Europe Cosmetic Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

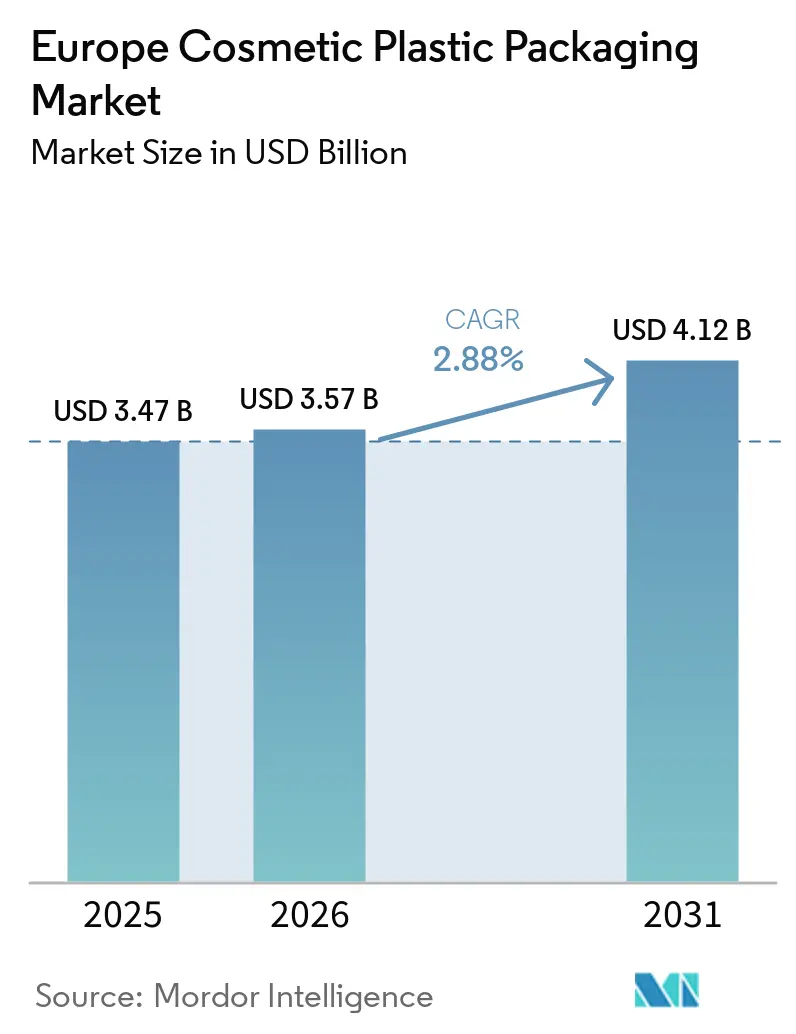

| Base Year Market Size (2025) | USD 3.47 Billion |

| Market Size (2026) | USD 3.57 Billion |

| Market Size (2031) | USD 4.12 Billion |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

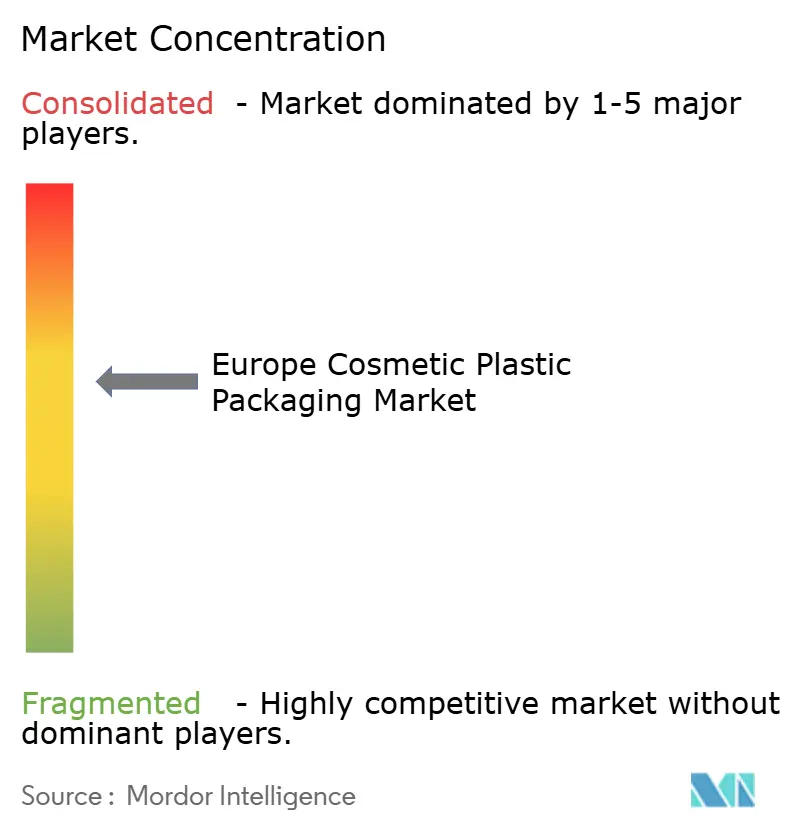

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cosmetic Plastic Packaging Market Analysis by Mordor Intelligence

Europe cosmetic plastic packaging market size in 2026 is estimated at USD 3.57 billion, growing from 2025 value of USD 3.47 billion with 2031 projections showing USD 4.12 billion, growing at 2.88% CAGR over 2026-2031. Moderate topline expansion masks deep structural change as circular-economy regulations, cost-inflation shocks, and premiumization trends reshape supply chains across every value-adding node of the Europea cosmetic plastic packaging market. Companies that pre-invest in compliance infrastructure, mono-material design libraries, and closed-loop recycling alliances already report faster quoting cycles, lower EPR liabilities, and superior customer retention, underscoring how regulation has become a competitive variable equal to aesthetics and unit cost. Germany’s mature extended-producer responsibility (EPR) framework, Spain’s Next Generation EU-funded recycling build-out, and France’s PFAS phase-out illustrate how local policy variance multiplies complexity yet also opens geographic white-space for agile suppliers. Digital printing, refillable systems, and tethered-cap engineering are the three technology clusters with the clearest line-of-sight to margin expansion inside the European cosmetic plastic packaging market, particularly as indie labels and prestige houses adopt shorter innovation cycles that commoditize conventional long-run packaging.

Key Report Takeaways

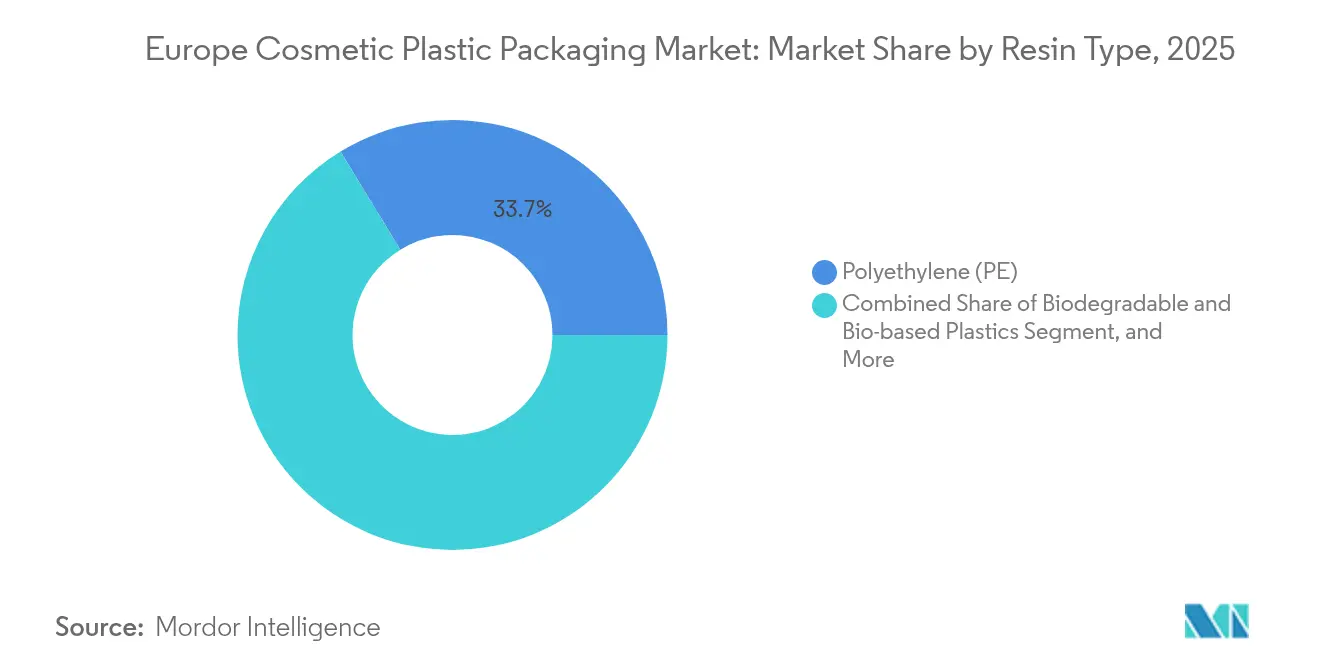

- By resin type, polyethylene led with 33.72% of the Europe cosmetic plastic packaging market share in 2025; biodegradable plastics are set to expand at a 4.55% CAGR to 2031.

- By product type, bottles captured 32.10% revenue share in 2025, while tubes and sticks are forecast to post the fastest 3.55% CAGR through 2031.

- By application, skin care accounted for 38.35% share of the Europe cosmetic plastic packaging market size in 2025, whereas makeup is advancing at a 4.66% CAGR to 2031.

- By sustainability profile,conventional formats still 67.60% share of the Europe cosmetic plastic packaging market size in 2025, whereas sustainable packaging volumes grow 6.55% CAGR to 2031.

- By country, Germany held 21.05% share of the Europe cosmetic plastic packaging market size in 2025; Spain shows the highest 6.74% CAGR outlook through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Cosmetic Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation of skin-care and dermo-cosmetics | +0.7% | Germany, France, UK core markets | Medium term (2-4 years) |

| Rise of refill/re-use business models in prestige beauty | +0.5% | Western Europe, expanding to Central Europe | Long term (≥ 4 years) |

| Brand-owner commitments to ≥50% PCR plastics by 2030 | +0.6% | EU-wide, UK alignment expected | Medium term (2-4 years) |

| Rapid growth of indie brands using short-run digital printing | +0.3% | Germany, France, Netherlands innovation hubs | Short term (≤ 2 years) |

| EU Single-Use Plastics Directive catalysing design change | +0.4% | All EU member states | Medium term (2-4 years) |

| Adoption of tethered caps ahead of 2024 deadline | +0.2% | EU-wide compliance requirement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumisation of Skin-Care and Dermo-Cosmetics

Clinical skin-care lines require airless pumps and vacuum chambers that safeguard unstable actives, lifting packaging cost-per-unit by 25-40% yet allowing brands to preserve 40-60% margin premiums. German and French consumers display the strongest willingness to pay for dermatologically validated formats, turning those two countries into anchor markets for high-spec packaging. Leading converters such as Gerresheimer reported EUR 1.9 billion (USD 2.05 billion) revenue in 2024, citing 15% cosmetic growth linked to barrier-enhanced plastic systems. EMA guidance blurs the cosmetic-pharma boundary, compelling suppliers to document leachables and extractables, which further cements the role of precision injection-molding and specialty resins. Over the medium term, premiumization is expected to add 0.7 percentage points to the Europe cosmetic plastic packaging market CAGR as more mass manufacturers launch quasi-pharma sub-brands.

Rise of Refill/Re-Use Business Models in Prestige Beauty

Prestige houses are switching to refill pods and cartridges that slash virgin-plastic intensity by up to 85%, a shift accelerated by EPR fee rebates tied to re-use ratios. Luxury brands recover the higher capex for reverse logistics through SKU lock-in and 30-50% price premiums on initial pack purchases. Quadpack logged 25% revenue growth from refill formats in 2024, and major maisons target 60% refillable penetration by 2027. NFC-enabled authentication extends the consumer journey while furnishing regulators with auditable data on reuse cycles. Although roll-out costs slow mid-market adoption, long-term (≥ 4 years) impact is pegged at +0.5 percentage points for the Europe cosmetic plastic packaging market.

Brand-Owner Commitments to ≥50% PCR Plastics by 2030

EU mandates (30% recycled content in PET bottles and 35% in other plastics) dovetail with voluntary pledges, producing structural PCR undersupply that inflates recycled-resin spot prices 20-40% above virgin equivalents. L’Oréal missed its 50% recycled-plastic target in 2024 due to color-matching and food-grade constraints. Large converters respond by acquiring recyclers and investing in chemical depolymerization despite higher energy intensity. The scramble for feedstock adds 0.6 percentage points to market growth as brand owners lock in multi-year contracts—thereby guaranteeing volume for compliant packaging suppliers inside the Europe cosmetic plastic packaging market.

Rapid Growth of Indie Brands Using Short-Run Digital Printing

Digital presses have cut minimum order quantities from 25,000 to under 1,000, enfranchising indie labels that prize agility. HCP Packaging recorded 40% growth in digitally printed cosmetic components in 2024 and a fall in average run size to 8,000 units. Variable-data artwork drives limited editions that spike social media engagement, while near-shoring print to EU facilities simplifies regulatory labeling and shortens lead times. The effect is immediate: +0.3 percentage points to CAGR over the next two years for the Europe cosmetic plastic packaging market as traditional converters retrofit lines to stave off share erosion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven material cost spikes squeezing converters | -0.4% | EU-wide, particularly hitting smaller converters | Short term (≤ 2 years) |

| Retailer "no-plastics" private-label pledges | -0.3% | UK, Germany, France retail concentration | Medium term (2-4 years) |

| Limited recycling streams for coloured/multilayer PET | -0.2% | Central and Eastern Europe infrastructure gaps | Long term (≥ 4 years) |

| Rising EPR fees for non-recyclable packs | -0.4% | Germany, France, Netherlands leading implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Material Cost Spikes Squeezing Converters

Polyethylene price volatility of 18-25% during 2024 wiped 8-12% off converter gross margins, as outlined by European Central Bank industrial price data. Smaller firms lacking hedging programs were forced into M and A or market exit, fuelling consolidation that has lifted the Herfindahl-Hirschman Index by 11 % since 2023. Electricity-intensive recycling operations faced twin pressure from energy tariffs and feedstock scarcity, temporarily dampening PCR usage despite regulatory incentives. Until spot prices normalize, the restraint subtracts 0.4 percentage points from near-term growth in the Europe cosmetic plastic packaging market.

Rising EPR Fees for Non-Recyclable Packs

Germany’s fee of up to EUR 1,800 (USD 1,944) per tonne for complex multilayer packs shifts the cost equation decisively toward mono-material alternatives. France followed with a 35% uptick in EPR collections in 2024 once modulation became recyclability-indexed. The financial shock forces smaller brands to pay punitive levies while redesigning SKUs, delaying innovation budgets, and compressing packaging volumes. This dynamic subtracts another 0.4 percentage points from the Europe cosmetic plastic packaging market CAGR through 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Biodegradable Materials Challenge Polyethylene Dominance

Polyethylene continues to underpin 33.72% of 2025 volumes, reaffirming its cost-performance balance across bottles, caps and flexible films in the Europe cosmetic plastic packaging market. Yet biodegradable plastics are rising 4.55% annually, their advance linked more to EPR fee relief and corporate scorecard metrics than to absolute cost advantage. Europe cosmetic plastic packaging market size tied to biodegradable grades is forecast to reach USD 0.64 billion by 2031, propelled by PHA’s superior moisture barrier relative to PLA for lotions and wipes. Production capacity, however, remains 2.4 million tonnes across all uses, a mismatch that sustains price premiums of 2-3× over PE.

The Europe cosmetic plastic packaging market pivots further as converters experiment with enzymatic depolymerization of cellulose blends to match PET-like clarity while matching compostability standards. Patent activity validates momentum: 127 biodegradable-packaging patents were granted in 2024, 35% of them cosmetic-focused. As brand owners publicize recycled-content progress, chemical compatibility tests intensify, especially for retinoid serums, where monomer migration risk remains tightly regulated. Because EPR schemes reward mono-material PE tubes and jars that incorporate PCR, polyethylene still expands in absolute tonnage even as share slips to an anticipated 30.1% by 2031.

By Product Type: Digital Innovation Drives Tube Growth

Bottle formats keep 32.10% share through their ubiquity in shampoos, micellar waters, and body lotions, but average wall thickness is declining under light-weighting programs, trimming resin usage per unit by 8-12%. Digital print adoption transforms tubes and sticks into the fastest-growing 3.55% CAGR cohort, providing bespoke graphics for seasonal drops and influencer capsules across the Europe cosmetic plastic packaging market. The Europe cosmetic plastic packaging market size attributable to tubes will add nearly USD 0.16 billion between 2026 and 2031 as indie brands favor MOQ-friendly runs.

Airless pumps, once a luxury exclusive, migrated into mid-tier acne treatments in 2024, widening the addressable base for precision components. However, the EU tethered-cap rule is compelling a rethink of hinge geometry for flip-top dispensers under 3 liters, escalating tooling spends by 20-25%. Pouches, historically niche in hair-conditioner refills, now capture eco-trade-up consumers, given 25-35% material savings versus rigid bottles. Still, recyclability trade-offs for barrier laminates temper momentum outside high-return-rate markets such as Germany.

By Application: Makeup Premiumization Accelerates Growth

Skin care remains anchor revenue at 38.35% share because facial cleansers, moisturizers, and SPF hybrids are daily-use staples that absorb packaging innovations at scale. Yet makeup’s 4.66% CAGR highlights shifting generational priorities. Gen Z regards lipstick cartridges as fashion statements, fueling interest in magnetized refill cores that cut single-use resin by 70% per life-cycle. Europe cosmetic plastic packaging market share for makeup formats is expected to move from 19.45% in 2025 to 22.85% by 2031, outpacing all other applications.

Hair care packaging shows mid-single-digit growth, anchored in concentrated powders and solid shampoos that ship in fiber-based sleeves. EU aerosol regulations exert pricing pressure on deodorants and fragrances, nudging innovation toward gas-free pump mechanisms supported by Aptar’s HDP all-plastic pump introduced in July 2024. Dermatological cross-overs think SPF-loaded foundations blur application taxonomy, pushing converters to create universal component libraries that accept multiple formula viscosities.

By Sustainability Profile: Regulatory Pressure Drives Transition

Conventional formats, still 67.60% of 2025 units, shrink incrementally as fee modulation narrows the price gap with eco-design. Sustainable packaging volumes grow 6.55% annually, unlocking USD 0.43 billion of incremental Europe cosmetic plastic packaging market size by 2031. However, lifecycle-analysis debates complicate procurement choices: bio-resin carbon footprints vary by agricultural practice, and paper-plastic hybrids challenge downstream sortation. Mono-material PE tubes with EVOH-free barriers are emerging as the consensus compromise, achieving 97% recyclability in German DSD streams.

Consumer willingness to pay a premium remains highest in luxury channels, enabling Albéa to invest EUR 45 million (USD 48.6 million) in sustainable R and D during 2024 and to launch 40% of new SKUs with bio-based or recycled inputs.In mass retail, compliance deadlines rather than consumer pull dictate adoption speed, positioning contract packagers with dual-line capability standard and sustainable to arbitrage timing mismatches across brand portfolios.

Geography Analysis

Germany controlled 21.05% of market revenue in 2025 thanks to a transparent fee matrix that prices non-recyclable packs up to EUR 1,800 per tonne, steering design toward PET and PE mono-structures that achieve the highest recycling rates. Its recycling ecosystem processed 14.2 million tonnes of packaging waste in 2024, enabling closed-loop sourcing deals between converters and CPG majors. Government-funded pilot plants for PHA fermentation and depolymerization signal future growth avenues, while engineering consultancies export local best practice across the continent.

Spain’s 6.74% CAGR outlook stems from EUR 2.1 billion (USD 2.27 billion) circular-economy allocations under Next Generation EU, with 35% earmarked for packaging. Collection targets now mirror Germany’s but operate at lower labor costs, making the Iberian Peninsula an emerging hub for regional consolidation. Spanish converters also leverage logistics corridors to North Africa and Latin America, capturing export synergies rarely achievable from Northern Europe manufacturing bases.

France’s ban on PFAS in cosmetics, effective January 2026, obliges rapid reformulation and packaging validation. ADEME recorded a 15% rise in sustainable-pack adoption during 2024, as companies pre-empt legislative risk. Italy’s CONAI consortium sustains 76.7% packaging-recycling performance, reinforcing supply security for PCR PET flake that cosmetics share with beverage verticals. The United Kingdom, diverging post-Brexit, levies a GBP 223.69 (USD 280.46) per tonne plastic tax above 30% virgin content. Converters serving both EU and UK now dual-certify packs, absorbing extra compliance overhead but widening addressable demand.

Competitive Landscape

The Europe cosmetic plastic packaging market displays moderate concentration. The top five players account for roughly 42% of regional turnover. Amcor’s USD 7.3 billion in 2024 packaging sales exemplify scale economies: diversified resin sourcing cushions inflation while internal recycling assets lock in PCR availability.[3]Amcor plc, “Annual Report 2024,” amcor.com Gerresheimer accelerated inorganic expansion by acquiring Bormioli Pharma for EUR 180 million (USD 194 million) to deepen its luxury-glass and high-barrier plastics capability. Quadpack winning B-Corp status signals that verified ESG credentials increasingly determine tender outcomes with prestige brands.

Horizontal alliances also proliferate: Berlin Packaging’s partnership with Vetropack offers turnkey glass and hybrid solutions that meet retailer no-plastics pledges without surrendering design flexibility. Technology is a second axis of competition. Aptar’s HDP mono-material pump removes metal springs, unlocking full recyclability, while Silgan Dispensing rolled out similar single-polymer dosage systems to maintain speed-to-market parity. Digital platforms further differentiate: suppliers integrate RFID labels into compacts to satisfy traceability clauses under the forthcoming EU Packaging and Packaging Waste Regulation.

Patent momentum corroborates innovation intensity. The European Patent Office issued 89 cosmetic-packaging patents in 2024, 42% on sustainable materials. ISO 14006 eco-design certification emerges as a table-stake in frame agreements with multinational cosmetics groups, reinforcing the commercial link between audit-ready sustainability credentials and preferred-supplier status in the Europe cosmetic plastic packaging market.

Europe Cosmetic Plastic Packaging Industry Leaders

Gerresheimer AG

AptarGroup Inc.

Amcor plc

Albéa S.A.

HCP Packaging Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Rieke introduced tethered caps tested for 50 opening cycles without detachment.

- September 2024: Albéa allocated EUR 50 million (USD 54 million) to new sustainable-pack facilities across Europe, including lines for refillable containers and mono-material tubes.

- August 2024: Gerresheimer acquired Bormioli Pharma for EUR 180 million (USD 194 million), adding premium glass and refill expertise.

- July 2024: AptarGroup unveiled HDP all-plastic pump, eliminating metal springs and cutting material cost by up to 20%.

Europe Cosmetic Plastic Packaging Market Report Scope

Cosmetic packaging encompasses both primary and secondary packaging. Primary packaging, known as cosmetic containers, serves as the outer covering for the cosmetic product. It comes into direct contact with the cosmetic product. Secondary packaging refers to the external covering of one or multiple cosmetic receptacles.

The estimates for the cosmetic packaging market include all the costs associated with cosmetic packaging solution manufacturing, from raw material procurement to end users. It consists of the cost of material used, other associated products, such as inks and adhesives, closures, and related services like finishing, printing, labeling and marking, packing, and transporting. The estimates exclude the cost of the content that is or is to be packed inside the personal care packaging solution. Personal care packaging and cosmetic packaging are interchangeably used across the study.

The European cosmetic plastic packaging market is segmented by resin type (PE (HDPE and LDPE), PP, PET and PVC, polystyrene (PS), and bio-based plastics (bioplastic)), product type (bottles, tubes, and sticks, pumps, and dispensers, pouches, and other product types), application (skincare, hair care, oral care, make-up products, deodorants and fragrances, and other applications), and country (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe). The report offers the market size in value terms in USD for all the abovementioned segments.

| Polyethylene Terephthalate (PET) | |

| Polyethylene (PE) | High-Density Polyethylene (HDPE) |

| Low-Density and Linear-LDPE | |

| Linear Low-Density Polyethylene (LLDPE) | |

| Polypropylene (PP) | |

| Biodegradable and Bio-based Plastics | |

| Other Resin Types |

| Bottles |

| Tubes and Sticks |

| Pumps and Dispensers |

| Pouches |

| Other Product Types |

| Skin Care |

| Hair Care |

| Make-up Products |

| Deodorants and Fragrances |

| Other Applications |

| Conventional Packaging |

| Sustainable Packaging |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Resin Type | Polyethylene Terephthalate (PET) | |

| Polyethylene (PE) | High-Density Polyethylene (HDPE) | |

| Low-Density and Linear-LDPE | ||

| Linear Low-Density Polyethylene (LLDPE) | ||

| Polypropylene (PP) | ||

| Biodegradable and Bio-based Plastics | ||

| Other Resin Types | ||

| By Product Type | Bottles | |

| Tubes and Sticks | ||

| Pumps and Dispensers | ||

| Pouches | ||

| Other Product Types | ||

| By Application | Skin Care | |

| Hair Care | ||

| Make-up Products | ||

| Deodorants and Fragrances | ||

| Other Applications | ||

| By Sustainability Profile | Conventional Packaging | |

| Sustainable Packaging | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the Europe cosmetic plastic packaging market in 2026?

The market is valued at USD 3.57 billion in 2026 and is projected to grow to USD 4.12 billion by 2031 at a 2.88% CAGR.

Which country leads demand for cosmetic plastic packs in Europe?

Germany accounts for 21.05% of regional revenue, buoyed by advanced recycling infrastructure and a stringent fee-modulated EPR system.

What segment is growing fastest within plastic cosmetic packs?

Tubes and sticks show the highest 3.55% CAGR through 2031, powered by digital printing and indie-brand demand.

Why are refillable systems important for beauty brands?

Refillable packaging can cut packaging waste by up to 85%, secure EPR fee rebates and sustain premium price points for luxury labels.

How are EU rules influencing packaging design?

The Single-Use Plastics Directive and tethered-cap mandate require mono-material structures and attached closures, accelerating redesign costs but boosting recyclability.

What challenges limit recycled content adoption?

PCR resin supply is tight, prices run 20-40% above virgin grades, and quality constraints such as color consistency hinder premium cosmetic uses.

Page last updated on: