Europe Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

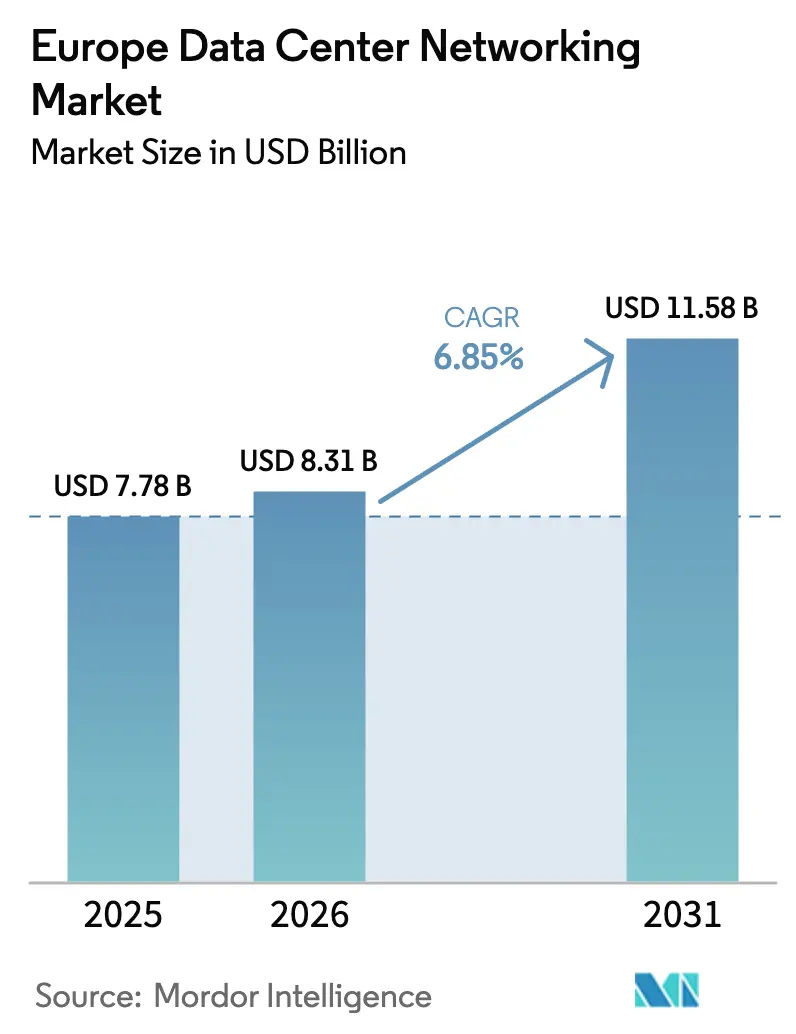

| Base Year Market Size (2025) | USD 7.78 Billion |

| Market Size (2026) | USD 8.31 Billion |

| Market Size (2031) | USD 11.58 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Data Center Networking Market Analysis by Mordor Intelligence

Europe data center networking market size in 2026 is estimated at USD 8.31 billion, growing from 2025 value of USD 7.78 billion with 2031 projections showing USD 11.58 billion, growing at 6.85% CAGR over 2026-2031. Expansive AI infrastructure roll-outs, rapid edge computing adoption, and EU-wide sustainability mandates form the structural bedrock of this growth. Hyperscalers are moving aggressively; Brookfield has earmarked EUR 20 billion for French AI capacity while Microsoft is deploying EUR 4 billion to expand regional cloud estates, signaling a multi-year investment super-cycle. Hardware refreshes linked to the shift from 100 GbE to 400 GbE and 800 GbE accelerate replacement sales, and liquid-cooled platforms gain traction as operators prepare for mandatory energy-use reporting. Consolidation is rewriting competitive lines: Hewlett Packard Enterprise seeks to fold Juniper Networks into its portfolio, Cisco defends share through Silicon One, and Arista Networks gains mindshare on the back of 800-gigabit switch success. Secondary metros such as Madrid, Berlin, and Warsaw capture new builds as FLAP hubs confront grid limits; these locations become testbeds for energy-efficient designs anchored in renewable power.

Key Report Takeaways

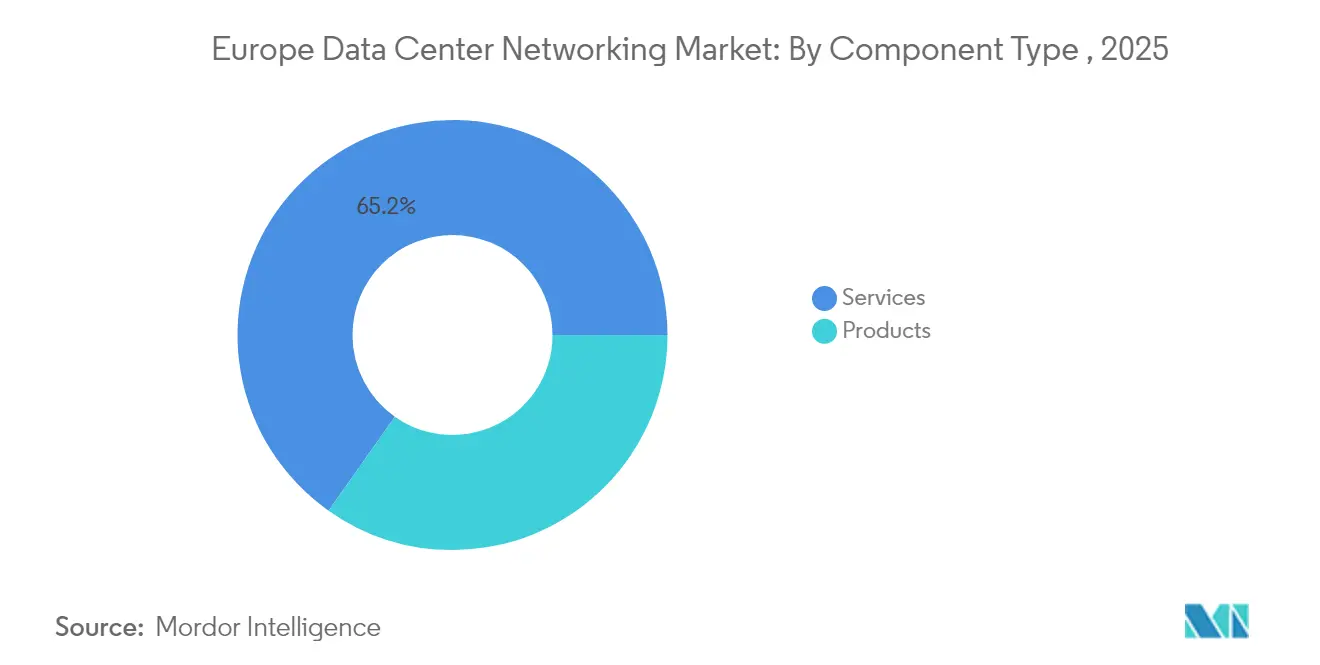

- By component, Ethernet switches led with 34.78% of Europe data center networking market share in 2025, while software-defined networking controllers are projected to record a 11.76% CAGR through 2031.

- By end-user, the IT & telecommunications segment held 36.05% share of the Europe data center networking market size in 2025; banking, financial services and insurance is expanding at a 12.65% CAGR to 2031.

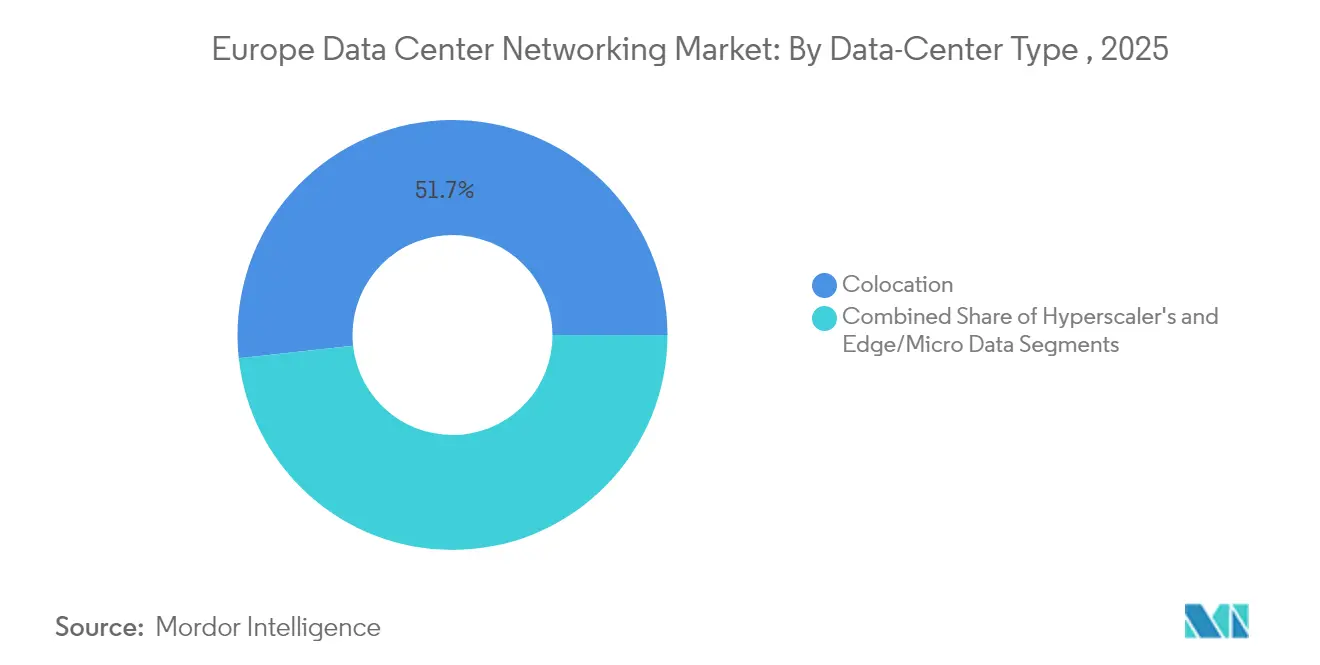

- By data-center type, colocation facilities accounted for 51.72% of the Europe data center networking market size in 2025, whereas hyperscaler cloud service providers are set to grow at a 14.05% CAGR.

- By bandwidth, 50-100 GbE configurations controlled 37.74% Europe data center networking market share in 2025, and >100 GbE deployments are forecast to rise at a 12.74% CAGR.

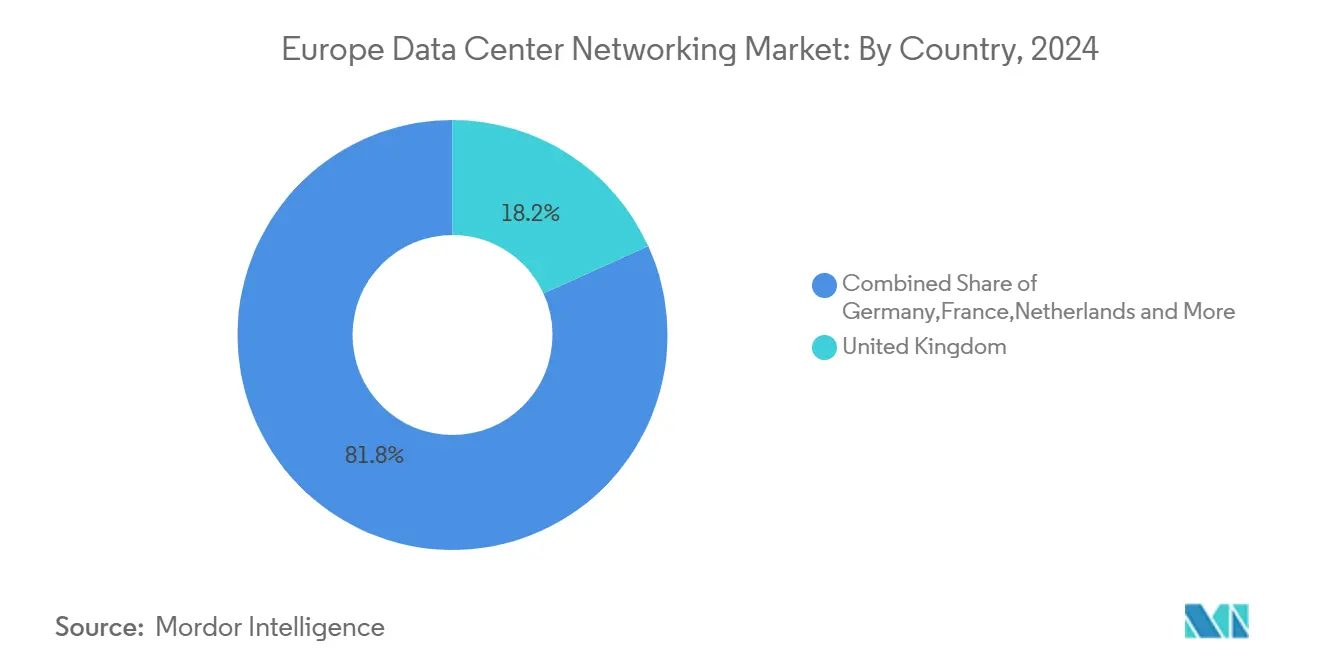

- By country, the United Kingdom captured 18.05% Europe data center networking market share in 2025; Spain is forecast to lead growth at a 10.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global data center networking market data by Mordor Intelligence represents that combined structure.

Europe Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud storage and reliable application performance | +1.8% | FLAP-D corridors and pan-EU enterprises | Medium term (2-4 years) |

| 5G and edge-computing traffic surge | +1.5% | Core EU markets, Nordic expansion | Medium term (2-4 years) |

| Migration to 400G/800G Ethernet switching | +1.2% | Frankfurt, Amsterdam, Dublin hyperscaler clusters | Short term (≤ 2 years) |

| EU push for energy-efficient liquid-cooled switching | +0.9% | Germany and Netherlands early adopters | Long term (≥ 4 years) |

| Shift of builds to secondary EU metros | +0.8% | Madrid, Berlin, Warsaw, Milan | Medium term (2-4 years) |

| Merchant silicon and open NOS adoption | +0.6% | Cost-sensitive Eastern Europe and SME segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud Storage and Reliable Application Performance

Forty-five percent of EU businesses procured cloud services in 2024, primarily for email hosting and file storage, underscoring mainstream reliance on off-premise platforms. Oracle Cloud Infrastructure was selected for European government workloads, indicating public-sector trust in cloud-native networks. Instant payment regulations require European banks to clear transactions within 10 seconds by 2025, a mandate that tightens latency budgets and favors ultra-low-jitter switching fabrics. The Trustworthy & Responsible AI Network linking leading hospitals depends on resilient inter-data-center paths to keep diagnostic AI online while remaining privacy-compliant. Together, regulatory imperatives and performance expectations elevate high-availability networking from operational necessity to board-level differentiator.

5G and Edge-Computing Traffic Surge

The EU intends to deploy 10,000 climate-neutral edge nodes by 2030, expecting 80% of processing to occur outside core sites.[1]Eurostat, “ICT Usage in Enterprises,” ec.europa.eu Demonstrations under the 5GMEC4EU program validate sub-millisecond edge fabrics that integrate optical circuit switching with SDN control planes. Deutsche Telekom positions edge as a pillar for national digital agendas, enabling smart-city telemetry and autonomous mobility. Micro data center revenues already exceeded USD 5.8 billion in 2023 and have a runway toward USD 160.8 billion by 2036, revealing a robust pipeline for ruggedized switches and intelligent edge controllers. This distributed topology re-routes traffic away from FLAP hubs, demanding new orchestration layers capable of real-time fault isolation across thousands of mini-sites.

Migration to 400G/800G Ethernet Switching

Hyperscale operators accelerated upgrades, with Arista supplying 7700R4 platforms to Meta’s European AI clusters and booking USD 7 billion in 2024 revenue, up 19.5% year on year. IEEE’s P802.3df release, coupled with interoperable 800 GbE demos at ECOC 2024, confirms the standardization path for next-gen optics. Cisco’s Silicon One unifies switching and routing on a single ASIC to simplify layer counts and trim energy draw. Google’s Jupiter network revision delivered 5× capacity while cutting capex by 30% through direct-connect optical fabrics.[2]Google Research, “Jupiter Rising: A Decade of Datacenter Networking,” research.google These transitions retire legacy 100 GbE estates, creating a replacement cycle that directly feeds Europe data center networking market expansion.

EU Push for Energy-Efficient Liquid-Cooled Switching

From September 2024, operators must file annual power-usage-effectiveness metrics under the revised Energy Efficiency Directive.[3]European Commission, “Directive (EU) 2023/1791 on Energy Efficiency,” ec.europa.eu CyrusOne’s FRA7 campus integrates waste-heat reuse, delivering 40 MW to local grids, a template for future German designs. Base-8 and Base-16 fiber plans improve port utilization and lower fan-out losses while meeting the EU sub-1.3 PUE objective. Berlin’s national strategy obliges new builds to tap renewables and export residual heat, compelling switch vendors to embed liquid-cool cold plates in top-of-rack gear. Vendors prioritizing green engineering, therefore, gain a policy-driven edge in the Europe data center networking market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising network complexity | -1.1% | Enterprise footprints across EU | Medium term (2-4 years) |

| Supply-chain shortage of optics and ASICs | -0.8% | Germany and Netherlands hit hardest | Short term (≤ 2 years) |

| Power-grid bottlenecks and permitting delays | -0.7% | FLAP-D metros and other urban centers | Long term (≥ 4 years) |

| Carbon- and water-use caps inflate TCO | -0.5% | EU-wide, tougher limits in Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Network Complexity

Hybrid cloud sprawl and AI pipelines complicate topologies faster than European enterprises can recruit qualified engineers. Juniper’s Apstra applies intent-based automation to multivendor fabrics, yet skills shortages persist as teams juggle Kubernetes, Terraform, and optical circuit switching. ETNO argues for policy relief that lets carriers recoup investments while delivering edge services. Without broad expertise, organisations defer upgrades, slowing refresh activity in the Europe data center networking market.

Supply-Chain Shortage of Optics and ASICs

Lead times for 400 G optical modules exceed 12 months, a constraint that mirrors COVID-era shocks according to Extreme Networks executives. European facilities remain dependent on Asian wafer fabs, a vulnerability highlighted in the Commission’s raw-materials foresight review. Lenovo’s Hungarian line eases regional tariffs but cannot fully offset shortages. Deferred deployments translate into lost quarters for switch revenue, trimming momentum during the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware platforms anchor bandwidth upgrades

Ethernet switches commanded 34.78% Europe data center networking market share in 2025, underscoring their role in leaf-spine fabrics that feed GPU clusters. Software-defined networking controllers, expanding at 11.76% CAGR, orchestrate diverse ASIC generations and automate failover, a necessity as average cluster sizes surpass 10,000 servers. Routers retain relevance for WAN ingress but cede internal roles to converged switches that flatten layers and squeeze latency. Storage networking, though growing slower, gains interest from financial services adopting immutable backup vaults to satisfy operational resilience rules. Application delivery controllers become indispensable at the edge, handling TLS offload near user eyeballs. Security appliances increasingly embed in switching OS images to comply with EU Digital Operational Resilience Act rules. Optical interconnects evolve fastest; co-packaged optics and linear pluggable optics battle for sockets as operators weigh cost, power and upgrade ease. Services hold a stabilizing influence as managed network contracts let enterprises offset the expertise gap that complexity creates.

A second-wave replacement super-cycle is forming around liquid-cool ready gear. Vendors pairing cold-plate chassis with direct-to-chip loops appeal to colocation landlords who must publish PUE scores. Merchant silicon levels hardware performance, shifting differentiation toward NOS features such as real-time fabric telemetry. Open networking distributions like SONiC persuade buyers that they can swap vendors without forklift rewires, making software support and lifecycle stewardship the new trust metric. This pivot realigns profit pools toward licenses and subscription telemetry rather than physical ports, yet packet-processing ASIC innovation remains critical for line-rate encryption and AI cluster congestion control.

By End-User: Financial institutions accelerate latency-sensitive builds

IT and telecommunications firms delivered 36.05% of 2025 revenue, leveraging rich peering and backbone assets to monetise hybrid cloud and 5G. Banks and insurers post the fastest 12.65% CAGR as instant-payment rules and model-driven risk scoring force ultra-low latency links between vaults and analytics engines. Government and defence entities adopt sovereign cloud frameworks such as Germany’s Deutsche Verwaltungscloud, prioritising data residency and zero-trust segmentation. Media and entertainment houses expand private CDNs, shifting transcoding to edge racks to curb backbone congestion during live sports streams. Healthcare networks participate in shared AI models for radiology, fuelling demand for encrypted east-west traffic inspection. Manufacturing deploys deterministic Ethernet for robotic cells and predictive maintenance, pushing OT and IT domain convergence. Education, retail and logistics round out remaining spend, upgrading campus cores to 100 GbE as digital curricula and omnichannel fulfilment mature.

EU regulatory pressure for operational resilience anchors capital outlays. The Digital Operational Resilience Act compels even mid-tier financial entities to test failover quarterly, driving redundant mesh deployments. Telecommunication operators reroute traffic toward multi-access edge units to offload RAN congestion, embedding workload-aware routing into core switches. Overall, vertical diversity cushions cyclical swings in the Europe data center networking market while BFSI share grows.

By Data-Center Type: Neutral facilities still dominate interconnection

Colocation sites held 51.72% Europe data center networking market size in 2025 as enterprises seek carrier-neutral meet-me rooms for multi-cloud interconnection. Hyperscaler cloud providers, however, show the highest 14.05% CAGR triggered by AI training farms that demand 800 GbE fabrics. Edge and micro data centers multiply at tower sites and metro POPs, mirroring telco timelines for 5G standalone. Enterprises continue to vacate legacy on-prem computer rooms, migrating workloads into shared halls to meet Scope 3 carbon accounting goals. The colocation segment invests in on-site renewables, district heat export and battery storage to answer EU disclosure rules. Hyperscalers deploy proprietary topologies that integrate optical circuit switching for elephant flows, reducing spine layers and wiring cost. Edge operators prioritise rugged hardware with zero-touch provisioning to cut truck rolls to rural sites. Together, these archetypes ensure sustained channel diversity and cushion demand fluctuations.

Industry consolidation intensifies: Penta Infra absorbed KPN’s Amsterdam asset, and nLighten snapped up seven edge facilities from Exa Infrastructure. Such roll-ups give providers larger footprints to secure multi-megawatt leases from AI tenants. Landlords integrate liquid-immersion pods and wasted-heat capture to win zoning approvals, reshaping design guides for rack-level networking gear. Hyperscalers adopt Build-Operate-Transfer models in emerging metros to hedge against licensing risk while still controlling network design DNA. The Europe data center networking market therefore tracks not just capacity growth but ownership churn.

By Bandwidth: High-speed optics underpin AI clusters

In 2025, 50-100 GbE links accounted for 37.74% spend, satisfying mainstream enterprise storage and VM migration. Deployments above 100 GbE post the steepest 12.74% CAGR, underpinned by GPU cluster rollout that benefits from 400 GbE and 800 GbE leaf-spine fabrics. The ≤10 GbE tier remains for management networks and small regional edge nodes where cost outranks bandwidth. 25-40 GbE continues as a bridging option for mid-cycle refresh projects. Operators future-proof cabling by installing MPO-16 trunks ready for 1.6 T lanes, limiting stranded fibre when speeds double. Coherent pluggables extend Ethernet directly over metro fibre, bypassing proprietary DWDM shelves and cutting capex. As green tariffs rise, optics suppliers push lower-power DSPs and linear drivers, stepping toward energy budgets compatible with EU net-zero targets.

Wide adoption of host-based congestion controls improves link utilisation, enabling operators to increase oversubscription without hurting GPU training times. Vendors promote telemetry-anchored traffic engineering, analysing per-flow micro-bursts and shaping queues in real time. These capabilities encourage enterprises that skipped 100 GbE to leapfrog straight to 400 GbE, deepening refresh demand across the Europe data center networking market.

Geography Analysis

Europe data center networking market revenue concentrates in the FLAP-D corridor, yet grid constraints in London and Frankfurt curtail new megawatt allocations, steering investors toward secondary metros. Frankfurt sits at 745 MW installed IT capacity but faces connection moratoriums until sub-stations come online, slowing near-term switch demand. London still leads at 993 MW, though high power tariffs incentivise operators to earmark incremental AI clusters for northern England sites where renewable PPAs are available. Amsterdam, with 506 MW, imposes floor-space caps, driving multi-storey vertical builds that require higher port densities. Dublin remains a hyperscale stronghold, but electricity regulator CRU limits future allocations, pressing cloud providers to co-invest in grid upgrades.

Secondary markets show double-digit expansion as a result. Madrid leverages surplus solar production and benign permitting to invite 100-MW campuses, generating sizeable orders for 400 GbE fabrics. Berlin and Warsaw benefit from east-west fibre backbones, positioning themselves as disaster-recovery nodes for FLAP tenants. Milan’s growth stems from undersea cable landings from Africa and the Middle East, turning the city into a latency bridge to EMEA south. Nordic facilities target AI inference and batch analytics thanks to cool climates, with Denmark and Sweden offering tax incentives that cut total cost of ownership. EU investment vehicles amplify geographic spread. The Digital Europe Program allocated EUR 1.3 billion to AI and cybersecurity in 2025, earmarking grants for edge nodes that will number 10,000 by 2030. Renewable-heavy grids in Finland and Norway support green branding claims, appealing to corporate ESG scorecards. Eastern European governments deploy investment subsidies to build sovereign cloud zones, ensuring data stays within borders and boosting local switch procurement. Aggregate demand therefore follows a hub-and-edge pattern: mature metros consume replacement gear, while emerging locales absorb greenfield shipments, together underpinning a resilient trajectory for the Europe data center networking market.

The data center networking market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America, South America, and Middle East. This is complemented by country-specific insights for Spain, Italy, Germany, Norway, Netherlands, and Poland, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Competition balances scale and specialisation. Cisco retains the broadest portfolio, spanning leaf-spine switches, WAN routers and zero-trust appliances, but faces margin compression as merchant silicon erodes ASIC differentiation. Arista Networks recorded USD 2.005 billion Q1 2025 revenue, a 27.6% jump fuelled by 800 GbE shipments into European AI buildouts, cementing its challenger status. Hewlett Packard Enterprise’s pending USD 14 billion acquisition of Juniper Networks aims to blend compute, storage and network orchestration into a single stack, though U.S. regulators continue their review.

White-box penetration rises as hyperscalers value software control over branded metal. SONiC distributions let operators mix ODM chassis with self-developed tooling, reducing vendor lock-in and spurring price competition. PLVision contributes hardened SONiC images for Europe’s temperate-edge deployments, illustrating a market tilt toward services value. Legacy router incumbents respond by embedding streaming telemetry and AI-assisted troubleshooting into NOS packages, seeking subscription revenue.

Liquid-cool engineering becomes a key differentiator. Vendors integrate dielectric coolant loops to maintain ASIC temperatures under 65 °C while slashing fan energy. Firms first to certify liquid-ready gear under EU eco-design directives gain early-mover bids. Meanwhile, optical module makers accelerate linear pluggable optics roadmaps, allowing 800 GbE adoption without costly DSPs. The interplay of consolidation, open software and sustainability requirements shapes a moderately concentrated structure that still leaves room for nimble entrants targeting niche functions in the Europe data center networking market.

Europe Data Center Networking Industry Leaders

Cisco Systems, Inc.

Arista Networks, Inc.

Huawei Technologies Co., Ltd.

Juniper Networks, Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Brookfield Asset Management confirmed a EUR 20 billion allocation for French data centers, directing EUR 15 billion into builds via its Data4 unit

- February 2025: Arista Networks posted USD 2.005 billion Q1 revenue, up 27.6% year on year, citing strong European AI switch demand

- January 2025: The European Commission cleared Hewlett-Packard Enterprise’s planned Juniper Networks acquisition, concluding no competition concerns in the WLAN and switching segments

- January 2025: Germany launched Deutsche Verwaltungscloud, its first sovereign government cloud offering secure services for federal agencies

- July 2024: CyrusOne broke ground on the EUR 1 billion FRA7 Frankfurt facility, integrating a 40 MW waste-heat system

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe data-center networking market as the annual revenue earned within the region from Ethernet switches, core and leaf routers, optical interconnects, network-security appliances, SDN controllers, and related support services that are physically deployed in colocation, hyperscale, edge, or enterprise data centers. According to Mordor Intelligence, this flow reached USD 7.78 billion in 2025, reflecting factory-gate hardware sales plus recurring maintenance booked in the same year.

Scope Exclusions: The valuation leaves out campus LAN equipment, structured-cabling labor, and carrier connectivity fees paid by tenants.

Segmentation Overview

- By Component

- Products

- Ethernet Switches

- Routers

- Storage Area Network (SAN)

- Application Delivery Controllers (ADC)

- Network Security Appliances

- Software-Defined Networking (SDN) Controllers

- Optical Interconnects

- Services

- Installation and Integration

- Training and Consulting

- Support and Maintenance

- Managed Network Services

- Products

- By End-User

- IT and Telecommunications

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Other End-Users

- By Data-Center Type

- Colocation

- Hyperscalers/Cloud Service Providers

- Edge/Micro Data Centers

- By Bandwidth

- Less Than or equals to 10 GbE

- 25–40 GbE

- 50–100 GbE

- Greater than 100 GbE

- By Country

- United Kingdom

- Germany

- France

- Netherlands

- Ireland

- Spain

- Italy

- Sweden

- Denmark

- Norway

- Poland

- Austria

- Belgium

- Switzerland

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed network-silicon engineers, facility architects in Frankfurt, London, and Madrid, and procurement heads at hyperscale operators. Short surveys with colocation managers and distributors clarified discount ladders, rack-level port densities, and lead-time shifts that documents rarely disclose.

Desk Research

We began with publicly available sources such as Eurostat ICT statistics, the European Data Centre Association capacity registry, ENISA threat-landscape updates, Ofcom infrastructure reviews, and customs trade records that reveal import surges around product launches. Company 10-Ks, investor decks, patent families from Questel, and news streams filtered through Dow Jones Factiva supplied shipment clues, ASP trends, and roadmap timings. Together, these signals showed how 100 GbE ports ceded share to 400 GbE and 800 GbE in 2024-2025. The sources mentioned are illustrative only; many additional open and paid references underpin our dataset.

Market-Sizing & Forecasting

The model starts with a top-down rebuild of installed megawatt capacity and typical port density, multiplies this pool by refresh cycles, and is cross-checked with selective bottom-up vendor revenue splits and sampled ASP × volume disclosures. Key variables like annual MW additions, share of >100 GbE ports, silicon cost curves, average PUE caps, and EU efficiency milestones feed a multivariate regression that projects demand to 2030. When bottom-up checks diverge by more than three percentage points, we adjust using the weighted consensus from expert calls.

Data Validation & Update Cycle

Outputs pass anomaly screens, variance reviews, and senior-analyst sign-off. Reports refresh every twelve months, with interim updates triggered by events such as major 400 GbE price resets or new regulatory mandates, ensuring clients receive the latest view.

Why Mordor's Europe Data Center Networking Baseline Commands Reliability

Published estimates vary because firms mix product scopes, apply differing ASP progressions, or convert currencies on outdated rates.

By anchoring results to clearly enumerated hardware classes, quarterly Euro inputs, and a disciplined refresh cadence, we give decision-makers a reproducible baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.78 B (2025) | Mordor Intelligence | |

| USD 7.33 B (2024) | Regional Consultancy A | Omits support services; books figures on shipment year, not revenue recognition |

| USD 9.17 B (2025) | Global Consultancy B | Folds campus LAN sales into scope and inflates ASPs aggressively |

| USD 9.37 B (2025 est.) | Industry Journal C | Derives Europe as fixed share of global total without local primary validation |

The comparison shows that our disciplined scope selection, dual-path validation, and annual updates deliver a balanced, transparent baseline that clients can trust for planning and investment.

Key Questions Answered in the Report

What is the projected value of the Europe data center networking market by 2031?

The market is forecast to reach USD 11.58 billion by 2031, supported by a 6.85% CAGR driven by AI infrastructure expansion and edge computing deployments.

Which component category currently leads spending?

Ethernet switches lead with 34.78% 2025 revenue share, reflecting their central role in spine-leaf and AI cluster networks.

Why is Spain the fastest-growing national market?

Spain benefits from cloud-first government policy, abundant renewable energy and strategic subsea cable routes, producing a 10.18% CAGR outlook to 2031.

What bandwidth tier is expanding most quickly?

Links above 100 GbE, particularly 400 GbE and 800 GbE, show the highest 12.74% CAGR as hyperscalers upgrade AI fabrics.

How will the HPE–Juniper merger affect competitive dynamics?

If completed, the merger would combine compute, storage and network portfolios, creating a stronger challenger to Cisco while potentially reshaping partner ecosystems across Europe.

Page last updated on: