Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

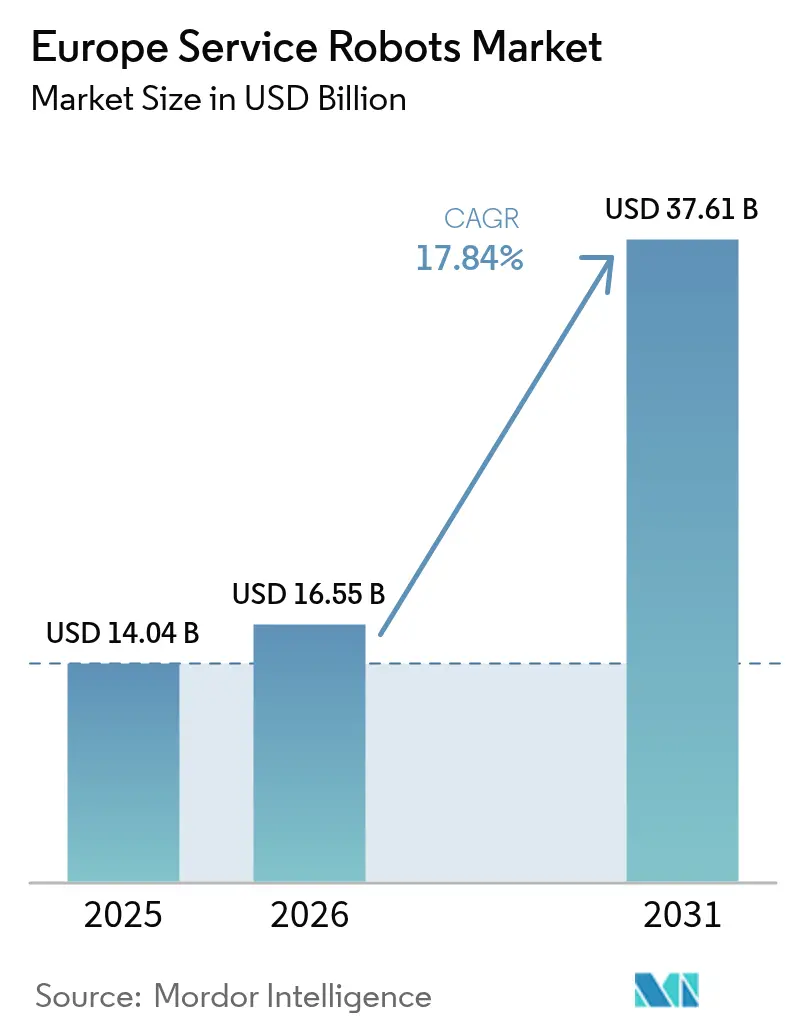

| Base Year Market Size (2025) | USD 14.04 Billion |

| Market Size (2026) | USD 16.55 Billion |

| Market Size (2031) | USD 37.61 Billion |

| Growth Rate (2026 - 2031) | 17.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Service Robots Market Analysis by Mordor Intelligence

The Europe service robots market size is expected to grow from USD 14.04 billion in 2025 to USD 16.55 billion in 2026 and is forecast to reach USD 37.61 billion by 2031 at 17.84% CAGR over 2026-2031. The growth path is propelled by policy-backed automation programs, large-scale demographic shifts, and expanding e-commerce networks that collectively accelerate capital spending on autonomous systems. Strategic EU funding of nearly EUR 500 million (USD 548 million) under Horizon Europe has de-risked R&D for robotics start-ups and deep-tech suppliers, while labor shortages exceeding 1 million vacancies in health, hospitality, and logistics continue to tighten wage structures and sharpen the return-on-investment logic for robotic deployments. Professional platforms currently dominate the Europe service robots market through their proven ability to replace repetitive manual tasks in warehouses, hospitals, and farms, yet the personal segment is scaling rapidly as aging-in-place initiatives create budget lines for socially assistive devices.

Key Report Takeaways

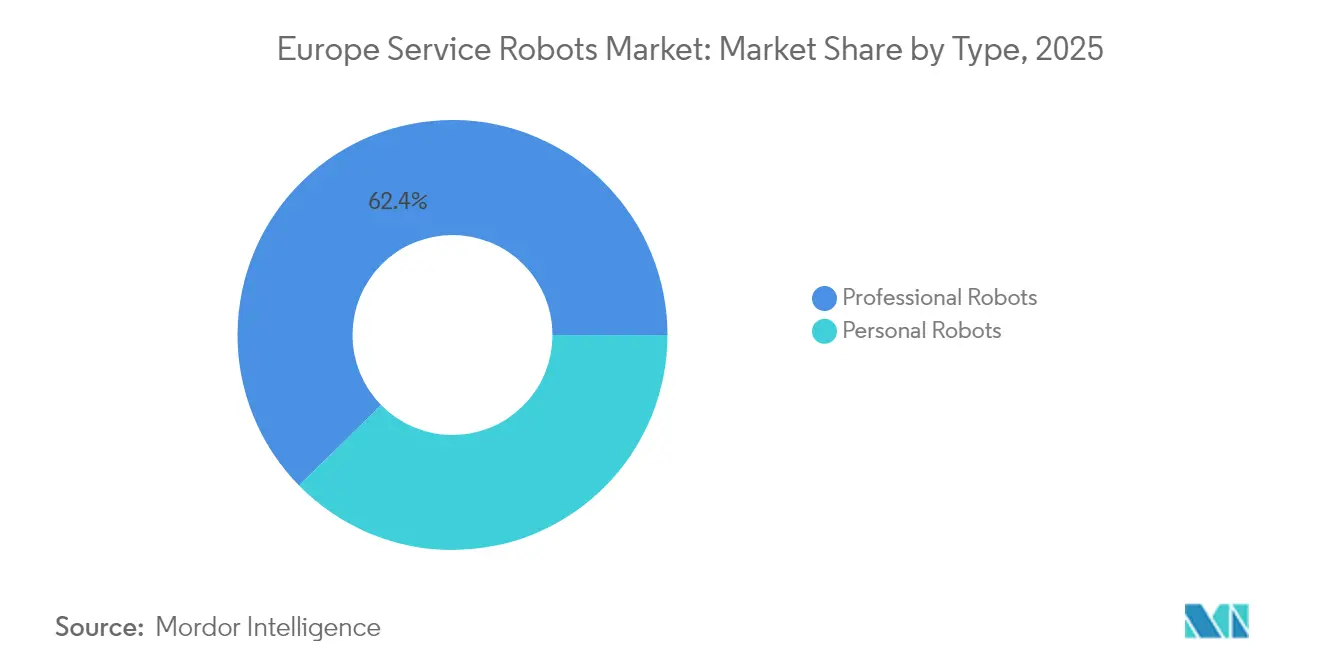

- By type, professional robots held 62.35% of the Europe service robots market share in 2025, while the personal segment is forecast to post a 19.21% CAGR through 2031.

- By operating environment, ground systems captured 70.25% revenue share in 2025; aerial systems are projected to climb at a 20.97% CAGR to 2031.

- By component, software accounted for 37.80% of the Europe service robots market size in 2025 and is expanding at an 18.32% CAGR.

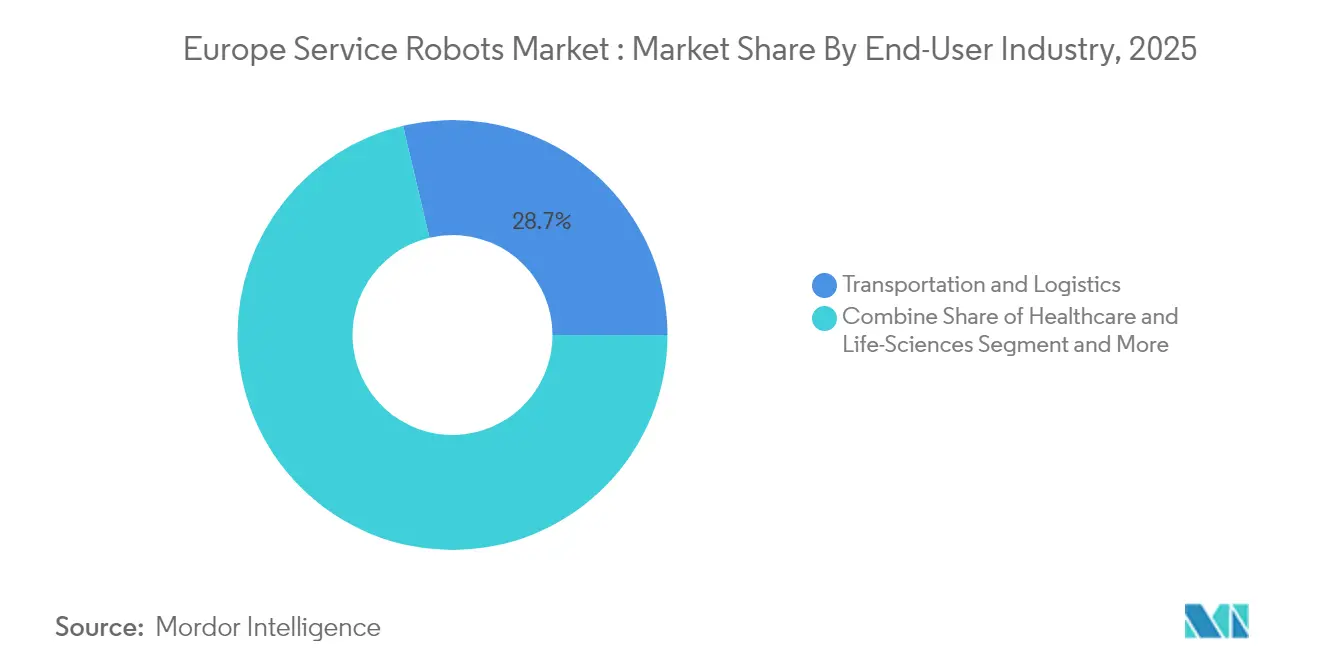

- By end-user industry, transportation and logistics led with 28.70% revenue share in 2025; agriculture is advancing at a 19.80% CAGR through 2031.

- By geography, Germany commanded 27.10% of the Europe service robots market share in 2025, whereas Spain is the fastest-growing national market at a 18.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Service Robots Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid labour-shortage-driven demand for AMRs in logistics & grocery fulfilment | 4.20% | Germany, Netherlands, France | Short term (≤ 2 years) |

| EU “Farm to Fork” subsidies accelerating agri-robot adoption | 3.80% | Spain, France, Italy, Netherlands | Medium term (2-4 years) |

| Hospital infection-control protocols boosting UV-C disinfection robots | 2.90% | Germany, France | Short term (≤ 2 years) |

| Ageing-in-place policies spurring elder-care companion robots | 3.10% | Germany, Italy, Finland, Denmark | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Labour-Shortage-Driven Demand for AMRs in Logistics & Grocery Fulfilment

E-commerce volumes continue to outpace available warehouse labor, pushing third-party logistics providers toward aggressive adoption of autonomous mobile robots. DHL expects 30% of its material-handling assets to be robotic by 2030, a position echoed by Toyota Material Handling Europe, which confirms that 24/7 uptime imperatives are no longer negotiable and human-only workflows are uneconomical. German integrators such as Movu Robotics are securing multi-site contracts that bundle storage, picking, and pallet transport modules into unified automation stacks, allowing retailers to compress order-to-ship cycles even during seasonal labor crunches. Investment appetite remains strong as robotics leasing and robots-as-a-service arrangements lower balance-sheet risk for mid-sized operators. The result is a structurally higher baseline for autonomous deployments in the Europe service robots market. [1]DHL, Source: DHL, “Indoor Mobile Robots,” dhl.com

EU “Farm to Fork” Subsidies Accelerating Agri-Robot Adoption

The European Commission’s EUR 30 million (USD 32.9 million) AgrifoodTEF program offers test beds and advisory services that speed certification for agricultural robots, translating policy into tangible capital projects on Spanish, French, and Dutch farms. Vineyard operators in Spain report energy use of 1.42 kWh/h for electric tracked weed-removal robots, proving economic viability against fuel-powered tractors. Germany’s robotics association notes measurable drops in soil compaction and emissions when lightweight field robots replace tractors, creating an environmental co-benefit that appeals to regulators and investors alike. Subsidy certainty through 2027 has pulled orders forward, lifting visibility in manufacturer order books and reinforcing the Europe service robots market’s pivot toward outdoor applications.[2]Digital Strategy, Source: European Commission, “AI Testing and Experimentation Facilities: AgrifoodTEF,” digital-strategy.ec.europa.eu

Hospital Infection-Control Protocols Boosting UV-C Disinfection Robots

COVID-era hygiene benchmarks have been codified into permanent hospital procurement policies, with NHS England targeting 500,000 robotic-assisted operations annually by 2035 and specifying UV-C systems as standard equipment in new facilities. French hospitals demonstrate how UV robots integrate with humanoid navigation assistants, reducing pathogen load while guiding patients and collecting environmental data for facility managers. Regulatory agencies now link capital grants to infection-control metrics, ensuring steady demand for sanitary automation across public and private healthcare networks. The driver pushes professional-grade mobile platforms further into the Europe service robots market, solidifying healthcare as a multi-year growth vertica. [3]NHS England, Source: NHS England, “Millions to benefit from NHS robot drive,” england.nhs.uk

Ageing-in-Place Policies Spurring Elder-Care Companion Robots

With 35% of Europeans projected to be older than 60 years by 2065, Ministries of Health are redirecting budget lines toward technologies that extend independent living. Projects such as ACCRA emphasize co-creation workshops that embed senior feedback into robot design, raising acceptance of devices that offer medication reminders, fall detection, and social engagement. Nordic pilot studies show willingness-to-pay increases when users participate in feature prioritization, underscoring the importance of participatory design in accelerating adoption. Public insurers in Germany and Finland are now reimbursing select assistive functions, removing an economic barrier for households and reinforcing personal-robot demand within the Europe service robots market

Restraints Impact Analysis of Europe Service Robots Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented safety standards delaying multi-country roll-outs | -2.10% | EU-wide | Medium term (2-4 years) |

| Persistent public scepticism over autonomous systems in heritage city centres | -1.40% | Italy, France, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Safety Standards Delaying Multi-Country Roll-Outs

The transition from the Machinery Directive to the new Machinery Regulation and the simultaneous introduction of the AI Act create a patchwork of certification hurdles. Manufacturers must perform redundant conformity assessments that lengthen development cycles and increase compliance costs. ISO 13482’s pending revision adds another moving target, while TÜV-certification bottlenecks slow time-to-market for SMEs. An EU-level Service Desk is planned for 2025, yet the interim uncertainty curbs the scale-up ambitions of pan-European fleets, tempering the otherwise strong trajectory of the Europe service robots market

Persistent Public Scepticism Over Autonomous Systems in Heritage City Centres

Historic urban layouts impose strict spatial constraints that challenge robot navigation and raise concerns about cultural preservation. Local authorities in Florence, Barcelona, and Lyon require extensive pilot testing and community consultations before granting operating permits, elongating payback periods for service providers. Studies by the Robotics4EU project reveal that perceived job displacement and safety fears among residents slow municipal adoption, particularly where tourism economies are sensitive to technological intrusion. This social-acceptance gap reduces deployment density in prime city-centre districts, sidelining potential volume for delivery and cleaning robots in the Europe service robots market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Service Robots Market Segment Analysis

By Type:

Professional Dominance Drives Current RevenueProfessional robots generated 62.35% of 2025 revenue, confirming their status as the economic backbone of the Europe service robots market. Uptake is concentrated in logistics, healthcare, and agriculture, where quantifiable savings on labor and uptime deliver rapid payback. The Europe service robots market size for professional platforms is forecast to expand in sync with fleet expansion programs at 3PLs and hospital chains, supported by robots-as-a-service contracts that shift spending from CapEx to OpEx. Software-centric moves by KUKA underline how incumbents are wrapping value-added analytics around hardware, a trend that reinforces switching costs for enterprise clients.

Personal robots remain a minority in absolute dollars yet emerge as the fastest-growing slice at 19.21% CAGR through 2031. Aging-in-place subsidies, falling component prices, and cloud connectivity create favorable economics for mobile assistants that handle routine chores and social interaction. Pilot data from Nordic programs confirm that care-robot usage cuts caregiver visits by 12% without compromising patient outcomes, offering fiscal relief for national health budgets. As social-acceptance studies progress, the Europe service robots market will likely witness a demand curve that mirrors the smartphone diffusion cycle rather than industrial automation pacing.

By Operating Environment:

Ground Systems Lead While Aerial Applications SurgeGround robots captured 70.25% of 2025 sales, reflecting regulatory maturity and proven ROI in structured indoor settings. Warehouses, hospitals, and hotels provide controlled environments where AMRs can leverage SLAM navigation with limited risk, ensuring predictable throughput gains. The Europe service robots market size associated with ground deployments continues to grow as retailers convert brownfield sites into automated micro-fulfilment hubs.

Aerial platforms, however, post a 20.97% CAGR on the back of infrastructure inspection and precision-agriculture use cases. BVLOS exemptions and the rollout of 5G standalone networks furnish the bandwidth and regulatory clarity needed for routine unmanned flights over power lines, pipelines, and crop fields. German utilities estimate that drone-based inspections cut outage-related penalties by 15%, creating a compelling TCO narrative. As risk-based SORA frameworks harmonize across member states, aerial volumes are expected to carve out an increasingly material share of the Europe service robots market.

By Component:

Software Leadership Reflects AI IntegrationSoftware logged 37.80% of 2025 component revenue, driven by fleet-orchestration layers, vision algorithms, and predictive-maintenance dashboards. The Europe service robots market share attributable to AI stacks is set to widen as manufacturers open APIs and monetize data streams. Cloud-native platforms such as KUKA’s mosaixx enable multi-vendor interoperability, letting integrators stitch heterogeneous fleets into unified dashboards.

Hardware remains critical, yet commoditization pressures shift margin capture toward code. Sensor fusion leveraging LiDAR, depth cameras, and mmWave radar enhances situational awareness, but the long-term differentiator is continuous-learning software that improves path planning with every mission. Edge AI chips cut latency and bandwidth costs, further consolidating the software-first value hierarchy in the Europe service robots market.

By End-User Industry:

Logistics Leads While Agriculture AcceleratesLogistics and transportation retained 28.70% revenue share in 2025 as parcel volumes pushed fulfilment centres beyond human throughput limits. The Europe service robots market size for logistics reflects both greenfield automated warehouses and retro-fits using modular AMRs. Operators report 35% productivity gains and 20% error reductions after robot deployment, metrics that underpin board-level funding for automation roadmaps.

Agriculture, although accounting for a smaller base, is expanding at a 19.80% CAGR, elevated by subsidy certainty and measurable sustainability benefits. EU climate targets motivate farmers to adopt autonomous weeders and precision sprayers that lower herbicide use by up to 70%. Pilot projects prove that ROI timelines fall below 36 months, even for mid-scale vineyards, moving robotics from experimental trials to mainstream capital budgeting across southern Europe.

By Component:

Power Systems Innovation Drives EfficiencyLithium-ion supply volatility and raw-material cost inflation steer OEMs toward energy-management breakthroughs. Swappable battery trays, regenerative braking on AMRs, and adaptive charging algorithms extend mission duration while lowering total cost of ownership. With power representing 22% of lifetime operating expense for mobile robots, incremental efficiency gains translate directly into adoption headroom for the Europe service robots market.

Control systems advance simultaneously, with real-time kernels and redundant safety layers meeting stricter cybersecurity clauses in the new Machinery Regulation. Edge processing reduces cloud dependency, cutting data egress fees and improving operational resilience in bandwidth-constrained environments such as underground logistics tunnels and remote farms. The convergence of power efficiency and intelligent control forms a virtuous design loop that heightens performance benchmarks and accelerates fleet scaling.

Geography Analysis

Germany Service Robots Market

Germany anchored 27.10% of 2025 revenue, leveraging a dense supplier ecosystem and close policy-industry collaboration. Federal research grants and flagship initiatives such as AgrifoodTEF shorten commercialization timelines, while the automotive supply chain’s precision-engineering culture underpins high-quality robot manufacture. KUKA, Neura Robotics, and Bosch Rexroth collectively act as talent magnets, reinforcing a virtuous cycle of innovation and scale that cements national leadership in the Europe service robots market.

Spain Service Robots Market

Spain represents the fastest-growing geography at a 18.62% CAGR through 2031, underpinned by Mediterranean greenhouse intensification and a policy agenda that rewards sustainability metrics. Regional governments co-fund robotics pilots that tackle labor scarcity in fruit-picking and transplanting, with energy-efficient electric robots showing compelling field performance. Knowledge-transfer networks such as Hisparob foster SME participation, broadening the innovation base and driving volume growth that surpasses larger economies in relative terms.

Broader European Markets

France, Italy, the Netherlands, and Nordic countries collectively supply diversified demand streams. French hospitals adopt humanoid assistants for patient interaction, the Netherlands pilots autonomous barges and greenhouse robots, and Nordic welfare models allocate funding for social-assistive devices in senior housing complexes. Italy’s focus on heritage-conscious navigation algorithms and the UK’s push for surgical robotics enrich the regional mosaic, ensuring that the Europe service robots market benefits from complementary specializations rather than zero-sum competition.

Regulatory Landscape

The Europe service robots market operates within the EU product-safety and AI governance stack, where CE-marking obligations increasingly intersect with AI-specific controls. Regulation (EU) 2024/1689 (AI Act) entered into force on 1 August 2024 and follows a phased implementation schedule through 2 August 2027, bringing risk management, transparency, and data-governance requirements into scope for many AI-enabled service-robot functions.

On the hardware and functional-safety side, Regulation (EU) 2023/1230 (Machinery Regulation) replaces the Machinery Directive 2006/42/EC and becomes fully applicable from 20 January 2027. It tightens expectations for autonomous and safety-critical features and reinforces third-party conformity assessment where applicable. In parallel, updated safety requirements under ISO 10218-2:2025 shape integrator and OEM design files and test protocols, which affects how multi-country rollouts are planned and certified across Europe.

Value Chain Analysis

The Europe service-robot value chain covers component suppliers (sensors, semiconductors, batteries, actuators), electronics manufacturing services (EMS), robot OEMs, and software and AI stack providers (navigation, perception, fleet management). Downstream system integrators then assemble end-to-end deployments for logistics, healthcare, agriculture, municipal services, and hospitality. Interoperability and risk-assessment workstreams led by European standardization bodies such as CEN/TC 310, alongside the European Commission Rolling Plan for ICT Standardisation (robotics and autonomous systems), increasingly influence integration requirements and procurement checklists for buyers operating cross-border fleets.

Upstream constraints also feed into cost and lead times. Late-2025 industry surveys point to continued semiconductor procurement difficulty and broad-based component pricing pressure, while European EMS market contraction in 2024 highlights manufacturing capacity and productivity headwinds for local build-out. In this environment, specialized European integrators and ecosystem coordinators (for example, InnoScale and platform-oriented integration networks) help OEMs manage compliance, localization, and after-sales service across multiple European countries, especially when service robots are deployed beyond tightly controlled industrial settings.

Competitive Landscape

Incumbent industrial-automation champions such as KUKA, ABB, and Bosch are repositioning portfolios to capture service-sector adjacencies. KUKA’s creation of a software-first business unit signals management’s recognition that recurring revenue streams from digital services can cushion hardware cycle volatility. Strategic alliances with cloud providers and systems integrators create ecosystem moats that smaller hardware-only rivals struggle to breach.

Start-ups benefit from record venture flows, yet capital gravitates toward teams that own proprietary AI pipelines rather than mechanical designs alone. Norway’s 1X and Germany’s Neura Robotics exemplify this shift, closing nine-figure rounds on the strength of perception software and low-latency control stacks tuned for human-scale tasks. Corporate venture funds from automotive and logistics conglomerates increasingly co-invest, ensuring commercial pilots and scale pathways for promising newcomers.

Meanwhile, digital marketplaces for robot-as-a-service contracts emerge, lowering procurement friction for SMEs and boosting installed-base stickiness for OEMs. Portfolio breadth, software depth, and go-to-market agility now matter more than unit-cost leadership. As a result, the Europe service robots market is entering a consolidation phase where platform economics favor firms able to orchestrate multi-modal fleets across diverse use cases.

Europe Service Robots Industry Leaders

KUKA AG

iRobot Corporation

SoftBank Robotics Group

PAL Robotics

Starship Technologies

- *Disclaimer: Major Players sorted in no particular order

Europe Service Robots Market Companies Covered in this Report

- KUKA AG

- iRobot Corporation

- SoftBank Robotics Group

- PAL Robotics

- Starship Technologies

- Amazon Robotics

- Northrop Grumman Corporation

- DJI

- Parrot SA

- Blue Ocean Robotics

- Boston Dynamics

- ANYbotics

- Lely Holding

- SeaRobotics Corporation

- GeckoSystems Corporation

- RedZone Robotics

- Dyson Ltd.

- Robotnik Automation

- Husqvarna Group

- Robobuilder Co. Ltd.

Market Opportunities and Future Outlook

One near-term opportunity is compliance readiness paired with fleet-scale deployment. With the EU AI Act in force since 1 August 2024 and staged applicability through 2027, and the Machinery Regulation becoming fully applicable on 20 January 2027, buyers face tighter documentation and post-market control expectations for autonomous systems. That raises the value of OEMs and integrators that can package CE-aligned safety cases with AI governance artifacts (risk management, logging, human oversight) and provide repeatable deployment templates for multi-site logistics, hospitals, and municipal operators.

Publicly funded innovation and test infrastructure also continues to support commercialization in service robotics. Horizon Europe calls that target agile, intelligent, and modular robotics platforms for industrial and service applications (for example, 2026 work-programme calls hosted on CORDIS) create non-dilutive funding routes for European developers and consortia, supporting continued work on modular platforms, human-robot interaction, and real-world validation. On the demand side, enterprise buyers are operationalizing fleet orchestration and retrofit programs, while regulated cold-chain and healthcare environments pull edge AI and traceability features into robot deployments to meet temperature and hygiene compliance requirements.

Recent Industry Developments in Europe Service Robots Market

- July 2026: iRobot announced an expanded Roomba lineup, including Roomba Max 775 Combo and Roomba Max 715 Vacuum Robot, alongside additional compact models aimed at modern home layouts. The refresh broadens feature tiers and form factors for European consumers, reinforcing competitive intensity in personal service robots where software, docking automation, and space-efficient design are key differentiators.

- March 2026: iRobot launched the Roomba Mini robot vacuum and mop with AutoEmpty Dock in the United Kingdom and Europe. The smaller footprint targets constrained living spaces and supports retail channel momentum in Europe, where compact home robotics can increase adoption without requiring larger floor plans.

- June 2025: NHS England launched a nationwide program targeting 500,000 robotic-assisted surgeries per year by 2035. The program formalizes multi-year procurement and capability-building for clinical robotics, supporting demand visibility for surgical platforms, supporting software, and hospital workflow integration services across the UK.

Europe Service Robots Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the Europe service robots market is defined as revenues generated from service robots deployed in non-factory environments to perform useful tasks for people or equipment, across professional and personal use cases, within Europe.

Scope exclusions: Industrial robots mainly used for production-line automation, along with standalone components and accessories that are not sold as part of a service robot system, are not counted.

Segments Covered in This Report

- By Type

- Personal Robots

- Domestic

- Research & Education

- Entertainment

- Professional Robots

- Field (Agriculture, Forestry)

- Defense and Security

- Medical and Healthcare

- Logistics and Warehouse AMRs

- Others

- Personal Robots

- By Operating Environment

- Aerial (UAV/Drone)

- Ground / Land

- Marine and Underwater

- By Component

- Sensors

- Actuators

- Control Systems and Edge AI

- Software (Navigation, Vision, Fleet-Mgmt)

- Power Systems (Batteries, Fuel-cells)

- By End-User Industry

- Military and Defense

- Agriculture, Construction & Mining

- Transportation and Logistics

- Healthcare and Life-Sciences

- Government and Municipal Services

- Hospitality and Retail

- Others

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Sweden

- Denmark

- Finland

- Norway

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for Europe and to ensure the assumptions we used can be traced back to public signals. We referred to sources such as IFR publications, Eurostat datasets, national statistics offices, customs and trade data portals, and peer-reviewed papers that track service robotics use in areas like healthcare, logistics, agriculture, and defense.

To connect the market to real spending and deployments, we also reviewed company filings, annual reports, investor presentations, and credible press coverage for product launches and tender wins. In addition, we used approved paid subscriptions for company financials and intelligence, patents, and shipment-level import and export checks when clarification was needed on supply flow or installed base growth. The sources listed here are illustrative only, and other public references were also used for collection, cross-checks, and follow-up clarification.

Primary Interviews and Surveys

Primary work was done to pressure test desk assumptions and translate technical adoption into measurable demand for Europe. We spoke with a mix of OEM-side leaders, system integrators, distributors, and large end users across sectors such as hospitals, warehouses, farms, and public services, and then we normalized inputs to align with comparable revenue definitions.

Because adoption varies by country and use case, feedback was gathered across major European economies and smaller markets. We re-contacted relevant sources when model outputs did not match deployment cues or pricing direction.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | |

| Mid tier: 56% | Functional/Unit leaders: 27% | |

| Smaller Players: 19% | Managers: 59% |

Market-Sizing & Forecasting

Sizing starts from a top-down build that reconstructs demand by linking Europe-level adoption signals to spending pools by application, and then mapping that demand to service robot revenue capture. Inputs used in the model include indicators such as warehouse automation intensity, healthcare staffing pressure and procedure volumes, agriculture labor scarcity, defense and public-safety procurement activity, and observed ASP ranges by robot class and payload (including service and software bundled into system pricing when sold together).

After the top-down totals were formed, we corroborated them with selective bottom-up approximations such as sampled ASP x shipment volumes from public disclosures, channel checks on unit volumes, and supplier roll-ups for a limited set of robot categories where disclosure is clearer. When gaps appeared, such as limited visibility for small deployments or pilot projects, we applied adjustments using adoption rates and replacement cycles discussed in interviews so totals remained realistic and repeatable.

Forecasting was carried out using scenario analysis supported by simple multivariate relationships, and the drivers were kept practical for annual refresh. Assumptions were anchored to expected rollout pace, regulation and safety compliance timelines, and pricing progression discussed by industry participants, before the final forecast curve was signed off.

Data Validation & Update Cycle

Validation is done through cross-checks against independent signals, so the model does not rely on one data series. Outputs are compared with public shipment and deployment cues, country-level activity differences, and price-direction reality checks, and any large variances are flagged for a second analyst review.

If an anomaly is found, inputs are revisited and relevant primary sources are re-contacted to confirm whether it is a true market shift or a definition mismatch. The report is refreshed annually, and interim updates are made when there are material events that can change demand, pricing, or availability. Before delivery, a final pass is completed so clients receive the most current version available at that time.

Mordor Intelligence's Europe Service Robots Market Market Size Compared With Other Published Estimates

Different published estimates for Europe service robots can land far apart, even when the topic label looks similar. This typically happens because firms mix different robot categories, change what they count as revenue, or use different years and FX timing when converting regional totals.

Some external figures narrow the scope to AI-enabled service robotics only, and they also tend to include a wider technology stack view that can blur the line between a robot system and enabling software layers. In Mordor Intelligence modeling, revenue is counted for service robot systems sold into non-industrial use cases in Europe, and industrial production-line robots are kept out so the demand pool stays consistent.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.55 B (2026) | |

| Industry Analytics Group A | USD 3.35 B (2024) | Uses an AI service robotics lens, which narrows the counted robot pool and can separate AI software layers differently, and it is also anchored to an earlier year that reduces the comparable total. |

| Industry Analytics Group B | USD 21.25 B (2033) | Reports a longer-dated forecast endpoint with growth assumptions compounded further out, and the scope framing emphasizes AI capabilities that may pull in adjacent technology value beyond service robot system revenue. |

Taken together, the spread mainly comes from scope and timing, not from one simple math difference. By keeping the counted revenue tied to system sales in Europe and then cross-checking with adoption and pricing signals, the estimate stays transparent and easier to replicate year to year.

Key Questions Answered in the Report

What is the current value of the Europe service robots market?

The market is valued at USD 16.55 billion in 2026 and is forecast to reach USD 37.61 billion by 2031.

Which segment is growing fastest within the Europe service robots market?

Personal robots exhibit the highest growth, advancing at a 19.21% CAGR through 2031 due to aging-in-place policies.

How large is the Germany share of the Europe service robots market?

Germany accounted for 27.10% of regional revenue in 2025, leading all national markets.

What role does software play in the Europe service robots industry?

Software captured 37.80% of component revenue in 2025 and is critical for AI-driven perception and fleet management.

Page last updated on: