Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 16.83 Billion |

| Market Size (2026) | USD 17.21 Billion |

| Market Size (2031) | USD 19.21 Billion |

| Growth Rate (2026 - 2031) | 2.23% CAGR |

| Fastest Growing Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Laundry Appliances Market Analysis by Mordor Intelligence

The European laundry appliance market size is expected to grow from USD 16.83 billion in 2025 to USD 17.21 billion in 2026 and is forecast to reach USD 19.21 billion by 2031 at 2.23% CAGR over 2026-2031. Demand now shifts from volume-driven replacement toward value-driven premiumization as energy-efficiency mandates and smart-home ecosystems redefine product differentiation in the European laundry appliance market.[1]European Commission, “Energy Efficient Products: Commission Moves to Improve Quality of Information,” europa.eu. Regulatory levers such as the simplified A-to-G energy label and the Right-to-Repair Directive accelerate early retirement of inefficient machines while simultaneously lengthening the service life of new models, creating a balanced pull-and-push dynamic that safeguards revenue. Manufacturers answer with inverter motors, heat-pump dryers, and app-based energy dashboards that lower lifetime running costs, a proposition that resonates in regions facing elevated utility tariffs. Consolidation further reshapes the competitive field; Whirlpool’s union with Arçelik to form Beko Europe and Midea’s purchase of Küppersbusch parent broaden scale advantages and R&D reach in the European laundry appliance market.

Key Report Takeaways

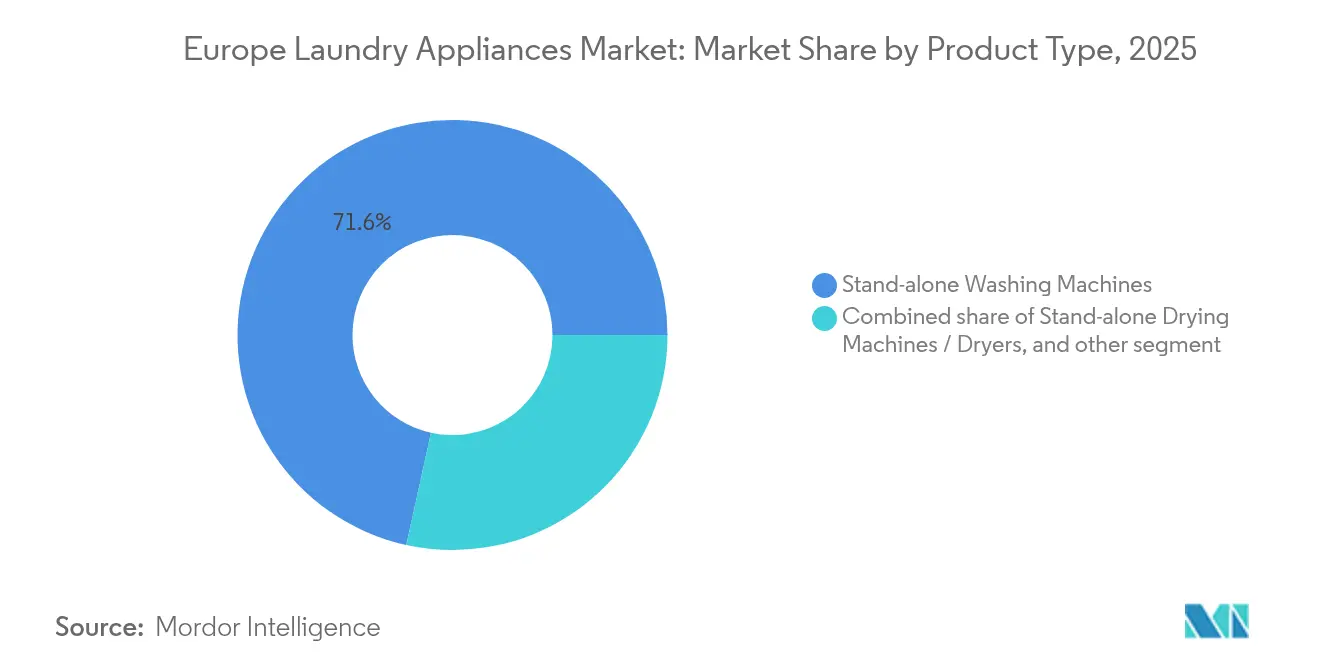

- By product type Stand-alone washing machines held 71.55% of the Europe laundry appliance market share in 2025, while combined washer-dryers are expanding at a 6.97% CAGR through 2031.

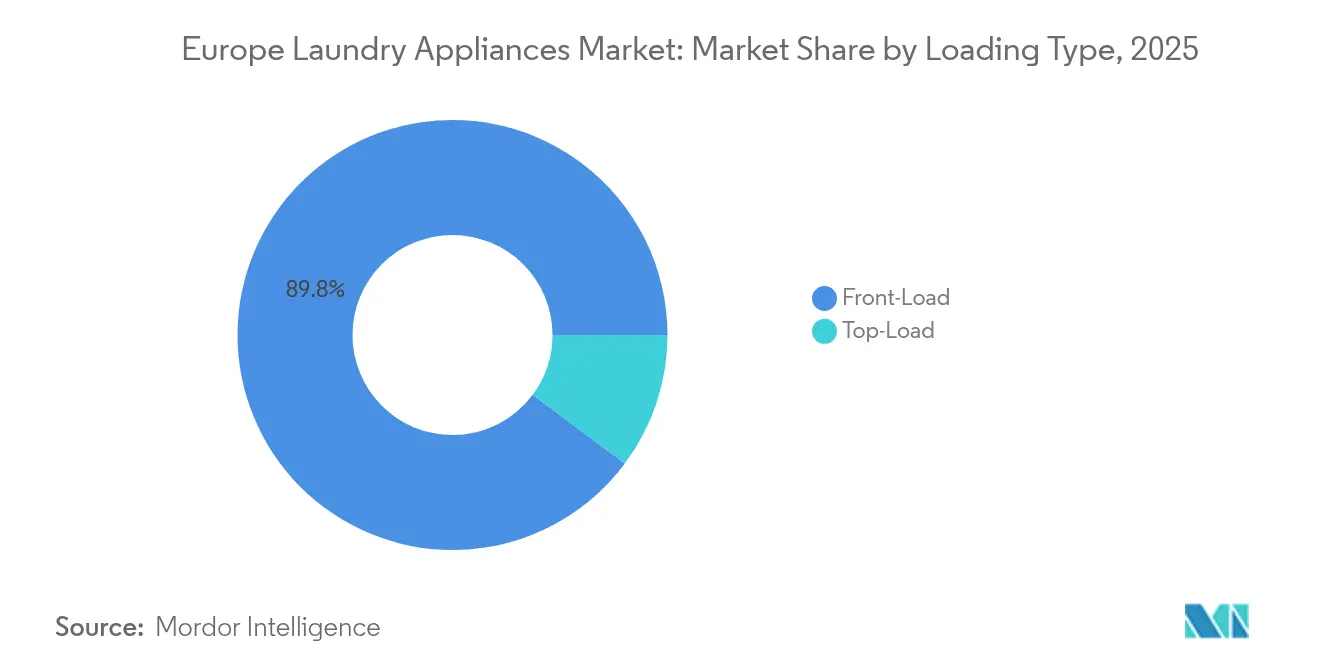

- By loading type Front-load models captured 89.80% of the Europe laundry appliance market size in 2025 and will advance at a 6.02% CAGR to 2031.

- By capacity The 6–8 kg class accounted for 55.70% of the Europe laundry appliance market share in 2025; machines above 8 kg are on track for an 7.88% CAGR.

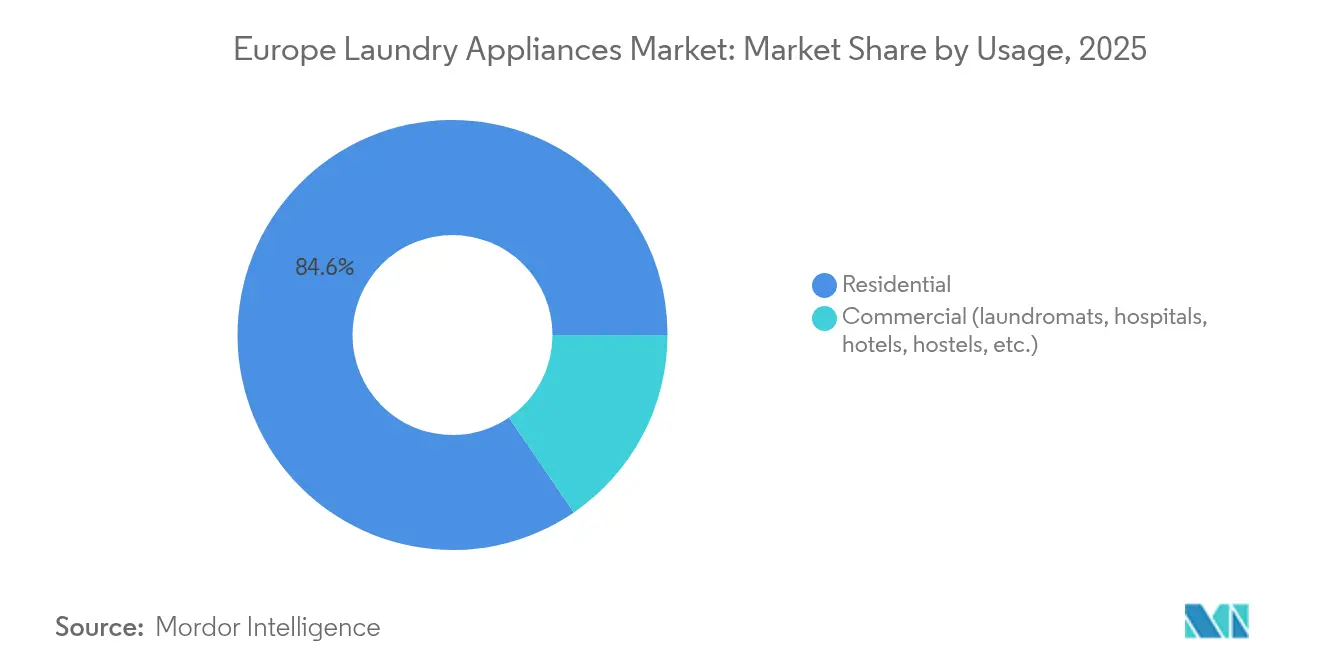

- By usage Residential installations represented 84.55% of the Europe laundry appliance market size in 2025, yet commercial units are rising at a 6.74% CAGR.

- By distribution channel B2C retail controlled 79.35% of the Europe laundry appliance market share in 2025, but B2B direct routes will increase at a 5.84% CAGR.

- By geography Germany led with 26.85% of the Europe laundry appliance market size in 2025, whereas Spain will post the highest 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Laundry Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of smart, IoT-enabled laundry appliances | +0.8% | Western Europe, BENELUX, Nordics | Medium term (2–4 years) |

| Energy-efficiency regulations spurring replacement demand | +0.6% | EU-27, UK | Short term (≤ 2 years) |

| Growing multi-family housing driving compact appliance sales | +0.4% | Germany, France, Urban Spain | Medium term (2–4 years) |

| Premiumization trend among urban households | +0.3% | Western Europe, Major Cities | Long term (≥ 4 years) |

| Circular-economy leasing models by OEMs | +0.2% | BENELUX, Germany, France | Long term (≥ 4 years) |

| Water-scarcity mitigation technologies | +0.1% | Spain, Italy, Southern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Smart, IoT-Enabled Laundry Appliances

Connected washers and dryers are moving from optional extras to baseline expectations as households prioritize live energy monitoring and predictive maintenance. BSH invested EUR 850 (USD 885.32) million in 2024 R&D, channeling a sizable portion into digital platforms that unite appliances with voice assistants and utility dashboards.[2]BSH Hausgeräte, “BSH Increases Turnover to 15.3 Billion Euros,” bsh-group.com. The latest EU label embeds QR codes linking to the EPREL database, giving buyers transparent efficiency metrics that bolster adoption in the Europe laundry appliance market. Northern countries, where electricity prices are high, lead uptake because real-time usage data translates directly into lower monthly bills. Commercial laundromats follow suit, installing sensor-rich equipment that trims downtime and introduces consumers to app-controlled cycles during public usage. As the installed base of smart machines grows, manufacturers launch subscription software and detergent services, creating recurring revenue layers that buffer cyclical hardware sales. The feedback loop reinforces premium positioning and cements digital ecosystems as a central battleground for share gains.

Energy-Efficiency Regulations Spurring Replacement Demand

The July 2025 tumble-dryer rule eliminates the crowded A+++-to-D scale, replacing it with a simple A-to-G ladder and effectively restricting future sales to heat-pump models.[3]European Commission, “New Measures for More Energy-Efficient Household Tumble Dryers,” europa.eu. Policymakers forecast 15 TWh savings and a 1.7 million tCO₂e cut by 2040, numbers retailers promote to position upgrades as financially prudent. Parallel Ecodesign rules introduce digital product passports, forcing brands to publish durability metrics that reward engineering rigor and expose corner-cutting competitors. German research reveals buyers now rank lifecycle footprint ahead of sticker price, an attitudinal shift that directly benefits high-efficiency SKUs. As a result, the Europe laundry appliance market sees a two-tier structure: premium classes command margin headroom, while bare-minimum compliant models confront commoditization. This regulatory squeeze triggers early retirements of aging units, giving OEMs a predictable baseline of replacement demand even when broader consumer sentiment cools.

Growing Multi-Family Housing Driving Compact Appliance Sales

Apartment construction across Europe compresses utility spaces, fueling the appetite for 45 cm-depth washers and heat-pump combo units that combine washing and drying in one cabinet. Spain’s residential pipeline, linked to tourism recovery, underpins the country’s forecast-leading 6.24% CAGR as developers bulk-buy standardized compact models for new flats. Property managers demand long warranties and remote diagnostics to lower service costs, influencing OEM feature roadmaps during product design. Household buyers, meanwhile, gravitate toward large 25 kg drums within narrow footprints, validating Korean brand investments in high-capacity combo technology. Nordic and BENELUX cities with average apartment sizes below 70 m² mirror this trend, making compact innovation a Europe-wide imperative. As form-factor ingenuity aligns with efficiency norms, the Europe laundry appliance market gains incremental value growth without relying on unit-volume expansion.

Premiumization Trend Among Urban Households

Rising disposable income and a home-centric lifestyle push consumers toward steam sanitization, auto-dosing, and fabric-specific AI cycles that preserve garments. Miele’s 2025 ribless drum increases usable volume while minimizing fiber stress, a showcase example of premium innovation that resonates with quality-driven buyers. Surveys indicate 81% of German shoppers and nearly four-fifths of Italian and Spanish consumers willingly pay more for robust, energy-efficient machines. Chinese entrant Haier doubles down on this space; its Casarte line logged 20% growth in Q1 2025, proving new luxury labels can tap latent demand. Manufacturers amplify experiential marketing through showroom kitchens and AR apps that dramatize wash-quality gains, smoothing the upsell journey. Premiumization cushions manufacturers against the slowing replacement cycle by lifting average selling prices in the Europe laundry appliance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity amid inflationary pressures | -0.5% | EU-27, UK | Short term (≤ 2 years) |

| Mature replacement market saturation in Western Europe | -0.3% | Germany, France, UK, BENELUX | Medium term (2–4 years) |

| Energy efficiency regulation compliance costs | -0.4% | EU-27 | Short to medium term |

| Supply chain disruptions due to geopolitical tensions | -0.6% | Eastern Europe, EU border nations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity Amid Inflationary Pressures

Although euro-area inflation has receded from its 2023 peak, it remains above pre-pandemic norms, suppressing household confidence and stretching appliance replacement cycles.[4]European Central Bank, “Why Are Euro-Area Households Still Gloomy?” ecb.europa.eu. APPLiA warns that simultaneous increases in regulatory compliance and input costs narrow manufacturer margins, forcing tough trade-offs between specification depth and shelf pricing. Entry-level and mid-tier segments show pronounced price elasticity, prompting many buyers to defer upgrades unless energy bills escalate sharply. Retailers respond by extending 0% financing, yet higher interest rates diminish the appeal of long repayment plans. OEMs turn to value engineering—streamlining chassis parts, localizing supply chains—to protect headline prices while meeting Class A energy thresholds. Promotions cluster around events like Black Friday, demonstrating that bargain hunting shapes purchase timing in the Europe laundry appliance market.

Mature Replacement Market Saturation in Western Europe

Penetration above 95% in Germany, France, and the UK caps organic unit growth, pushing competitors to nudge earlier upgrade triggers rather than courting first-time buyers. The European Environment Agency notes washing-machine lifespans lengthened from 11.6 to 12.5 years between 2019 and 2023, a trend intensified by Right-to-Repair legislation that obliges OEMs to supply spare parts for up to a decade. France leads with its repairability index, now a mandatory label on appliance packaging that steers consumers to longer-lasting machines. These measures reduce natural churn, compelling brands to monetize installed bases through software, detergents, and buy-back programs. New entrants face steep hurdles because after-sales networks and brand equity dominate buyer decisions in saturated territories. Consequently, innovation cadence, not sheer volume, determines share shifts in the Europe laundry appliance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combination Units Challenge the Status Quo

Stand-alone washers controlled 71.55% of 2025 shipments, a testament to habit‐entrenched purchasing where separate machines still symbolize reliability and throughput. The Europe laundry appliance market size for these models is forecast to rise modestly, signaling maturity yet durability. Combined washer-dryers, enjoying a 6.97% CAGR, owe momentum to shrinking apartment footprints and improved heat-pump drying that remedies historic energy concerns. Korean brands pushing 25 kg drums inside standard frames illustrate how engineering solves capacity constraints without enlarging cabinets. Premium cues such as allergen-neutralizing steam and AI load sensing entice households that equate multifunctionality with value. OEM roadmaps therefore converge: integrate identical smart modules across stand-alone and combo lines to blunt development cost inflation while meeting tightening EU standards.

Regulatory shifts further tilt the playing field; the July 2025 rule effectively bans non-heat-pump dryers, blurring technology distinctions between combo units and traditional stand-alone dryers. Retailers already spotlight energy-class symbols next to combination machines, easing consumer anxiety about operating costs and reinforcing the premium narrative. Commercial users, especially boutique hotels, increasingly adopt combo units to reduce back-of-house floor space, signaling crossover appeal beyond residential niches. Early evidence shows combo machines achieving comparable service lifespans, once considered a weak point, addressing prior concerns over dual-function wear. Investors note that higher average selling prices help recoup incremental R&D spending within three years, a metric supportive of continued portfolio expansion. The Europe laundry appliance market thus witnesses category convergence accelerated by policy, technology, and real-estate trends

By Loading Type: Front-Load Leadership Remains Unshaken

Front-load machines posted a 89.80% share in 2025 because European kitchens and utility rooms favor under-counter installation and stacked dryer configurations. The loading design uses gravity for tumble action, allowing lower water volumes and gentler fabric agitation, attributes that translate into Class A energy and water scores. OEMs refine spin algorithms and drum patterns to push residual moisture below statutory thresholds, trimming dryer cycle lengths. Consumers reward these gains with higher Net Promoter Scores, reinforced by marketing that links front‐loaders to lower wardrobe replacement costs. Top-loaders persist mainly in rural installations or retrofit situations where plumbing aligns better with vertical orientation. Yet even in those niches, energy labels erode top-loader appeal, making widespread comeback unlikely in the Europe laundry appliance market.

Manufacturers continue to tweak magnetic door seals, counterbalancing higher spin speeds with vibration dampers that safeguard apartment block tranquility. Smart apps now offer tailored programs—wool, baby clothes, or sportswear—leveraging drum reversals unique to horizontal axes. Service data reveal declining warranty claims as brushless motors replace carbon-brush predecessors, indicating the maturation of front-load architectures. Marketing focuses on sanitary steam options that meet post-pandemic hygiene expectations, adding perceived-value layers that justify marginal price bumps. With capacity growth migrating to larger drums rather than alternate loading styles, front-load dominance appears structurally sound. Consequently, front-load innovation remains a priority funding line in every major R&D budget within the Europe laundry appliance market.

By Capacity: Larger Drums Propel Efficiency Uptake

The 6–8 kg segment dominates at 55.70% because it balances family laundry volume with standard cabinet dimensions across European dwellings. Above-8 kg machines lead growth at 7.88% CAGR, reflecting consumer strategy to run fewer cycles and capitalize on time-of-use energy tariffs that reward full loads. Manufacturers redesign rib patterns and ventilation paths to maintain wash quality at higher fill factors, a shift validated by Miele’s ribless drum that boosts usable volume without widening chassis. Larger drums also suit duvet and curtain washing, reducing reliance on commercial laundromats and reinforcing home-centric convenience trends. Below-6 kg units cling to relevance in student housing and micro-apartments but face cannibalization as OEMs fit larger drums into the same footprints. The overall arc signals a capacity race that dovetails with resource conservation, strengthening the sustainability halo of the Europe laundry appliance market.

Policy pressure amplifies the trend; energy tests normalize to full-load metrics, thus favoring machines that handle bigger batches efficiently. Retailers respond by sequencing showroom displays from smallest to largest drums, visually steering shoppers toward higher-margin SKUs. Service data indicate no disproportionate wear in larger bearings, alleviating previous durability fears. Marketing collateral now plays on lifestyle imagery—washing bedding at home after ski weekends—tying capacity directly to experiential freedom. Finance options structure payments over an expected ten-year life, reframing the upfront premium as pennies per cycle. This capacity upswing thereby feeds both OEM profitability and consumer utility, reinforcing volume migration in the Europe laundry appliance market.

By Usage: Commercial Momentum Outpaces Household Growth

Household demand still covers 84.55% of shipments, yet hotel, healthcare, and institutional buyers drive a faster 6.74% CAGR as hygiene regulations tighten post-pandemic. Miele Professional logged EUR 819 (USD 853.03) million sales in 2023, illustrating commercial appetite for programmable disinfection cycles that comply with EN 14065 laundry standards. Hospitality operators upgrade to heat-pump dryers to meet corporate sustainability targets and reduce linen turnaround times, while healthcare facilities install barrier washers that segregate clean and soiled sides for infection control. Self-service laundromats embed IoT telemetry, lowering unplanned downtime and delivering app-based alerts that transfer usage familiarity back into the residential market. OEMs tailor seven-year warranties and on-site service contracts, capturing lifetime value beyond the initial invoice. These dynamics carve a profitable niche that supplements slowing residential replacement, boosting overall resilience in the Europe laundry appliance market.

Investment analysts note commercial buyers exhibit lower price elasticity than households, allowing premium feature bundling such as real-time performance dashboards and detergent auto-dosing. Electrolux Professional derives 60% of revenue from Europe, underscoring regional dependence on institutional contracts. Segment cross-pollination intensifies; hotel laundry departments pilot closed-loop water systems first, paving the regulatory path for future residential adoption. Commercial volume growth also stabilizes factory utilization, enabling OEMs to weather consumer downturns without drastic production cuts. Networked machine fleets funnel anonymized performance data into cloud analytics, refining next-generation product development. The commercial surge hence injects diversification and data intelligence into the Europe laundry appliance market.

By Distribution Channel: Direct Engagement Redraws the Map

Traditional retail still generates 79.35% of sales because shoppers value physical demonstration and turnkey installation. Yet manufacturer-run webstores and flagship showrooms spearhead a 5.84% CAGR in B2B-direct and B2C-direct channels, improving margin capture and end-user insight. BSH’s Experience and Design Centers immerse visitors in live demos of connected ecosystems, converting foot traffic into higher attachment rates for warranties and consumables. Digital storefronts personalize promotions using CRM data, elevating cross-sell success for pedestals or water softeners. As e-commerce share could hit 60% by 2027, partnerships with logistics specialists ensure two-person delivery and haul-away of old units, neutralizing a historical brick-and-mortar advantage. Retailers counter by layering installation bundles and refurbish buybacks to protect footfall. This tug-of-war injects channel innovation that keeps the Europe laundry appliance market competitive and customer-centric.

Commercial buyers prefer factory-direct relationships for fleet diagnostics, uptime SLAs, and custom programming, solidifying OEM footholds in professional segments. High-volume contracts enable predictive spare-parts stocking, lowering lead times and service costs. Financing arms offer lease-to-own structures that bundle maintenance, aligning accounting treatment with cash-flow realities of hotels and care homes. Direct portals funnel machine utilisation data back to engineering teams, shortening product-improvement loops. As GDPR-compliant data sharing matures, manufacturers leverage anonymized insights to personalize firmware updates across residential fleets as well. Consequently, omnichannel mastery becomes a strategic pillar for share retention in the Europe laundry appliance market.

Geography Analysis

Germany’s 26.85% share stems from its export-oriented economy, deep manufacturing base, and consumer affinity for precision engineering. BSH posted EUR 15.3 billion (USD 15.93 billion) turnover in 2024, aided by home-market loyalty that tolerates premium price points. A strong compliance culture means energy and repair regulations translate swiftly into purchasing behavior, reinforcing advanced feature demand. Brand-trust indices consistently place German labels at the top, making domestic satisfaction a benchmark for continental neighbors. Regional subsidies for high-efficiency appliances, coupled with smart-grid pilot programs, further anchor Germany as a bellwether for technology adoption in the Europe laundry appliance market.

Spain serves as the growth engine with a 6.05% CAGR, buoyed by tourism-led hotel refurbishments and a robust residential construction pipeline. Southern provinces face water scarcity, prompting uptake of closed-loop wash systems that cut consumption by up to 98%. Government stimulus for energy-class upgrades encourages households to swap aged stock before failure, reducing the dominance of reactive replacement. Spanish retailers increasingly bundle warranties with real-time leak detection, addressing concerns over apartment water damage. These factors push Spain’s per-capita appliance spend closer to core-EU averages, driving catch-up potential in the Europe laundry appliance market.

France and Italy contribute sizeable volume but display distinct consumer psychologies. France’s repairability and forthcoming durability indices prioritize long service life, nudging OEMs to design quick-access panels and modular control boards. Italy’s style-centric buyers gravitate to aesthetic alignment with cabinetry, spurring partnerships between appliance and kitchen-furniture brands. BENELUX states champion circular-economy pilots such as the Papillon leasing model that offers ultra-efficient machines to lower-income groups for EUR 7 (USD 7.29) monthly payments. Nordic consumers pay top euro for heat-pump dryers suited to cold, humid climates, aligning utility savings with environmental stewardship. The UK, meanwhile, wrestles with post-Brexit import costs yet maintains appetite for high-efficiency appliances to curb soaring energy bills. Collectively, these regional nuances create a mosaic of micro-markets that add complexity and opportunity within the Europe laundry appliance market.

Regulatory Landscape

EU rules for laundry appliances are anchored in the Ecodesign and Energy Labelling framework administered by the European Commission, with product information surfaced via the EPREL database and QR codes on the A-to-G label. From 1 July 2025, updated ecodesign and energy-labelling measures for household tumble dryers under Delegated Regulation (EU) 2023/2534 reset the market toward high-efficiency designs and reduce room for legacy, low-efficiency offerings.

The policy perimeter expanded with the Ecodesign for Sustainable Products Regulation (EU) 2024/1781, adopted in June 2024, which replaces the prior directive framework and sets the basis for durability, reparability, and circularity requirements through delegated acts and a 2025-2030 working plan (mid-term review in 2028). Within this trajectory, the washing machines and washer-dryers regime remains governed by Regulation (EU) 2019/2023 (ecodesign) and Delegated Regulation (EU) 2019/2014 (energy labelling), supported by harmonised standards referenced in Implementing Decision (EU) 2021/936, amended on 15 January 2025; the ESPR working plan also flags 2026 as a target year for updated ecodesign requirements for household washing machines and washer-dryers.

Value Chain Analysis

The European laundry-appliances value chain starts with upstream raw materials and components such as copper for motor windings, electronic control boards, and drum-bearing assemblies, then moves to OEM design and manufacturing, assembly, testing, and compliance documentation for ecodesign and energy-labelling requirements. Regional manufacturing footprints concentrate around established hubs such as Poland, Germany, and Hungary, while product engineering choices increasingly reflect EU requirements on efficiency and serviceability (including mandated spare-part availability for professional repairers under Regulation (EU) 2019/2023).

Downstream, distribution runs through B2C retail and growing direct-to-consumer and direct-to-business channels, supported by installation, take-back or haul-away, warranty, and captive or authorized service networks. Trade bodies such as APPLiA coordinate across the chain by tracking regulatory impacts on sourcing and advocating for harmonized Single Market implementation, while the shift toward ESPR (Regulation (EU) 2024/1781) increases operational load around product data, component traceability, and end-of-life considerations. As these requirements tighten, after-sales operations and parts logistics become more central to value capture.

Competitive Landscape

Market concentration remains moderate, with the top companies holding a significant share of the market. BSH leads the group, followed by Whirlpool and Electrolux, each maintaining strong competitive positions. Whirlpool’s spin-off of its EMEA assets into Beko Europe alongside Arçelik in 2024 created a 24-million-unit annual capacity powerhouse, intensifying economies of scale. Strategic competition pivots around smart-connectivity portfolios, energy-class leadership, and circular-economy services such as buy-back schemes. Miele Professional capitalizes on healthcare and hospitality niches, posting record sales amid stricter hygiene mandates. Electrolux Professional aims for 3-4% annual growth, leveraging acquisitions to fill product gaps and deepen regional coverage. Chinese giants, notably Haier, leverage acquisition and localized R&D to erode price-premium moats while upholding feature parity, challenging incumbents to accelerate innovation cycles.

Patent filings concentrate on vibration dampening, AI wash algorithms, and refrigerant efficiency, signaling where future differentiators lie. Service platforms shift from call-center models to predictive apps that auto-schedule maintenance, cutting downtime for commercial laundries and enhancing brand stickiness. Supply-chain resilience has become a competitive metric; BSH diversifies microcontroller sourcing, while Electrolux invests in European motor plants to reduce shipping risk. Sustainability credentials crystallize into procurement criteria for institutional buyers, elevating cradle-to-gate CO₂ disclosures as a bid qualifier. Brands that master closed-loop recycling programs gain access to green-finance incentives, lowering capital costs relative to lagging rivals. Such multidimensional rivalry keeps margins tight yet stimulates continual technical advancement in the Europe laundry appliance market.

Marketing increasingly centers on experiential storytelling that marries technology with lifestyle—quiet spin cycles for open-plan living, or allergen removal for young families. Influencer collaborations on social media personalize complex specs, translating kilowatt-hours into relatable monthly savings. OEMs turn to cross-industry alliances; Bosch cooperates with energy utilities to bundle dynamic-pricing tariffs, while Haier partners with detergent brands for co-branded auto-dose cartridges. As digital twins map factory lines, lead times shorten, enabling limited-edition color runs that test regional tastes without inventory risk. The competitive field therefore rewards agile supply chains, authentic sustainability narratives, and data-powered customer intimacy, ensuring relentless evolution in the Europe laundry appliance market.

Europe Laundry Appliances Industry Leaders

BSH Hausgeräte GmbH

Whirlpool Corporation

Electrolux AB

LG Electronics Inc.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven redesign creates opportunities for OEMs and suppliers that can commercialize repairability, durability, and data transparency as sellable features rather than obligations. Regulation (EU) 2024/1781 (ESPR), in force from 18 July 2024, formalizes a pathway for performance and information requirements across physical goods, reinforcing demand for modular architectures, standardized parts strategies, and digital documentation that can support emerging durability and circularity disclosures. This aligns with the market shift toward premiumization and connected functionality already appearing in product roadmaps.

Industrial footprint optimization and localized capacity investments also support faster replenishment and tailored assortments for European retailers and direct channels. In June 2026, BSH opened a EUR 130 million manufacturing facility in Rudna Wielka near Rzeszow, Poland (developed by Panattoni), highlighting ongoing reconfiguration of European production and logistics around efficiency and scale. In parallel, the Commission review cycle for household washing machines and washer-dryers, based on existing rules under Regulations (EU) 2019/2023 and (EU) 2019/2014 with a revision review scheduled for December 2025, supports further product-cycle upgrades in energy and water performance, serviceability, and digital product information. This creates a runway for differentiated offerings in compact formats and high-efficiency drying solutions.

Recent Industry Developments

- June 2026: Arcelik agreed to acquire Whirlpool Corporation's remaining 25% stake in Beko Europe for EUR 71.5 million, moving the joint venture to full Arcelik ownership. The step simplifies governance and can accelerate portfolio and manufacturing decisions across Europe under a single controller, sharpening competitive pressure on incumbents.

- April 2026: BSH Hausgeraete reached an agreement with employee representatives on a social plan tied to the closure of its Nauen washing-machine production, with shutdown scheduled for June 30, 2027. The move signals longer-horizon restructuring of European manufacturing footprints, with implications for sourcing, allocation, and service parts planning.

- July 2024: The European Commission implemented the A-to-G energy label for tumble dryers alongside updated ecodesign and labelling measures, steering the category toward higher-efficiency technology choices. This regulatory reset tightened shelf eligibility and made energy-class visibility a stronger driver of product positioning and retailer merchandising across Europe.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers laundry appliances sold in Europe that are used to wash and dry clothes, including household-focused machines and their related product formats, measured in revenue terms at the market level.

Scope exclusions: We exclude laundry detergents and additives, repair-only services, and standalone spare parts that are not sold as part of a new appliance sale.

Segmentation Overview

- By Product Type

- Stand-alone Washing Machines

- Stand-alone Drying Machines / Dryers

- Combined Washer-Dryers

- By Loading Type

- Front-Load

- Top-Load

- By Capacity

- Below 6 Kg

- 6 - 8 Kg

- Above 8 Kg

- By Usage

- Residential

- Commercial (laundromats, hospitals, hotels, hostels, etc.)

- By Distribution Channel

- B2B / Direct from Manufacturers

- B2C / Retail Consumers

- By Geography

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the fact base for demand and supply signals that are visible in public data. We referenced sources such as Eurostat household and housing statistics, UN Comtrade trade flows for relevant appliance codes, and national statistics offices for population, household formation, and durable goods ownership. To keep assumptions realistic at the country level, we also reviewed EU Commission materials on energy labels and ecodesign rules, plus consumer price index series published by central banks and statistical agencies.

After that, we used company annual reports, investor presentations, and audited filings to understand how revenue is reported, how Europe is defined, and how pricing changed over time. In a few places, we also used paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level trade databases, mainly to speed up cross-checks and reduce manual cleaning. The sources listed here are illustrative and not exhaustive, and many other public documents and data tables were referred to during collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to convert broad indicators into practical sizing inputs, especially where public data is not fully aligned with product boundaries. We spoke with a mix of manufacturers, distributors, retailers, service ecosystem participants, and category specialists across major European markets so that pricing, replacement cycles, and mix shifts could be validated. Inputs from these discussions were used to test the split between washers, dryers, and other formats, and to confirm how online sales, promotions, and energy-efficiency upgrades are affecting realized prices.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | |

| Mid tier: 57% | Functional/Unit leaders: 32% | |

| Smaller Players: 18% | Managers: 55% |

Market-Sizing & Forecasting

Our core sizing starts from a top-down demand pool build using household stock, appliance penetration, and replacement timing by country, which is then converted into annual unit demand before being priced to revenue using observed price bands. To keep the totals practical, results are corroborated with selective bottom-up checks such as sampled country level average selling price times shipment volume, retailer channel checks, and supplier revenue splits for Europe where disclosure allows.

Key inputs that shaped the model included household growth and urban housing mix, renovation and home turnover indicators, washer versus dryer attachment rates, energy-label driven feature upgrades that shift price points, and online share changes that influence promotional intensity. We also monitored import reliance and intra-Europe trade patterns to sanity check supply availability and mix shifts. Forecasts were built using scenario analysis supported by a light multivariate regression on household formation, real disposable income trend, and appliance price inflation, and then adjusted based on expert views on replacement cycles and premiumization. Where country detail was thin, gaps were handled by using peer-country analogs with similar housing stock and income levels, and then re-tested in interviews before finalizing.

Data Validation & Update Cycle

Validation was done through multiple cross-checks so the final numbers stay consistent with real-world signals. We compared outcomes against independent markers such as appliance trade value trends, country-level consumer spending direction, and company-reported regional performance, and then reworked any country that broke these checks.

A second analyst review is used to inspect unusual swings, mix changes, and pricing jumps, and follow-up calls are triggered when a key assumption changes materially. Reports are refreshed annually, and interim updates are added when regulation, macro shocks, or major channel changes alter demand expectations. Before delivery, the latest public updates are re-checked so clients receive a current view.

Mordor Intelligence's Europe Laundry Appliances Market Market Size Measured Against Other Published Estimates

Published market sizes for Europe laundry appliances can differ even when the category name looks the same, because the counted products, pricing level, and geographic coverage are not always aligned. In practice, the biggest gaps usually come from whether the estimate is built from household demand and replacement behavior, or from producer-side revenue and trade values that may not capture the same boundary.

Trade values, country-level appliance indicators, and consumer price inflation are the checks that keep Mordor Intelligence tied to a Europe-wide end-market revenue view that follows the report country list and the included appliance set (washing machines, dryers, and other laundry appliances). Other estimates often move because some use EU-only coverage instead of Europe, some mix in institutional and commercial demand without clearly separating it, and some apply wholesale pricing that removes parts of channel value that buyers commonly expect in a market value number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.83 B (2025) | |

| Regional Consultancy A | USD 14.80 B (2026) | Uses a different base year and can include institutional or commercial laundry demand, which shifts assumed unit demand and average selling prices compared with a household-led Europe view. |

| Trade Journal B | USD 6.60 B (2024) | States EU household washing and drying machines at nominal wholesale value and excludes logistics, retail margins, and marketing costs, so the total is not comparable to a Europe end-market revenue number. |

The spread in the table is mainly explained by geography selection (EU versus Europe), the pricing level used (wholesale versus end-market value), and whether non-household demand is blended into the total. By keeping the inputs traceable to household demand, replacement cycles, and visible pricing signals, the resulting figure stays easier to reproduce and to update when conditions change.

Key Questions Answered in the Report

What is the forecast value of the Europe laundry appliance market by 2031?

Market value is expected to reach USD 19.21 billion, growing at a 2.23% CAGR.

Which country currently leads sales of laundry appliances in Europe?

Germany leads with 26.85% share thanks to a large economy, manufacturing depth, and premium-brand affinity.

Why are combined washer-dryers gaining popularity?

Urban apartment sizes are shrinking, and heat-pump technology now delivers energy-class A performance in one compact cabinet.

How will EU regulations affect tumble-dryer technology from 2025 onward?

Only highly efficient heat-pump models will remain on shelves after the A-to-G label transition, driving early replacement of older units.

What strategic move reshaped competition in 2024?

Whirlpool and Arçelik created Beko Europe, a 24-million-unit capacity entity that boosts scale and R&D leverage.

Which segment is growing faster—commercial or residential?

Commercial installations are advancing at 6.74% CAGR, outpacing residential upgrades due to strict hygiene standards.

Page last updated on: