Conveyor Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

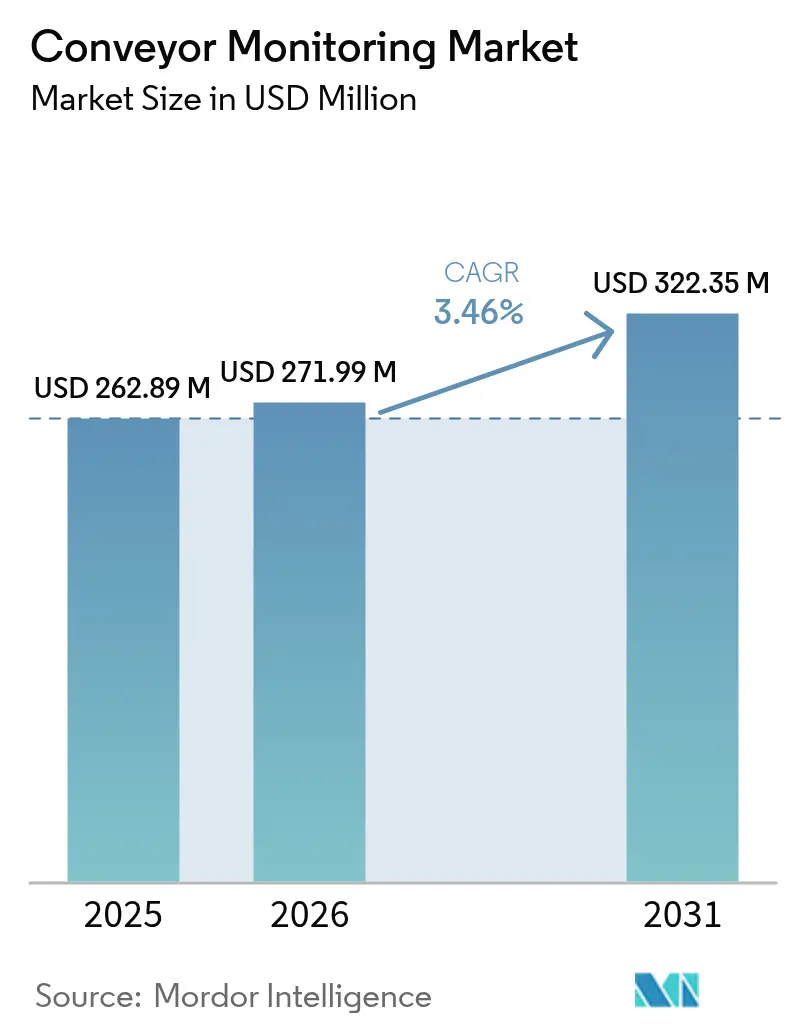

| Market Size (2026) | USD 271.99 Million |

| Market Size (2031) | USD 322.35 Million |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Conveyor Monitoring Market Analysis by Mordor Intelligence

The conveyor monitoring market size was valued at USD 262.89 million in 2025 and estimated to grow from USD 271.99 million in 2026 to reach USD 322.35 million by 2031, at a CAGR of 3.46% during the forecast period (2026-2031). Demand is growing because operators are shifting from reactive inspections to predictive diagnostics that pair vibration and thermal sensors with edge analytics, a change that reduces unscheduled stoppages and extends component life. Mining, logistics, and e-commerce facilities continue to drive sensor deployments, while moderate-cost wireless IIoT upgrades are unlocking retrofit opportunities for aging conveyors. Hardware still dominates current spending, yet cloud software subscriptions are expanding faster as users seek prescriptive alerts that integrate directly with maintenance work-order systems. Cyber-security hardening and regulatory safety mandates add further momentum, although uncertain payback periods for smaller plants temper the conveyor monitoring market expansion in price-sensitive regions.

Key Report Takeaways

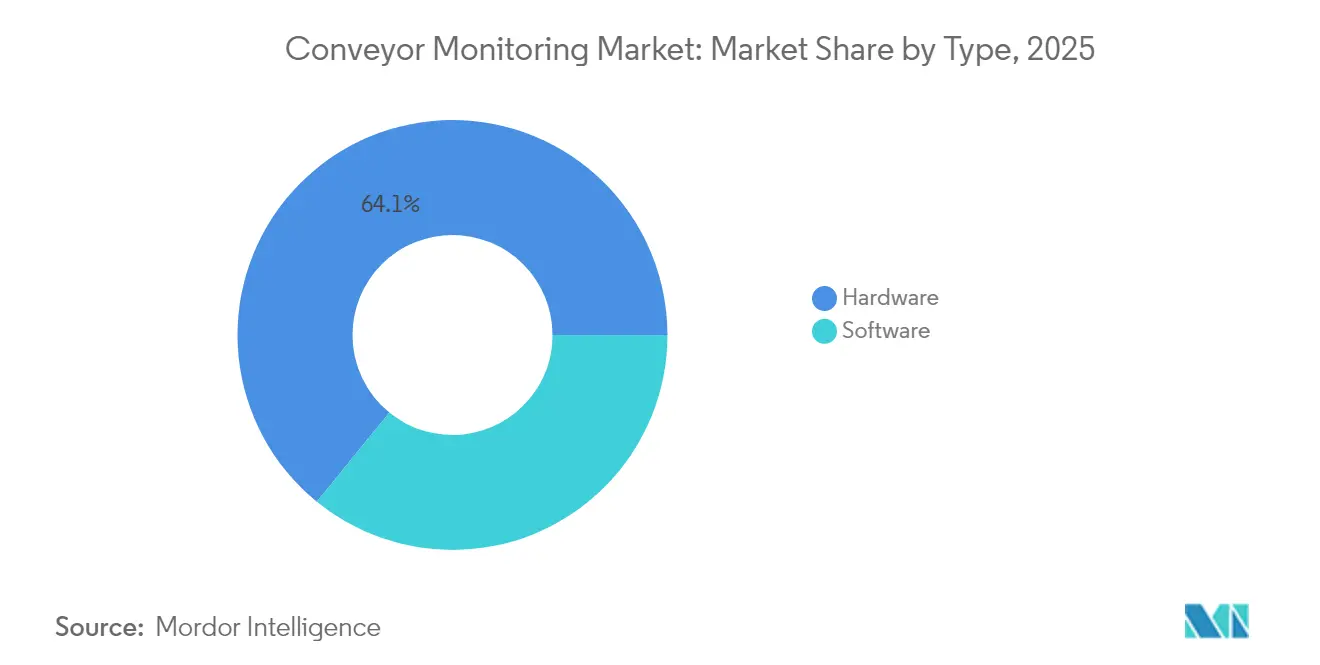

- By component, hardware captured 64.13% revenue share in 2025, while software is projected to expand at a 4.43% CAGR through 2031.

- By monitoring focus, belt monitoring accounted for 71.05% of 2025 installations, whereas motor monitoring is forecast to grow at a 4.62% CAGR to 2031.

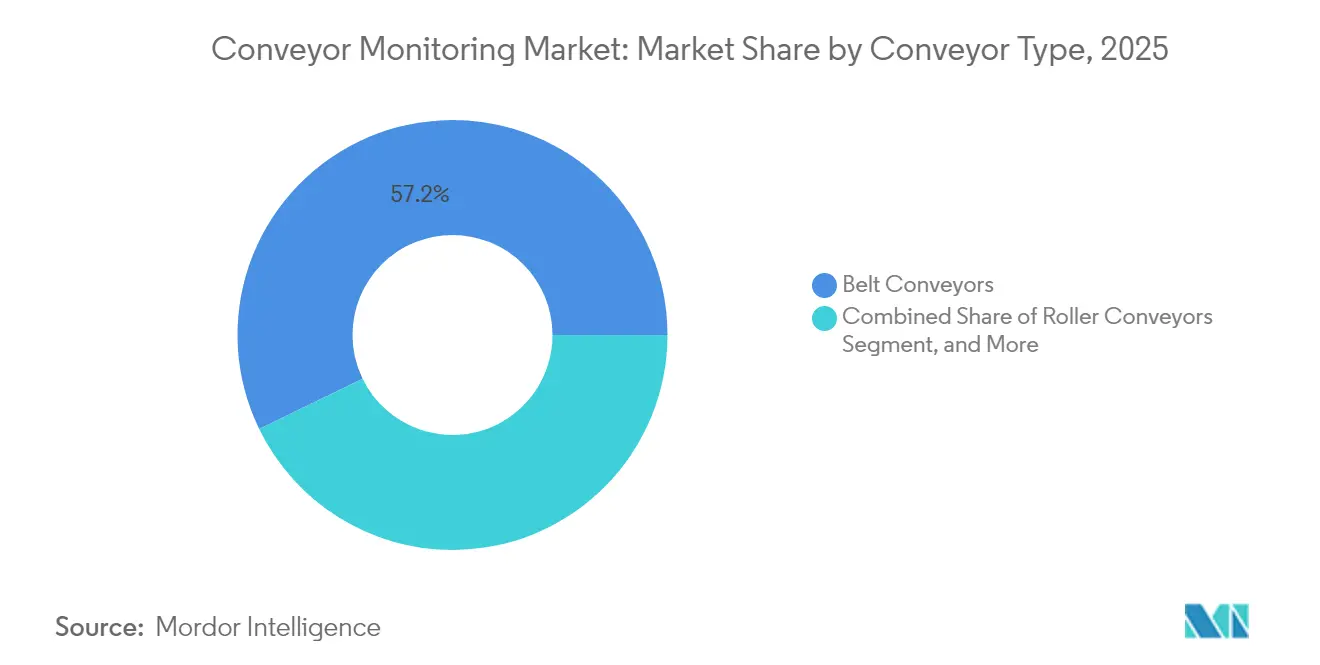

- By conveyor type, belt conveyors held 57.21% of 2025 deployments; overhead conveyors represent the fastest-growing form at a 4.29% CAGR.

- By end-user, mining led with 30.12% of 2025 revenue, yet logistics and warehousing is on track for a 4.08% CAGR to 2031.

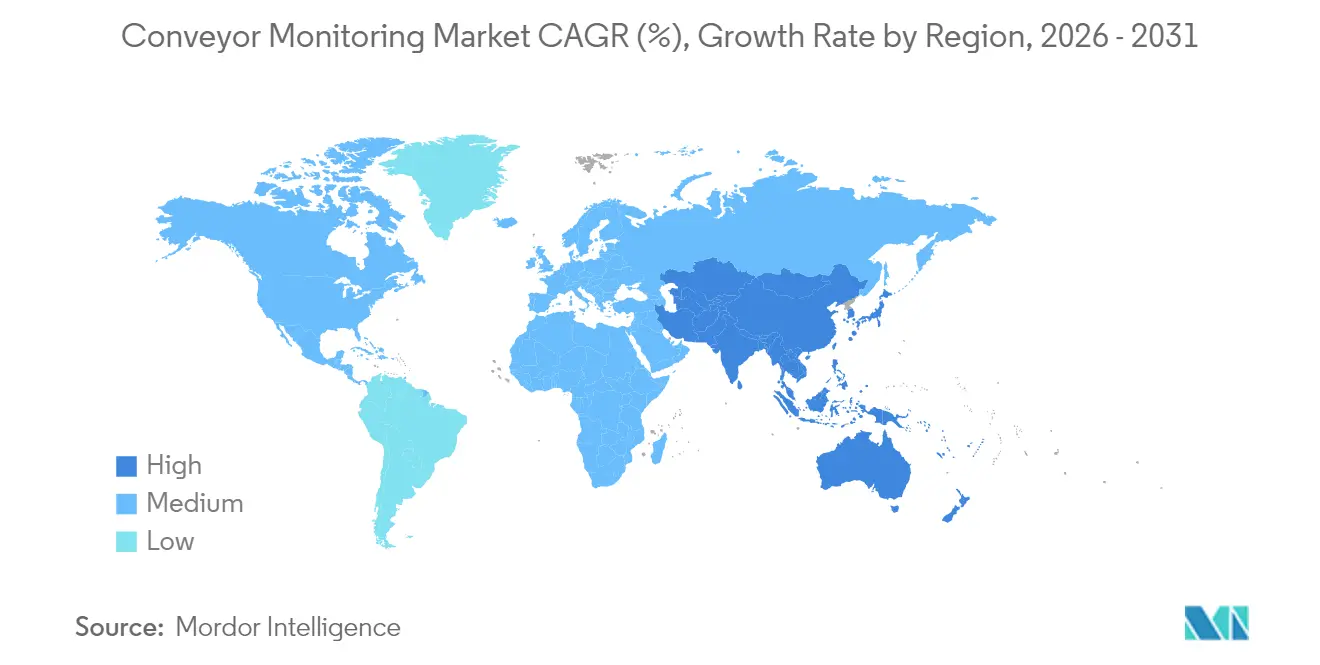

- By geography, North America commanded 35.21% of 2025 sales, while Asia-Pacific shows the highest regional growth at a 4.19% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Conveyor Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Predictive Maintenance Tools and Techniques | +0.9% | Global, with early concentration in North America and Europe | Medium term (2-4 years) |

| Stringent Workplace Safety Regulations Driving Automation of Conveyor Health Monitoring | +0.7% | North America (MSHA), Europe (Machinery Directive), South Africa, Australia | Short term (≤ 2 years) |

| Rapid Expansion in E-commerce Fulfilment Centres Demanding Continuous Conveyor Uptime | +0.6% | North America, Europe, Asia-Pacific (China, India) | Short term (≤ 2 years) |

| Increasing Throughput Requirements in Mining and Bulk Material Handling | +0.5% | Australia, South America (Chile, Brazil), Africa (South Africa), North America | Medium term (2-4 years) |

| Integration of Low-Cost Wireless IIoT Sensors Enabling Retrofit Monitoring in Legacy Conveyors | +0.4% | Asia-Pacific, South America, Middle East | Medium term (2-4 years) |

| Emergence of Conveyor Digital Twins Combined with Edge Analytics for Real-Time Optimisation | +0.3% | North America, Europe, advanced manufacturing hubs in Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Predictive Maintenance Tools and Techniques

Predictive maintenance cuts repair costs by up to 30% and extends asset life by 40% as operators replace time-based checks with sensor-driven, condition-based tasks.[1]U.S. Department of Energy, “Predictive Maintenance 4.0,” energy.gov Mining companies now stream accelerometer, ultrasonic, and infrared data through edge gateways that forecast bearing failures weeks ahead, keeping conveyors online during 24/7 operations. Low-cost MEMS sensors priced under USD 50, paired with wireless Bluetooth or LoRaWAN modules, make continuous monitoring affordable at scale. Rio Tinto links conveyor health data to autonomous haulage analytics, boosting ore throughput per conveyor kilometer by 15%. Vendors such as ABB clamp retrofit sensors onto existing motors, converting legacy drives into connected assets that transmit vibration, temperature, and magnetic-flux data to mobile dashboards.[2]ABB Ltd., “ABB Ability Smart Sensor for Motors,” abb.com

Stringent Workplace Safety Regulations Driving Automation of Conveyor Health Monitoring

The U.S. MSHA 30 CFR Part 56 rule requires the detection of belt misalignment and slippage, prompting rapid sensor retrofits in both surface and underground mines.[3]Mine Safety and Health Administration, “30 CFR Part 56 – Safety and Health Standards,” msha.gov South Africa’s Mine Health and Safety Act carries similar obligations; regulators attribute 12% of 2024 mining fatalities to conveyor incidents, a statistic that accelerated the adoption of continuous belt-rip detection. The EU Machinery Directive requires documented hazard assessments, and the forthcoming EU AI Act will compel audit trails for predictive models, favoring vendors that deliver pre-certified systems. New Zealand tightened conveyor guarding and emergency-stop standards in 2024, prompting upgrades with the addition of proximity sensors and pull-cord switches.

Rapid Expansion in E-Commerce Fulfillment Centers Demanding Continuous Conveyor Uptime

Amazon operates kilometer-scale conveyor networks that sort more than 1,000 parcels per hour and loses up to USD 20,000 for every downtime hour. Predictive monitoring provides 15–30 minutes of warning before critical failures, allowing traffic rerouting around stressed segments. Walmart’s USD 1.1 billion supply-chain automation drive included AI-driven conveyor analytics across 350 regional centers, resulting in a 40% reduction in downtime. DHL achieved a 25% labor-cost reduction after rolling out predictive platforms in 200 warehouses. Always-on operating models and the rise of same-day delivery preserve demand for conveyor monitoring market solutions that function without planned maintenance windows.

Increasing Throughput Requirements in Mining and Bulk Material Handling

High-capacity conveyors now carry up to 15,000 metric tons per hour, which accelerates wear on belts, idlers, and drives. BHP’s 12 km Escondida conveyor added fiber-optic belt monitoring in 2024 and can detect longitudinal rips within 2 seconds, preventing multi-day outages. Anglo American fitted acoustic sensors that identify noisy bearings before failure, allowing swaps during scheduled maintenance. Port grain and coal terminals follow similar tactics to avoid environmental spills and maritime loading delays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited In-House Skillset to Manage Monitoring Solutions and Analyse Data | -0.5% | Global, acute in emerging markets (Southeast Asia, South America, Africa) | Short term (≤ 2 years) |

| High Costs of Installation and Maintenance | -0.4% | Small and mid-sized facilities globally | Short term (≤ 2 years) |

| Uncertain Return on Investment for Small and Mid-Sized Facilities | -0.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Cyber-Security Vulnerabilities in Connected Conveyor Systems | -0.2% | Global, critical in regulated industries (mining, food processing) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited In-House Skillset to Manage Monitoring Solutions and Analyse Data

The conveyor monitoring market still confronts a shortage of engineers trained in signal processing and predictive analytics. Terabytes of vibration, temperature, and acoustic data often overwhelm existing maintenance teams, especially in Southeast Asia and South America, where technical talent migrates toward higher-wage economies. Vendors answer this skills gap with managed services. Honeywell Forge offers a concierge tier where specialists interpret data weekly and issue prioritized repair lists.

High Costs of Installation and Maintenance

Comprehensive retrofits range from USD 50,000 to USD 150,000 per line, well above annual maintenance budgets for many small factories. Ongoing software licenses and calibration add USD 5,000–15,000 per year. While wireless networks avoid conduit costs, battery replacements and radio interference introduce new upkeep demands. Subscription or leasing models from SKF now spread payments over multi-year periods, bringing barrier-to-entry relief for lower-volume users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Platforms Gain Share Despite Hardware Dominance

Hardware commanded 64.13% of 2025 revenue due to the up-front purchase of sensors, gateways, and control modules, yet software subscriptions are on track for a 4.43% CAGR through 2031, outpacing physical asset growth. This swing highlights how operators strive for further performance gains from existing sensors. Rockwell FactoryTalk Analytics unifies vibration, temperature, and energy data into a single risk score, while Emerson Plantweb Insight enables corporate reliability teams to benchmark across sites.

Growing preference for outcome-based contracts accelerates this shift. Pay-as-you-go models allow plants to test applications before full scale-up, a key incentive in the conveyor monitoring market where budget constraints can delay capital approvals.

By Monitoring Focus: Motor Monitoring Closes Gap on Belt-Centric Systems

Belt integrity still tops user priority lists, explaining 71.05% of 2025 installations. Fiber-optic cables inside belt carcasses and laser scanners that detect splice misalignment trigger immediate stops, preventing catastrophic downtime. Fenner Dunlop’s Intelliguard solution cuts detection time to under 2 seconds.

Motor monitoring, however, posts a faster 4.62% CAGR, reflecting the reality that electric drives cause 30-40% of unexpected conveyor halts. SKF’s wireless vibration kits and Nidec’s embedded-sensor motors report temperature, current, and imbalance anomalies to cloud dashboards, letting planners replace bearings during scheduled shutdowns. As variable-frequency drives proliferate, users need analytics tuned for harmonic distortion and insulation stress, expanding addressable revenue for the conveyor monitoring market.

By Conveyor Type: Overhead Systems Rise in Automotive and Aerospace

Belt conveyors held 57.21% of 2025 projects because they carry bulk material over long distances at mines, cement plants, and ports. Standardized sensor interfaces make belt systems easy candidates for predictive upgrades.

Overhead conveyors, expanding at a 4.29% CAGR, move vehicle bodies and aerospace parts in three-dimensional space, demanding position tracking and collision avoidance. Ford’s Michigan Assembly Plant uses RFID and optical sensors on overhead lines to reduce work-in-process inventory by 20%. Hybrid lines that mix robots and humans require real-time health scores to synchronize speed and safety, adding edge analytics nodes at every motor group.

By End-User Industry: Logistics Overtakes Mining in Growth Trajectory

Mining accounted for 30.12% of the 2025 spend, as kilometer-long belts are critical path assets where every unscheduled stop can cost USD 50,000–200,000 per hour. Condition monitoring thus rapidly penetrated large copper, iron ore, and coal operations.

Logistics and warehousing now show a 4.08% CAGR as e-commerce giants aim for 99.5% uptime. The conveyor monitoring market size for parcel hubs grows in tandem with same-day delivery commitments; Amazon handled 5.9 billion packages in 2024 and embeds predictive alerts within its warehouse management stack. Food, consumer goods, and automotive producers apply similar logic, tailoring sensor housings for wash-down or paint-shop environments.

Geography Analysis

North America led 2025 revenue with 35.21% of the conveyor monitoring market. Strict MSHA rules mandate continuous belt inspection, and skilled-labor costs above USD 35 per hour strengthen the ROI for predictive systems. Canadian miners in remote regions value monitoring because replacement parts often require helicopter delivery, which can stretch outages if failures go undetected.

Asia-Pacific records the fastest 4.19% CAGR as China, India, and ASEAN states retrofit legacy lines to hit productivity goals without costly greenfield plants. China’s Ministry of Industry and Information Technology allocated RMB 50 billion to smart manufacturing upgrades in 2024. India’s production-linked incentives reimburse automation spending that improves throughput, spurring software demand across 2,500 new factories built last year. Japan’s aging workforce drives automation to cover shrinking technical head counts.

Europe, South America, and the Middle East and Africa supply the balance of global revenue. Germany’s automotive lines integrate conveyor KPIs with Industry 4.0 platforms to maintain flexible mixed-model assembly. Brazil’s Vale installs rip-detection sensors across Minas Gerais after heightened post-Brumadinho oversight. Saudi Arabia’s Vision 2030 allocates USD 500 billion for diversified industrial clusters that emphasize modern materials-handling infrastructure

Competitive Landscape

The top five suppliers, ABB, Siemens, Honeywell, Rockwell Automation, and Emerson, hold an estimated 35-45% conveyor monitoring market share. They bundle sensors, analytics, and integration services, leveraging installed PLC and DCS footprints to cross-sell monitoring add-ons. Specialty firms such as 4B Braime, Fenner Dunlop, and ContiTech dominate belt-rip and splice-integrity niches, differentiating through domain expertise and rugged sensor designs.

Consolidation is ongoing. Rockwell bought Plex Systems for USD 2.2 billion to weave manufacturing execution data into FactoryTalk health dashboards. Emerson merged with AspenTech to fuse process simulation and predictive analytics, forming a USD 16 billion hybrid software-hardware player.

White-space competition centers on low-cost wireless kits priced below USD 25,000 per line. Start-ups ship battery sensors that link straight to cloud APIs, bypassing plant control networks, ideal for remote mines and distributed parcel hubs. Vendors also compete on cybersecurity, making IEC 62443 certification a bidding prerequisite in food, pharma, and critical infrastructure tenders.

Conveyor Monitoring Industry Leaders

Eaton Corporation plc

Parker Hannifin Corporation

ABB Ltd.

Emerson Electric Co.

ContiTech AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: SKF rolled out PredictiveGuard, a subscription package bundling wireless sensors, cloud analytics, and remote diagnostic support that targets small and mid-sized factories with monthly pricing below USD 1,000 per monitored conveyor line

- September 2025: Honeywell and Amazon Web Services launched a Conveyor Digital Twin Service inside the Honeywell Forge suite, letting logistics hubs simulate belt tension scenarios and schedule maintenance directly from the AWS IoT Core dashboard

- June 2025: Rockwell Automation released FactoryTalk Edge Gateway 2.0, adding on-device machine-learning models that classify bearing faults and belt misalignment locally before forwarding summarized alerts to PlantPAx DCS environments

- March 2025: ABB introduced Ability Edge Insight for Conveyors, a plug-and-play gateway that embeds vibration analytics and cyber-security hardening for legacy drives, enabling operators to activate cloud diagnostics in under 30 minutes

Global Conveyor Monitoring Market Report Scope

The conveyor monitoring market report is segmented by Type (Hardware, and Software), Type of Monitoring (Conveyor Belt Monitoring, and Conveyor Motor Monitoring), Conveyor Type (Belt Conveyors, Roller Conveyors, Overhead Conveyors, Pallet Conveyors, Screw and Other Specialty Conveyors), End-user Industry (Automotive, Consumer Goods Packaging, Mining, Food and Beverage, Logistics and Warehousing, Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Conveyor Belt Monitoring |

| Conveyor Motor Monitoring |

| Belt Conveyors |

| Roller Conveyors |

| Overhead Conveyors |

| Pallet Conveyors |

| Screw and Other Specialty Conveyors |

| Automotive |

| Consumer Goods Packaging |

| Mining |

| Food and Beverage |

| Logistics and Warehousing |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Type | Hardware | ||

| Software | |||

| By Type of Monitoring | Conveyor Belt Monitoring | ||

| Conveyor Motor Monitoring | |||

| By Conveyor Type | Belt Conveyors | ||

| Roller Conveyors | |||

| Overhead Conveyors | |||

| Pallet Conveyors | |||

| Screw and Other Specialty Conveyors | |||

| By End-user Industry | Automotive | ||

| Consumer Goods Packaging | |||

| Mining | |||

| Food and Beverage | |||

| Logistics and Warehousing | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the conveyor monitoring market expected to grow to 2031?

Global revenue is forecast to expand from USD 271.99 million in 2026 to USD 322.35 million by 2031, posting a 3.46% CAGR.

Which segment adds the most revenue today?

Hardware components, sensors, controllers, and communication modules, represent 64.13% of 2025 revenue.

What drives adoption in e-commerce facilities?

Fulfillment centers lose up to USD 20,000 per hour during unplanned conveyor outages, so predictive monitoring offers quick ROI by cutting downtime up to 40%.

Why is motor monitoring gaining momentum?

Electric drives cause 30–40% of conveyor stoppages, and vibration analysis catches bearing or alignment faults weeks early, fueling a 4.62% CAGR for motor monitoring solutions.

Which region is growing the fastest?

Asia-Pacific shows the highest regional CAGR at 4.19% because China, India, and ASEAN nations subsidize Industry 4.0 retrofits in manufacturing.

Page last updated on: