Europe Flexible Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

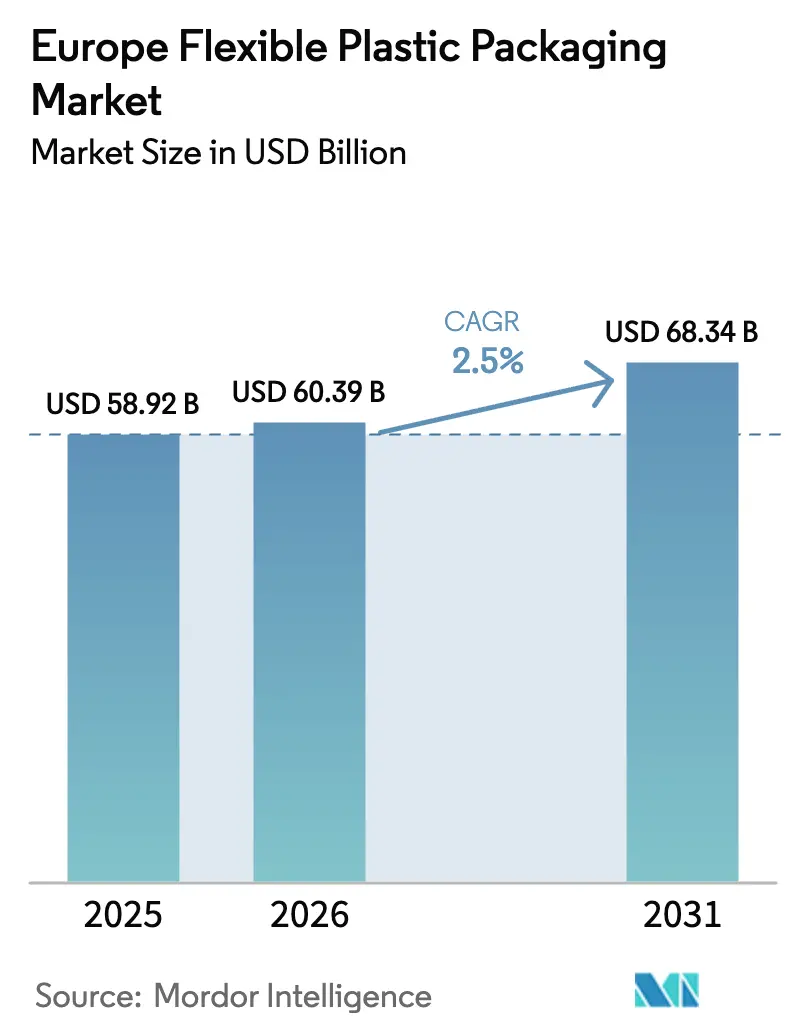

| Base Year Market Size (2025) | USD 58.92 Billion |

| Market Size (2026) | USD 60.39 Billion |

| Market Size (2031) | USD 68.34 Billion |

| Growth Rate (2026 - 2031) | 2.50% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Flexible Plastic Packaging Market Analysis by Mordor Intelligence

Europe flexible plastic packaging market size in 2026 is estimated at USD 60.39 billion, growing from 2025 value of USD 58.92 billion with 2031 projections showing USD 68.34 billion, growing at 2.50% CAGR over 2026-2031. Steady growth signals a mature landscape adapting to the European Union’s Packaging and Packaging Waste Regulation, which requires all packs sold in the bloc to be recyclable by 2030. Regulatory pressure, combined with e-commerce expansion and heightened food-safety expectations, is pushing brand owners to favor mono-material films, lightweight formats, and post-consumer-recycled content. Amcor’s 2025 takeover of Berry Global is accelerating scale-driven R&D on recyclable barrier solutions. Simultaneously, rapidly rising Extended Producer Responsibility (EPR) fees in the Nordics and the United Kingdom’s Plastic Packaging Tax are shifting cost calculations toward designs that minimize material use and speed sortation. Early movers in migration-safe high-barrier films are carving defensible niches in meat and dairy, while converters with digital printing capacity are winning short-run orders tied to product seasonalities and retailer promotions.

Key Report Takeaways

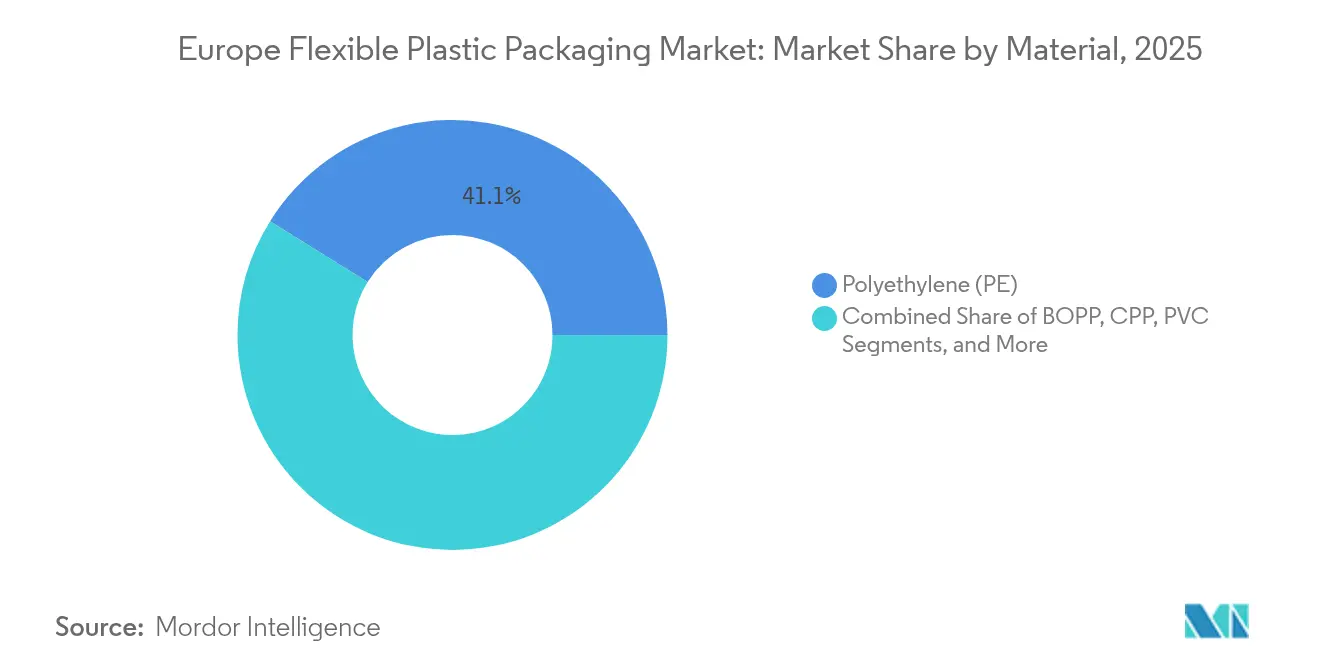

- By material type, polyethylene led with 41.12% of the Europe flexible plastic packaging market share in 2025, while BOPP is projected to expand at a 4.69% CAGR through 2031.

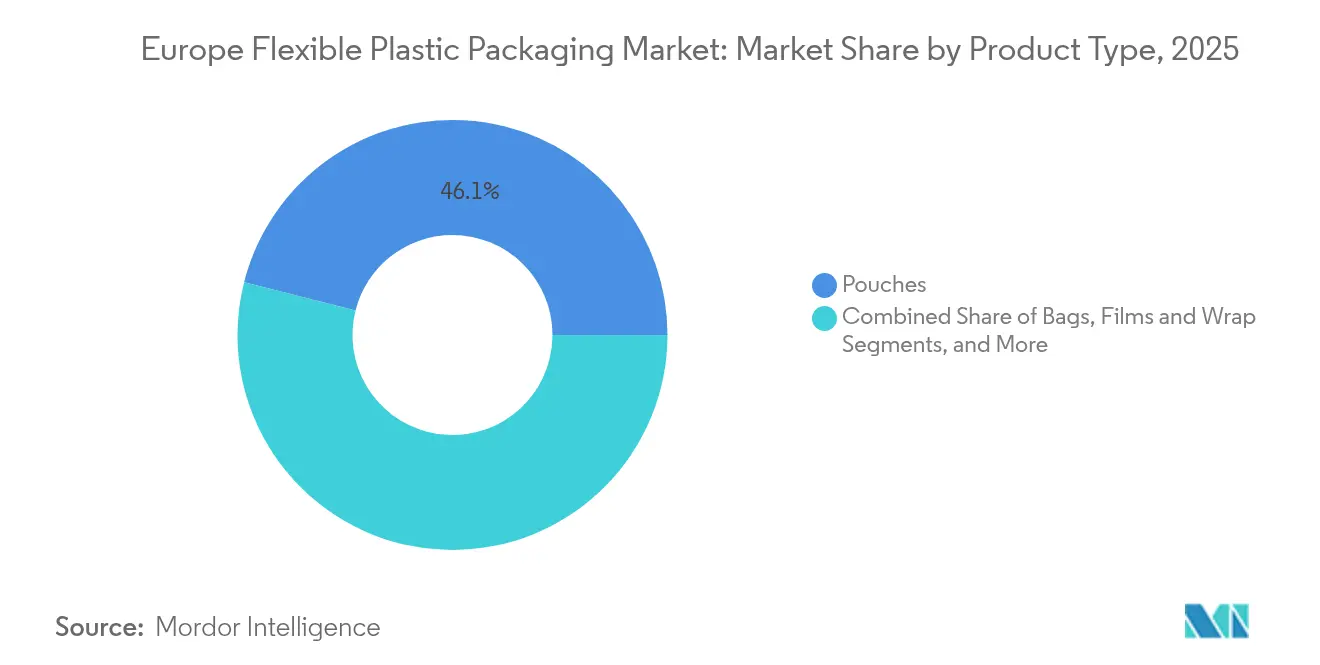

- By product type, pouches accounted for 46.05% of the Europe flexible plastic packaging market size in 2025; films and wraps are advancing at a 3.66% CAGR to 2031.

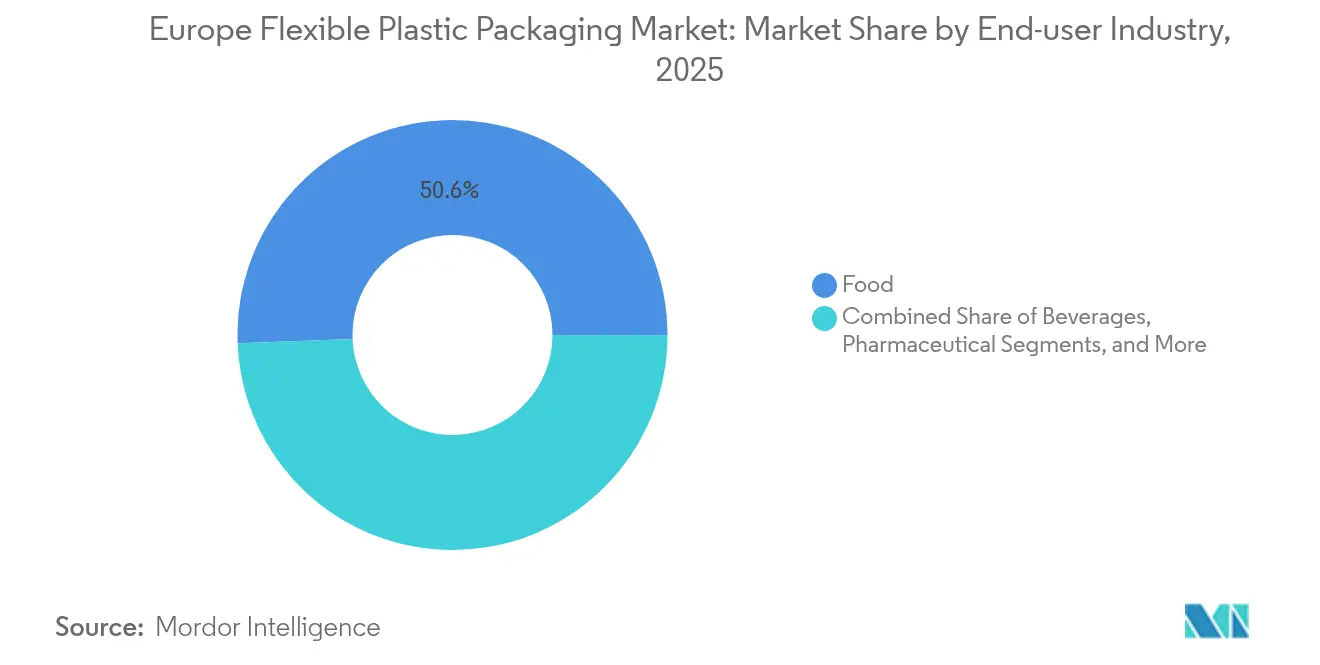

- By end-user industry, food held 50.62% revenue share in 2025, whereas pharmaceutical packaging is the fastest-growing segment at 6.31% CAGR through 2031.

- By geography, the United Kingdom led with 22.05% of the Europe flexible plastic packaging market size in 2025; the Nordics region is forecast to grow at 5.08% CAGR from 2026-2031.

- Amcor, Constantia Flexibles and Mondi together captured about 14.72% of Europe flexible plastic packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global flexible plastic packaging market data by Mordor Intelligence represents that combined structure.

Europe Flexible Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-driven retailer mandates | +0.5% | Germany, Austria, Switzerland | Medium term (2-4 years) |

| Re-closable snack & pet-food pouch demand | +0.7% | France, Belgium, Netherlands, Luxembourg | Short term (≤ 2 years) |

| Migration-safe high-barrier films adoption | +0.6% | Germany and neighboring markets | Medium term (2-4 years) |

| E-commerce parcel-ready grocery mailers | +0.4% | United Kingdom | Short term (≤ 2 years) |

| Contract-manufacturing boom in Poland | +0.3% | Poland and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustainability-driven retailer mandates across the DACH region

Retailers in Germany, Austria, and Switzerland are imposing packaging requirements that exceed statutory thresholds. Otto Group reports that 98% of its outbound packaging now meets internal recyclability or compostability specifications, including mailers made from 100% recycled “wild plastic.”[1]Otto Group, “Our Heritage: The Future,” ottogroup.com Suppliers that can document verified life-cycle savings are climbing preferred-vendor lists, prompting converters such as Jindal Films Europe to commit to releasing up to 10 novel sustainable films per year. Design optimization is likewise pivotal: retailers are factoring transport-emission metrics into bid evaluations, so lighter-gauge webs and down-gauged stand-up pouches are winning tenders. For the Europe flexible plastic packaging market, these mandates accelerate the shift to mono-material laminates and raise entry barriers for converters without robust environmental tracking systems.

Surge in re-closable snack & pet-food pouch demand in France & Benelux

Preference for portion control is elevating re-closable pouch volumes across France, Belgium, and the Netherlands. Presentations at the Future Pet Food Conference 2024 showed innovations in sliders and laser-scored tear zones that preserve oxygen and moisture barriers. United Petfood’s 2024 sustainability report confirms a strategic pivot toward mono-material zipper films that support recyclability targets. Converters able to combine re-closability with compatibility for near-infrared sorting are securing 15-20% price premiums. Rising single-person households further fuel unit-size fragmentation, making snack pouches a focus area for high-margin SKU launches in the European flexible plastic packaging market.

Migration-safe high-barrier films adoption by German meat packers

A peer-reviewed study in Foods warns of chemical leaching from traditional multilayers. German processors are therefore investing in solvent-free, EVOH-based MAP webs that hold aroma and inhibit oxidation while meeting ‘no intentional additives’ guidelines. Collaborative R&D projects between polymer scientists and machinery suppliers are producing proprietary barrier structures that pass EU 10/2011 migration limits. Early adopters in the Europe flexible plastic packaging market are realizing price uplifts through claims of reduced food waste and safer contact layers, which resonate with retailers’ quality scorecards.

E-commerce parcel-ready mailers uptake in UK grocery

Online grocery penetration surpassed 13% of food retail sales in 2024, spurring demand for flexible packs engineered for last-mile rigors. DHL’s trend report highlights corner-reinforced mailers that survive automated sortation yet fold flat for returns. UK brand owners want formats containing 30% recycled plastic to avoid the Plastic Packaging Tax.[2]United Kingdom Government, “Plastic Packaging Tax Statistics Commentary,” gov.uk QR codes and RFID options are emerging to authenticate freshness on doorstep delivery. As e-grocery continues scaling, the Europe flexible plastic packaging market is witnessing heightened specification complexity, favoring converters with integrated printing and lamination assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating EPR fees in Nordics | -0.6% | Sweden, Denmark, Finland, Norway | Medium term (2-4 years) |

| PP and PE resin price volatility | -0.4% | Pan-European, higher in Eastern Europe | Short term (≤ 2 years) |

| Consumer opposition to non-recyclable laminates | -0.3% | Germany and France | Medium term (2-4 years) |

| Labour shortages for retort-pouch lines in Spain | -0.2% | Spain and Southern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extended Producer Responsibility fees escalating in Nordics

Sweden’s polluter-pays fee tables and Denmark’s 2025 regulation, expected to cost firms USD 330 million annually, are raising variable costs for converters using multi-material laminates. Finnish data show rising tariffs for non-sorted flexible plastics. Smaller brands may exit certain SKU formats, narrowing order books for price-sensitive converters in the Europe flexible plastic packaging market.

PP & PE resin price volatility post-Ukraine conflict

Polyethylene contracts rose 3-4% in Q1 2025 versus Q4 2024, according to Flexible Packaging Europe.[3]Flexible Packaging Europe, “Press Releases,” flexpack-europe.org Such unpredictability squeezes margins for converters locked into fixed-price retail supply deals. Some brand owners are moving to index-linked contracts, yet capital-expenditure decisions on new cast lines are stalling, delaying incremental capacity in the Europe flexible plastic packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recyclable BOPP Gains Ground on Dominant PE

Polyethylene retained a 41.12% share of the Europe flexible plastic packaging market in 2025 due to its versatility and low cost. The segment’s scale offers converters economies that safeguard margins even as EPR fees rise. Yet the European flexible plastic packaging market size associated with BOPP is expanding at a 4.69% CAGR, the fastest among polymers, driven by its superior moisture and aroma barriers, which permit down-gauging without performance loss. TOPPAN’s 80% acquisition of Irplast in March 2025 underscores confidence in European demand for high-performance BOPP capable of entering polypropylene mechanical-recycling streams. Cast polypropylene occupies a niche for heat-seal and transparency-critical packs, while PVC is retreating under regulatory scrutiny, shrinking its footprint in the Europe flexible plastic packaging market. EVOH remains integral for oxygen-barrier applications but is increasingly co-extruded into mono-material PP or PE structures to avoid multi-layer EPR penalties.

Recyclability is dictating R&D investment. Jindal Films Europe targets mono-PP replacements for legacy PET/PE laminates, promising parity in stiffness and optical clarity. Converters integrating chain-of-custody PCR sources are securing long-term contracts with retailers that publicly report recycling rates. Meanwhile, volatile PP and PE feedstock pricing is pushing procurement teams toward multi-sourcing to hedge exposure. Regulatory developments, particularly the PPWR recyclability criteria, are poised to tilt market dynamics further toward materials with clear end-of-life pathways, solidifying BOPP’s trajectory inside the Europe flexible plastic packaging market.

By Product Type: Pouches Retain Primacy as Films Accelerate

Pouches accounted for 46.05% of Europe flexible plastic packaging market share in 2025 and continue gaining SKU breadth thanks to their ergonomic dispensability and high shelf-visibility. Gualapack’s Pouch5, a mono-PP stand-up pouch certified for widespread curbside collection, typifies the convergence of barrier integrity and recyclability. Multinationals such as Nestlé and Kraft Heinz leverage retort-capable spouted pouches to extend ambient shelf life, while resealable child-nutrition formats capture parental demand for portion-controlled feeding. Films and wraps, though traditionally commoditized, are registering the swiftest expansion at 3.66% CAGR, propelled by online grocery, where ship-ready overwraps reduce damage claims. Automated fulfilment centers favor thin films that combine puncture resistance with anti-slip exteriors, broadening usage beyond secondary packaging.

Bags remain vital for industrial powders and agricultural inputs but lag consumer-facing categories on innovation. Nevertheless, the shift to paper-plastic hybrids for pet-food sacs, designed for easier delamination, hints at gradual modernization. Across every format the Europe flexible plastic packaging market is converging on mono-material designs. Digital press runs of under 3,000 sqm enable late-stage customization, slashing inventory and waste. Suppliers that can demonstrate certified recyclability without compromising seal integrity will capture outsized contract renewals under stricter EPR fee schedules set for 2026-2027 across major EU economies.

By End-user Industry: Pharmaceuticals Outpace High-Volume Food

Food represented 50.62% of revenue in 2025, yet the pharmaceutical segment is advancing at 6.31% CAGR, the fastest within the Europe flexible plastic packaging industry. Demand stems from an aging population, chronic disease prevalence, and the rise of specialty biologics requiring high-barrier protection. ACG’s 2025 launch of the CelluPod paper-based blister demonstrates how pharma suppliers are diversifying beyond PVC. Otsuka Holdings’ shift to mono-material sachets trimmed total pack costs by 7% despite a 15% jump in multi-layer barrier film pricing, proving recyclability can coincide with savings. Antimicrobial and anti-counterfeit features, such as UV-responsive inks, are further differentiators, pushing average unit values above commodity food packs.

Within food, fresh produce and protein require permeability-tailored films to extend shelf life, while confections depend on high-gloss metallicized BOPP for aesthetics. Personal-care and household cleaners are migrating toward refill pouches that cut plastic use up to 70% per refill cycle. As refill stations proliferate in UK and German retailers, this loop-ready format is set to carve incremental share in the Europe flexible plastic packaging market. Beverage makers are trialing hot-fill stand-up pouches for isotonic drinks, adding variety to single-serve options. Each end-user group faces distinct compliance and branding pressures, yet all converge on the twin imperatives of robust functionality and clear post-use recovery routes.

Geography Analysis

The United Kingdom contributed 22.05% to Europe's flexible plastic packaging market size in 2025, anchored by dynamic food exporters and leading pharmaceutical fillers. The Plastic Packaging Tax collected USD 340 million in its first fiscal year; companies report an average of 32% recycled content across taxable volumes. With EPR implementation slated for 2025, brand owners are front-loading redesign projects to avoid surcharges. E-grocery leaders such as Ocado and Tesco are specifying curbside-recyclable mailers for chilled boxes, sustaining double-digit tonnage growth in films and envelopes. Brexit-related customs friction remains a latent risk, especially for resins imported from continental plants, but fluctuating exchange rates have yet to dent the United Kingdom’s influence on procurement decisions across the wider Europe flexible plastic packaging market.

Germany and France, together representing nearly one-third of regional demand, exhibit distinctive innovation vectors. Germany’s meat sector drives uptake of migration-safe high-barrier laminates, generating sustained orders for solvent-free adhesive lines. Its Packaging Act revisions obligate proof that packs are ‘design for recycling’, encouraging converters to certify mono-material output via third-party labs. France’s consumer appetite for resealable snack and pet-food pouches has boosted zipper-film capacity; laser-etch tear technology supports portion control and waste reduction. The two markets are also early adopters of digital watermarking initiatives designed to raise NIR sorting accuracy, an emerging competitive lever in the Europe flexible plastic packaging market.

The Nordics register the fastest trajectory at 5.08% CAGR through 2031. Robust deposit-return schemes and high per-capita environmental spending create favorable conditions for premium recyclable films. Denmark’s incoming EPR law, covering 41,000 firms, intensifies the compliance calculus. Sweden’s central fee model further penalizes non-sorted laminates. Converters supplying these markets must certify compatibility with established mechanical recycling flows or risk delistings. Elsewhere, Poland’s contract-manufacturing engine is lifting flexible pack volumes bound for Western retailers, while Spain contends with operational bottlenecks caused by skilled-labor shortages even as its Circular Economy Action Plan targets a 50% cut in single-use plastics by 2026. Italy maintains demand for barrier pouches safeguarding olive oil and cured meats, leveraging domestic culinary branding to sustain higher pack unit values within the Europe flexible plastic packaging market.

The flexible plastic packaging market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Latin America, Middle East and Africa, and Asia. This is complemented by country-specific insights for Spain, France, Germany, Italy, United Kingdom, and Russia, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Europe flexible plastic packaging market is fragmented, with the top five suppliers accounting for about 20% of regional turnover. Amcor’s 2025 merger with Berry Global, priced near USD 1.8 billion, enhances integrated lamination and printing assets across 55 European plants, targeting USD 650 million in annual synergies. Constantia Flexibles’ majority stake in Aluflexpack bolsters aluminium-based barrier offerings for both food and pharma. Mondi’s acquisition of Schumacher Packaging’s Western Europe plants adds corrugated integration that supports hybrid paper-plastic solutions.

Competition is intensifying around mono-material oxygen- and moisture-barrier structures. Huhtamaki’s blueloop™ portfolio features recyclable PE-based films with proprietary microwave-safe coatings, targeting ready-meal trays. Jindal Films Europe plans 10 new product launches per year, including metallized BOPP that meets PP stream recyclability guidelines. Smaller disruptors are leveraging digital print to offer mass-customized pouches in weeks, undercutting large incumbents on agility. However, rising EPR costs and complex regulatory audits favor well-capitalized players able to self-certify design-for-recycling scores, prompting further consolidation in the Europe flexible plastic packaging market.

Strategic collaboration with resin producers and recycling firms is now standard. Amcor’s pilot with Borealis on chemically recycled polypropylene demonstrates value-chain integration aimed at guaranteed feedstock supply. Meanwhile, Constantia Flexibles partners with Tomra to validate NIR detectability of new wrapper substrates, enabling immediate sort-line acceptance. Participation in cross-industry alliances, such as Ceflex, adds lobbying power as PPWR secondary legislation crystallizes. Investment in mechanical and chemical recycling capacity is becoming a differentiator, including direct equity stakes in reclaim plants to ensure PCR availability for premium brand contracts.

Europe Flexible Plastic Packaging Industry Leaders

Constantia Flexibles

ALPLA Group

Huhtamaki Oyj

Amcor PLC

Mondi PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed its all-stock combination with Berry Global, creating a global packaging leader with projected USD 650 million synergies.

- April 2025: Mondi finalized the purchase of Schumacher Packaging’s Western Europe operations, expanding capacity in sustainable formats.

- March 2025: TOPPAN acquired 80% of BOPP specialist Irplast, strengthening recyclable mono-material film development.

- March 2025: Constantia Flexibles took a majority stake in Aluflexpack AG, enhancing food and pharma barrier capabilities.

- January 2025: ACG unveiled CelluPod paper-based blisters and PVC-free pharma packs at Pharmapack Europe.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe flexible plastic packaging market as all primary and secondary packs produced within Europe that are made chiefly from pliable plastic films, such as mono-PE, BOPP, CPP, PVC, EVOH, and related blends, converted into pouches, bags, wraps, or rollstock used across food, beverage, household, personal care, and pharmaceutical channels.

Scope Exclusions: Rigid containers, aluminum or paper-only laminates, transport sacks, and bulk industrial liners are not included.

Segmentation Overview

- By Material Type

- Polyethylene (PE)

- Bi-oriented Polypropylene (BOPP)

- Cast Polypropylene (CPP)

- Polyvinyl Chloride (PVC)

- Ethylene Vinyl Alcohol (EVOH)

- Other Material Types

- By Product Type

- Pouches

- Bags

- Films and Wraps

- Other Product Types

- By End-user Industry

- Food

- Confectionery and Snacks

- Breads and Cereals

- Fresh Produce

- Dairy based products

- Other Food Products

- Beverage

- Non-Alcoholic Beverages

- Dairy based Drinks

- Juices

- Sports and Energy Drinks

- Flavoured Water

- Other Non-Alcoholic Beverages

- Alcoholic Beverages

- Cocktails and Pre-Mixed Drinks

- Wine and Spirits

- Non-Alcoholic Beverages

- Personal Care and Household Care

- Pharmaceutical

- Other Industries

- Food

- By Country

- United Kingdom

- Germany

- France

- Italy

- Poland

- Spain

- Nordics

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed converters, resin suppliers, and packaging buyers in Germany, Italy, the UK, and Poland. Discussions tested run-rate capacities, PCR content premiums, and end-user switch rates from rigid to flexible formats, letting us refine assumptions uncovered during desk work and stress test early volume estimates.

Desk Research

We pooled trade-flow statistics from Eurostat's Comext, converter capacity files issued by Flexible Packaging Europe, and national packaging waste registers to size polymer flows by grade. Regulatory texts, such as EU PPWR drafts and UK Plastic Packaging Tax guidance, clarified recyclability thresholds, while patent abstracts on mono-material barrier films sourced through Questel helped benchmark technology adoption. Company 10-Ks, investor decks, and Factiva news streams supplied average selling prices and plant utilization clues. This list is illustrative; many additional open and paid references informed the desk phase.

Market-Sizing & Forecasting

A top-down reconstruction converts Eurostat production plus net imports of flexible film into finished pack equivalents, applying loss factors and conversion yields. Results are cross-checked with sampled bottom-up roll-ups that multiply average selling price by indicative output at fifteen leading plants. Key variables in the model include resin price spreads, EPR fee escalators, pouch penetration in ambient foods, e-commerce parcel volumes, and mandated recycled content targets. Forecasts rely on multivariate regression linking these drivers to historic pack demand and are moderated through scenario analysis where policy timetables or resin volatility diverge. Data gaps in supplier roll-ups are filled using median yields from peer plants of comparable gauge and run length.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, peer analyst reconciliation, and a senior sign-off. Our figures refresh each year and are reopened sooner if material events, such as resin duty shifts or a major merger, alter supply or price baselines. A last verification is always run before final delivery.

Why Mordor's Europe Flexible Plastic Packaging Baseline Commands Reliability

Published estimates often differ because firms pick unlike material scopes, diverging recycled content assumptions, or distinct refresh cadences.

Key Gap Drivers: Competitors sometimes bundle paper or foil laminates, ignore duty-paid import inflows, or apply static average selling prices despite quarterly resin swings, whereas Mordor's model adjusts for those factors and is updated annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 58.92 B (2025) | Mordor Intelligence | - |

| USD 63.17 B (2025) | Global Consultancy A | Includes paper-based flexibles and composite laminates, inflating value |

| USD 55.87 B (2023) | Industry Journal B | Uses pre-tax ASPs from 2022 and omits Polish converter expansion |

Taken together, the comparison shows that when consistent scope, current prices, and verified trade data are applied, Mordor's balanced baseline offers decision makers a dependable, transparent point of departure for sizing opportunities and tracking regulatory impacts.

Key Questions Answered in the Report

What is the current value of the Europe flexible plastic packaging market?

The market stands at USD 60.39 billion in 2026 and is projected to climb to USD 68.34 billion by 2031.

Which product format dominates sales across Europe?

Pouches hold 46.05% share owing to consumer convenience and retailer shelf-efficiency advantages.

Why is BOPP growing faster than other packaging polymers?

BOPP’s strong barrier performance combined with full compatibility in polypropylene recycling streams is driving a 4.69% CAGR through 2031.

How do Extended Producer Responsibility fees affect brand owners?

Higher EPR tariffs in markets like Sweden and Denmark penalize hard-to-recycle laminates, pushing design teams toward mono-material solutions to cut compliance costs.

Which end-use sector is expanding at the highest rate?

Pharmaceutical applications are advancing at 6.31% CAGR, spurred by stringent safety rules and rising home-health deliveries.

What strategic moves are leading companies making?

Amcor merged with Berry Global for scale in recyclable films, Constantia Flexibles bought Aluflexpack for aluminium barrier assets, and Mondi expanded capacity through Schumacher Packaging acquisitions, all aiming to strengthen sustainable offerings in Europe.

Page last updated on: