Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.09 Billion |

| Market Size (2026) | USD 13.61 Billion |

| Market Size (2031) | USD 16.49 Billion |

| Growth Rate (2026 - 2031) | 3.91% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Washing Machine Market Analysis by Mordor Intelligence

The Europe washing machine market size is expected to grow from USD 13.09 billion in 2025 to USD 13.61 billion in 2026 and is projected to reach USD 16.49 billion by 2031, registering a CAGR of 3.91% from 2026 to 2031. The Europe washing machine market is moving through a pivotal phase shaped by stricter European Union efficiency frameworks, faster replacement behavior, and premium features that lift average selling prices while improving lifecycle value[1]European Commission, “Energy Labelling and Ecodesign Frameworks,” European Commission, commission.europa.eu. Product development is accelerating in response to the 2021 rescaled A to G label that raised the bar for top-tier performance, with leading models now surpassing Class A by wide margins in energy use. Front-loaders continue to anchor category dynamics, while smart, Matter-enabled control ecosystems expand consumer appeal through easier app-based operation and energy-aware cycle scheduling. Competitive focus has shifted toward durability, repairability, microplastic mitigation, and secure interoperability, as brands align with new European Union rules and use firmware to keep installed products current across longer service lives.

Key Report Takeaways

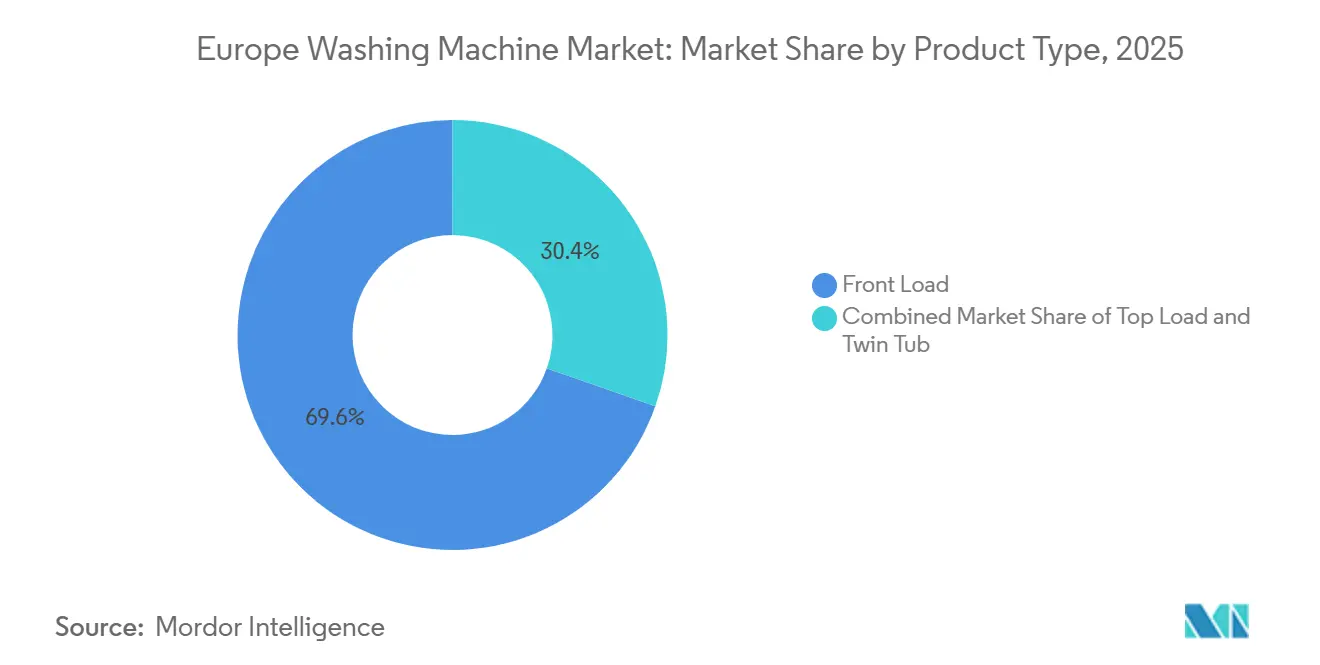

- By product type, front-load led with 69.62% revenue share of the Europe washing machine marketin 2025, and smart front-load IoT-enabled washers are forecast to expand at a 5.88% CAGR through 2031.

- By capacity, 5–8 kg commanded 46.25% share in 2025, while above-8 kg is projected to grow at a 4.55% CAGR through 2031.

- By technology, conventional held a 73.25% share of the Europe washing machine market in 2025, while smart/connected IoT machines are expected to post a 6.12% CAGR through 2031.

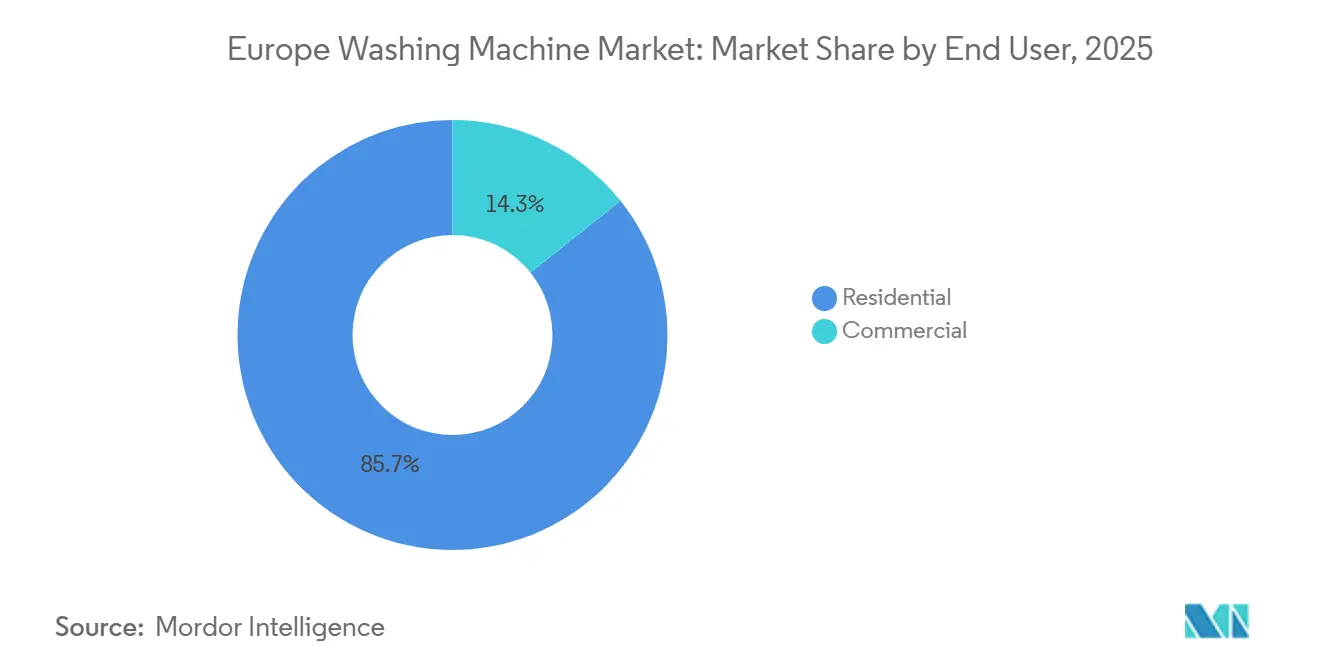

- By end-user, residential accounted for 85.74% of the Europe washing machine market size in 2025, while commercial is projected to expand at a 4.65% CAGR through 2031.

- By distribution channel, B2C/retail captured 57.98% of sales in 2025, while online/digital B2C is forecast to grow at a 4.86% CAGR through 2031.

- By geography, Germany held a 28.34% share in 2025, while Spain is projected to post the fastest growth at a 4.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Washing Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Union Energy Label and Ecodesign Tightening Shift Demand Toward High-Efficiency A–C Class Washers | +1.2% | European Union-wide, strongest in Germany, France, Nordics | Medium term (2-4 years) |

| Replacement Cycle Acceleration from the Aging Installed Base and Post-Pandemic Usage Intensity | +1.0% | Western Europe with spill-over to BENELUX | Short term (≤ 2 years) |

| Migration To Larger Drum Sizes (≥8 Kg) For Bulky Textiles and Family Loads | +0.6% | Germany, United Kingdom, BENELUX, multi-generational households | Medium term (2-4 years) |

| Omnichannel Retail Scale-Up Lifts Category Throughput | +0.5% | National, early gains in the United Kingdom, Germany, Netherlands | Short term (≤ 2 years) |

| France's 2025 Microfiber-Filter Rule Catalyzes Redesign And Upsell | +0.4% | Pan-European, strongest in France, the Netherlands, Nordics | Medium term (2-4 years) |

| Repairability scores and modular design premiumize TCO value | +0.3% | France, Belgium, Germany, and a broad European Union adoption by 2026 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

European Union Energy Label and Ecodesign Tightening Shift Demand Toward High-Efficiency A–C Class Washers

The 2021 rescale of the energy label replaced A+++, A++, and A+ with a single A to G scale, which reset the top tier to stimulate further innovation and pushed manufacturers to deliver beyond prior thresholds. By late 2025, flagship models like Samsung’s Bespoke AI Washer A-65% demonstrated class lower consumption versus the Class A minimum on the standardized test load, signaling rapid gains in core energy performance. The Ecodesign for Sustainable Products Regulation, effective July 2024, expands the policy lens to durability, repairability, recyclability, and Digital Product Passports, reinforcing a system view of lifecycle performance that favors brands able to validate and update claims over time. The European Commission’s 2025–2030 Ecodesign Work Plan names washing machines among priority product groups, with expected delegated acts from 2026 and modeled household savings by 2030 that strengthen the case for efficient replacements. Leading manufacturers are commercializing higher efficiency at accessible price points, as shown by Miele’s 2025 EnergyHero model positioned with 40% better economy than the Class A threshold in a widely available configuration.

Replacement Cycle Acceleration from Aging Installed Base and Post-Pandemic Usage Intensity

Installed bases across Western Europe are maturing, and many units purchased during the 2005–2015 expansion wave are now at or beyond typical replacement windows, which has led to elevated replacement activity since 2024. Field telemetry shows changing wash behavior, with Electrolux’s analysis of millions of cycles in 2024 indicating a shift toward more frequent, shorter programs that add wear to key components and nudge upgrades earlier than planned[2]Electrolux Group, “Speed Laundering Report 2025,” Electrolux Group, electrolux.com. The European Union Right to Repair Directive 2024/1799 sets 10-year repair obligations and better access to spare parts and technical information, which is improving transparency and shaping buyer expectations for the next generation of units. Member states are moving to transpose the directive by July 31, 2026, and Germany introduced a national draft in January 2026 that signaled steady progress toward harmonized implementation. In the transition period, some consumers are replacing sooner to capture higher efficiency and repairability before national transposition is complete, which contributes to short-term volume support in several Western markets.

Migration to Larger Drum Sizes (≥8 kg) for Bulky Textiles and Family Loads

Above-8 kg capacity models are forecast to expand at a 4.55% CAGR through 2031, ahead of the 6–8 kg mainstream, as households opt for bigger drums to handle thick synthetics, bedding, and outerwear that previously required multiple runs. Product lines have shifted the baseline, with Miele elevating entry capacity to 8 kg and broadening quick and gentle cycle availability in everyday price bands. New features like Samsung’s AI Ecobubble and AI Wash+ improve cleaning and resource use for heavier loads by adjusting drum motion, water mixing, and detergent dosing in real time. Larger drums help time-constrained, dual-income households compress weekend laundry into fewer cycles, and they match the preferences of multi-generational homes that consolidate laundering to keep utility costs predictable. The result is a steady mix shift toward 8–11 kg platforms that integrate resource management with cycle performance to maintain label-leading efficiency across a wider load range.

Repairability Scores and Modular Design Differentiation Premiumize TCO Value

France’s durability index for washing machines became operational in April 2025, requiring in-store display of a 1 to 10 score that factors robustness, ease of maintenance, spare-part policies, and software longevity, which moves buyers to consider the total cost of ownership rather than sticker price alone. Belgium adopted an aligned methodology in May 2025 to ease cross-border compliance and reinforce consistent consumer guidance across the region. The European Union Right to Repair Directive complements these efforts by codifying minimum repair standards and timelines, which support a shift toward modular designs with replaceable subassemblies and documented service procedures. Manufacturers are responding with offers that match the new rules, such as extended motor warranties and refurbishment pilots that make certified pre-owned options more visible on mainstream channels. Together, these measures foster a premium narrative built on longevity, upgradability through firmware, and predictable service economics that strengthen brand differentiation where products look similar.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Western Europe's near-saturated household penetration caps volume upsides | -0.8% | Western Europe's core markets | Long term (≥ 4 years) |

| Consumer budget pressure and elevated energy bills defer discretionary upgrades | -0.5% | Southern Europe with spill-over to the United Kingdom | Short term (≤ 2 years) |

| European Union right-to-repair extends product lifetimes, delaying replacements | -0.3% | Pan-European, strongest in Germany, France, Belgium, post-July 2026 | Long term (≥ 4 years) |

| Water scarcity tariffs and wastewater rules constrain intensive cycles | -0.2% | Southern Europe and Mediterranean regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Western Europe's Near-Saturated Household Penetration Caps Volume Upsides

Most households in Western Europe already own a washing machine, which limits unit growth and tilts market momentum toward replacements and product mix upgrades rather than new installations. In markets like Germany, procurement decisions in rentals often sit with property managers who stretch replacement intervals to manage capital budgets, which flattens unit trajectories despite technology advances. Consolidation strategies, such as forming Beko Europe from Whirlpool EMEA and Arçelik’s regional business, seek scale and fixed-cost leverage to operate profitably at low volume growth rates. European Union durability standards and longer-life design philosophies also lengthen service spans, which further constrain volume potential even as consumer expectations and regulation push for better performance and repairability[3]European Committee for Standardization, “EN 50731 Durability Standard,” CEN, cen.eu. Brands respond by emphasizing premium features, connectivity, and lifecycle service programs that expand revenue per unit over time rather than relying on frequent replacements.

Consumer Budget Pressure and Elevated Energy Bills Defer Discretionary Upgrades

Households in southern Europe and select United Kingdom subregions face tighter budgets and higher utility bills that keep some buyers in a repair-first mindset until failure or a major functional shortfall occurs. Even when efficient models offer long-term savings, immediate cash constraints slow adoption unless incentives, financing, or visible performance jumps can justify the spending. The European Union’s ecodesign and consumer information measures are improving transparency on long-run savings, but payback horizons still require consumers to discount future benefits amid short-run cost concerns. Brands are using clear energy and water savings in marketing to increase perceived value and align with time-of-use tariff benefits where available. Over the forecast period, gradual easing of inflation in some countries and broader access to financing could help unlock pending demand, yet pricing sensitivity remains a near-term cap on premiumization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: IoT Integration Reshapes Front-Load Dominance

Front-load machines commanded 69.62% of the Europe washing machine market share in 2025 as consumers favored high spin efficiency, lower water use, and under-counter fitness, and within this format, smart front-load variants are projected to grow at a 5.88% CAGR through 2031 as Matter-compatible controls make integration easier across home platforms. Leading launches since 2024 showcase touch-centric control and fabric-aware programs, with Samsung bringing AI Wash+ and a 7-inch AI Home interface into its European range and linking to SmartThings for energy-aware scheduling. BSH enabled a cross-brand experience through Home Connect and early adoption of Matter, lowering setup friction for buyers who prioritize seamless device onboarding and voice assistance. LG’s AI DD algorithms and connected ThinQ stack compete at similar price points, while Haier Europe’s hOn application gained multi-million active users across categories, anchoring engagement at the portfolio level. Top-load maintains a niche footprint where legacy preferences persist, and twin-tub designs continue in limited rural settings that value manual control and grid flexibility, though both subtypes see constrained innovation compared to front-load ecosystems.

Historical production constraints during 2020–2022 affected the availability of connected SKUs, but supply normalization and interoperability standards now allow brands to scale smart features across broader price tiers. Software paths have become a core differentiator as updates deliver new programs such as microplastic reduction cycles and allergen removal without hardware change, which extends relevance across the service life. Security and compliance requirements under the European Union’s emerging digital product framework increase the resources needed for safe connectivity, which reinforces incumbent advantages while raising hurdles for new entrants. Compact front-load combos with integrated heat-pump drying are gaining traction in urban retrofits, blending space savings with Class A complete-cycle ratings suited to apartments. Over the forecast period, the Europe washing machine market will continue to center on increasingly intelligent front-loaders as brands embed energy management and filtration capabilities that meet emerging ecodesign thresholds.

By Capacity: Above-8 kg Drums, Capture Family and Bulky-Load Premiums

The 6–8 kg tier held 46.25% of sales in 2025, balancing weekly laundry volume, energy label performance, and standard cabinetry fit for most European households. Above-8 kg platforms are the fastest-rising capacity choice with a 4.55% CAGR outlook, gaining favor among larger families and buyers who want to clear bedding, sportswear, and outerwear in fewer cycles. Product portfolios are resetting defaults upward, with manufacturers elevating entry capacity and offering precision dosing and mixed-load optimization so that bigger drums maintain low-resource profiles on partial loads. Premium series from incumbents also pair higher capacity with filtration and hygiene features, amplifying perceived value and reinforcing upselling logic for households considering a long-term unit. Space-constrained urban buyers benefit from compact formats that still achieve 6–8 kg without compromising door clearance or under-counter integration.

Innovations like multi-drum architecture and adaptive resource controls compress cycle time for mixed garments, which reduces the time cost of larger loads. Mixed fabric programs that protect delicate fabrics at low temperatures while addressing heavy soil on synthetics are replacing older assumptions that bigger drums trade off care quality for speed. Over the forecast, manufacturers are expected to fine-tune load-detection logic to push even higher accuracy in water and detergent use, which helps maintain Class A outcomes across variable loads. As entry price points migrate toward 8 kg and beyond, buyers will see less need to compromise on capacity even in compact-floorplan homes.

By Technology: Smart/Connected Machines Exploit Firmware Differentiation

Conventional units retained 73.25% of the mix in 2025, yet smart/connected IoT washers are set to be the fastest-growing technology group with a 6.12% CAGR that reflects advancing interoperability and tangible energy-management benefits. APPLiA has projected a rapid rise in connected washer ownership across European Union households, which supports a steady transition in new-unit sales toward embedded connectivity and cloud-based features. Grid-aware scheduling through platforms like SmartThings integrates machine operation with time-of-use tariffs to reduce consumption and shift loads to cleaner energy periods. Environmental features like microplastic-care cycles make it easier for households to achieve impact reductions without changing habits, which validates price premiums for connected SKUs. Warranties and refurbishment programs reassure value-focused buyers that smart hardware will remain serviceable across longer horizons, even as software continues to evolve.

Software security and lifecycle support are now central to purchase decisions in the Europe washing machine industry, as European Union digital requirements formalize patching practices and vulnerability handling for connected appliances. Matter compatibility simplifies onboarding and cross-brand control, making it easier for families to use apps they already trust to coordinate daily routines. Over-the-air updates that add wash programs or refine dosing logic keep devices current with evolving textiles and detergent chemistry, extending relevance well into the second decade of service. Conventional machines continue to appeal on initial price and perceived simplicity, which keeps the base broad even as connected share grows steadily. The Europe washing machine market is therefore bifurcating into software-forward platforms with recurring digital services and durable conventional lines optimized for long, low-maintenance lifecycles.

By End User: Commercial Deployments Monetize Subscription and Data Services

Residential customers represented 85.74% of 2025 revenue, while commercial sites are forecast to grow faster at a 4.65% CAGR by adopting predictive maintenance, remote management, and pay-per-use models. Property managers of multi-unit buildings are integrating connected washers with mobile access and cashless payments to improve tenant convenience and utilization while collecting performance data. Launderettes are upgraded to machines with precise dosing and specialized cycles to justify premium pricing per load, creating visible differentiation in crowded urban locations. Commercial systems emphasize uptime guarantees and modular repairs to keep revenue streams steady, which supports service contracts and fleet-level monitoring features. As right-to-repair and data-sharing rules take hold, multi-vendor service arrangements will become more common, improving cost control for operators while preserving flexibility across brands.

The Europe washing machine market will continue to rely on residential replacements in mature countries while pursuing greenfield gains in select catch-up regions, but commercial deployments add a recurring revenue layer that smooths sales cycles for leading manufacturers. Predictive diagnostics can minimize downtime windows and time for maintenance during low-demand periods, which raises effective throughput at busy locations. Remote configuration and firmware updates help operators roll out new cycles and sustainability features without onsite visits, aligning with brand commitments to lower total lifecycle impact. Over the forecast, growth in commercials will reflect the economics of multi-unit purchases and service contracts, with connectivity translating directly into revenue and retention advantages. Residential adoption of similar features should continue to trail commercials in direct monetization but will benefit from the same pipeline and reliability improvements.

By Distribution Channel: Online B2C Gains as Assortment and Logistics Scale

B2C/retail channels accounted for 57.98% of 2025 sales, and online B2C is the fastest-growing sub-channel with a 4.86% CAGR as consumers use digital paths for selection, financing, and delivery coordination at scale. Manufacturers are leveraging showroom-style brand outlets to demonstrate interfaces and dosing features, then route transactions to direct digital stores to capture data and offer tailored service bundles. Online marketplaces and brand-owned stores differentiate with installation and haul-away commitments that reduce friction for bulky goods purchases and improve trust in delivery windows. In parallel, direct ecosystems link installation with app onboarding and energy settings to ensure immediate value realization from day one. Traditional multi-brand showrooms remain important for tactile evaluation and serve as high-conversion feeders into digital checkout flows where promotions and financing are easiest to apply.

The Europe washing machine market is also seeing the rise of brand-operated partner portals for B2B buyers, which support centralized procurement and fleet management for commercial operators. As regulation increases transparency in digital marketplaces, listing and ranking clarity will raise the bar for product data and warranty disclosures, benefiting established brands with strong content operations. Over time, the combination of channel breadth, last-mile reliability, and digital configuration will determine share shifts inside B2C, particularly in countries with dense delivery networks and robust returns handling. Richer first-party data from direct channels will feed product and service design loops that focus on in-use outcomes rather than only pre-sale features. These shifts reinforce a service-led posture that can lift value per unit while still meeting stricter policy goals on repair and durability.

Geography Analysis

Germany held 28.34% of the Europe washing machine market share in 2025, supported by domestic engineering leaders, demand for premium features, and early policy transposition that sets benchmarks for the rest of the European Union. BSH continues to invest in high-efficiency lines that exceed Class A minimum and pair with Home Connect functionality to embed resource optimization in everyday use. The country initiated a draft law in January 2026 to implement European Union right-to-repair provisions, signaling policy continuity and operational clarity for the next model cycle. France, the second-largest market, has become a policy reference point with its durability index for washing machines effective since April 2025, which provides standardized guidance for consumers on reliability and maintenance[4]Service Public France, “Durability Index for Appliances,” Government of France, service-public.fr. Premium buyers in France have shown sustained interest in quiet operation and compact, built-in designs, areas where German-engineered SKUs have performed well.

Spain is projected to be the fastest-growing country through 2031, and the Europe washing machine market size for Spain is set to expand at a 4.55% CAGR as new households form in its largest cities and infrastructure catches up to northern peers. Value-led brands that meet Class B or C ratings continue to gain share at mid-range price points, while financing and loyalty programs widen access to A-class models for urban buyers. Italy’s structure favors independent specialists more than some neighbors, which slows full omnichannel integration but preserves advisory-led selling in regional catchments. The United Kingdom, outside the European Union but broadly aligned to energy-efficiency norms for exporters, shows strong online penetration for major appliances and faster uptake of connected washers among early adopters. Within-country disparities persist, with premium hubs adopting advanced energy features sooner than value-led regions.

BENELUX and the Nordics contribute robust value relative to population due to high incomes, early smart-home adoption, and public procurement norms that reward best-in-class performance on resource use. Belgium’s adoption of France’s durability index methodology underlines a shared approach to consumer transparency that may reduce compliance friction for brands selling across borders. Nordic buyers are attentive to energy and water performance and benefit from widespread time-of-use tariffs that heighten the utility of grid-aware scheduling in connected ecosystems. Eastern and southern countries outside the core still present greenfield potential in select pockets where penetration is lower, though income and broadband constraints temper near-term connected adoption. Across the region, policies on repair and product passports are creating a common compliance framework that should tighten performance dispersion and focus competition on usability and service.

Competitive Landscape

Competition has pivoted away from broad price wars toward differentiation in firmware longevity, microfiber mitigation, and interoperability with smart-home standards that make devices easier to deploy and maintain. Product milestones from 2024 include Class A-plus performance margins for flagship washers and new AI-driven dosing and fabric detection routines meant to improve outcomes at lower temperatures and with reduced water. Extended warranties and official refurbishment channels are becoming important levers to capture value and demonstrate confidence in long service lives, particularly in markets that emphasize repair scores at the point of sale. The Europe washing machine market therefore rewards engineering depth and compliance readiness alongside software roadmaps that keep installed units current through updates.

Strategic consolidation remains a rational response to saturated Western Europe volumes, with the Beko Europe structure aiming to rationalize overlapping factories and unify distribution coverage from Western to Eastern markets. Component and module control has become more salient as connected features take hold, with vertically integrated brands advantaged in supply resilience and firmware delivery cadence. Interoperability moves, such as early partnerships around Matter, signal intent to remove onboarding friction and reassure buyers that ecosystems will remain open and secure across device generations. Ecosystem apps continue to broaden into energy services and consumables, linking core cycles with detergent optimization and maintenance reminders that sustain user engagement. Regulatory programs, including the Digital Product Passport, are further professionalizing product data management and creating opportunities for compliance-led differentiation.

Microplastic initiatives are another fast-maturing battleground where brands are piloting integrated capture and reduction cycles to pre-empt standardization outcomes and position for premium buyers. Partnerships with filtration specialists highlight how different paths to compliance may converge around validated capture metrics and maintenance-friendly designs. The strongest incumbents are aligning value propositions with a longer-planned service life and an app-first user model that supports continuous improvements without hardware changes. As the Europe washing machine market enters the next cycle, competitive strategies will blend policy leadership, industrial design, and software that monetize service and sustainability rather than only headline specifications. Over the forecast horizon, the brands that balance firmware innovation with durability and transparent service economics are best placed to defend and expand share.

Europe Washing Machine Industry Leaders

BSH Hausgeräte GmbH

Beko Europe B.V.

Electrolux Group

Haier Europe

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Samsung Electronics unveiled the Bespoke AI Washer A-65% at IFA 2025, achieving 65% better energy efficiency than the Class A minimum, with AI Wash+ detection, a 7-inch AI Home touchscreen, and SmartThings integration enabling energy-aware scheduling; Samsung also launched a second-generation Bespoke AI Laundry Combo with expanded drying capacity and shorter drying times.

- September 2025: BSH Home Appliances launched Bosch Series 8 washing machines at IFA 2025 with 11 kg capacity, efficiency beyond the Class A floor, i-Dos with Detergent Scan, and deeper Home Connect integration, while expanding its Matter partnership and self-cleaning microfiber filter concept.

- September 2025: Haier Europe showcased Candy’s MultiWash at IFA 2025, a three-drum washing machine coordinated by an AI Intelligent Central System to manage water and electricity across simultaneous customized programs, while confirming that its hOn app surpassed 10 million connected users.

- August 2025: LG Electronics introduced the LG HeatPump WasherDryer (WashCombo) at IFA 2025, achieving Energy Class A for complete wash-dry cycles using DUAL Inverter HeatPump technology based on R290 refrigerant, alongside a Microplastic Care Cycle that targets synthetic-fiber release reductions.

Europe Washing Machine Market Report Scope

A washing machine is an electronic home appliance that is used to wash various types of clothes without applying any physical effort. A complete background analysis of the Europe Washing Machine Market, which includes an assessment of the emerging trends by segments and regional markets, significant changes in market dynamics, and market overview, is covered in the report. The Europe Washing Machine Market is segmented by Product Type (Front Load and Top Load), by Technology (Fully automatic and Semi-automatic), by Distribution Channel (Multi-brand Stores, Specialty Stores, Online and Other Distribution Channels), and by Geography (Germany, United Kingdom, France, Italy, Switzerland, Russia, Rest of Europe).

By Product Type

| Front Load | With Dryers |

| Without Dryers | |

| Top Load | With Dryers |

| Without Dryers | |

| Twin Tub |

By Capacity

| Below 5 kg |

| 5 - 8 kg |

| Above 8 kg |

By Technology

| Conventional |

| Smart / Connected (IoT) |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly from the Manufacturers |

By Geography (Europe)

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Product Type | Front Load | With Dryers |

| Without Dryers | ||

| Top Load | With Dryers | |

| Without Dryers | ||

| Twin Tub | ||

| By Capacity | Below 5 kg | |

| 5 - 8 kg | ||

| Above 8 kg | ||

| By Technology | Conventional | |

| Smart / Connected (IoT) | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly from the Manufacturers | ||

| By Geography (Europe) | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the Europe washing machine market growth outlook for 2031?

The Europe washing machine market size is projected to reach USD 16.49 billion by 2031 at a 3.91% CAGR from 2026 to 2031.

Which product format leads sales in Europe?

Front-load washers lead with a 69.62% share in 2025, supported by efficiency, space-saving, and stronger spin performance that shortens drying time.

Where is the fastest country-level growth expected?

Spain shows the fastest trajectory to 2031, with the Europe washing machine market size for the country set to expand at a 4.55% CAGR as urban household formation and upgrades continue.

How are European Union policies influencing product strategy?

The 2021 energy label rescale, ESPR, and Right to Repair are steering designs toward high efficiency, long service life, and transparent repair, which strengthens premium and connected offers.

What technologies are expanding the most?

Smart/Connected IoT washers are the fastest-growing technology group with a 6.12% CAGR, driven by Matter interoperability, energy-aware scheduling, and firmware-based feature updates.

Page last updated on: