Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

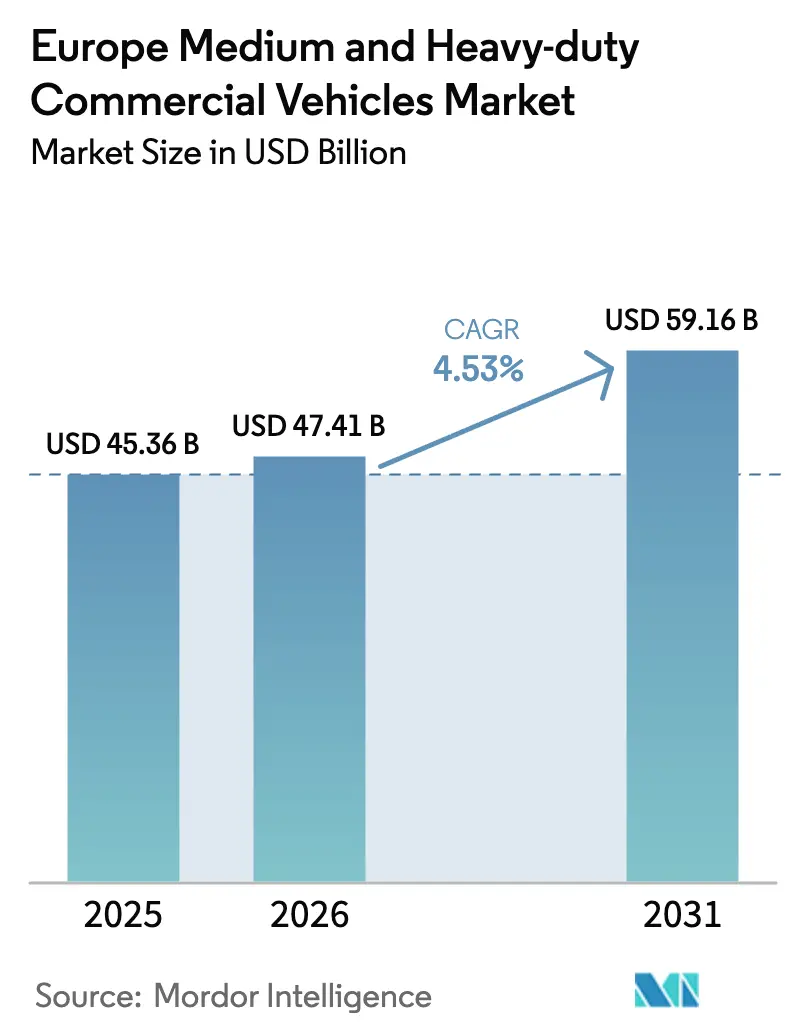

| Base Year Market Size (2025) | USD 45.36 Billion |

| Market Size (2026) | USD 47.41 Billion |

| Market Size (2031) | USD 59.16 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

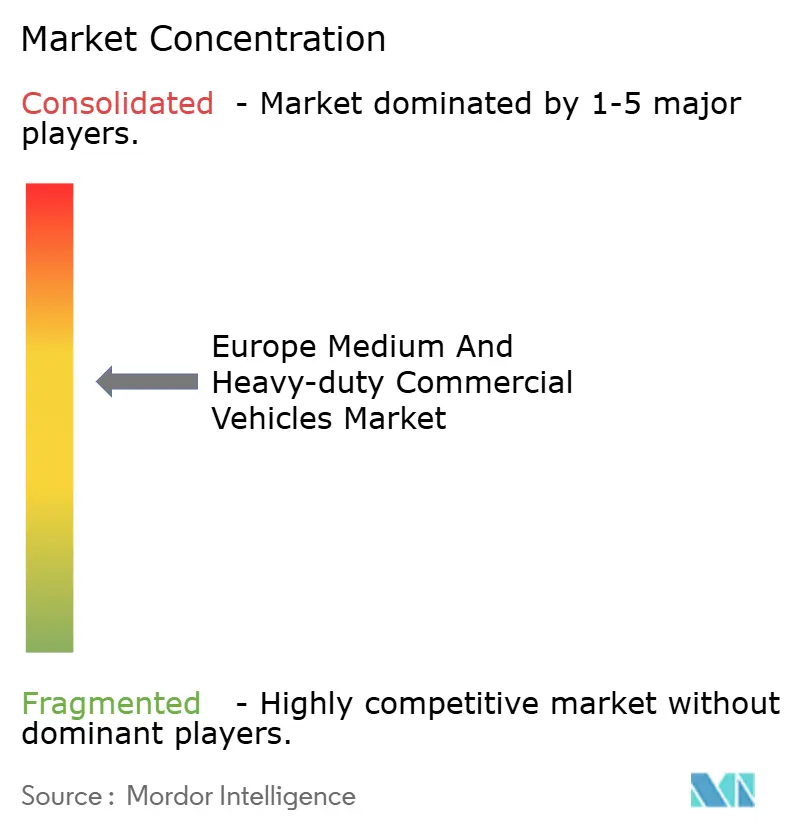

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Medium And Heavy-duty Commercial Vehicles Market Analysis by Mordor Intelligence

The Europe medium and heavy-duty commercial vehicles market size is expected to grow from USD 45.36 billion in 2025 to USD 47.41 billion in 2026 and is forecast to reach USD 59.16 billion by 2031 at a 4.53% CAGR over 2026–2031. Current growth reflects a twin-track propulsion landscape in which diesel continues to anchor long-haul economics while battery-electric platforms dominate urban and regional distribution. Tightened EU CO₂ standards, expanded low-emission zones and battery pack prices that fell below USD 100 per kilowatt-hour in 2025 are pulling forward electrification investment across the Europe medium and heavy commercial vehicle market. German and Nordic infrastructure advantages enable rapid electric truck uptake, yet payload penalties on the 26-tonne-plus class temper long-haul adoption. Competitive intensity is escalating as Chinese entrants undercut incumbent pricing, forcing legacy OEMs to modularize platforms and pivot toward software-defined revenue streams.

Key Report Takeaways

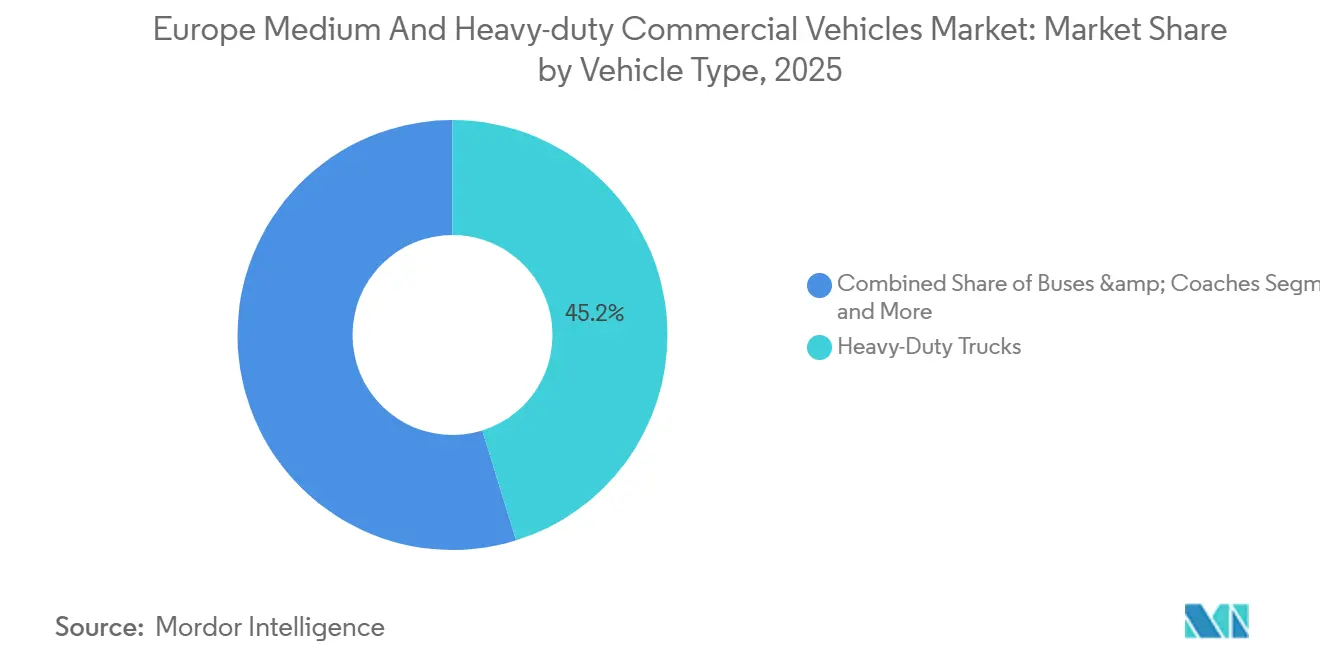

- By vehicle type, heavy-duty trucks led with 45.23% of the Europe medium and heavy commercial vehicle market share in 2025, while buses and coaches record the fastest 4.55% CAGR through 2031.

- By propulsion type, internal combustion engines retained 63.81% share of the Europe medium and heavy commercial vehicle market in 2025, yet electric propulsion is set to expand at a 4.68% CAGR to 2031.

- By end-use application, regional and urban distribution commanded 27.84% of the Europe medium and heavy commercial vehicle market size in 2025; public transport moves ahead at a 4.58% CAGR.

- By gross vehicle weight, the 16-26 tonne class captured 34.46% of 2025 demand; the 10-16 tonne band accelerates at a 4.65% CAGR.

- By geography, Germany held 27.15% share in 2025, whereas the United Kingdom is set for the quickest 4.63% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Medium And Heavy-duty Commercial Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU CO₂ Standards Tightening | +1.2% | EU27, United Kingdom, Norway | Medium term (2-4 years) |

| Declining Battery Cost Trajectory | +1.1% | Pan-European | Medium term (2-4 years) |

| Urban Low-Emission Zones Pushing Fleet Electrification | +0.9% | Germany, France, United Kingdom, Italy, Netherlands | Short term (≤ 2 years) |

| OEM Platform Modularization Enabling Cost Parity | +0.8% | Germany, Sweden, Italy | Long term (≥ 4 years) |

| Digital Freight Platforms Optimizing Load Factors | +0.5% | Germany, Netherlands, France, United Kingdom | Medium term (2-4 years) |

| Hydrogen Corridor Development Along TEN-T Core Network | +0.4% | Germany, Netherlands, Belgium, Nordic region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU CO₂ Standards Tightening for HDVs

Under the 2024 revision, emissions must significantly decrease by the end of the decade and achieve a substantial reduction by the following decade, using recent baselines. Penalties are imposed for every excess gram of CO₂ per tonne-kilometer. In response, OEMs are ramping up electric truck production, despite the lower total cost of ownership for long-haul diesel. Fleet renewal cycles have been shortened to a few years, as operators seek to avoid losses on diesel asset values. A lifecycle assessment, which factors in upstream electricity, is steering buyers towards renewable contracts and depot chargers. Scania's roadmap indicates that to remain compliant, electric trucks need to account for a considerable share of new European registrations within the next several years [1]“Capital Markets Day 2025 Presentation,” Scania AB, scania.com .

Declining Battery Cost Trajectory

In 2025, pack prices dropped significantly, coinciding with lithium iron phosphate chemistry capturing a substantial share of installations in European commercial vehicles. Chinese suppliers, CATL and BYD, accounted for a majority of this volume, due to their integration of mining, cell production, and pack assembly. This strategy enabled them to achieve a notable cost advantage over their EU counterparts, who grappled with elevated energy costs. Despite a significant surge in nickel and lithium prices at the start of 2025, the overall price drop revealed a shift in economic dynamics: urban trucks, charged at depots, are now on track to match diesel vans in cost parity over a medium-term horizon, adhering to Euro VII standards.

Urban Low Emission Zones Pushing Fleet Electrification

In recent years, numerous cities across Europe have implemented low-emission zones, with several planning to adopt zero-emission-only regulations in the near future. These measures are significantly impacting a portion of the continent's freight corridors. The expansion of London's ultra-low emission zone has driven a substantial increase in electric van registrations in the region. Over the next few years, cities such as Paris, Milan, and Amsterdam are expected to transition from Euro VI standards to complete bans. This shift is creating a divided fleet, where electric trucks dominate inner-city operations, while diesel and hydrogen vehicles continue to be used for intercity routes. Smaller operators are struggling with stranded diesel assets, whereas larger integrators are utilizing battery leasing to achieve a considerable reduction in upfront truck costs.

OEM Platform Modularization Enabling Cost Parity

By deploying skateboard chassis that isolate batteries and e-axles from cabs, Daimler Truck, Volvo, and Scania have significantly reduced production costs compared to bespoke architectures. MAN's eTGM and eTGX, set for release in the near future, share a substantial portion of their parts across various models and offer over-the-air feature updates, enhancing post-sale value. Software now plays a pivotal role, differentiating predictive range, fleet integration, and dynamic charging services, thereby establishing annuity streams that effectively reduce customer churn. However, this platform homogeneity has lowered entry barriers, allowing Chinese OEMs to replicate designs at a considerably lower cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Payload & Range Trade-Offs | -0.6% | Pan-European, acute in Nordic and Iberian corridors | Medium term (2-4 years) |

| Limited Public Fast-Charging Capacity More Than 500 kW | -0.5% | Eastern Europe, rural corridors | Short term (≤ 2 years) |

| Grid Connection Lead-Times More Than 24 Months | -0.4% | Germany, France, United Kingdom, logistics clusters | Medium term (2-4 years) |

| Volatile Nickel & Lithium Prices | -0.3% | Pan-European | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Payload And Range Trade Offs For E-Trucks on Long-Haul Routes

Battery-electric trucks weighing over 26 tonnes are at a disadvantage, carrying significantly less payload than their diesel counterparts. This payload reduction, primarily due to the weight of the battery, diminishes revenue, especially for cargoes like electronics and pharmaceuticals that are sensitive to volume constraints. These trucks, with a limited real-world range, require mid-route charging for longer journeys. This necessity adds considerable time to their travel schedules, disrupting tight timelines. A study highlighted that when factoring in both the payload loss and the downtime for charging, battery trucks incur noticeably higher costs per kilometer on long hauls [2]“Electric Trucks in Europe: Total Cost of Ownership Update 2025,” Benedikt Kloss, mckinsey.com . Meanwhile, while hydrogen fuel-cell pilots have addressed the weight challenges, they grapple with limited refueling options, with very few stations available across Europe.

Limited Public Fast-Charging Capacity More Than 500 kW

In recent years, the number of megawatt chargers installed across the continent has remained limited, with the majority concentrated in Germany, the Netherlands, and Sweden. Eastern TEN-T routes have significant gaps between chargers, forcing operators to rely heavily on depot infrastructure and restricting battery trucks to base loops. The process of securing permits and constructing grid connections with higher capacity is time-consuming, delaying public roll-outs even when funding is available. Although Daimler Truck and Volvo's joint venture aims to establish a substantial number of charging points in the coming years, this effort is expected to meet only a fraction of the anticipated demand, creating challenges for early adopters while allowing late adopters to benefit from a more developed network.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Heavy-Duty Dominance Meets Transit Electrification

Heavy-duty trucks held 45.23% of the Europe medium and heavy commercial vehicle market in 2025, backed by intercontinental freight and construction haulage. Buses and coaches post the quickest 4.55% CAGR through 2031 as municipal electrification accelerates under EU cohesion funds. Medium-duty trucks absorb e-commerce growth by blending 6-16 tonne flexibility with depot charging. Electric buses surpassed diesel orders in Volvo Group’s 2025 backlog, signaling a tipping point. Heavy-duty diesel maintains primacy on 400-km-plus missions, though hydrogen fuel-cell pilots are edging into Alpine and Nordic corridors.

Urban buses are increasingly adopting batteries, due to route predictability. Meanwhile, medium-duty trucks are expected to achieve significant penetration in the near future, primarily focusing on last-mile deliveries. Over the long term, the market for buses and coaches in Europe's medium and heavy commercial vehicle sector is anticipated to witness substantial growth, driven by policy-induced replacement cycles. On the other hand, while heavy-duty trucks in Europe’s medium and heavy commercial vehicle market may see a slight dip in share, it's largely due to the gradual shift from diesel to weight-penalized electric and hydrogen alternatives, expected by decade's end.

By Propulsion Type: ICE Incumbency Versus Electric Momentum

Internal combustion engines commanded 63.81% of revenue in 2025, but electric drivetrains chart the fastest 4.68% CAGR into 2031. Long-haul lanes remain dominated by diesel, due to its significantly higher energy density and the convenience of widespread refueling. In the realm of waste management, niche fleets are increasingly turning to CNG and LNG, with biogas helping to offset fuel premiums. In the near future, battery-electric vehicles are projected to account for the majority of electric registrations, supported by more affordable battery packs and a growing number of city bans on diesel. Meanwhile, plug-in hybrids are losing traction as their cost-saving advantages diminish, and pure hybrids find their niche, primarily in stop-start refuse duties.

While fuel-cell electric trucks are expected to have limited adoption in Europe in the near term, several TEN-T pilots hint at their potential for long-haul viability. OEMs are gravitating towards a clear propulsion strategy: battery-electric vehicles for urban and regional routes, and hydrogen or synthetic diesel for longer journeys. If the current adoption trends persist, the market size for electric propulsion in Europe's medium and heavy commercial vehicle sector could grow significantly in the coming years. Furthermore, with the anticipated scaling of megawatt charging networks, this segment's market share in Europe might see substantial growth over the same period.

By End-Use Application: Urban Distribution Leads, Public Transport Accelerates

Regional and urban distribution secured 27.84% of revenue in 2025 owing to route predictability, depot chargers and electrification alignment. Public transport grows quickest at 4.58% as 47 cities mandate zero-emission bus procurement, thus locking diesel out of tender processes. Long-haul retains diesel dominance with battery trucks penalized on payload and range, though hydrogen pilots sprout along Germany-Netherlands corridors. Construction and mining are slowest to shift, with only minimal electric share in 2025 due to off-grid challenges.

Since last year, e-commerce volumes have been steadily increasing, supporting distribution growth and driving demand for medium-sized electrified rigs. Significant public transport funding over the coming years ensures a consistent flow of bus orders. Meanwhile, as fuel-cell cost curves evolve, intercontinental freight economics hint at a gradual shift in substitution patterns. Consequently, players in Europe's medium and heavy commercial vehicle market are strategically balancing their focus: securing immediate urban victories while also positioning themselves for alternative fuels in the long-haul segment.

By Gross Vehicle Weight Class: Mid-Weight Flexibility Drives Growth

The 16-26 tonne bracket held 34.46% share in 2025 by serving construction and municipal duties, yet the 10-16 tonne class enjoys a leading 4.65% CAGR as e-commerce spreads to secondary cities. Trucks in the light-to-medium weight category are leading the charge in electrification, with a significant portion of upcoming registrations projected to be electric. This surge is largely due to the optimal alignment of battery range and urban access. Meanwhile, heavier trucks continue to rely predominantly on diesel, although hydrogen pilots are being explored to mitigate payload concerns.

As the EU tightens CO₂ caps more aggressively on heavier truck classes, OEMs are shifting their focus. They're prioritizing the electrification of medium-weight models, aiming to capitalize on valuable regulatory credits. Additionally, urban low-emission zone policies are boosting the demand for light-to-medium electric vehicles, which benefit from avoiding access fees. Looking ahead, advancements in gravimetric density batteries might enable heavier electric trucks to overcome current payload challenges. However, for now, the European medium and heavy commercial vehicle market remains distinctly influenced by weight-specific economic factors.

Geography Analysis

Germany accounted for 27.15% of the European medium and heavy commercial vehicle market in 2025, holding a significant share due to its strong manufacturing base, extensive Autobahn corridors, and substantial annual road freight volume. Federal subsidies that cover a large portion of depot charger costs, along with rapid grid connections, are accelerating the deployment of electric vehicles. The United Kingdom rises fastest at a 4.63% CAGR through 2031 as post-Brexit route reshoring fuels domestic haulage and London’s borough-wide diesel ban forces fleets into electrification.

During the same period, France, Italy, and Spain are projected to collectively account for a notable portion of the market. France benefits from its low-carbon nuclear electricity, which reduces lifecycle trucking emissions and simplifies compliance. Italy leverages its Mediterranean port throughput to enhance regional distribution, while Spain is increasing its renewable energy share to support green charging infrastructure. Nordic countries are expected to achieve a significant share in electric truck registrations, supported by advancements in cold-weather battery technology and substantial purchase subsidies for trucks.

Eastern European markets are anticipated to grow at a slower pace due to persistent infrastructure challenges. For example, gaps in fast-charging stations along key corridors, such as the Poland-Balkans route, are deterring electric vehicle investments. Although Belgium and the Netherlands have smaller market volumes, they play a strategic role as chokepoints, with major ports like Rotterdam and Antwerp enforcing zero-emission drayage. Austria, Denmark, and Ireland are relying on EU cohesion grants to expand their charging infrastructure. This dynamic highlights a two-speed transition in Europe, where Western and Nordic countries lead adoption, while Eastern regions are expected to follow as infrastructure development progresses. Consequently, while the European medium and heavy commercial vehicle market reflects an aggregated growth rate, it conceals significant local variations and diverse national trajectories.

Competitive Landscape

In 2025, the five largest OEMs - Daimler Truck, Volvo Group, Scania, MAN Truck & Bus, and IVECO - held a significant share of the market, indicating a moderate concentration. Meanwhile, Chinese competitors BYD and SANY Europe managed to reduce prices considerably using integrated battery supply chains and benefiting from export incentives. Strategic moves include platform modularization and a shift towards software revenue: Daimler’s eActros now predicts real-time range based on traffic and weather, Volvo offers a subscription bundle of financing, charging, and predictive maintenance, and IVECO collaborates with Nikola for hydrogen fuel-cell deployments.

Emerging opportunities lie in megawatt charging, battery-swapping depots, and vehicle-to-grid services that capitalize on idle batteries. Companies like Nikola, Quantron, and Tevva are venturing into retrofit and fuel-cell markets, pushing established players to diversify into both battery-electric and hydrogen solutions. In Germany and the Netherlands, adherence to ISO 15118 vehicle-to-grid standards is now a criterion for tender eligibility, granting a competitive edge to OEMs that opt out of proprietary protocols.

As investments in both electric and traditional diesel technologies strain balance sheets, margin pressures mount. Both Daimler and Volvo project their R&D expenditures will remain a significant portion of their revenue for the foreseeable future. This financial discipline could lead to more alliances, reminiscent of the recent fast-charge joint venture. While new market players benefit from reduced cost structures, they still face the hurdle of certifying to EU safety and cybersecurity standards, hindering rapid market entry. Consequently, the European medium and heavy commercial vehicle market is evolving into a landscape of mixed competition: established players leverage scale efficiencies, while newcomers challenge with cost disruptions, all influenced by policy incentives.

Europe Medium And Heavy-duty Commercial Vehicles Industry Leaders

Daimler AG (Mercedes-Benz AG)

Man Truck & Bus

PACCAR Inc.

Scania AB

Volvo Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: IVECO launched the S-eWay Artic electric tractor, offering an impressive range designed to support extended travel across significant European routes. This vehicle is tailored to meet the demands of long-haul transportation, emphasizing sustainability and efficiency for core markets in the region.

- June 2025: In the United Kingdom, MAN Truck & Bus introduced the eTGS, accompanied by a comprehensive turnkey depot charging solution designed to address and minimize risks associated with potential delays in infrastructure development.

Europe Medium And Heavy-duty Commercial Vehicles Market Report Scope

The scope of the report includes Vehicle Type (Medium-Duty Trucks and More), Propulsion Type (ICE and Electric), End-Use Application (Long-Haul Freight and More), GVW Class (6-10t and More), and Geography.

By Vehicle Type

| Medium-Duty Trucks |

| Heavy-Duty Trucks |

| Buses & Coaches |

By Propulsion Type

| Internal Combustion Engine | Diesel |

| CNG / LNG | |

| LPG | |

| Electric | Battery Electric |

| Hybrid Electric | |

| Plug-in Hybrid Electric | |

| Fuel-cell Electric |

By End-Use Application

| Long-Haul Freight |

| Regional & Urban Distribution |

| Construction & Mining |

| Public Transport |

By Gross Vehicle Weight Class

| 6–10 t |

| 10–16 t |

| 16–26 t |

| More Than 26 t |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Belgium |

| Norway |

| Poland |

| Ireland |

| Austria |

| Czech Republic |

| Denmark |

| Estonia |

| Rest of Europe |

| By Vehicle Type | Medium-Duty Trucks | |

| Heavy-Duty Trucks | ||

| Buses & Coaches | ||

| By Propulsion Type | Internal Combustion Engine | Diesel |

| CNG / LNG | ||

| LPG | ||

| Electric | Battery Electric | |

| Hybrid Electric | ||

| Plug-in Hybrid Electric | ||

| Fuel-cell Electric | ||

| By End-Use Application | Long-Haul Freight | |

| Regional & Urban Distribution | ||

| Construction & Mining | ||

| Public Transport | ||

| By Gross Vehicle Weight Class | 6–10 t | |

| 10–16 t | ||

| 16–26 t | ||

| More Than 26 t | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Norway | ||

| Poland | ||

| Ireland | ||

| Austria | ||

| Czech Republic | ||

| Denmark | ||

| Estonia | ||

| Rest of Europe | ||

Market Definition

- Vehicle Type - The category covers truck category.

- Vehicle Body Type - This includes Medium-duty Commercial Trucks and Heavy-duty Commercial Trucks

- Fuel Category - The category includes various fuel types such as Gasoline, Diesel, LPG (Liquefied Petroleum Gas), CNG (Compressed Natural Gas), HEV (Hybrid Electric Vehicles), PHEV (Plug-in Hybrid Electric Vehicles), BEV (Battery Electric Vehicles), and FCEV (Fuel Cell Electric Vehicles)

| Keyword | Definition |

|---|---|

| Electric Vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| BEV | A BEV relies completely on a battery and a motor for propulsion. The battery in the vehicle must be charged by plugging it into an outlet or public charging station. BEVs do not have an ICE and hence are pollution-free. They have a low cost of operation and reduced engine noise as compared to conventional fuel engines. However, they have a shorter range and higher prices than their equivalent gasoline models. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. |

| Plug-in Hybrid EV | A vehicle that can be powered either by an ICE or an electric motor. In contrast to normal hybrid EVs, they can be charged externally. |

| Internal combustion engine | An engine in which the burning of fuels occurs in a confined space called a combustion chamber. Usually run with gasoline/petrol or diesel. |

| Hybrid EV | A vehicle powered by an ICE in combination with one or more electric motors that use energy stored in batteries. These are continually recharged with power from the ICE and regenerative braking. |

| Commercial Vehicles | Commercial vehicles are motorized road vehicles designed for transporting people or goods. The category includes light commercial vehicles (LCVs) and medium and heavy-duty vehicles (M&HCV). |

| Passenger Vehicles | Passenger cars are electric motor– or engine-driven vehicles with at least four wheels. These vehicles are used for the transport of passengers and comprise no more than eight seats in addition to the driver’s seat. |

| Light Commercial Vehicles | Commercial vehicles that weigh less than 6,000 lb (Class 1) and in the range of 6,001–10,000 lb (Class 2) are covered under this category. |

| M&HDT | Commercial vehicles that weigh in the range of 10,001–14,000 lb (Class 3), 14,001–16,000 lb (Class 4), 16,001–19,500 lb (Class 5), 19,501–26,000 lb (Class 6), 26,001–33,000 lb (Class 7) and above 33,001 lb (Class 8) are covered under this category. |

| Bus | A mode of transportation that typically refers to a large vehicle designed to carry passengers over long distances. This includes transit bus, school bus, shuttle bus, and trolleybuses. |

| Diesel | It includes vehicles that use diesel as their primary fuel. A diesel engine vehicle have a compression-ignited injection system rather than the spark-ignited system used by most gasoline vehicles. In such vehicles, fuel is injected into the combustion chamber and ignited by the high temperature achieved when gas is greatly compressed. |

| Gasoline | It includes vehicles that use gas/petrol as their primary fuel. A gasoline car typically uses a spark-ignited internal combustion engine. In such vehicles, fuel is injected into either the intake manifold or the combustion chamber, where it is combined with air, and the air/fuel mixture is ignited by the spark from a spark plug. |

| LPG | It includes vehicles that use LPG as their primary fuel. Both dedicated and bi-fuel LPG vehicles are considered under the scope of the study. |

| CNG | It includes vehicles that use CNG as their primary fuel. These are vehicles that operate like gasoline-powered vehicles with spark-ignited internal combustion engines. |

| HEV | All the electric vehicles that use batteries and an internal combustion engine (ICE) as their primary source for propulsion are considered under this category. HEVs generally use a diesel-electric powertrain and are also known as hybrid diesel-electric vehicles. An HEV converts the vehicle momentum (kinetic energy) into electricity that recharges the battery when the vehicle slows down or stops. The battery of HEV cannot be charged using plug-in devices. |

| PHEV | PHEVs are powered by a battery as well as an ICE. The battery can be charged through either regenerative breaking using the ICE or by plugging into some external charging source. PHEVs have a better range than BEVs but are comparatively less eco-friendly. |

| Hatchback | These are compact-sized cars with a hatch-type door provided at the rear end. |

| Sedan | These are usually two- or four-door passenger cars, with a separate area provided at the rear end for luggage. |

| SUV | Popularly known as SUVs, these cars come with four-wheel drive, and usually have high ground clearance. These cars can also be used as off-road vehicles. |

| MPV | These are multi-purpose vehicles (also called minivans) designed to carry a larger number of passengers. They carry between five and seven people and have room for luggage too. They are usually taller than the average family saloon car, to provide greater headroom and ease of access, and they are usually front-wheel drive. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the sales volume with their respective average selling price (ASP). While estimating ASP factors like average inflation, market demand shift, manufacturing cost, technological advancement, and varying consumer preference, among others have been taken into account.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.