Cosmetic And Perfumery Glass Bottle Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

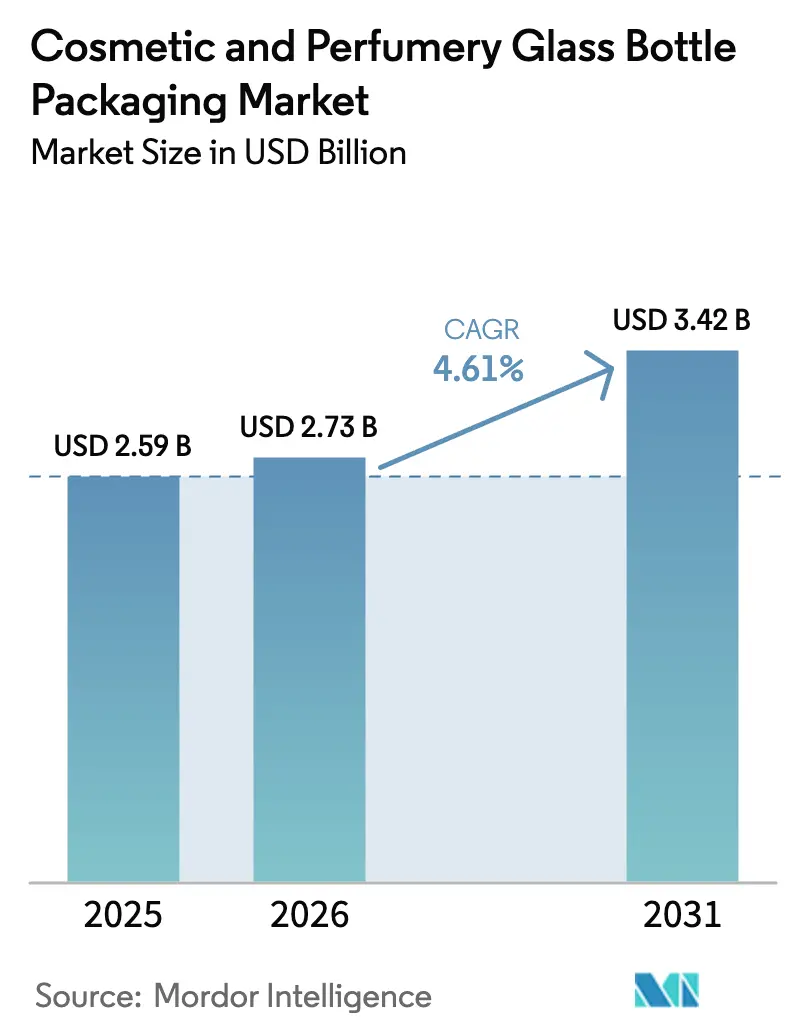

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 3.42 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

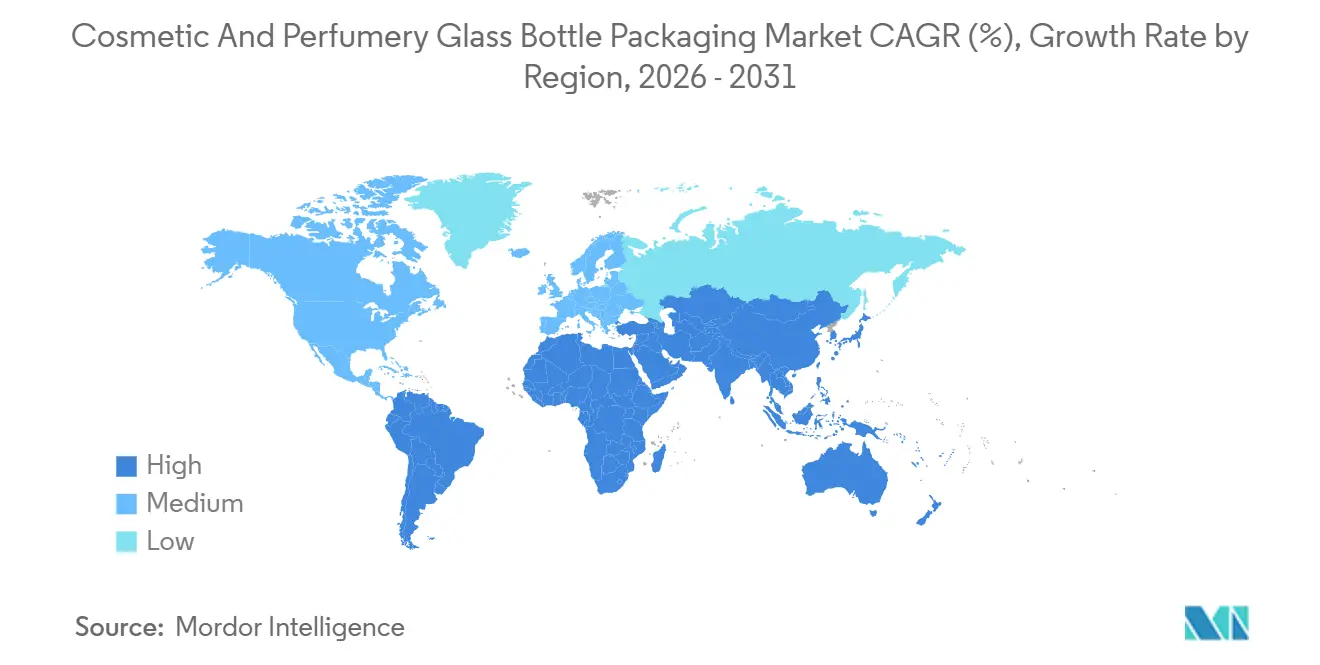

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetic And Perfumery Glass Bottle Packaging Market Analysis by Mordor Intelligence

The cosmetic and perfumery glass bottle packaging market size is projected to be USD 2.59 billion in 2025, USD 2.73 billion in 2026, and reach USD 3.42 billion by 2031, growing at a CAGR of 4.61% from 2026 to 2031. Consumers are paying more for prestige fragrances, serums, and refill-ready hair care, pushing brand owners to specify heavier flacons, custom shapes, and photogenic coatings. At the same time, regulators and investors insist on infinitely recyclable materials and audited carbon footprints, so glassmakers are upgrading furnaces, expanding post-consumer cullet use, and adding laser-etch capabilities. E-commerce now accounts for a double-digit share of category sales, which means bottles must survive six-day parcel journeys without breakage while still looking flawless on social media product pages. Competitive dynamics intensified after mid-2024 as private equity entered the sector and a leading supplier announced plans to divest its molded-glass unit, spurring mid-tier manufacturers to chase new accounts with shorter lead times and lower minimum orders. Against this backdrop, Asia-Pacific’s middle-income expansion and on-shored luxury supply chains are setting the pace for future volume growth, even as Europe retains its lead in design and sustainability know-how.

Key Report Takeaways

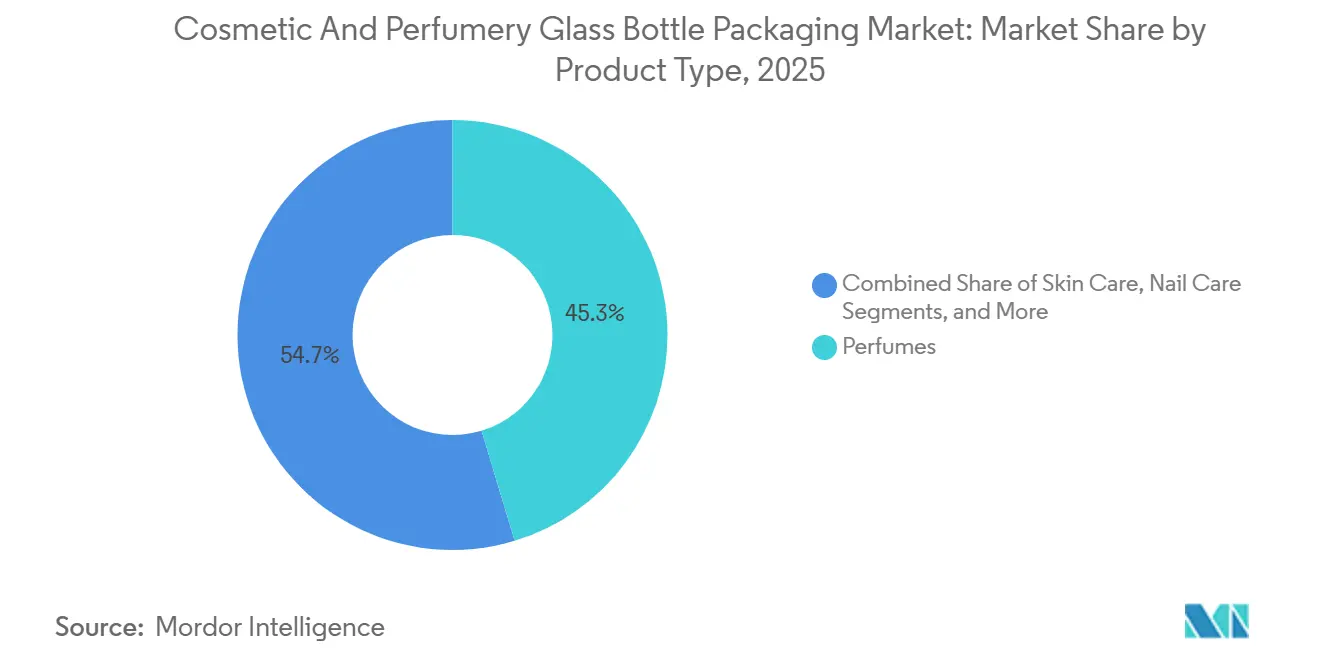

- By product type, perfumes led the cosmetic and perfumery glass bottle packaging market, accounting for 45.32% of revenue in 2025, while hair care is forecast to expand at a 5.53% CAGR through 2031.

- By capacity, the 50-150 ml segment captured 39.43% of the cosmetic and perfumery glass bottle packaging market size in 2025, whereas bottles above 150 ml are projected to grow the fastest at a 5.17% CAGR to 2031.

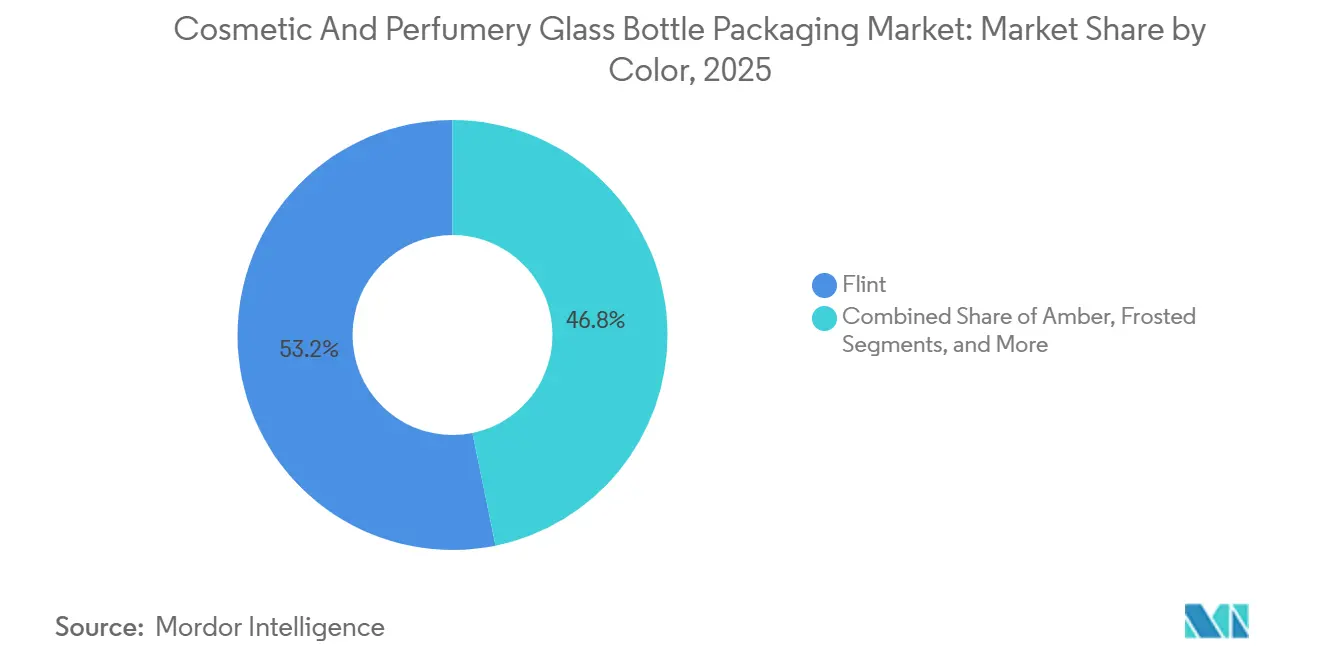

- By color, flint glass accounted for 53.21% revenue share in 2025, and special-colored glass is advancing at a 5.57% CAGR, the quickest among all color segments.

- By geography, Europe commanded 32.56% of the cosmetic and perfumery glass bottle packaging market in 2025, while Asia-Pacific is set to register the highest regional CAGR of 5.48% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cosmetic And Perfumery Glass Bottle Packaging Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumisation of Beauty and Fragrance Products | +1.2% | Global, concentrated in Europe, North America, China, India, South Korea | Medium term (2-4 years) |

| Sustainability Push for Infinitely Recyclable Glass | +0.9% | Global, led by EU and adopted in North America, rising in Asia-Pacific | Long term (≥ 4 years) |

| E-Commerce Demand for Aesthetic, Impact-Resistant Packs | +0.7% | Global, strongest in North America and Europe, growing elsewhere | Short term (≤ 2 years) |

| Laser-Enabled Personalisation and Anti-Counterfeit Engraving | +0.5% | Global, early uptake in Europe and North America, spreading to Middle East and Asia-Pacific | Medium term (2-4 years) |

| EU-2025/40 Regulation Favouring Recyclable Mono-Material Packs | +0.4% | Europe, spillover to export-oriented Asia and South America | Short term (≤ 2 years) |

| Electrified and Lightweight Furnaces Cutting Cost and CO₂ | +0.3% | Europe leadership, adoption in Asia-Pacific and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premiumisation Of Beauty And Fragrance Products

Rising disposable incomes and experiential retail are steering purchases toward prestige scents and clean-formula hair care that require heavier, ornate bottles for sensory appeal. Brazil’s prestige beauty value climbed 13% in 2024 to BRL 3 billion (USD 576 million), while India’s luxury beauty revenue is forecast to quintuple by 2035, giving suppliers fertile ground for bespoke molds and low-acid flint glass. Latin America’s fragrance culture gravitates toward extrait formats sold in compact yet weighty vessels, reinforcing glass’s premium aura. Brands leverage distinctive flacons, such as Valentino’s Born in Roma launch, to secure online buzz and shelf presence. Suppliers that can deliver custom shapes within 60-day lead times and 50,000-piece minimums are winning those high-margin briefs.

Sustainability Push For Infinitely Recyclable Glass

Eco-scores now influence listing decisions at retailers, prompting glassmakers to raise cullet content and publish verified carbon footprints. Verescence attained CDP Double A status in 2025 after lifting 100% PCR-glass use inside its French and Spanish furnaces. EU Regulation 2025/40 sets mandatory recycled-content thresholds and discourages composite decorations that contaminate cullet streams, pushing brands toward mono-material flacons. In Brazil, ABIHPEC’s reverse-logistics program collected 966,345 tonnes of post-consumer packaging, reinforcing local preference for recyclable glass.[1]Associação Brasileira da Indústria de Higiene Pessoal Perfumaria e Cosméticos, “Industry Overview,” abihpec.org.br Investments such as Verescence’s USD 553.7 million (EUR 490 million) buyout earmark funds for furnace electrification and AI-driven process control, further shrinking Scope 1 and Scope 2 emissions.

E-Commerce Demand For Aesthetic, Impact-Resistant Packs

Online beauty sales expose glass to 3-7% breakage, which erodes margins and brand equity. Suppliers respond with borosilicate blends that dominate 55% of the United States durability-critical volume and with rib-reinforced designs that cut damage without adding mass. Social-media merchandising remains vital, so finishes such as gradient metallics and matte frosting must withstand parcel vibrations and thermal cycling.[2]Qosmedix, “2025 Beauty Packaging Predictions,” qosmedix.com Berlin Packaging’s Doft New York jars illustrate this dual brief by pairing soft-heel geometry with Instagram-ready coatings that survived U.S. courier networks.[3]Industry Intelligence, “Glass Packaging in Beauty Sector Evolves with Lighter Bottles,” industryintel.com

Laser-Enabled Personalisation And Anti-Counterfeit Engraving

Counterfeit fragrances siphon revenue and tarnish reputations, so brands embed laser-etched batch codes linked to NFC chips or QR portals. Middle East demand for bespoke oud bottles showcases the value-add: limited editions carry individualized messages that command 20-30% premiums while deterring diversion. Bormioli Luigi’s USD 4.63 million (EUR 4.1 million) sputtering line enables metallic coatings that lasers can partially strip to reveal unique patterns, serving collectors and travel-retail exclusives.

Restraints Impact Analysis of Cosmetic And Perfumery Glass Bottle Packaging Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic Packaging Cost and Weight Advantage | -0.8% | Global mass-market segments | Short term (≤ 2 years) |

| Volatile Energy and Soda-Ash Input Prices | -0.6% | Global, acute in Europe and import-dependent regions | Medium term (2-4 years) |

| EU Packaging-Minimisation Rules Curbing Heavy Flacons | -0.3% | Europe, knock-on to export hubs | Medium term (2-4 years) |

| High E-Commerce Breakage And Return Rates | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plastic Packaging Cost And Weight Advantage

Polypropylene and PET remain 18.1% lighter than glass, resulting in lower freight spend and a 15% carbon footprint advantage over comparable formats. Online returns for beauty products hit 18.1%, with 82% blamed on breakage, a liability plastics largely avoid. Although Verescence trimmed bottle mass by up to 15%, glass still weighs 40-50% more than plastic equivalents. Emerging-market logistics amplify the gap; Brazil’s brands face import duties that make heavy bottles expensive, nudging innovators toward paper or solid formats. Glassmakers must therefore compete on sensory appeal, refillability, and infinite recyclability rather than cost.

Volatile Energy And Soda-Ash Input Prices

Soda ash hovered near USD 220 per tonne in 2024, while natural-gas spikes pushed European furnace costs higher, compressing margins.[4]U.S. Geological Survey, “Mineral Commodity Summaries 2024: Soda Ash,” usgs.gov Carbon allowances added EUR 20-30 per tonne of CO₂, taxing a process that emits 1.2-1.5 tonnes of CO₂ per tonne of glass. Zignago Vetro’s 14.5% revenue drop in H1 2024 illustrated the squeeze from destocking and energy volatility. Hybrid furnaces such as Bormioli Luigi’s 65% electric unit promise a 50% CO₂ cut by 2030 but demand USD 226.0 million (EUR 200 million) over four years, a hurdle for smaller players. To hedge, suppliers pass through surcharges pegged to gas indices, yet beauty brands prefer fixed prices, shifting commodity risk back to glassmakers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cosmetic And Perfumery Glass Bottle Packaging Market Segment Analysis

By Product Type:

Prestige Hair Care Accelerates AdoptionPerfumes commanded 45.32% of the cosmetic and perfumery glass bottle packaging market share in 2025, cementing fragrance as the historical anchor for glass usage. However, the cosmetic and perfumery glass bottle packaging market size tied to premium hair care is forecast to expand at a 5.53% CAGR as salon-grade shampoos and serums migrate from plastic to refill-compatible glass that signals purity and sustainability. Skin care jars and droppers stay relevant where UV defense and chemical inertness matter, while nail varnish bottles remain niche but stable. Brazilian hair care sales reached BRL 32.3 billion (USD 6.14 billion) in 2024, outpacing skin care and highlighting the appetite for shelf-worthy flacons that function in humid climates. Latin American perfume culture continues to demand compact, ornate bottles for high-concentration oils, reinforcing glass’s tactile allure.

Prestige hair care brands leverage larger-volume bottles to amortize mold costs and introduce refill pods that lower packaging weight per use. Keune’s switch to glass illustrates how professional channels embrace durability and recyclability to command 30% price premiums. Fragrance innovations focus on NFC-enabled caps and laser-etched serial numbers that elevate collectability, especially in travel retail. Skin care innovators like Drunk Elephant rely on amber flacons to shelter vitamin C and retinol without resorting to opaque plastics. Overall, cosmetics lines increasingly treat primary packs as brand assets rather than mere containers, channeling budget to distinctive geometry, texture, and smart authentication.

By Capacity:

Growing Demand For Formats Above 150 mlThe 50-150 ml range captured 39.43% of the cosmetic and perfumery glass bottle packaging market size in 2025, owing to its alignment with eau de parfum norms and facial-serum fills. Yet bottles exceeding 150 ml will register the highest 5.17% CAGR as refillable hair and body care lines prioritize value packs to reduce plastic and shipping frequency. Sub-50 ml vessels remain crucial for travel and sampling, particularly in duty-free zones where perfumes below 15 ml comply with airline liquid limits. Verescence’s catalog minimums challenge indie brands, so smaller glassmakers offer stock shapes with 1,000-piece order thresholds to capture fast-moving influencer launches.

E-commerce stress tests point to higher breakage in thin-wall bottles under 30 ml and oversized jars above 200 ml, steering digital-first brands toward mid-range capacities reinforced with internal ribs. Refillable perfume systems blend large primary flacons with 30 ml concentrate pods, cutting material per use while retaining a luxury outer shell. South America’s growth in 100-200 ml hair care packs shows how market education around refill discounts can reshape size mix. Deposit-return schemes in Australia test consumer willingness to cycle glass vials back into supply chains for credit, pointing to future hybrid ownership models.

By Color:

Special Finishes Drive Social-Media VisibilityFlint glass accounted for 53.21% of the cosmetic and perfumery glass bottle packaging market share in 2025 because its transparency lets scents and serums showcase hue and fill. Yet special-colored glass, ranging from amber to gradient metallics, is forecast to grow 5.57% CAGR as brands seek Instagram-ready differentiation. Amber blocks over 90% of UV radiation, protecting vitamin-sensitive actives in skin care and essential oils. Frosted or sand-blasted surfaces communicate understated luxury and resist fingerprints, aligning with minimalist design favored by Gen Z.

Bormioli Luigi’s metallic sputtering line enables limited runs with laser-etched patterns, marrying anti-counterfeiting and aesthetic goals for travel-exclusive SKUs. Gradient ombré techniques and vibrant cobalt or emerald shades serve niche identities but require dedicated furnaces, raising minimum order quantities. Clear UV-blocking coatings now offer flint-like visibility with SPF-grade protection, a compromise attractive to fragrance houses wary of color distortion. Ultimately, finishes that photograph well and withstands courier networks will continue to outpace standard flint in revenue growth.

Geography Analysis

Europe Cosmetic And Perfumery Glass Bottle Packaging Market

Europe retained 32.56% of the cosmetic and perfumery glass bottle packaging market in 2025, underpinned by French, Italian, and German glass clusters that supply LVMH, Hermès, and L’Oréal. Verescence runs four plants and five decoration sites across the region and earned CDP Double A largely through USD 553.7 million of sustainability-oriented investment. Bormioli Luigi’s hybrid furnace, operational since 2025, hit 65% electric fusion and targets a 50% CO₂ cut by 2030, illustrating EU support for decarbonized manufacturing. An Italian antitrust probe involving nine companies, which concluded in December 2025, momentarily clouded pricing visibility but is expected to restore normal competitive bidding. European producers still grapple with energy levies and packaging-minimization rules that discourage heavy, ornate designs, nudging them toward lightweighting and mono-material collars.

APAC Cosmetic And Perfumery Glass Bottle Packaging Market

Asia-Pacific is forecast to grow at a 5.48% CAGR, propelled by rising middle-income consumers in China and India, plus Verescence’s earlier purchase of South Korea’s Pacificglas, which localized luxury supply lines. India’s luxury beauty spend is expected to quintuple by 2035, driving demand for domestic molded-glass capacity across Piramal, HNGIL, and Pragati plants. South Korea’s exports to South America quadrupled to USD 70.2 million in 2024, creating new regional flows for premium K-Beauty bottles. China remains the volume anchor, yet volatility in 2024 hurt European suppliers’ revenues as destocking intensified. Japan’s aging population sustains steady demand for anti-aging creams in glass jars, while Australia and New Zealand serve as live test beds for refillable pilots, thanks to supportive waste regulations.

The Americas and MEA Cosmetic And Perfumery Glass Bottle Packaging Market

North America shows robust per-capita beauty spend and borosilicate adoption, but faces pressure to substitute for plastic. Gerresheimer holds roughly 24.2% United States share and is investing USD 180 million in Georgia capacity even while planning to divest its USD 830.6 million (EUR 735 million) molded-glass arm. Mexico’s proximity offers just-in-time delivery for United States brands, though tariff uncertainty tempers long-range planning. South America’s cosmetic and perfumery glass bottle packaging market is anchored by Brazil, where exports hit USD 1 billion in 2025, and prestige fragrances thrive on cultural affinity for concentrated oils. Middle East and Africa fragrance spend is on track to reach USD 7.21 billion by 2032, and high consumer awareness of eco-labels is driving the uptake of engraved authenticity codes and refill initiatives.

Competitive Landscape

The cosmetic and perfumery glass bottle packaging market is moderately concentrated, with Verescence, Gerresheimer, Pochet, Heinz-Glas, and Bormioli Luigi controlling most luxury flacon supply. Verescence changed ownership in June 2025 when Movendo Capital and Draycott acquired the company for EUR 490 million, securing a producer that ships 600 million bottles annually and holds EcoVadis Platinum certification, a status increasingly required by top beauty houses. Gerresheimer’s plan to spin off its molded-glass unit underscores a sector pivot toward high-margin systems and solutions; the carve-out frees up shares for mid-tier firms targeting standard-catalogue opportunities. Bormioli Luigi’s investment in hybrid melting and sputtering upgrades differentiates its offer with measured CO₂ savings and bespoke metallic finishes, both critical to brand storytelling.

Regional disruptors add competitive friction. PGP Glass, bought by Blackstone for roughly USD 1 billion in 2020, operates 1,600 tonnes-per-day capacity and sought to acquire Verescence in 2024, signaling ambitions to enter the prestige tier. Smaller European firms woo indie beauty labels by offering 1,000-piece minimums and 30-day prototypes, filling a gap between commodity standards and 50,000-unit custom runs. Strategic alliances between flacon makers and closure specialists integrate Zamac caps, aluminum collars, and NFC-enabled corks into turnkey projects, simplifying procurement for brands pressed by rapid product-drop cycles.

Technology adoption is diverging. European leaders pour capital into electrified furnaces and AI-guided process controls, chasing Science Based Targets initiative alignment, while some Asian producers leverage cheaper fuel and labor to undercut on price. ISO 14001 and ISO 50001 certifications are now baseline entry tickets for global beauty tenders, and failure to demonstrate decarbonization progress can disqualify bidders at the RFP stage. Meanwhile, Italy’s two-year antitrust review highlighted how close-knit the supplier base remains and underscored barriers to entry such as furnace-start costs and the need for 24-month customer qualification windows. As private equity deepens its footprint, capital for plant upgrades will continue flowing, but expectations for EBITDA uplift will intensify price competition in standard-shape flacons.

Cosmetic And Perfumery Glass Bottle Packaging Industry Leaders

Gerresheimer AG

HEINZ-GLAS GmbH & Co. KGaA

Bormioli Luigi S.p.A.

Stoelzle Glass Group

PGP Glass Private Limited

- *Disclaimer: Major Players sorted in no particular order

Cosmetic And Perfumery Glass Bottle Packaging Market Companies Covered in this Report

- Verescence France SASU

- Gerresheimer AG

- Pochet SAS

- HEINZ-GLAS GmbH & Co. KGaA

- Bormioli Luigi S.p.A.

- Vitro, S.A.B. de C.V.

- PGP Glass Private Limited

- Stoelzle Glass Group

- Zignago Vetro S.p.A.

- Berlin Packaging LLC

- Saver Glass SAS

- Pragati Glass Pvt Ltd

- Baralan International S.p.A.

- Lumson S.p.A.

- vetroelite packaging s.r.l

- Feemio Group Co., Ltd.

- Brandsamor Commerce LLC

- Allied Glass Containers Limited

- SGB Packaging Group Inc.

- Beatson Clark Ltd

Recent Industry Developments in Cosmetic And Perfumery Glass Bottle Packaging Market

- November 2025: K-Beauty exports to South America quadrupled to USD 70.2 million in 2024, with cosmetics representing 90% of shipments and Brazil taking 45% share, signaling stronger regional demand for premium Korean glass packaging.

- October 2025: L’Oréal Luxe Brazil confirmed Valentino’s Born in Roma as the country’s top luxury fragrance launch in H1 2025, spotlighting the role of bespoke flacons in driving shelf and online visibility.

- August 2025: Gerresheimer unveiled plans to divest its molded-glass business, which posted EUR 735 million (USD 830.6 million) revenue, aiming to refocus on high-margin drug-delivery systems.

- July 2025: Verescence published its 2024-2025 Sustainability Report, detailing 98% water recycling and elevated PCR-glass usage across French furnaces.

Global Cosmetic And Perfumery Glass Bottle Packaging Market Report Scope

The Cosmetic and Perfumery Glass Bottle Packaging Market Report is Segmented by Product Type (Perfumes, Skin Care, Nail Care, Hair Care, Other Product Type), Capacity (0 to 50 ml, 50 to 150 ml, More Than 150 ml), Color (Flint, Amber, Frosted, Special-Colored, Other Color), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

| Perfumes |

| Skin Care |

| Nail Care |

| Hair Care |

| Other Product Type |

| 0 to 50 ml |

| 50 to 150 ml |

| More Than 150 ml |

| Flint |

| Amber |

| Frosted |

| Special-Colored |

| Other Color |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Perfumes | |

| Skin Care | ||

| Nail Care | ||

| Hair Care | ||

| Other Product Type | ||

| By Capacity | 0 to 50 ml | |

| 50 to 150 ml | ||

| More Than 150 ml | ||

| By Color | Flint | |

| Amber | ||

| Frosted | ||

| Special-Colored | ||

| Other Color | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the cosmetic and perfumery glass bottle packaging market in 2026?

It is estimated at USD 2.73 billion in 2026, on track toward USD 3.42 billion by 2031.

Which region is expanding the fastest?

Asia-Pacific is projected to post a 5.48% CAGR during 2026-2031, driven by China, India, and South Korea.

What product segment is growing quickest?

Glass bottles for prestige hair care are forecast to increase at 5.53% CAGR through 2031 as brands shift from plastic to refill-ready glass.

Why are brands choosing special-colored glass?

Amber, frosted, and metallic finishes offer UV protection and social-media appeal, pushing the segment to the fastest 5.57% CAGR among color options.

How are suppliers lowering carbon footprints?

Investments in hybrid furnaces, higher PCR-glass content, and AI-guided process controls are reducing Scope 1 and Scope 2 emissions across European facilities.

What risks could slow market growth?

Plastic’s cost advantage, volatile energy and soda-ash prices, and EU packaging-minimisation rules exert downward pressure on glass demand and margins.

Page last updated on: