Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

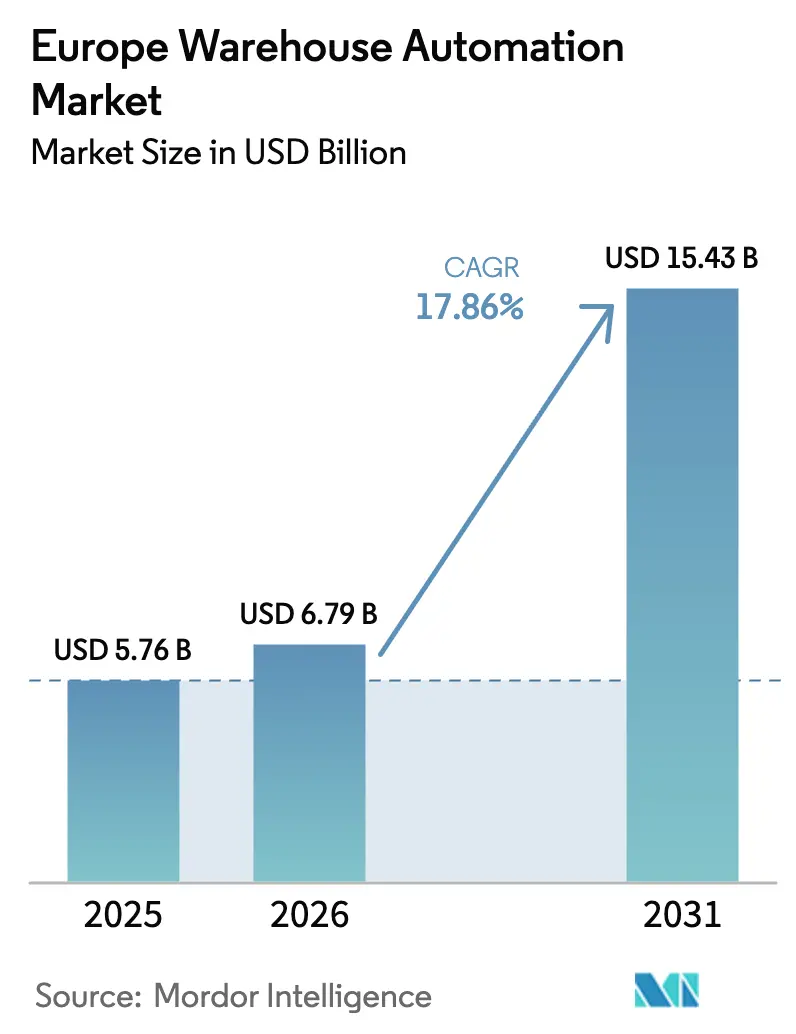

| Base Year Market Size (2025) | USD 5.76 Billion |

| Market Size (2026) | USD 6.79 Billion |

| Market Size (2031) | USD 15.43 Billion |

| Growth Rate (2026 - 2031) | 17.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Warehouse Automation Market Analysis by Mordor Intelligence

The Europe warehouse automation market size is expected to grow from USD 5.76 billion in 2025 to USD 6.79 billion in 2026 and is forecast to reach USD 15.43 billion by 2031 at 17.86% CAGR over 2026-2031. Order-processing speed, labor scarcity, and AI-driven robotics convergence are widening the adoption base at both greenfield and retrofit sites, while flexible financing models open the door to small and mid-sized operations. Hardware continues to anchor most investment thanks to high-ticket items such as automated storage and retrieval systems (AS/RS) and pallet conveyors, yet software layers that turn raw machine data into real-time decisions are growing even faster. Pan-European e-commerce, especially in groceries, keeps fulfillment volumes high in every quarter, encouraging warehouse operators to build distributed micro-fulfillment networks instead of a few mega hubs.[1]FedEx, “Growth Opportunities in Cross-Border E-Commerce,” fedex.com Simultaneously, stricter cold-chain regulations and sustainability goals press operators to install energy-efficient motors, edge-AI orchestration, and predictive analytics that lower kilowatt-hours per pick.

Key Report Takeaways

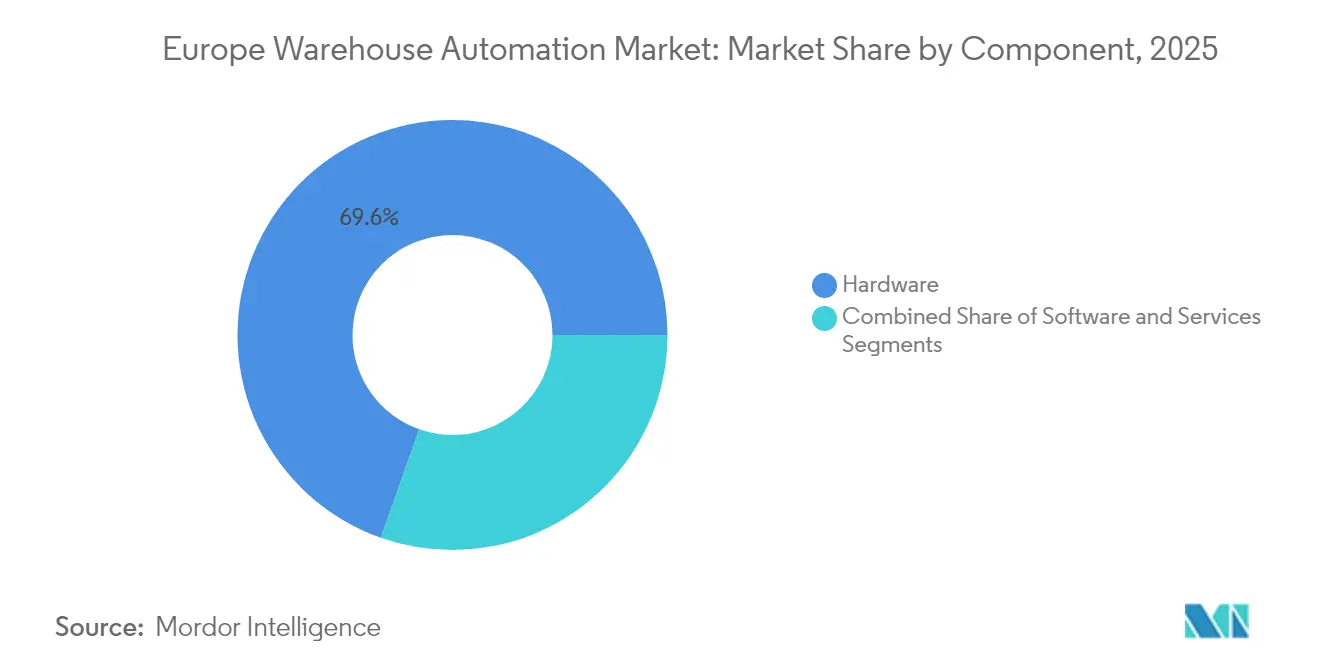

- By component, hardware retained 69.60% of the European warehouse automation market share in 2025; Software solutions are projected to post the highest 18.6% CAGR through 2031.

- By end-user industry, e-commerce and groceries led with a 32.45% revenue share of the European warehouse automation market in 2025; manufacturing is forecast to expand at a 19.15% CAGR between 2026-2031.

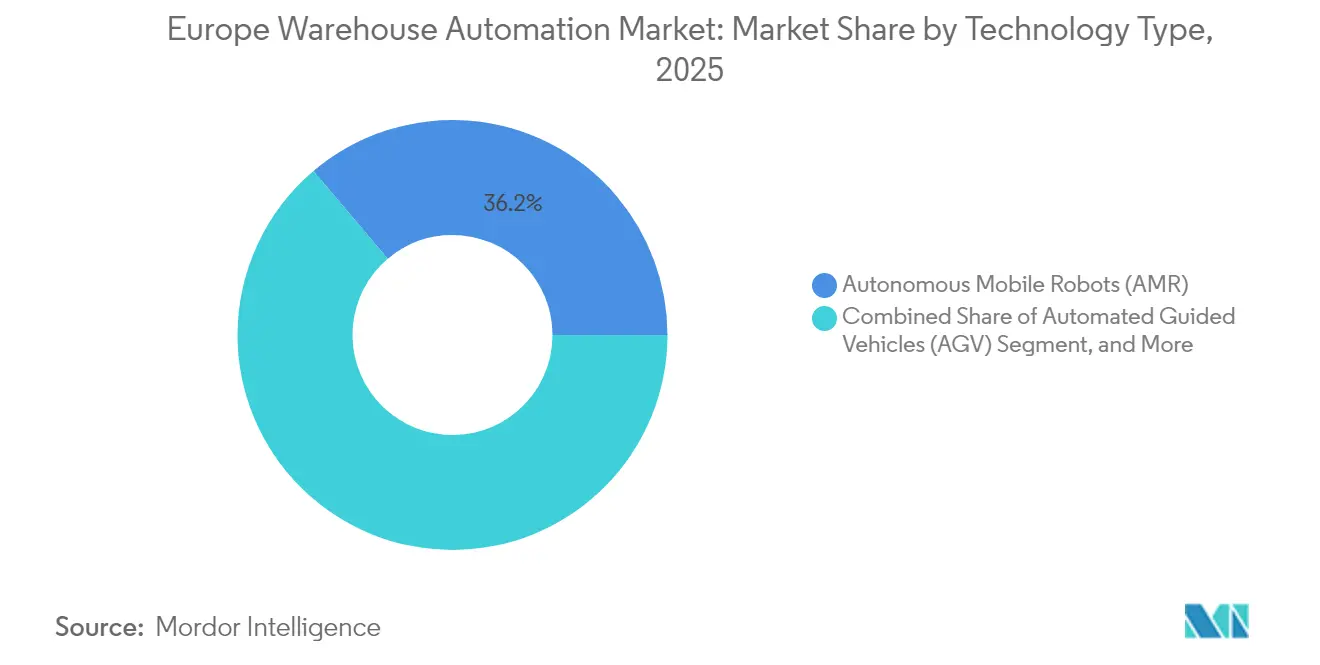

- By technology type, autonomous mobile robots (AMR) held 36.20% of the European warehouse automation market size in 2025; automated guided vehicles (AGV) are advancing at a 19.1% CAGR to 2031.

- By warehouse size, facilities above 40,000 m² accounted for 51.05% of the European warehouse automation market size in 2025, while small sites below 10,000 m² are growing at an 18.55% CAGR.

- By country, Germany represented 29.35% of the 2025 revenue of the European warehouse automation market, whereas Spain is set to post the highest 19.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Warehouse Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential growth in e-commerce order volumes | +2.5% | Germany, UK, France | Short term (≤ 2 years) |

| Rapid Industry 4.0 adoption across manufacturing | +1.8% | DACH region, Central Europe | Medium term (2–4 years) |

| Acute warehouse-labor shortages and wage inflation | +1.9% | Western and Eastern Europe | Medium term (2–4 years) |

| EU cross-border trade expansion | +2.1% | EU-wide | Long term (≥ 4 years) |

| Stricter cold-chain regulations | +1.2% | Northern and Mediterranean Europe | Long term (≥ 4 years) |

| Edge-AI orchestration and energy savings | +1.7% | Germany, Netherlands, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exponential growth in e-commerce order volumes

Seven markets will account for 70% of continental e-commerce by 2025, yet Romania and Hungary already post around 15% annual growth. DHL eCommerce Poland notes that success hinges on advanced route optimization, live parcel tracking, and seamless returns that manual setups cannot match. Operators are therefore dispersing inventory into numerous regional hubs so orders can cross one or two borders instead of four. Sophisticated order-orchestration engines decide in milliseconds which node should fulfill a basket based on duty costs, transit time, and stock freshness. Automation platforms win deals when they offer the same user interface and spare parts lists in every country, simplifying multi-site roll-outs.

Rapid Industry 4.0 adoption across manufacturing

Germany’s robot density of 429 units per 10,000 employees underscores leadership in factory automation, yet studies from MHP and Ludwig-Maximilian University flag that the wider DACH region trails China and the U.S. in Industry 4.0 maturity. Manufacturers now extend digitization to adjoining warehouses so production, kitting, and dispatch flow in one synchronized loop. MULTIVAC’s EUR 100 million (USD 110 million) expansion in Wolfertschwenden couples automated logistics with flexible production cells to guard uptime. Fraunhofer IML’s EUR 18 million (USD 19.8 million) Digital Testbed Air Cargo shows public-private labs filling R&D gaps. Brownfield retrofits dominate spending since most operators prefer installing shuttle aisles and AMR lanes in existing facilities instead of building new shells.

Acute warehouse-labor shortages and wage inflation

Aging demographics, stricter immigration rules, and rising minimum wages have pushed several operators to demand three-month payback periods on automation bids. Goods-to-person AMR stations raise pick rates two- to three-fold while reducing walking distance to under 100 meters per shift. AG Logistics in the Netherlands combined Körber layer pickers with legacy conveyors and kept headcount flat despite double-digit growth, highlighting technology’s role in employee retention. Tilburg-based Fabory moved to an almost lights-out model where two staff members per shift supervise a STILL fleet and see order-to-ship cycles shrink from one day to under three hours. Upskilling programs now focus on PLC diagnostics, cobot troubleshooting, and data-driven decision making rather than manual picking.

EU cross-border trade expansion

Cross-border sales inside the bloc now grow twice as fast as domestic e-commerce, with 32% of shoppers buying from a different member state in 2025. Temu’s decision to fulfill 80% of European orders via six in-country warehouses by December 2024 proves how proximity cuts delivery lead times from weeks to mere days.[2]Forest Shipping, “Temu Local Warehouses for European Orders,” forestshipping.com Spanish micro-fulfillment centers show that robotic shuttle systems paired with AI demand forecasting can triple order density in tight urban footprints. Peak-season elasticity is another reason operators embrace scalable AMR fleets that can be rented for two-month bursts and sent back afterward. DHL’s capital program of EUR 3.066 billion (USD 3.373 billion) for 7,500 cobots and 51,000 wearables underlines the up-front cash required to meet next-day delivery pledges.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX requirements | −1.4% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Cyber-security and data-sovereignty concerns | −1.2% | EU-wide | Medium term (2–4 years) |

| Scarcity of integration talent and long lead-times | −1.6% | High-automation regions | Medium term (2–4 years) |

| Legacy-system interoperability gaps | −0.9% | Mature industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX requirements

A person-to-goods system often starts at USD 1 million per site, keeping many SMEs on the sidelines. Robotics-as-a-Service models now cut the entry ticket to roughly USD 100,000 by converting CAPEX into monthly fees, yet banks still demand collateral or parent guarantees. TGW advises involving finance teams from day one so internal rate-of-return metrics shape the scope. DLL’s pre-financing packages that bundle robots, software, and integration costs show lenders tailoring products to intralogistics. Finally, pocket sorters like TGW SmartPocket can go live in six months, reducing construction spend and interest costs compared with conventional sorters.

Cyber-security and data-sovereignty concerns

The EU AI Act and High-Performance Computing regulation oblige vendors to document algorithmic risks, pushing some operators to keep orchestration on-premises rather than in a U.S. cloud.[3]Warehouse-Logistics & Fraunhofer IML, “Warehouse Logistics News,” warehouse-logistics.com Time-Sensitive Networking standards harden industrial Ethernet but also raise certification costs. Germany and France, mindful of data protection, often ask for split-tunnel designs where sensitive order data never leaves national soil. Attack-surface growth is evident as every sensor, AMR, and wearable connects to Wi-Fi 6 or private 5G. As a result, security audits now add two to three months to typical project timelines and can delay green-button sign-off until all penetration tests pass.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Software Disruption

Hardware accounted for 69.60% of the European warehouse automation market size in 2025, anchored by AS/RS aisles, conveyors, and AMR fleets. Cube-based storage such as AutoStore achieves four-fold inventory density while trimming kilowatt hours per pick, explaining its rapid uptake in high-rent urban hubs. Services revenue grows steadily as full-service contracts guarantee uptime and predictive-maintenance analytics signal part replacements weeks in advance. TGW’s 20-year lifetime-service deal with Betty Barclay illustrates how integrators lock in annuity streams beyond initial installs.

Meanwhile, software recorded the fastest 18.6% CAGR and is starting to eat into hardware budgets by extracting more cycles from existing machines using AI orchestration engines. Warehouse execution systems now tap edge GPUs to orchestrate hundreds of bots in microseconds, proving that value is tilting toward code as much as steel.

By End-User Industry: E-commerce Leads While Manufacturing Accelerates

E-commerce and groceries held a 32.45% revenue share in 2025 as next-day delivery became the norm in Germany, France, and the UK. Dark stores and ambient-to-frozen shuttle lanes enable grocers to batch-pick mixed-temperature baskets without manual handling.

Manufacturing, however, is projected to grow at a 19.15% CAGR, with Europe warehouse automation market share gains driven by brownfield retrofits that mesh shop-floor MES with warehouse management systems. Automotive and white-goods plants now sequence kitting totes straight to assembly positions, eliminating buffer stock and shrinking lead times. Food-and-beverage operators deploy pallet shuttles inside −25 °C zones to comply with EU cold-chain rules, while pharma players such as B. Braun integrate GxP-compliant robotics to minimize contamination risk.

By Technology Type: AMR Leadership Challenged by AGV Resurgence

AMR systems captured 36.20% of the European warehouse automation market share in 2025, due to flexible navigation and quick redeployment. Continuous price erosion plus open-source mapping libraries have lowered unit costs by almost 15% since 2022, making AMRs viable for seasonal peaks.

Paradoxically, AGVs are forecast to clock a 19.1% CAGR because standardized, low-spec laser guidance appeals to mid-size warehouses with straight-line routes. Shuttle-based AS/RS excels where high throughput trumps density, whereas cube-based grids rule in fashion and cosmetics, where SKU breadth is king. AI-enabled palletizing robots now manage mixed cartons at 700 cycles per hour, matching human versatility with better ergonomics. Finally, warehouse software suites post the fastest growth as WMS, WES, and WCS layers merge into one unified decision stack hosted at the edge for latency reasons.

By Warehouse Size: Large-Scale Dominance Meets Small-Scale Innovation

Facilities above 40,000 m² contributed 51.05% to the European warehouse automation market size in 2025 because multi-client 3PL hubs and plant-attached distribution centers still attract nine-figure budgets.

Yet sub-10,000 m² sites will expand at an 18.55% CAGR after Robotics-as-a-Service and plug-and-play systems erase hefty pit-deepenings and mezzanine works. TGW SmartPocket and Ocado Porter illustrate modularity: operators add pockets or bots when SKU counts rise, safeguarding cash. Mid-scale buildings between 10,000–40,000 m² remain the battleground where integrators pitch either high-density cube grids or hybrid AMR-plus-conveyor flows, depending on product mix.

Geography Analysis

Germany delivered 29.35% of the total 2025 revenue and remains the cornerstone of European warehouse automation market expansion. Anchor projects such as Betty Barclay’s Nußloch center with 120,000 storage slots illustrate the appetite for turnkey solutions that fuse fashion, e-commerce, and retail replenishment. Research spending is robust, evidenced by Fraunhofer IML’s Digital Testbed Air Cargo, a EUR 18 million sandbox for AI-enabled material flow. That said, locally hosted orchestration software is often mandatory because German clients rank data sovereignty alongside uptime.

Spain is racing ahead at a 19.3% CAGR, propelled by urban micro-fulfillment and its gateway role to North Africa. Barcelona and Madrid now house several cube-based AS/RS sites under 5,000 m², where robots and shuttle lifts compress order-to-ship cycles below 90 minutes. Genebre’s automated hub and B. Braun’s new plant are emblematic of diversified end-user demand. The warm climate plus EU Regulation 2019/138 further boost cold-chain investments, pushing operators to adopt energy-efficient variable-speed drives and insulated shuttle lanes.

The UK, France, Italy, and the Netherlands round out the top tier. Britain keeps investing despite Brexit complexities; Matalan’s KNAPP facility in Knowsley offers a scalable template that can flex from 200,000 to 400,000 picks per day without adding square footage. France benefits from central-location hubs like Poupry, where C-LOG processes 3.5 million online orders annually with next-evening delivery cut-off at 7 PM. Italy shows that diverse sectors from AgriEuro e-commerce to ABB’s component plant favor modular cubes for B2C peaks, yet stick with traditional conveyors for pallet outbound. The Netherlands, meanwhile, leverages Rotterdam and Schiphol logistics gateways; AG Logistics’ Körber layer pickers illustrate how local 3PLs mix legacy racking with new robotics for phased modernizations.

Competitive Landscape

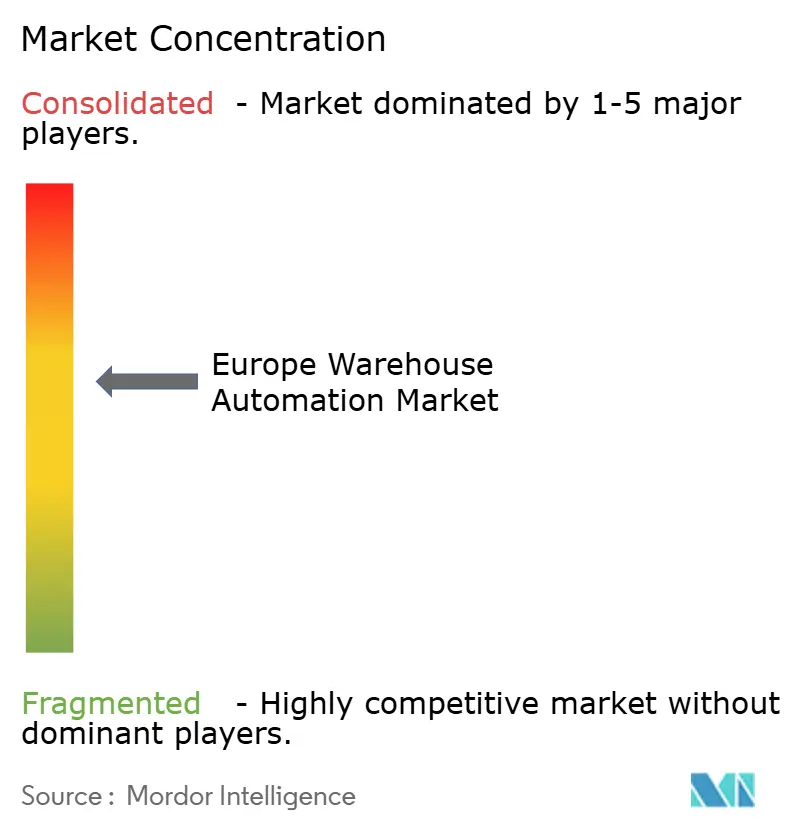

The European warehouse automation market remains moderately fragmented. Swisslog, SSI Schaefer, TGW Logistics, and Dematic keep leveraging global portfolios and in-house software stacks, but innovators like AutoStore, Ocado, and Exotec continue nibbling market share with niche-specific architectures. Partnerships rather than pure acquisitions dominate because speed to market outranks vertical integration; witness FORTNA aligning with AutoStore, Rockwell, and Hai Robotics to bundle cube grids, PLCs, and AMRs into one throat to choke.

Consolidation is accelerating nonetheless. Vanderlande’s EUR 300 million purchase of Siemens Logistics added fast-parcel sorters to its airport baggage roots, while Element Logic’s ABCO buyout expands North American reach. Suppliers now differentiate on algorithmic prowess: Arvato’s Moonshot WMS with Microsoft embeds AI to predict pick-density spikes hours ahead, trimming labor by double digits. Compliance readiness also matters; firms that can deliver EU AI Act documentation win tenders against technically similar rivals. White-space opportunity persists in small-site Robotics-as-a-Service where monthly fees align with cash-strapped SMEs.

Three strategic themes dominate boardrooms: 1) Edge computing that slashes cloud latency yet respects data-locality laws; 2) Energy-savvy drives and regenerative braking to cut emissions; 3) Lifecycle services baked into contracts so uptime, spares, and software updates sit under one SLA. As a result, top-tier integrators bundle financing, compliance, and after-sales into proposals, making it harder for pure-play robot start-ups to compete unless they partner.

Europe Warehouse Automation Industry Leaders

Swisslog Holding AG (KUKA AG)

SSI Schaefer AG

TGW Logistics Group GmbH

KNAPP AG

Vanderlande Industries B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TGW Logistics won OVS Italy, INTERSPORT completion, and Genebre Barcelona contracts, extending reach into fashion, sports, and industrial valves.

- April 2025: BSH Hausgeräte tapped TGW for appliance DC while AUTODOC went live, signaling automotive aftermarket automation momentum.

- March 2025: Ocado Intelligent Automation unveiled Porter AMR for 1.5-ton pallets, pushing deeper into non-food segments.

- February 2025: TGW launched the SmartPocket sorter that runs autonomous trolleys on overhead rails for modular scalability and 30% lower energy consumption.

- December 2024: Temu activated six European warehouses to fulfill 80% of continental orders locally, halving transit times.

Europe Warehouse Automation Market Report Scope

The European warehouse automation market study involves segmentation by component wherein hardware (AGV/AMR, AS/AR, piece picking, etc.), software (warehouse management systems, warehouse execution systems), and services (value-added services, maintenance, etc.) sub-segments are being analyzed.

Further, the warehouses and fulfillment centers perform activities across end-users, such as food and beverage, post and parcel, apparel, general merchandise, and manufacturing, to name a few. The manufacturing industry majorly includes the automotive, electronics, and pharmaceutical sectors. The study also provides the impact of COVID-19 on the market studied.

By Component

| Hardware | Mobile Robots (AGV, AMR) |

| Automated Storage and Retrieval Systems (AS/RS) | |

| Conveyors and Sortation Systems | |

| Palletizing and Depalletizing Systems | |

| Automatic ID and Data Capture (AIDC) | |

| Piece-Picking Robots | |

| Software | Warehouse Management Systems (WMS) |

| Warehouse Execution Systems (WES) | |

| Services |

By End-User Industry

| Food and Beverage |

| Post and Parcel |

| E-commerce and Groceries |

| General Merchandise and 3PL |

| Apparel and Footwear |

| Manufacturing (Durable/Non-Durable) |

| Other End-User Industries |

By Technology Type

| Autonomous Mobile Robots (AMR) |

| Automated Guided Vehicles (AGV) |

| Cube-Based AS/RS (e.g., AutoStore) |

| Shuttle-Based AS/RS |

| Mixed-Case Palletizing Robotics |

| Warehouse Software Suites (WMS/WES/WCS) |

By Warehouse Size

| Small-Scale (<10,000 m²) |

| Mid-Scale (10,000–40,000 m²) |

| Large-Scale (>40,000 m²) |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Rest of Europe |

| By Component | Hardware | Mobile Robots (AGV, AMR) |

| Automated Storage and Retrieval Systems (AS/RS) | ||

| Conveyors and Sortation Systems | ||

| Palletizing and Depalletizing Systems | ||

| Automatic ID and Data Capture (AIDC) | ||

| Piece-Picking Robots | ||

| Software | Warehouse Management Systems (WMS) | |

| Warehouse Execution Systems (WES) | ||

| Services | ||

| By End-User Industry | Food and Beverage | |

| Post and Parcel | ||

| E-commerce and Groceries | ||

| General Merchandise and 3PL | ||

| Apparel and Footwear | ||

| Manufacturing (Durable/Non-Durable) | ||

| Other End-User Industries | ||

| By Technology Type | Autonomous Mobile Robots (AMR) | |

| Automated Guided Vehicles (AGV) | ||

| Cube-Based AS/RS (e.g., AutoStore) | ||

| Shuttle-Based AS/RS | ||

| Mixed-Case Palletizing Robotics | ||

| Warehouse Software Suites (WMS/WES/WCS) | ||

| By Warehouse Size | Small-Scale (<10,000 m²) | |

| Mid-Scale (10,000–40,000 m²) | ||

| Large-Scale (>40,000 m²) | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe warehouse automation market in 2026?

The market reached USD 6.79 billion in 2026 and is forecast to climb to USD 15.43 billion by 2031 on an 17.86% CAGR.

Which component category is growing fastest?

Software, particularly warehouse execution systems and AI orchestration layers, is projected to record a 18.6% CAGR through 2031.

Which European country shows the highest growth momentum?

Spain is set to expand at a 19.3% CAGR thanks to urban micro-fulfillment and its role as a southern European logistics hub.

What technology type currently holds the largest share?

Autonomous mobile robots account for 36.20% of 2025 revenue, though automated guided vehicles are expanding faster.

How are small warehouses affording automation?

Robotics-as-a-Service and modular plug-and-play systems reduce upfront costs to roughly USD 100,000, making advanced solutions accessible to SMEs.

What is the main restraint hindering wider adoption?

High upfront CAPEX remains the biggest hurdle, especially in SME-heavy regions, although leasing and RaaS models are easing entry barriers.

Page last updated on: