Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.61 Billion |

| Market Size (2026) | USD 31.79 Billion |

| Market Size (2031) | USD 53.86 Billion |

| Growth Rate (2026 - 2031) | 11.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Free From Food Market Analysis by Mordor Intelligence

The Europe free form food market size was valued at USD 28.61 billion in 2025 and estimated to grow from USD 31.79 billion in 2026 to reach USD 53.86 billion by 2031, at a CAGR of 11.12% during the forecast period (2026-2031). The market is undergoing significant changes due to increasing consumer awareness of food allergies and intolerances. The market growth is further supported by the increasing adoption of plant-based, vegan, and flexitarian diets, driven by health considerations and environmental concerns. The advancement in food processing techniques and ingredient innovation has improved the quality of meat and dairy alternatives. Manufacturers are developing products using alternative proteins, non-dairy emulsifiers, and allergen-free binders to match the taste, texture, and nutritional content of conventional products. While supermarkets and hypermarkets remain the primary distribution channels due to their extensive product range, online retail is gaining prominence by offering convenient access to specialized products. Regional market dynamics show variations across Europe. Western European countries demonstrate strong market presence due to high consumer awareness and product availability. Eastern European markets are showing rapid growth driven by expanding middle-class consumption and improved product accessibility.

Key Report Takeaways

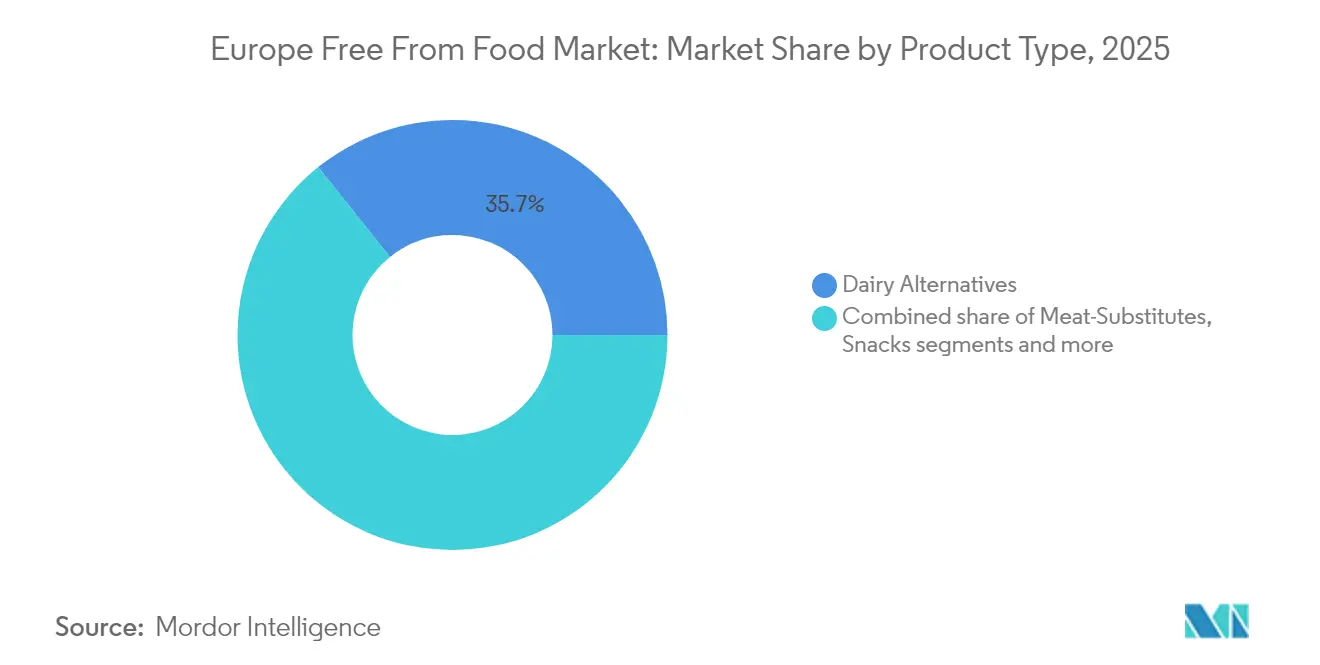

- By product type, dairy alternatives held 35.74% share of the Europe free from food market size in 2025, whereas meat substitutes are projected to climb 11.67% annually to 2031.

- By free from type, dairy-free products led with 36.92% of the Europe free from food market share in 2025; meat-free is on track for 11.56% CAGR to 2031.

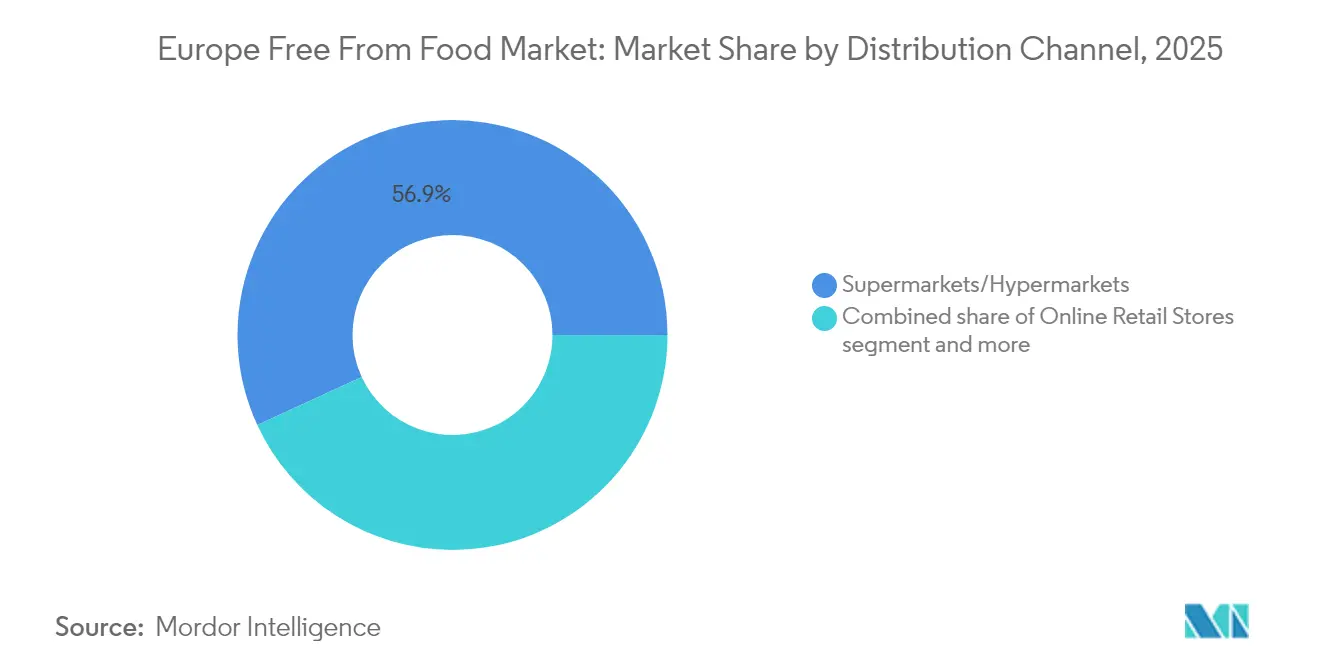

- By distribution channel, supermarkets and hypermarkets controlled 56.88% revenue in 2025; online retail is the fastest mover at a 12.41% CAGR through 2031.

- By geography, the United Kingdom captured 16.05% of the Europe free from food market share in 2025, while Russia exhibits the strongest growth at 12.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Free From Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of food allergies and intolerances | +1.2% | Global, with highest impact in Nordic countries | Long term (≥ 4 years) |

| Surge in vegan and flexitarian diets | +1.8% | Western Europe core, expanding to Eastern Europe | Medium term (2-4 years) |

| Growing consumer demand for clean label products drives the market | +1.1% | Germany, Netherlands, the United Kingdom leading adoption | Medium term (2-4 years) |

| Rapid scale-up of allergen-free ingredient processing tech | +0.9% | Industrial hubs in Germany, France, Netherlands | Short term (≤ 2 years) |

| Increased awareness through digital and social media | +0.7% | Urban centers across Europe, youth demographics | Short term (≤ 2 years) |

| Rise in premium product positioning | +0.6% | High-income markets in Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of food allergies and intolerances

The increase in food allergies and intolerances across Europe is driving growth in the market. For instance, the United Kingdom's Food Standards Agency reports that approximately 6% of adults, representing over 2.4 million individuals in 2024, have clinically confirmed food allergies. This significant number highlights the widespread need for dietary exclusion options [1]Source: Food Standards Agency, “Around 6% of the UK Adult Population Have a Food Allergy,” food.gov.uk. The requirement for lifelong dietary management among individuals with food allergies ensures sustained demand for certified allergen-free food products. The development of improved diagnostic methods, including molecular allergology, component-resolved diagnostics, and basophil activation tests, has enhanced allergy detection accuracy. These diagnostic advances have increased the diagnosed population and improved public and medical awareness, expanding the free form product consumer base. Urban areas show higher rates of allergies, potentially due to environmental factors, indicating that city markets will experience stronger demand growth. This market growth was further validated by significant industry investments, as evidenced by Gluten-free specialist Juvela's establishment of a EUR 1.5 million allergen-free bakery in South Wales, United Kingdom, which opened in June 2025.

Surge in vegan and flexitarian diets

The Europe free from food market demonstrated significant expansion, primarily attributed to the escalating prevalence of vegan and flexitarian dietary preferences, fundamentally transforming consumer behavior patterns across the region. This market evolution materialized from intensified health consciousness, environmental considerations, and ethical consumption paradigms among European consumers. Consumers actively sought plant-based alternatives beyond medical or allergy-related requirements, implementing deliberate lifestyle modifications aligned with personal wellness and sustainability objectives. According to the Federal Statistical Office, Germany's production of meat substitutes reached 126,500 tons in 2024, representing a 4.0% increase from 2023 [2]Source: Federal Statistical Office, “1.5 Kilos of Meat Substitute Products per Capita Produced in Germany in 2024,” destatis.de. This quantifiable growth demonstrated the substantial consumer demand for plant-based alternatives and the market's systematic expansion through product development initiatives. Moreover, supporting this consumer shift toward plant-based alternatives, Netherlands-based Vivera launched new tofu products in June 2025, including soft and smoked tofu, and Tofusion bites that combine tofu, vegetables, and spices for versatile meal preparation. The market's robust performance and growth trajectory reflected a fundamental change in European consumer preferences, indicating continued market expansion and product innovation in the free from food segment.

Growing consumer demand for clean label products drives the market

The clean label movement has expanded from ingredient reduction to full transparency in food production across the Europe free from food market. European consumers demonstrate a pronounced preference for products without artificial preservatives, colors, and flavors, necessitating manufacturers to undertake comprehensive product reformulations and develop innovative solutions using natural ingredients. The European natural food additives market growth is driven by health-conscious consumer preferences and increased packaged food consumption, supported by upcoming European Union regulations that favor natural over synthetic ingredients. Danone exemplifies this market adaptation, with 90.3% of its products in healthy categories and 81.2% without added sugars, as reported in its 2023 Health and Nutrition Data. The European organic food market continues to demonstrate robust growth, particularly in organic and plant-based categories, generating substantial opportunities for natural food additives. Germany, France, and the Netherlands have emerged as primary markets, where consumers exhibit the highest propensity to pay premium prices for clean-label products, presenting strategic opportunities for manufacturers.

Rapid scale-up of allergen-free ingredient processing tech

In the Europe free from food market, high hydrostatic pressure processing demonstrates significant potential in reducing protein allergenicity while maintaining nutritional value. This processing method enhances functional properties, including emulsifying and foaming capabilities, which enables manufacturers to develop allergen-free products that match conventional products in texture and taste. The advancement of enzyme engineering through directed evolution and immobilization techniques has improved stability and catalytic efficiency while reducing production costs across European manufacturing facilities. Notable market participants, particularly Nestlé, have initiated substantial capital investments in precision fermentation technologies for the production of animal-free dairy alternatives, with specific emphasis on fermentation-derived whey proteins, although market acceptance among European consumers remains a crucial consideration. The convergence of these technological innovations, coupled with heightened consumer awareness and robust regulatory frameworks, continues to drive the expansion of the European free from food market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing of free from products hamper the market growth | -1.4% | Price-sensitive markets in Eastern Europe | Medium term (2-4 years) |

| Lack of standardization across the European Union Nations | -0.8% | Cross-border trade corridors | Long term (≥ 4 years) |

| Taste and texture challenges | -0.5% | Mass market consumers across Europe | Medium term (2-4 years) |

| Risk of nutritional dilution in ultra-processed free from lines | -0.4% | Manufacturing and import-dependent regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium pricing of free from products hamper the market growth

Price disparities persist between free from products and conventional alternatives across European markets, with plant-based options typically commanding higher prices that restrict widespread adoption beyond dedicated consumer segments. The higher costs result from specialized ingredient procurement, separate production facilities required to prevent cross-contamination, and limited production volumes that impede economies of scale. Companies such as Rival Foods are addressing this challenge by focusing on achieving price parity with animal meat through production optimization and cost reduction initiatives, having secured EUR 10 million in Series B funding to double their production capacity in the Netherlands in June 2025. The affordability challenge is particularly significant given that in 2024, 93.3 million people in the European Union were at risk of poverty or social exclusion, according to the European Commission [3]Source: European Commission, “Living Conditions in Europe - Poverty and Social Exclusion,” commission.europa.eu. This economic situation restricts access to higher-priced, free from products among economically vulnerable groups. Due to inflation, consumers have increasingly shifted toward private labels and discount retailers, benefiting affordable free from options while requiring premium brands to demonstrate value through enhanced functionality or taste quality.

Lack of standardization across European Nations

The European Union's diverse regulatory landscape for free from food creates compliance challenges that increase market entry costs and restrict cross-border expansion opportunities. The Netherlands has established specific protocols for allergen cross-contact management and precautionary allergen labeling, requiring compliance by 2026. Due to these regulatory variations, manufacturers must maintain separate product formulations and labeling systems, hindering the benefits of a unified market. The inconsistent precautionary allergen labeling requirements across countries, where some nations mandate specific risk assessments while others accept general statements, create consumer uncertainty and restrict product distribution. Furthermore, the absence of standardized thresholds for "free from" claims across European Union member states compels manufacturers to adopt the most stringent standards, resulting in elevated production costs and limited product differentiation opportunities. These regulatory complexities pose a significant barrier to market entry and expansion, particularly affecting small manufacturers who lack the necessary resources to navigate multiple regulatory frameworks effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy-Free Foods Emerge as Innovation Catalyst

In 2025, the dairy alternatives segment secures a commanding 35.74% share, solidifying its position as the leading product type in the free from market. This surge in dominance is largely attributed to the escalating popularity of plant-based milk alternatives oat, almond, and soy, which have now achieved taste, texture, and culinary versatility levels akin to traditional dairy. Once considered niche, these products have seamlessly transitioned to mainstream staples on European retail shelves, bolstered by enhanced distribution networks and a surge in consumer demand. Meanwhile, the meat-substitute segment, with a projected 11.67% CAGR through 2031, stands out as the fastest-growing product category. Its swift rise is propelled by the increasing embrace of flexitarian and vegan diets, alongside breakthroughs in food science, particularly precision fermentation. This cutting-edge technology paves the way for meat analogues that not only mimic the taste and texture of traditional animal proteins but also match their nutritional profile, broadening their appeal to mainstream consumers.

In the bakery and confectionery realm, gluten-free innovations are taking center stage. A testament to this trend is Dr. Schär’s March 2024 debut of gluten-free marble cake and muffins. The snacks category is pivoting towards premium, clean-label, and allergen-free products. Meanwhile, the beverage sector is reaping the rewards of the widespread adoption of plant-based milks. Ready meals are witnessing a surge in demand, driven by a quest for convenient, nutritious, and allergen-free options. Companies are responding with investments in cutting-edge packaging and shelf-life technologies. The baby food market, characterized by stringent regulatory standards, continues to command premium pricing, largely due to parents' unwavering preference for allergen-free nutrition. Lastly, the “other” category is expanding, encompassing a diverse range of specialized products, from protein bars and functional foods to tailored ingredients, all crafted to cater to specific dietary needs.

By Free From Type: Dairy-Free Acceleration Challenges Meat-Free Dominance

In 2025, the dairy-free segment commanded a dominant 36.92% market share, fueled by rising awareness of lactose intolerance, a surge in plant-based nutrition adoption, and growing environmental concerns. Innovations in ingredients and precision fermentation have notably enhanced the taste and functionality of dairy alternatives. In February 2024, Danone transformed its yogurt facility into an Alpro-branded oat beverage plant, boasting a daily output of 300,000 liters for 26 European markets. Health-conscious consumers continue to show robust demand for GMO-free dairy alternatives, while gluten-free options gain traction due to ongoing refinements. Owing to advancements in precision fermentation, the dairy-free segment is poised to achieve sensory and functional parity with traditional dairy products faster than other free from categories. Additionally, the market is adapting to evolving dietary preferences, offering sugar-free, additive-free, and allergen-specific formulations.

Projecting an 11.56% CAGR through 2031, the meat-free product segment stands as the fastest-growing category. This growth is driven by rising consumer adoption and a robust distribution network. Technological advancements in food production have birthed meat alternatives that closely mimic the taste and texture of traditional animal proteins. Furthermore, strategic expansions in retail channels have bolstered the accessibility of plant-based products, including burgers and sausages. As flexitarian consumers increasingly emphasize health benefits and environmental sustainability, the segment's growth trajectory underscores its deep market penetration and the widespread integration of plant-based foods across diverse consumer profiles.

By Distribution Channel: Online Retail Disrupts Traditional Grocery Dominance

Supermarkets and hypermarkets maintain a commanding 56.88% market share in 2025, establishing their predominant position in the retail landscape. This substantial market presence is attributed to multiple fundamental factors, including well-established consumer purchasing patterns, the necessity for physical product examination, comprehensive product assortment under a single retail environment, price competitiveness achieved through operational scale efficiencies, and strategically positioned store locations. These retail establishments further strengthen their market position through specialized service offerings, encompassing dedicated in-store bakery operations, extensive fresh produce departments, and specialized free from product sections.

The online retail distribution channel demonstrates substantial growth potential, with a projected CAGR of 12.41% through 2031. This expansion is characterized by sophisticated product discovery mechanisms and the systematic implementation of direct-to-consumer sales methodologies. The digital infrastructure facilitates precise market segmentation and consumer targeting strategies for free from product manufacturers. The shift toward digital commerce is validated by Eurostat data, which indicates that 77% of European Union internet users engaged in online purchases in 2024, with food deliveries constituting 21% of total transactions. This trend demonstrates the increasing consumer acceptance and integration of digital platforms in food purchasing behaviors.

Geography Analysis

In 2025, the United Kingdom holds a 16.05% share of Europe's free from food and beverage market. This dominance is reinforced by stringent allergen labeling regulations and a robust consumer base. The market's maturity is underscored by consumers' heightened awareness of dietary alternatives and their deep trust in product safety and quality. With a rising plant-based movement and a vast retail infrastructure, the United Kingdom solidifies its position as Europe's innovation leader in the free from sector. Additionally, the United Kingdom benefits from a well-established network of manufacturers and retailers that prioritize innovation and cater to diverse dietary needs. The presence of prominent brands and consistent investment in research and development further strengthens the country's leadership in this market.

Russia's free from market is on the rise, with a projected CAGR of 12.48% through 2031. This growth is driven by increasing health consciousness and a growing demand for gluten-free, dairy-free, and plant-based products. Strategic government initiatives, such as the 2023 Strategy for Organic Production and the Food Security Doctrine, promote domestic production, organic farming, and clean-label choices. With rising consumer spending and regulatory support for e-commerce and non-GMO policies, Russia's market development is poised for acceleration. Furthermore, the expansion of local production capabilities and the growing presence of international brands in the Russian market are contributing to the diversification of product offerings, making free from products more accessible to a broader consumer base.

Germany, Italy, France, and other European nations are advancing in the free from sector, each shaped by distinct consumer trends and regulatory environments. Germany benefits from strong distribution networks, which ensure the availability of free from products across various retail channels, including supermarkets, specialty stores, and online platforms. Italy's demand is spurred by wellness trends and dietary inclusivity in its tourism sector, with restaurants and hotels increasingly accommodating dietary restrictions. France, known for its culinary heritage, is gradually embracing plant-based alternatives, supported by a growing number of startups and established companies introducing innovative products. Additionally, countries like Spain, the Netherlands, Poland, Belgium, and Sweden are emerging as key players, driven by increased consumer awareness, evolving dietary preferences, and enhancements in retail and distribution networks.

Competitive Landscape

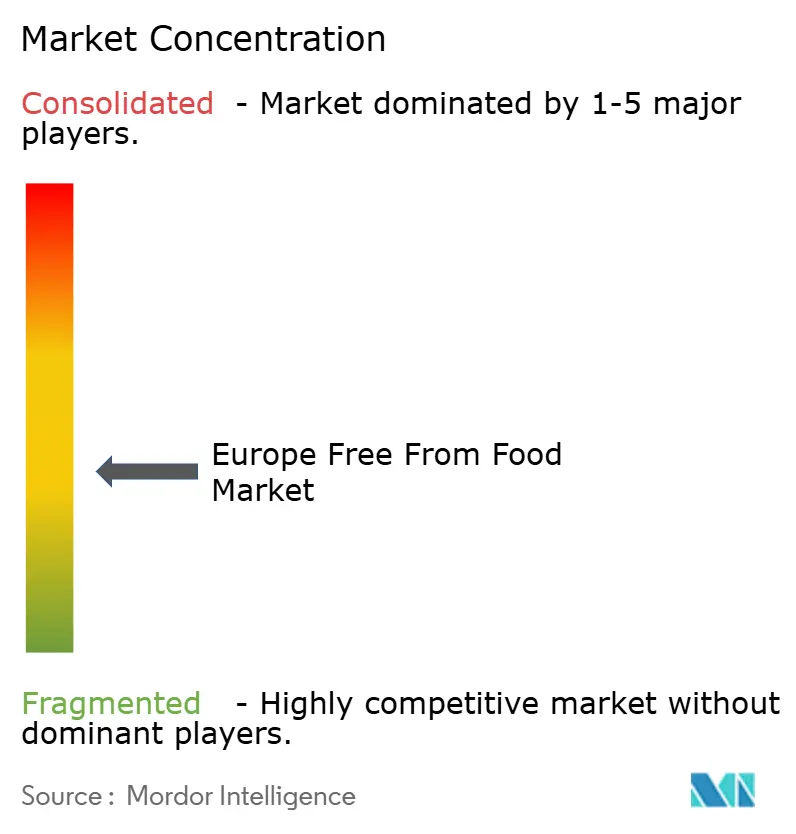

Europe's free from food market is moderately fragmentated. This market structure creates a competitive environment where established multinational corporations and specialized free from brands actively compete for market share. Market leaders, including Danone S.A., Nestlé S.A., General Mills Inc., and Oatly Group AB, implement comprehensive growth strategies combining organic innovation with strategic acquisitions. These companies are making substantial investments in advanced technologies, including high hydrostatic pressure processing, precision fermentation, and enzyme engineering, to enhance product functionality while maintaining clean label standards.

The competitive landscape is evolving with emerging opportunities in specialized free from categories that extend beyond traditional allergen-free products. Companies are developing solutions for specific health conditions, implementing sustainable packaging innovations, and creating personalized nutrition options for diverse dietary requirements. New market entrants are establishing their presence through direct-to-consumer channels and specialized product positioning, challenging established players in niche segments.

Market dynamics are further shaped by strategic collaborations and expansion initiatives. A notable development is the planned European market entry of JUST Egg, a plant-based egg alternative, through its partnership with Vegan Food Group (VFG) in April 2025. This partnership exemplifies the industry trend of technology-focused companies collaborating with established market players to expand their geographical presence and enhance market penetration.

Europe Free From Food Industry Leaders

Danone S.A.

Nestlé S.A.

General Mills Inc.

Oatly Group AB

Arla Foods amba

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Violife launched Supreme Cheddarton, a plant-based cheddar cheese alternative, in the United Kingdom. The product contains 30% less fat than traditional dairy cheddar and is the first in its category to be a high-protein option.

- January 2025: Califia Farms introduced a new line of plant-based milk products containing three ingredients. The products include almond milk and oat milk, each made with its respective base ingredient (almonds or oats), water, and minimal salt.

- August 2024: Plant-based food company The Happy Pear introduced a range of high-fiber granolas and vitamin drinks in the United Kingdom. The products contain 100% natural ingredients and use sustainable packaging.

- July 2023: Dr Schär invested USD 13.2 million to expand its gluten-free biscuit production at its manufacturing facility in Dreihausen, Germany. The investment includes new equipment for measuring biscuit cream, which will improve ingredient dosing accuracy and reduce waste.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European free-from food market as packaged foods and beverages intentionally formulated without at least one common dietary component, such as gluten, lactose/dairy, meat, GMOs, or major allergens, and sold through retail and food-service outlets across EU and U.K. territories.

Scope exclusion: Nutraceutical pills, prescription hypo-allergenic formulas, and loose bulk ingredients are kept outside this assessment.

Segmentation Overview

- By Product Product

- Bakery and Confectionery

- Dairy Alternatives

- Snacks

- Beverages

- Meat Substitutes

- Ready Meals

- Baby Food

- Others

- By Free From Type

- Gluten-Free

- Dairy-Free

- Meat-Free

- GMO-Free

- Others

- By Distribution Channel

- Supermarkets/Hypermarkets

- Online Retail Stores

- Convenience Stores

- Specialty Stores

- Others

- By Geography

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with dietitians, procurement heads at supermarket chains, and plant-based brand managers across Germany, the U.K., France, Spain, and Poland to cross-check ingredient cost swings, private-label penetration, and likely reformulation timelines. These conversations filled data gaps and grounded our assumptions before final triangulation.

Desk Research

We began with trade data and consumer nutrition surveys from Eurostat, FAO, and the European Food Safety Authority, then reviewed allergy prevalence papers in journals like Foods and Nutrients. Sales splits came from annual reports and 10-Ks of diversified food groups as compiled on D&B Hoovers, while pricing corridors were validated through retailer scans in Factiva archives. Regulatory insights were drawn from the EU Food Information Regulation and national labeling directives. The sources named illustrate, rather than exhaust, the wider literature consulted.

Market-Sizing & Forecasting

We anchor 2024 demand using a top-down reconstruction of packaged food retail sales, stripping out conventional items through prevalence-based penetration filters for gluten-free, dairy-free, meat-free, and GMO-free lines. Select bottom-up tests, supplier roll-ups for oat-drink processors and sampled average selling price multiplied by volumes in specialty aisles, fine-tune totals. Key variables include diagnosed celiac incidence, vegan population share, online grocery share, plant protein price index, advertising spend on "clean-label" claims, and new product launch counts. A multivariate regression with lagged health-awareness indices projects each driver, and ARIMA smoothing adjusts for pandemic distortions.

Data Validation & Update Cycle

Outputs pass variance checks against trade flows, retailer scan panels, and historic CAGR bands, with anomalies escalated to senior reviewers. Reports refresh each year; material events such as new allergen rules trigger interim updates, and an analyst re-verifies figures just before delivery.

Why Mordor's Europe Free From Food Baseline Commands Reliability

Published values often differ because firms choose dissimilar product buckets, pricing anchors, and refresh cadences.

Key gap drivers include segment breadth, as some rivals count only gluten-free lines, differing average price progression for premium dairy alternatives, and shorter forecast windows that miss regulatory phase-ins. Our model locks scope to all retail free-from categories, applies country-wise weighted ASPs, and benefits from annual reconfirmation, elements that together yield a balanced view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.61 B (2025) | Mordor Intelligence | - |

| USD 15.0 B (2024) | Regional Consultancy A | Excludes meat-free and GMO-free ranges |

| USD 9.0 B (2024) | Global Consultancy B | Uses supermarket scan data only, ignores food-service |

In summary, our disciplined scope setting, dual-approach modeling, and live validation loops let decision-makers rely on Mordor Intelligence figures as the most transparent, repeatable baseline available today.

Key Questions Answered in the Report

What is the current size of the Europe free from food market and where is it headed?

The market is worth USD 31.79 billion in 2026 and, growing at an 11.12% CAGR, is projected to reach USD 53.86 billion by 2031.

Which product type holds the largest revenue share today?

Dairy alternatives lead with 35.74% of 2025 sales, reflecting strong consumer acceptance of plant-based milks, yogurts and cheeses.

What is the fastest-growing product category through 2031?

Meat substitutes are forecast to expand at a 11.67% CAGR from 2026 to 2031, outpacing all other product types.

Which free-from segment is currently dominant?

Dairy-free items command the highest share at 36.92% in 2025, driven by rising lactose intolerance awareness and sustainability concerns.

Page last updated on: