for Cybersecurity, “Biometrics Security and Privacy Guidelines,” enisa.europa.eu Yet GDPR compliance imposes stricter consent and data minimization demands on continuous facial capture versus voluntary fingerprint scans, triggering extra data-protection-impact assessments. As a result, many facility managers adopt a dual system whereby fingerprint remains the high-assurance factor for regulated zones, while face serves as a convenience factor for the lobby. This coexistence limits full displacement but still trims unit sales growth in traditional access-control corridors of the European fingerprint sensor market.

Semiconductor component shortages disrupting supply chains

Lead times for analog front-end chips and secure microcontrollers exceeded 20 weeks in 2024, delaying automotive launches and forcing some OEMs to downgrade to less advanced sensor SKUs. Smaller European fabless firms, lacking volume leverage, have pivoted to broker channels or redesigns that remove scarce components, moves that stretch engineering budgets and time-to-market. While macro inventory corrections are underway, elevated demand for ADAS and 5G radios continues to consume wafer capacity, implying partial relief only after 2026 and capping upside scenarios for the European fingerprint sensor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Ultrasonic Technology Drives Premium Growth

Capacitive devices retained the lion’s share at 34.72% in 2025, reflecting mature tooling, broad package options, and stable yields that suit price-sensitive smartphones and tablets. In contrast, ultrasonic sensors are scaling at a 13.12% CAGR, leveraging their ability to image through up to 4 mm of OLED glass while rejecting spoof attempts via liveness detection. This performance upgrade enables original equipment manufacturers to market waterproof phones without compromising unlock speed, thereby supporting the European fingerprint sensor market’s premium tier. Optical sensors remain in demand for enhanced forensic-image resolution in border kiosks, yet their thicker module height limits their usage in slim wearables. Thermal-based parts serve ruggedized industrial kiosks that must survive dust, grease, and outdoor moisture; although niche, these deployments carry superior unit margins that cushion vendors against ASP erosion elsewhere.

The European fingerprint sensor market continues to bifurcate along cost and specification lines. Ultrasonic dice are expected to migrate into mid-range handsets between 2026 and 2027 as yield learning curves and new 6-inch panel integrations lower module costs. Capacitive makers defend their installed base with wafer-level chip-scale packaging and AI-enhanced image reconstruction, which shrinks silicon area without compromising accuracy. The net result is a coexistence scenario in which each sensing modality commands distinct verticals: ultrasonic for banking, premium phones, and automotive; capacitive for mass-market electronics; optical for government; and thermal for mission-critical industrial use cases, thereby broadening the Europe fingerprint sensor market addressable revenue pool for specialized suppliers.

By Application: IoT Expansion Accelerates Beyond Mobile

Smartphones and tablets accounted for 43.22% of 2025 shipments, supported by operating-system-native biometric APIs that make fingerprint enrollment seamless for end-users. However, the IoT devices and other applications bucket is forecast to expand at a rapid 14.23% CAGR through 2031, driven by smart locks, connected thermostats, and industrial gateways that require secure local access. European smart-home integrators such as ekey have already installed more than 50,000 biometric door systems in Alpine climates, validating sensor ruggedness at sub-zero temperatures. Laptops remain a steady 10-12% slice of demand, anchored by Microsoft’s Windows Hello certification and enterprise multifactor mandates.

Developers in Austria and the Netherlands are trialing combined door-access and payment functionality on a single smart card, signaling a future convergence where one embedded fingerprint die supports multiple applets, thereby lowering per-function costs. Such multi-role innovation is crucial for sustaining unit growth when smartphone attachment rates plateau.

By End-user Industry: Government Digitization Outpaces Private Sector

Although consumer electronics accounted for 48.15% of 2025 revenue, the government vertical is projected to grow at the fastest rate, with a 13.35% CAGR through 2031, as ID card refresh cycles, ePassport rollouts, and police mobile-identity kits proliferate. Portugal’s Citizen Card program alone mandates fingerprint enrollment for over 10 million residents and synchronizes with Brussels-driven wallet frameworks. BFSI adoption is fueled by the Strong Customer Authentication (SCA) rules under PSD2, which direct banks to adopt possession-plus-inherence factors for high-value transactions. Military and defense remain lower-volume but higher-priced, demanding conformal-coated assemblies that withstand salt spray, shock, and electromagnetic interference on forward-deployed hardware.

The healthcare and automotive segments are also deepening their integration, utilizing fingerprints for patient chart pull-ups and driver profile personalization in luxury vehicles. These diverse niches produce smaller but premium orders that offset headline ASP compression in the phone market. Consequently, suppliers with modular IP easily re-spin form factors to win deals across sectors, establishing a resilient revenue mix for the European fingerprint sensor market.

By Sensor Placement: In-display Integration Transforms User Experience

In-display installations captured a 35.64% share in 2025 by blending larger touch areas with the aesthetic imperative of bezel-less phones. The European fingerprint sensor market is now witnessing a swift 13.84% CAGR rise in side-mounted buttons, particularly in rugged hand-helds and mid-priced Android devices, where integration simplicity trims tooling costs while preserving one-handed accessibility. Rear-mounted and front-mounted modules stay relevant in entry-level handsets and legacy enterprise laptops that prize repairability over sleek design.

Technology trade-offs include display backlight leakage, which can distort optical readings, electromagnetic coupling during wireless charging, and alignment challenges that arise when device frames shrink below 7 mm. Sensor vendors have introduced acoustic dampening layers and adaptive image reconstruction algorithms to mitigate these issues, keeping user rejection rates below 0.5%. Looking ahead, multilayer display stacks with embedded polarizers will enable even thinner under-panel ultrasonic sensors, paving the path for foldable phones and rollable screens within the European fingerprint sensor market.

Geography Analysis

Germany’s commanding 18.73% share reflects synergies between its automotive titans and industrial automation leaders, who embed fingerprint security into both vehicles and smart factory lines. Mercedes-Benz equips new luxury sedans with door-pillar sensors that tie driver identity to seat positions, infotainment profiles, and data keychains, ensuring a personalized experience while preventing theft. On the plant floor, fingerprint-gated human–machine interfaces safeguard proprietary robotics code, fulfilling Industry 4.0 cybersecurity audits. Domestic component ecosystems reduce procurement friction and enable German integrators to prototype swiftly, reinforcing the country’s competitive lead in the European fingerprint sensor market.

Italy is moving forward rapidly under the EUR 191.5 billion National Recovery and Resilience Plan, which allocates substantial funds for digital public services. Municipalities digitize citizen interactions, tax portals, health records, and transport passes, requiring on-device fingerprint checks that respect GDPR minimization. Italian POS vendors bundle certified sensors into next-generation payment terminals, helping banks like UniCredit phase out the use of signature slips and card PINs. This synchronized top-down funding and bottom-up fintech uptake propels Italy to the fastest CAGR of 12.89% in the region.

Elsewhere, the United Kingdom utilizes its fintech sandbox to pilot fingerprint-on-card authentication for subscription services and commuter rail passes, while France allocates defense spending to ruggedized sensors for secure facilities. Spain modernizes social-security kiosks, and the Netherlands pioneers distributed identity wallets that link universities, insurers, and municipalities. Sweden’s cashless culture experiments with biometric wearables for clinic check-ins. Finally, market potential in Russia remains latent due to supply chain restrictions, although domestic banks continue to roll out fingerprint ATMs. Combined, these varied national agendas underpin steady growth across the broader European fingerprint sensor market.

Regulatory Landscape

Fingerprint sensing deployments in Europe operate under the General Data Protection Regulation (GDPR, Regulation (EU) 2016/679). Because biometric data used to uniquely identify a person (including fingerprints) is treated as special category data, many commercial and public-sector use cases depend on explicit consent, substantial public interest, or other defined exemptions. In payments, Strong Customer Authentication under Commission Delegated Regulation (EU) 2018/389 reinforces controls around inherence-based authentication, which raises baseline expectations for secure sensor integration and template protection across biometric cards, terminals, and mobile payment flows.

Product compliance is also shifting toward horizontal cybersecurity obligations. The Cyber Resilience Act (Regulation (EU) 2024/2847) sets cybersecurity requirements for products with digital elements, including biometric readers and identity or access components that embed software and connectivity. For border and travel identity systems, Commission Implementing Decision (EU) 2019/329 for the Entry/Exit System (EES) references fingerprint quality and enrollment requirements, including NIST Fingerprint Image Quality (NFIQ 2.0 or newer), shaping performance and robustness criteria for sensors used in kiosks and enrollment stations. In February 2026, CEN-CENELEC work (CEN/TC 224 WG 17) also pointed to ongoing efforts on harmonized cybersecurity requirements for identity management systems and biometric readers to support CRA-aligned conformity and procurement specifications.

Value Chain Analysis

The Europe fingerprint sensor value chain covers algorithm and sensor IP development, semiconductor fabrication, module packaging and test, device integration, and distribution into end markets such as consumer electronics, smartcards and payments, government IDs, and industrial and automotive access. European players are most visible in R&D, product definition, and higher-assurance system integration, with firms such as Fingerprint Cards AB (Sweden), IDEX Biometrics (Norway), Thales (France), Dermalog Identification Systems (Germany), Jenetric (Germany), STMicroelectronics (Switzerland/France), and IDloop (Germany) supporting certified and vertical-specific solutions for regulated deployments.

High-volume wafer fabrication and back-end assembly for many sensor modules remain concentrated outside Europe, notably in Taiwan, South Korea, and the United States, with packaging and test in China and parts of Southeast Asia. This structure keeps import dependency and component allocation as an ongoing constraint, particularly for secure microcontrollers and analog front ends. Within Europe, logistics and redistribution play an outsized role, with the Netherlands (Rotterdam) acting as a hub for inbound modules and onward shipments to consuming markets such as Germany and France. Channel access and inventory reach are reinforced through authorized distribution, including Fingerprint Cards AB expanding its global distribution partnership with Future Electronics in November 2024 to support broader EMEA coverage for embedded and industrial design-in activity.

Competitive Landscape

Competition in the European fingerprint sensor market is moderate. Nordic incumbents Fingerprint Cards and IDEX Biometrics benefit from their early familiarity with the General Data Protection Regulation (GDPR) and Common Criteria certifications, which appeal to government bid evaluators. Their proximity to European standards bodies accelerates compliance updates, providing a time-to-market advantage as eID frameworks evolve. Asian contenders such as Goodix, Egis, and Synaptics focus on high-volume consumer electronics, leveraging cost leadership from large-scale back-end packaging lines in Shenzhen and Suzhou.

Technology roadmaps diverge along specialization lines. Qualcomm and Goodix dominate ultrasonic nodes, sustaining temporary performance moats through the use of proprietary transducer materials and beam-forming firmware. Conversely, STMicroelectronics and Infineon pursue vertical integration, embedding fingerprint matrices atop secure microcontroller wafers to deliver single-SKU turnkey solutions for smartcards and IoT nodes. NEXT Biometrics differentiates itself through large-area, flexible sensors that capture FBI FAP-20 and FAP-30 certifications, winning orders for passport readers and point-of-sale systems.[4]Finansavisen, “NEXT Biometrics Receives NOK 6.3 Million Purchase Order,” finansavisen.no

Strategic moves in 2025 highlight ecosystem building. Fingerprint Cards partnered with jNet on system-in-package modules that shorten design cycles for embedded security appliances. Anonybit collaboration introduces decentralized biometric storage designed for single-sign-on deployment in enterprises. Meanwhile, NEXT Biometrics launched a compact sensor that simplifies integration in ID cards and ATMs, signaling a push toward volume government deals. The cumulative effect of such partnerships fosters middleware interoperability, providing buyers with multiple certified building blocks and further stimulating adoption across the European fingerprint sensor market.

Europe Fingerprint Sensor Industry Leaders

Fingerprint Cards AB

STMicroelectronics NV

Synaptics Incorporated

Guangdong Goodix Technology Co., Ltd.

IDEMIA France SAS

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-led product differentiation is a clear whitespace area as the Cyber Resilience Act (Regulation (EU) 2024/2847) raises minimum cybersecurity expectations for biometric readers and identity or access products that include software, connectivity, and update mechanisms. That direction shifts opportunity toward suppliers that can bundle secure elements, template protection, and lifecycle vulnerability management into a more complete offering, rather than competing primarily on sensor bill-of-materials. It also aligns with procurement behavior in regulated government, BFSI, and transport environments.

Interoperability and standardization work further supports new design-in paths across countries and verticals. CEN/TC 224 activity on identification and biometric-related standards, alongside coordination forums such as the European Association for Biometrics (EAB), provides a basis for common specifications that can reduce re-qualification friction for eID, border-control kiosks, and payment credential programs. On the demand side, fingerprint-enabled payments and terminals already show traction in completed deployments, including more than 30 live commercial biometric card programs in 2024 (as referenced in the report context). Industry partnerships that package sensors with secure components for card OEMs, including Fingerprint Cards and IN Groupe/SPS working with the STMicroelectronics STPay-Topaz-Bio chipset for contactless biometric cards, also strengthen the case for wider rollout in closed-loop transport, campus ID, and enterprise access credentials where certification and turnkey integration reduce adoption barriers.

Recent Industry Developments

- March 2026: Fingerprint Cards AB became the first biometric company to pass EMVCo's new biometric assessment for payment card sensors, aligned to standards released in November 2025. The milestone strengthens its position with card manufacturers and issuers that prioritize independently assessed performance and security for biometric payment cards, raising the competitive bar for payment-focused sensor suppliers.

- November 2025: Synaptics Incorporated entered a strategic engagement with Qualcomm Technologies to advance touch and fingerprint technologies across PC and mobile platforms. The collaboration targets tighter hardware and software integration for OEM reference designs, helping streamline supplier qualification and accelerating adoption of combined touch-and-biometric user interfaces in high-volume devices.

- July 2024: Fingerprint Cards AB and IN Groupe (through its SPS brand) launched a secure component solution for contactless biometric cards using the STMicroelectronics STPay-Topaz-Bio chipset. The packaged approach reduces integration complexity for card OEMs by combining secure elements and biometric functionality, supporting broader rollout of fingerprint-on-card authentication in payments and adjacent credential programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from fingerprint sensors sold and integrated across Europe for user identification and authentication in devices, cards, and access systems.

Scope exclusions: We exclude non-fingerprint biometric modalities, and we do not treat finished consumer devices as the market when they only contain a sensor component.

Segmentation Overview

- By Sensor Type

- Optical

- Capacitive

- Thermal

- Ultrasonic

- By Application

- Smartphones and Tablets

- Laptops

- Smartcards

- IoT Devices and Other Applications

- By End-user Industry

- Military and Defence

- Consumer Electronics

- Banking, Financial Services and Insurance (BFSI)

- Government

- Other End-user Industries

- By Sensor Placement

- Front-mounted

- Rear-mounted

- Side-mounted

- In-display

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Sweden

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to align definitions for Europe, because the same sensor can be described as a component, a module, or a feature. We reviewed public sources such as Eurostat for macro indicators, the European Commission for digital identity and security initiatives, and ENISA publications for authentication and cyber risk context.

To translate demand into a practical sizing view, we also referenced sources such as ITU and OECD digital adoption statistics, plus publicly available customs and trade tables that show electronics and component flows into Europe. Company annual reports, investor decks, and reputable press were checked for product focus and shipment momentum, and we used paid subscriptions for company financials and patent databases to verify product direction. The sources listed here are illustrative, and other public documents and references were used during data collection and cross-checking.

Primary Interviews and Surveys

Primary work focused on validating what is actually shipped in Europe and how pricing moves by sensor type and placement, for example in-display versus rear. We spoke with component suppliers, device and smartcard ecosystem participants, and buyers in consumer electronics, government programs, and security related deployments across APAC, EMEA, and the Americas to pressure-test assumptions and close data gaps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | |

| Mid tier: 45% | Functional/Unit leaders: 38% | |

| Smaller Players: 21% | Managers: 49% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs Europe demand using device and card deployment pools, then applies fingerprint adoption rates by application, followed by an estimated sensor content per unit. After forming that demand pool, we corroborate it with selective bottom-up checks, such as sampled ASP times shipment volumes for key application groups and channel feedback on mix shifts, so totals can be adjusted when the two views diverge.

Key inputs used in the model include smartphone and tablet shipment direction, laptop penetration of biometric login, smartcard issuance and upgrades for identity and payment use, the split of sensor placement (in-display, side-mounted, rear and front), and the technology mix (capacitive, optical, ultrasonic, and thermal). Pricing assumptions are handled through observed mix change and realistic ASP erosion, rather than a flat price drop, since in-display and ultrasonic designs behave differently. For forecasting, we used scenario analysis supported by short trend lines on major input drivers, and the final path was confirmed through expert consensus on adoption pacing and procurement cycles. Where country level splits were incomplete, shares were bridged using proxy indicators such as device demand concentration and public program intensity, and then normalized back to the Europe total.

Data Validation & Update Cycle

Outputs are validated through multiple checks, including comparing implied sensor shipments against the application demand pools and reviewing whether ASP and mix moves are consistent with what interviews indicate. When large variances show up, assumptions are revisited and, if needed, respondents are re-contacted to clarify what changed, for example a shift from capacitive to in-display optical in a major device cycle.

Before sign-off, the model is reviewed in steps, with a separate pass for arithmetic accuracy, definition consistency, and country roll-up logic. Reports are refreshed annually, and interim updates are done when a material event affects demand, supply, or pricing. Right before delivery, a final update sweep is carried out so the view reflects the latest public signals and validated inputs.

Mordor Intelligence's Europe Fingerprint Sensor Market Market Sizing Compared With Other Published Estimates

Published market values for fingerprint sensors in Europe can differ more than expected, even when the growth story sounds similar. Most gaps come from how each publisher defines what is being counted, which year is treated as the base, and how pricing and mix change are carried into the forecast.

Some sources narrow scope to only a couple of sensor types or limit the technology discussion to touch and swipe styles, which can compress the starting value. The table shows that spread clearly, and Mordor Intelligence counts Europe revenues across major sensor types and placements, then ties the totals back to device and card demand pools before the forecast is finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.48 B (2025) | |

| Regional Consultancy A | USD 1.80 B (2024) | Uses an earlier base year and a narrower segment view that emphasizes limited sensor types and simplified technology buckets, with fewer explicit checks on placement mix and smartcard related demand. |

| Trade Journal B | USD 2.00 B (2026) | Focuses on the European Union and uses a module-level framing in the narrative, which can shift what gets counted and can also change the price assumption timing versus a broader Europe roll-up. |

Overall, the gap is mainly explained by geography choice (EU versus wider Europe), the sensor and application scope that gets included, and how ASP progression is updated across the mix. By anchoring the model to observable demand pools and then stress-testing with pricing and mix checks, we keep the final figure traceable and repeatable.

Key Questions Answered in the Report

How large is the Europe fingerprint sensor market in 2026?

The Europe fingerprint sensor market size is USD 2.79 billion in 2026, with a forecast to hit USD 5.01 billion by 2031.

Which sensor technology is growing fastest?

Ultrasonic sensors are advancing at a 13.12% CAGR thanks to in-display smartphone adoption and high-security payment use cases.

Why is Italy showing the highest growth rate?

Italy benefits from National Recovery and Resilience Plan funds that finance eID rollouts, smart-city projects, and biometric payment pilots, resulting in a 12.89% CAGR.

What is driving fingerprint use in banking cards?

Banks are deploying biometric smartcards to meet PSD2 Strong Customer Authentication while keeping contactless transaction flows smooth.

How are semiconductor shortages affecting suppliers?

Lead times for critical analog front ends stretch beyond 20 weeks, forcing redesigns and delaying launches in automotive and IoT lines.

Which companies dominate government procurements?

Nordic firms Fingerprint Cards and IDEX Biometrics lead due to Common Criteria certifications that align with EU ePassport and eID specifications.

Page last updated on: