Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

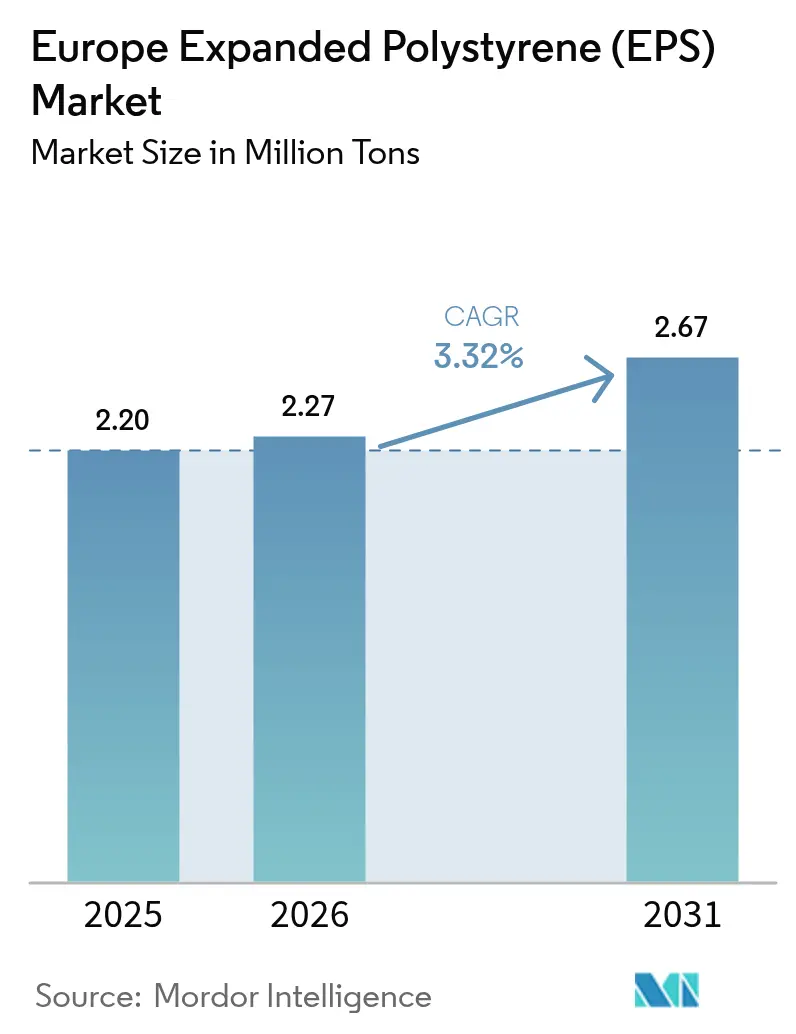

| Base Year Market Size (2025) | 2.20 Million tons |

| Market Volume (2026) | 2.27 Million tons |

| Market Volume (2031) | 2.67 Million tons |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Expanded Polystyrene (EPS) Market Analysis by Mordor Intelligence

The Europe Expanded Polystyrene Market size was valued at 2.20 million tons in 2025 and estimated to grow from 2.27 million tons in 2026 to reach 2.67 million tons by 2031, at a CAGR of 3.32% during the forecast period (2026-2031). Demand flows primarily from building insulation upgrades and protective packaging for sensitive goods, while sector resilience is reinforced by robust domestic supply chains, incremental recycling gains, and technology upgrades that lower embodied carbon footprints. Regulatory drivers such as the EU Energy Performance of Buildings Directive, effective from 2025, compel higher R-values across new builds and retrofits, keeping insulation volumes stable even as substitutes gain share. Simultaneously, the surge in mRNA biologic logistics and appliance reshoring sustains packaging volumes, helping buffer commodity segments against margin compression from styrene volatility. Nevertheless, the Europe Expanded Polystyrene market negotiates mounting headline risk tied to feedstock price swings, fire-safety regulations in dense urban cores, and customer trials of paper-, pulp-, and mycelium-based alternatives.

Key Report Takeaways

- By product type, white EPS held 70.86% of Europe Expanded Polystyrene market share in 2025. Gray and silver EPS is projected to expand at a 3.74% CAGR through 2031.

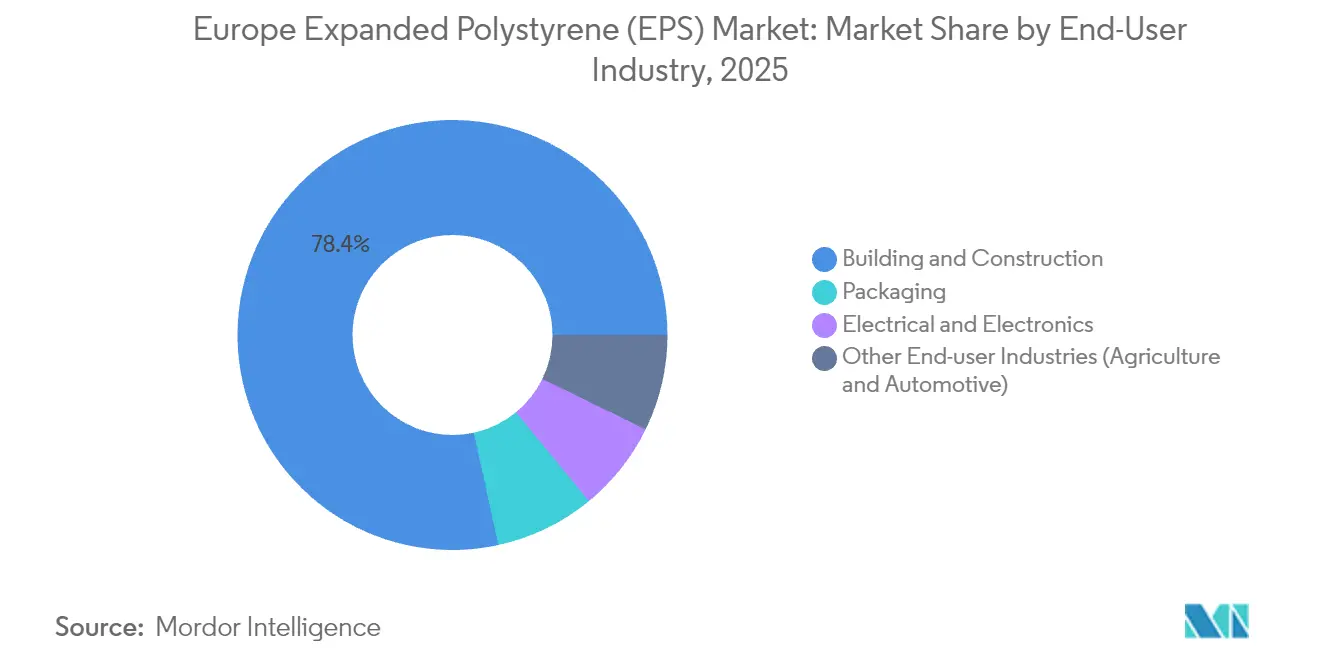

- By end-user, building and construction captured 78.42% of Europe Expanded Polystyrene market size in 2025. Packaging is forecast to log the fastest 3.69% CAGR between 2026 and 2031.

- By geography, the Rest of Europe commanded a 51.98% share of Europe Expanded Polystyrene market size in 2025, whereas, Sweden is poised to advance at a 3.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Expanded Polystyrene (EPS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Building-energy codes mandating higher R-values from 2025 | +1.20% | Germany, France, Nordic countries with spillover to Central Europe | Medium term (2-4 years) |

| Mandatory cold-chain capacity additions for mRNA-class biologics | +0.80% | Netherlands, Belgium, Germany, with distribution across EU | Short term (≤ 2 years) |

| Re-shoring of appliance production boosting domestic protective packaging | +0.60% | Germany, Italy, Poland, Czech Republic | Medium term (2-4 years) |

| Grey-EPS adoption in EU “Renovation Wave” retrofit projects | +0.70% | Western Europe, Nordic countries | Long term (≥ 4 years) |

| Low-cost modular housing programmes | +0.50% | Sweden, Netherlands, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Building Energy Codes Drive Thermal Performance Requirements

Stricter national and EU-wide energy codes compel developers to design walls, roofs, and floors with lower U-values, lifting insulation thickness requirements and supporting steady volume demand for Europe's Expanded Polystyrene market solutions. Germany’s Gebäudeenergiegesetz already specifies exterior wall U-values near 0.20 W/(m²K), which typically necessitates 12-16 cm of EPS, cementing roughly 40% share for the foam in German façade systems despite height-based fire-safety limits. France and the Nordics extend similar performance stipulations, and the 2024 recast of the Energy Performance of Buildings Directive sets a net-zero mandate for new structures from 2030, locking in long-range insulation demand. Retrofit volumes also rise under the EU Renovation Wave, with grants steering homeowners toward thermally efficient yet affordable systems. Producers broaden their Neopor and graphite-enriched lines in this compliance-driven landscape to deliver superior R-values without costly structural modifications.

mRNA Biologics Cold Chain Expansion

Rapid commercialization of mRNA vaccines and advanced therapeutics requires 2 °C-to-8 °C stability from factory to clinic. EPS shippers dominate this lane because the material’s closed-cell matrix provides predictable insulation and cushioning over long-haul flights and last-mile parcels. Manufacturers such as Cold Chain Technologies have added European capacity in Breda, Netherlands, specifically to serve pharma corridors reaching 80% of EU GDP centers within a six-hour drive. Regulatory tightening under European Pharmacopoeia Supplement 11.7 pushes packaging suppliers to validate extractables and leachables, favoring incumbent EPS formulations with proven compliance records. The cold-chain opportunity carries premium margins that partially offset styrene spread volatility in commodity construction foam.

Appliance Manufacturing Reshoring Momentum

Europe-based appliance producers have shortened supply chains since 2024 to mitigate freight shocks and geopolitical risk. Lines relocated to Germany, Italy, and Poland create incremental demand for molded-foam cushions, corner blocks, and rigid inserts to protect washing machines, refrigerators, and HVAC units during multi-modal transit. Because lead times shrink when packaging is sourced close to assembly plants, local EPS converters win a greater share over Asian imports, supporting stable plant utilization in Central Europe. The Europe Expanded Polystyrene market captures uplift in protective packaging tonnage and added-value components—such as structural liners that double as energy-saving insulation inside appliance cabinets.

EU Renovation Wave Accelerates Gray EPS Adoption

The European Commission aims to double renovation rates by 2030 and, crucially, prioritizes building-envelope upgrades. Space-restricted façades, common in dense city blocks, favor graphite-infused gray EPS because it cuts thermal conductivity by up to 20% versus white grades, allowing slimmer panels without sacrificing R-value. Polish producers ship competitively priced gray EPS across the bloc, lowering installed costs in Ireland and Scandinavia by an estimated 24%, which accelerates uptake. Circular product families such as BEWI’s CIRCULUM integrate recycled feedstock, aligning with EU waste-reduction goals and enhancing contractor acceptance.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Styrene monomer price volatility tracking crude-oil spreads | -0.90% | Global impact with particular pressure on Northwest Europe | Short term (≤ 2 years) |

| Commercialisation of mycelium & moulded-pulp substitutes | -0.40% | Netherlands, Germany, Nordic countries leading adoption | Medium term (2-4 years) |

| Carbon-pricing schemes inflating Scope-3 footprints of petro-polymers | -0.60% | EU ETS coverage across all member states, with early impact in Germany, Netherlands, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Feedstock Cost Volatility Pressures Margins

Styrene accounts for up to 70% of EPS cash costs, making profitability sensitive to benzene-and naphtha swings. January 2025 contract hikes of EUR 55 per ton announced by Trinseo illustrate producer attempts to defend margins[1]Trinseo, “Trinseo Announces Price Increase for Polystyrene, ABS, and SAN in Europe,” TRINSEO.COM . Structural tightness deepens as Versalis shutters its Brindisi cracker in April 2025, widening the region’s import dependency and magnifying freight and currency risks. The mismatch between volatile raw-material outlays and fixed-price construction contracts squeezes converter cash flows, challenging smaller plants across Northwest Europe.

Sustainable Alternatives Gain Market Traction

Brand owners and retailers pursue fiber-based, mycelium-grown, or multi-use plastic systems to meet EU packaging-design rules targeting 100% recyclability by 2030[2]NSF, “New EU Regulation 2025/40 on Packaging and Packaging Waste,” NSF.ORG . DS Smith’s TailorTemp corrugated solution claims a 40% lower CO₂ footprint than EPS while maintaining pharma temperature control for 36 hours, signaling credible technical competition in select niches. If drop-in replacements scale, they could erode market share in premium packaging just as regulation squeezes single-use foams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gray EPS Drives Performance Innovation

Europe's Expanded Polystyrene market size for white grades accounted for 70.86% share of overall consumption. White EPS persists in cavity walls, slab-on-grade floors, and perimeter drainage boards where cost remains the critical selector and modest panel thicknesses suffice for code compliance. However, gray and silver grades register the fastest 3.74% CAGR to 2031 as graphite’s infrared-reflective particles lower λ-values to around 0.030 W/(m·K). In external thermal insulation composite systems, gray EPS reduces layer thickness from 16 cm to 12 cm for the same U-value, unlocking façade renovation in urban districts with tight lot lines. BEWI’s CIRCULUM line couples the performance edge with recycled bead content, helping architects reconcile energy and circularity targets. Producers invest in in-line blowing-agent recovery and continuous block molding to embed more reclaim without sacrificing mechanical properties, positioning gray EPS as a technical and eco-credential upgrade within the Europe Expanded Polystyrene market.

By End-user Industry: Construction Dominance Faces Packaging Growth

Building and construction accounted for 78.42% of Europe Expanded Polystyrene market share, thanks to exterior insulation, underfloor panels, and civil-works void formers. Germany’s and Italy’s heat-pump boom has increased under-slab insulation sales, while Spain’s tourism-led refurbishments add hospitality retrofits. Despite the dominant base, growth moderates as mineral wool captures mid-rise and high-rise cladding following stricter fire codes. Packaging, meanwhile, expands at a 3.69% CAGR, boosted by biologics logistics and e-commerce fragile-goods shipping. Pharmaceutical shippers value EPS’s validated temperature maps and drop-test data, while appliance OEMs count on local molding shops for just-in-time cushion sets. Electrical and electronics packaging remains steady, and specialty uses—from seedling trays to auto bumper-core spacers—deliver incremental volume diversity, fortifying the Europe Expanded Polystyrene market against construction cyclicality.

Geography Analysis

The rest of Europe amassed 51.98% of the Europe Expanded Polystyrene market size in 2025 as Poland, the Czech Republic, and other Central-Eastern producers supply cost-competitive blocks and molded parts across the continent. Germany remains the single largest national consumer, upheld by stringent insulation mandates and ongoing residential rooftop conversions; however, fire-safety restrictions above 22 m height temper multi-story volumes. The UK shows flat demand as builders favor non-combustibles for recladding but still specify EPS-filled insulated concrete forms in low-rise housing.

Sweden leads growth at a 3.71% CAGR through 2031, powered by government-backed retrofits, prefabricated wooden frames that integrate EPS cores, and strong cleantech investment that earmarks funds for circular insulation systems. Denmark and Norway advance on district-heating trench projects that install EPS as frost protection, while Finland leverages forest-industry synergies to integrate foam under cross-laminated timber floors. Southern Europe presents a mixed picture: Italy’s low-interest loans and homeowners’ tax rebates stimulate EPS-based ETICS yet supply is tight amid styrene price jumps; France’s temporary suspension of its polystyrene packaging ban lifts near-term sentiment for converters. Spain benefits from hospitality refurbishments along its coastal zones plus new cold-storage warehouses tied to agrifood exports.

Value Chain Analysis

Europe's EPS value chain begins with upstream aromatics and styrene production, followed by polymerization into expandable polystyrene (EPS) beads by integrated resin producers. Downstream block molding and shape molding convert the beads into insulation boards (including graphite-enhanced grades) and protective packaging formats. The material then moves through distributors and converters to end users in building and construction (notably ETICS) and packaging, with installation contractors and logistics providers influencing service levels and lead times, particularly for validated cold-chain shipper programs.

The chain is also being shaped by post-use collection, sorting, and recycling loops. EPR-linked collection and take-back models are expanding, with Citeo and EUMEPS deploying professional packaging take-back systems at delivery points from January 2026. Industry bodies such as EUMEPS have been feeding technical input on the Packaging and Packaging Waste Regulation (PPWR), including Article 29 topics such as EPS fish boxes. Bottlenecks persist where harmonized collection and treatment infrastructure varies by member state, leaving recycled-content availability and quality less consistent than virgin bead supply for converters. This elevates the role of association-led standardization and design-for-recycling practices to keep molded and insulation applications aligned with mechanical recycling streams.

Competitive Landscape

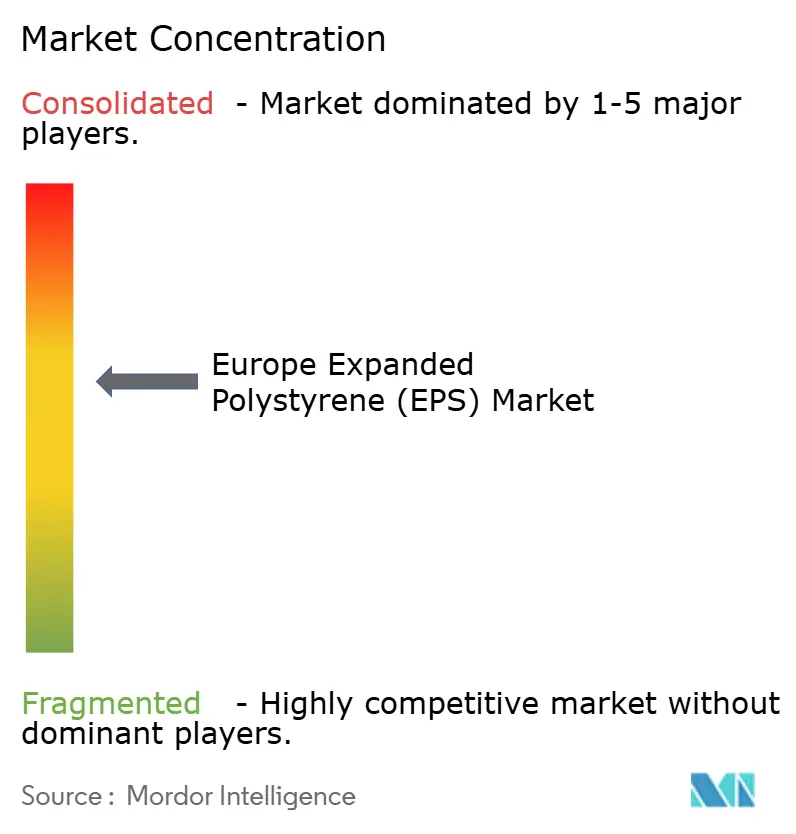

The Europe expanded polystyrene market exhibits consolidated concentration, with five integrated resin producers supporting a network of regional block molders and shape molders. BASF’s planned 50 kt per-year Neopor capacity lift at Ludwigshafen, operational in 2027, underscores incumbents’ push toward premium graphite lines to preserve margin while meeting energy benchmarks. BEWI runs a closed-loop scheme processing roughly 2,500 t per month of post-consumer foam at Nordic hubs, feeding recycled bead back into CIRCULUM grades that win public-procurement bids emphasizing circularity. Versalis allocates EUR 2 billion to retrofit assets toward sustainable chemistry, signaling longer-term supply diversification beyond fossil styrene.

Rationalization is unfolding: Trinseo divests selected PS assets to slash European exposure, while smaller independent extruders confront high power tariffs and volatile styrene spreads. Technology differentiation intensifies around advanced recycling and continuous process innovations; Sulzer’s column-based EPS train enables higher recycled-content rates without degassing penalties, giving converters a route to comply with 2030 recyclability thresholds. Competitive dynamics now hinge on scale, circular supply chains, and ability to certify lower life-cycle emissions, more so than on price alone. The Europe Expanded Polystyrene market thus tilts toward larger, vertically integrated groups capable of co-developing fire-retardant recipes, bio-based blowing agents, and digital design tools that optimize structural foam placement inside prefabricated panels.

Europe Expanded Polystyrene (EPS) Industry Leaders

BASF

BEWi

Alpek SAB de CV

SABIC

Synthos

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Circularity-linked capacity and standards are creating near-term whitespace across insulation and packaging grades. BEWI opened a dedicated EPS recycling facility at its Fredrikstad insulation site in February 2026, designed for up to 3,500 tonnes per year of EPS. The plant provides an outlet for post-consumer foam and supports recycled-feedstock branded offerings. On the design side, EN 18092:2025 (published by CEN in October 2025) sets design-for-recycling guidelines for EPS insulation, giving product developers, specifiers, and waste operators a clearer route to align panel design with collection and recycling requirements.

Opportunity is also being reshaped by industry structure and premium-grade positioning. BEWI and The Rock Capital Group finalized the merger of their EPS raw material businesses into a new entity with four facilities and total capacity of 375,000 metric tons. This expands supply options for downstream converters and supports more coordinated grade development across regions. BASF's announced 50,000 metric tons per year Neopor capacity expansion at Ludwigshafen (October 2024, with commissioning scheduled for early 2027) reinforces ongoing investment in graphite-based EPS for renovation constraints where thinner insulation still meets required thermal performance. With PPWR entering into force on 11 February 2025 and its 2030-oriented recyclability framework, suppliers that combine validated recycling routes with DfR-compliant insulation and molded packaging specifications have a practical basis to win tenders that prioritize circular procurement criteria.

Recent Industry Developments

- June 2026: BASF announced the closure of EPS production assets at its Ulsan Plastics site in South Korea, effective mid-June 2026. The company stated that European styrenics operations were unaffected, while the decision signaled continued portfolio optimization and tighter alignment of global EPS footprints with regional demand and cost positions.

- February 2025: BEWI agreed with The Rock Capital Group to merge their EPS raw material businesses, creating a new entity with total annual production capacity of 375,000 tonnes across four facilities. The consolidation strengthens upstream supply scale for European converters and supports more coordinated investment in grades tailored to insulation and packaging requirements.

- October 2024: BASF announced a 50,000 metric tons per year expansion of Neopor (graphite-based EPS) production capacity at Ludwigshafen, with startup scheduled for early 2027. The move reinforces the shift toward higher-performance EPS used in energy-efficient building insulation and adds future capacity headroom for renovation-driven demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers expanded polystyrene (EPS) material supplied and consumed across Europe for insulation, protective packaging, and other common end uses. The scope is measured across the full value of EPS resin and the converted product sold into the region.

Scope exclusions: We exclude expanded polystyrene used only as a minor additive in blends and non-EPS foams that are marketed under broader polystyrene foam labels.

Segmentation Overview

- By Product Type

- White EPS

- Gray and Silver EPS

- By End-user Industry

- Building and Construction

- Electrical and Electronics

- Packaging

- Other End-user Industries (Agriculture and Automotive)

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Norway

- Sweden

- Denmark

- Finland

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the model guardrails, with attention to polymer demand signals, construction activity, and packaging volumes across Europe. Public sources were referenced for industrial production and trade series (Eurostat), for plastics and waste policy direction (European Commission), and for packaging and recycling indicators (European Environment Agency). Where insulation demand needed extra context, energy performance directives and national building statistics were checked so country trends were not taken at face value.

Alongside these references, we reviewed company annual reports, investor presentations, and reputable press coverage to understand capacity moves, plant utilization commentary, and regional supply patterns. A paid subscription was used for company financials, and another for shipment-level import and export checks, which helped validate directional volume movement and identify outlier years. The desk sources named above are illustrative only, and other public references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with EPS raw material suppliers, converters, distributors, and large end users in construction and packaging across major European countries. Respondent input was used to confirm typical application splits, how pricing passes through energy and styrene costs, and the pace of substitution and recycling adoption. Those details then helped us tune assumptions where public data was not specific enough for the EPS scope used in this report.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | |

| Mid tier: 54% | Functional/Unit leaders: 36% | |

| Smaller Players: 20% | Managers: 49% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs country demand pools from construction insulation activity, packaging output indicators, and polymer consumption signals. These pools were then converted into EPS volume using typical material intensity ranges. To keep the results realistic, the model also used a selective bottom-up cross-check based on sampled supplier and converter revenues, observed capacity changes, and ASP by grade and application. Totals were adjusted only when the two views disagreed beyond a reasonable range.

A few practical inputs were tracked closely because they move the EPS market in Europe in ways visible in the data, including housing starts and renovation intensity, insulation code tightening, packaging mix shifts, styrene and energy-linked cost pass-through, and the share of gray and silver EPS in insulation applications. Forecasting relied mainly on scenario analysis, since construction cycles and policy-driven packaging changes do not move in a straight line every year. Where data gaps existed for smaller countries, ratios were inferred from similar markets and rechecked with interview feedback before being locked into the forecast.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including trade flows, capacity and utilization commentary, and downstream activity indicators by country. If a country trend looked too steep compared with what participants reported, we revisited inputs, reran sensitivity checks, and re-contacted sources when the mismatch remained unresolved.

A multi-step review is applied before sign-off, including peer checks on assumptions, unit conversions, and year-over-year movements. Reports are refreshed annually, with interim updates when material events occur, such as major capacity additions, regulatory shifts affecting packaging, or sharp feedstock price swings. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Europe Expanded Polystyrene Eps Market Estimate Compared With Other Published Estimates

Published market sizes for Europe EPS often do not match because the underlying unit of measurement, the included product boundary, and the price build used to convert volume to value are not the same. Differences also appear when one estimate leans on a single application trend, such as insulation, while another spreads demand across packaging and other uses with different growth patterns.

Extruded polystyrene (XPS) insulation boards sit outside Mordor Intelligence's scope for this report, which is a key reason some value-based estimates appear higher when they combine adjacent foam insulation categories. Another gap driver is the value conversion itself, since some publishers apply a single blended Europe-wide ASP while others use country and application pricing that changes with styrene and energy pass-through timing. Refresh cadence matters as well, because large construction slowdowns or packaging regulation updates can shift near-term volumes and prices, and not all estimates use the same cut-off date.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.20 M (2025) | |

| Global Consultancy A | USD 2.25 B (2024) | This figure is presented as a value market and may apply a broad price assumption and wider foam scope, which can pull in non-EPS items such as XPS or other polystyrene foam revenues that are not counted here. |

| Industry Association B | USD 2.62 M (2030) | The estimate is stated as a volume forecast and likely reflects a shorter horizon with different country weighting, and it may not apply the same application mix checks that smooth construction cycle swings. |

Taken together, the spread is mainly explained by unit choice (volume versus value), adjacent category inclusion, and how pricing is carried forward across countries and end uses. By keeping the EPS definition tight and then tying the totals back to observable construction and packaging indicators, the resulting number stays easier to reproduce and explain on a country-by-country basis.

Key Questions Answered in the Report

How large is the Europe Expanded Polystyrene market in 2026?

It totals 2.27 million tons in 2026 and is forecast to reach 2.67 million tons by 2031.

What is the projected CAGR for Europe’s EPS consumption?

Volume is expected to rise at a 3.32% CAGR between 2026 and 2031.

Which product type grows fastest through 2031?

Gray and silver EPS, boosted by higher thermal efficiency, expands at a 3.74% CAGR.

Which end-use segment offers the highest growth?

Packaging, driven by pharma cold-chain and e-commerce demand, records a 3.69% CAGR.

Which country posts the quickest EPS growth?

Sweden leads with a projected 3.71% CAGR, leveraging prefabricated housing and retrofit programs.

Page last updated on: