Market Overview

| Study Period | 2020 - 2031 |

|---|---|

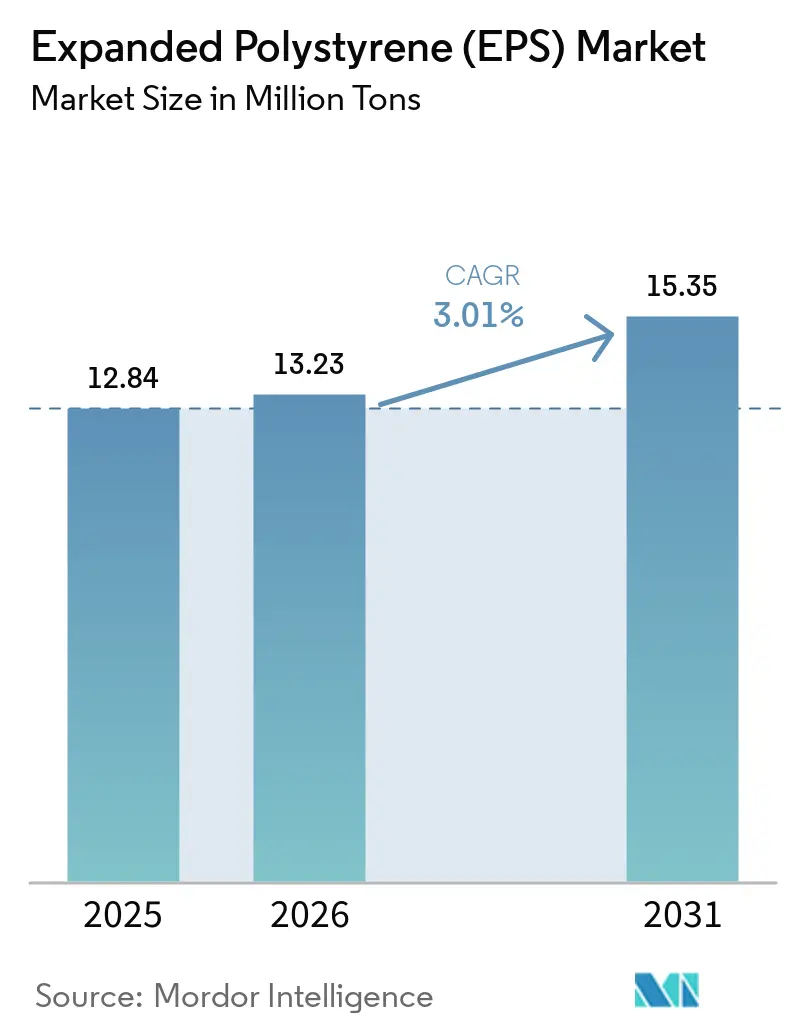

| Market Volume (2026) | 13.23 Million tons |

| Market Volume (2031) | 15.35 Million tons |

| Growth Rate (2026 - 2031) | 3.01% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Expanded Polystyrene (EPS) Market Analysis by Mordor Intelligence

Expanded Polystyrene market size in 2026 is estimated at 13.23 million tons, growing from 2025 value of 12.84 million tons with 2031 projections showing 15.35 million tons, growing at 3.01% CAGR over 2026-2031. Volume growth reflects the push–pull between rising consumption in construction and packaging and the cost pressures generated by stringent volatile-organic-compound limits on styrene processing. The Expanded Polystyrene market continues to capitalize on its favorable thermal conductivity-to-price ratio, which keeps demand steady even as molded pulp, bio-foams, and paper-based liners scale up. Asia-Pacific remains the single largest outlet, while North America leverages the material for e-commerce last-mile insulation. Corporate strategies increasingly pivot on chemical recycling pathways and feedstock diversification, signaling that circular-economy compliance is an emerging competitive prerequisite across the Expanded Polystyrene market.

Key Report Takeaways

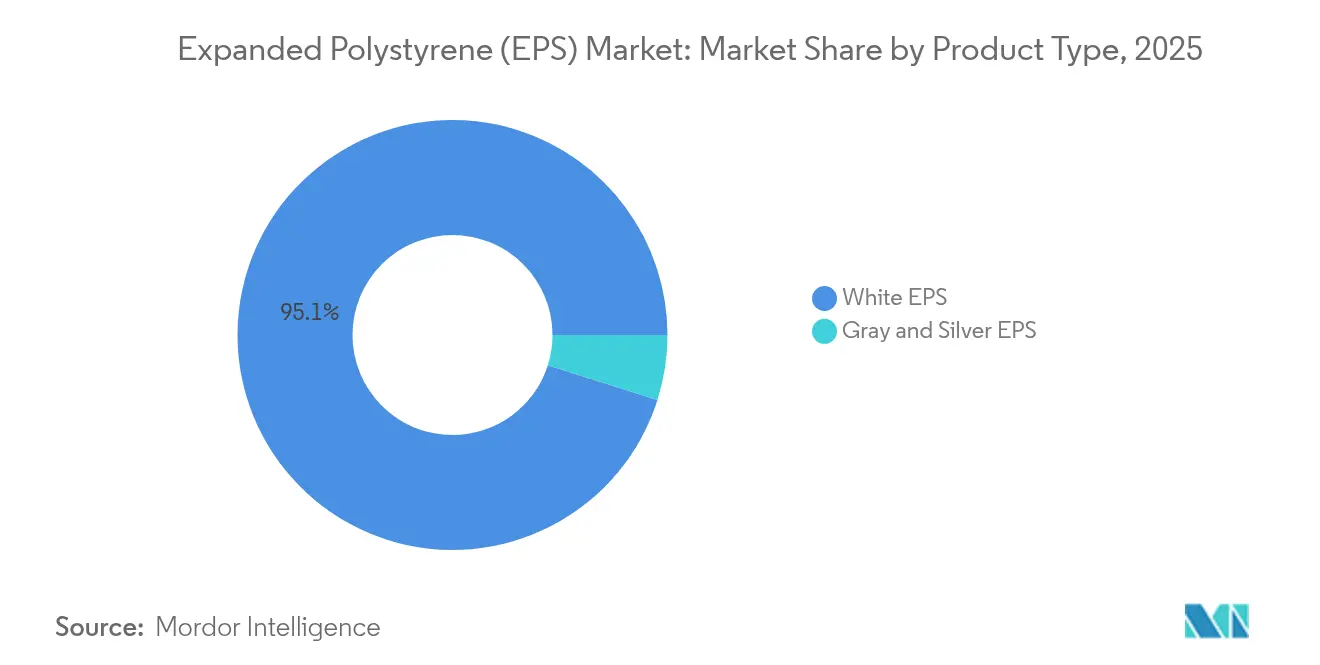

- By product type, white EPS held 95.12% of the Expanded Polystyrene market share in 2025; gray and silver EPS are projected to register the fastest 3.89% CAGR through 2031.

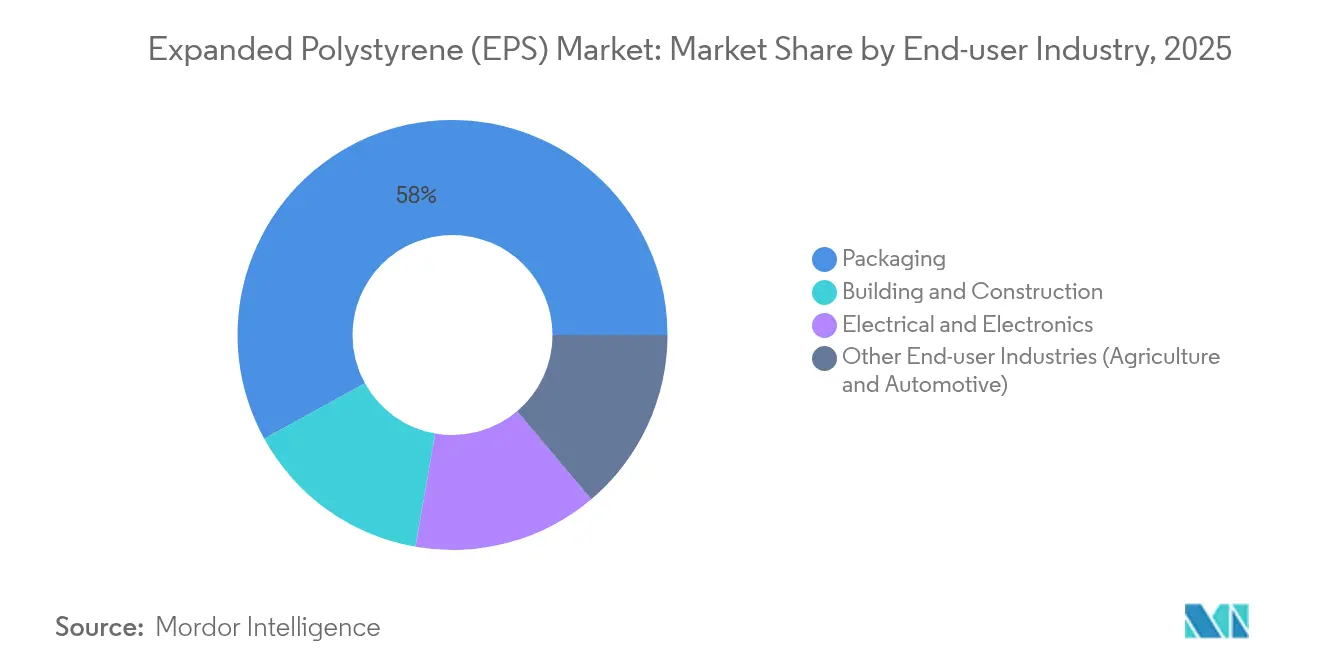

- By end-user industry, packaging contributed 58.02% of the Expanded Polystyrene market size in 2025 and shows a 3.34% CAGR outlook to 2031.

- By geography, Asia-Pacific accounted for 66.75% of the Expanded Polystyrene market size in 2025, and is expected to expand at the quickest 3.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Expanded Polystyrene (EPS) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated push for net-zero-ready buildings | +0.8% | Europe, Japan, spreading globally | Medium term (2-4 years) |

| Resurgent cold-chain investments in emerging APAC | +0.7% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| E-commerce last-mile insulated packaging boom | +0.6% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Mandatory seismic insulation codes | +0.4% | Europe, Japan | Long term (≥ 4 years) |

| Modular prefab construction uptake | +0.3% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Push for Net-Zero-Ready Buildings

Rapid decarbonization targets are redrawing insulation specifications worldwide. Energy-performance mandates in Europe require near-zero-energy new builds, pushing architects toward materials that combine low λ-values with proven durability. Gray and silver EPS deliver up to 20% lower thermal conductivity than standard grades, enabling thinner wall assemblies without compromising U-value compliance. Japan’s 2024 energy-efficiency revision tightens thermal-envelope criteria, further amplifying demand for graphite-enhanced Expanded Polystyrene market solutions. As building owners prioritize operating-cost reductions, EPS gains traction in continuous insulation and structural insulated panels, reinforcing the Expanded Polystyrene market’s profile in the high-performance building segment.

Resurgent Cold-Chain Investments in Emerging APAC

Southeast Asian governments are funneling billions into cold-chain logistics to curb food spoilage and uphold drug-safety standards. EPS boxes and liners dominate because they combine R-value stability with shock absorption at the lowest delivered cost per unit. Semiconductor assembly hubs in Vietnam rely on EPS clamshells to maintain narrow thermal windows, while regional vaccine campaigns depend on validated EPS shippers to protect temperature-sensitive biologics.

E-Commerce Last-Mile Insulated Packaging Boom

North American online grocery revenue leapt in 2024, intensifying demand for lightweight insulation that can survive two-day ground delivery[1]US Department of Commerce, "E-commerce Retail Sales," census.gov. Meal-kit brands and direct-to-consumer pharmacies specify EPS because it satisfies FDA temperature-stability rules and provides a familiar unboxing experience. Amazon’s 2024 expansion of same-day fresh delivery to 40 new metros demonstrated the logistical importance of proven EPS formats that integrate with automated fulfillment centers. The Expanded Polystyrene market, therefore, captures incremental tonnage from every new micro-fulfillment hub that opens across urban corridors in the United States.

Mandatory Seismic Insulation Codes in Europe and Japan

Seismic zones are introducing dual-function envelope requirements, demanding insulation that mitigates structural vibration. Japan’s 2024 Building Standards Law revision incorporates EPS layers into base-isolation systems, citing the foam’s low density and resilience. Italy and Greece adopted comparable provisions after post-event assessments showed that flexible foam panels preserved wall integrity during quakes. Retrofits funded under Italy’s modified Superbonus program stipulate advanced EPS assemblies, extending the Expanded Polystyrene market tailwind well into the next decade.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC emission ceilings on styrene | -0.5% | Europe, North America | Medium term (2-4 years) |

| Rapid scale-up of molded pulp thermal liners | -0.3% | North America, Europe | Short term (≤ 2 years) |

| EU “Design for Recycling” mandates | -0.4% | Europe, potential global spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening VOC Emission Ceilings on Styrene

The EU lowered occupational styrene limits to 20 ppm in 2024, forcing manufacturers to retrofit abatement systems that can add 3–5% to operating costs. EPA enforcement actions in the United States climbed 40% the same year, raising compliance risk. Smaller converters lacking capital for regenerative thermal oxidizers may exit, narrowing regional supply and nudging prices upward across the Expanded Polystyrene market.

EU “Design for Recycling” Mandates Curbing Single-Use EPS

The 2024 Packaging and Packaging Waste Regulation revision imposes recyclability criteria that single-use EPS often fails to meet unless collection is guaranteed[2]European Commission, “Packaging and Packaging Waste,” ec.europa.eu . Mechanical recycling rates linger below 30% across Europe, so brand owners face higher extended-producer-responsibility fees when they choose EPS. This cost penalty accelerates material substitution in disposable coffee cups and takeaway trays, eroding a niche of the Expanded Polystyrene market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Thermal-Enhanced Grades Win Share from Commodity Foam

White EPS accounted for 95.12% of the Expanded Polystyrene market in 2025, yet gray variants are on track to expand faster at 3.89% CAGR through 2031. Builders in Germany and France specify graphite-infused panels to meet U-values without thicker walls, illustrating how performance upgrades redirect demand even when prices are higher. Manufacturers such as BASF added 40% Neopor capacity in 2024 to satisfy this construction pull. Concurrently, reflective silver EPS grades penetrate industrial insulation niches where surface temperatures exceed 80 °C, tapping small but growing specialized opportunities. Commodity packaging still leans heavily on white foam because logistics buyers prioritize low upfront cost. As building codes tighten, however, higher-R-value lines will gradually chip away at white EPS dominance within the Expanded Polystyrene market.

White EPS’s cost edge keeps it entrenched in appliance cushioning, molded fish crates, and block-molded architectural shapes. Gray EPS, despite its premium, secures volume through energy-efficient façade systems, ensuring that every new near-zero-energy project allocates tonnage to graphite grades. The expansion of silver EPS stays modest but lucrative, given its fit for petrochemical pipe insulation and high-temperature cold-box linings in LNG terminals. These trends confirm that differentiated performance creates defensible value pockets, even inside a largely commoditized Expanded Polystyrene market.

By End-User Industry: Packaging Remains Anchor as Construction Accelerates

Packaging represented 58.02% of 2025 tonnage, underscoring the material’s entrenched role in temperature-controlled logistics. The segment is forecast to grow at 3.34% CAGR, buoyed by meal-kit subscriptions, biologics shipping, and fresh-grocery delivery windows that average 30 hours from fulfillment to doorstep. Building and construction is also a significant consumer, helped by stimulus-backed retrofit programs in Europe and infrastructure upgrades in India. Structural insulated panels and insulated concrete forms integrate EPS cores, providing steady pull for the Expanded Polystyrene market.

Electronics packaging keeps demand stable through semiconductor exporting nations such as Malaysia and Mexico, where EPS trays protect delicate assemblies. Agricultural trays and seedling blocks extend EPS reach into controlled-environment farming, particularly in vertical-farm modules that rely on thermal isolation. Automotive volume is smaller but rising due to lightweight spare-wheel wells and under-seat blocks that leverage EPS’s energy-absorption properties. These outlets collectively illustrate the versatility that enables the Expanded Polystyrene market to weather substitution threats in any downstream channel.

Geography Analysis

Asia-Pacific secured 66.75% of global tonnage in 2025 and is projected to rise at a 3.21% CAGR to 2031. China’s urbanization pipeline sustains housing starts, while India’s PM Gati Shakti program channels billions into road and warehousing projects, translating into higher insulation demand. Southeast Asia, led by Thailand and Vietnam, bankrolls cold-chain expansion to meet food-safety directives, pulling incremental EPS volumes for pallet-sized fish boxes and vaccine coolers. The region’s vertically integrated styrene complexes keep delivering costs low, giving local producers a structural advantage across the Expanded Polystyrene market.

North America is a significant market, driven by e-commerce and modular construction cycles. U.S. state-level energy codes increasingly require continuous-insulation layers, and factory-assembled wall panels frequently embed EPS cores to accelerate job-site completion. Canada’s multibillion-dollar cold-storage builds in Quebec and Ontario drive fresh packaging orders, ensuring a dependable baseline for regional EPS demand. Mexico rounds out the North American picture with rising electronics exports, necessitating anti-static EPS packs for printed-circuit-board transit.

Europe confronts stricter waste-reduction rules, although the Europe expanded polystyrene (EPS) market continues to rely on EPS for deep-energy retrofits funded by the EU Green Deal. Italy’s seismic-retrofit incentives and Germany’s Building Energy Act sustain panel sales, while the United Kingdom’s booming meal-delivery services offset volume lost to molded-pulp bans in single-use cutlery. Petrochemical expansions in Saudi Arabia and infrastructure corridors in Brazil suggest these territories could increase their shares as logistics networks mature.

Competitive Landscape

The Expanded Polystyrene market is moderately consolidated. The Expanded Polystyrene market features a blend of integrated petrochemical majors and nimble regional foam molders. The scale creates cost leadership, yet regional specialists hold ground by servicing niche specifications and providing short lead times. Investment has tilted toward chemical recycling, exemplified by SABIC’s joint venture with Plastic Energy to convert waste polystyrene into circular feedstock at its Geleen complex. Competitive intensity peaks in Southeast Asia, where independent converters exploit duty-free access to styrene monomer and compete on custom-mold tooling. In mature Western markets, players push premium gray EPS and bio-based lines to retain share under sustainability-focused procurement policies.

Expanded Polystyrene (EPS) Industry Leaders

-

BASF

-

BEWi

-

Alpek SAB de CV

-

SABIC

-

Synthos

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: In a joint pilot project, BASF, Sto SE & Co. KGaA, and ABG FRANKFURT HOLDING GmbH introduced an EPS insulation board containing 10% recycled material. Installed on a residential building in Frankfurt, the board matched conventional EPS in performance and ease of use. Developed using BASF’s Neopor F 5 Mcycled, the product supports circularity by incorporating mechanically recycled EPS waste.

- October 2024: BASF is enhancing its styrene value chain at Ludwigshafen by increasing Neopor production capacity by 50,000 metric tons annually to meet rising demand. The new facilities will begin operations in early 2027. Neopor, a graphite-infused expandable polystyrene (EPS) granulate, is primarily used for energy-efficient building insulation.

Global Expanded Polystyrene (EPS) Market Report Scope

Expanded Polystyrene (EPS) is a lightweight cellular plastic material consisting of small hollow spherical balls. It is closed cellular construction that gives EPS its remarkable characteristics. It is a well-established insulation material used in various applications as it has a light yet rigid foam with good thermal insulation and high impact resistance. The expanded polystyrene market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into white EPS and grey and silver EPS. By end-user industry, the market is segmented into building and construction, electrical and electronics, packaging, and other end-user industries. The report also covers the market size and forecasts for the market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kiloton).

By Product Type

| White EPS |

| Gray and Silver EPS |

By End-user Industry

| Building and Construction |

| Electrical and Electronics |

| Packaging |

| Other End-user Industries (Agriculture and Automotive) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | White EPS | |

| Gray and Silver EPS | ||

| By End-user Industry | Building and Construction | |

| Electrical and Electronics | ||

| Packaging | ||

| Other End-user Industries (Agriculture and Automotive) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Expanded Polystyrene market in 2026?

The market stands at 13.23 million tons in 2026, projected to rise to 15.35 million tons by 2031.

Which region leads demand?

The Asia-Pacific holds 66.75% of global tonnage thanks to intensive construction and packaging activity.

How fast is packaging demand for EPS growing?

Packaging volumes are expanding at a 3.34% CAGR through 2031, supported by e-commerce and cold-chain logistics.

What drives the adoption of gray EPS?

Building codes calling for higher thermal performance push gray graphite-enhanced grades, which grow at a 3.89% CAGR.

How are regulators affecting EPS production?

Stricter styrene VOC limits in the EU and U.S. compel producers to invest in advanced emission-control technologies.

Are there viable, sustainable alternatives to EPS?

Molded pulp liners like ClimaCell offer near-comparable insulation and are gaining share in North American parcel shipping.

Page last updated on: