Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 25.35 Billion |

| Market Size (2026) | USD 26.16 Billion |

| Market Size (2031) | USD 30.59 Billion |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

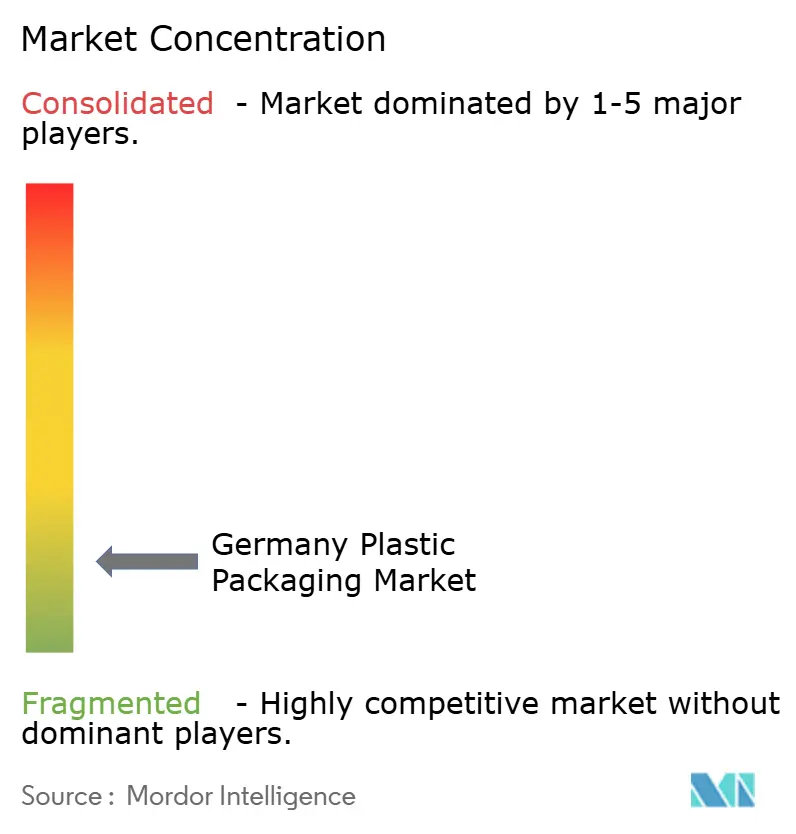

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Plastic Packaging Market Analysis by Mordor Intelligence

The Germany plastic packaging market size was valued at USD 25.34 billion in 2025 and estimated to grow from USD 26.16 billion in 2026 to reach USD 30.59 billion by 2031, at a CAGR of 3.18% during the forecast period (2026-2031). Solid demand from e-commerce parcel fulfillment, tighter Extended Producer Responsibility (EPR) rules under the Verpackungsgesetz, and rapid recycled-content adoption are guiding this measured expansion. Brand owners are redesigning rigid and flexible formats around mono-material polyethylene to pass near-infrared sortability tests, while beverage bottlers accelerate rPET uptake ahead of the European Union’s 2025 recycled-content deadline. At the same time, proposed virgin-resin taxes and Germany’s high industrial power tariffs weigh on converter margins, prompting capacity shifts toward energy-efficient extrusion and stretch-blow molding lines. Steady downstream pull from pharmaceutical cold-chain applications, supported by biologics pipelines and tamper-evident mandates, further underpins growth through 2031.

Key Report Takeaways

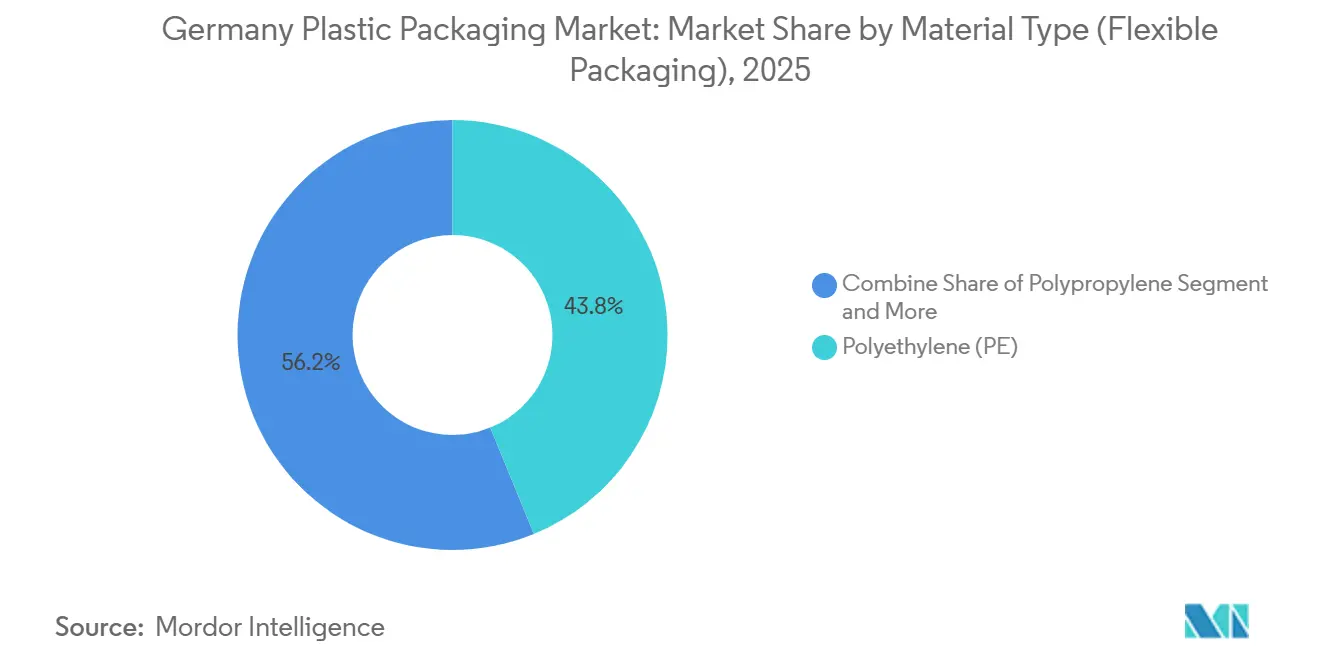

- By material, polyethylene held 43.82% of the Germany plastic packaging market share in 2025, while ethylene-vinyl alcohol copolymer is projected to post the fastest 4.23% CAGR to 2031.

- By packaging type, bottles and jars led with 29.43% revenue share in 2025; pouches are forecast to expand at a 4.14% CAGR through 2031.

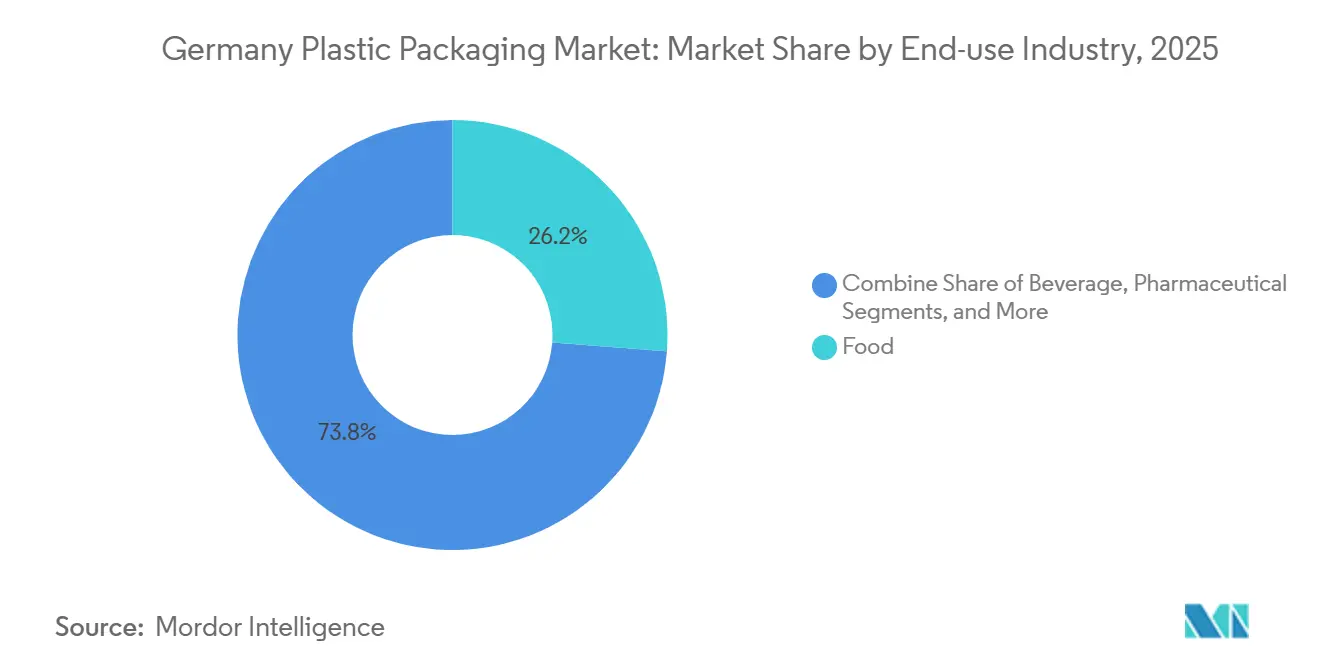

- By end use, food accounted for 26.21% of the Germany plastic packaging market size in 2025, and pharmaceutical applications are advancing at a 4.57% CAGR, the highest among end users.

- By distribution channel, direct sales dominated with a 57.14% share in 2025, whereas indirect channels are set to grow at a 3.53% CAGR on the back of digital procurement uptake.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended Producer Responsibility Mandates Driving Recyclable Mono-Material Demand | +1.2% | National, spillover to Austria and Switzerland | Medium term (2-4 years) |

| E-commerce Boom Fueling Lightweight Flexible Parcel Mailers | +0.9% | Berlin, Hamburg, Munich logistics hubs | Short term (≤2 years) |

| Lightweighting in Automotive and Industrial Sectors Shifting from Metal to Rigid Plastics | +0.6% | Baden-Württemberg and Bavaria clusters | Long term (≥4 years) |

| Mehrweg PET Refill Quotas Accelerating rPET Adoption | +0.8% | Beverage-dense regions, North Rhine-Westphalia | Medium term (2-4 years) |

| Convenience-Ready Meal Culture Boosting Microwave-Suitable Plastic Trays | +0.5% | Urban centers nationwide | Short term (≤2 years) |

| Cold-Chain Biologics Pipeline Expanding Demand for Medical-Grade Plastic Vials and Blisters | +0.7% | Hesse and Bavaria pharma hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Extended Producer Responsibility Mandates Driving Recyclable Mono-Material Demand

Germany’s Verpackungsgesetz now obliges every package placed on the market to be registered in the LUCID database and to be financially backed by a dual-system operator, with non-compliance fines that can reach EUR 200,000 (USD 216,000). Rising plastic-recycling quotas, already at 63% for the overall stream and set at 90% for PET bottles by 2025, have forced converters to replace multi-material laminates with mono-PE or mono-PP alternatives that pass near-infrared optical sorting. Demand for certified recyclable films is therefore outpacing total market growth, rewarding vertically integrated players that run in-house wash-and-pellet lines. The upcoming EU Packaging and Packaging Waste Regulation, which sets recyclability design rules for inks, labels, and closures from 2030, is expected to amplify this momentum.

E-commerce Boom Fueling Lightweight Flexible Parcel Mailers

German online retail surpassed EUR 86.7 billion (USD 94.0 billion) in 2023, sending more than 4.5 billion parcels and driving urgent demand for co-extruded polyethylene mailers that cut transport weight 40-60% versus corrugated cardboard.[1]Bundesverband E-Commerce und Versandhandel, “German E-Commerce Market Data 2023,” bevh.org Logistics providers in Berlin, Hamburg, and Munich report that lighter mono-PE mailers allow payload density gains of about 12-15% per truck, directly reducing Scope 3 emissions declarations required under the EU Corporate Sustainability Reporting Directive. Marketplaces such as Amazon and Zalando must now verify that all third-party sellers register packaging with LUCID, accelerating sales of RecyClass-certified mailers through indirect digital channels. Converters offering 30% post-consumer recycled (PCR) content already enjoy premium contract renewals as brand owners prepare for tighter recycled-content obligations in 2027-2030.

Lightweighting in Automotive and Industrial Sectors Shifting from Metal to Rigid Plastics

German vehicle makers produced 4.1 million units in 2023 and face a 95 g/km fleet-average carbon cap from 2025. Automakers deploy glass-fiber-reinforced polypropylene to replace heavier steel and aluminum in door panels, dash substrates, and battery enclosures, realizing up to 40% weight savings and extending electric-vehicle range by 8-12 km per charge. These light, rigid resins are used in industrial transport packaging, where reusable HDPE crates displace steel bins in just-in-time logistics. Suppliers that guarantee 25% rPP content for non-visible components by 2026 have already secured multiyear contracts with Bavaria-based tier-one systems integrators.

Mehrweg PET Refill Quotas Accelerating rPET Adoption

Germany’s deposit-return system posted a 98.5% PET bottle recovery rate in 2024, unlocking 450,000 t of post-consumer feedstock.[2]Deutsche Pfandsystem GmbH, “PET Bottle Return Statistics 2024,” dpg-pfandsystem.de Yet mechanical recycling capacity still trails demand by roughly 15-20%, pushing converters to import food-grade flakes from Poland, Romania, and Scandinavia at premiums of EUR 150-250/t over virgin resin. New bottle-to-bottle lines in Austria and France aim to close this gap, while beverage fillers increase orders for heavier preforms in Mehrweg (refillable) PET formats that withstand 15-20 reuse cycles. These dynamics elevate rPET value, but also prompt early investment in chemical-recycling routes that qualify as recycled content under mass-balance accounting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proposed EUR 0.80 per kg German Plastics Tax Inflating Virgin Resin Prices | -0.8% | National, cross-border trade with Poland and Czech Republic | Short term (≤2 years) |

| Retailer-Led Fiber Shift Shrinking Plastic Shelf Share | -0.5% | Discount retail chains nationwide | Medium term (2-4 years) |

| High German Electricity Costs Raising Conversion Margins | -0.4% | National, acute in energy-intensive blow-molding and extrusion | Short term (≤2 years) |

| Limited Food-Grade rPCR Supply Curtailing Recycled-Content Targets | -0.6% | National, import dependence on Eastern Europe and Scandinavia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proposed EUR 0.80 per kg German Plastics Tax Inflating Virgin Resin Prices

A domestic levy mirroring the EU plastics tax would raise polyethylene and polypropylene costs by 8-12% if full pass-through occurred, at a time when converters already face recycled-content premiums.[3]Eurostat, “Industrial Electricity Prices 2025,” ec.europa.eu/eurostat Some processors import resin from neighboring markets, yet freight and upcoming disclosures under the Carbon Border Adjustment Mechanism erode much of this pricing edge. Uncertainty also deters capital spending on virgin-resin extrusion lines, redirecting funds toward recycling partnerships and chemical-recycling pilot plants.

Retailer-Led Fiber Shift Shrinking Plastic Shelf Share

Aldi, Lidl, and other discount grocers target 20-30% plastic-reduction by 2025, swapping PET trays for corrugated cartons or molded-fiber alternatives in produce and bakery aisles.[4]Lidl Deutschland, “Sustainability Report 2024,” lidl.de While fiber adoption faces moisture-barrier limits, it has already trimmed rigid PET and polystyrene demand by low-double-digit rates in 2024. Converters serving fresh-food brands must now co-develop mono-material trays with thin-barrier coatings that compete on cost and recyclability, or risk delisting from the country’s dominant discount channel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene Retains Leadership amid Compliance-Driven Reformulations

Polyethylene secured 43.82% of Germany plastic packaging market share in 2025 owing to its low cost and proven recyclability. Demand concentrates in mono-PE films that satisfy VerpackG sortability and in HDPE bottles for household care, both segments benefiting from stable resin supply and mature mechanical recycling streams. Polypropylene is the workhorse for rigid crates and thermoformed dairy cups, with converters experimenting with high-impact copolymer grades that withstand 100-cycle reuse programs. Ethylene-vinyl alcohol copolymer, although accounting for less than 3% of total consumption, registers the fastest 4.23% CAGR thanks to its ultra-low oxygen transmission performance in chilled ready-meal pouches and pharmaceutical blisters. Limited German food-grade rPCR availability constrains rPET penetration beyond beverages, yet mass-balance certified resins from Austria and France support incremental progress. Chlorine-containing PVC remains confined to niche medical tubing and shrink-sleeve usages, under persistent regulatory and disposal scrutiny.

Polyethylene’s dominance also reflects converter moves toward single-family material hierarchies that simplify reclaim. Südpack’s RecyClass-approved mono-PE confectionery wrap, launched in 2024, typifies this trajectory, pairing <10 cc/m²/day oxygen ingress with easy near-infrared detection. Polypropylene suppliers likewise roll out cast-film solutions that eliminate polyethylene seal layers, ensuring full PP construct recyclability. Meanwhile, chemical firms such as BASF and Borealis scale mass-balance allocations, allowing brand owners to claim recycled content without altering physical resin properties. Collectively, these initiatives reinforce the Germany plastic packaging market’s shift to compliance-friendly polyolefins through 2031.

By Packaging Type: Bottles Anchor Revenue, Pouches Command Growth Momentum

Bottles and jars captured 29.43% value in 2025, buoyed by beverage and pharmaceutical lines that leverage Germany’s 98.5% return deposit infrastructure. Growing refill quotas for Mehrweg PET elevate heavier preforms, cushioning revenue even as unit volumes plateau. Films and wraps remain essential to pallet load stabilization, yet the fastest-growing segment is pouches, forecast to grow at a 4.14% CAGR. E-commerce and single-serve meal-kit adoption favor lightweight stand-up formats that lower transport emissions up to one-third compared with rigid trays. Rigid trays and clamshells face pressure from discount-retailer fiber programs, though polypropylene monotrays that meet RecyClass guidelines offer a defensive path.

Pallets and industrial crates thrive in automotive supply loops where HDPE and PP versions replace steel alternatives, satisfying OEM CO₂ targets and eliminating corrosion spend. Closure and dispensing subsystems innovate around tethered-cap requirements under the EU Single-Use Plastics Directive, with Berry Global’s 100% recycled-HDPE cap commercialized on national cola lines in 2024. Across categories, the German plastic packaging market size gains resilience by aligning design with recyclability, weight reduction, and retailer shelf requirements.

By End-Use Industry: Food Dominates, Pharmaceutical Sets the Pace

Food retained 26.21% share of Germany plastic packaging market size in 2025, spanning confectionery, dairy, and fresh produce. Snack makers drive steady demand for moisture-proof BOPP wraps, while yogurt brands pivot toward mono-PP cups that pass sortability audits. Pharmaceutical consumption, however, advances at the fastest pace, with a 4.57% CAGR as biologics pipelines proliferate. mRNA vaccines and monoclonal antibodies require shatterproof polymer vials and prefilled syringes that withstand -80 °C transit, a feature added by Gerresheimer and other medical specialists. Beverage bottlers continue to invest in refillable and single-use PET, balancing lighter weights against rising recycled-content thresholds. Cosmetics are packaged in rPE and rPP bottles that convey sustainability messaging without compromising aesthetics. Industrial users, including chemical drums and intermediate bulk containers, adopt reusable HDPE systems to trim lifecycle costs.

The pet-food niche shifts can be formatted to retortable stand-up pouches, reducing package mass by 60-70%. Meanwhile, retailer fiber substitution is tempering rigid polystyrene clamshell use in produce aisles, yet ongoing shelf-life concerns prevent a full-scale conversion. Overall, material agility and regulatory compliance drive end-use dynamics within the Germany plastic packaging market.

By Distribution Channels: Direct Contracting Leads, Digital Intermediation Scales

Direct sales pathways accounted for 57.14% revenue in 2025 because brand owners value guaranteed resin supply, technical codevelopment, and locked-in recycled-content specifications. Converters with vertically integrated wash-flaking lines secure multi-year volume commitments from beverage and personal-care leaders, reinforcing the Germany plastic packaging market’s durable contract structure. Indirect channels are nonetheless projected to expand at a 3.53% CAGR through 2031, propelled by cloud-based platforms that aggregate small- and medium-sized enterprise demand. Distributors stock prequalified medical blisters and custom-print pouches, offering next-day shipment from hubs in Frankfurt and Leipzig.

Smaller cosmetics labels, natural-food startups, and third-party marketplace sellers increasingly tap these intermediaries to circumvent minimum-order hurdles. However, the lack of deep material science support limits indirect channels on highly regulated pharmaceuticals and barrier-sensitive foods. As EPR enforcement tightens, both routes must verify LUCID registration and RecyClass certification, equalizing compliance burdens while preserving their respective value propositions in the Germany plastic packaging market.

Geography Analysis

North Rhine-Westphalia, Bavaria, and Baden-Württemberg collectively generated nearly 60% of national demand in 2025, reflecting dense clusters of consumer-goods majors, automotive OEMs, and beverage fillers. Düsseldorf’s chemical corridor channels steady polyethylene and polypropylene resin into flexible-film lines serving personal-care and pharma products, while Cologne’s logistics infrastructure redistributes finished packs across mainland Europe. Munich and Ingolstadt anchor Bavaria’s automotive pull for reusable HDPE crates and glass-fiber-PP under-hood parts, supporting above-average CAGR within the regional Germany plastic packaging market. Stuttgart-area suppliers mirror that trend, with injection-molded battery-module housings gaining traction as electric-vehicle output scales.

Northern ports at Hamburg and Bremen facilitate the import of PCR flakes from Scandinavia and the Netherlands, which are then fed into adjacent bottle-to-bottle operations that supply domestic cola and mineral-water brands. Eastern Länder, led by Saxony and Thuringia, attract mid-tier film extruders seeking lower labor costs and proximity to Polish and Czech resin bases. Despite smaller local consumer populations, these plants enjoy stable export flows to Austria and Switzerland, where VerpackG-style EPR rules drive demand for German-standard recyclable formats. Rural regions focus on agricultural drums and bulk-sack applications, registering slower but steady gains tied to modernized farming supply chains.

Industrial power tariffs remain 25-30% above the EU average, eroding margins for energy-intensive blow-molding yet inspiring investments in solar rooftops and biogas cogeneration that could narrow the gap after 2028. Integration of the Carbon Border Adjustment Mechanism from 2026 also curtails arbitrage for cheaper non-EU resin, reinforcing local circularity loops. In aggregate, geographic diversity cushions the Germany plastic packaging market against localized regulatory or cost shocks while fostering region-specific specialization.

Competitive Landscape

The Germany plastic packaging market in 2025 remained moderately concentrated, with the top five converters controlling about 35–40% of revenue. Major players pursued capacity expansions and technology upgrades to secure feedstock and meet specialized demand: Amcor deepened its cold‑chain capabilities through Moda Systems and captive wash‑lines for rPE pellets, ALPLA invested EUR 50 million to enlarge its Austrian bottle‑to‑bottle plant for rPET supply, and Gerresheimer commissioned a EUR 35 million ISO‑Class 7 vial facility targeting biologics producers seeking polymer alternatives to glass.

Mid‑sized converters such as Südpack and Constantia Flexibles capitalized on barrier‑coating science to deliver mono‑PE wraps with oxygen ingress below 10 cc/m²/day, a decisive attribute for confectionery clients under VerpackG recyclability audits. Strategic partnerships also focused on access to circular feedstocks, with Constantia and BASF piloting mass‑balance pyrolysis oils, and Eastman preparing a polyester‑renewal plant to export rPET to German converters from 2026. Meanwhile, digital procurement startups like Packiro aggregated SME orders, challenging legacy distributor models by offering transparent CO₂ calculators and instant RecyClass documentation.

Equipment upgrades further reshaped the competitive landscape, as converters shifted toward all‑electric extrusion and LED ultraviolet curing to cut power consumption by up to 30%, protecting margins in Germany’s costly energy environment. With the combined share of top players still below 50%, regional specialists in pharmaceutical blisters, molded‑fiber hybrids, and industrial drums retained space to thrive, sustaining healthy rivalry and innovation across the market.

Germany Plastic Packaging Industry Leaders

Amcor Plc

Mondi Group

Constantia Flexibles Group GmbH

Gerresheimer AG

Alpla Werke Alwin Lehner GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: BASF started up a EUR 120 million (USD 132 million) chemical-recycling pilot in Ludwigshafen, supplying food-grade pyrolysis oil to German flexible-film converters under mass-balance contracts through 2028.

- February 2026: Mondi introduced a mono-material polypropylene stand-up pouch containing 35% post-consumer recycled content that passed retort testing for wet pet food and entered commercial production at its Halle extrusion plant.

- January 2026: Gerresheimer signed a five-year agreement with BioNTech to deliver up to 200 million cold-chain polymer vials annually from the Essen facility, covering future mRNA vaccine volumes.

- January 2026: Berry Global commissioned a 25,000 t recycled-HDPE pelletizing line in Schweinfurt, lifting its German recycled-resin capacity to 65,000 t per year.

Germany Plastic Packaging Market Report Scope

The Germany Plastic Packaging Market Report is Segmented by Material Type (Rigid Plastic: Polyethylene, Polypropylene, Polyethylene Terephthalate, Polyvinyl Chloride, Polystyrene and Expanded Polystyrene, Other Rigid Plastic; Flexible Plastic: Polyethylene, Biaxially Oriented Polypropylene, Cast Polypropylene, Polyvinyl Chloride, Ethylene-Vinyl Alcohol, Other Flexible Plastic), Packaging Type (Rigid: Bottles and Jars, Trays and Clamshells, Pallets and Crates, Other; Flexible: Pouches, Bags and Sacks, Films and Wraps, Other), End-use Industry (Food, Beverage, Pharmaceutical, Cosmetics and Personal Care, Industrial, Pet Food and Animal Care, Other), Distribution Channels (Direct Sales, Indirect Sales), and Geography. Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Rigid Plastic | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | |

| Polystyrene (PS) and Expanded Polystyrene (EPS) | |

| Other Rigid Plastic | |

| Flexible Plastic | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Polyvinyl Chloride (PVC) | |

| Ethylene-Vinyl Alcohol (EVOH) | |

| Other Flexible Plastic |

By Packaging Type

| Rigid Plastic Packaging | Bottles and Jars |

| Trays and Clamshells | |

| Pallets and Crates | |

| Other Rigid Plastic Packaging | |

| Flexible Plastic Packaging | Pouches |

| Bags and Sacks | |

| Films and Wraps | |

| Other Flexible Plastic Packaging |

By End-use Industry

| Food | Confectionery and Snacks |

| Breads and Cereals | |

| Fresh Produce | |

| Dairy-Based Products | |

| Other Food Products | |

| Beverage | Bottled Water |

| Juices and Nectars | |

| Dairy-Based Beverages | |

| Carbonated Soft Drinks | |

| Other Beverages | |

| Pharmaceutical | |

| Cosmetics and Personal Care | |

| Industrial | |

| Pet Food and Animal Care | |

| Other End-use Industry |

By Distribution Channels

| Direct Sales Channels |

| Indirect Sales Channels |

| By Material Type | Rigid Plastic | Polyethylene (PE) |

| Polypropylene (PP) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyvinyl Chloride (PVC) | ||

| Polystyrene (PS) and Expanded Polystyrene (EPS) | ||

| Other Rigid Plastic | ||

| Flexible Plastic | Polyethylene (PE) | |

| Biaxially Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Polyvinyl Chloride (PVC) | ||

| Ethylene-Vinyl Alcohol (EVOH) | ||

| Other Flexible Plastic | ||

| By Packaging Type | Rigid Plastic Packaging | Bottles and Jars |

| Trays and Clamshells | ||

| Pallets and Crates | ||

| Other Rigid Plastic Packaging | ||

| Flexible Plastic Packaging | Pouches | |

| Bags and Sacks | ||

| Films and Wraps | ||

| Other Flexible Plastic Packaging | ||

| By End-use Industry | Food | Confectionery and Snacks |

| Breads and Cereals | ||

| Fresh Produce | ||

| Dairy-Based Products | ||

| Other Food Products | ||

| Beverage | Bottled Water | |

| Juices and Nectars | ||

| Dairy-Based Beverages | ||

| Carbonated Soft Drinks | ||

| Other Beverages | ||

| Pharmaceutical | ||

| Cosmetics and Personal Care | ||

| Industrial | ||

| Pet Food and Animal Care | ||

| Other End-use Industry | ||

| By Distribution Channels | Direct Sales Channels | |

| Indirect Sales Channels | ||

Key Questions Answered in the Report

What is the forecast value of Germany plastic packaging by 2031?

The market is projected to reach USD 30.59 billion by 2031, advancing at a 3.18% CAGR between 2026 and 2031.

Which material leads volumes in German plastic packs today?

Polyethylene is the largest, accounting for 43.82% of total revenue in 2025 owing to recyclability and cost advantages.

Why are pouches gaining faster than trays or bottles?

E-commerce and meal-kit brands favor lightweight stand-up pouches that cut transport emissions by up to one-third versus rigid trays.

How are deposit-return rules influencing bottle design?

Mehrweg quotas and EU recycled-content mandates drive heavier, refillable PET preforms and accelerate rPET procurement contracts.

What restrains growth despite stable consumer demand?

A proposed EUR 0.80 per kg plastics tax, high industrial power prices, and retailer shifts toward fiber formats squeeze converter margins.

Which regions inside Germany show the highest packaging demand?

North Rhine-Westphalia, Bavaria, and Baden-Württemberg together generate nearly 60% of national plastic-packaging consumption.

Page last updated on: