Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

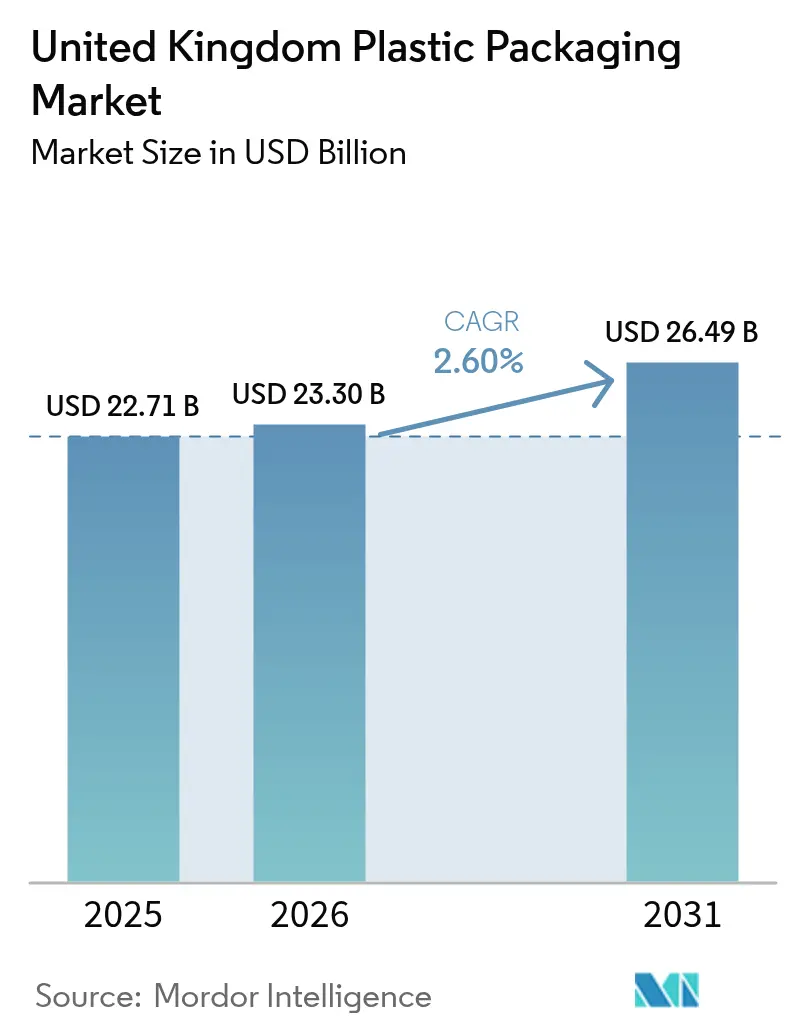

| Base Year Market Size (2025) | USD 22.71 Billion |

| Market Size (2026) | USD 23.3 Billion |

| Market Size (2031) | USD 26.49 Billion |

| Growth Rate (2026 - 2031) | 2.60% CAGR |

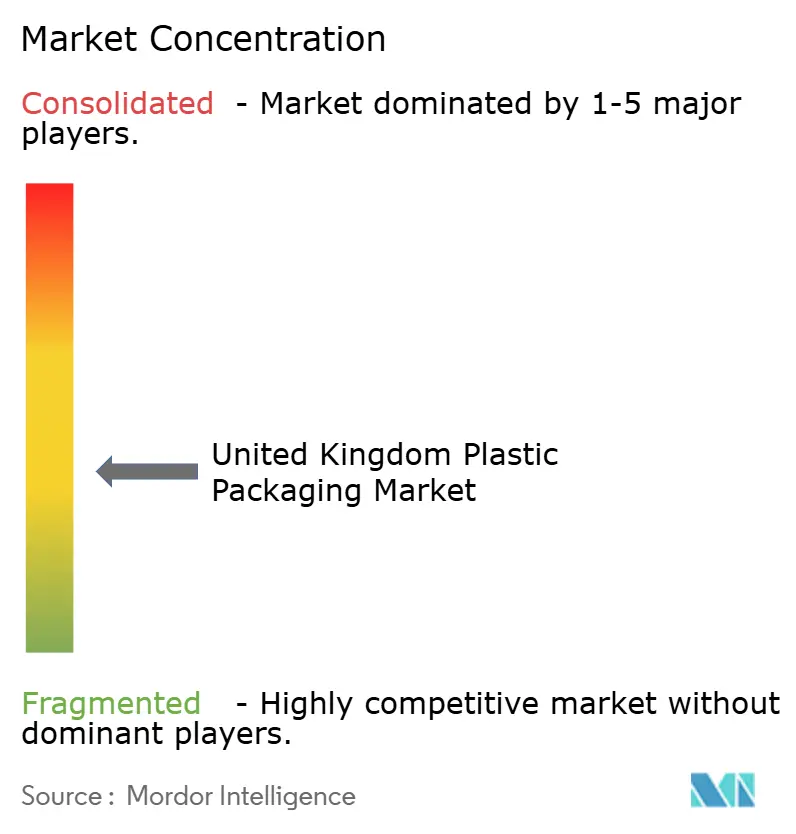

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Plastic Packaging Market Analysis by Mordor Intelligence

The United Kingdom plastic packaging market size in 2026 is estimated at USD 23.3 billion, growing from 2025 value of USD 22.71 billion with 2031 projections showing USD 26.49 billion, growing at 2.6% CAGR over 2026-2031. The shift from volume to value is reshaping pricing power as sustainability premiums and regulatory compliance costs are embedded into contracts. Chemical recycling pilots, mono-material barrier films, and refillable delivery systems are redefining design rules while acting as early indicators for global circular-economy standards. Flexible formats advance at the expense of rigid options, driven by e-commerce logistics and lightweight convenience requirements. Material substitution decisions increasingly weigh feedstock volatility, tax incentives, and consumer perception of recycled content.

Key Report Takeaways

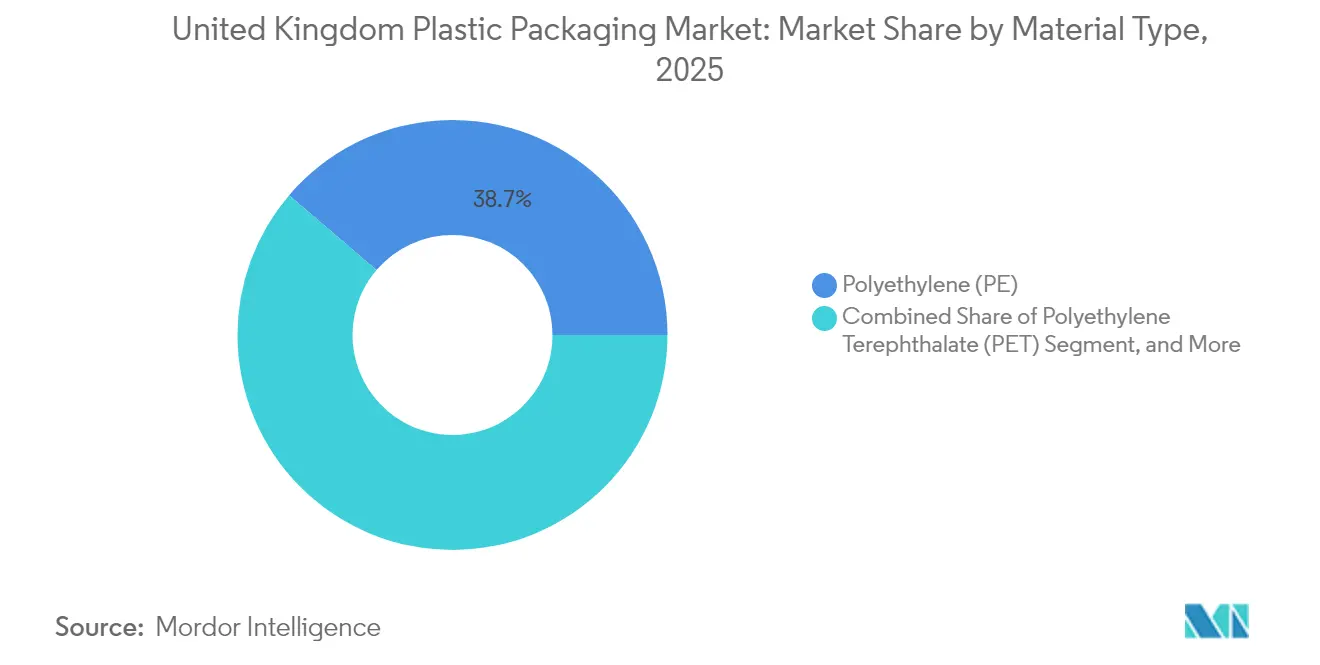

- By material type, polyethylene held 38.74% of the United Kingdom plastic packaging market share in 2025, while polyethylene terephthalate is forecast to post the fastest 3.41% CAGR through 2031.

- By packaging type, flexible solutions commanded 55.32% revenue in 2025, and the same segment is set to expand at a 3.71% CAGR to 2031.

- By product form, pouches and sachets contributed 31.05% of the United Kingdom plastic packaging market size in 2025, whereas films and wraps are projected to rise at a 4.04% CAGR between 2026 and 2031.

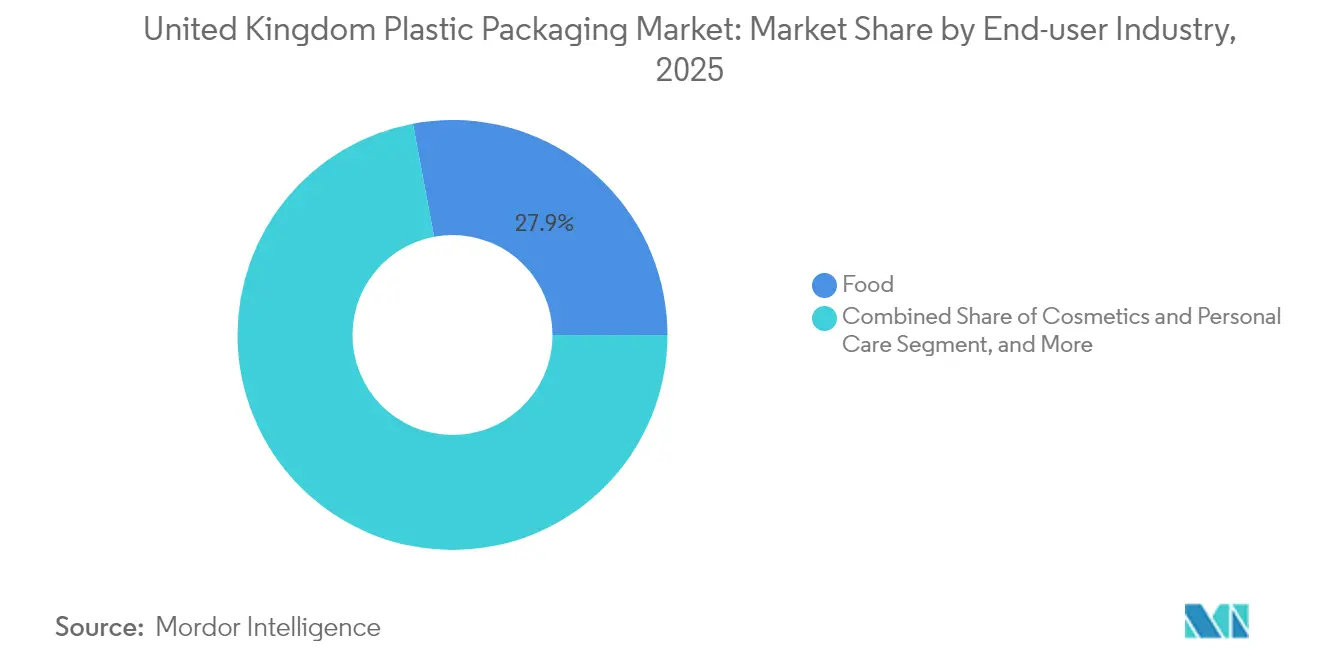

- By end-user industry, food applications secured a 27.95% share in 2025, but cosmetics and personal care are heading for the highest 4.88% CAGR to 2031.

- By manufacturing process, extrusion led with 27.86% revenue share in 2025, yet thermoforming is anticipated to deliver a 4.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight convenience formats | +0.8% | United Kingdom-wide, urban centers | Medium term (2-4 years) |

| E-commerce protective packaging | +0.6% | Nationwide, highest in London and Manchester | Short term (≤2 years) |

| Recycled-content plastics under 30% tax | +0.4% | Nationwide, regulation driven | Long term (≥4 years) |

| Chemical recycling capacity scale-up | +0.3% | North England and Scotland clusters | Long term (≥4 years) |

| United Kingdom Plastics Packaging Tax effect | +0.5% | Nationwide, mandatory compliance | Medium term (2-4 years) |

| Mono-material high-barrier films | +0.2% | Nationwide, municipal collection dependent | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight Convenience Formats

Urban consumers prioritize portability and portion control, encouraging 15-20% material reductions versus legacy rigid packs. Single-dose formats extend from snacks to pharmaceuticals, lowering contamination risk while boosting adherence. Coveris introduced its MonoFlexBP resealable tray line in September 2025, merging easy-open functionality with curbside recyclability. Aging populations and busier lifestyles sustain demand for formats that trade bulk economics for usability, supporting steady margin expansion for converters that optimize downgauging.

Growth in E-commerce Protective Packaging

Online order volumes are subject packs to high compression, puncture, and drop forces across multiple shipping cycles. Engineered films and void-fill systems balance strength with dimensional-weight savings, cutting freight costs and damage claims. TekniPlex Healthcare’s March 2025 capacity boost targets temperature-controlled and tamper-evident pharma shipments, underscoring channel-specific needs. Logistics-optimized designs translate directly into customer satisfaction metrics and repeat-purchase propensity.

Uptake of Recycled-Content Plastics Under 30% Tax

The GBP 200 per tonne levy on packs containing under 30% recycled content compels vertical integration and feedstock contracts to guarantee supply. HMRC guidance validates mass-balance chemical recycling within the threshold, broadening compliance options.[1]United Kingdom Government, “Single-use plastic wet wipes ban,” gov.uk The framework anchors a two-tier pricing landscape that rewards investment in recycled resin and penalizes virgin dependency, positioning first movers for cross-border advantage as similar mandates proliferate in Europe.

Chemical Recycling Capacity Scale-Up

Pyrolysis and gasification plants progress from pilot to commercial scale, processing contaminated and mixed residual streams unsuited to mechanical recycling. Dow and Mura Technology’s partnership exemplifies regional build-out that will shorten feedstock haulage distances and support closed-loop food-grade output. Economic viability improves as carbon-pricing schemes elevate landfill and incineration costs, narrowing the gap with virgin polymer pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile resin prices linked to energy costs | −0.7% | Nationwide, manufacturing hubs most exposed | Short term (≤2 years) |

| Single-use plastics regulations | −0.4% | Nationwide, foodservice and retail hot spots | Medium term (2-4 years) |

| Retailer refill/re-use pilots | −0.3% | Urban retail centers | Long term (≥4 years) |

| Micro-plastics backlash | −0.2% | Consumer goods sectors nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Resin Prices Linked to Energy Costs

Ethylene and propylene production accounts for roughly 60-70% of cracker operating costs, so swings in natural-gas inputs distort converter margins. The British Plastics Federation recorded pronounced PE and PP price turbulence in July 2025, forcing buyers to adopt hedging tools and shorter contracts that raise administrative burden. Importers face dual exposure to euro and U.S.-dollar swings against sterling, complicating cost forecasting and inventory strategies.

Single-Use Plastics Regulations

Targeted bans, such as the April 2024 wet-wipe prohibition, compel rapid redesign or material substitution, often with higher unit costs and performance trade-offs. Compliance audits demand new traceability systems and supplier certifications that raise overhead. In foodservice, bans on specific cutlery and plates mandate compostable or paper alternatives that may lack durability, potentially elevating food-waste rates and undermining sustainability narratives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene Dominance, PET Innovation

Polyethylene, spanning LDPE, LLDPE, and HDPE grades, retained 38.74 of % United Kingdom plastic packaging market share in 2025 because of processing ease and cost-performance balance in films. Polyethylene terephthalate is on course for a 3.41% CAGR with beverage lightweighting and ready-meal trays fueling demand. Converters value PET’s clarity and gas barrier, paying the premium for thinner walls and hotter-fill tolerance. Mechanical recycling rates favor clear PET, catalyzing brand commitments to food-grade rPET integration. Polypropylene’s colored variants lag recycling advances, limiting volume growth. Polystyrene use wanes under disposability scrutiny, while engineered resins and emerging biopolymers occupy specialized niches where functional gains justify higher costs.

Recycled-content mandates push polyolefin advancements such as odor-removal additives and compatibilizers that elevate post-consumer blend quality. Innovia Films debuted a PVC-free coater in April 2025 to eliminate halogen concerns while protecting oxygen-sensitive foods. Long term, material portfolios will reflect a disciplined trade-off between regulatory risk, circularity credentials, and application-specific performance needs within the United Kingdom plastic packaging market.

By Packaging Type: Flexible Formats Consolidate Leadership

Flexible solutions delivered 55.32% revenue in 2025 and are projected to achieve a 3.71% CAGR to 2031. A single auto-form seal pouch can cut material use by up to 70% versus a comparable rigid option, reducing freight emissions and waste-handling charges. Coveris’s August 2025 MonoFlex Thermoform pack for tortillas extends mono-material flexibles into categories once dominated by rigid trays.

Rigid containers remain relevant for carbonated beverages, fragrances, and heavy-duty chemicals requiring stand-up stability and tamper resistance, yet landfill levies and Extended Producer Responsibility fees constrain growth. As multilayer film recycling technologies mature, flexible adoption is expected to permeate cosmetics and household cleaners, accelerating the United Kingdom plastic packaging market transition toward leaner supply chains.

By Product Form: Pouches Lead, Films Accelerate

Pouches and sachets accounted for 31.05% of the United Kingdom plastic packaging market size in 2025, thanks to portion control trends, easy-tear functionality, and improved high-speed filling compatibility. High-growth films and wraps, projected at a 4.04% CAGR, address the rise of omnichannel retail by protecting mixed SKUs during courier transit. Automated pallet-wrap systems combine stretch and shrink films to stabilize loads while optimizing cube utilization.

Bottles and jars continue to serve premium spirits and skin-care serums, where shelf presence and re-closability support brand equity. Rigid trays cater to ready meals that demand oven or microwave endurance, but film-sealed paperboard hybrids are beginning to erode share. DS Smith’s TailorTemp launch in January 2025 fuses thermal insulation with lightweight board to challenge EPS boxes in cold-chain routes.

By End-User Industry: Food Stability, Cosmetics Upswing

Food applications delivered 27.95% revenue in 2025, underpinned by stringent hygiene regulations and extended life requirements. Mono-material barrier films that withstand high-pressure processing or retort sterilization are being fast-tracked to satisfy supermarkets’ recyclability targets without compromising safety. Cosmetics and personal care, rising at a 4.88% CAGR, champion airless pumps, refill pods, and recycled PET jars that reinforce eco-premium positioning.

Meadow’s Daisy Top refill cap, recognized in September 2024, trims primary-pack tonnage by up to 70% and boosts repeat purchase frequency via convenient replenishment. Pharmaceuticals prioritize tamper-evidence and anti-counterfeit embossing, enabling suppliers to command higher margins for specialty features. Industrial bulk liners focus on puncture strength and static dissipative properties, but face slow growth as commodity cycles plateau.

By Manufacturing Process: Extrusion Scale, Thermoforming Precision

Extrusion generated a 27.86% share in 2025 on the back of high-output blown-film lines servicing food and e-commerce applications. Process tweaks, including inter-layer bubble cooling, let converters push thinner gauges without sacrificing toughness. Thermoforming is predicted to clock a 4.81% CAGR through 2031 as portion-controlled ready meals, medical drapes, and shell-and-lid combos demand tight tolerances and stackable profiles.

Broanmain Plastics installed automated robotic demolding in March 2025 to offset labor shortages and elevate repeatability. Injection molding supports caps and closures integrating tethered features mandated by EU directives, while blow molding innovations deliver 25% weight cuts in HDPE milk bottles via optimized parison programming. Emerging rotational molding niches include reusable bulk-dispense cartridges for refill stations, reflecting wider system redesign efforts across the United Kingdom plastic packaging market.

Geography Analysis

London and the South East channel premium cosmetic and specialty-food volumes, reinforcing demand for high-clarity rPET and decorated stand-up pouches. Northern England and Scotland, anchored by petrochemical clusters, favor industrial and food processing packs and host multiple announced chemical-recycling builds, granting converters localized feedstock advantages. Scotland’s Circular Economy Act imposes aggressive recycled-content thresholds ahead of national timetables, incentivizing early supplier alignment. Wales is piloting reuse-inclusive deposit return schemes, hinting at design divergence that multiregional brand owners must anticipate.

The Department for Environment, Food and Rural Affairs confirmed a United Kingdom-wide deposit return scheme go-live date of October 2027, giving bottle producers a firm horizon for tethered-closure and label-adhesive modifications. Simpler Recycling rules, effective March 2026, harmonize household material segregation, unlocking broader mechanical-recycling yield for mono-material flexibles. Local authorities still vary in sorting technology investment, dictating nuanced pack-format decisions. Northern Ireland’s alignment reduces cross-border complexity but requires vigilance against differing post-Brexit customs enforcement.

Regional development funds are channeling grants into polymer de-inking, odor-removal, and composite delamination projects, accelerating technology diffusion outside traditional manufacturing bases. Converters clustered in the Midlands benefit from motorway proximity but remain exposed to natural-gas volatility concentrated in large-scale industrial estates. As recycled-content pipelines stabilize, proximity to depolymerization units may outstrip historical proximity to end-use markets in strategic weightings for future plant siting across the United Kingdom plastic packaging market.

Competitive Landscape

The market is moderately fragmented, yet consolidation is quickening as sustainability investments stretch balance sheets. Amcor’s 2025 merger with Berry Global positions the combined entity to leverage in-house chemical-recycling offtake and negotiate multi-year feedstock agreements, lowering input cost risk. Constantia Flexibles’ May 2025 coffee-pack partnership on recyclable barrier films illustrates how collaborative R and D accelerates niche solutions.[3]Constantia Flexibles, “Recyclable coffee packs partnership,” constantiaflexibles.com Smaller converters gravitate to bespoke runs, rapid lead times, and localized service to defend share against integrated multinationals.

Strategic moves center on vertical integration, with converters procuring stakes in recycling plants to lock in PCR resin and satisfy 30% thresholds. Others double down on design-for-recycling advisory, embedding themselves in early brand development stages. White-space innovations include refill-ready rigid shells paired with flexible liners and paper-based hybrids designed for curbside sort lines. The competitive narrative is moving from price per unit toward verified environmental performance, certified traceability, and consumer experience differentiation within the United Kingdom plastic packaging market.

United Kingdom Plastic Packaging Industry Leaders

Amcor PLC

Sealed Air Corporation

Polystar Plastics Ltd

Coveris Holdings SA

Constantia Flexibles GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Coveris launched MonoFlexBP resealable trays targeting ready meals.

- May 2025: Constantia Flexibles partnered with a coffee-brand owner to deliver recyclable high-barrier films.

- April 2025: Innovia Films introduced a PVC-free coater to eliminate halogens in flexible packs.

- March 2025: TekniPlex Healthcare expanded capacity for pharma e-commerce packaging.

United Kingdom Plastic Packaging Market Report Scope

Plastic packaging is a part of the multi-faceted system for providing products, from the point of manufacture to the point of consumption. Its principal purpose is to guard and ensure the safe and secure delivery of the product in its flawless and perfect condition to the end user (manufacturer of the product or the consumer). Its role in a circular economy is to sustain the value of a product for as long as required and help remove product waste.

The UK plastic packaging market is segmented by packaging type (rigid plastic packaging and flexible plastic packaging), product type (bottles and jars, trays and containers, pouches, bags, and films and wraps), and end-user industry (food, beverage, healthcare, personal care, and household). The market sizes and forecasts are provided in terms of value (in USD million) for all the above segments.

By Material Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

By Packaging Type

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

By Product Form

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

By End-User Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Manufacturing Process

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Other Manufacturing Processes |

| By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and EPS | |

| Other Material Types | |

| By Packaging Type | Flexible Plastic Packaging |

| Rigid Plastic Packaging | |

| By Product Form | Bottles and Jars |

| Trays and Containers | |

| Pouches and Sachets | |

| Bags and Sacks | |

| Films and Wraps | |

| Other Product Forms | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceuticals and Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries | |

| By Manufacturing Process | Extrusion |

| Injection Molding | |

| Blow Molding | |

| Thermoforming | |

| Other Manufacturing Processes |

Key Questions Answered in the Report

What is the 2026 value of the United Kingdom plastic packaging market?

The United Kingdom plastic packaging market size is USD 23.3 billion in 2026.

How fast is the market projected to grow?

It is expected to rise at a 2.6% CAGR, reaching USD 26.49 billion by 2031.

Which packaging type is expanding the quickest?

Flexible formats lead growth with a projected 3.71% CAGR through 2031, fueled by e-commerce logistics demand.

Which material commands the largest market share?

Polyethylene holds 38.74% of 2025 revenue due to versatility across films and rigid containers.

How does the Plastics Packaging Tax influence material choice?

The GBP 200 (USD 270.14) per tonne levy for packs under 30% recycled content financially favors recycled resin and accelerates design shifts toward mono-material solutions.

Page last updated on: