Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

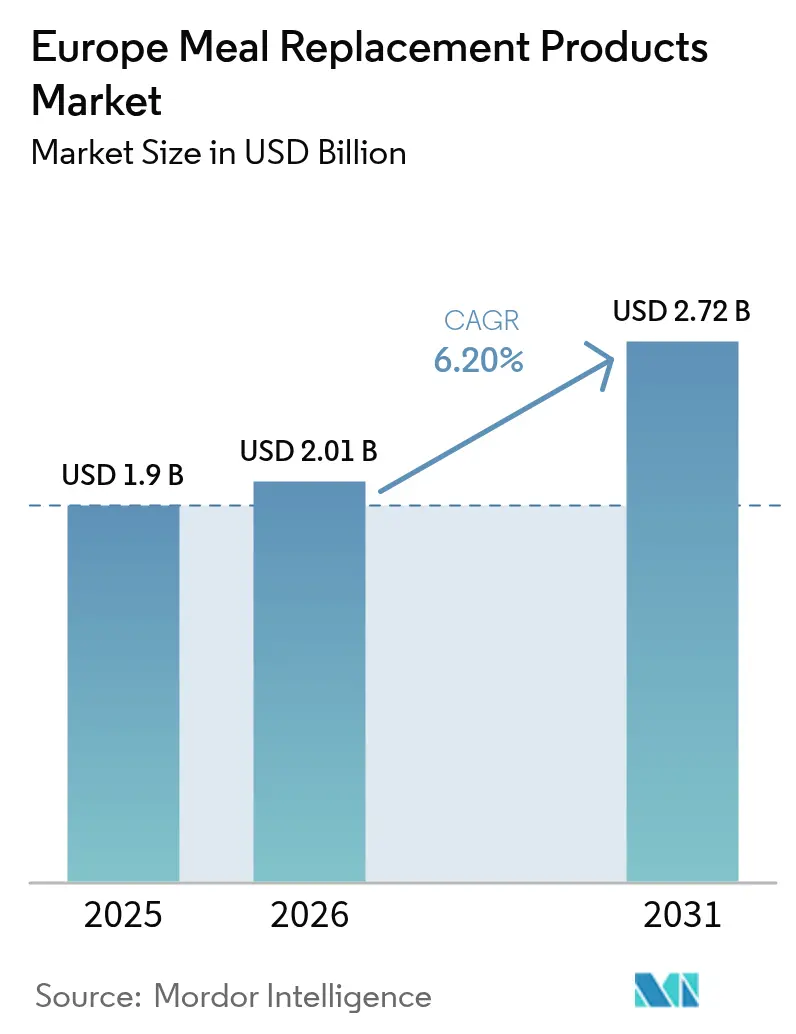

| Base Year Market Size (2025) | USD 1.9 Billion |

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.72 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Meal Replacement Products Market Analysis by Mordor Intelligence

The Europe Meal Replacement Products Market size is projected to be USD 1.90 billion in 2025, USD 2.01 billion in 2026, and reach USD 2.72 billion by 2031, growing at a CAGR of 6.20% from 2026 to 2031. This growth trajectory reflects the convergence of health-conscious consumer behavior, workplace wellness adoption, and technological innovations in product formulation and packaging. The market's expansion accelerates as European consumers increasingly prioritize convenient nutrition solutions that align with busy lifestyles while meeting stringent regulatory standards set by the European Food Safety Authority [1]Source: European Food Safety Authority, "Novel food" efsa.europa.eu. Supply–chain resilience and regulatory agility have emerged as strategic differentiators for manufacturers seeking to secure raw-material access, sustain research and development pipelines, and protect margins. Competition remains moderate, allowing both global multinationals and agile entrants to gain ground through differentiated positioning and channel expansion. The market confronts significant headwind,s including raw material supply disruptions, exemplified by sunflower lecithin shortages causing 3-4x price increases since the Russia-Ukraine conflict.

Key Report Takeaways

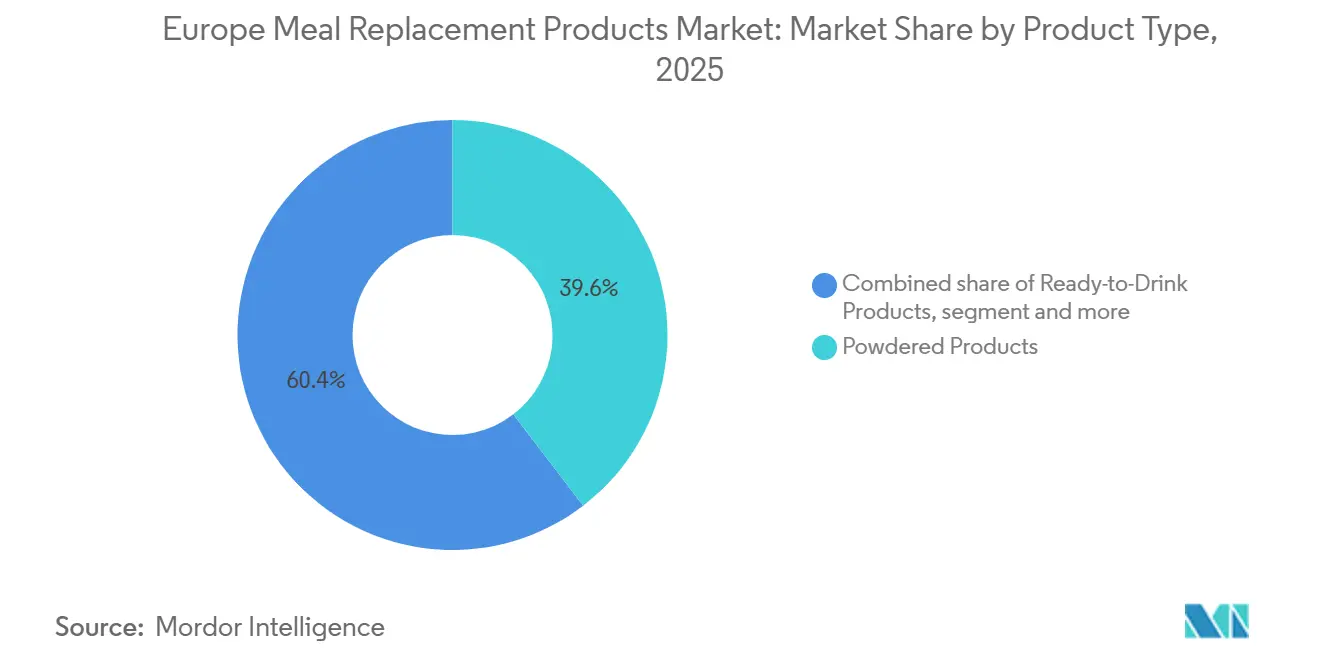

- By product type, powdered products led with 39.59% of Europe's meal replacement products market share in 2025, whereas soup formats are advancing at a 10.02% CAGR through 2031.

- By packaging format, bottles/jars held 32.33% of the European meal replacement products market size in 2025, and tetra packs and cartons are expanding at a 7.49% CAGR to 2031.

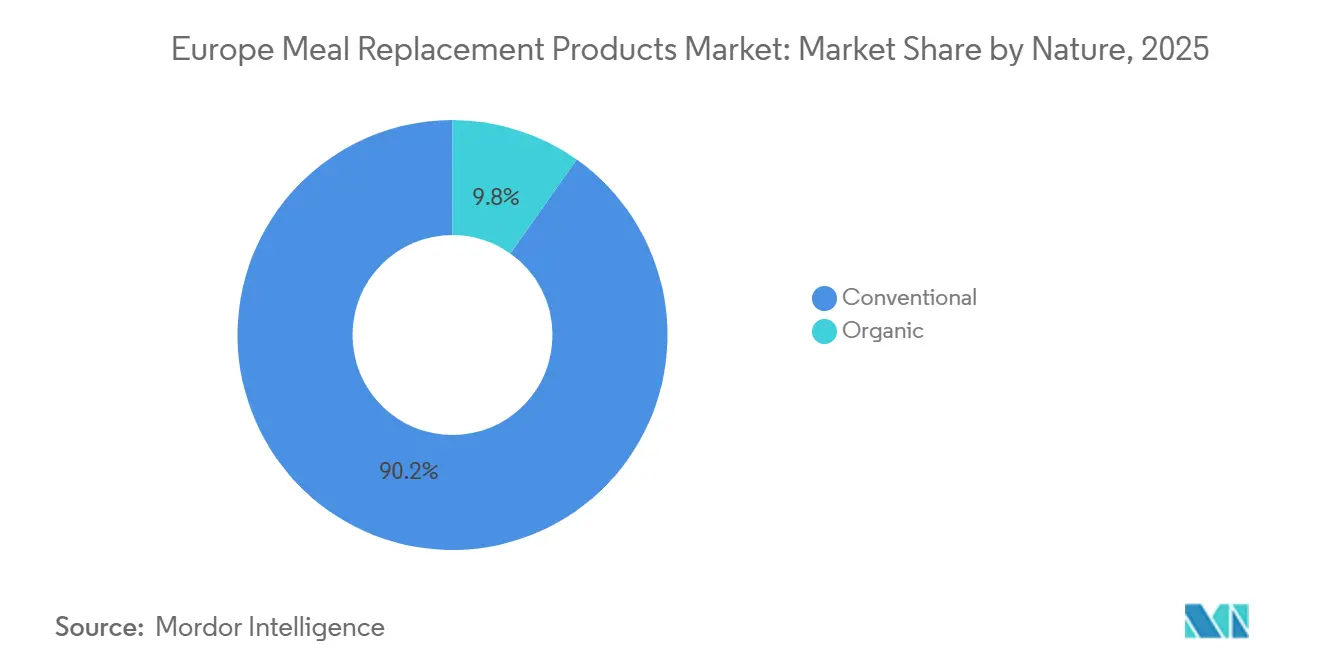

- By nature, conventional offerings commanded 90.19% share of the European meal replacement products market size in 2025, while organic variants are forecast to rise at an 9.75% CAGR between 2026 and 2031.

- By distribution channel, pharmacies and health stores contributed 40.66% share of the European meal replacement products market size in 2025; online retailers recorded the fastest CAGR at 9.11% through 2031.

- By geography, Germany held 21.41% of the European meal replacement products market share in 2025 and is set to grow at 8.13% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Meal Replacement Products Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-Conscious Consumers Embrace Protein-Rich Alternatives | +2.1% | Global, strongest in Germany, UK, Netherlands | Medium term (2-4 years) |

| Convenient Product Formats Drive Adoption of Meal Replacement Solutions | +1.8% | Urban centers across Europe, led by UK, France | Short term (≤ 2 years) |

| Corporate Wellness Programs Support Meal Replacements | +1.2% | Continental Europe, Nordic countries | Medium term (2-4 years) |

| Portion Control Awareness Increases Product Adoption | +0.9% | Western Europe, emerging in Eastern Europe | Long term (≥ 4 years) |

| Technology Advances Enhance Product Quality | +0.7% | Manufacturing hubs in Germany, Netherlands, France | Long term (≥ 4 years) |

| E-Commerce Enhances Global Market Distribution | +0.6% | All European markets, accelerated in post-COVID landscape | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health-Conscious Consumers Embrace Protein-Rich Alternatives

European consumers increasingly prioritize protein-rich nutrition solutions, with 45% of health-focused individuals specifically citing increased protein consumption as a dietary goal. This trend extends beyond traditional fitness enthusiasts to encompass mainstream consumers seeking satiety, weight management, and muscle support benefits. The protein fortification movement now spans categories previously untouched by nutritional enhancement, including ice cream, cakes, and breakfast cereals, indicating market maturation beyond conventional shake formats. Novel protein sources gain regulatory acceptance, with the European Commission authorizing UV-treated yellow mealworm powder in January 2025 for use in bread, pasta, and processed foods, expanding ingredient options for manufacturers [2]Source: Publications Office of the European Union, "COMMISSION IMPLEMENTING REGULATION (EU) 2025/89 of 20 January 2025", eur-lex.europa.eu. The convergence of flexitarian dietary patterns with protein consciousness creates sustained demand for plant-based and hybrid protein formulations that deliver both nutritional density and environmental sustainability credentials.

Convenient Product Formats Drive Adoption of Meal Replacement Solutions

Format innovation accelerates adoption as consumers demand nutrition solutions that integrate seamlessly with mobile lifestyles and hybrid work patterns. Ready-to-drink formats capture market momentum by eliminating preparation barriers, particularly appealing to time-constrained professionals and urban commuters who prioritize immediate consumption capability. The shift toward convenience extends beyond liquid formats to include portion-controlled bars, single-serve packets, and ambient-stable formulations that require no refrigeration or mixing equipment. Tetra Pak's Industrial Protein Mixer addresses foaming challenges during liquid production, enabling manufacturers to reduce product loss by over EUR 250,000 annually while extending shelf life and improving operational efficiency. This technological advancement directly supports the scalability of convenient liquid formats that drive category growth across European markets.

Corporate Wellness Programs Support Meal Replacements

Workplace nutrition initiatives gain momentum as employers recognize the connection between employee health and productivity outcomes, particularly in post-pandemic recovery environments. Pluxee, a major European employee benefits provider, projects 7-9% CAGR for meal and food benefits from 2024-2026, with current market penetration at only 25% of addressable opportunities, indicating substantial expansion potential. Small and medium enterprises represent the largest untapped segment, with only 10% currently offering employee benefit packages, creating a significant growth runway as digital meal benefit platforms reduce implementation barriers. The digitalization of meal benefits reaches 92% of business volume, enabling seamless integration of meal replacement products into corporate wellness programs through virtual cards and mobile applications. Corporate wellness adoption accelerates in Continental Europe, where supportive tax exemption frameworks and regulatory environments encourage employer investment in employee nutrition programs.

Technology Advances Enhance Product Quality

Manufacturing technology evolution enables superior product quality while addressing traditional formulation challenges that historically limited consumer acceptance. European machinery manufacturers including Bühler, GEA, and Andritz develop specialized equipment for plant-based protein processing, with Bühler's Protein Application Centre in Switzerland offering both pilot-scale and industrial 200 kg/h production lines for product development and scale-up. Advanced processing techniques including ultrasonic extraction, pulsed electric fields, and enzymatic modification improve protein functionality, solubility, and digestibility while reducing off-flavors that previously deterred mainstream adoption. Flavor mitigation technologies become critical as manufacturers expand beyond traditional vanilla and chocolate profiles to accommodate diverse European taste preferences and cultural dietary patterns. The integration of AI and precision nutrition capabilities enables personalized formulation approaches, with companies like PepsiCo establishing Advanced Personalization Ideation Centers to develop individualized nutrition solutions.

Restraints Impact Analysis of Europe Meal Replacement Products Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Shortages Disrupt Supply Chain | -1.4% | Eastern Europe supply corridors, manufacturing centers | Short term (≤ 2 years) |

| Regulations Constrain Product Development and Marketing | -0.8% | EU-wide, varying national implementation | Medium term (2-4 years) |

| Consumer Concerns Over Food Additives Impact Sales | -0.6% | Western Europe, health-conscious demographics | Long term (≥ 4 years) |

| Balancing Product Freshness with Quality Standards | -0.4% | Distribution networks across Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Shortages Disrupt Supply Chain

Supply chain vulnerabilities intensify as geopolitical tensions and climate events disrupt critical ingredient flows, with sunflower lecithin shortages exemplifying systemic risks facing European manufacturers. The Russia-Ukraine conflict eliminated over 50% of global sunflower seed production, causing lecithin prices to increase 3-4x and forcing widespread reformulation efforts across the industry. European protein ingredient supply faces additional pressure from import dependency, with EU self-sufficiency at only 3% for high-protein crops like soybean meal, exposing manufacturers to price volatility and trade disruptions [3]Source: European Parliament, "EU protein strategy", europarl.europa.eu. China's dominance in vitamin and amino acid supply chains creates concentration risk, supplying over 70% of vitamins and 75% of lysine globally, making European meal replacement manufacturers vulnerable to supply disruptions and regulatory changes. The European Commission's protein strategy initiatives aim to boost domestic production through CAP support measures, but structural constraints including land availability and competitiveness challenges limit near-term supply security improvements.

Regulations Constrain Product Development and Marketing

Regulatory complexity under the EU Novel Foods Regulation creates development bottlenecks and market entry barriers, particularly for innovative ingredients and processing technologies. EFSA's updated guidance effective February 2025 requires comprehensive dossiers including compositional, toxicological, nutritional, and consumption data for novel ingredients, potentially extending approval timelines and increasing development costs. The EU Deforestation Regulation, postponed to end-2025, threatens to create compliance premiums for European manufacturers using soybean-derived ingredients, potentially disadvantaging them versus global competitors using non-compliant supply chains. Varying national implementation of EU directives creates market fragmentation, with countries like Italy maintaining distinct botanical ingredient lists and maximum level requirements that complicate pan-European product launches. The regulatory framework's emphasis on safety and transparency, while protecting consumers, lengthens innovation cycles and favors established players with regulatory expertise over smaller innovative entrants seeking to introduce disruptive formulations or novel protein sources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Meal Replacement Products Market Segment Analysis

By Product Type:

Soups Accelerate GrowthSoup products emerge as the fastest-growing segment with 10.02% CAGR through 2031, despite powdered products maintaining market leadership at 39.59% share in 2025. This growth differential reflects a culturally significant segment in markets with strong soup traditions like Germany and Eastern Europe. Nutritional Bars capture a steady market position by addressing portion control and portability needs, while the ready-to-drink format preference evolves toward immediate consumption convenience, particularly among urban professionals and mobile consumers who prioritize grab-and-go nutrition solutions.

The segment dynamics reveal a fundamental shift in consumption patterns as European lifestyles increasingly favor convenience over preparation time. Tetra Pak's development of specialized protein mixing technology addresses foaming challenges in liquid production, enabling manufacturers to scale RTD formats while maintaining product quality and extending shelf life. Other Product Types, including emerging formats like protein-enriched snacks and functional beverages, gain traction as manufacturers expand beyond traditional meal replacement categories to capture broader nutrition occasions throughout the day.

By Packaging Format:

Sustainability Drives InnovationTetra Packs and Cartons demonstrate the highest growth trajectory at 7.49% CAGR through 2031, challenging the dominance of bottles/jars, which hold 32.33% market share in 2025. This shift reflects mounting sustainability pressures and technological breakthroughs in paper-based packaging that maintain product integrity while reducing environmental impact. Tetra Pak's paper-based barrier technology, validated through large-scale trials with Lactogal in Portugal, achieves up to 33% carbon footprint reduction while increasing renewable content to 90%.

Pouches maintain steady growth by offering lightweight, flexible packaging solutions that optimize logistics costs and shelf space efficiency. The packaging evolution extends beyond environmental considerations to encompass e-commerce optimization, with formats designed for shipping durability and consumer unboxing experience becoming increasingly important as online retail channels expand. The other category includes emerging packaging innovations such as recyclable single-serve sachets and biodegradable containers that address specific market niches and regulatory requirements across different European jurisdictions.

By Nature:

Organic Segment Capitalizes on Premium PositioningOrganic products achieve 9.75% CAGR through 2031, while conventional products maintain 90.19% market share in 2025, indicating a premium segment expansion driven by health-conscious consumers willing to pay for certified organic ingredients and production methods. The organic growth trajectory benefits from increasing consumer awareness of ingredient sourcing, environmental impact, and perceived health benefits associated with organic certification standards. European organic regulations provide clear differentiation criteria that enable premium pricing and brand positioning strategies.

The conventional segment's market dominance reflects price sensitivity among mainstream consumers and the broader accessibility of non-organic formulations across diverse retail channels. However, the growth differential suggests gradual market share erosion as organic products become more widely available and price premiums moderate through scale economies. Manufacturers increasingly offer dual product lines to capture both value-conscious and premium segments, with organic variants serving as brand halo products that enhance overall portfolio perception and justify premium pricing across related product categories.

By Distribution Channel:

E-Commerce Transforms Retail LandscapeOnline Retailers achieve the highest growth rate at 9.11% CAGR through 2031, while pharmacies and health stores retain 40.66% market share in 2025. In Europe, pharmacies and health stores have emerged as the leading sales points for meal replacements, leveraging their reputation as trusted, expert-driven outlets. This dominance stems from consumers' inclination to seek professional guidance on nutrition and weight management, coupled with the confidence they derive from acquiring premium, authentic health products at specialized retailers. The e-commerce acceleration benefits from improved logistics infrastructure, subscription model adoption, and personalized nutrition trends that favor direct-to-consumer relationships. Rohlik Group's EUR 160 million funding round in 2025 to expand across DACH and Central and Eastern Europe exemplifies the investment momentum behind online grocery platforms that serve as key distribution channels for meal replacement products.

Convenience Stores maintain important roles in impulse purchasing and expert consultation scenarios, particularly for sports nutrition and specialized dietary requirements. The multi-channel approach becomes essential as consumers demonstrate channel-switching behavior based on purchase occasion, product type, and convenience factors. Other distribution channels, including corporate wellness programs and healthcare provider recommendations, represent emerging opportunities that align with the medicalization of nutrition and workplace health initiatives gaining traction across European markets.

Geography Analysis

Germany Meal Replacement Products Market

In 2025, Germany accounted for 21.41% of Europe's meal replacement products market, with an anticipated 8.13% CAGR growth through 2031. With one of Europe's largest food and beverage sectors, Germany benefits from a strong manufacturing and distribution network. Its large population and high purchasing power drive significant demand for meal replacements and convenience foods. This establishes Germany as a key hub for both consumption and production, surpassing smaller EU nations in market penetration. While urbanization and fast-paced lifestyles influence demand across Europe, these factors are particularly evident among Germany's workforce. Meal replacements, such as shakes, bars, and ready-to-drink beverages, appeal to professionals, fitness enthusiasts, and individuals focused on weight management. Germany's workforce structure and productivity-oriented culture further increase the demand for quick, nutritionally balanced meals. Additionally, Germany serves as a leading innovation hub, driving advancements in plant-based formulations, protein-enriched products, and functional foods. As the European market experiences growing interest in clean-label, vegan, and allergen-free products, German consumers, known for adopting these trends early, significantly contribute to the country's market share.

United Kingdom, Spain and France Meal Replacement Products Market

The UK's growth trajectory moderates as market saturation approaches, creating opportunities for innovative formats and premium positioning strategies. Brexit-related regulatory divergence from EU standards creates both challenges and opportunities, as UK-specific product formulations may emerge while cross-border trade complexity increases operational costs for manufacturers serving both UK and continental European markets. In Spain, the market is driven by increasing health consciousness, corporate wellness program adoption, and integration of convenient nutrition solutions into Mediterranean dietary patterns. The Spanish market benefits from strong economic recovery, urbanization trends, and cultural shifts toward fitness and wellness that align with meal replacement product positioning. Germany and France represent substantial markets with steady growth trajectories, supported by strong manufacturing bases, health-conscious consumer segments, and corporate wellness initiatives that incorporate nutrition benefits into employee programs. These markets demonstrate sophisticated consumer understanding of nutritional labeling and ingredient quality, creating demand for premium formulations and transparent sourcing practices.

Broader European Markets

Italy, the Netherlands, Poland, Belgium, and Sweden represent diverse growth opportunities with varying market characteristics and development stages. The Netherlands benefits from advanced logistics infrastructure and high e-commerce penetration that support online retail growth, while Italy's market development accelerates through increasing fitness culture adoption and urbanization trends. Poland demonstrates rapid economic development that enables premium nutrition product adoption, while Belgium and Sweden represent smaller but affluent markets with high health consciousness and willingness to pay for quality nutrition solutions. The rest of Europe encompasses markets ranging from Nordic countries with established health and wellness cultures to Eastern European markets experiencing dietary westernization and increasing disposable income that supports meal replacement product adoption across diverse consumer segments.

Competitive Landscape

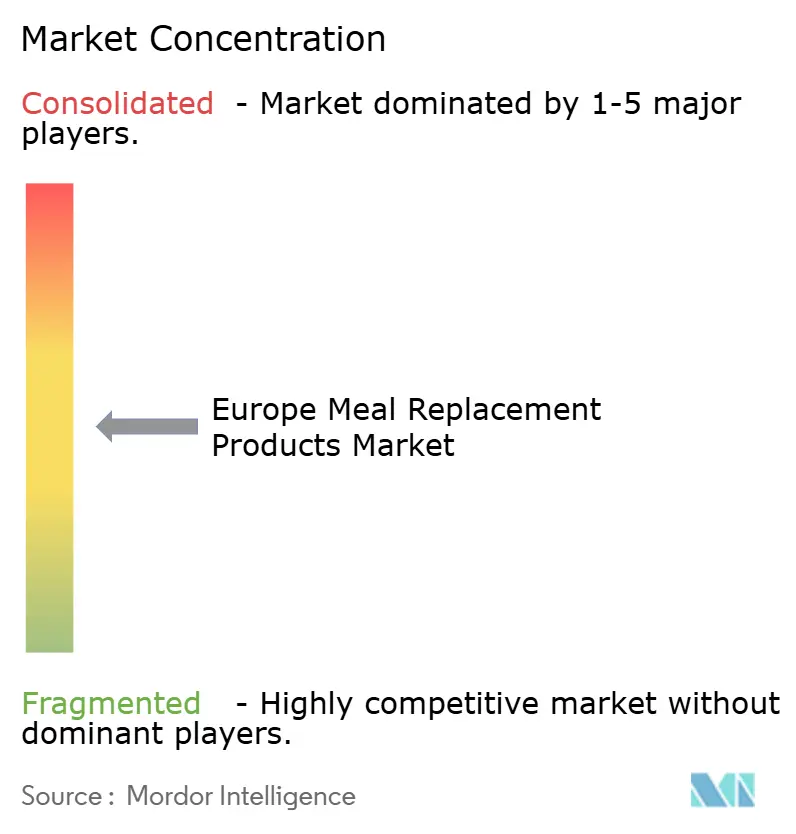

The European meal replacement products market exhibits moderate fragmentation, creating a competitive environment where established multinational players compete alongside specialized nutrition brands and emerging disruptors. Market leaders, including Herbalife Nutrition Ltd., YFood Labs GmbH, Huel Ltd., and Otsuka Holdings Co., Ltd., leverage extensive distribution networks, regulatory expertise, and research and development capabilities to maintain market position, while smaller players differentiate through specialized formulations, direct-to-consumer models, and niche positioning strategies.

The competitive dynamics intensify as traditional food companies expand into nutrition categories while specialized sports nutrition brands broaden their target demographics beyond fitness enthusiasts to capture mainstream health-conscious consumers. Strategic patterns reveal increasing emphasis on sustainability credentials, with companies investing in packaging innovations and supply chain transparency to meet evolving consumer expectations and regulatory requirements. The market disruption exemplified by Mars' decision to shut down Foodspring despite a EUR 250 million acquisition demonstrates the challenges of sustaining growth in increasingly competitive conditions where consumer acquisition costs rise and brand differentiation becomes more difficult.

Technology adoption accelerates as companies integrate AI-driven personalization, advanced manufacturing processes, and digital marketing capabilities to optimize product development cycles and consumer engagement strategies. White-space opportunities emerge in corporate wellness channels, personalized nutrition solutions, and sustainable packaging innovations that address regulatory compliance requirements while delivering cost-effective manufacturing solutions.

Europe Meal Replacement Products Industry Leaders

-

Herbalife Nutrition Ltd.

-

YFood Labs GmbH

-

Huel Ltd.

-

Otsuka Holdings Co Ltd.

-

Almased GmbH

- *Disclaimer: Major Players sorted in no particular order

Europe Meal Replacement Products Market Companies Covered in this Report

- Abbott Laboratories

- Almased GmbH

- YFood Labs GmbH

- Glanbia Plc

- Fresenius Kabi Deutschland GmbH

- Mars Inc.

- Nestle S.A.

- Danone S.A.

- Herbalife Nutrition Ltd.

- Enervit S.p.A.

- Heaven Labs (Mana)

- Amway Corporation

- Jimmy Joy

- LighterLife

- Huel Ltd

- Orkla Group (Nutrilett)

- Certmedica International GmbH (Farmoline)

- Naturhouse Health, S.A.

- Otsuka Holdings Co Ltd.

Recent Industry Developments in Europe Meal Replacement Products Market

- September 2025: Dozz, the first chilled, ready-to-eat soup in a 100% recyclable aluminium can, set a new standard for food-to-go in the United Kingdom. Designed to be eaten cold right out of the container without the need for a bowl, microwave or silverware, the inventively presented set of ten nutritious soups were aimed at busy, health-conscious consumers seeking a quick lunch or snack on the run.

- July 2025: Arla Protein, a brand of Arla Foods, introduced a ready-to-drink milkshake targeting on-the-go consumers in Denmark. Arla Protein Milkshake, available in 200ml cups, featured a creamy texture and delivered 20g of protein per serving. It was lactose-free, contained no added sugars and was under 182 calories, making it an appealing choice for health-conscious consumers. The milkshake came in two flavours: Vanilla Fudge and Chocolate Brownie.

- April 2025: More Nutrition, a German healthy lifestyle brand, entered the United Kingdom market by introducing a bestselling range of protein snacks, iced coffees, collagen and functional food products. Known for its high-protein, low-sugar product range, the brand aimed to meet growing British demand for convenient, functional food and drink options that supported health without compromising on taste. More Nutrition's bestselling range included Protein Iced Coffee, Protein Bars, Clear Whey Protein Isolate, Whey and Casein Protein blends, Zerup syrups, Flavoured Powders, among others.

- January 2025: Tribe, the UK-based natural energy bar brand, recently launched a new Protein + Focus bar with lion's mane mushroom and adaptogens in early 2025, supported by a GBP 2.4 million funding round. Additionally, Tribe partnered with Wildfarmed to launch the UK's first energy bar made with regeneratively farmed oats in April 2025, with these oat bars now available in Sainsbury's.

Europe Meal Replacement Products Market Report Scope

A meal replacement is a beverage, bar, bowl of soup, etc. that is meant to replace a substantial meal and typically has a set amount of calories and nutrients. The Europe meal replacement products market is segmented by product type, distribution channel, and geography. By product type, the market studied is segmented into ready-to-drink products, nutritional bars, powdered supplements, and other product types. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, pharmacies and health stores, and other distribution channels. Furthermore, the report takes into consideration the market for meal replacement products in established and emerging countries of Europe including the United Kingdom, Spain, Italy, Germany, Russia, France, and Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

Segmentation Overview

By Product Type

| Powdered Products |

| Ready-to-Drink Products |

| Nutritional Bars |

| Soups |

| Other Product Types |

By Packaging Format

| Bottles/Jars |

| Pouches |

| Tetra Packs and Cartons |

| Others |

By Nature

| Conventional |

| Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Pharmacies and Health Stores |

| Online Retail Stores |

| Other Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Powdered Products |

| Ready-to-Drink Products | |

| Nutritional Bars | |

| Soups | |

| Other Product Types | |

| By Packaging Format | Bottles/Jars |

| Pouches | |

| Tetra Packs and Cartons | |

| Others | |

| By Nature | Conventional |

| Organic | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Pharmacies and Health Stores | |

| Online Retail Stores | |

| Other Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 size of the Europe meal replacement products market?

The segment is valued at USD 2.01 billion in 2026.

How fast is the category expected to grow through 2031?

It is projected to post a 6.20% CAGR, reaching USD 2.72 billion by 2031.

Which product format shows the strongest growth momentum?

Soups offerings lead with a 10.02% CAGR through 2031.

How important is e-commerce to future sales?

Online retailers are forecast to expand at an 9.11% CAGR, driven by subscription models and rapid-delivery grocery platforms.

Page last updated on: