Europe Crowd Lending And Crowd Investing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

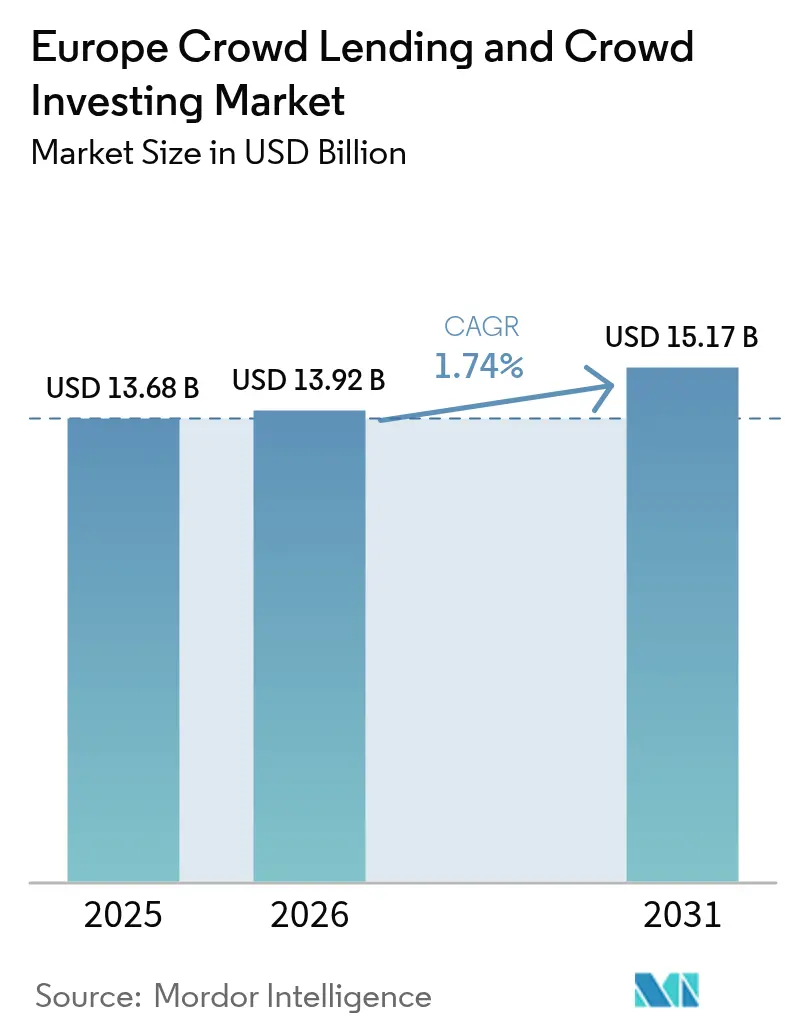

| Base Year Market Size (2025) | USD 13.68 Billion |

| Market Size (2026) | USD 13.92 Billion |

| Market Size (2031) | USD 15.17 Billion |

| Growth Rate (2026 - 2031) | 1.74% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Crowd Lending And Crowd Investing Market Analysis by Mordor Intelligence

The Europe crowd lending and crowd investing market size was valued at USD 13.68 billion in 2025 and estimated to grow from USD 13.92 billion in 2026 to reach USD 15.17 billion by 2031, at a CAGR of 1.74% during the forecast period (2026-2031). The measured expansion signals a maturing ecosystem in which regulatory convergence under the European Crowdfunding Service Providers Regulation (ECSPR) replaces the earlier phase of exponential growth. Debt-based platforms continue to dominate origination volumes, yet their yield advantage over bank deposits narrowed to 150-200 basis points in late 2024 as the European Central Bank raised base rates to 3.75%. Market opportunities increasingly revolve around embedded-finance APIs, tokenized debt instruments, and renewable-energy project pipelines aligned with EU taxonomy rules. Strategic consolidation is underway because the fixed cost of compliance favors larger operators, while cross-border passporting enables any licensed provider to serve 27 EU jurisdictions from a single home license. As a result, Lithuania, the Netherlands, and Germany are emerging as regional growth hubs, whereas France experienced funding contraction in 2024 amid real-estate delays and fraud scandals.

Key Report Takeaways

- By business model, debt-based crowdlending held 19.75% of the Europe crowd lending and crowd investing market share in 2025, whereas tokenized securities are forecast to expand at a 2.75% CAGR through 2031.

- By borrower type, SME and real-estate special-purpose vehicles captured 43.12% of the Europe crowd lending and crowd investing market share in 2025, and are growing at a 3.58% CAGR toward 2031.

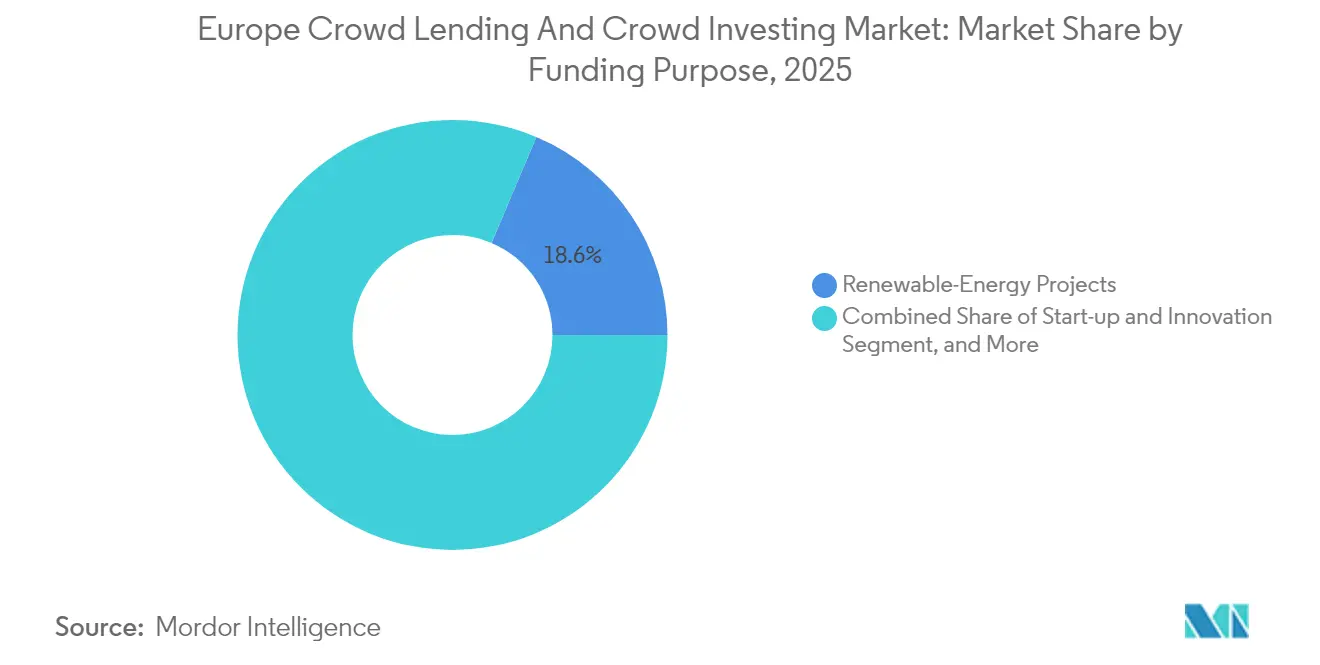

- By funding purpose, renewable-energy projects accounted for an 18.62% of the Europe crowd lending and crowd investing market share in 2025, and are advancing at a 2.85% CAGR through 2031.

- By investor type, institutional and family-office capital is projected to grow at a 2.93% CAGR to 2031, while sophisticated retail investors retained 13.70% of the Europe crowd lending and crowd investing market share in 2025.

- By geography, Lithuania posted the fastest trajectory with a 2.06% CAGR between 2026-2031, whereas the United Kingdom preserved a 14.50% of the Europe crowd lending and crowd investing market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Crowd Lending And Crowd Investing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone-enabled onboarding and embedded-finance APIs | +0.3% | Nordic and Baltic regions | Short term (≤ 2 years) |

| PSD2 / SEPA Instant rails lowering payment friction | +0.4% | Germany, Netherlands, pan-EU | Medium term (2-4 years) |

| ECSPR passporting accelerates cross-border scale-up | +0.5% | All EU except UK, Switzerland | Medium term (2-4 years) |

| Real-estate crowdlending replacing mezzanine loans | +0.2% | United Kingdom, Germany, France | Long term (≥ 4 years) |

| SME green-transition mandates | +0.3% | Germany, Netherlands, France, wider EU | Long term (≥ 4 years) |

| Tokenized debt instruments and fractional liquidity | +0.1% | Germany, Netherlands, Switzerland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smartphone-enabled onboarding and embedded-finance APIs

Ubiquitous smartphone penetration allows borrowers and investors to complete identity verification, risk profiling, and funding transactions in minutes, driving rapid user acquisition for Baltic and Nordic platforms. Open-banking APIs let these providers embed white-label lending flows into third-party financial services apps, increasing distribution with minimal incremental customer-acquisition cost.[1]De Nederlandsche Bank, “Banking-as-a-Service,” dnb.nl The user experience improvement shortens the funnel from account creation to loan commitment, raising conversion ratios that boost origination volume. Instant digital KYC processes built on government e-ID frameworks further streamline compliance. Collectively, these factors add an estimated 0.3 percentage points to the market CAGR by widening the addressable audience. Competitive differentiation is shifting from headline yield toward seamless omnichannel access, pushing laggard platforms to upgrade their mobile stacks.

PSD2 / SEPA Instant rails lowering payment friction

Payment Services Directive 2 mandated access to customer bank data for licensed third parties, while the SEPA Instant Credit scheme delivers near-real-time euro transfers. Together, they compress settlement cycles from two to three days to under ten seconds, materially improving cash-flow timing for SMEs and investor reinvestment velocity.[2]European Investment Fund, “EIF Invests EUR 200 Million in Green Private Credit Fund,” eif.org Dutch analyses show that instant rails reduce transaction abandonment by 18% when compared with legacy batch payments. Faster cash recycling increases platform revenue because servicing fees accrue sooner, and it reduces idle balance risk. The harmonized payment layer also supports multijurisdictional scaling, making regional expansion less operationally complex. As uptake grows, platforms can price liquidity premiums more competitively, reinforcing a 0.4 percentage-point uplift to long-run growth.

ECSPR passporting accelerates cross-border scale-up

Since November 2023, any provider licensed under ECSPR can solicit investors and borrowers across the European Economic Area without additional national approvals, removing the patchwork regime that previously fragmented demand. Lithuanian platforms, for example, grew aggregate funding from EUR 230 million in 2023 to a projected EUR 300 million in 2024 after opening German and Spanish investor funnels. Passporting also allows specialized lenders to match-fund niche borrowers-such as small-scale wind projects, in markets where local volume would otherwise be insufficient. Marketing and disclosure documents now follow one common template, lowering legal spend per new country. These efficiencies contribute roughly 0.5 percentage points to CAGR, making regulatory alignment the single largest structural tailwind through 2030.

Real-estate crowd-lending replacing mezzanine bank loans

Property developers increasingly substitute mezzanine bank tranches with high-coupon platform debt to maintain leverage ratios in a tight-credit cycle. In Western Europe, yields sit 400-600 basis points above senior mortgages yet remain cheaper than private-equity equity slugs, making the product attractive on both sides of the marketplace. United Kingdom originations rose in late 2024 despite macro headwinds because top-tier platforms underwrite low-loan-to-value portfolios and release funds in construction drawdowns. As banks retreat from speculative residential projects due to Basel III capital charges, crowdlenders occupy the gap and secure first-loss protection via junior equity buffers. The secular shift sustains a 0.2 percentage-point boost to growth, especially in urban infill and brownfield redevelopment niches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ECB rates eroding yield advantage | -0.6% | Eurozone | Short term (≤ 2 years) |

| Macro-cycle default spikes in consumer credit | -0.4% | Southern Europe | Short term (≤ 2 years) |

| Crowdfunding fraud scandals reduce trust | -0.2% | France, Germany | Medium term (2-4 years) |

| Country-by-country MiFID II marketing caps | -0.3% | All EU members | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising ECB rates eroding platform yield advantage

Between early 2022 and October 2024, the ECB deposit facility moved from -0.50% to 3.75%, compressing the rate spread that once underpinned retail appetite for platform loans. When German term deposits began paying 2.5%, consumer lenders could no longer charge borrowers 14-15% without incurring unsustainable default risk. Yield-seeking capital, therefore, migrated to money-market funds, dragging platform funding volumes 25% lower quarter-on-quarter in Italy and Spain. Operators responded by cutting marketing budgets and tightening credit scores, yet those defensive moves limit top-line growth. Analysts estimate the headwind subtracts 0.6 percentage points from aggregate CAGR over the next two years until rate normalization resumes.

Crowdfunding fraud scandals are reducing investor trust.

The 2024 shutdown of 181 fraudulent investment websites by the French Financial Markets Authority underscored persistent due diligence gaps.[3]French Financial Markets Authority, “AMF Shuts Down 181 Fraudulent Investment Websites in 2024,” amf-france.org The high-profile EUR 645 million JuicyFields Ponzi scheme further dented sentiment, especially among first-time retail investors. Platforms responded with escrow segregation and third-party trustee structures, but onboarding conversion still fell 12% in France relative to pre-scandal baselines. ECSPR’s harmonized disclosure may rebuild confidence, yet reputational damage lingers and carries an estimated -0.2 percentage-point drag on medium-term growth. Investor-compensation schemes and fit-and-proper tests for platform managers raise compliance costs, making scale even more critical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Debt Leadership and Tokenized Upside

Debt-based platforms originated loans worth USD 2.7 billion in 2025, equivalent to 19.75% of the Europe crowd lending and crowd investing market share. Stable fee income and clearer legal treatment under ECSPR should sustain a 2.06% CAGR for this cohort to 2031. Equity crowd-investing trails because MiFID II categorizes many offerings as transferable securities, increasing prospectus costs and cooling supply. Tokenized securities, however, are pacing for a 2.75% CAGR as Berlin Hyp’s EUR 100 million blockchain Pfandbrief validated institutional demand for on-chain settlement. Over the outlook horizon, hybrid revenue-share models will likely remain below 5% of the Europe crowd lending and crowd investing market size due to limited secondary-market liquidity.

The operating-margin profile also favors debt platforms, whose servicing revenue compounds over multiyear amortization schedules. By contrast, equity portals derive most income upfront and must continually replenish deal inventory. Tokenized debt instruments add optionality because they create tradable slices that attract market-making activity; early pilots indicate bid-ask spreads under 50 basis points once loan pools exceed EUR 5 million. Overall, debt’s embedded scale economies cement its lead, but tech-driven niches will capture incremental wallet share among institutional allocators.

By Borrower Type: SME and Property Dominance

SME and real-estate borrowers secured 43.12% of the total 2025 originations, the largest slice of the Europe crowd lending and crowd investing market. These cohorts are forecast to compound at 3.58% because mandatory ESG retrofits, electrification, and energy-efficiency upgrades drive relentless funding needs. Consumer-credit verticals remain sizeable but face sharper default risk in Southern Europe, where unemployment crossed 9% in 2024. Platforms now apply tighter debt-to-income caps and dynamic pricing algorithms, which restrain volume expansion but protect loan books.

Business lending’s average ticket size of EUR 125,000 produces superior unit economics relative to sub-EUR 5,000 consumer advances, allowing platforms to amortize fixed underwriting costs across larger balances. Risk-weighted-asset relief that banks obtain from securitizing green SME pools creates syndication exit paths, further reinforcing the segment’s pull. Conversely, real-estate delays in France highlight construction-cycle sensitivity; still, mezzanine demand persists because developers prefer crowd debt over equity dilution when margins compress.

By Funding Purpose: Renewable Energy Outpaces All Segments

Renewable-energy projects represented 18.62% of 2025 volumes and carry the quickest outlook ascent at 2.85% CAGR, outstripping real-estate development, SME working-capital, and personal-finance loans. Solar rooftop aggregators in Germany and Poland structure ABS take-outs at scale, giving platforms a programmatic exit. Feed-in-tariff longevity and predictable kilowatt-hour cash flows appeal to pension funds seeking natural-rate hedges. Real estate still corners the absolute leader slot in dollars lent, but permitting delays and building-cost inflation shaved its contribution by 24.9% in France during the first half of 2024.

Going forward, regulatory carbon budgets intensify project pipelines for energy-efficiency retrofits in commercial buildings. These initiatives qualify for EU taxonomy labeling, making them bankable with subordinated crowd tranches. Start-up and innovation funding will likely remain volatile, tied to venture-capital cycles, whereas debt-consolidation niches lose relative appeal once ECB rates normalize.

By Investor Type: Institutional Influx Changes Liquidity Dynamics

Sophisticated retail investors controlled 13.70% of originations in 2025, but institutional and family-office money is climbing at a forecast 2.93% CAGR, encouraged by EIF’s USD 217 million green private-credit mandate. Insurance companies, for instance, use short-duration SME pools to match liability gaps without breaching Solvency II constraints. Non-sophisticated retail segments face tighter exposure caps under MiFID II, trimming their share of future inflows.

Institutional participation demands higher data granularity; hence, platforms invest in IFRS-compliant reporting dashboards and scenario-analysis toolkits. Secondary-market liquidity is slowly improving through tokenized notes that fractionalize repayment streams into EUR 100 lots, widening the buy-side base. As the professional cohort’s share rises, average loan tenors extend and coupon dispersion narrows, pushing platforms toward specialized origination where underwriting edge is defensible.

Geography Analysis

The United Kingdom preserved 14.50% of aggregate 2025 volumes, leveraging legacy brand equity from first-wave fintech adoption despite forfeiting ECSPR passport rights after Brexit. Top players such as Funding Circle emphasize co-lending programs with regional banks to maintain pipeline density, while Zopa’s December 2024 USD 87 million raise earmarks generative-AI risk models for eventual re-entry into continental markets. Domestic consolidation is brisk; 70 M&A deals closed in 2024 as compliance overheads rose.

Germany functions as the gravitational center for green-energy debt. Enpal securitized EUR 100 million of rooftop-solar receivables under EIB credit enhancement, setting a template replicated by heat-pump financiers. Fast-track permitting reforms could unlock a EUR 5 billion annual pipeline by 2027, underscoring Germany’s strategic relevance to the Europe crowd lending and crowd investing market.

France saw a 24.9% year-on-year drop to EUR 830 million in H1 2024 because 15-20% of property developments slipped beyond six-month delay thresholds. However, AMF’s clampdown on fraud buttressed long-run credibility by expelling 181 rogue portals. In parallel, Lithuania booked a 2.06% CAGR outlook thanks to streamlined licensing and a 48% reduction in active platforms, enabling survivors to tap Western European investors at a lower acquisition cost.

Poland exemplifies emerging-market upside via synthetic securitizations. Inbank’s PLN 625 million (USD 156 million) program finances solar and heat-pump installations, signaling institutional comfort with local credit infrastructure. The Netherlands and Spain capitalize on PSD2 instant rails, improving cash recycling for SME borrowers. Overall, geographic growth corridors align with regulatory agility, green-finance incentives, and digital-ID penetration.

Regulatory Landscape

Europe crowd lending and crowd investing operates under the European Crowdfunding Service Providers Regulation (ECSPR), Regulation (EU) 2020/1503, which sets a harmonized framework for both investment-based and lending-based crowdfunding across the EU. Under ECSPR, ESMA maintains a public register of authorized crowdfunding service providers (CSPs), and a single authorization in one Member State enables cross-border passporting across EU markets through the home National Competent Authority (NCA), replacing the earlier fragmented national regimes.

Investor-protection and offer-structure rules drive much of the compliance burden and shape the operating model. Key requirements include the Key Investment Information Sheet (KIIS), mandatory knowledge testing and loss-bearing simulations for non-sophisticated investors, and governance, risk management, and supervisory cooperation requirements implemented through Level 2 RTS/ITS and delegated acts. ECSPR also caps in-scope fundraising at EUR 5 million per project calculated over 12 months, which pushes larger rounds into MiFID II/prospectus pathways and influences platform product design and borrower selection, particularly for SME and real-estate SPV funding.

Value Chain Analysis

The value chain starts with borrower and project origination (SMEs, real-estate SPVs, and renewable-energy developers) and investor acquisition across retail, sophisticated retail, and institutional channels. It then moves into underwriting, credit scoring, pricing, and disclosure production aligned to ECSPR templates (including KIIS). Platforms sit at the orchestration layer, integrating digital onboarding, e-ID/KYC and AML controls, open-banking connectivity, and payment execution via PSD2 access and SEPA Instant rails, followed by disbursement, servicing, collections, and investor reporting that must meet standardized transparency and risk-management expectations.

Downstream, funding continuity is increasingly supported by institutional capital structures such as forward-flow agreements and securitizations that recycle receivables and reduce balance-sheet intensity for leading platforms. Custody/nominee arrangements (where used) and trustee-like structures help manage investor ownership records and cash segregation, while secondary liquidity experiments, including tokenized notes, extend the distribution layer for certain products. A key structural bottleneck remains the EUR 5 million ECSPR project cap, which constrains larger borrowers and redirects more mature issuers toward MiFID II/prospectus routes; at the same time, ESMA and NCA supervision raises fixed compliance costs that favor scaled operators and accelerate consolidation.

Competitive Landscape

Regulatory harmonization and higher interest-rate carry compress gross spreads, making operational scale the decisive moat. Lithuania’s top three platforms already command roughly 30% national volume following ECSPR rollout, illustrating the consolidation arc. Larger Western European incumbents leverage balance-sheet lending and forward-flow partnerships with asset managers to smooth origination cycles. AI-driven credit-decision engines cut manual underwriting time 40%, freeing resources for customer-service differentiation.

Strategic technology upgrades center on embedded-finance rails: APIs allow banks to outsource niche loan verticals under a white-label model, capturing fee income without direct risk. Meanwhile, tokenization pilots executed by Berlin Hyp and OpenBrick entice institutions that once avoided illiquid private credit. Cross-border M&A is set to intensify because passporting unlocks immediate revenue synergies once compliance playbooks align. The Europe crowd lending and crowd investing market, therefore, resembles a barbell, with a handful of pan-regional leaders on one end and specialized vertical-niche players on the other, while mid-tier generalists struggle.

Europe Crowd Lending And Crowd Investing Industry Leaders

Funding Circle Holdings plc

Zopa Bank Limited

LendInvest plc

Crowdcube Limited

Mintos Marketplace AS

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Cross-border scaling under ECSPR passporting creates room for platforms that can industrialize multi-country distribution, onboarding, and reporting while keeping investor protections consistent across jurisdictions. ESMA authorization registers and market monitoring point to a sizeable regulated platform base (with hundreds of ECSPR-licensed entities referenced across EU datasets), and activity concentrates in a limited set of countries, leaving space to deepen penetration in under-served markets. The most practical route is localized borrower acquisition paired with pan-EU investor funnels.

On the product and funding-model side, opportunities cluster around infrastructure that institutional investors rely on, including standardized data packs, risk analytics, and repeatable take-out structures. Evidence within the research perimeter includes continued supervisory focus on harmonized disclosures (KIIS) and governance, alongside EU-level green-finance programs such as the European Investment Fund (EIF) partnership program announced in 2025 to share credit risk for renewable-energy and other green projects. Tokenized debt and fractional liquidity remain development areas within the ECSPR perimeter, while the EUR 5 million per-project limit continues to shape addressable deal size. That constraint affects how platforms build pipelines and syndication structures, either keeping projects within ECSPR scope or routing larger offerings through MiFID II/prospectus channels.

Recent Industry Developments

- June 2026: Funding Circle completed its tenth public securitisation of investor loans (SBOLT 2026-1), marking a decade of issuance and bringing cumulative public securitisation issuance to GBP 2.5 billion. British Business Bank participated for the first time, reinforcing the role of public and quasi-public capital in scaling marketplace loan funding. The transaction supports a more repeatable funding stack for SME loan origination beyond purely retail investor flows.

- May 2026: Zopa Bank received FCA approval to offer retail investment services under a new UK regulatory regime that took effect on April 6, 2026. The approval extends Zopa beyond lending and savings into investments, widening the addressable customer wallet and increasing competitive intensity for platforms serving sophisticated retail investors. It also signals regulatory maturation for app-led investment distribution that can be paired with embedded finance and marketplace credit products.

- September 2025: The second phase of the EU Markets in Crypto-Assets (MiCA) rules entered into force, providing a clearer rulebook for crypto-asset activities relevant to tokenization and settlement experimentation. For crowd-lending and crowd-investing platforms, the change supported exploration of tokenized loan notes and stablecoin-enabled cross-border payment workflows alongside ECSPR-compliant disclosures. This regulatory clarity advanced product-design options for platforms exploring digital securities within Europe.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market captures the value of funds raised through European online platforms that match investors with borrowers or issuers, covering crowd lending and crowd investing transactions completed in the region and reported in monetary terms.

Scope exclusions: We exclude donation and reward crowdfunding, and we also exclude traditional bank loans and private placements that do not originate through crowdfunding-style platforms.

Segmentation Overview

- By Business Model

- Debt-based Crowdlending

- Equity-based Crowd Investing

- Revenue-share / Royalty

- Tokenised Securities

- By Borrower Type

- Business (SME and Real-Estate SPV)

- Consumer

- By Funding Purpose

- Real Estate Development

- Renewable-Energy Projects

- SME Working-Capital and CapEx

- Start-up and Innovation

- Personal Finance and Debt-Consolidation

- By Investor Type

- Retail (Non-Sophisticated)

- Sophisticated Retail

- Institutional and Family-Office

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Lithuania

- Poland

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping what counts as a platform-enabled origination in Europe, and then aligning that to how activity is reported in public sources. We used official materials that anchor definitions and volumes, including European Securities and Markets Authority (ESMA) crowdfunding market reports, European Commission publications on the European Crowdfunding Service Providers Regulation (ECSPR), and European Central Bank (ECB) rate and macro series that influence investor yield expectations.

To make country patterns easier to validate, we also reviewed national regulator updates and registers where available, such as national financial supervisors, along with association pages and platform disclosures that show originations, default commentary, and investor mix at a high level. Supporting context was taken from company filings, investor presentations, and reputable press coverage. We used a paid subscription database selectively for company financials and patent lookups when specific product feature claims needed clarification. The desk sources listed above are illustrative, and we also relied on other public sources for data collection, cross-checking, and clarifying assumptions.

Primary Interviews and Surveys

Primary work focused on validating what share of volume is genuinely platform-originated, how lending versus investing is counted, and how fast cross-border activity is expanding under ECSPR. We spoke with platform operators, investor-facing intermediaries, and risk or compliance professionals across major European markets, then used the inputs to stress-test desk assumptions such as active investor behavior and typical deal sizes.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | |

| Mid tier: 46% | Functional/Unit leaders: 41% | |

| Smaller Players: 22% | Managers: 46% |

Market-Sizing & Forecasting

The model begins with a top-down build that reconstructs platform origination in Europe using regulated activity signals, country-level adoption patterns, and macro drivers that shape demand for alternative finance. Once the core demand pool is set, we corroborate it with selective bottom-up approximations, such as sampling typical average ticket sizes times deal counts from disclosures, plus channel checks on how volumes are split between consumer, SME, and real estate-linked financing.

Inputs treated as practical sizing fingerprints include the number of active authorized providers by country, observed lending-versus-equity mix, typical project sizes by use (for example, real estate development versus SME working capital), investor participation trends (retail versus more sophisticated investors), and the interest rate environment that affects fundraising success and reinvestment rates. Forecasting uses scenario analysis driven by these factors, where base-case paths are reviewed with primary respondents to confirm what feels realistic for originations, risk appetite, and cross-border scaling. When bottom-up visibility is weak for smaller markets, gaps are handled by applying country analogs with similar regulation maturity and platform density, then applying a final adjustment after interview feedback.

Data Validation & Update Cycle

Validation runs in several passes so the numbers stay explainable. We compare outputs against independent signals such as official EU crowdfunding volumes, authorization counts, and clear inflection points tied to rates or regulation, then review outliers before sign-off. If a country total shifts too sharply without a matching external signal, we revisit assumptions, and in some cases re-contact respondents to confirm what actually changed.

Each report is refreshed annually, and interim updates are triggered when there are material events, such as major regulatory shifts, platform exits, or sudden funding contractions in a key country. Before delivery, an analyst runs a final update pass so the published market size reflects the latest available public and interview-backed inputs.

Mordor Intelligence's Europe Crowd Lending and Crowd Investing Market Size Compared With Other Published Estimates

Published estimates for this market often differ because the underlying definition is not always consistent. The most common gaps come from geography coverage and what is counted as a qualifying platform transaction. Currency timing and the treatment of cross-border activity can also change reported totals even when the overall narrative is similar.

Key gap drivers are usually practical rather than complex. Some estimates lean on EU-only regulated volumes, which can understate totals if non-EU European countries are included in another scope. Others fold in adjacent models such as reward crowdfunding or broader fintech lending that does not meet a platform origination test. Differences also show up in how average deal sizes are projected forward, whether the base case assumes stable reinvestment rates after rate changes, and how often the dataset is refreshed when authorization lists and platform reporting change.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.68 B (2025) | |

| EU Regulator Dataset A | USD 4.64 B (2024) | This figure reflects EU reported volumes under the ECSPR reporting perimeter, so it is narrower than a Europe-wide view and is sensitive to the ramp-up of licensing and reporting coverage by member state. |

| Trade Index B | USD 3.49 B (2025) | This estimate is typically based on tracked P2P lending investment volumes only, which can exclude equity crowdfunding, omit parts of institutional flows, and rely on partial platform reporting or voluntary disclosures. |

The table shows a wide spread that mainly comes from what gets included in the measured transaction pool. In Mordor Intelligence's model, the count is built to cover both crowd lending and crowd investing across Europe, rather than only ECSPR-reported EU volumes or P2P lending investment trackers. With that scope clarified, the remaining differences are mostly due to refresh cadence and how deal size and cross-border momentum are carried into the base year.

Key Questions Answered in the Report

What is the projected value of the Europe crowdlending market in 2031?

The market is forecast to reach USD 15.17 billion by 2031, reflecting a 1.74% CAGR from 2026.

How does ECSPR passporting benefit platforms?

A single license now grants access to 27 EU jurisdictions, cutting legal costs and enabling smaller Baltic and Nordic providers to tap larger Western European investor pools.

Which segment is growing fastest within European crowdlending?

Renewable-energy project financing shows the highest outlook, advancing at a 2.85% CAGR on the back of EU Green Deal mandates.

Why are institutional investors increasing their allocations?

Yield premiums over corporate bonds, ESG-aligned opportunities, and improved reporting standards entice pension funds, insurers, and family offices to enter the market.

How have rising ECB rates affected platform economics?

Higher deposit rates have shrunk the historical 300-400 basis-point yield premium to 150-200 points, prompting platforms to focus on efficiency and specialized niches.

Page last updated on: