Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

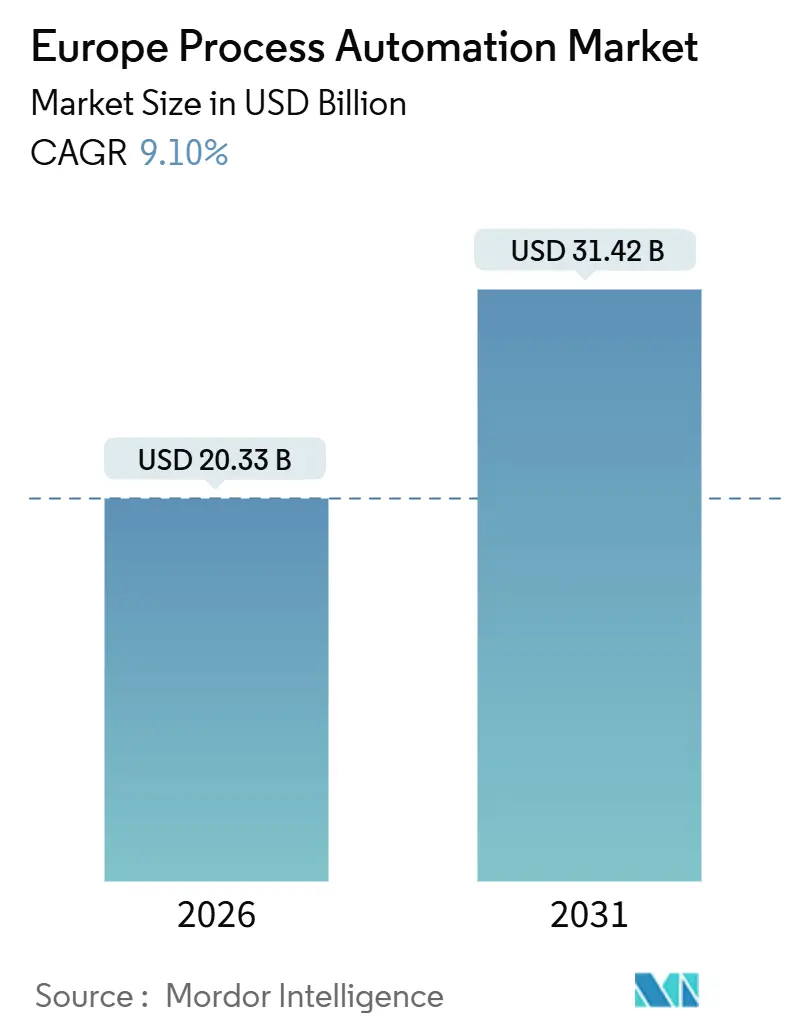

| Market Size (2026) | USD 20.33 Billion |

| Market Size (2031) | USD 31.42 Billion |

| Growth Rate (2026 - 2031) | 9.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Process Automation Market Analysis by Mordor Intelligence

The Europe process automation market size reached USD 20.33 billion in 2026 and is projected to climb to USD 31.42 billion by 2031, reflecting a 9.1% CAGR. Continental manufacturers are automating to blunt volatile electricity prices, meet decarbonization targets, and retrofit aging plants without disrupting production cycles. Cyber-secure upgrades dominate because the NIS2 Directive requires critical operators to report incidents within 24 hours, a rule that is reshaping capital allocation priorities. Demand is also shifting from heavy hydrocarbons toward high-margin pharmaceuticals and food processing, where real-time traceability requirements are accelerating software adoption. Competitive strategies center on edge intelligence that removes latency from safety loops, while opportunities surface in modular hydrogen projects that prize open-standard architectures.

Key Report Takeaways

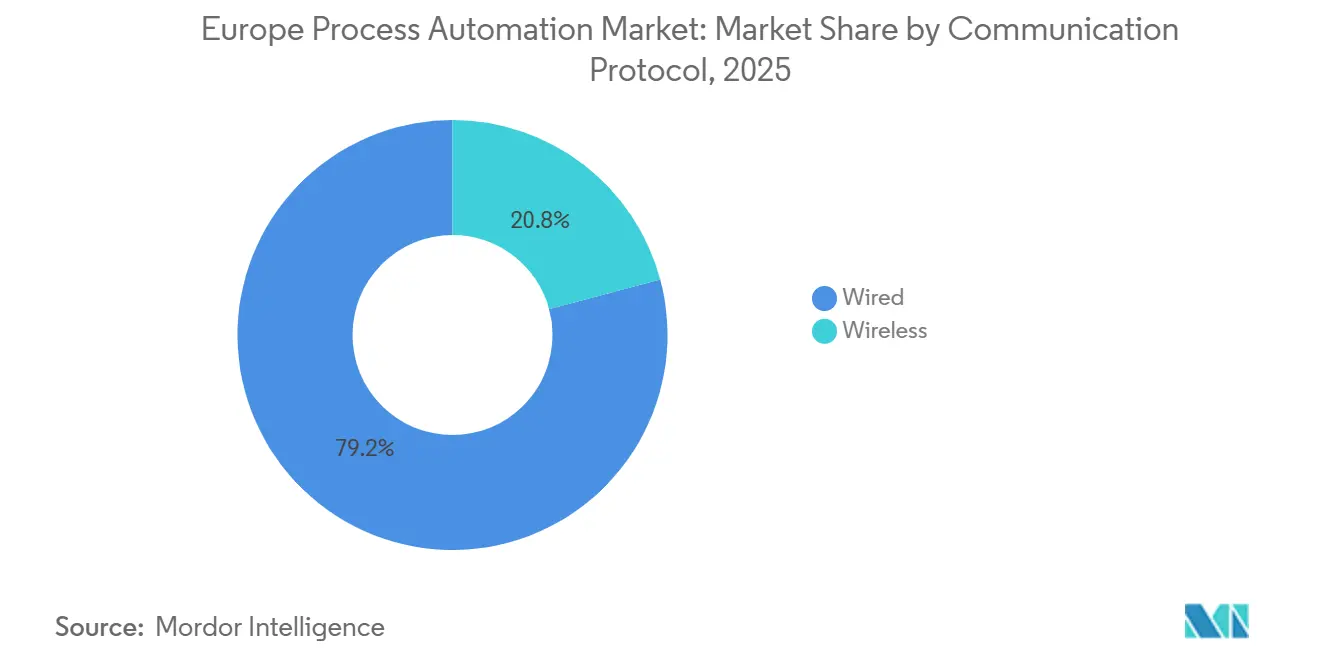

- By communication protocol, wired links retained 79.16% of the 2025 Europe process automation market share, yet wireless solutions are advancing at a 9.46% CAGR through 2031.

- By system type, hardware dominated with 56.19% of the revenue in 2025, whereas software is expected to expand at a 9.52% CAGR through 2031.

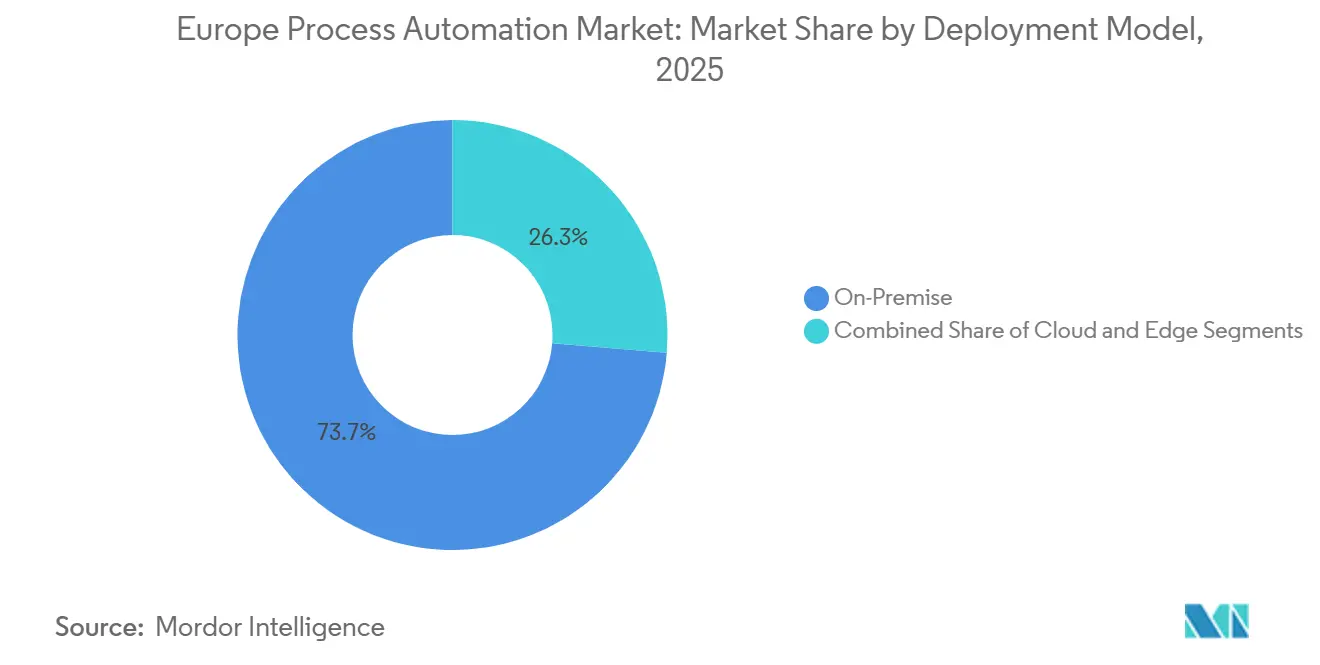

- By deployment model, on-premise installations accounted for 73.69% of the Europe process automation market size in 2025, while edge computing is expected to accelerate at a 22.71% CAGR.

- By end-user industry, the oil and gas sector led with a 28.71% revenue share in 2025, but the pharmaceuticals sector is forecast to grow fastest at a 10.69% CAGR.

- By country, Germany captured 33.19% revenue in 2025, whereas Poland is set to grow at a 10.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Process Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Emphasis on Energy Efficiency and Cost Reduction | +2.1% | Germany, France, United Kingdom, Nordic countries | Medium term (2-4 years) |

| Demand for Safety Automation Systems | +1.4% | Oil and gas hubs in Norway, Netherlands, United Kingdom; chemical clusters in Germany | Short term (≤ 2 years) |

| Industry 4.0 and IIoT Integration Across Brownfield Plants | +1.8% | Germany, France, Italy, Poland | Medium term (2-4 years) |

| EU Decarbonisation Policies Driving Retrofit Automation | +1.6% | European Union member states, with concentration in Germany, France, Spain | Long term (≥ 4 years) |

| Digital Product Passport Mandate Boosting Traceability Automation | +1.2% | European Union member states, strongest in automotive and electronics manufacturing regions | Medium term (2-4 years) |

| Green Hydrogen Pilot Plants Requiring Modular Automation | +0.9% | Germany, Netherlands, Spain, Portugal, Norway | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Emphasis on Energy Efficiency and Cost Reduction

European plants are contending with electricity prices that remain 40-60% above pre-2021 levels; therefore, operators are installing variable-speed drives, waste-heat recovery loops, and energy dashboards that reduce specific consumption by double-digit percentages.[1]Siemens AG, “Sustainability Report 2024,” siemens.com As carbon-border taxes begin in 2026, real-time energy metrics are transforming from a cost topic into a market-access prerequisite. Advanced process control software, once limited to refineries, now optimizes ovens, dryers, and fermenters, revealing energy waste hidden behind batch variability. Machine-learning models are being layered on historians to predict fouling or compressor-blade wear before losses compound. Vendors are shifting toward subscription pricing because energy dashboards and predictive models require continual updates rather than one-off sales.

Industry 4.0 and IIoT Integration Across Brownfield Plants

With the median European process asset older than three decades, retrofits dominate capex. Wireless vibration probes and infrared cameras bypass cable trays, letting plants digitalize piecemeal instead of shutting down for rewiring.[2]ABB Ltd, “Ability System 800xA Deployment Update,” abb.com Edge gateways run fast loops locally yet pass curated data to cloud historians, balancing latency and analytics. The retrofit wave, however, increases cybersecurity exposure, so operators now allocate up to 12% more for network segmentation, one-way firewalls, and anomaly detection. Growth, therefore, hinges on suppliers that offer pre-integrated cyber-secure sensor-edge bundles ready for brownfield deployment.

EU Decarbonisation Policies Driving Retrofit Automation

The Fit for 55 package assigns a carbon budget to every high-emitter, prompting cement, steel, and chemical operators to embed greenhouse-gas counters inside their control systems. Emerson integrated emissions ledgers into its DeltaV DCS, allowing plants to automatically feed EU-ETS dashboards.[3]Emerson Electric Co., “DeltaV Carbon Ledger Integration,” emerson.com District heating networks replace pneumatic valves with electro-hydraulic actuators that swing based on weather forecasts, slashing gas use. Operators favor modular skids that scale across budget cycles, spreading cost and limiting downtime. Vendors that ship prefabricated, carbon-aware modules gain a first-mover edge.

Digital Product Passport Mandate Boosting Traceability Automation

Since March 2024, every regulated product sold in the European Union must include machine-readable material, repairability, and recycling data. Pharmaceutical and electronics makers rushed to deploy serialization plus blockchain links, lifting Rockwell’s production-center installs by 41% in 2025. Smaller automation vendors partner with ERP houses to offer end-to-end traceability stacks, challenging incumbents that historically sold siloed solutions. Food processors retrofit track-and-trace middleware across legacy batch lines, merging quality records with sustainability reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure and Integration Complexity | -1.3% | Fragmented small and medium enterprises across Southern and Eastern Europe | Short term (≤ 2 years) |

| Cybersecurity Compliance Costs in OT Networks | -0.9% | Critical infrastructure sectors in Germany, France, Netherlands, United Kingdom | Medium term (2-4 years) |

| Ageing Workforce and OT-IT Skills Shortage | -0.7% | Germany, Italy, France, United Kingdom | Long term (≥ 4 years) |

| Vendor Lock-in Concerns With Proprietary Architectures | -0.5% | Multi-site operators in chemical, pharmaceutical, and food processing industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Integration Complexity

Retrofit projects often top EUR 5 million (USD 5.65 million) for mid-sized sites, and more than half of that sum finances integration labor that stitches PROFIBUS, Modbus, and HART loops into Ethernet backbones. Financing remains scarce for smaller firms in Southern and Eastern Europe, so many projects proceed in phases that extend the payback period. Edge sensors and hybrid clouds increase architectural complexity, forcing operators to manage three distinct data planes: on-premises, edge, and cloud, each with its own governance rules.

Cybersecurity Compliance Costs in OT Networks

The NIS2 Directive requires critical operators to file breach reports within 24 hours and demonstrate supply-chain oversight, resulting in annual security expenditures exceeding EUR 800,000 for mid-sized plants. Zoning networks, installing unidirectional gateways, and enforcing multi-factor authentication add latency and administration overhead that some plants fear will degrade control loops. The compliance burden slows IIoT adoption at cautious sites, pitting digitalization goals against risk appetite.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Protocol: Wireless Gains in Hazardous Retrofits

Wired links secured 79.16% of the 2025 process automation market share, as deterministic PROFIBUS, Modbus, and HART continue to dominate safety-critical duties. Wireless nodes, however, are set to grow at a 9.46% CAGR, particularly in hazardous oil, chemical, and wastewater zones where conduit trenching is cost-prohibitive. Emerson shipped 29% more Wireless 1410 gateways into European refineries in 2025, enabling operators to instrument tanks and flare stacks that had previously run blind. Municipal water utilities choose battery-powered LoRaWAN level sensors for remote lift stations, cutting civil works.

Latency and certification keep wired backbones entrenched around safety instrumented systems. Pharmaceutical vision systems flood networks with high-speed images that still overload wireless bands. A hybrid future is emerging where edge gateways aggregate wireless field data, compress it, and then forward it to historians over redundant fiber backhauls, maintaining loop integrity while easing retrofit economics.

By System Type: Software Layers on Hardware Base

Hardware captured 56.19% of 2025 revenue as distributed control systems and programmable logic controllers form the control core of continuous plants. Software revenues, growing at a 9.52% CAGR, reflect a pivot toward predictive maintenance, model-predictive control, and digital twins that boost yields without requiring the removal of installed equipment. Honeywell notes that 68% of its European Experion customers now subscribe to cloud analytics that surface optimization opportunities.

Distributed control systems remain the standard for petrochemical polymerization and biotech fermentation, where hundreds of tightly coupled loops demand deterministic scans. Programmable logic controllers dominate batch sectors such as flavors and fragrances. Sensors, valves, and motors are increasingly bundled with algorithms that flag failures before downtime occurs. Human-machine interfaces migrate from proprietary panels to browser dashboards on tablets, shrinking capex but widening the threat surface for cyber attackers.

By Deployment Model: Edge Surges for Latency-Critical Loops

On-premises architectures accounted for 73.69% of the 2025 process automation market size, a legacy of air-gapped philosophies that prioritize uptime. Edge nodes, forecast to grow 22.71% yearly, move analytics closer to pumps, turbines, and reactors that cannot tolerate cloud round-trip delays. Schneider Electric’s edge controllers secured 47% more orders from European district heating networks in 2025, as cities optimized their flow against weather models.

Pharmaceutical contract manufacturers utilize cloud historians to share batch data with brand owners while still maintaining the edge for sub-second bioreactor control. Green hydrogen electrolysers require millisecond current modulation to track renewable energy fluctuations, so developers deploy modular skids that run control logic locally while backhauling summaries to the cloud. Hybrid orchestrators that span on-premises, edge, and cloud are now a procurement priority.

By End-User Industry: Pharmaceutical Outpaces Traditional Leaders

Oil and gas remained the largest buyer with 28.71% revenue share in 2025, but decarbonization caps refinery investment. Pharmaceuticals will lead growth at a 10.69% CAGR, driven by the need for continuous bioprocessing that requires near-instant oxygen and pH control, as well as unit-level genealogy. Rockwell booked 38% more European pharmaceutical orders in 2025, driven by cell-therapy expansions.

Chemicals invest in systems to comply with REACH emission rules, integrating manufacturing execution systems into sites formerly run on spreadsheets. Utilities retrofit turbines for variable renewable energy sources, installing combustion optimizers that widen the operating windows. Food and beverage processors automate packaging and clean-in-place cycles to offset labor shortages, while pulp mills pursue energy savings as Asian capacity drives down prices. Mining and metals adopt automation to meet tighter discharge permits, but remain capital-disciplined.

Geography Analysis

Germany’s dominant share rests on Ruhr-Valley chemicals and North Sea hydrogen initiatives, yet capex splits between cautious retrofit of legacy crackers and aggressive modular electrolysers. SIMATIC PCS neo logged more than 40 German installations in 2025, underscoring a shift toward flexible, open-standard automation. Dual-apprentice programs produce hybrid OT-IT engineers, enabling German plants to absorb Industry 4.0 layers without relying on outside integrators.

France leverages its France 2030 plan to co-finance pharmaceutical mega-projects and aerospace composites lines that rely on digital twins and augmented-reality commissioning. Plants utilize edge controllers to model carbon intensity in real-time, supporting tax-credit claims. The United Kingdom manages post-Brexit dual standards, keeping offshore oil and gas automation buoyant as operators extend the life of North Sea assets with remote monitoring and predictive analytics.

Poland is the continental hot spot, fueled by battery and chemical greenfields that embed IIoT from day one. Automation demand skews toward extended control systems, unified historians, and traceability suites that conform to Digital Product Passport rules. ABB’s order boom illustrates how multinational OEMs leverage Polish cost advantages while staying close to Western markets.

In the Nordics, hydrogen electrolyser pilots require controllers that modulate load in tandem with wind spikes. Netherlands ports automate ammonia and methanol import terminals aimed at hydrogen re-exports, calling for pipeline monitoring and custody-transfer instrumentation. Spain and Portugal retrofit combined-cycle plants with advanced controls that flex to balance solar surges. Eastern European cohesion fund projects introduce cloud-coupled SCADA into historically manual operations, although skills shortages slow momentum.

Regulatory Landscape

Europe process automation investments increasingly track EU-wide digital and product rules affecting OT software, connected devices, and AI-enabled control and analytics. The NIS2 Directive has become a practical compliance anchor for critical operators through 24-hour incident reporting and expanded supply-chain oversight, pushing more spending toward IEC 62443-aligned hardening for DCS/SCADA networks, segmentation, and monitored remote access.

Newer horizontal digital regulation also shapes automation architectures and procurement. Regulation (EU) 2024/1689 (the EU Artificial Intelligence Act) establishes a harmonized framework for AI systems placed on the EU market, including industrial analytics, decision-support, and other AI-enabled automation functions. In April 2026, the European Commission issued the first Digital Markets Act review report (COM(2026) 178 final), reinforcing enforcement around interoperability obligations for gatekeeper-controlled platforms. This increases the value of open interfaces and verifiable interoperability within industrial software stacks.

Value Chain Analysis

The value chain begins with component and device suppliers (sensors, transmitters, valves/actuators, drives, PLC/DCS hardware) and moves through control software layers (SCADA/DCS/MES, advanced process control, historians, analytics) and cybersecurity tooling. Engineering, integration, and lifecycle services sit downstream of these layers. In Europe, deployments typically involve system integrators and automation service partners to retrofit brownfield assets, where integration labor is a major cost driver due to mixed protocols and legacy installed bases.

Recent partnerships point to IT/OT convergence and cloud infrastructure as core value-chain junctions rather than add-ons. In April 2025, OMRON and Cognizant partnered to combine OMRON hardware with Cognizant cloud, AI, and digital twin capabilities, reflecting the growing role of digital services firms in OT modernization. In November 2025, SAP and partners (including Deutsche Telekom, NVIDIA, and Siemens) announced the Industrial AI Cloud initiative tied to European digital sovereignty needs, aligning industrial analytics and orchestration with local infrastructure and compliance. Standards bodies such as ETSI also continue to influence interoperability and orchestration expectations through NFV and related management specifications, reinforcing modular, interface-driven designs across automation and industrial IT stacks.

Competitive Landscape

The top five vendors capture roughly 45-50% of European revenue, conferring moderate concentration. ABB, Siemens, and Schneider Electric safeguard large distributed-control estates through long-term service agreements and proprietary buses, but open-standard OPC UA nodes in hydrogen and pharmaceutical projects chip away at this moat. Emerson and Honeywell pivot to analytics subscriptions that monetize installed hardware via predictive maintenance.

Edge-orchestration gaps let startups deliver containerized microservices that run across any hardware, tempting operators seeking to escape vendor lock-in. Pharmaceutical continuous-manufacturing lines favor pre-validated skids, advantaging suppliers whose modules comply with good manufacturing practice out of the box. Cybersecurity prowess is now a sales lever; vendors flaunt IEC 62443 certificates and on-call incident teams to appease NIS2 audits. Patent filings related to machine-learning optimization and digital twins surged in 2024-2025, with Siemens, ABB, and Schneider Electric securing more than 60% of the grants, signaling sustained R&D investment.

Europe Process Automation Industry Leaders

ABB Limited

Siemens AG

Schneider Electric SE

General Electric Co.

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is clearest where operators need cyber-secure modernization without multi-year rip-and-replace programs, especially on brownfield sites with mixed PROFIBUS/Modbus/HART estates and limited downtime windows. This supports demand for packaged modernization offers that combine controls, edge compute, and security controls pre-engineered for faster commissioning. These bundles align with NIS2-driven incident readiness and supply-chain assurance. Schneider Electric addressed this directly in June 2026 with the launch of Industrial Automation Modernization as a Service, bundling EcoStruxure Automation Expert with HPE SimpliVity infrastructure, which supports subscription-style modernization for distributed plants.

A second opportunity area centers on industrial data platforms and sovereign AI-ready infrastructure that keeps sensitive OT and production data within European residency and governance requirements while still enabling advanced analytics and orchestration. In June 2026, T-Systems and Scheer Group formed a partnership around sovereign AI-powered process automation using Scheer orchestration on T-Systems' Munich-based Industrial AI Cloud and GPU infrastructure, reflecting enterprise demand for hosted automation that fits European compliance and data control priorities. This also raises the emphasis on integration between plant-floor data historians, MES, and enterprise workflows, particularly in regulated industries such as pharmaceuticals and food processing, where traceability and auditability are procurement requirements.

Recent Industry Developments

- July 2026: Mitsubishi Electric reached an agreement to transfer 70% of its subsidiary Mitsubishi Electric FA Industrial Products to Konecranes, while retaining a 30% stake. The transaction reshapes Mitsubishi Electric’s factory automation portfolio and can shift channel focus and investment priorities across European industrial customers that buy automation-related products and services.

- June 2026: Schneider Electric announced a definitive agreement to acquire Cognite Holding B.V., an industrial data and AI software provider, for USD 3.1 billion. Bringing Cognite’s industrial data platform into Schneider Electric’s stack strengthens the ability to connect plant-floor systems to enterprise analytics and AI use cases, reinforcing software-led differentiation in European process automation projects.

- October 2024: SAP and partners advanced Industrial AI Cloud positioning around European digital sovereignty for industrial workloads, creating a clearer route for regulated operators to run AI-enabled automation on locally governed infrastructure. This supports deployments that require strong data residency and security controls while connecting OT data streams to enterprise applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe process automation market covers spending on industrial process automation hardware and software used to monitor, control, and optimize plant operations across process industries within Europe, measured in USD value terms.

Scope exclusions: This scope excludes office-led automation tools and pure IT workflow automation that is not directly tied to industrial process control and instrumentation in plants.

Segmentation Overview

- By Communication Protocol

- Wired

- Wireless

- By System Type

- Hardware

- Supervisory Control and Data Acquisition System (SCADA)

- Distributed Control System (DCS)

- Programmable Logic Controller (PLC)

- Manufacturing Execution System (MES)

- Valves and Actuators

- Electric Motors

- Human Machine Interface (HMI)

- Process Safety Systems

- Sensors and Transmitters

- Software

- Advanced Process Control (APC)

- Data Analytics and Reporting Software

- Other Software

- Hardware

- By Deployment Model

- On-Premise

- Cloud

- Edge

- By End-User Industry

- Oil and Gas

- Chemical and Petrochemical

- Power and Utilities

- Water and Wastewater

- Food and Beverage

- Paper and Pulp

- Pharmaceutical

- Other End-User Industry

- By Country

- United Kingdom

- Germany

- France

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting structure of the market and to map demand drivers across Europe. We relied on public and official sources such as Eurostat, national statistical offices, the International Energy Agency, and European Commission publications, which helped us track industrial output, energy transition projects, and compliance signals.

To translate these signals into market numbers, the desk phase also used company annual reports, investor presentations, and product documentation to understand solution adoption patterns (for example, SCADA, DCS, PLC, MES, and HMI) and typical replacement cycles. A few paid subscriptions were used only for company financials and to read patent activity at a high level, so technology direction could be cross-checked against what was heard in interviews. The sources named above are illustrative, and many other public references were also consulted to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how buyers and system integrators in Europe are budgeting across automation hardware and software, and how plans are shifting with cloud, edge, and cybersecurity requirements. We spoke with a mix of process-industry users and supply-side experts, and coverage was balanced across major European countries and the rest of the region so local investment cycles could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | |

| Mid tier: 42% | Functional/Unit leaders: 32% | |

| Smaller Players: 21% | Managers: 55% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where Europe industrial activity and process-industry investment signals are translated into automation spend, then split into hardware and software using adoption patterns observed in end-user industries. The totals are then corroborated using selective bottom-up approximations, including sampled supplier revenue splits, channel checks, and ASP x unit logic for common system classes, which helps correct for over-counting in overlapping solution labels.

Key model inputs include process-industry output and capacity additions, energy and utilities capex cycles, compliance-driven upgrades (including cybersecurity and safety requirements), the mix shift toward cloud and edge deployments, and average replacement and modernization cycles for control systems. Because not every country publishes equally detailed series, gaps are handled through proxy indicators (such as industrial production indices and project pipelines) and then rechecked with interview feedback before being applied. Forecasting is run using scenario analysis, where drivers like industrial capex, modernization intensity, and software attach rates are varied within ranges agreed with primary respondents, and the final curve is selected only after the resulting growth pattern matches observed spending behavior in Europe.

Data Validation & Update Cycle

Validation is done in multiple steps so the final numbers do not depend on a single assumption. We compare outputs against independent signals such as process-industry production trends, announced plant upgrades, and the observed pace of modernization in major countries, and then investigate outliers until the variance can be explained.

Before sign-off, the model is reviewed by another analyst who checks arithmetic integrity, unit consistency, and year-over-year movement, and interview re-contact is triggered when a major discrepancy shows up by country or by system type. Reports are refreshed annually, and interim updates are made when material events change investment patterns, such as policy shifts, large energy projects, or supply chain disruptions. Right before delivery, a final review pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Europe Process Automation Market Size Compared Against Other Published Estimates

Published market values for Europe process automation can differ because the market label is used in different ways and the time base also varies. Differences usually come from what is counted as process automation, how software is treated, whether services are included, and which year is treated as the current anchor.

The table shows a clear spread that mostly comes from scope bundling and timeline choices. Some sources fold in office-led automation like RPA and BPM or wider workflow software under the same heading, while in Mordor Intelligence's model the count is limited to industrial process automation hardware and software used in plants, with cloud and edge treated as deployment modes rather than extra categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 20.33 B (2026) | |

| Global Consultancy A | USD 17.57 B (2024) | Uses an earlier base year and a broader definition that mixes industrial automation with business process and workflow automation, which changes what gets counted as market revenue. |

| Industry Publisher B | USD 45.72 B (2032) | Reports a later-year forecast value under an expanded automation umbrella, so the figure reflects longer compounding and may include adjacent software layers beyond plant-focused process control. |

When the scope is kept tight around plant-level automation and the years are aligned, the gap across estimates narrows quickly. Our approach keeps assumptions traceable to observable industrial indicators, and the checks from interviews help ensure the final value is not driven by an overly aggressive software or forecast uplift.

Key Questions Answered in the Report

What is the projected value of the Europe process automation market in 2031?

The process automation market is forecast to reach USD 31.42 billion by 2031, up from USD 20.33 billion in 2026.

Which segment is growing fastest within European deployment models?

Edge computing is the fastest, expanding at a 22.71% CAGR because latency-critical loops need local processing.

Why is wireless adoption rising in hazardous-area retrofits?

Wireless sensors avoid costly conduit work, letting plants instrument tanks and flare stacks while meeting safety certifications.

How do EU decarbonization policies influence automation spending?

Fit for 55 carbon budgets push operators to embed emissions counters and energy optimizers directly into control systems.

Which country offers the highest growth outlook through 2031?

Poland leads with a 10.16% CAGR as battery and chemical investors build greenfield plants incorporating Industry 4.0 from inception.

How does NIS2 affect mid-sized operators?

They now devote up to EUR 1.2 million annually to OT security tools and audits to meet 24-hour incident-reporting rules.

Page last updated on: