Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

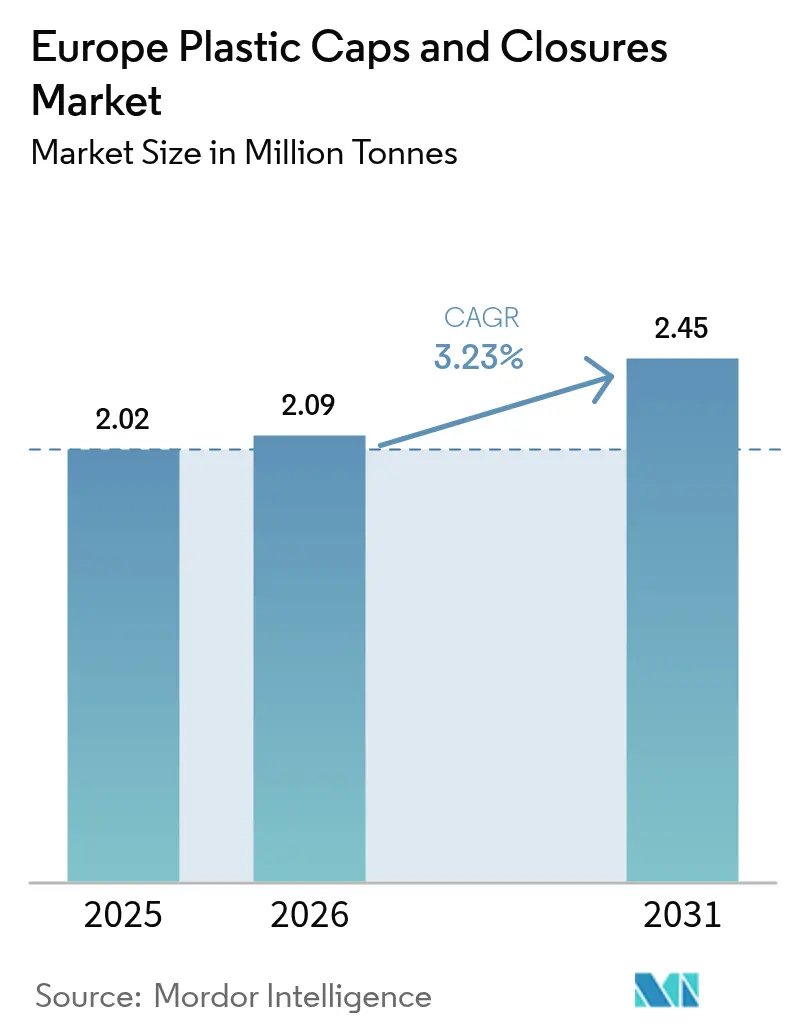

| Base Year Market Size (2025) | 2.02 Million tonnes |

| Market Volume (2026) | 2.09 Million tonnes |

| Market Volume (2031) | 2.45 Million tonnes |

| Growth Rate (2026 - 2031) | 3.23% CAGR |

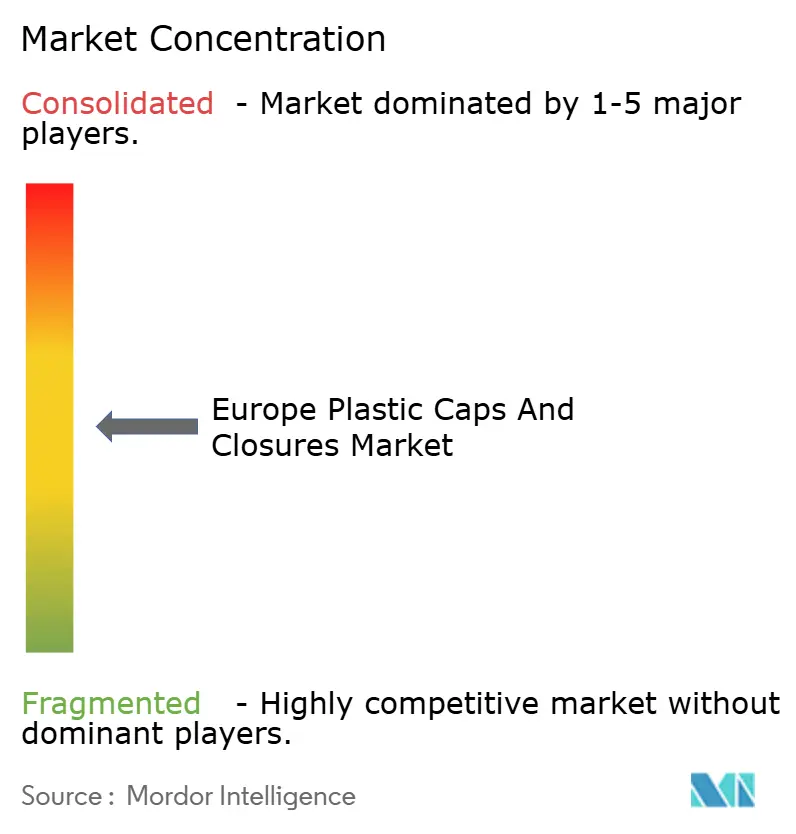

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Plastic Caps And Closures Market Analysis by Mordor Intelligence

The Europe plastic caps and closures market size is projected to be 2.02 Million Tonnes in 2025, 2.09 Million Tonnes in 2026, and reach 2.45 Million Tonnes by 2031, growing at a CAGR of 3.23% from 2026 to 2031. Brand owners are racing to retrofit tethered-cap designs before enforcement penalties bite, even as lightweighting rules pressure converters to shave grams without jeopardizing seal integrity. Recycled-content quotas under Regulation 2025/40 have shifted material choices toward food-grade rPET and rHDPE, tightening resin supply and nudging converters into backward integration deals. Flexible pouches are eliminating closures in certain household-chemical lines, yet premium cosmetics, dairy RTD, and craft spirits continue to specify higher-value dispensing and tamper-evident formats, balancing the competitive landscape. Leading suppliers are therefore diversifying across dispensing technologies and verticalizing into recycling to stabilize margins as the Europe plastic caps and closures market navigates its next legislative wave.

Key Report Takeaways

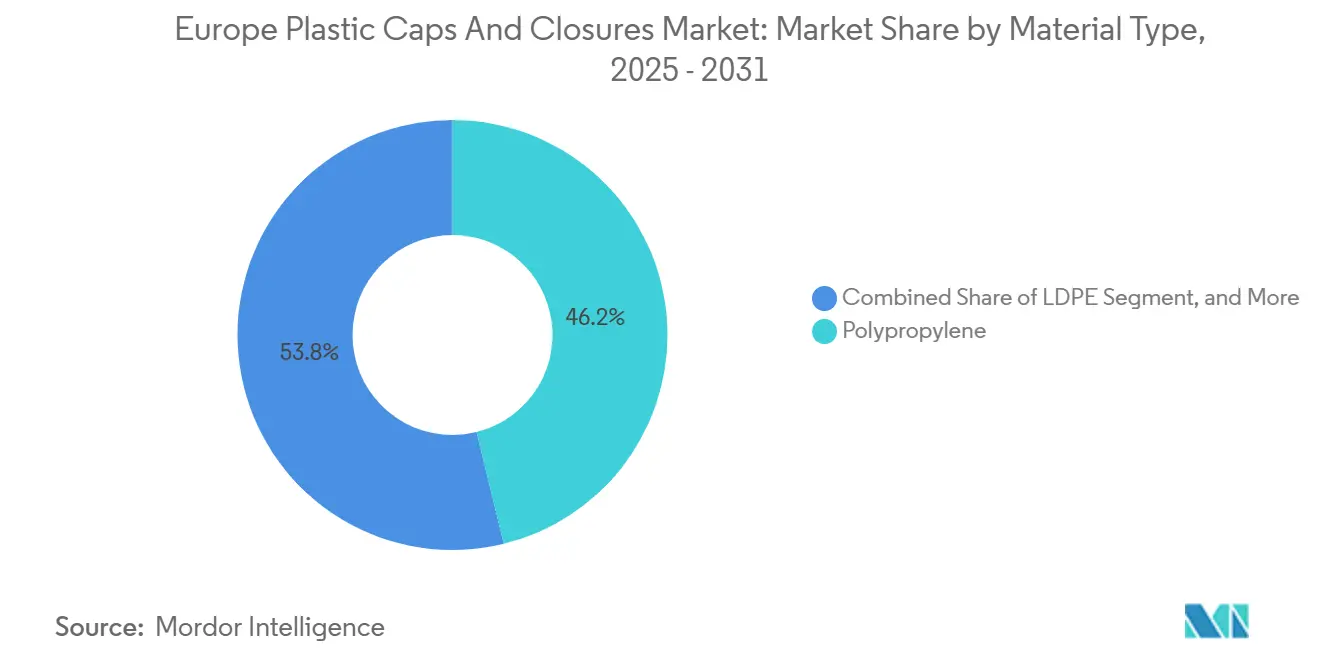

- By material type, polypropylene captured 46.16% of the Europe plastic caps and closures market share in 2025, while low-density polyethylene is advancing at a 5.52% CAGR through 2031.

- By product type, screw caps accounted for 57.85% revenue share in 2025; dispensing closures are set to expand at a 5.21% CAGR to 2031.

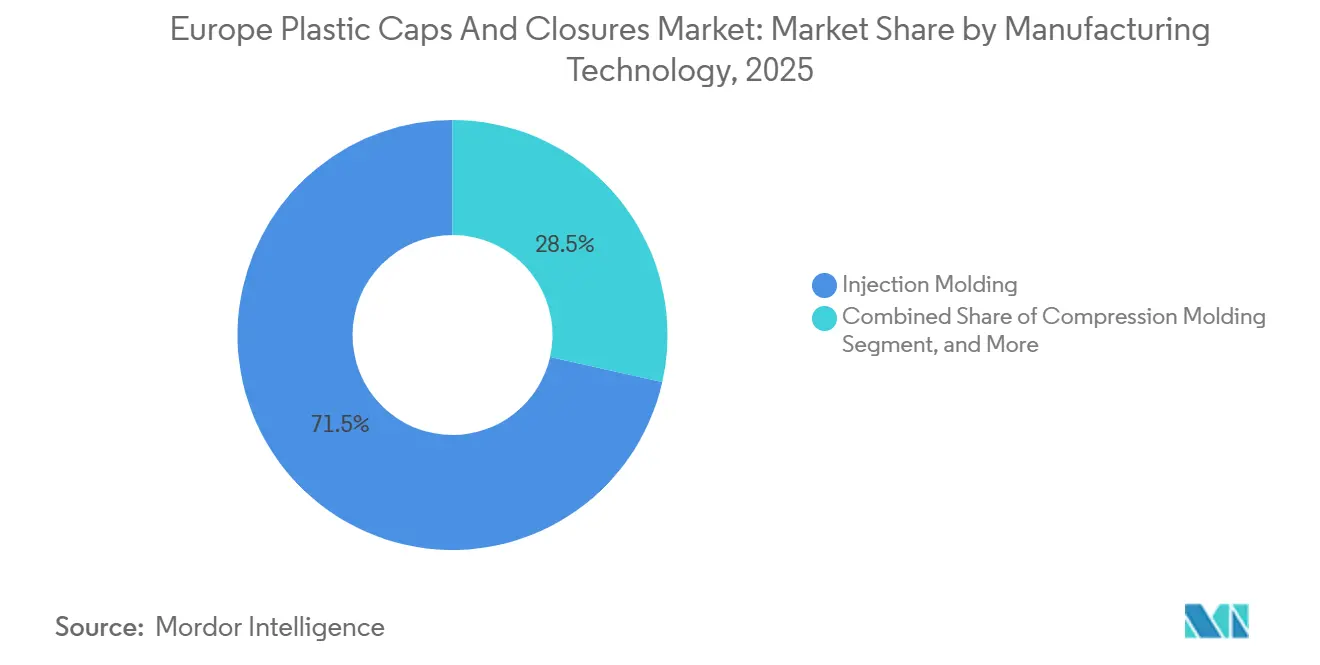

- By manufacturing technology, injection moulding held 71.49% of the Europe plastic caps and closures market size in 2025, whereas compression moulding is forecast to rise at a 4.91% CAGR.

- By end-user industry, beverage applications led with 42.75% share of the Europe plastic caps and closures market size in 2025, while cosmetics and toiletries register the fastest growth at 4.96% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Plastic Caps And Closures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting Mandates from EU Packaging and Packaging-Waste Regulation | +0.90% | EU-27, with early compliance in Germany, France, Netherlands | Medium term (2-4 years) |

| High Adoption of Tethered Caps Ahead of 2024 EU Directive Deadline | +1.20% | EU-27, particularly beverage-intensive markets (Germany, Spain, Italy) | Short term (≤ 2 years) |

| Growing Demand for High-Barrier, Aseptic-Ready Closures in Dairy RTD Lines | +0.70% | Western Europe (Germany, France, UK), expanding to Poland, Czech Republic | Medium term (2-4 years) |

| Brand-Owner Shift Toward Recycled-Content Caps | +0.80% | EU-27, driven by France, Germany, Benelux sustainability mandates | Long term (≥ 4 years) |

| Craft Spirits Boom Driving Premium, Tamper-Evident Closures | +0.50% | UK, Ireland, Germany, Scandinavia | Medium term (2-4 years) |

| Rapid Growth of E-Commerce Refill Formats Requiring Leak-Proof Closures | +0.60% | Western Europe urban centers, expanding to Southern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Adoption of Tethered Caps Ahead of the 2024 Deadline

Demand for tethered designs spiked once the Single-Use Plastics Directive became enforceable, forcing 450 million beverage lines to retool at speed. Orders at Guala Closures surged 340% in 2024, stretching mold lead times to 16 weeks. The new hinges must withstand 10,000 open-close cycles, effectively excluding commodity PP grades. Patent-protected stress-relief grooves from BERICAP keep failure rates below 0.5% in field trials. Although tethering raises per-cap resin use by 8-12%, the design is now non-negotiable for carbonated drinks, locking in a near-term volume uplift for the Europe plastic caps and closures market.

Lightweighting Mandates from EU Packaging Regulation

Regulation 2025/40 caps closure mass and links compliance to design-for-recycling criteria under ISO 18604. Coca-Cola European Partners reported an 18% resin saving after switching to thin-wall caps, equivalent to 12,000 metric tons in 2025. Thin walls, however, risk hinge brittleness at sub-zero haulage temperatures, pushing converters toward higher-molecular-weight PP grades. Precision tooling for sub-2-gram closures gives early movers a cost edge, even as higher scrap rates accompany the learning curve. The combined effect is a measurable 0.9% uplift to CAGR across the forecast period.

Aseptic-Ready Closure Demand in Dairy RTD Lines

Shelf-stable dairy and plant-based beverages need closures that survive 135 °C filling and 90-day ambient storage. Multi-layer liners with EVOH keep oxygen ingress below 0.5 cm³ per day, extending flavour life. A EUR 35 million (USD 39.6 million) German line will add 800 million aseptic caps annually by 2026. Premium closures fetch 40-60% price uplifts, securing a 0.7% push on market CAGR as brands pay for cold-chain avoidance.

Brand-Owner Shift Toward Recycled-Content Caps

Amcor lifted its rHDPE usage to 18% in 2025 by tapping chemical-recycling streams. Food-grade rHDPE trades at a 25-35% premium, but vertical integration and long-term offtake agreements are narrowing differentials. Scarcity of recycled PP that meets EFSA limits keeps supply tight, positioning recyclate access as a competitive moat. Model projections assign an extra 0.8% boost to CAGR for the Europe plastic caps and closures market as recycled-content mandates scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stand-Up Pouches Encroaching on Household-Chemical SKUs | -0.60% | Western Europe, particularly UK, Germany, France | Medium term (2-4 years) |

| Deposit-Return Schemes Steering Beverage Players to Aluminum Cans | -0.90% | Germany, Netherlands, Scandinavia, expanding to France, Spain | Short term (≤ 2 years) |

| Lack of Continent-Wide rPET/rHDPE Food-Grade Supply | -0.50% | EU-27, acute in Southern and Eastern Europe | Long term (≥ 4 years) |

| High Capital Intensity for Tethered-Cap Retrofits in Legacy PET Lines | -0.70% | EU-27, concentrated in Italy, Spain, Poland with aging bottling infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Deposit-Return Schemes Steering Brands Toward Aluminium Cans

Collection rates for cans now exceed 92% in key DRS markets, compared with 78-82% for PET bottles. Coca-Cola Europacific Partners raised its can mix to 38% of European volume in 2025. Each 1-point share shift removes 450 million plastic closures per year, a structural drag that subtracts 0.9% from forecast CAGR. Closure suppliers are pivoting toward non-carbonated beverages and functional waters to cushion the blow.

High Capital Intensity for Tethered-Cap Retrofits

Older PET bottling lines, especially in Italy and Spain, need EUR 8-10 million (USD 9-11 million) upgrades to handle tethered closures, often exceeding mid-tier converters’ financing capacity. Licensing fees for patented hinges add ongoing royalty burdens. These economics deter reinvestment, locking in a -0.7% CAGR impact for the Europe plastic caps and closures market as some plants downsize or exit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polypropylene Anchors Beverage Demand

Polypropylene claimed 46.16% of the Europe plastic caps and closures market share in 2025 because it balances heat resistance with low unit cost. Growth skews toward low-density polyethylene, which is advancing at a 5.52% CAGR through 2031 as squeezable tubes in beauty and condiment lines favour softer resins for fingertip control.

Lower melt viscosity allows LDPE to form thinner walls, shaving 12% average resin per cap. High-density polyethylene retains pharma and child-resistant niches that demand ISO 8317 torque resistance, while bio-attributed PP under ISCC PLUS is on track for price parity by 2028, giving sustainability-minded brands a drop-in alternative without tooling changes.

By Product Type: Dispensing Closures Gain Premium Traction

Threaded screw caps still accounted for 57.85% of 2025 revenue, confirming their ubiquity in water and CSD segments of the Europe plastic caps and closures market. Dispensing variants, however, are growing 5.21% per year as airless pumps protect antioxidant serums from oxidation.

Aptar’s silicone-free valve removes elastomer migration, a key clean-beauty ask. Child-resistant push-and-turn formats climbed 4.3% in 2025, and NFC-enabled tamper-evident bands are turning closures into authentication tools. Sports caps and flip-tops round out the portfolio, chasing hydration and condiment trends.

By Manufacturing Technology: Compression Moulding Eyes Spirits

Injection moulding delivered 71.49% of the Europe plastic caps and closures market size in 2025, thanks to 32-64 cavity stacks that churn out sub-USD 0.01 caps. Compression moulding, though higher in unit cost, is gaining a 4.91% CAGR slice by offering cork-like textures and lower leak rates for premium whisky closures.

BERICAP’s Hungarian plant underscores the pivot toward premium spirits willing to pay a 25% uplift for tactile branding. Blow moulding stays limited to closures exceeding 50 mm diameter in agrochemical and industrial drums where drop impact is king.

By End-User Industry: Cosmetics Sprint Ahead

Beverages kept a 42.75% revenue share in 2025, yet cosmetics and toiletries are expanding fastest at 4.96% CAGR. Refillable palettes and magnetic-lock closures from L’Oréal cut plastic per use by 70%, but still command double-digit premiums, cushioning margins.

Food closures are rebounding with food-service sachets, pharmaceuticals demand stricter child-resistant validation, and household cleaners migrate to trigger sprayers with adjustable dosing. Automotive and agrochemical niches contribute the remaining 8%, with concentred formulations shrinking closure diameters but raising chemical-compatibility standards.

Geography Analysis

Germany, France, and Italy provided 58% of installed moulding capacity in 2025, giving the Europe plastic caps and closures market a central-western production hub. Germany’s Bavaria and Baden-Württemberg clusters supply Coca-Cola, Nestlé, and Procter and Gamble, while France leads early recycled-content adoption as Danone’s Evian line hit 50% rHDPE in closures by 2025. Italy specializes in premium spirits seals but faces retrofit pain for tethered compliance in Southern wineries.

Post-Brexit United Kingdom rules added 10% compliance cost for incoming closures, yet its craft-spirits boom offsets the burden. Spain's shift of 15% CSD volume to aluminium cans cut PET closure demand, though mineral-water producers in Catalonia hold the fort. Slovenia and Austria are rising low-cost moulding hubs, sitting within four-hour trucking to Vienna, Zagreb, and Budapest, perfect for Eastern European brand proximity.

Scandinavia shows the highest aluminium-can penetration, stunting beverage-closure growth, but craft beer and aquavit brands still require tamper-evident designs. Poland and Czech Republic lure pharma-closure investors with skilled labour and API proximity. The January 2026 Packaging Waste Regulation will finally harmonize recycled-content thresholds across member states, reducing certification duplication for converters operating in multiple EU jurisdictions.

Competitive Landscape

Europe’s top five converters BERICAP, Guala Closures, UNITED CAPS, Berry Global, and Aptar collectively hold roughly 38% share, indicating a moderately fragmented structure. They are racing to lock in rHDPE feedstock, with Guala acquiring a Romanian recycler that adds 15,000 t annual capacity. Patent licensing for tethered hinges is emerging as a royalty stream as smaller converters opt to pay rather than design new systems.

Aseptic dairy and clean-beauty dispensing closures remain lucrative white spaces were certification and material science act as high entry barriers. Aptar’s silicone-free valve and UNITED CAPS’ aluminium-look compression caps illustrate innovation aimed at premium margins. Private-label supermarkets source from regional mid-sized moulders, squeezing commodity-closure prices and forcing larger players to emphasize patented or recycled-content offerings.

Compliance costs under ISO 15378 and ISO 22000 continue to shield established converters from low-cost Asian entrants. Yet disruptors leveraging bio-attributed PP and mono-material designs are courting eco-conscious niche brands ready to accept 10-15% price mark-ups for verified circularity, adding fresh competitive tension to the Europe plastic caps and closures market.

Europe Plastic Caps And Closures Industry Leaders

BERICAP GmbH and Co. KG

Guala Closures Group

Amcor plc

ALPLA Werke Alwin Lehner GmbH and Co KG

AptarGroup Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Origin Materials entered a strategic partnership with Berlin Packaging to deliver 100% rPET 1881 bottlecaps targeting European beverage lines.

- February 2025: The PPWR became legally effective, mandating 30% recycled-content plastic beverage bottles by 2030 and 65% by 2040.

- January 2024: Envipco reported a 764% European revenue jump to EUR 19.9 million, driven by DRS roll-out across Greece, Hungary and Romania.

- June 2024: : European Commission published EN 17665:2022+A1:2023, standardizing test protocols for tethered-cap attachment.

Europe Plastic Caps And Closures Market Report Scope

The Europe Plastic Caps and Closures Market Report is Segmented by Material Type (PET, PP, LDPE, HDPE, PVC, Other Materials), Product Type (Screw Caps, Snap-On Caps, Dispensing Closures, Child-Resistant Closures, Tamper-Evident Closures, Other Product Types), Manufacturing Technology (Injection Molding, Compression Molding, Blow Molding), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, Cosmetics and Toiletries, Household Chemicals, Other Industries), and Geography. The Market Forecasts are Provided in Terms of Volume (Tonnes).

By Material Type

| Polyethylene Terephthalate (PET) |

| Polypropylene (PP) |

| Low-Density Polyethylene (LDPE) |

| High-Density Polyethylene (HDPE) |

| Polyvinyl Chloride (PVC) |

| Other Materials |

By Product Type

| Screw Caps |

| Snap-On Caps |

| Dispensing Closures |

| Child-Resistant Closures |

| Tamper-Evident Closures |

| Other Product Types |

By Manufacturing Type

| Injection Molding |

| Compression Molding |

| Blow Molding |

By End-User Industry

| Beverage |

| Food |

| Pharmaceutical and Healthcare |

| Cosmetics and Toiletries |

| Household Chemicals |

| Other Industries |

By Country

| Germany |

| United Kingdom |

| Spain |

| France |

| Italy |

| Slovenia |

| Austria |

| Switzerland |

| Hungary |

| Croatia |

| Romania |

| Greece |

| Russia |

| Rest of Europe |

| By Material Type | Polyethylene Terephthalate (PET) |

| Polypropylene (PP) | |

| Low-Density Polyethylene (LDPE) | |

| High-Density Polyethylene (HDPE) | |

| Polyvinyl Chloride (PVC) | |

| Other Materials | |

| By Product Type | Screw Caps |

| Snap-On Caps | |

| Dispensing Closures | |

| Child-Resistant Closures | |

| Tamper-Evident Closures | |

| Other Product Types | |

| By Manufacturing Type | Injection Molding |

| Compression Molding | |

| Blow Molding | |

| By End-User Industry | Beverage |

| Food | |

| Pharmaceutical and Healthcare | |

| Cosmetics and Toiletries | |

| Household Chemicals | |

| Other Industries | |

| By Country | Germany |

| United Kingdom | |

| Spain | |

| France | |

| Italy | |

| Slovenia | |

| Austria | |

| Switzerland | |

| Hungary | |

| Croatia | |

| Romania | |

| Greece | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How fast is demand growing for tethered closures in Europe?

Orders surged 340% in 2024 as bottlers moved to meet the July 2024 directive, adding a 1.2% uplift to overall CAGR.

Which resin currently dominates closure production?

Polypropylene held 46.16% market share in 2025 due to its balance of heat resistance and cost.

Why are dispensing closures gaining traction?

Airless pumps and controlled-dose valves in premium cosmetics and pharma are expanding at a 5.21% CAGR to 2031.

What is the biggest geographic market for closures?

Germany, France, and Italy together account for 58% of installed molding capacity and remain the supply backbone.

How are recycled-content rules affecting material choices?

Regulation 2025/40 is pushing brand owners toward rHDPE and rPET, adding a projected 0.8% CAGR tailwind.

Are aluminum cans a threat to plastic closures?

Yes, deposit-return schemes have shifted 6 percentage points of soft-drink volume into cans since 2023, removing about 2.7 billion plastic caps annually.

Page last updated on: