Europe Electronic Contract Manufacturing and Design Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

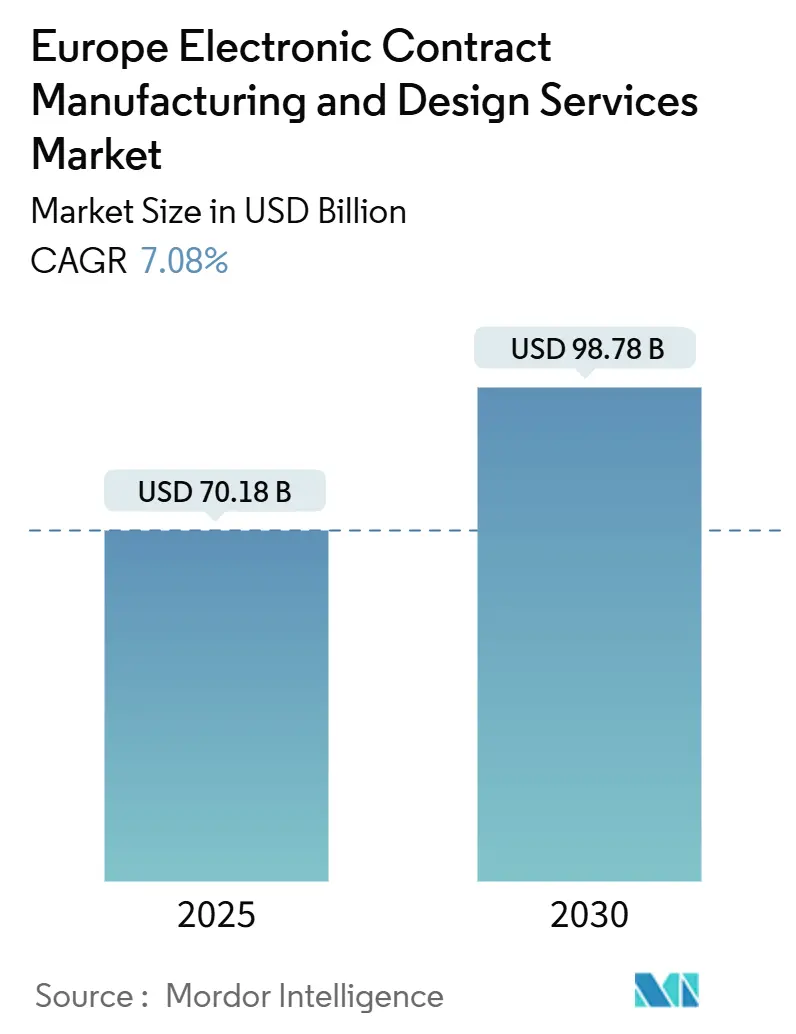

| Market Size (2025) | USD 70.18 Billion |

| Market Size (2030) | USD 98.78 Billion |

| Growth Rate (2025 - 2030) | 7.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electronic Contract Manufacturing and Design Services Market Analysis by Mordor Intelligence

The Europe electronic contract manufacturing and design services market size stands at USD 70.18 billion in 2025 and is on track to reach USD 98.78 billion by 2030, reflecting a 7.08% CAGR through the forecast period. This sustained expansion mirrors a regional pivot toward supply-chain sovereignty: European OEMs are outsourcing increasingly complex electronics even as they reshore selected high-value programs to mitigate exposure to Asian production concentrations. Investments stimulated by the EU Chips Act, rapid Industry 4.0 deployments across EMS plants, and surging demand from e-mobility and medical technology jointly reinforce market momentum. Early-2025 indicators point to recovering order backlogs following the 2024 inventory correction cycle, while digital twin adoption is driving measurable efficiency gains at leading facilities. That said, the sector must still navigate skilled-labor shortages, volatile component lead times, and elevated energy prices.

Key Report Takeaways

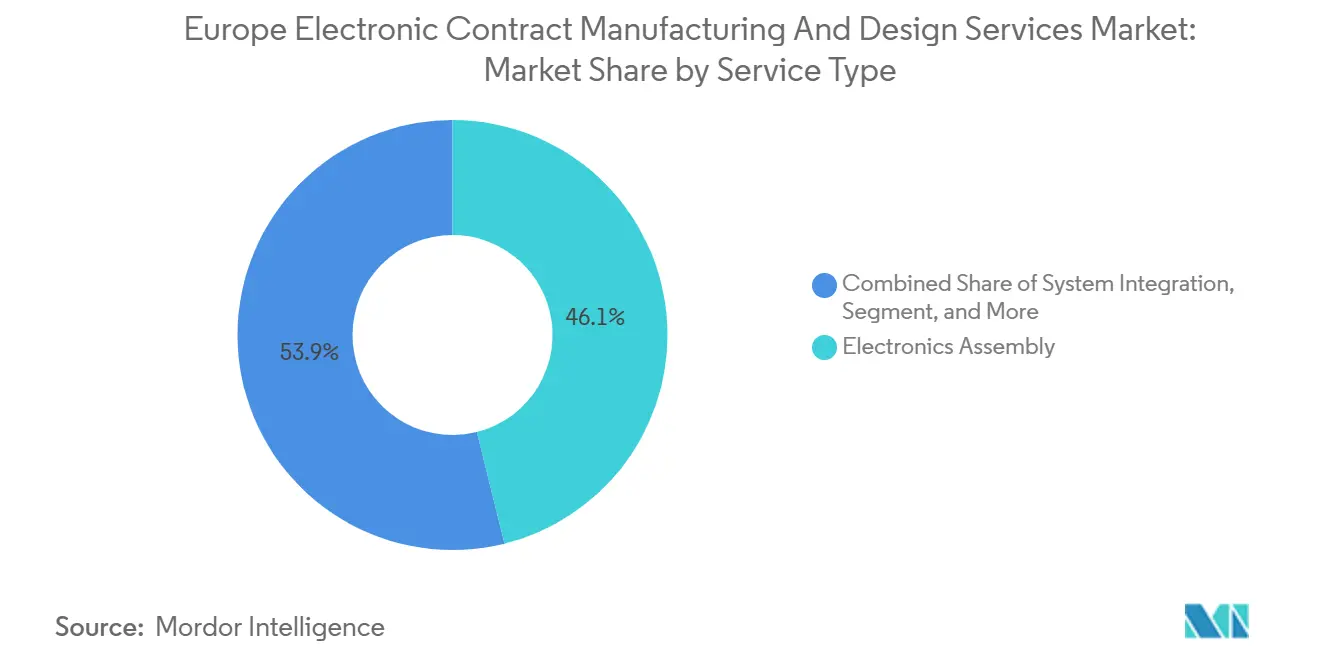

- By service type, electronics assembly led with 46.12% of the Europe electronic contract manufacturing and design services market share in 2024. Engineering design is advancing at a 7.81% CAGR to 2030.

- By end-use industry, industrial and robotics accounted for 28.36% of the Europe electronic contract manufacturing and design services market size in 2024. Healthcare and medical devices is poised to expand at an 8.12% CAGR through 2030.

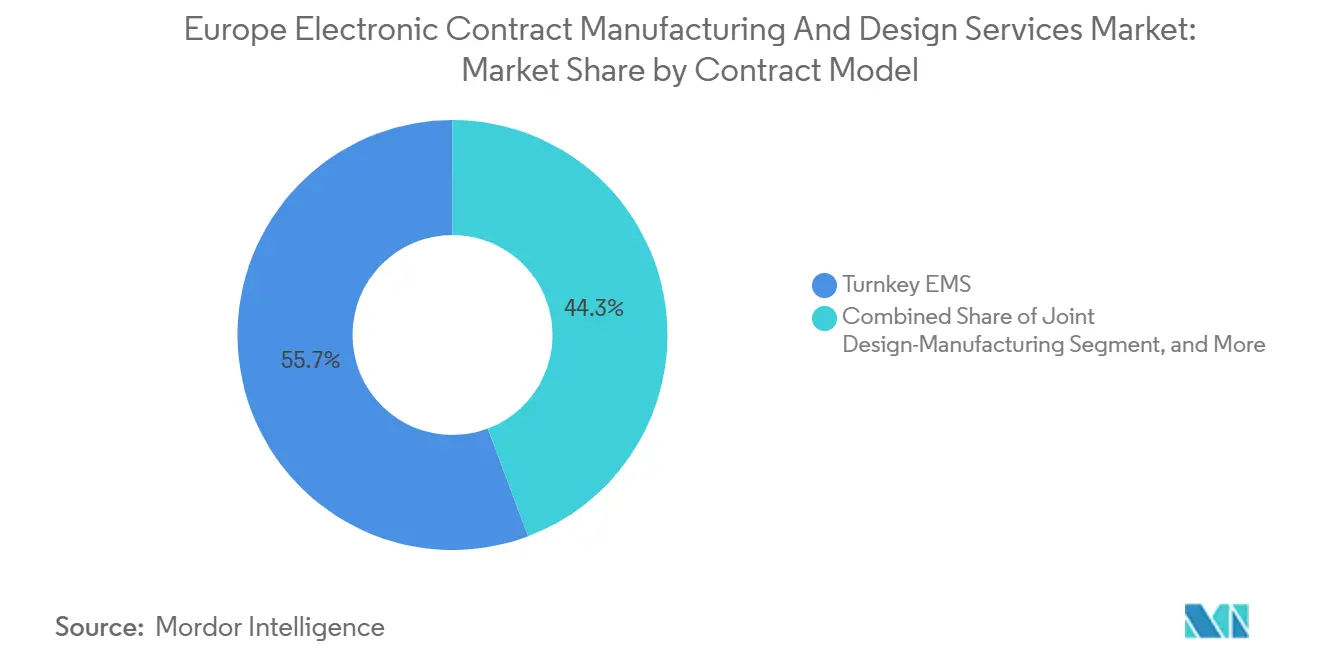

- By contract model, turnkey EMS captured 55.74% of the Europe electronic contract manufacturing and design services market size in 2024, while joint design-manufacturing relationships are growing at an 8.56% CAGR.

- By company size, firms with USD 20–100 million revenue are projected to rise at a 9.71% CAGR, even though providers generating above USD 500 million still hold 48.06% share.

- By geography, Germany contributed 22.51% revenue share in 2024, whereas Poland is forecast to post an 8.41% CAGR between 2025 and 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Electronic Contract Manufacturing and Design Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating outsourcing of complex electronics | +1.2% | Germany, France, Italy, Nordic region | Medium term (2–4 years) |

| Reshoring incentives and supply-chain nationalisation programs | +1.8% | EU-wide, strongest in Germany and Eastern Europe | Long term (≥ 4 years) |

| Growing adoption of Industry 4.0 and digital twins across EMS plants | +1.0% | Germany, Netherlands, Austria, Czech Republic | Medium term (2–4 years) |

| Demand spike from e-mobility power electronics and battery management systems | +1.4% | Germany, France, Sweden, Hungary | Short term (≤ 2 years) |

| Expansion of smart-medtech and wearable device manufacturing | +0.9% | Switzerland, Germany, Ireland, Denmark | Medium term (2–4 years) |

| Near-term inventory rightsizing after 2022–2023 bullwhip distortion | +0.5% | EU-wide, especially Germany and Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Outsourcing of Complex Electronics by European OEMs

Automotive tier-ones and industrial automation leaders are expanding EMS partnerships to offload advanced driver-assistance, high-density powertrain, and edge-AI modules, thereby avoiding fresh CAPEX while accessing state-of-the-art process equipment. Bosch, Continental, and ZF signed multi-year agreements with regional EMS houses for next-generation inverter boards in 2024. Infineon’s packaging and test alliance with Amkor in Porto highlights the shift from in-house to external specialists for once-in-house steps.[1]Infineon Technologies, “Infineon and Amkor Deepen Partnership,” infineon.com Source: in4ma, “Half-Year Statistics 2025,” in4ma.de Stronger collaboration now spans life-cycle testing and field-failure analytics, pushing EMS providers into roles traditionally reserved for OEM engineering teams.

Demand Spike from E-Mobility Power Electronics and Battery Management Systems

EV penetration surpassed 22% of regional light-vehicle sales in 2025, catalyzing call-offs for high-current boards, SiC inverter stacks, and battery management controllers. Semikron-Danaher and Infineon expanded the outsourcing of press-fit assembly to support Bosch’s rollout of the ninth-generation e-axle. Automotive functional-safety constraints anchor this work in established European sites where ASIL-D certification experience exists.

Expansion of Smart-MedTech and Wearable Device Manufacturing

Post-pandemic healthcare policies accelerated procurement of connected diagnostic equipment and continuous remote-monitoring devices. Swiss-based EMS plants with ISO 13485 accreditation doubled surface-mount capacity in 2024. Ireland’s med-tech corridor added micro-fluidics back-end lines capable of sub-15 µm placement accuracy, attracting start-ups commercializing implantable biosensors.

Near-Term Inventory Rightsizing After 2022-2023 Bullwhip Distortion

Channel partners curtailed bookings throughout 2024, but destocking largely concluded by Q1 2025, enabling EMS providers to normalize WIP days. in4ma reports rising book-to-bill ratios above 1.05 across the D-A-CH cluster during April 2025. Healthy backlog visibility now underpins capex for selective capacity debottlenecking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labour Shortage And Rising Wage Inflation In Manufacturing Hubs | -1.1% | Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Persistent Component Lead-Time Volatility And Allocation Risk | -0.8% | EU-wide, particularly affecting automotive and industrial segments | Medium term (2-4 years) |

| High Capex Barrier For Advanced Assembly And Testing Lines | -0.6% | Germany, France, Italy, Switzerland | Medium term (2-4 years) |

| Intensifying Energy-Price Volatility Impacting Cost Structures | -0.4% | Germany, Netherlands, Belgium, energy-intensive manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled Labour Shortage and Rising Wage Inflation in Manufacturing Hubs

Germany alone is expected to enter 2025 short of 13,000 SMT technicians, press-fit specialists, and test engineers needed for planned semiconductor fabs. Wage rates in Bavaria and Baden-Württemberg increased by 6–8% year-on-year in 2024, narrowing the landed-cost gap with select Asian locations. Policymakers responded by funding dual-education pathways; however, the talent deficit remains acute for high-mix, low-volume lines that require process-capability expertise.[2]European Commission, “IPCEI Microelectronics Workforce Strategy,” europa.eu

Persistent Component Lead-Time Volatility and Allocation Risk

Although headline shortages eased in 2025, automotive-grade microcontrollers, SiC MOSFETs, and certain MLCC types continue facing allocation windows exceeding 40 weeks. Smaller EMS houses lack purchasing power for guaranteed allocations and must carry higher buffer stocks, inflating working capital. Many diversify toward regional distributors but encounter extended qualification cycles that delay NPI ramps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Engineering Design Accelerates Innovation Partnerships

Engineering design captured renewed priority, expanding at a 7.81% CAGR through 2030 as OEMs seek collaborative ideation frameworks that compress time-to-market. Electronics assembly still supplied 46.12% of the Europe electronic contract manufacturing and design services market share in 2024, anchored by steady consumer and industrial volumes. System integration rose on the back of turnkey edge-AI gateways, while aftermarket services monetized circular economy mandates.

The Europe electronic contract manufacturing and design services market size for engineering design is projected to climb further as ASIC design houses such as IC’Alps formalize foundry alliances that cover tape-out to final test, shortening prototype cycles by up to 30 days. Joint design-manufacturing arrangements likewise grow at an 8.56% CAGR, underscoring the competitive weight of unified DFM, regulatory validation, and volume transfer capabilities.

By End-Use Industry: Healthcare Drives Premium Service Demand

Electronic manufacturing services for healthcare and medical devices are expected to register an 8.12% CAGR, driven by surgical robotics, connected drug-delivery platforms, and Class III implantables that require ISO 13485 traceability. Industrial and robotics maintained the largest slice, equal to 28.36% of the Europe electronic contract manufacturing and design services market size in 2024, thanks to sustained automation spending across EU factories.

The Europe electronic contract manufacturing and design services industry benefits where medical OEMs outsource PCB-As requiring stringent biocompatibility and 100% electronic lot history. Polish EMS entities such as Assel invested in bio-cleanroom upgrades to capture this premium segment. Automotive electrification, meanwhile, anchors mid-term volume through inverter boards and thermal-management controllers.

By Contract Model: Joint Design-Manufacturing Partnerships Reshape Relationships

Turnkey projects accounted for 55.74% of 2024 bookings, underscoring OEMs' preference for single-point responsibility that encompasses procurement, build, and logistics. Yet joint design-manufacturing projects, scaling at 8.56% CAGR, illustrate an evolution toward shared IP generation and early-stage co-engineering that improves manufacturability and regulatory compliance.

This shift favors EMS providers investing in EDA toolchains, simulation labs, and certification consulting. The Europe electronic contract manufacturing and design services market size attached to joint design-manufacturing is forecast to expand disproportionately in automotive ADAS modules, where functional-safety reviews commence at concept freeze. Consignment and build-to-print niches persist where legacy BOM ownership or sensitive semiconductor content dictates OEM control.

By Company Size: Small Providers Capitalize on Specialization Opportunities

While providers exceeding USD 500 million capture 48.06% share, firms in the USD 20–100 million band clock a 9.71% CAGR, reflecting nimble pivots into med-tech, avionics LRUs, and after-sales repair. Regional champions employ deep domain know-how, bilingual technical sales, and proximity advantages to dislodge larger rivals in low-volume, high-complexity tenders.

M&A remains active: Variosystems’ purchase of Schurter Solutions and Cicor’s NEP acquisition strengthen regional footprints, but dozens of founder-led specialists remain independent. These niche players anchor the fragmented long-tail of the Europe electronic contract manufacturing and design services market, offering OEMs redundancy and local language program management.

Geography Analysis

Germany retained a 22.51% revenue share in 2024, driven by automotive and sophisticated industrial automation projects. Capacity additions are closely tied to public-private programs, such as IPCEI-Microelectronics, which subsidize high-complexity backend lines. However, energy costs running 20–25% above the EU median, as well as acute engineering vacancies, dampened some 2024 margins. Firms respond by colocating high-labor content work in Slovakia or Hungary while keeping pilot lines and final test in Bavaria.

Poland is on course for an 8.41% CAGR to 2030, supported by FDI flows from Western OEMs seeking nearshored capacity within the single market. Electronics parks near Wroclaw and Gdansk benefit from logistics corridors that shorten lead times versus East Asia. Government R&D grants under the Smart Growth Operational Program further encourage investments in automation.[3]Sertec 360, “Company Profile,” sertec360.com

France, Italy, Spain, and the United Kingdom supply mature demand anchored in aerospace, rail, and defense. France is expected to show a recovery in early 2025 for aerospace LRUs as Airbus output normalizes, while Switzerland is enjoying double-digit momentum in wearable diagnostics. Nordic countries specialize in telecom baseband and ruggedized industrial PCs but see heightened consolidation, evidenced by 43 EMS M&A deals across 2019–2025.

Competitive Landscape

The Europe electronic contract manufacturing and design services market exhibits moderate fragmentation: the top five providers collectively controlled slightly above 45% revenue in 2024. Consolidation is accelerating through acquisitions that bundle complementary process expertise, secure strategic customers, and expand geographic reach. Cicor’s 2024 purchase of NEP and ongoing German target negotiations exemplify this roll-up play.

Technology investments set the competitive tempo. Leading firms implement AI-driven SPI correction loops, autonomous material replenishment guided by AMR fleets, and cloud-hosted digital twins. Compliance proficiency presents additional barriers, including ISO 13485 for medical devices, ISO 26262 for automotive functional safety, EN 9100 for aerospace, and TISAX for data security.

Strategic alliances deepen vertical integration. Infineon-Amkor’s Portugal site secures power semiconductor back-end capacity, while photonixFAB’s EUR 47.6 million (USD 54.89 million) program builds EU photonics pilot lines that EMS houses can leverage for early-volume optical transceiver work. Smaller specialists stay competitive by offering extreme micro-assembly, repair services, and multilingual engineering support.

Europe Electronic Contract Manufacturing and Design Services Industry Leaders

Hon Hai Precision Industry Co. Ltd. (Foxconn)

Flex Ltd.

Jabil Inc.

Zollner Elektronik AG

GPV International A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: in4ma released statistics covering 427 EMS companies and EUR 20 billion revenue, extending D-A-CH visibility.

- March 2025: APECS pilot line secured EUR 730 million (USD 841.94 million) to advance heterogeneous integration across eight nations.

- February 2025: Etteplan upgraded aftermarket portfolio with AR training and predictive maintenance.

- January 2025: Kontron rolled out enhanced European repair and pro-services hubs.

Europe Electronic Contract Manufacturing and Design Services Market Report Scope

| Engineering Design |

| Electronics Assembly |

| System Integration |

| After-Market Services |

| Automotive And Mobility |

| Industrial And Robotics |

| Healthcare And Medical Devices |

| Aerospace And Defence |

| ICT And Telecom |

| Consumer Electronics |

| Turnkey EMS |

| Consignment/Build-to-Print |

| Joint Design-Manufacturing |

| Partial EMS |

| Large (≥USD 500 m) |

| Mid-Tier (USD 100-500 m) |

| Small (USD 20-100 m) |

| Micro (<USD 20 m) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Service Type | Engineering Design |

| Electronics Assembly | |

| System Integration | |

| After-Market Services | |

| By End-Use Industry | Automotive And Mobility |

| Industrial And Robotics | |

| Healthcare And Medical Devices | |

| Aerospace And Defence | |

| ICT And Telecom | |

| Consumer Electronics | |

| By Contract Model | Turnkey EMS |

| Consignment/Build-to-Print | |

| Joint Design-Manufacturing | |

| Partial EMS | |

| By Company Size Of EMS Provider | Large (≥USD 500 m) |

| Mid-Tier (USD 100-500 m) | |

| Small (USD 20-100 m) | |

| Micro (<USD 20 m) | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe electronic contract manufacturing and design services market in 2025?

It is valued at USD 70.18 billion and is forecast to reach USD 98.78 billion by 2030 at a 7.08% CAGR.

Which service segment leads regional revenue?

Electronics assembly accounted for 46.12% of 2024 turnover.

Which end-use sector is growing fastest?

Healthcare and medical devices shows an 8.12% CAGR through 2030, driven by connected diagnostics and surgical robotics.

Why is Poland expanding capacity so quickly?

Poland combines EU regulatory alignment, cost-competitive labor, and favorable investment incentives, giving it an 8.41% CAGR outlook.

What competitive factors differentiate leading EMS providers?

Advanced Industry 4.0 adoption, compliance credentials such as ISO 13485 and ISO 26262, and strategic alliances for semiconductor back-end capacity define leadership.

How are component shortages affecting operations?

Persistent lead-time volatility for automotive microcontrollers and SiC devices forces EMS houses to hold higher inventories and deepen supplier partnerships.

Page last updated on: