Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

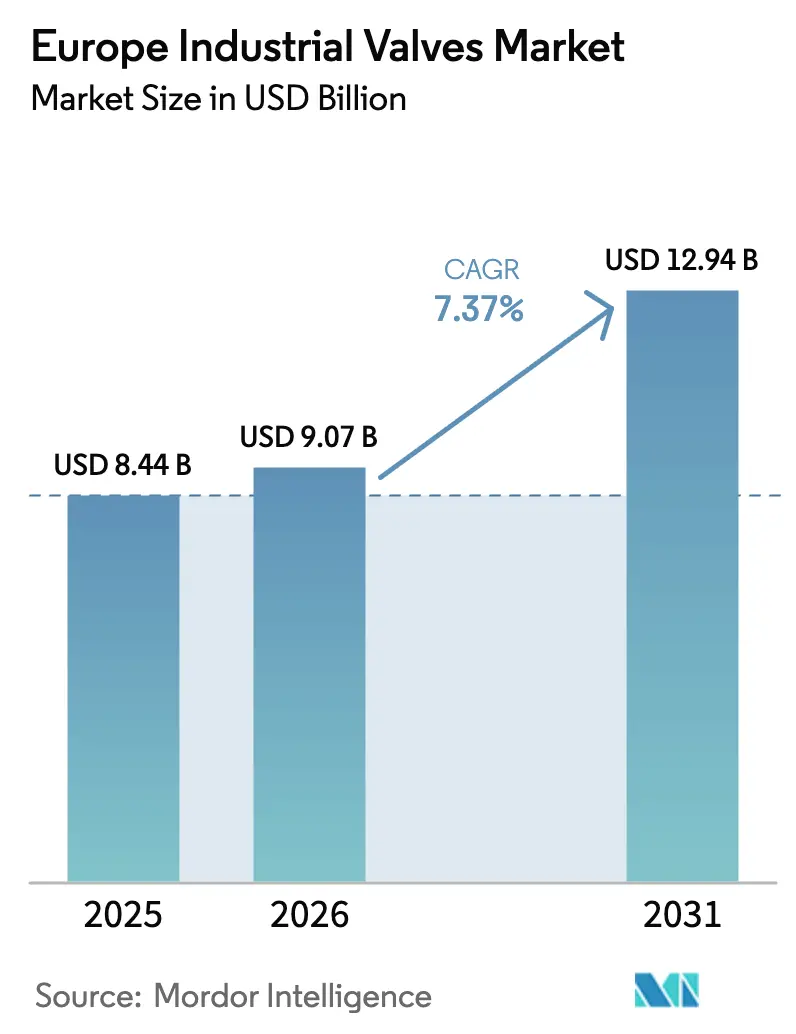

| Base Year Market Size (2025) | USD 8.44 Billion |

| Market Size (2026) | USD 9.07 Billion |

| Market Size (2031) | USD 12.94 Billion |

| Growth Rate (2026 - 2031) | 7.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Industrial Valves Market Analysis by Mordor Intelligence

The Europe industrial valves market size reached USD 9.07 billion in 2026 and is projected to expand to USD 12.94 billion by 2031, translating into a 7.37% CAGR over the forecast period. Momentum stems from hydrogen pipelines, carbon-capture networks, and offshore-wind balance-of-plant additions that demand corrosion-resistant, leak-tight flow-control devices. Operators are accelerating retrofits to meet EN ISO 15848-1 fugitive-emission limits, while digital-twin upgrades cut unplanned downtime and mitigate the region’s skilled-labor shortfall. Procurement preferences are tilting toward turnkey hardware-software-service bundles, and European supply-chain localization is reshaping lead times and material sourcing. Together, these forces underpin sustained revenue expansion for the Europe industrial valves market.

Key Report Takeaways

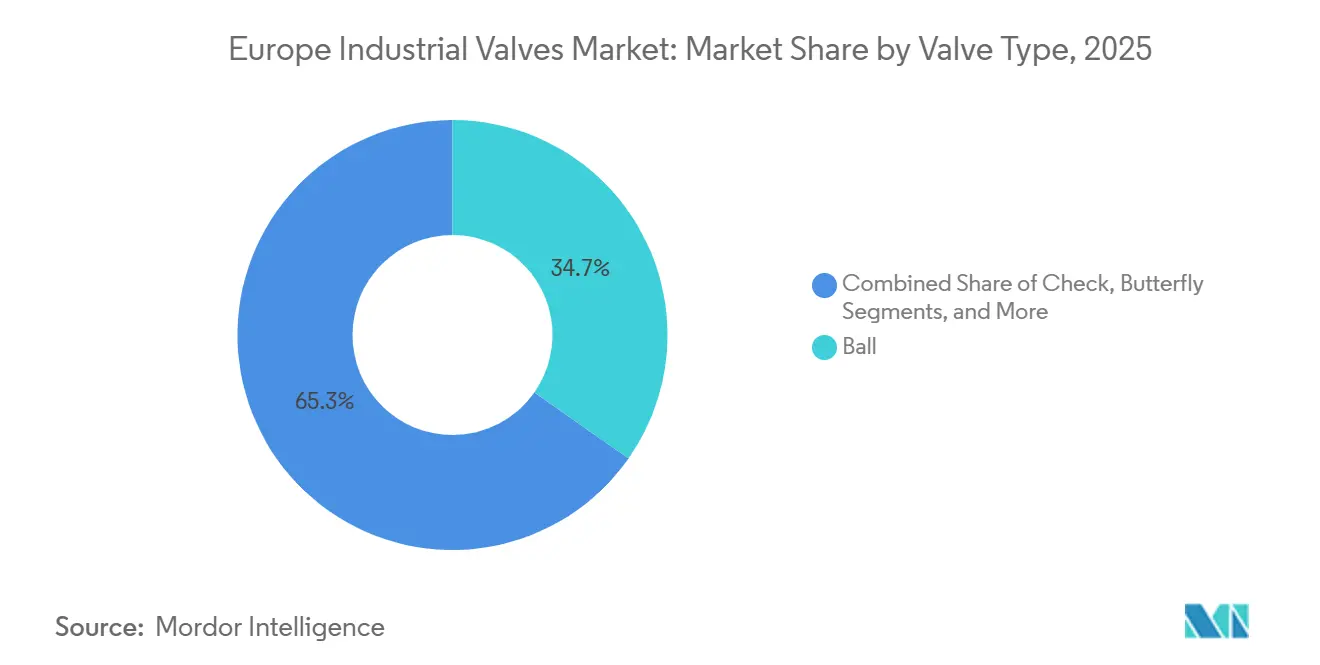

- By valve type, ball valves led with 34.73% share in 2025 of the Europe industrial valves market, whereas check valves are forecast to grow at a 7.88% CAGR through 2031.

- By actuation technology, electric actuation commanded 39.74% of the Europe industrial valves market share in 2025, while electro-hydraulic systems record the highest projected CAGR at 7.93% to 2031.

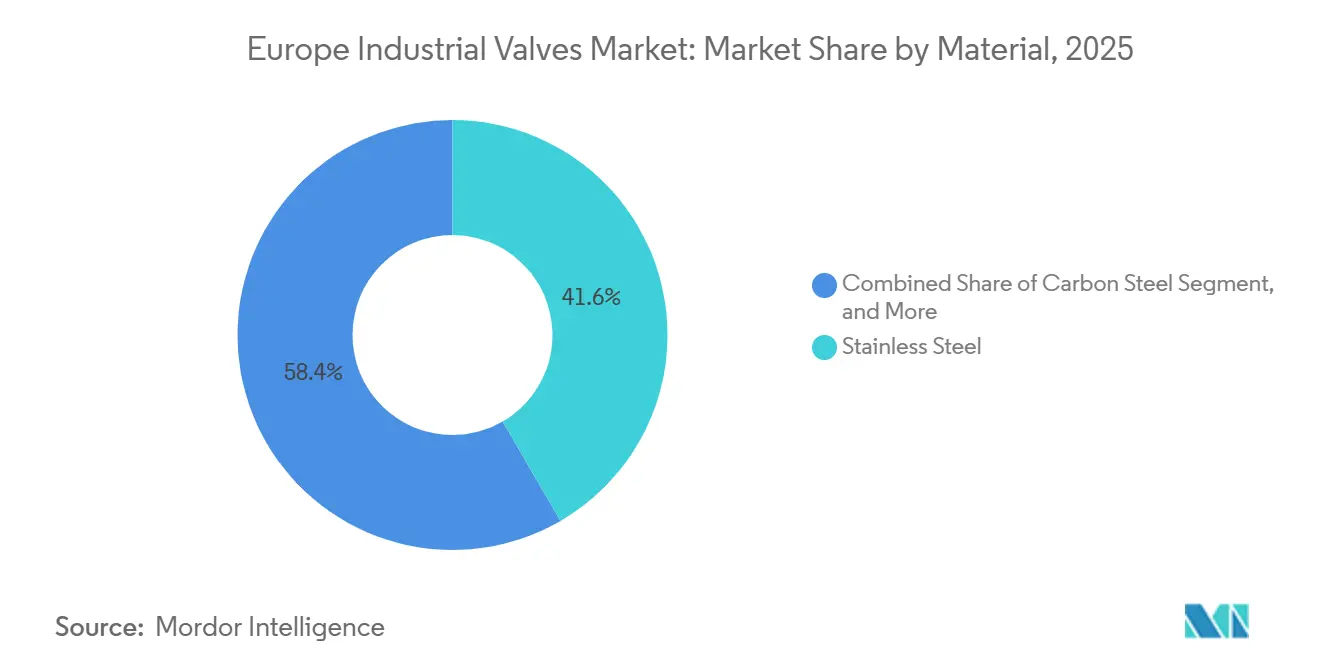

- By material, stainless steel accounted for 41.63% of the Europe industrial valves market size in 2025, whereas alloy and cryogenic grades are set to expand at an 8.21% CAGR from 2026 to 2031.

- By end user, oil and gas contributed 28.74% revenue in 2025 of the Europe industrial valves market, yet power and energy applications are advancing at a 7.78% CAGR to 2031.

- By geography, Germany held 26.84% share in 2025 of the Europe industrial valves market, whereas Spain is poised for the fastest 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Industrial Valves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding hydrogen and CCUS project pipeline post-2026 | +1.8% | Germany, Netherlands, Norway, with spillover to Poland and Spain | Medium term (2-4 years) |

| Mandatory leak-detection and fugitive-emission norms (EN ISO 15848-1) | +1.2% | EU-wide, with stricter enforcement in Germany, France, and Nordics | Short term (≤ 2 years) |

| Digital retrofit programs for brown-field flow control assets | +1.0% | Germany, UK, France, Italy (legacy industrial base) | Medium term (2-4 years) |

| Offshore wind balance-of-plant valve demand surge | +1.3% | UK, Germany, Denmark, Netherlands (North Sea and Baltic corridors) | Medium term (2-4 years) |

| Revival of European petrochemical CAPEX (2027–2030) | +0.9% | Belgium, Netherlands, Germany (Rhine-Ruhr cluster) | Long term (≥ 4 years) |

| Rising district-heating upgrades in CEE and Nordics | +0.7% | Poland, Czech Republic, Finland, Sweden, Denmark | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Hydrogen and CCUS Project Pipeline Post-2026

Thirty-two hydrogen infrastructure projects designated under the IPCEI Hy2Infra scheme unlock EUR 5.2 billion (USD 5.88 billion) in state aid, creating demand for roughly 120,000 valves rated to 100 bar hydrogen service by 2030.[1]European Commission, “EU Industrial Carbon Management Strategy,” energy.ec.europa.eu Germany’s H2Global auctions and the EU Industrial Carbon Management Strategy add parallel requirements for cryogenic and supercritical-carbon-dioxide designs, specifications currently certified by only six European manufacturers. Import terminals in Hamburg and Wilhelmshaven already specify minus 33 °C ball valves, and cross-border CO₂ pipelines now call for elastomer-sealed throttling valves resistant to carbonic-acid corrosion. Electro-hydraulic actuators with fail-safe spring return are favored for unmanned compression stations, accelerating adoption across the Europe industrial valves market.

Mandatory Leak-Detection and Fugitive-Emission Norms

EN ISO 15848-1 became enforceable in January 2024, compelling refineries and chemical plants to replace or retrofit roughly 400,000 legacy valves by 2027.[2]International Organization for Standardization, “EN ISO 15848-1,” iso.org Real-time acoustic monitoring, as deployed via Flowserve’s RedRaven platform, alerts operators before emissions exceed 10 ppm limits, helping avoid fines of up to EUR 500,000 (USD 565,000) per incident. Suppliers have responded with live-loaded packing and bellows-sealed bonnets that add 15-25% to initial costs but slash lifetime labor. Compliance urgency, especially in Germany and France, is pushing demand for certified designs across the Europe industrial valves market.

Digital Retrofit Programs for Brown-Field Assets

Roughly 8 million pneumatic actuators installed between 1990-2010 lack digital diagnostics, forcing costly manual rounds. Emerson’s DeltaV upgrades, supporting HART-IP and Ethernet-APL since March 2024, overlay intelligence without rewiring, cutting retrofit costs by 40%. BASF’s Ludwigshafen complex retrofitted 12,000 valves with wireless sensors, reducing unplanned shutdowns by 18%. With VDMA projecting a shortage of 15,000 certified technicians by 2028, predictive analytics has shifted from optional to essential, bolstering the Europe industrial valves market.

Offshore Wind Balance-of-Plant Valve Demand

The North Sea and Baltic Sea hosted 22 GW of offshore wind at end-2024, with 18 GW under construction and commissioning between 2026-2029.[3]WindEurope, “Offshore Wind in Europe: Key Trends and Statistics 2024,” windeurope.org Each gigawatt needs about 1,200 corrosion-resistant valves for pitch control, cooling water, and fire suppression. Ørsted’s Hornsea 3 contract specified duplex-steel valves capable of 10,000 cycles annually, three times the duty of onshore turbines. Digital twins such as Siemens Gamesa’s OMNIplus platform help schedule maintenance and cut costly vessel trips, reinforcing growth in the Europe industrial valves market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended EPC lead-times owing to supply-chain localization rules | -0.6% | EU-wide, with acute impact in Germany, France, and Italy | Short term (≤ 2 years) |

| Skilled valve-maintenance labor shortage in Europe | -0.5% | Germany, UK, Netherlands, Poland (industrial clusters) | Medium term (2-4 years) |

| Price volatility in nickel and special alloys | -0.4% | EU-wide, with pass-through constraints in competitive tenders | Short term (≤ 2 years) |

| Stringent end-user cybersecurity compliance delaying smart-valve rollouts | -0.3% | Critical infrastructure sectors: energy, water, chemicals (EU-wide) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extended EPC Lead-Times from Localization Rules

The Critical Raw Materials Act obliges 40% domestic processing of nickel, chromium, and molybdenum by 2030, prompting manufacturers to re-shore foundries at higher labor and energy costs. Flowserve’s EUR 45 million Essen expansion adds capacity but lengthens delivery cycles to 38 weeks for stainless and nickel-alloy valves. Traceability under the EU Deforestation Regulation inflates administrative overhead, squeezing smaller suppliers in the Europe industrial valves market.

Skilled Valve-Maintenance Labor Shortage

VDMA data show retirements outpacing apprentices three-to-one, leaving Germany 15,000 specialists short by 2028. Complexity rises as smart valves integrate cybersecurity features mandated by NIS2, yet only 22% of current technicians can troubleshoot modern protocols. Interim reliance on predictive analytics mitigates but does not eliminate the risk, restraining the Europe industrial valves market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Check Valves Gain Ground in Emission-Critical Loops

Check valves are projected to rise at a 7.88% CAGR through 2031 as operators add passive back-flow prevention to meet EN ISO 15848-1 standards. Ball valves retained 34.73% share in 2025, supported by quarter-turn simplicity in natural-gas and chemical services. Gate valves dominate large-bore water networks, though slow actuation dampens automation prospects. Butterfly valves are preferred for district heating owing to slim wafer profiles, while globe valves continue in throttling duties where precise modulation offsets higher pressure drop. Passive dual-plate designs, closing faster than swing checks, curb water hammer in offshore wind cooling loops.

Ball-valve dominance is reinforced by compatibility with electric and electro-hydraulic actuators, crucial for hydrogen and subsea applications. Recent metal-seated models resist hydrogen embrittlement over 10,000 cycles. Butterfly valves benefit from high-temperature elastomers that boost service life in 150 °C hot-water loops. Gate valves face headwinds except in legacy systems where replacement costs remain prohibitive, whereas specialty safety valves undergo seat-tolerance upgrades to curb hydrogen leakage.

By Actuation Technology: Electro-Hydraulic Systems Capture Offshore and Nuclear Niches

Electro-hydraulic actuators will post a 7.93% CAGR, favored for fail-safe spring return and high torque density in offshore wind, nuclear, and hydrogen compression. Electric actuation, with 39.74% share in 2025, thrives on digital positioner integration and predictive algorithms. Manual operation lingers in hazardous zones where explosion-proof gear is cost-prohibitive, while pneumatic units remain in plants with legacy air infrastructure but face long-term energy-efficiency headwinds.

Rotork’s IQ3 electro-hydraulic design eliminates centralized hydraulic circuits, trimming topside weight 30% on floating platforms. Auma’s latest electric series delivers 40% more torque per kilogram, enabling direct drive of large butterfly valves. Fraunhofer research indicates shifting from pneumatic to electric actuators can cut auxiliary power by 8-12%, speeding retrofits across the Europe industrial valves industry.

By Material: Alloy and Cryogenic Grades Surge on Hydrogen and LNG Demand

Alloy and cryogenic grades are forecast to climb at an 8.21% CAGR, propelled by liquefied hydrogen, ammonia, and LNG terminals across Northern Europe. Stainless steel led with 41.63% share in 2025, balancing corrosion resistance and cost for food, pharma, and water. Carbon steel serves low-pressure loops, whereas nickel-alloy steels dominate minus 253 °C hydrogen service specified under Germany’s H2Global tenders.

High-temperature Inconel valves are being installed in France’s Flamanville 3 reactor and multiple small-modular-reactor programs, areas where valve count per megawatt is 30% higher than conventional units. Cast-iron usage declines as the revised Drinking Water Directive bans leaded bronze bodies, steering municipal buyers toward ductile-iron or polymer-lined options.

By End-User Industry: Power and Energy Leads Growth on Nuclear and Renewables

Power and energy applications, including nuclear restarts, small-modular reactors, and offshore-wind balance-of-plant, are set to grow at a 7.78% CAGR, overtaking oil and gas, which held a 28.74% share in 2025. Europe’s energy-security pivot sparks valve demand for 180,000 units by 2030, spanning safety-injection, cooling, and hydrogen-compression loops. Chemicals and petrochemicals witness modest rebound, with EUR 3.2 billion investments announced in 2024.

Water and wastewater utilities integrate smart valves to curb non-revenue water, while food and beverage processors adopt hygienic actuators for recipe-driven automation. Pulp and paper mills retrofit high-temperature globe valves into black-liquor circuits to meet tighter emissions rules, stabilizing demand despite flat production volumes.

Geography Analysis

Germany contributed 26.84% to the Europe industrial valves market in 2025, supported by Rhine corridor chemicals, automotive supply chains, and North Sea wind farms. Demand tilts toward retrofits; 62% of 2025 sales were for MRO rather than greenfield. Cryogenic valves for ammonia imports in Hamburg and Wilhelmshaven illustrate shifting specifications, yet a looming technician shortfall clouds maintenance capacity.

Spain is poised for the fastest 8.02% CAGR through 2031. Its National Hydrogen Roadmap targets 11 GW electrolyzers, necessitating 40,000 high-purity valves. The H2Med undersea pipeline, backed by EUR 350 million grants, will add 8,000 hydrogen-rated valves and solidify a local high-pressure supply chain.

The United Kingdom, France, Italy, and the Nordic-CEE cluster account for the remaining 73.16%. The UK’s 18 GW offshore-wind pipeline and Hinkley Point C nuclear build underwrite demand for 25,000 safety-critical valves. France’s reactor life-extension program requires seismic-qualified Inconel valves, and Italy’s Piombino FSRU added 1,200 cryogenic units in 2024. District-heating upgrades in Poland and Finland further fuel valve replacements across the Europe industrial valves market.

Competitive Landscape

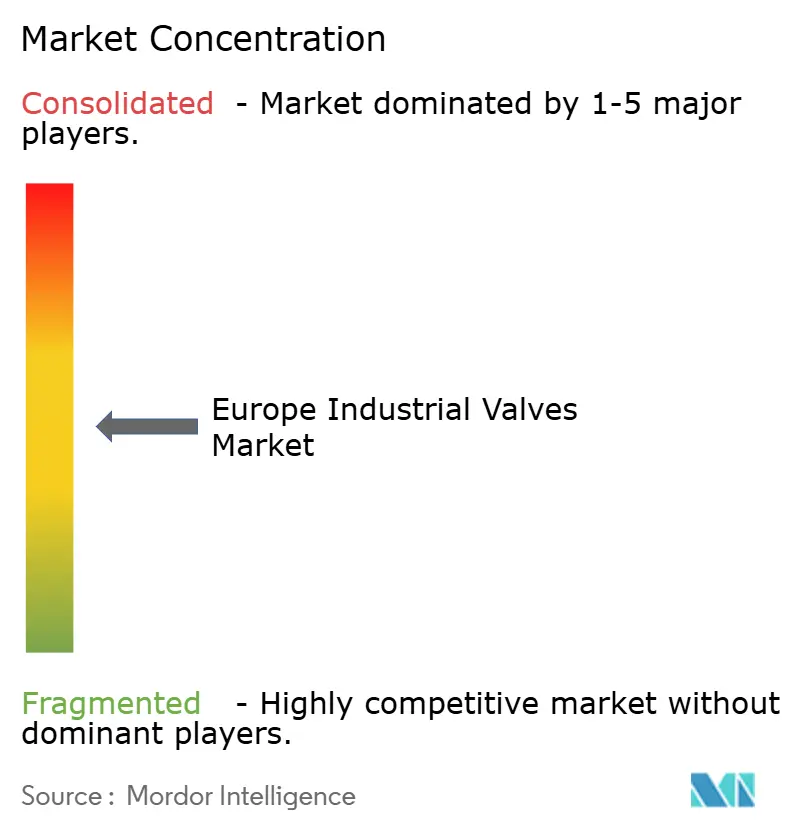

The Europe industrial valves market is moderately concentrated, as the top five suppliers, Emerson, Flowserve, Schlumberger-Cameron, Pentair, and IMI, collectively hold most of the share, leaving whitespace for specialists such as SAMSON, KLINGER, ARI-Armaturen, and Spirax-Sarco. Strategies coalesce around digital-twin analytics, localized service networks, and certification for hydrogen and carbon-capture duty. Emerson’s Branson Ultrasonics buy, and Flowserve’s Velan service-network acquisition exemplify moves toward integrated hardware-software-service offerings that trim total ownership costs by up to 20%.

Smaller contenders are leveraging compliance expertise to disrupt incumbents; SAMSON's SIL 3-certified control valves, launched in April 2024, integrate functional-safety logic that simplifies compliance with IEC 61508 and reduces engineering hours for safety-instrumented systems by 30%, a value proposition that resonates with chemical and pharmaceutical end users facing stringent process-safety-management audits. The NIS2 Directive, which entered force in October 2024 and mandates cybersecurity-by-design for all critical-infrastructure control loops, is creating a two-tier market, as suppliers that can demonstrate IEC 62443 compliance for networked actuators and positioners are capturing premium contracts, while those without certified cybersecurity architectures are relegated to manual or pneumatic applications with lower margins.

Emerging disruptors include digital-native startups such as Festo's valve-analytics subsidiary, which uses machine-learning algorithms trained on 10 million valve-cycle datasets to predict failure modes 6 to 9 months in advance, enabling condition-based maintenance that reduces spare-parts inventory by 25%. However, technology adoption is constrained by the installed base of legacy pneumatic actuators, which number approximately 8 million units across European process industries and represent a multi-billion-euro retrofit opportunity that will unfold over the next decade as operators balance cybersecurity mandates, labor shortages, and capital-budget constraints.

Europe Industrial Valves Industry Leaders

Danfoss A/S

Sirca International

Emerson Electric Co.

Schlumberger Limited

Flowserve Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Flowserve completed a EUR 45 million (USD 50.85 million) Essen foundry expansion to supply hydrogen-compression and CO₂-injection valves.

- November 2025: Emerson won a USD 28 million contract to furnish IEC 62443-secure control valves for the H2Med hydrogen pipeline.

- October 2025: Danfoss partnered with Orsted to pilot electro-hydraulic actuators on Hornsea 3, targeting 30% topside weight savings.

- September 2025: Alfa Laval introduced hygienic butterfly valves with embedded sensors that cut batch-changeover times 15%.

Europe Industrial Valves Market Report Scope

The Europe Industrial Valves Market Report is Segmented by Valve Type (Globe, Ball, Butterfly, Gate, Plug, Check, Safety/Relief, Other Valve Types), Actuation Technology (Manual, Electric, Pneumatic, Hydraulic, Electro-hydraulic), Material (Carbon Steel, Stainless Steel, Alloy and Cryogenic Alloys, Cast Iron and Ductile Iron), End-user Industry (Oil and Gas, Power and Energy, Chemicals and Petrochemicals, Water and Waste-water, Food and Beverage, Pulp and Paper, Other End-user Industries), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Valve Type

| Globe |

| Ball |

| Butterfly |

| Gate |

| Plug |

| Check |

| Safety / Relief |

| Other Valve Types |

By Actuation Technology

| Manual |

| Electric |

| Pneumatic |

| Hydraulic |

| Electro-hydraulic |

By Material

| Carbon Steel |

| Stainless Steel |

| Alloy and Cryogenic Alloys |

| Cast Iron and Ductile Iron |

By End-user Industry

| Oil and Gas |

| Power and Energy (incl. Nuclear and Renewables BOP) |

| Chemicals and Petrochemicals |

| Water and Waste-water |

| Food and Beverage |

| Pulp and Paper |

| Other End-user Industries |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Valve Type | Globe |

| Ball | |

| Butterfly | |

| Gate | |

| Plug | |

| Check | |

| Safety / Relief | |

| Other Valve Types | |

| By Actuation Technology | Manual |

| Electric | |

| Pneumatic | |

| Hydraulic | |

| Electro-hydraulic | |

| By Material | Carbon Steel |

| Stainless Steel | |

| Alloy and Cryogenic Alloys | |

| Cast Iron and Ductile Iron | |

| By End-user Industry | Oil and Gas |

| Power and Energy (incl. Nuclear and Renewables BOP) | |

| Chemicals and Petrochemicals | |

| Water and Waste-water | |

| Food and Beverage | |

| Pulp and Paper | |

| Other End-user Industries | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe industrial valves market in 2026 and what growth rate is expected?

The market stands at USD 9.07 billion in 2026 and is forecast to register a 7.37% CAGR to reach USD 12.94 billion by 2031.

Which valve type holds the largest share?

Ball valves led with 34.73% revenue share in 2025, mainly due to quarter-turn ease and bidirectional sealing.

What is driving Spain’s fast growth?

Spain’s hydrogen roadmap and the H2Med pipeline are catalyzing demand for high-pressure and cryogenic valves, supporting an 8.02% CAGR through 2031.

Why are electro-hydraulic actuators gaining traction?

They combine high torque density with fail-safe spring return, making them ideal for offshore wind turbines and nuclear safety circuits.

How are EU policies affecting supply chains?

The Critical Raw Materials Act and localization mandates extend EPC lead times but enhance long-term resilience by re-shoring casting and forging.

Page last updated on: