Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

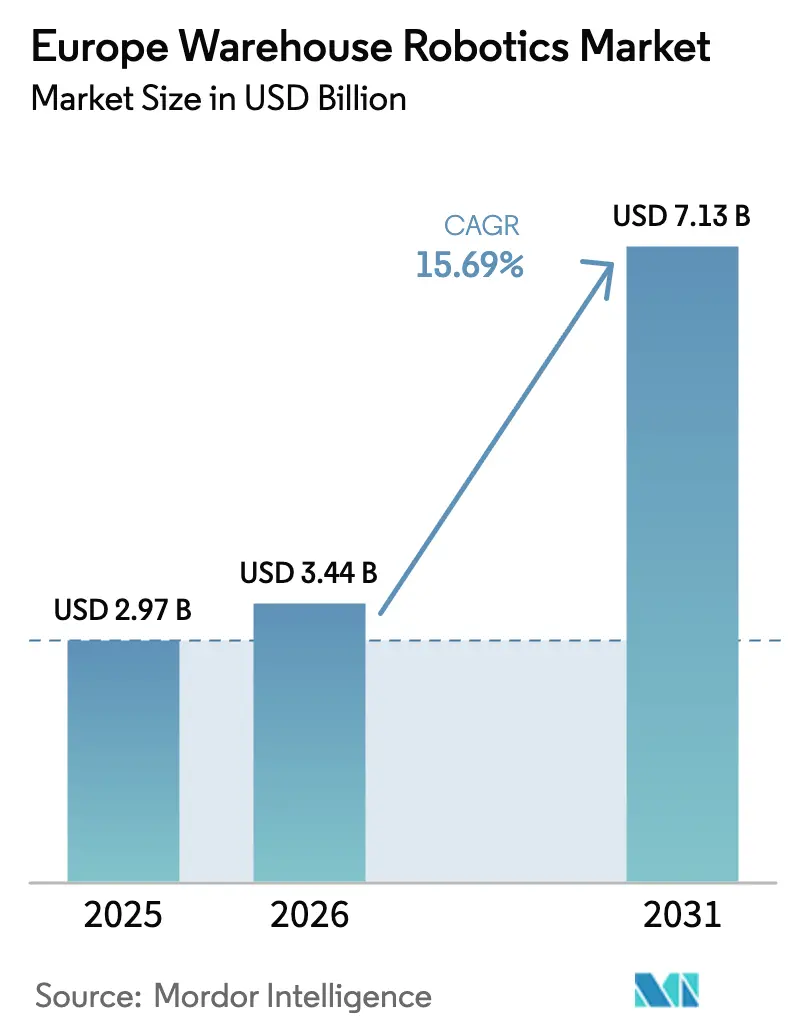

| Base Year Market Size (2025) | USD 2.97 Billion |

| Market Size (2026) | USD 3.44 Billion |

| Market Size (2031) | USD 7.13 Billion |

| Growth Rate (2026 - 2031) | 15.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Warehouse Robotics Market Analysis by Mordor Intelligence

The Europe warehouse robotics market size is valued at USD 3.44 billion in 2026 and is forecast to expand to USD 7.13 billion by 2031, underpinned by a 15.69% CAGR. The trajectory reflects sustained e-commerce penetration, persistent labor shortages, and policy pressure to improve energy efficiency. Demand is increasingly tilted toward agile automation that can be installed in weeks rather than months, allowing operators to match fulfillment capacity with volatile order volumes. Hardware remains most of today’s spending, yet the fastest incremental value is moving into fleet-orchestration software that can optimize path planning, task allocation, and predictive maintenance. Competitive intensity is accelerating as venture-backed mobile-robot suppliers scale in a market long dominated by legacy integrators.

Key Report Takeaways

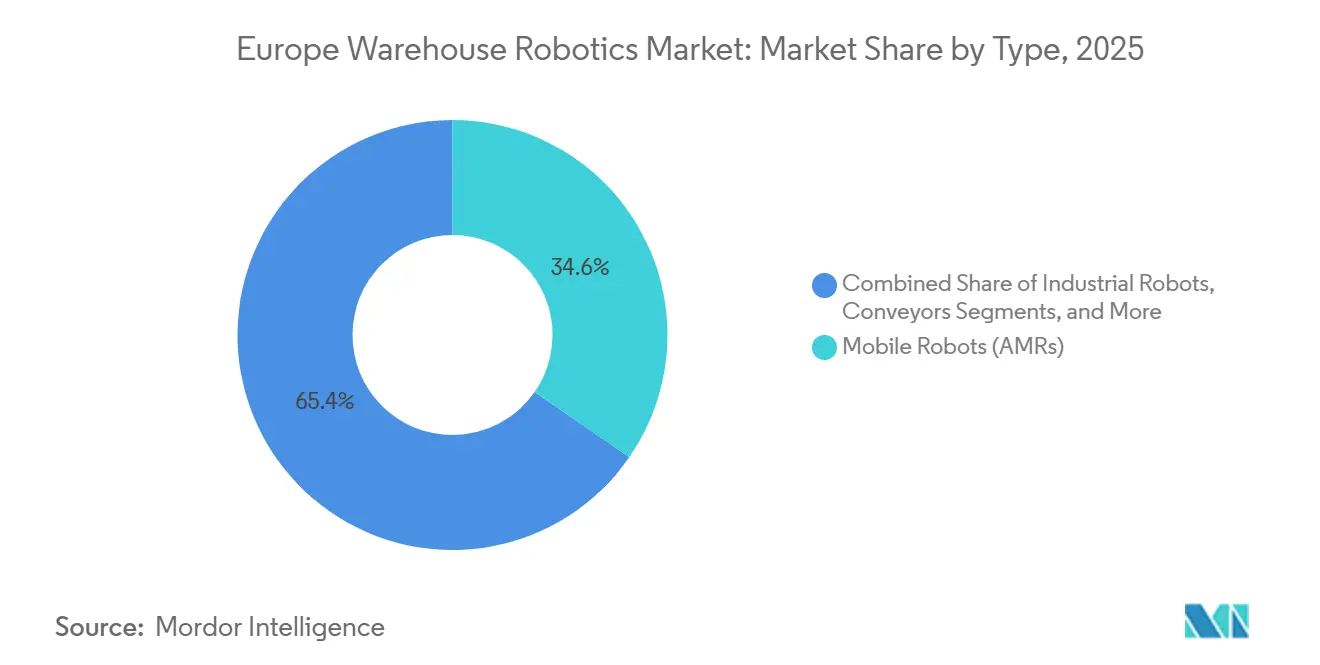

- By type, mobile robots held 34.63% of the Europe warehouse robotics market share in 2025, and are projected to record the highest 16.33% CAGR through 2031.

- By function, storage dominated with 46.73% share of the Europe warehouse robotics market size in 2025, whereas trans-shipments are forecast to expand at 16.56% CAGR to 2031.

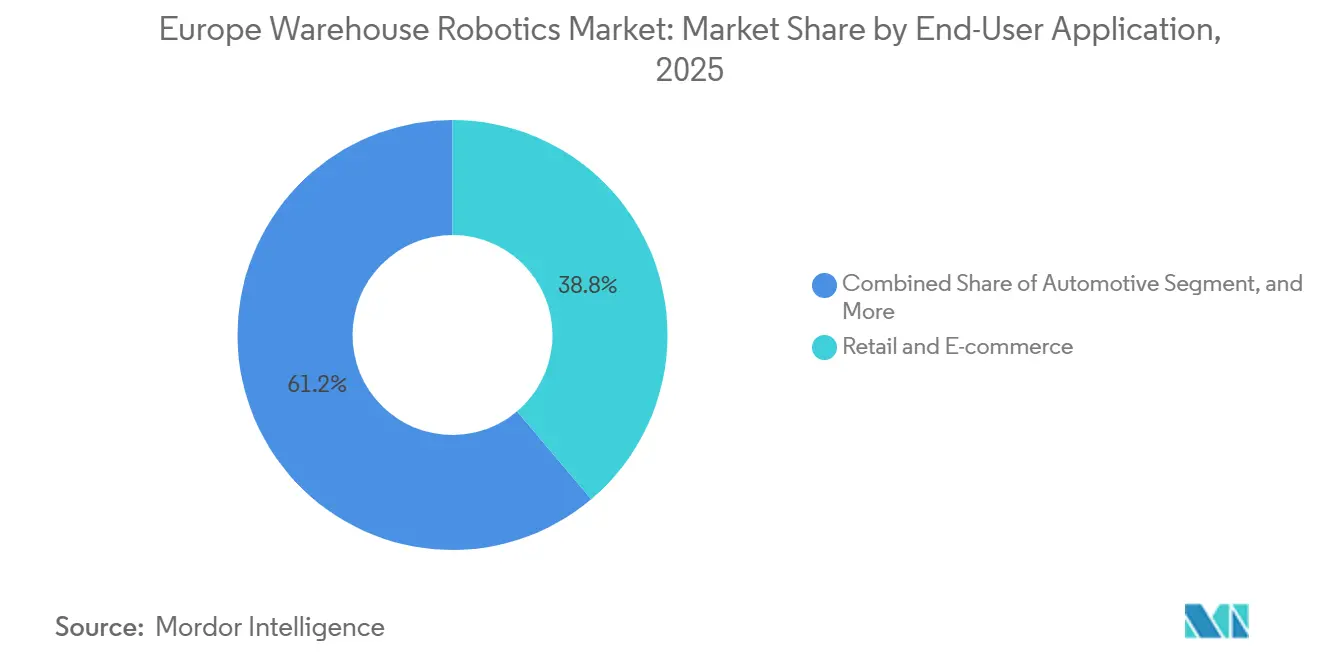

- By application, retail and e-commerce captured 38.83% of the Europe warehouse robotics market in 2025 and stands to grow at a 16.21% CAGR during the outlook period, with pharmaceuticals trailing close behind as the fastest-scaling niche.

- By component, hardware accounted for 62.84% share in 2025, yet software-driven revenues are rising at 17.11% CAGR as orchestration platforms become pivotal.

- By country, Germany led with 31.84% of the Europe warehouse robotics market share in 2025, while Spain is set to post the quickest 16.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Warehouse Robotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge of e-commerce micro-fulfillment centers | +3.2% | Western Europe (Germany, UK, France, Netherlands), expanding to Spain and Italy | Short term (≤ 2 years) |

| Growing SKU proliferation in omni-channel retail | +2.8% | Pan-European, concentrated in Germany, UK, France retail hubs | Medium term (2-4 years) |

| Rising intra-logistics labor shortages | +3.5% | Germany, Netherlands, UK, Nordics; acute in urban fulfillment zones | Medium term (2-4 years) |

| EU Green Deal incentives for energy-efficient automation | +2.1% | EU-27 member states; strongest uptake in Germany, Netherlands, Denmark | Long term (≥ 4 years) |

| Proliferation of open API-based robot orchestration software | +2.4% | Germany, Netherlands, UK; technology hubs with high WMS integration complexity | Medium term (2-4 years) |

| Venture capital inflow into AMR start-ups | +1.9% | UK, Germany, France, Switzerland; concentrated in robotics innovation clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge of E-Commerce Micro-Fulfillment Centers

Micro-fulfillment centers positioned within 10 kilometers of city cores compress delivery windows to under 2 hours while cutting real-estate costs by 60% relative to regional distribution centers. Ocado’s grid-based robots in Villeneuve-d’Ascq process 60,000 grocery orders weekly with 98.5% picking accuracy, showing how vertically integrated automation captures both margin and data. AutoStore’s 100,000-bin project at Norway Post in 2024 demonstrated 400% space-utilization gains that make micro-warehousing viable even when lease rates exceed EUR 25 per square meter. Retailers therefore internalize fulfillment and demand modular robots able to scale from 5,000 to 50,000 SKUs without redesign, reinforcing the growth path of the Europe warehouse robotics market.

Growing SKU Proliferation in Omni-Channel Retail

Retailers that manage more than 100,000 SKUs across stores and online channels see manual picking errors climb 12% for every additional 10,000 SKUs. KNAPP’s Open Shuttle Fork at Boozt.com dynamically re-slots fast movers every 4 hours, shortening operator walk-distance by 40%. Zalando’s 150,000-SKU facility in Mönchengladbach leverages vision-guided piece-picking that adapts to packaging changes without reprogramming. Such flexibility is unattainable with static conveyor layouts, driving demand for software-rich mobile robots that help the Europe warehouse robotics market meet diverse order profiles.

Rising Intra-Logistics Labor Shortages

A survey indicated that most logistics operators struggled to fill warehouse roles in 2024. Wage inflation exceeding 8% in German logistics has compressed operating margins to single digits, shortening the payback period for automation to less than 18 months, even for fleets of EUR 3 million. GEODIS replaced 300 pickers with 1,000 LocusBots and lifted throughput 2.5 times in 2024.[1]Maersk, “Logistics Labor Shortage Survey 2024,” MAERSK.COM Labor scarcity, therefore, remains the single most immediate catalyst for the European warehouse robotics market.

EU Green Deal Incentives for Energy-Efficient Automation

The Energy Efficiency Directive mandates 32.5% energy-use reduction by 2030, exposing non-compliant warehouses to fines up to 4% of annual revenue. ABB’s Robotic Item Picker employs recuperative servo drives that reduce electricity demand 35% per 1,000 picks while maintaining 1,200-item hourly throughput.[2]ABB, “ABB Robotic Item Picker Launch with Covariant AI,” NEW.ABB.COM High energy tariffs of EUR 0.30 per kilowatt-hour in the Netherlands make such savings pivotal, placing sustainability incentives at the core of the Europe warehouse robotics market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and long ROI cycles | -2.7% | Southern Europe (Spain, Italy), Eastern Europe; SME-dominated logistics markets | Short term (≤ 2 years) |

| Fragmented legacy WMS/ERP integration challenges | -2.1% | Germany, France, UK; enterprises with multi-vendor IT stacks | Medium term (2-4 years) |

| Limited availability of safety-certified cobot standards | -1.3% | EU-27; regulatory harmonization gaps between member states | Long term (≥ 4 years) |

| Persistent shortage of robot-skilled maintenance talent | -1.6% | Spain, Italy, Eastern Europe; regions with limited industrial automation heritage | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Long ROI Cycles

Typical greenfield projects demand EUR 2 million to EUR 5 million, amounting to 24–36 month payback that many Spanish and Italian operators deem excessive. Robots-as-a-Service contracts payable at EUR 1,500 to EUR 3,000 per robot per month mitigate cash-flow risk but still require multi-year commitments. Small and mid-sized firms handling fewer than 10,000 daily orders therefore delay adoption, tempering near-term momentum in the Europe warehouse robotics market.

Fragmented Legacy WMS and ERP Integration Challenges

Enterprises running mixed stacks of SAP, Oracle, and bespoke warehouse systems face integration outlays upward of EUR 1 million, and project timelines often slip by three to six months. Siemens’ Simatic Robot Pick AI Pro slashes integration to eight weeks via pre-configured SAP connectors. However, only a third of European WMS deployments currently support the VDA 5050 protocol natively, leaving middleware as a stop-gap that adds latency. Interoperability bottlenecks thus slow some deployments in the Europe warehouse robotics market even when the capital budget is approved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mobile Robots Lead Flexibility Shift

Mobile robots, including AMRs and AGVs, captured 34.63% of 2025 Europe warehouse robotics market share and are projected to grow at 16.33% CAGR through 2031. GXO’s 500-unit Geek+ rollout achieved triple throughput in a French sporting-goods site after only eight weeks of installation.[3]GXO, “GXO and Geek+ AMR Deployment in France,” GXO.COM The Europe warehouse robotics market size for mobile robots is set to widen further as parcel hubs replace fixed conveyors with self-navigating units able to adapt to daily SKU churn.

Sortation systems remain indispensable where parcel volume exceeds 50,000 units per day, evidenced by BEUMER’s BG Sorter running 15,000 parcels hourly at DHL’s Leipzig hub. Yet their EUR 5 million-plus price tag and year-long lead times limit uptake to mega-sites. Industrial robots are expanding into intralogistics, as exemplified by KUKA’s KMR iisy cobot, which delivers 800 picks per hour and addresses mixed-SKU zones. The preference for reconfigurable solutions keeps mobile platforms squarely at the heart of growth for the Europe warehouse robotics market.

By Function: Trans-Shipments Accelerate Cross-Docking Velocity

Storage remained the largest function in 2025, holding 46.73% share within the Europe warehouse robotics market. However, trans-shipments are forecast to post a 16.56% CAGR as operators strive to clear inventory inside 24 hours to contain carrying costs. Exotec’s partnership with Decathlon resulted in a 80% shift of orders to direct cross-dock flows, eliminating static holding areas and reducing the facility footprint by 40%.

Packaging automation is also on the rise, particularly in Germany, where labor costs exceed EUR 18 per hour, enabling robotic case erectors to pay back within three years. Returns processing and kitting still rely heavily on people due to SKU variability, but new vision-guided pick-and-place tools indicate an emerging inflection point. As the same-day economy matures, throughput velocity rather than storage density will dictate layout, steering investments toward high-speed sorters and mobile robots that keep the Europe warehouse robotics market expanding.

By End-User Application: Retail Dominance Masks Pharmaceutical Upside

Retail and e-commerce applications contributed 38.83% of 2025 revenue and will advance at 16.21% CAGR to 2031. Amazon’s GBP 1.2 billion commitment to Proteus AMRs across United Kingdom and German sites illustrates scale economics that only automated fleets can sustain. Yet pharmaceutical operators, though smaller in total spend, deploy deeper automation to guarantee temperature integrity and traceability. Swisslog Healthcare’s 27,000-bin AutoStore at NHS Highland secures 99.9% accuracy at 2-8 °C storage, a precision level that manual processes cannot guarantee.

Automotive players use AMRs for line-side replenishment, cutting work-in-process inventories by 30%. Electrical and electronics warehouses pursue vertical-lift systems to maximize space, while food and beverage operators grapple with multi-temperature complexity that favors modular micro-fulfillment. Collectively these verticals reinforce steady, demand-diverse growth across the Europe warehouse robotics market.

By Component: Software Growth Signals Value Migration

Hardware accounted for 62.84% of 2025 spending, yet software revenues are scaling at a 17.11% CAGR as operators shift to data-driven control layers. SAP’s move to embed orchestration directly into Extended Warehouse Management illustrates how enterprise software giants now view robotics as a native extension of supply-chain suites. The Europe warehouse robotics market size tied to software is accordingly predicted to expand faster than any mechanical segment.

Services revenues grow in absolute terms but face compression as Robots-as-a-Service models bundle maintenance inside monthly fees. ABB’s Madrid training center, which will skill 500 technicians annually, aims to close the maintenance talent gap that could otherwise stall fleet uptime. VDA 5050 standardization allows heterogeneous fleets to run on a single dashboard, accelerating multi-vendor site rollouts and further boosting the software portion of the Europe warehouse robotics market.

Geography Analysis

Germany led with 31.84% of 2025 revenue, reflecting dense automotive and e-commerce clusters that support mega-sites exceeding 50,000 square meters. Germany’s stringent ISO 10218-2 compliance adds EUR 50,000 to EUR 100,000 per deployment, yet local operators value the 99.5% uptime benchmark delivered by established integrators. Spain, on a lower automation base, is forecast to expand at a 16.67% CAGR as Barcelona and Madrid attract EUR 2 billion of logistics real-estate investment and deploy greenfield facilities free of legacy constraints.

The United Kingdom continues to invest despite Brexit-induced border frictions, with Amazon’s Proteus network ensuring two-day coverage. France’s grocery retailers, led by Auchan, partner with Ocado to integrate grid robotics that handle 60,000 orders weekly, a model under assessment by Carrefour and Casino. Italy trails in adoption owing to fragmented warehouses under 10,000 square meters; however, fashion majors like Inditex are piloting mobile robots in Milan to drive brand-specific logistics.

The Netherlands leverages its cross-border gateway, hosting AutoStore integrator labs and serving next-day delivery windows across Belgium, Germany, and the United Kingdom. Nordic countries showcase high automation density, whereas most Eastern European sites remain manual because labor still averages EUR 9 to EUR 13 per hour. Overall, regional penetration differs widely, yet the Europe warehouse robotics market is converging as southern and eastern markets seek to replicate western benchmarks.

Regulatory Landscape

Warehouse robotics deployments across Europe operate within EU machinery safety and functional safety requirements, with additional governance expectations starting to shape how companies document and demonstrate controls. Conformity assessment and documentation obligations can affect time-to-deploy, and a central reference point is Regulation (EU) 2023/1230 (Machinery Regulation), which replaces the 2006 Machinery Directive and becomes mandatory on 20 January 2027. The regulation tightens requirements around software integrity, networked control systems, and self-learning functions that are relevant for AMRs, AS/RS, and robot cells used in intralogistics.

In May 2026, the European Commission adopted a Digital Omnibus proposal clarifying that AI systems serving safety functions in machinery are primarily handled through the Machinery Regulation framework, reducing duplication versus the AI Act for safety-related embedded AI. The Machinery Regulation also formalizes the concept of a “substantial modification” (including digital changes) that can trigger a new conformity assessment for the modified portion. This is material for operators updating fleet software, navigation stacks, or safety logic in live sites while maintaining CE conformity.

Value Chain Analysis

The Europe warehouse robotics value chain starts with component suppliers such as sensors, safety systems, controllers, drives, batteries, and compute. Robot and subsystem OEMs, including AMRs/AGVs, AS/RS, sortation, and pallet-handling players, then feed into systems integrators and software providers that deliver WMS/WCS integration, fleet orchestration, and site commissioning. Lifecycle services (simulation, installation, safety validation, training, maintenance, and spares) run alongside facility operators such as retailers, 3PLs, and manufacturers, where multi-vendor interoperability and uptime determine realized ROI.

Recent program-level moves in Europe point to increasing standardization and multi-site replication. Exotec announced the Skyfleet multi-site automation program for Decathlon across seven warehouse sites spanning France, the UK, Portugal, Italy, and Germany (March 2026), while Lyreco completed a modernization of its Villaines-la-Juhel facility in France with over 100 Skypod robots (April 2026). On the upstream side, Colruyt Group and KION launched a new R&D center for next-generation supply chain robotics (July 2026), reflecting continued investment aimed at productization and software-defined automation that reduces reliance on bespoke, one-off integration.

Competitive Landscape

Dematic, Swisslog, SSI Schaefer, Vanderlande, and KNAPP dominate the market, holding the lion's share. Meanwhile, over 50 AMR start-ups, alongside aggressive Chinese entrants, carve out a significant portion, largely driven by competitive pricing. In 2024, investors showcased their enthusiasm for vision navigation and real-time inventory scanning, evident from Seegrid's USD 50 million Series C and Dexory's USD 80 million Series B funding rounds. Responding to this trend, industry giants are forging AI partnerships such as ABB has harnessed Covariant's reinforcement learning, boosting first-pick accuracy to an impressive 98%, and Siemens has integrated SAP connectors, streamlining IT overhead costs.

Emerging disruptors are leveraging open API orchestration and RaaS models to bypass capital budget constraints, with 25% of 2024 European deployments structured as operational leases charging EUR 1,500 to EUR 3,000 (USD 1,695 to USD 3,390) per robot per month. VDA 5050 protocol adoption by 12 AMR vendors in 2024 commoditized fleet management interfaces, enabling operators to deploy heterogeneous robot fleets under unified control layers and eroding proprietary system lock-in that incumbents historically exploited.

Strategic moves include SSI Schaefer's EUR 100 million (USD 113 million) acquisition of Wanzl Group in July 2024 to consolidate retail automation capabilities, and Amazon's verticalization of robotics through Proteus AMR deployments processing 5 billion items annually across UK and German fulfillment centers, a scale that creates cost advantages unattainable by third-party integrators. Technology differentiation is migrating from mechanical precision to AI-driven adaptability, with Siemens' Simatic Robot Pick AI Pro launched in March 2025 processing 1,200 items per hour with 98% accuracy through vision systems that handle packaging variations without reprogramming.

Europe Warehouse Robotics Industry Leaders

ABB Ltd.

KUKA AG

SSI Schaefer AG

KION Group AG

KNAPP AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is scaling software-defined, interoperable automation across heterogeneous fleets, which aligns with the market shift toward orchestration platforms and open interfaces. This direction is supported by VDA 5050 adoption dynamics and the growing emphasis on WMS-native orchestration referenced in the broader context. Enterprise-led adoption examples include SAP embedding robotics orchestration into Extended Warehouse Management (November 2025), which supports tighter integration between WMS workflows and AMR and robot execution layers and reduces middleware complexity for multi-vendor sites.

Another opportunity involves expanding beyond classic AMRs into new form factors and broader AI-enabled task coverage in mixed environments, using live pilots and large buyer programs as reference points. Vodafone, SAP, and Accenture launched a pilot at a Vodafone warehouse in Duisburg, Germany (April 2026), using humanoid robots for tasks such as inspection and pallet stacking integrated with SAP EWM. Separately, Amazon announced an investment of over EUR 10 billion to modernize European warehouse and delivery networks (June 2026), which reinforces demand for next-generation autonomous systems within high-throughput fulfillment operations and can pull through spend on integrators, safety validation services, and fleet-operations tooling.

Recent Industry Developments

- July 2026: ABB Robotics launched the Flexley Stack F712 autonomous forklift, using vSLAM navigation to support warehouse storage and intralogistics moves. The release expands AMR portfolios into forklift-class handling, increasing automation coverage for pallet transport and put-away workflows where labor and safety constraints are acute.

- November 2025: SAP embedded robotics orchestration inside SAP Extended Warehouse Management to enable real-time fleet coordination across VDA 5050-compliant robots. By bringing orchestration closer to core WMS processes, the move reduces integration friction for multi-vendor robot fleets and strengthens software-centric differentiation in warehouse robotics deployments.

- July 2024: SSI Schaefer acquired Wanzl Group for EUR 100 million to consolidate retail automation capabilities. The deal broadened SSI Schaefer’s portfolio for store and warehouse intralogistics, supporting end-to-end project delivery across automated storage, material flow, and last-meter handling requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers robotics and automation systems that are deployed inside warehouses across Europe to move, store, pick, sort, and package goods, along with the related software and services that make these systems run in daily operations.

Scope exclusions: We exclude non-warehouse factory-floor automation and last-mile delivery robots that operate outside the warehouse environment.

Segmentation Overview

- By Type

- Industrial Robots

- Sortation Systems

- Conveyors

- Palletizers

- Automated Storage and Retrieval Systems (ASRS)

- Mobile Robots (AGVs and AMRs)

- By Function

- Storage

- Packaging

- Trans-shipments

- Other Functions

- By End-user Application

- Food and Beverage

- Automotive

- Retail and E-commerce

- Electrical and Electronics

- Pharmaceutical and Healthcare

- Other End-user Applications

- By Component

- Hardware

- Software

- Services

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base market structure and keep country-level assumptions grounded. We relied on public signals such as Eurostat datasets on labor, output, and trade, plus guidance from the European Commission on automation, safety, and industrial policy that can influence capital spending.

To ground demand drivers, we also reviewed sources such as national statistical offices for warehousing and transport activity, customs and trade releases for machinery categories, and trade bodies focused on intralogistics and material handling. Company annual reports, earnings decks, and reputable press were used to track expansion plans, distribution center footprints, and investment priorities. In parallel, we used paid subscriptions focused on company financials and intelligence, alongside patent databases, to map product direction and check that technology adoption trends align with what respondents described in interviews. These desk sources are not exhaustive, and we used additional public references for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary interviews and structured surveys were carried out with warehouse operators, integrators, component suppliers, and software and service providers, so assumptions could be tested against what is actually being deployed. Inputs were also taken across key European countries and the rest of the region to reflect differences in labor costs, e-commerce intensity, and automation maturity, then used to reconcile gaps seen in public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | |

| Mid tier: 51% | Functional/Unit leaders: 32% | |

| Smaller Players: 19% | Managers: 56% |

Market-Sizing & Forecasting

Market sizing was built with a top-down and bottom-up approach, starting from the addressable warehouse automation spending pool by country and then filtering it to robotics-specific adoption. In practice, trade and production indicators for automation equipment, warehousing activity, and investment intensity were used to reconstruct the demand pool, followed by an adjustment for how fast robotics is penetrating key warehouse tasks.

To make the totals usable, the model tracks practical inputs such as new warehouse and fulfillment capacity additions, e-commerce order volumes and throughput intensity, labor availability and wage pressure, and typical system mix shifts toward mobile robots and AS/RS in large sites. We also factor in replacement cycles, project lead times, and the share of spending that falls under services and software versus hardware, since this affects the value capture timing from year to year. After the top-down build, selective bottom-up checks were done using sampled average selling price ranges by system type and plausible installed base additions drawn from channel feedback, and then the totals were corrected where the implied units or spend looked inconsistent.

For forecasting, scenario analysis was used because investment timing can swing with macro conditions and supply chain confidence. Base case, conservative, and faster adoption tracks were reviewed with primary respondents, and the final forecast path reflects the most repeated expectations on rollout pace, budget approvals, and technology readiness.

Data Validation & Update Cycle

Validation was done through step-by-step cross-checks, where outputs were compared against independent signals such as warehouse construction activity, automation investment commentary, and the implied split between hardware, software, and services. When the model created large country-level jumps, we rechecked the assumptions behind adoption rates, pricing, and installation timing, and triggered follow-up calls to confirm whether the shift was real or caused by a modeling artifact.

Before sign-off, the full workbook is reviewed in multiple internal passes to confirm consistent definitions, currency handling, and year mapping of revenues. Reports are refreshed annually, and interim updates are made when there are material events that can change demand, such as regulation changes, major capacity expansions, or supply constraints. Right before delivery, we run a final update sweep so outputs reflect the latest available information.

Mordor Intelligence's Europe Warehouse Robotics Market Size Compared Against Other Published Estimates

Published market sizes for Europe warehouse robotics often look different, even when the topic name sounds similar. This usually happens because each publisher draws the market boundary in a slightly different way, then applies different timing rules for when revenues are counted.

The key gap drivers in this market tend to be whether conveyor and sortation heavy packages are counted fully as robotics, how AS/RS value is treated, and if software and services are included as part of the same spend pool. Differences can also come from base year selection, the way prices are progressed over time, and whether country-level adoption is validated with operator and integrator feedback or assumed from a single macro indicator.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.97 B (2025) | |

| Industry Publisher A | USD 3.67 B (2025) | This figure appears to reflect a broader automation basket, where large conveyor and sortation packages are more likely to be counted fully, which can lift the value in years with big fulfillment buildouts. |

| Industry Research Outlet B | USD 1.96 B (2024) | This estimate is anchored to an earlier base year and may apply more conservative adoption and pricing progressions, and it is not always clear how AS/RS and services are treated inside the total. |

The table shows a spread that mainly comes from what gets counted as warehouse robotics versus wider warehouse automation, and from when multi-year projects are recognized as revenue. In Mordor Intelligence's model, automation types like conveyors, sortation systems, AS/RS, and mobile robots are included, but the totals are built country by country with adoption and revenue timing checked through interviews so that short-term swings are not overstated when large projects get announced late in the year.

Key Questions Answered in the Report

How large is the Europe warehouse robotics market in 2026?

The Europe warehouse robotics market size stands at USD 3.44 billion in 2026 and is forecast to reach USD 7.13 billion by 2031.

What is the expected growth rate for warehouse robotics in Europe?

The market is projected to register a 15.69% CAGR during 2026-2031, driven by e-commerce fulfillment, labor shortages, and energy-efficiency mandates.

Which robot type is expanding fastest in European warehouses?

Mobile robots, covering AMRs and AGVs, are set to grow at 16.33% CAGR as operators prioritize flexible automation that installs in weeks.

Why is software important in Europe’s warehouse robotics space?

Standardization via VDA 5050 and AI-driven optimization shift value toward orchestration software, enabling multi-vendor fleets to operate under one control layer and supporting a 17.11% CAGR for software revenues.

Which country is the most attractive for warehouse robotics deployment in Europe?

Germany leads on absolute spending because of automotive and e-commerce density, while Spain shows the fastest growth potential at 16.67% CAGR owing to new real-estate developments.

Page last updated on: