Europe Financial Advisory Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

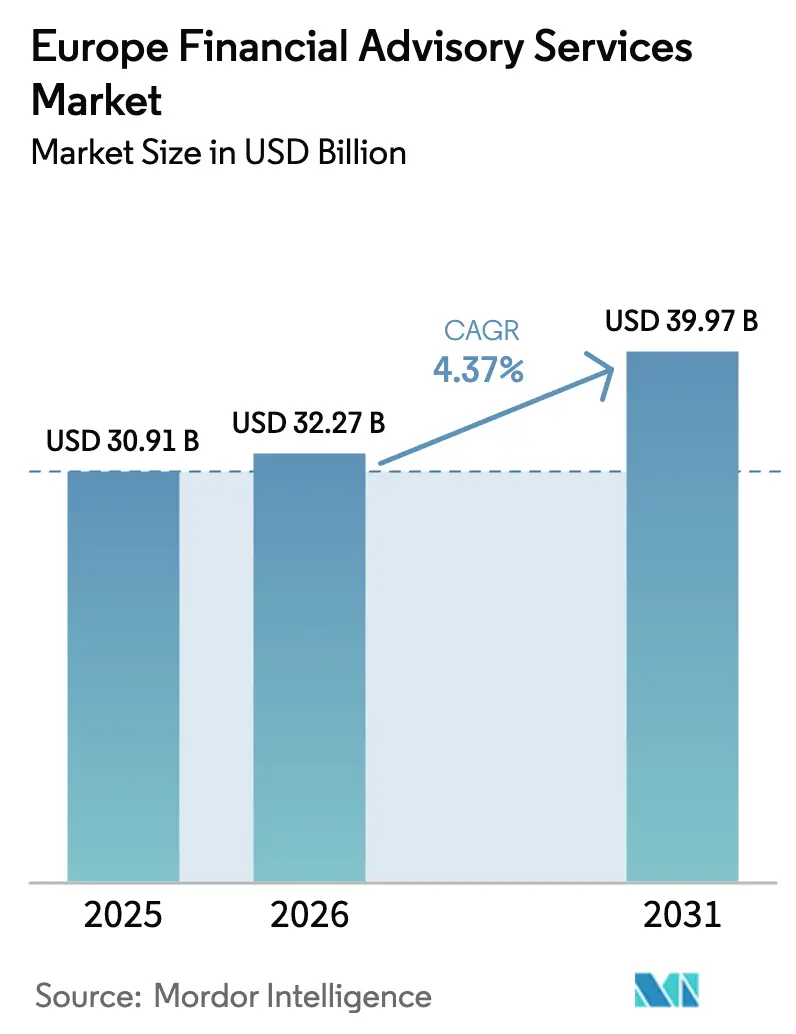

| Base Year Market Size (2025) | USD 30.91 Billion |

| Market Size (2026) | USD 32.27 Billion |

| Market Size (2031) | USD 39.97 Billion |

| Growth Rate (2026 - 2031) | 4.37% CAGR |

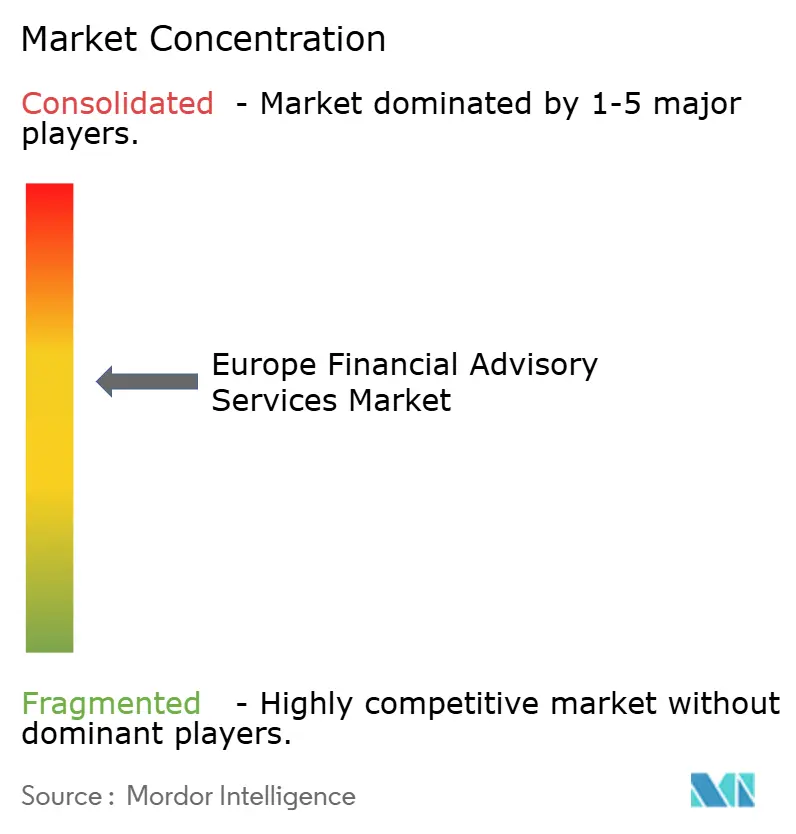

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Financial Advisory Services Market Analysis by Mordor Intelligence

The Europe Financial Advisory Services Market size was valued at USD 30.91 billion in 2025 and is estimated to grow from USD 32.27 billion in 2026 to reach USD 39.97 billion by 2031, at a CAGR of 4.37% during the forecast period (2026-2031).

Momentum stems from regulatory expansion that sustains premium tax and compliance mandates, while the MiCA regime and DAC frameworks create new advisory niches in digital assets and cross-border reporting. Demand is also shaped by corporate deal activity and private capital flows that elevate transaction, valuation, and restructuring needs. Advisory delivery is modernizing as clients adopt hybrid and digital touchpoints, with wealth and corporate finance clients expecting real-time analytics and seamless collaboration alongside expert input. Within this landscape, the Europe Financial Advisory Services Market continues to reward firms that blend technical depth with scalable platforms and that turn regulatory burden into structured, tech-enabled service lines.

Key Report Takeaways

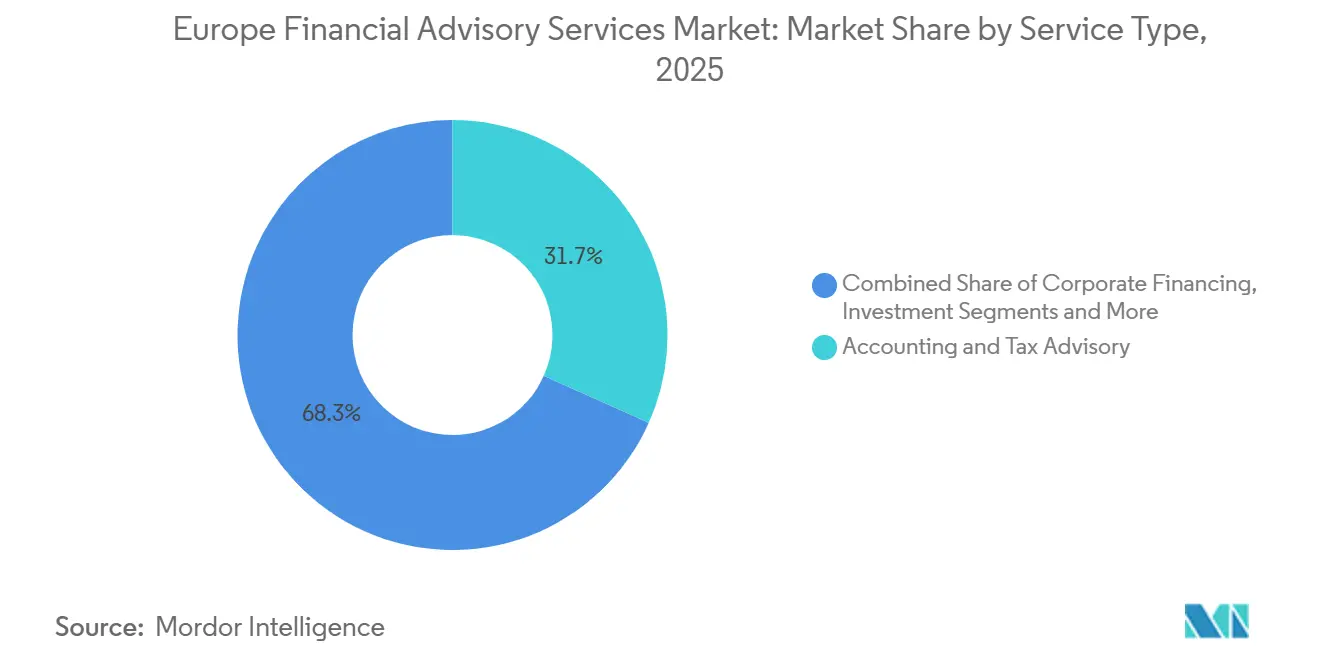

- By service type, Accounting and Tax Advisory led with a 31.75% share in 2025, while Investment services are projected to expand at a 6.34% CAGR through 2031.

- By organization size, Large enterprises held 57.07% of revenues in 2025, while SMEs are projected to grow at a 5.82% CAGR to 2031.

- By industry vertical, BFSI accounted for 32.48% of revenues in 2025, while Retail and e-commerce are projected to grow at a 6.12% CAGR through 2031.

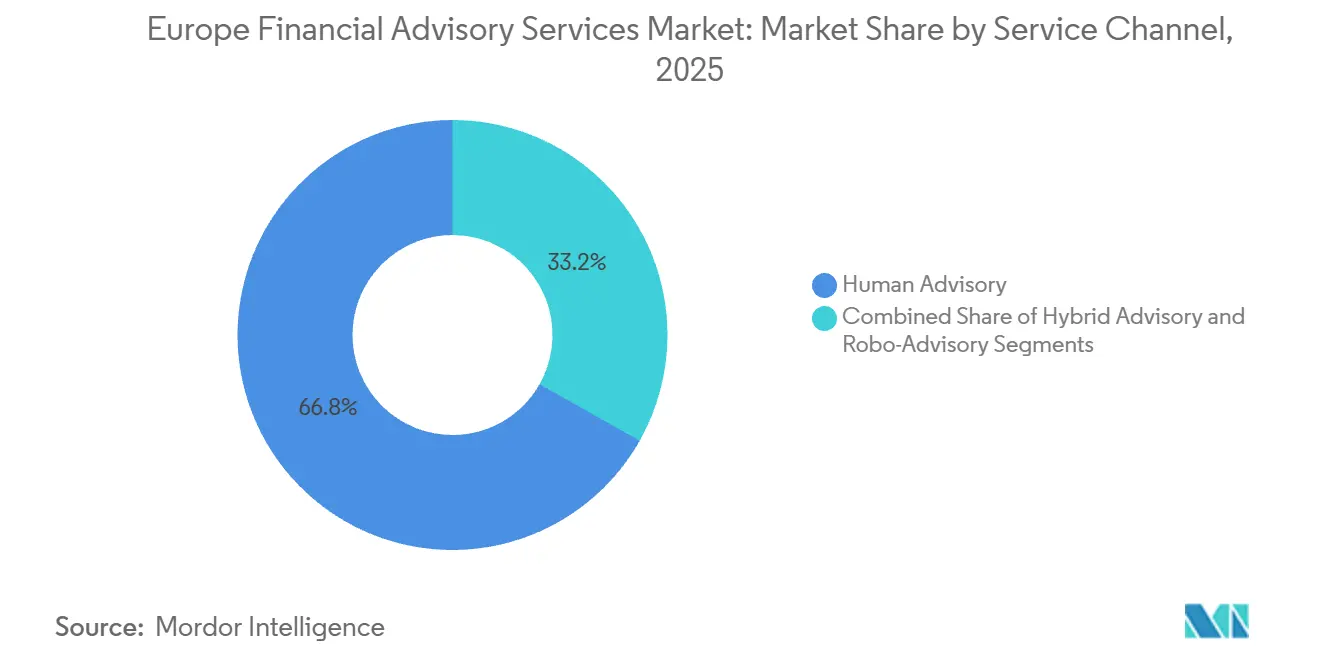

- By service channel, Human Advisory represented 66.81% of revenues in 2025, while Robo Advisory is projected to expand at a 12.67% CAGR to 2031.

- By delivery mode, On-site consulting held a 63.22% share in 2025, while Remote and Virtual delivery is projected to grow at a 10.41% CAGR through 2031.

- By geography, the United Kingdom led with a 21.53% revenue share in 2025, while the Rest of Europe is projected to be the fastest-growing region at a 6.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global financial advisory services market data by Mordor Intelligence represents that combined structure.

Europe Financial Advisory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory complexity is driving specialist tax advisory demand | +1.2% | Europe-wide, acute in Germany, France, the Nordics | Long term (≥ 4 years) |

| Rising M&A activity is accelerating corporate finance advisory spend | +0.8% | Global, concentrated in the United Kingdom, the Netherlands, and Germany | Medium term (2-4 years) |

| SME sector expansion is boosting demand for integrated planning | +0.4% | Europe-wide, strongest in Germany, France, Central & Eastern Europe | Medium term (2-4 years) |

| ESG‑reporting mandates are catalyzing sustainability advisory | +0.5% | Europe-wide, CSRD Phase 1 will be enforced from January 2025 | Short term (≤ 2 years) |

| Digital‑asset adoption is creating new compliance niches | +0.3% | Europe-wide, MiCA enforcement from Dec 2024, DAC8 from Jan 2026 | Short term (≤ 2 years) |

| Cross-border family‑office migration fuelling wealth advisory | +0.4% | Global, concentrated in the United Kingdom, Switzerland, UAE as a destination | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Regulatory Complexity Driving Specialist Tax Advisory Demand

Regulatory scope in Europe keeps widening, creating steady demand for specialist tax, reporting, and governance advisory services across multinational groups and cross-border structures in the Europe Financial Advisory Services Market. The MiCA framework introduces a harmonized regime for crypto asset service providers that lifts requirements for authorization, conduct, and disclosure, which has opened new compliance niches around policy design, control implementation, and supervisory engagement. DAC updates and Pillar Two obligations are increasing filing, data exchange, and intra-group coordination needs, reinforcing the case for centralized workbench solutions for tax and finance leaders. MiFID II adjustments that raise transparency expectations and United Kingdom regulatory divergence post Brexit are adding to governance design and cross-market mapping tasks for advisory teams that operate across borders. CSRD and DORA extend the lens to sustainability disclosures and operational resilience, increasing the breadth of policy, process, and controls work that many corporates must address in parallel across the Europe Financial Advisory Services Market.[1]Salesforce, “The Corporate Sustainability Reporting Directive (CSRD): A Guide for Companies,” Salesforce, salesforce.com The cumulative effect is a multi-year pipeline of regulatory change that favors firms with multi-disciplinary tax, legal, and technology capabilities that can be deployed consistently across several Europe jurisdictions.

Rising M&A Activity Accelerating Corporate Finance Advisory Spend

Deal momentum and larger average transaction sizes have strengthened demand for corporate finance, valuation, diligence, and restructuring advice across the Europe Financial Advisory Services Market. European dealmakers outpaced regional benchmarks in 2025, with activity supported by strategic repositioning, portfolio concentration, and cross-border buyer interest in quality assets. Big-ticket deals drove the market, with European dealmakers outperforming their regional index by +4.7 percentage points in 2025, a significant rise from +0.7 percentage points in 2024, though deal volume remained stable at 153 completions versus 155 in 2024. European M&A value reached USD 746 billion through December 1, 2025, twelve percent higher than the total for all of 2024, with deal value surging 23% in H2 versus H1 and the average Q4 deal more than twice Q1's size. Global dealmaking updates point to a shift from resilience to redefinition, with buyers focusing on technology, energy transition, and infrastructure themes where advisory support is essential for underwriting and value creation planning. Private capital continues to fund platform roll-ups and corporate carve-outs, sustaining mid-market transaction pipelines where advisory teams often provide end-to-end support on sell and buy-side mandates. Post-closing value creation agendas increasingly depend on operating model change and digital integration, deepening advisory involvement beyond execution to transformation phases in the Europe Financial Advisory Services Market. The net effect is a multi-year uplift in corporate finance advisory hours, particularly in the United Kingdom, the Netherlands, and Germany, where cross-border deal flows and financing depth support larger transactions[2]A&O Shearman, “Transactional activity in Europe gains momentum heading into 2026,” A&O Shearman, aoshearman.com.

ESG Reporting Mandates Catalysing Sustainability Advisory

The Corporate Sustainability Reporting Directive mandates adoption of European Sustainability Reporting Standards and requires sustainability statements in annual management reports aligned with double-materiality principles, reporting on both financial risks/opportunities and the company's impacts on environment/society, with Phase 1 entities (large Public-Interest Entities already subject to NFRD) reporting from 2025, Phase 2 (other large companies meeting at least two of: over 250 employees, over USD 41.66 million (EUR 40 million) net turnover, or over USD 20.83 million (EUR 20 million total assets) from 2026, and Phase 3 (listed SMEs) from 2027. Many companies are preparing for heightened assurance over time, which favors external support for documentation, governance, and remediation roadmaps that align with financial and sustainability reporting. Advisory teams are also translating climate, supply chain, and stakeholder-centric requirements into practical disclosure programs that integrate with enterprise planning and risk processes. The European Commission proposed amendments in early 2025 to simplify reporting and postpone application dates, with scope reduction focusing on large undertakings exceeding 1,000 employees and USD 468.70 million (EUR 450 million) in net turnover, aiming to exempt approximately 80 percent of companies initially in scope, yet the Omnibus simplification package extends deadlines only by one to two years[3]Arbor. Amar, “What is the EU CSRD? The Ultimate Guide 2025 for Carbon Accounting,” Arbor. Amar, www.arbor.eco. As boards and lenders emphasize data quality and comparability, firms able to combine reporting expertise with technology configurability are well positioned to capture growth in the Europe Financial Advisory Services Market.

SME Sector Expansion Boosting Demand for Integrated Planning

Europe's 26.1 million SMEs show resilience despite headwinds, with SME real value added declining slightly in 2024 (-0.2%) but a rebound of 1.6 percent projected for 2025, driven by micro-SMEs, as German SME lending facilities surpassed USD 44.78 billion (EUR 43 billion) in the first half of 2025 alone, with savings banks supporting transformation financing and advisory services to help companies navigate regulatory complexity and leverage sustainability as a strategic advantage. At the European level, proposals to streamline company formation, e-invoicing, and cross-border procedures promise to reduce administrative burden, which helps amplify demand for templated diagnostics and fixed price advisory bundles[4]Accountancy Europe, “SME update,” Accountancy Europe, accountancyeurope.eu. A new Small mid-cap category and other simplification measures under discussion are intended to improve access to finance and listing conditions, which would expand the pool of advisory clients that seek capital markets readiness and governance upgrades. As these measures take hold, SMEs are turning to external partners to align compliance, tax, and planning across borders, which strengthens the role of scaled, tech-enabled advisory models in the Europe Financial Advisory Services Market. The overall effect is a durable mid-market growth engine that complements large enterprise spending and supports healthy diversification of revenue mix for advisory firms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee pressure from commoditised & automated tools | -0.9% | Europe-wide, most acute in the United Kingdom, Nordics | Short term (≤ 2 years) |

| Acute shortage of senior certified advisers | -0.7% | Europe-wide, particularly Germany, France, Nordics | Long term (≥ 4 years) |

| Escalating cyber‑security risk curbing digital uptake | -0.4% | Global, heightened in financial hubs | Medium term (2-4 years) |

| Consolidation among audit‑advisory giants limits mid-tier competition | -0.3% | Global, strongest in the United Kingdom, the Netherlands, and Belgium | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fee Pressure From Commoditised & Automated Tools

Automation raises client expectations for speed and price certainty, which compresses fee rates in standardized work and forces advisers to sharpen specialization in the Europe Financial Advisory Services Market. Wealth managers identify technology disruption and AI as leading themes, and clients increasingly expect live dashboards, scenario tools, and instant insights within standard engagements. As DIY analytics spreads, entry-level tasks lose pricing power, making value articulation and outcome-based pricing critical to maintain margins. Mid-tier firms face the strongest pressure where scale investments in platforms are needed, but resources are tighter, which accelerates partnerships and selective outsourcing. Providers that combine human expertise with explainable AI and audit trails are better placed to defend fees and move conversations to business outcomes in the Europe Financial Advisory Services Market.

Acute Shortage of Senior Certified Advisers

Talent scarcity at senior levels limits delivery capacity in complex mandates and raises wage pressures across compliance and advisory specialties in the Europe Financial Advisory Services Market. Professional bodies highlight continued work to improve the attractiveness of the profession and expand the pipeline, as firms compete for scarce skills in tax, assurance, and digital domains. The scarcity is most visible in specialist areas like ESG reporting and crypto policy implementation, where regulatory timelines require experienced practitioners. Firms respond with targeted upskilling, cross-border mobility, and selective outsourcing to protect delivery schedules and service quality. These talent dynamics reinforce the advantage of platforms that codify knowledge, standardize delivery, and amplify senior time with technology across the Europe Financial Advisory Services Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Investment Advisory Surges Amid Digital-Asset Demand

Accounting and Tax Advisory led service-type revenues with 31.75% in 2025 as complex cross-border tax rules and DAC9 preparations concentrated demand for Pillar Two filings and data-sharing controls. Investment services are the fastest-growing category at a 6.34% CAGR from 2026 to 2031 as digital-asset advisory scales under MiCA authorization and conduct rules for crypto-asset service providers, while DAC8 broadens reporting for crypto and e-money transactions from January 2026. Corporate finance advisory benefits from revived deal flow and larger transaction sizes, strengthening demand for buy-side and sell-side financial, tax, and commercial diligence, along with valuation and carve-out support. Other services that include risk management and compliance also expand as sector-specific rules increase the need for operating model design, data governance, and monitoring programs across regulated industries. The Europe financial advisory services market benefits from combined regulatory and transactional catalysts that pull specialized tax, audit-adjacent assurance, and sustainability expertise into integrated client programs, which encourages firms to build multidisciplinary teams and shared data platforms.

Client priorities shift toward evidence-based advisory and managed services as reporting obligations scale, which positions firms to move beyond projects to recurring, platform-enabled engagements. The Europe financial advisory services market increasingly connects investment and tax advisory with ESG reporting and assurance readiness as CSRD requirements drive a EUR-denominated spend cycle on materiality, data, and audit workflows. Firms integrate AI into portfolio analytics, tax documentation, and control testing to improve accuracy and cycle times while maintaining audit trails that align with regulatory expectations. This integration reduces low-value labor while elevating client expectations of real-time insights, so providers differentiate on experience design, transparency, and industry specialization. Coordination between service lines is central to winning multi-year mandates, which reinforces the pivot from isolated projects to solution suites and co-sourced operating models.

By Organization Size: SMEs Expand Faster on Digital-Maturity Funding

Large Enterprises held a 57.07% revenue share in 2025 as multi-jurisdiction footprints, internal controls, and transformation budgets sustained demand for audit-adjacent, tax, and strategy advisory at scale. SMEs expand faster at a 5.82% CAGR as grants and toolkits lower adoption barriers for digital finance and compliance, which supports fixed-price diagnostics and standardized implementations that package planning, reporting, and ESG. Germany’s SME lending facilities exceeded USD 44.78 billion (EUR 43 billion) in H1 2025, with savings banks supporting transformation financing and advisory, a trend that increases demand for working capital analytics and investment planning. Brussels moved to a 28th-regime framework to accelerate company establishment and embed e-invoicing that automates VAT and selected reporting, which reduces friction in cross-border operations. The Europe financial advisory services market serves SMEs with modular solutions and hybrid delivery models that compress project cycles and spread costs, while larger firms prioritize governance, multi-country coordination, and integrated data architectures.

SME ambitions are increasingly international as firms shift focus to European and Asian markets, which raises demand for cross-border tax, trade, and financing advisory services. New proposals for a Small Mid-cap category extend simplified listing and reduced prospectus obligations to eligible firms, and data protection relief for low-risk processing reduces overhead for compliance. Hybrid staffing models combine on-site work for critical workshops and remote collaboration for analysis and reporting, which increases utilization and lowers travel costs while maintaining client engagement. Large enterprise programs emphasize Pillar Two compliance, CSRD assurance, and complex diligence on cross-border deals, which often require large multi-disciplinary teams and integrated PMOs. Across both segments, providers align talent and tools to address cost pressure while preserving advisory quality, with nearshore teaming and standardized accelerators improving throughput and consistency.

By Industry Vertical: BFSI Leads as Retail & E-Commerce Accelerates

Banking, Financial Services, and Insurance captured a 32.48% revenue share in 2025 as capital rules, risk governance needs, and digital banking competition sustained consulting budgets across finance, risk, and technology. Retail and E-Commerce is the fastest-growing vertical with a 6.12% CAGR from 2026 to 2031, driven by omnichannel integration, analytics-enabled customer journeys, and strategic buyer interest that supports portfolio rebalancing. Technology, media, and telecom remain high-volume transaction sectors as organizations invest in AI and data platforms for improved decision-making, which increases advisory demand for diligence and value creation planning. Manufacturing and industrials see stable demand as defense investment strengthens and as supply chain and energy strategies become central to capital allocation and deal rationale. Public sector modernization programs focus on digital services and infrastructure, which expand opportunities in funding advisory, program controls, and performance management across Europe initiatives.

Healthcare and pharmaceuticals sustain activity due to aging demographics and digital care models, drawing private capital to technology-enabled platforms and clinical service niches. Real estate advisory demand recovers as pricing expectations reset and as institutional investors re-enter logistics and student housing, which requires data-led underwriting and financing support. Defense and aerospace attract fresh investor attention under higher security budgets, while professional services consolidators pursue scale plays to expand client coverage and software integration capability. Across verticals, privacy and conduct rules such as MiFID II and GDPR anchor standardized processes for onboarding, client reporting, and vendor oversight, which raises the bar for cross-border workflow design. The Europe financial advisory industry aligns service mix by sector to address regulatory expectations, strategic transformation, and investor requirements while enabling clients to fund growth and reduce operational risk.

By Service Channel: Robo-Advisory Expands at 12.67% as Hybrid Gains Share.

Human Advisory holds a 66.81% channel share in 2025, yet Robo-Advisory advances at a 12.67% CAGR through 2031 as automation reduces unit cost and scales planning for simpler needs. Hybrid advisory gains traction among SMEs and affluent clients that want digital convenience with expert access, which improves cost efficiency while meeting rising expectations for personalization and speed. Wealth managers cite technology and AI innovation as a top theme and are increasing the adoption of real-time dashboards, scenario simulators, and AI-powered insights to improve client outcomes and internal productivity. Private banks and advisers prioritize converting advisory capability into fee-generating digital products with explainable personalization, audit trails, and human-in-the-loop workflows to satisfy regulatory and fiduciary expectations. The Europe financial advisory services market uses a hybrid design to navigate fee pressure, capacity constraints, and client demands for instant insight, with human advisers focusing on complex, cross-border, and multi-generational planning that cannot be automated.

AI adoption helps firms increase throughput without equal headcount growth, which supports scale in SME segments that demand value pricing and quick turnarounds. Adoption patterns in the United Kingdom and across Europe indicate a steady increase in AI-enabled tools for forecasting, reporting, and investment insights as part of hybrid interactions. Clients expect seamless, borderless service because high-net-worth families are globally mobile and often need coordinated advice across tax, investments, and estate planning. The Europe financial advisory services market is seeing human-centric engagement remain essential for complex cases while automated tools support ongoing monitoring, simulation, and periodic rebalancing decisions. Providers that balance automation with expert oversight can improve experience and trust while preserving margins for higher-value work.

By Delivery Mode: Remote/Virtual Accelerates at 10.41% as Hybrid Models Dominate

On-site Consulting retains a 63.22% delivery share in 2025 as high-stakes workshops, stakeholder alignment, and regulatory reviews still benefit from presence. Remote or Virtual delivery grows at a 10.41% CAGR through 2031 as standardized toolkits, collaboration platforms, and secure data rooms improve utilization and collaboration while cutting travel costs. Hybrid models blend on-site immersion for critical gates with remote execution for analysis and reporting, which improves throughput and client satisfaction on multi-country programs. Remote-only projects rise for technology advisory and analytics, supported by stronger data sharing and standardized evidence libraries that fit audit and supervisory expectations. The Europe financial advisory services market incorporates platform investments to streamline delivery and strengthen quality assurance across distributed teams and cross-border engagements.

Financial services clients favor vendors that offer unified platforms for planning, risk, and reporting to avoid the complexity of multiple systems and improve governance. Banks and wealth managers emphasize safe and quick embedding of AI and automation into front-line processes for productivity gains and better engagement. Advisory firms expand virtual CFO services and finance and accounting outsourcing partnerships as clients seek flexible cost models and access to specialized skills. Nearshore teaming in similar time zones supports collaboration and cycle times for finance operations and audit support, which can outperform traditional offshore models for certain activities. Providers refine talent models and delivery playbooks to meet rising client expectations on speed, transparency, and outcomes while maintaining the documentation standards regulators require.

Geography Analysis

The United Kingdom leads country-level revenues with a 21.53% share in 2025 as it remained the largest M&A market by value in late 2025 and supports deep advisory activity across financial services, technology, and life sciences. The Europe financial advisory services market benefits in the United Kingdom from strong financing networks, international deal participation, and continued buyer interest that is supported by currency dynamics and strategic portfolio repositioning. The rest of Europe is the fastest-growing geography at a 6.79% CAGR to 2031, with the Netherlands expected to reach 30% of non-PIE audit firms under PE ownership by end-2025 and increased M&A value supported by accelerated timetables and public takeovers. Germany’s advisory demand is supported by a rebound in deal value into Q4 2025 and by structural investments that support industrial transformation, which is reflected in cross-border interest and sustained diligence and restructuring activity. France is positioned for faster consulting growth through 2031 with a significant digital transformation budget and a programmatic push into AI-enabled planning and advisory tools.

Benelux ranks high for expected deal growth as Belgium recorded a value rise through 2025 and Luxembourg continues to refine its tax environment while adopting targeted reforms, which support corporate finance, tax structuring, and cross-border wealth planning mandates. Spain advanced into a top FDI destination in Europe with stronger deal value, which opens mandates for strategic planning, capital raising, and integration. Italy’s ongoing bank consolidation and select large transactions highlight the need for balance sheet advisory and risk-based diligence that addresses regulatory thresholds. The Nordics combine deep innovation ecosystems with a sustainability focus and serve as hubs for technology and sustainability advisory, while cross-border work increases due to shared standards and multi-market expansion strategies. The Europe financial advisory services market aligns coverage and capabilities to local regulatory nuances while integrating delivery across regional hubs to serve pan-European programs efficiently.

The United Kingdom market maintains a strong pipeline as strategic buyers and private capital pursue high-quality assets and larger deal sizes while select sectors consolidate for scale and capability. The Netherlands illustrates how private equity reshapes professional services ownership, which accelerates investment in digital tools and managed service platforms at mid-market firms. Germany’s market signals steady recovery into 2026 as clients pursue portfolio realignments and succession planning in the SME segment, which lifts advisory demand in tax, finance, and restructuring. France’s momentum in digital programs and AI helps sustain advisory demand in data, controls, and reporting as CSRD and Pillar Two workstreams increase. Across geographies, providers grow through a mix of organic investments and selective acquisitions to deepen specialization and extend cross-border reach.

The financial advisory services market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America.

Competitive Landscape

Market structure is evolving as private equity investment reshapes ownership, funds platform upgrades, and accelerates consolidation across mid-sized advisory firms in the Europe Financial Advisory Services Market. The Netherlands shows a notable rise in PE-backed non-PIE audit firms, and similar trends are visible in the United Kingdom and Nordics, which helps unlock capital for technology, new service lines, and geographic expansion. Consolidation raises the importance of platform integration, client experience, and brand, while also intensifying competition for senior talent in specialist domains. As ownership models diversify, firms that align incentives around capability building and client outcomes are better placed to win in the Europe Financial Advisory Services Market. These shifts point to a more capital-intensive competitive game where scale, specialization, and technology maturity increasingly define advantage in the Europe Financial Advisory Services Market.

Strategic moves highlight technology differentiation and service breadth rather than large cross-border takeovers in banking due to political and regulatory constraints. Major networks continue investing in AI-enabled platforms to digitize tax, assurance, and advisory workflows that meet supervisory evidence standards and client expectations for transparency and speed. Firms also partner with technology vendors to embed analytics, ESG data, and explainable personalization into client portals, which elevates experience and supports outcome-based contracting. KPMG advised on multiple transactions in 2025 across media, machinery, automotive retail, and protective equipment, illustrating demand for integrated M&A, financing, and restructuring support. Leading firms plan structural changes to simplify governance and improve risk management while enhancing growth capacity and quality controls across jurisdictions.

White-space opportunities are expanding in cross-border regulatory advisory as Europe and the United Kingdom rules diverge and as digital assets and crypto tax reporting enter the operational mainstream. Sustainability implementation beyond compliance gains importance as Phase 2 CSRD entities begin reporting in 2026 and seek integrated solutions across data, process, and assurance. Digital-asset structuring and controls design become mainstream advisory work as MiCA and DAC8 codify authorization, reporting, and investor protection guardrails. Firms that align specialization with platform-enabled delivery will be positioned to monetize scale and navigate fee pressure while maintaining differentiation. Competitive dynamics, therefore, favor providers that can integrate sector expertise, regulatory depth, and data-led delivery across multiple Europe jurisdictions.

Europe Financial Advisory Services Industry Leaders

KPMG

Deloitte

EY

PwC

BDO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bridgepoint has agreed to buy a majority stake in Interpath Advisory, the restructuring and financial advisory firm spun out from KPMG United Kingdom, in a deal valuing the business at around USD 1,005.21 million, marking a major private equity investment in professional services.

- January 2026: Interpath announced Bridgepoint’s planned majority acquisition and said it will use the backing to accelerate international growth and broaden services across restructuring, M&A, and advisory offerings.

- July 2025: EY announced plans to move its Birmingham office from One Colmore Square to a new office at Three Chamberlain Square in the Paradise Birmingham development in 2026, reflecting continued investment in the Midlands.

- November 2024: International private equity firm Cinven reached an agreement to take a majority stake in Grant Thornton United Kingdom, one of the United Kingdom’s leading professional services firms, supporting strategic growth and reinforcing private equity’s role in the sector.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe financial advisory services market as all fee-based advice and project revenues earned by licensed professionals and firms that guide people or organizations on investments, capital structure, taxation, deals, or risk. We focus strictly on contract or retainer fees recorded inside Europe, whether delivered on-site or through virtual channels.

Scope excludes pure asset-management charges, brokerage commissions, and internal advisory work billed inside the same corporate group.

Segmentation Overview

- By Service Type

- Corporate Finance

- Accounting And Tax Advisory

- Investment

- Other Services

- By Organization Size

- Large Enterprises

- Small & Medium-sized Enterprises (SMEs)

- By Industry Vertical

- Banking, Financial Services, Insurance (BFSI)

- IT & Telecommunication

- Manufacturing

- Retail And E-Commerce

- Public Sector

- Healthcare And Pharmaceuticals

- Other Industry Verticals

- By Service Channel

- Human Advisory

- Hybrid Advisory

- Robo-Advisory

- By Delivery Mode

- On-site Consulting

- Remote / Virtual Consulting

- By Geography

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Partner-level consultants, SME finance heads, and wealth managers in the UK, DACH, Nordics, Iberia, and CEE share insights on average billable hours, digital-advice uptake, and ESG audit demand. These interviews validate secondary signals, close information gaps, and underpin every assumption we log.

Desk Research

We begin with open-access regulators such as the European Securities and Markets Authority, the UK Financial Conduct Authority, and the European Central Bank, letting us map adviser counts, mandate volumes, and fee caps. Trade groups including Accountancy Europe and the European Federation of Financial Advisers supply channel mix ratios, while Eurostat, IMF, and Bank for International Settlements datasets ground our macro context.

Company filings mined through D&B Hoovers, contract notices on Tenders Info, and real-time articles from Dow Jones Factiva flag pricing shifts and new service launches. The sources named are illustrative, and many others reinforce the evidence base that Mordor analysts compile.

Market-Sizing & Forecasting

We start with a top-down pool: Eurostat gross output for consulting and advisory is filtered by the financial-advisory share from regulator and trade data, then adjusted for cross-border service exports. Select bottom-up checks, billing rate times staff headcount for twenty sampled firms, anchor the totals. Key drivers in the model include licensed adviser population, corporate deal count, household financial assets, cloud banking penetration, and share of virtual advice sessions. A multivariate regression plus scenario analysis projects these variables through 2030, and gaps in sampled firm data are bridged using median peer ratios.

Data Validation & Update Cycle

Mordor analysts run variance tests against ECB fee indexes, reconcile currency swings monthly, and escalate anomalies for senior review. Reports refresh each year, with interim updates whenever material regulation or mega-deals shift demand, so clients always receive the latest view.

Why Mordor's Europe Financial Advisory Services Baseline earns trust in Europe

Published estimates often diverge because firms pick different revenue pools, geographies, or inflation treatments.

Some studies widen scope to include wealth or brokerage income; others rely on static penetration rules, while Mordor's disciplined service-fee focus, dual-path modeling, and annual refresh curb such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 30.92 B (2025) | Mordor Intelligence | |

| USD 42.65 B (2024) | Global Consultancy A | Omits SME advisory and back-calculates from deal values |

| USD 312.5 B (2024) | Industry Update B | Adds wealth-management and brokerage revenue |

The comparison shows that anchoring figures to clearly bounded fee streams, validated inputs, and repeatable steps lets Mordor Intelligence deliver a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the Europe Financial Advisory Services Market CAGR and projected size by 2031?

The Europe Financial Advisory Services Market size is expected to grow from USD 30.91 billion in 2025 to USD 32.27 billion in 2026 and is forecast to reach USD 39.97 billion by 2031 at 4.37% CAGR over 2026-2031.

Which service category holds the largest share in the Europe Financial Advisory Services Market?

Accounting and Tax Advisory held the largest 2025 share at 31.75%, driven by complex cross-border obligations and sustained regulatory change.

Which service category is growing the fastest through 2031 in the Europe Financial Advisory Services Market?

Investment services are projected to grow the fastest at a 6.34% CAGR, helped by MiCA-related authorization and compliance demand.

Who spends more today, and who is growing faster by client size?

Large enterprises accounted for 57.07% of 2025 revenues, while SMEs show faster growth at a projected 5.82% CAGR to 2031.

Which industry vertical leads revenue within the Europe Financial Advisory Services Market?

BFSI led with a 32.48% revenue share in 2025 due to regulatory intensity and digital competition across banking and insurance.

Which country contributes the most revenue in the Europe Financial Advisory Services Market?

The United Kingdom led with a 21.53% revenue share in 2025, while the Rest of Europe is projected to grow fastest at a 6.79% CAGR.

Page last updated on: