Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Location Intelligence Market is Segmented by Component (Software and Services), Solution Type (Geocoding and Reverse, Geocoding, and More), Location Type (Indoor and Outdoor), Deployment (Cloud and On-Premise), Application (Workforce Management, Asset Management and More), End-User Vertical (Retail and Consumer Goods, Government and Defense, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

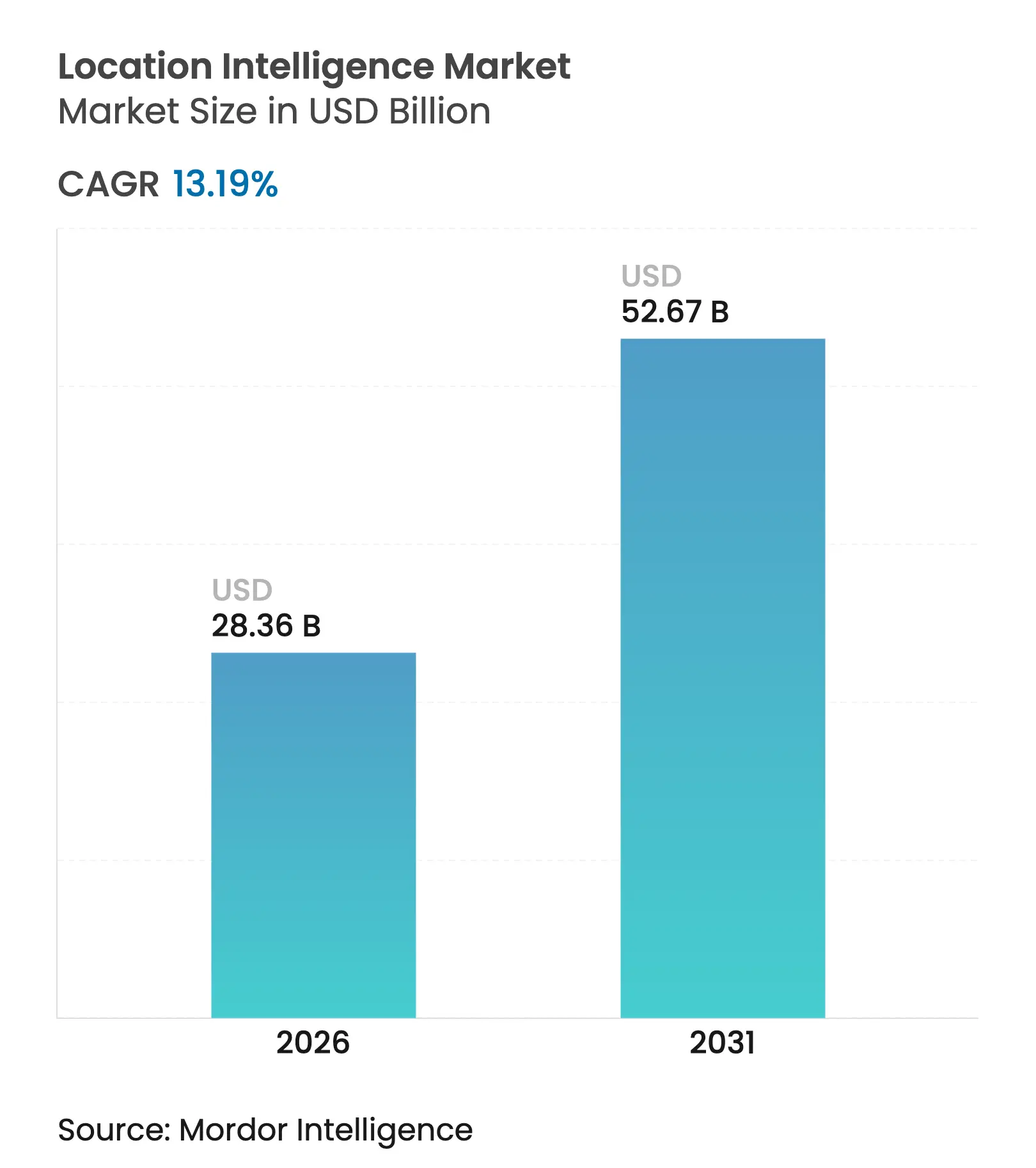

| Market Size (2026) | USD 28.36 Billion |

| Market Size (2031) | USD 52.67 Billion |

| Growth Rate (2026 - 2031) | 13.19 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Location intelligence market size in 2026 is estimated at USD 28.36 billion, growing from 2025 value of USD 25.06 billion with 2031 projections showing USD 52.67 billion, growing at 13.19% CAGR over 2026-2031. Heightened enterprise demand for spatial analytics, a surge in IoT-enabled data streams, and cloud-native GIS platforms are pushing the market toward large-scale real-time decision support. The smartphone and IoT geolocation boom is feeding high-density data that unlock granular consumer and asset insights, while e-commerce logistics teams are standardizing on location-aware route optimization to cut delivery times. Satellite mega-constellations are delivering sub-meter accuracy essential for autonomous mobility, and LiDAR-based indoor mapping is opening new productivity gains inside factories, hospitals, and retail spaces. On the risk side, evolving privacy regulations and upfront indoor-positioning costs threaten to slow some deployments, yet vendor focus on consent management and cloud subscription models is cushioning the impact.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Smartphone

and IoT geolocation boom

Smartphone

and IoT geolocation boom

| +3.2% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+3.2%

|

Geographic Relevance

:

Global,

with Asia-Pacific leading

adoption

|

Impact Timeline

:

Medium

term (2-4 years)

|

E-commerce

and logistics demand for real-time analytics

E-commerce

and logistics demand for real-time analytics

| +2.8% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) | |||

Cloud-native

GIS/SaaS adoption

Cloud-native

GIS/SaaS adoption

| +2.1% | Global, enterprise focus in developed markets | Medium term (2-4 years) | |||

LiDAR-enabled

indoor mapping for enterprise assets

LiDAR-enabled

indoor mapping for enterprise assets

| +1.9% | North America and EU leading, selective Asia-Pacific uptake | Long term (≥ 4 years) | |||

Satellite

mega-constellation APIs for sub-meter insights

Satellite

mega-constellation APIs for sub-meter insights

| +1.4% | Global coverage with defense/automotive priority | Long term (≥ 4 years) | |||

Post-quantum

secure geofencing in defense

Post-quantum

secure geofencing in defense

| +0.8% | North America, EU, select Asia-Pacific nations | Long term (≥ 4 years) | |||

Smartphone

and IoT geolocation boom

Smartphone

and IoT geolocation boom

| +3.2% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Smartphone and IoT Geolocation Boom

More than 700 million users now supply 20 billion daily location pings via Mapbox Movement, enabling enterprises to distill fine-grained behavioral patterns at city-block resolution. Edge-enhanced 5G IoT devices reduce latency and uplift accuracy, supporting life-critical use cases from emergency dispatch to autonomous navigation. Asia-Pacific’s mobile economy delivered USD 880 billion to regional GDP in 2024, showing the macroeconomic weight of location-centric digital services.[1]GSMA Intelligence, “The Mobile Economy Asia Pacific 2025,” GSMA, gsma.com Double-digit smartphone adoption in emerging markets is therefore set to extend the data exhaust that fuels the location intelligence market.

E-commerce and Logistics Demand for Real-time Analytics

Retailers and 3PLs are embedding location intelligence in routing engines to compress last-mile delivery windows and sustain customer loyalty. FairPrice Group, for instance, integrated Google Cloud AI and geospatial APIs to steer in-store carts and plan demand-driven replenishment, slashing stock-outs and queue times. Autonomous vans and drone fleets require centimeter-level positioning that conventional GPS cannot guarantee in dense urban cores, pushing adoption of multisensor fusion frameworks. Connected inventory platforms now combine geofencing alerts with predictive purchase intent, ensuring fulfillment centers pre-stage stock near hotspots of demand.

Cloud-native GIS/SaaS Adoption

Enterprises are retiring on-premise GIS silos in favor of platforms such as CARTO’s cloud engine, which executes spatial SQL directly inside data warehouses like BigQuery and Snowflake to honor data-gravity principles.[2]CARTO Engineering, “Spatial Extension for Snowflake and BigQuery,” CARTO, carto.comThis architecture compresses rollout schedules, preserves governance, and supports elastic scaling for analytic bursts. Subscription pricing converts capital outlays to predictable opex, while hybrid clouds align with data-sovereignty mandates in regulated sectors. Providers are also embedding no-code spatial notebooks that enable business analysts to craft geofencing models without GIS scripting.

LiDAR-enabled Indoor Mapping for Enterprise Assets

SICK’s LiDAR-LOC achieves sub-10 mm accuracy, underpinning precise AGV navigation and high-value asset tracking inside production halls. Coupled with SLAM algorithms, LiDAR point clouds feed industrial digital twins that replay forklift trajectories and flag bottlenecks. Healthcare campuses deploy similar systems to accelerate equipment retrieval and patient wayfinding. UWB and Wi-Fi 6E convergence is further boosting coverage, and academic trials demonstrate centimeter-level precision for complex pick-and-place robotics in clean-rooms.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Data-privacy

regulations (GDPR, CCPA, etc.)

Data-privacy

regulations (GDPR, CCPA, etc.)

| -2.3% | EU and California leading, spreading globally | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-2.3%

|

Geographic Relevance

:

EU

and California

leading, spreading globally

|

Impact Timeline

:

Short

term (≤ 2 years)

|

Up-front

cost of indoor positioning infrastructure

Up-front

cost of indoor positioning infrastructure

| -1.7% | Global, particularly impacting SMEs | Medium term (2-4 years) | |||

Fragmented

geospatial data standards

Fragmented

geospatial data standards

| -1.1% | Global, with regional variations | Medium term (2-4 years) | |||

Sustainability

scrutiny of high-compute geo-analytics

Sustainability

scrutiny of high-compute geo-analytics

| -0.9% | EU leading, expanding to North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Data-privacy Regulations (GDPR, CCPA, etc.)

The draft American Data Privacy and Protection Act classifies geolocation as sensitive data that demands explicit opt-in, mirroring GDPR’s consent protocols.[3]IAPP Staff, “Congress Advances the American Data Privacy and Protection Act,” IAPP, iapp.org Developers are therefore shifting toward differential-privacy aggregates and on-device processing to sustain analytics quality while honoring user rights. Echo Analytics’ GeoPersona framework shows how probabilistic clustering can deliver audience insights without exposing individual tracks. Firms are investing in automated consent orchestration layers and encryption-in-use technology to maintain compliance across jurisdictions.

Up-front Cost of Indoor Positioning Infrastructure

Comprehensive indoor systems often require dense UWB anchors, specialized LiDAR units, and calibration services that can deter SMEs. Yet case studies reveal organizations saving USD 20,000 annually after migrating to self-hosted mapping stacks instead of perpetual API charges, indicating an emerging cost-optimization path. Hardware commoditization and open standard protocols continue to erode deployment barriers, while cloud subscription models reallocate capex into manageable opex envelopes over multiyear terms.

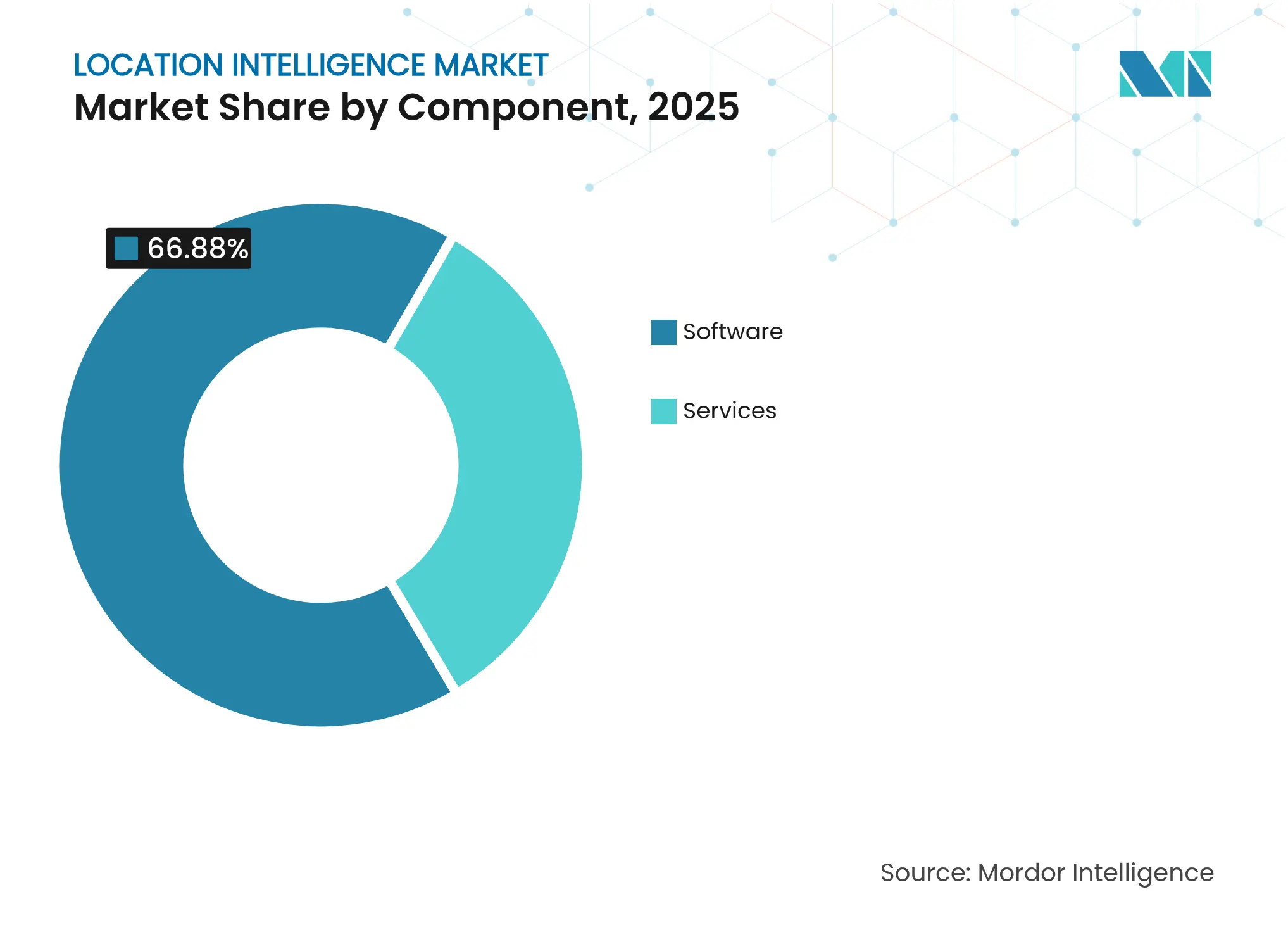

By Component: Software Dominance Drives Platform Consolidation

Software accounted for 66.88% of the location intelligence market share in 2025, reflecting enterprise reliance on fully integrated ingestion-to-visualization stacks. Esri’s FY 2024 revenue of USD 1.2 billion underscores the pull of end-to-end GIS ecosystems that bundle spatial ETL, AI toolkits, and application APIs. As a recurring subscription model, software earnings compound as datasets and users expand, reinforcing vendor lock-in. Services, by contrast, are projected to post an 17.93% CAGR as enterprises seek tailored data governance blueprints, privacy audits, and custom algorithm design. The services opportunity is magnified by hybrid-cloud complexity, where consultants must knit together on-prem edge nodes with public-cloud analytics pipelines.

Platform consolidation continues as hyperscalers embed native geospatial kernels that offload spatial joins to serverless engines, minimizing egress fees. Vendors are also curating industry-specific data layers—such as foot-traffic heatmaps for retail—turning software marketplaces into one-stop shops. This trend strengthens network effects; each additional dataset enhances platform gravity, attracting more analysts and reinforcing software’s leading slice of the location intelligence market.

Note: Segment shares of all individual segments available upon report purchase

By Solution Type: Geocoding Foundation Enables Advanced Analytics

Geocoding and reverse-geocoding retained 31.12% revenue share in 2025, a testimony to their role as the mandatory staging gate for any spatial workflow. Direct quality upgrades ripple through routing, proximity marketing, and risk underwriting algorithms. Meanwhile, data integration and ETL tools are accelerating at 16.86% CAGR as organizations harmonize feeds from IoT endpoints, satellite rasters, and transactional records. Low-code connectors that auto-detect coordinate systems are shrinking time-to-insight, while streaming ETL engines now enrich 1 million events per second.

Reporting and visualization suites are shifting from static tiles to live map dashboards that refresh on every Kafka event. Machine-learning-driven anomaly detection highlights unexpected footfall spikes or delivery slowdowns in real time. Emerging solution niches—AR spatial overlays, natural-language spatial query bots, and voice-first assistants—are capturing early adopters in field service and mobility contexts, adding diversity to the overall location intelligence market.

By Location Type: Indoor Positioning Accelerates Enterprise Adoption

Outdoor services contributed 68.35% to the location intelligence market size in 2025 thanks to mature GPS coverage and ubiquitous smartphone sensors. Yet indoor positioning leads growth at a 16.02% CAGR as corporations seek end-to-end asset visibility. Energy utilities calibrate switch-gear inspections with sub-meter indoor tags, while airports deploy wayfinding apps that shave minutes off passenger transfers. Indoor accuracy challenges such as multipath and signal attenuation are easing through UWB chipsets integrated into flagship smartphones. ZaiNar’s RF-based 3D tracking illustrates how multi-protocol stacks can localize assets even in GPS-denied zones, bridging indoor and outdoor contexts seamlessly.

Regulatory audits increasingly require proof of staff evacuation times or forklift hazard zones, making indoor heatmaps an indispensable compliance artifact. Real-estate owners are packaging indoor location APIs into tenant services, preparing buildings for autonomous cleaning robots and micro-fulfillment hubs. As indoor coverage expands, the location intelligence market gains a unified spatial fabric across every square meter of enterprise operations.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Deployment: Cloud Infrastructure Drives Scalability

Cloud deployments accounted for 62.75% of the location intelligence market size in 2025, and growth continues at 19.21% CAGR. Elastic compute tiers ingest terabytes of telemetry during promotional surges, then scale down overnight, preserving budget discipline. Data-warehouse-native spatial functions move proximity joins close to where data already sits, eliminating costly extracts. Zero-ETL architectures are becoming a board-level KPI as firms benchmark data latency against real-time decision needs.

On-premise stacks persist in defense, finance, and critical infrastructure segments that cannot risk shared-tenant environments. Nevertheless, hybrid topologies—where sensitive layers remain on-prem while anonymized aggregates flow into the cloud—are mainstreaming. Vendors are rolling out edge bundles that process positional queries locally, slashing round-trip latency for autonomous vehicles and smart-factory cobots. Edge-cloud orchestration thus opens a continuum of deployment options tailored to workload and compliance demands.

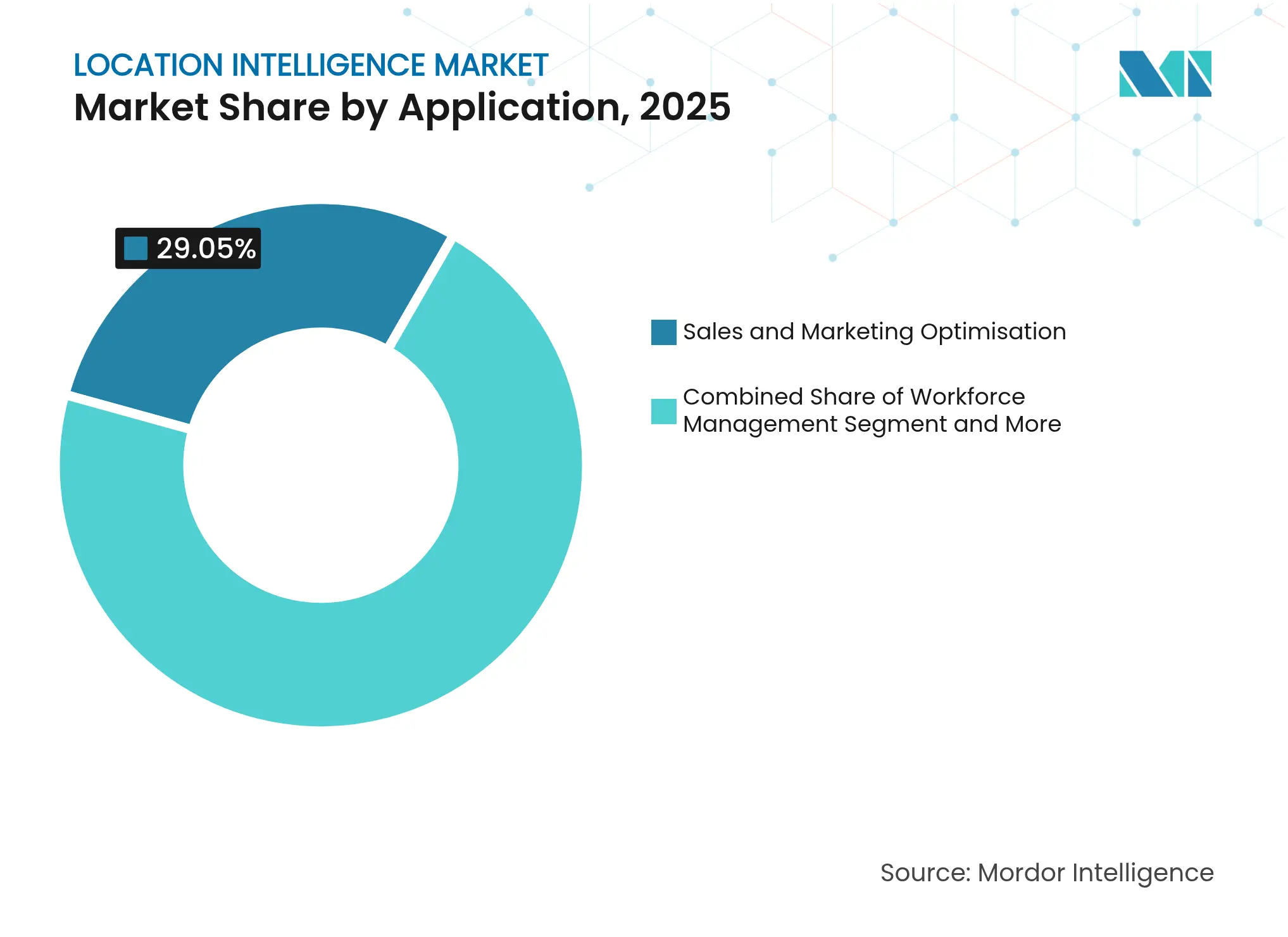

By Application: Facility Management Emerges as Growth Driver

Sales and marketing optimization held 29.05% of 2025 revenue, driven by geo-targeted campaigns and retail site selection models that correlate spending to catchment demographics. Yet facility management is climbing fastest at 17.39% CAGR as operators digitize floor plans and deploy sensor beacons to monitor occupancy, HVAC efficiency, and safety compliance. Predictive maintenance algorithms overlay asset age, usage intensity, and location-based risk factors to prioritize work orders, cutting downtime.

Workforce management suites now compute real-time travel paths inside warehouses, reducing pick times and boosting labor utilization. Asset-tracking modules fuse BLE tags with Wi-Fi RTT to trigger theft-prevention alerts and chain-of-custody audits. Risk management dashboards integrate weather, crime, and supply-chain disruptions to foresee hotspots. Across each vertical, the location intelligence market is embedding spatial context into previously siloed operational workflows.

Note: Segment shares of all individual segments available upon report purchase

By End-user Vertical: Utilities Sector Drives Infrastructure Modernization

Retail and consumer goods retained 24.08% of spending in 2025 by leveraging foot-traffic analytics, inventory heatmaps, and personalized promotions. Utilities and energy, however, are projected to rise at 15.78% CAGR as grid operators roll out digital twins and situational-awareness maps to handle distributed renewables. Pipeline operators are overlaying corrosion sensors with terrain models to prioritize maintenance, while wind-farm developers optimize turbine siting via high-resolution topographic layers.

Government and defense agencies expand situational-awareness platforms that blend drone imagery, public-safety feeds, and social-media sentiment. Manufacturers embed RTLS tags into work-cells to fine-tune line balancing, and logistics carriers implement AI-driven dispatch engines that trim route miles. In finance, branch optimization and fraud detection harness geospatial clustering to refine risk models. Telecoms apply RF propagation maps to plan 5G densification, and media groups stream location-based content to smartphones at events and stadiums.

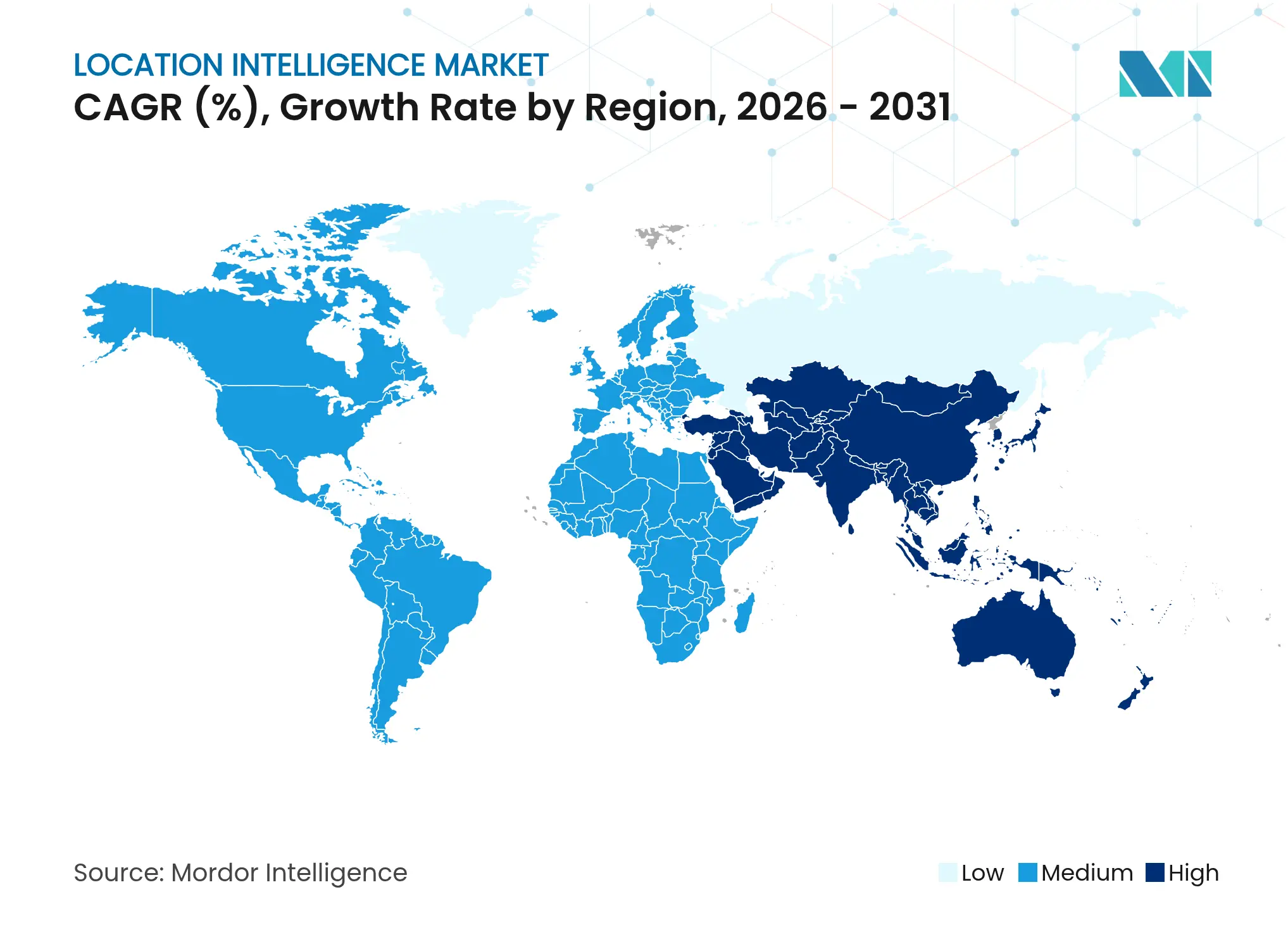

North America generated 28.01% of global revenue in 2025, underpinned by enterprise software maturity and the scale of defense procurement. Google Maps alone delivered USD 11.1 billion in 2024, highlighting the monetization potential of location APIs. Widespread 5G coverage, skilled developer pools, and robust venture finance accelerate innovation, while California’s CCPA and various state bills shape privacy-by-design roadmaps. The region is also an early adopter of autonomous driving pilots, pushing demand for centimeter-grade maps, HD LiDAR layers, and edge-processed object detection. Cloud hyperscalers headquartered in the United States continue to bundle spatial AI services, cementing the region’s platform leadership.

Asia-Pacific is the fastest growing territory at a 19.35% CAGR, propelled by urbanization, mobile-first consumers, and state-sponsored smart-city programs. The region supplied USD 880 billion in mobile-economy value during 2024 and is forecast to add 400 million 5G subscribers by 2030. China’s location services market surpassed CNY 1.27 trillion in 2024, buoyed by indoor positioning, autonomous driving pilots, and social-commerce overlays. Southeast Asian e-commerce hubs are adopting geospatial route orchestration to cope with dense megacity traffic. Diverse regulatory maturity and infrastructure gaps pose execution risks, yet vendors tailoring lightweight SDKs and pay-as-you-go pricing are capturing SME demand across India, Indonesia, and Vietnam.

Europe offers a fertile but tightly regulated market. GDPR’s stringent consent rules spur investment in privacy-enhancing technologies, nudging vendors to develop differential privacy and on-device analytics. Utility majors such as Endesa exploit spatial demand modeling to guide renewable rollouts and grid upgrades. The Galileo satellite navigation system and Copernicus Earth-observation data sets furnish an indigenous tech stack that supports precision agriculture and environmental monitoring. However, fragmented national rules and varied broadband coverage require localized go-to-market tactics. Public-private consortiums are funding 3D urban models for climate resilience, creating new demand arcs for the location intelligence market.

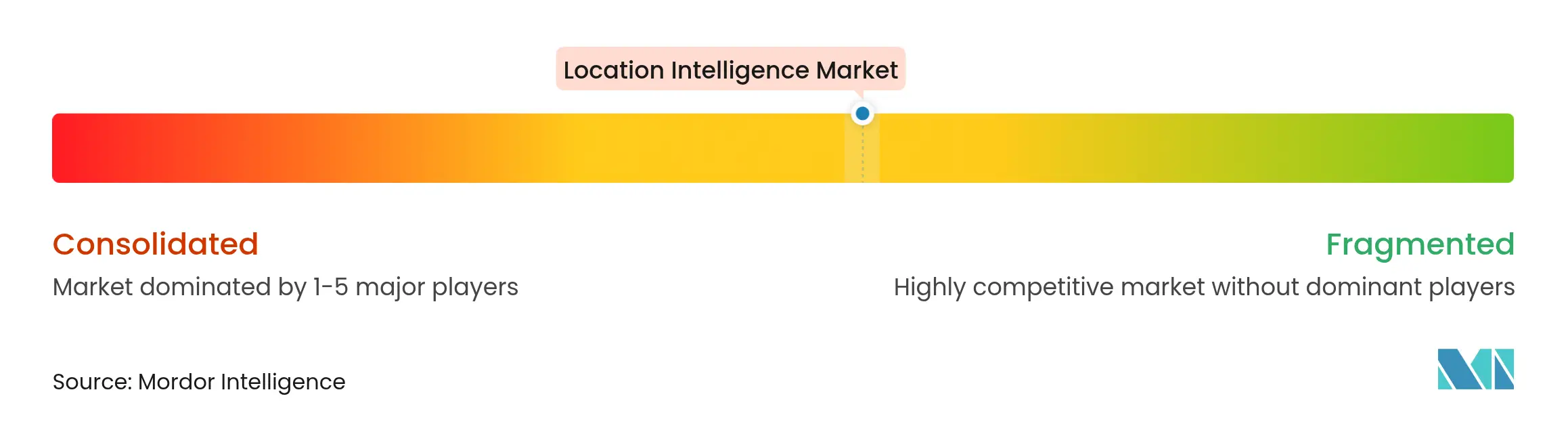

Market Concentration

The location intelligence market sits at a moderate concentration level: global platform leaders coexist with niche innovators serving domain-specific needs. Esri, Google, and Microsoft wield expansive product portfolios, deep partner networks, and multi-billion-dollar R&D budgets that perpetuate their advantage. Esri’s ArcGIS ecosystem, for example, wraps spatial ETL, AI models, and a low-code app studio in one license, anchoring user stickiness. Google folds geospatial APIs into its Ads, Cloud, and Android assets, creating natural cross-sell leverage. Microsoft embeds Azure Maps into its Fabric data estate, enabling joint BI and geospatial dashboards.

Specialists flourish by focusing on automotive, developer tooling, or defense navigation. HERE Technologies boasts a USD 4.4 billion automotive backlog, supplying HD maps to 70 OEMs. Mapbox wins developer hearts with customizable vector SDKs and hit USD 172.4 million revenue in 2024. IBM and Oracle differentiate via enterprise data governance, embedding spatial AI into existing ERP and database lines. White-space innovation is visible in quantum-resistant navigation: Q-CTRL’s quantum sensors promise 50x GPS accuracy and spoof-proof resilience for defense customers.

M&A momentum underscores the race for vertically integrated stacks. T-Mobile allocated USD 775 million to acquire Vistar Media and Blis, stitching out-of-home ad inventory with mobile analytics to form a unified retail media network. Viavi’s USD 150 million purchase of Inertial Labs expands inertial navigation for aerospace assets. Cloud alliances also shape the field: HERE and AWS launched a USD 1 billion partnership in 2025 to inject live streaming maps into supply-chain control towers. Overall, battle lines concentrate on AI enrichment, centimeter-level accuracy, and privacy-preserving data engineering.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Location Intelligence Baseline Earns Trust

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 25.06 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 24.70 B (2025) | Global Consultancy A | Narrow component list and vendor self-reporting bias | ||

USD 21.50 B (2024) | Industry Research Group B | Broader inclusion of adjacent analytics tools and no mid-year refresh |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.