Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.53 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Food Emulsifiers Market Analysis by Mordor Intelligence

Europe food emulsifiers market size in 2026 is estimated at USD 1.24 billion, growing from 2025 value of USD 1.19 billion with 2031 projections showing USD 1.53 billion, growing at 4.28% CAGR over 2026-2031. Sustained demand is coming from clean-label reformulation, the pivot to plant-derived ingredients, and retailer commitments that favor non-GMO inputs. Price swings in sunflower and rapeseed oils are squeezing gross margins for lecithin and glyceride processors. Yet, multi-functional emulsifiers that lower total ingredient counts are helping manufacturers offset cost pressure. The European food emulsifiers market is also being reshaped by flexitarian diets, which are accelerating the uptake of plant-based meat and dairy alternatives and expanding the addressable pool for premium lecithin and mono-diglyceride blends. Meanwhile, technical advances in enzymatic modification and heat-stable chemistries are widening use cases in high-temperature bakery, frozen desserts, and protein-fortified beverages.

Key Report Takeaways

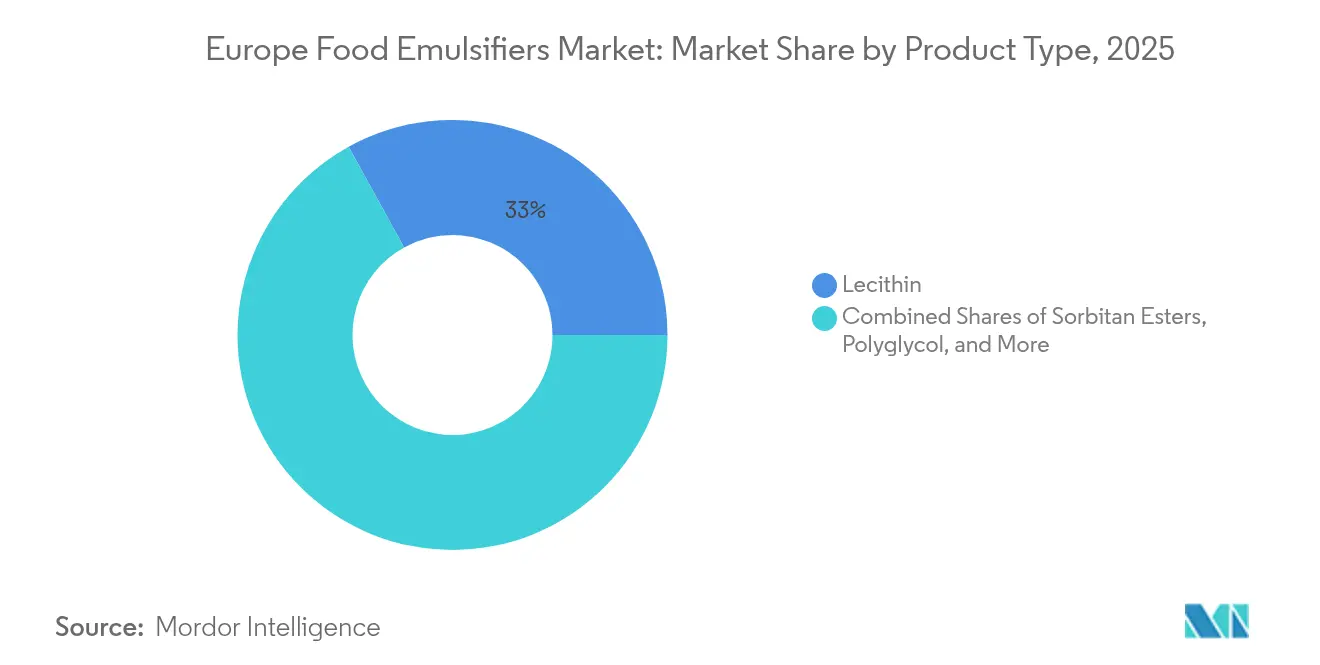

- By product type, lecithin held 33.02% of 2025 revenue while mono- and di-glycerides are projected to rise at a 6.02% CAGR through 2031.

- By source, plant-derived emulsifiers captured 59.58% of 2025 demand and are expected to expand at a 6.84% CAGR.

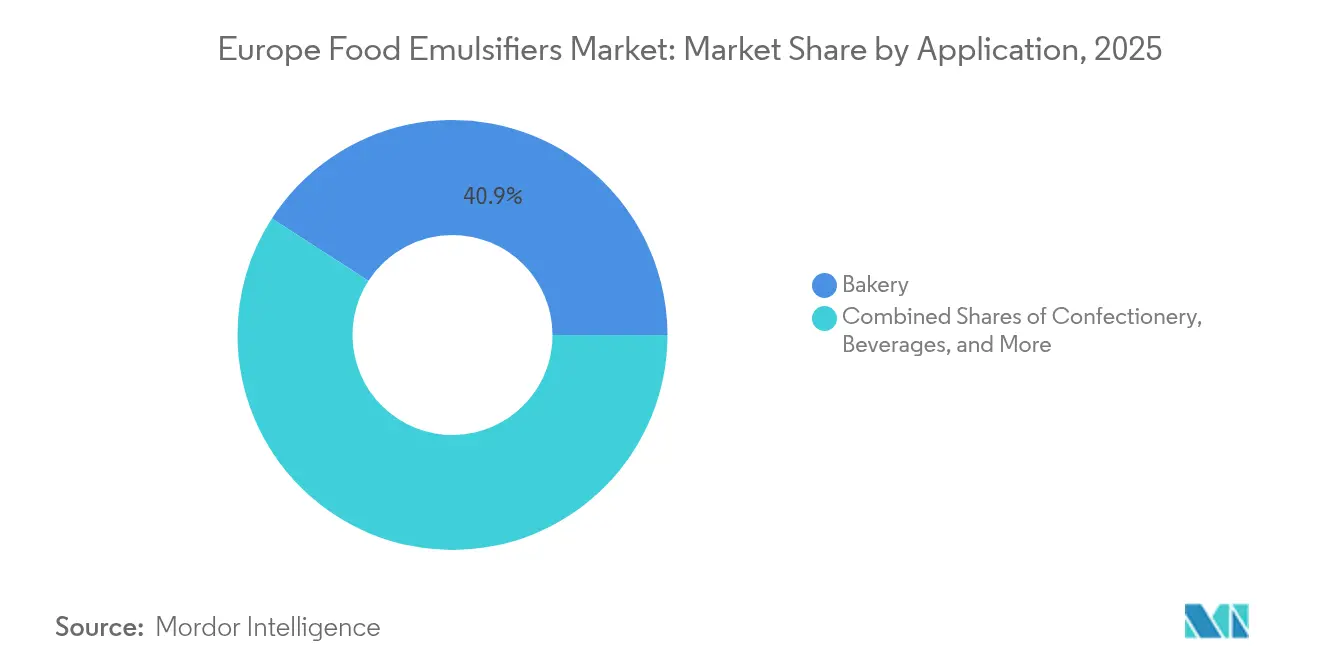

- By application, bakery led with 40.88% share in 2025, whereas plant-based meat and dairy alternatives are advancing at an 7.65% CAGR to 2031.

- By geography, the United Kingdom accounted for 25.41% value in 2025, while Spain is forecast to achieve a 5.82% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Food Emulsifiers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of processed and convenience foods | +0.9% | UK, Germany, France, Netherlands | Medium term (2-4 years) |

| Expansion in bakery and confectionery sectors | +1.1% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Innovation in functional foods, including sports nutrition and high-protein products | +0.7% | UK, Germany, Netherlands | Long term (≥ 4 years) |

| Shift toward clean-label and plant-based emulsifiers | +1.3% | UK, Germany, France, Spain, Netherlands | Short term (≤ 2 years) |

| R&D investments for multi-functional emulsifiers | +0.5% | Germany, Netherlands, UK | Long term (≥ 4 years) |

| Increasing use in margarine, spreads, and ice cream for shelf-life extension | +0.6% | Germany, UK, Italy, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumption of Processed and Convenience Foods

Urbanization and the growth of dual-income households are driving the demand for ready meals, sauces, and dressings—all categories that heavily depend on emulsifiers. According to the Agriculture and Horticulture Development Board data from 2025, retail sales of chicken convenience meals was 38% in the United Kingdom[1]Source: Agriculture and Horticulture Development Board 2025, "Ready meals remain a staple as consumers crave convenience", ahdb.org.uk. For example, mayonnaise and salad dressings use egg yolk or lecithin to stabilize oil-water interfaces, while frozen pizzas and lasagnas rely on mono-diglycerides to prevent cheese separation during reheating. The UK and Germany have the highest per-capita spending on convenience foods, a trend further supported by the increasing penetration of e-commerce grocery platforms, which favor shelf-stable, pre-portioned formats. However, the market is stabilizing through premiumization. Organic frozen meals and plant-based ready-to-eat options are gaining shelf space, with these products often requiring more emulsifiers per serving to replicate the texture of traditional formulations. Furthermore, the shift toward smaller pack sizes—driven by the increase in single-person households—raises emulsifier intensity per kilogram of finished product due to higher surface-area-to-volume ratios.

Expansion in Bakery and Confectionery Sectors

The bakery sector continues to serve as the foundation of the industry, but its growth is branching out. Industrial bread and biscuit manufacturers are increasingly using emulsifier blends, such as mono-diglycerides combined with DATEM. This approach enhances product softness and reduces staling, effectively lowering returns and waste. Meanwhile, artisan bakeries are exploring lecithin to meet clean-label requirements while maintaining the crumb structure in sourdough and whole-grain loaves. In the confectionery segment, chocolate and praline producers are seeking alternatives to polyglycerol polyricinoleate (PGPR) that provide similar viscosity reduction without the association with palm oil. Germany and France lead this segment, collectively accounting for over 40% of bakery and confectionery emulsifier consumption. Consumers are increasingly choosing organic or high-protein options, which require advanced emulsification solutions. Spain’s confectionery sector is benefiting from a recovery in tourism, boosting seasonal production of turron and polvorones, both of which rely on sorbitan esters to prevent fat bloom. In Italy, the gelato industry is adopting mono-diglycerides to improve overrun and freeze-thaw stability. This shift is further accelerated by rising energy costs, which are encouraging longer cold-storage durations.

Shift Toward Clean-Label and Plant-Based Emulsifiers

Clean-label reformulation has transitioned from being a niche differentiator to a standard expectation across European retail. Non-GMO sunflower or rapeseed-sourced lecithin now carries a 15-20% price premium over soy-derived alternatives. However, brand owners accept this cost to avoid allergen declarations and comply with EU organic standards. This shift goes beyond ingredient replacements. Manufacturers are adopting enzymatic modification processes to create emulsifiers with simpler INCI names, avoiding the negative perception associated with E-numbers. For instance, Cargill plans to launch a sunflower lecithin line in 2024, specifically designed for the plant-based dairy sector, illustrating how suppliers are tailoring their portfolios to capitalize on the premiumization of alternative proteins. Major retailers like Tesco and Carrefour have set a 2026 deadline for clean-label compliance in their private-label ranges, accelerating reformulation timelines. Meanwhile, smaller bakeries and confectioners face challenges due to a lack of in-house R&D capabilities, making it difficult to replace traditional emulsifiers without affecting texture or shelf life. This gap creates a significant opportunity for ingredient suppliers to offer co-development partnerships, effectively leveraging their technical expertise alongside the raw materials they provide.

Innovation in Functional Foods, Including Sports Nutrition and High-Protein Products

Protein fortification is driving changes in emulsifier specifications. Whey and pea protein isolates, which have poor solubility, can destabilize oil-in-water emulsions. To address this, lecithin or modified starches are often used to maintain homogeneity in products like ready-to-drink shakes and protein bars. For example, Kerry Group introduced a lecithin-alginate blend in 2024 for high-protein beverages, highlighting a trend where suppliers combine emulsifiers with stabilizers to simplify formulations for brands entering the functional-nutrition market. Although the 0.7% CAGR contribution is smaller compared to clean-label or bakery trends, it carries significant long-term strategic value. Sports nutrition in Northern Europe is expected to grow at double-digit rates, driven by aging populations focused on muscle maintenance and younger generations adopting fitness-oriented lifestyles. The Netherlands and the UK, which lead in per-capita consumption of protein-enriched foods, serve as key test markets for innovative emulsifier systems. However, regulatory challenges remain: the European Commission's novel-food approval process can delay commercialization by 18-24 months, slowing the introduction of emulsifier innovations to the market.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict EU regulations on food additives | -0.8% | All European markets | Short term (≤ 2 years) |

| Heightened price volatility for vegetable oils and lecithin, driven by war-related supply shocks | -1.2% | Germany, France, Italy, Spain | Short term (≤ 2 years) |

| Disrupted sunflower seed and oilseed supply | -0.7% | Germany, France, Spain | Medium term (2-4 years) |

| Competition from alternative stabilizers and texturizers | -0.5% | UK, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strict EU Regulations on Food Additives

The European Food Safety Authority (EFSA) regularly re-evaluates approved additives, and its recent assessments have introduced stricter acceptable daily intake (ADI) limits for certain emulsifiers, such as titanium dioxide (E171) and specific polysorbates. Although most mainstream emulsifiers remain approved, the regulatory environment is becoming increasingly stringent. The EU's "Farm to Fork" strategy seeks to reduce pesticide use by 50% by 2030. While primarily focused on pesticide reduction, this strategy indirectly impacts oilseed cultivation practices, potentially increasing costs for organic or low-residue lecithin. Additionally, compliance with traceability requirements, like the EU Deforestation Regulation, adds administrative complexity for palm-oil-derived emulsifiers, even when sourced from certified sustainable plantations. Brands face challenges when substituting emulsifiers, as this requires stability testing and sensory panels, a process that can take 6 to 12 months. Regulatory uncertainty also discourages investment in new emulsifier chemistries. If an ingredient is re-evaluated within five years of commercialization, the return on research and development (R&D) investments is reduced. Smaller suppliers, often lacking dedicated regulatory affairs teams, are at a disadvantage. This situation may accelerate market consolidation, favoring multinationals with in-house EFSA liaison capabilities.

Heightened Price Volatility for Vegetable Oils and Lecithin, Driven by War-Related Supply Shocks

In 2024, sunflower oil prices rose by 60% compared to pre-conflict averages, increasing lecithin costs as it is a byproduct of oil refining. Ukraine and Russia previously supplied over 50% of Europe's sunflower seed imports. While Europe has partially mitigated the shortfall by sourcing from Argentina and Turkey, issues such as logistics bottlenecks and inconsistent quality persist. Rapeseed oil, the primary European alternative, is also facing challenges. Poor weather conditions in France and Germany caused a 12% decline in 2024 harvests, tightening domestic crushing margins. Smaller bakeries and confectioners, lacking hedging mechanisms, are struggling with rising costs that further compress their already narrow margins. Some are shifting to synthetic emulsifiers like polysorbates, but these are associated with E-number concerns and could require reformulation if clean-label demands grow stricter. This volatility is also impacting long-term R&D plans. Ingredient suppliers remain cautious about expanding sunflower-lecithin capacities due to uncertainties surrounding feedstock availability beyond 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mono-Diglycerides Lead Innovation

In 2025, lecithin captured 33.02% of the product market share, supported by its GRAS status, multifunctionality, and alignment with clean-label trends. While soy lecithin remains a cost-effective choice, sunflower and rapeseed variants are increasingly favored in premium bakery products and plant-based dairy alternatives. Mono- and di-glycerides are expected to grow at a 6.02% CAGR through 2031, making them the fastest-growing product type. Their versatility is notable: they not only act as emulsifiers but also serve as dough conditioners, anti-staling agents, and aerators in whipped toppings. Bakery professionals prefer distilled monoglycerides for their higher active content and neutral flavor, while ice cream manufacturers rely on acetylated monoglycerides to enhance freeze-thaw stability.

Sorbitan esters, while catering to niche applications, are valued for high-end uses such as reducing chocolate viscosity, aerating cake batter, and producing non-dairy whipped creams, where their thermal stability justifies premium pricing. Polyglycerol esters, though used in smaller volumes, are critical for low-fat spreads and reduced-calorie dressings, as they stabilize emulsions more efficiently than lecithin. The "Others" category includes emerging chemistries like sucrose esters and enzymatically modified lecithins, which attract formulators seeking innovative functionalities or cleaner labels. Palsgaard's 2024 patent for a heat-resistant polyglycerol ester blend underscores ongoing innovation in this segment, focusing on bakery applications that emphasize oven-spring and crumb softness.

By Source: Plant-Derived Dominates

In 2025, plant-derived emulsifiers accounted for 59.58% of the source-based market share and are projected to grow at a 6.84% CAGR, surpassing their animal-derived counterparts. This growth is driven by three key factors: increasing adoption of vegan and flexitarian diets, allergen-avoidance measures, and sustainability mandates from retailers. Leading the plant segment are sunflower lecithin, rapeseed-derived mono-diglycerides, and soy-based emulsifiers. Additionally, coconut and palm kernel oils serve as primary sources of fatty acids for mono-diglyceride production. The European Commission's emphasis on circular agriculture further supports the use of side-streams, such as lecithin extracted from spent rapeseed meal or sunflower hulls, which helps reduce waste and lower carbon emissions.

Animal-derived emulsifiers, including egg yolk lecithin and dairy-based mono-diglycerides, maintain a presence in traditional bakery and confectionery applications. Their superior emulsifying properties and flavor enhancement justify their higher costs. However, compliance with the EU Animal By-Products Regulation's traceability requirements adds complexity. Furthermore, avian influenza outbreaks in 2024 disrupted egg-lecithin supply chains. While some premium chocolate manufacturers continue to prefer egg lecithin for its mouthfeel benefits, the industry is gradually shifting toward plant-based alternatives as sensory differences narrow. With the plant-derived emulsifiers segment expected to grow at a 6.84% CAGR, it could capture nearly 68.75% of the market share by 2031, driving significant changes in procurement strategies across the value chain.

By Application: Plant-Based Meat and Dairy Alternatives Surge

In 2025, bakery applications dominated the demand landscape, accounting for 40.88%. Bread, biscuits, cakes, and pastries, the primary consumers, collectively utilized over 400,000 metric tons of emulsifiers across Europe. According to the Office for National Statistics data from 2024, consumer spending on bread and cereals in the United Kingdom was USD 31,000 million. In the industrial bakery realm, mono-diglycerides and DATEM play pivotal roles, enhancing dough machinability and extending shelf life. On the other hand, artisan and in-store bakeries are turning to lecithin, meeting clean-label demands while preserving crumb structure. Following closely, dairy and frozen desserts stand as the second-largest application. Ice cream manufacturers harness mono-diglycerides to manage ice-crystal growth and boost overrun. Simultaneously, yogurt producers utilize lecithin for fruit preparation stabilization. Plant-based meat and dairy alternatives are emerging as the fastest-growing application, boasting an impressive 7.65% CAGR. Emulsifiers play a crucial role in oat milk, almond milk, and pea-protein beverages, preventing phase separation and ensuring a creamy mouthfeel. Sunflower lecithin has become the go-to choice, sidestepping soy allergen issues and championing a non-GMO stance. Meanwhile, plant-based cheese and butter analogs are leveraging mono-diglycerides to mimic the meltability and spreadability of traditional dairy fats. This technical hurdle has ignited collaborative R&D efforts between ingredient suppliers and alternative-protein startups. Mid-single-digit growth is observed in confectionery, beverages, and sauces/dressings/spreads, fueled by trends in premiumization and innovative portion sizes. While meat, poultry, and seafood applications remain niche, they predominantly employ lecithin in processed sausages and restructured products to enhance fat binding.

Geography Analysis

In 2025, the United Kingdom accounted for 25.41% of the European emulsifier market value, supported by its concentrated food-manufacturing base and post-Brexit innovation grants aimed at clean-label reformulation. The presence of major bakery groups and plant-based dairy brands in the UK drives significant demand for emulsifier R&D and technical support. However, as the market matures, growth is shifting towards premium and functional categories, while mainstream bakery and confectionery volumes remain flat. Spain is projected to grow at a 5.82% CAGR through 2031, the highest among the listed geographies. The premiumization of the Mediterranean diet is increasing demand for olive oil-derived emulsifiers, while the recovery of tourism is boosting confectionery and ice cream production. Spanish ingredient suppliers are also investing in enzymatic modification technologies to develop clean-label emulsifiers from local oilseed crops.

Germany, France, and Italy represent mature but stable markets, each with distinct characteristics. Germany's highly automated bakery sector prefers cost-efficient mono-diglycerides and DATEM, while its plant-based food segment is expanding rapidly, driven by flexitarian consumers and private-label innovations from retailers. According to the United States Department of Agriculture data from 2023, 1.5 million people in Germany consumed plant-based foods. In France, the artisan bakery tradition sustains demand for lecithin and specialty emulsifiers that support long-fermentation doughs and organic certifications. Italy's gelato and confectionery industries are increasingly adopting emulsifiers to improve freeze-thaw stability and resist fat bloom, aligning with rising export volumes to North America and Asia. The Netherlands, though smaller in size, plays a significant role in plant-based dairy and sports nutrition, serving as a test market for innovative emulsifier systems. Regulatory harmonization under EFSA allows innovations validated in the Netherlands to scale quickly across the EU, reducing time-to-market for ingredient suppliers.

The Rest of Europe—covering Eastern European markets, Scandinavia, and smaller Western nations—shows diverse growth trends. In Poland and the Czech Republic, industrialization of bakery production is driving the adoption of mono-diglycerides. Meanwhile, Scandinavian countries prioritize organic and non-GMO emulsifiers, even at premium price points. This geographic diversity requires suppliers to maintain varied portfolios and provide localized technical support, favoring multinationals with pan-European operations over regional specialists.

Competitive Landscape

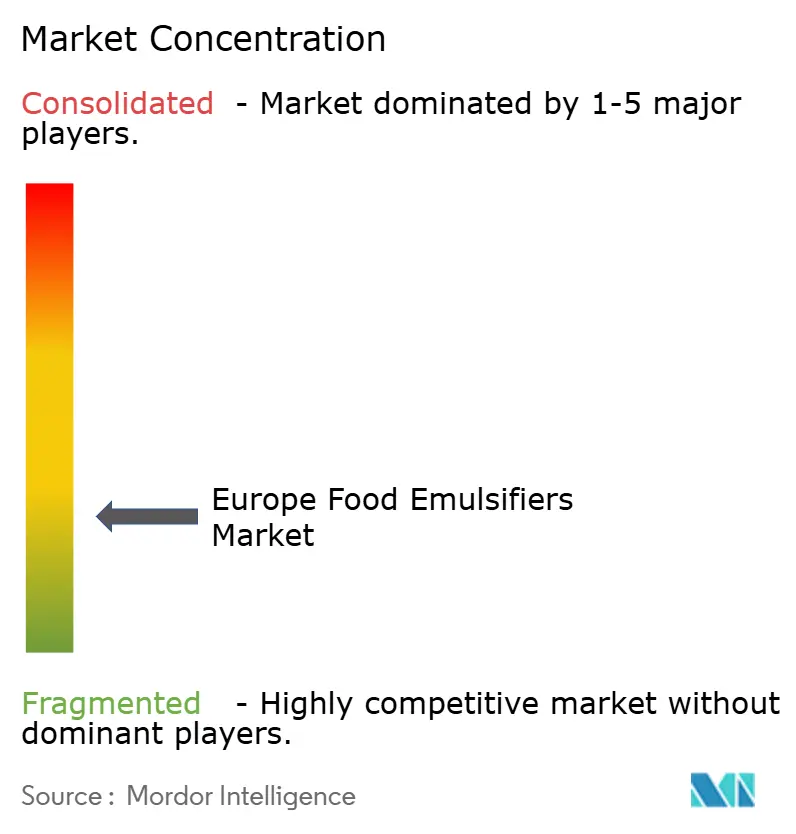

The European food emulsifiers market registers a low concentration, reflecting a fragmented structure where no single player commands a dominant share. Global agri-processors—Cargill, ADM, Bunge—leverage vertical integration from oilseed crushing through emulsifier synthesis, capturing margin across the value chain. Specialty ingredient houses such as Palsgaard, Corbion, and BASF differentiate through application-specific blends and technical co-development services, often partnering with mid-tier bakeries or plant-based startups that lack in-house formulation expertise.

Regional players like Lasenor and LECICO focus on niche applications—confectionery emulsifiers or organic-certified lecithin—where customization and rapid turnaround justify premium pricing. Strategic patterns center on three axes: clean-label portfolio expansion, backward integration into sustainable feedstocks, and digital tools for formulation optimization. Kerry Group's 2024 acquisition of a sunflower-lecithin producer in Ukraine signals a bet on non-GMO supply security, while Ingredion's partnership with a Dutch enzyme supplier aims to commercialize lecithin with enhanced heat stability for plant-based cheese.

White-space opportunities exist in enzymatically modified emulsifiers that deliver functionality at lower usage rates, reducing total ingredient costs—a critical lever for price-sensitive categories like private-label bakery. Smaller contenders are also exploring fermentation-derived emulsifiers, though regulatory approval timelines and scale-up challenges remain barriers. ISO 22000 and FSSC 22000 certifications are table stakes for European food-ingredient suppliers, ensuring traceability and food-safety compliance across complex supply chains.

Europe Food Emulsifiers Industry Leaders

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Ingredion Incorporated

-

International Flavors and Fragrances Inc.

-

Kerry Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2023: Vantage Food launched SIMPLY KAKE emulsifier, a patent-pending alternative to conventional baking aids, formulated to complement food manufacturers’ cleaner label initiatives while attaining taller, lighter, and more evenly baked cakes and sweet goods.

- July 2023: JDM Food Group announced plans to merge with Henry Broch Foods (HBF) to create a new company, Jardin and Broch, which would continue to operate separately in their home markets with innovation in its wet ingredients segment.

Europe Food Emulsifiers Market Report Scope

Food emulsifiers are either synthetic or natural food additives that assist the stabilization and formation of emulsions by reducing surface tension at the oil-water interface.

The European Food Emulsifiers market is segmented by product type into mono-, di-glycerides, and derivatives, lecithin, sorbitan esters, polyglycerol esters, and others. By source, the market is segmented into plant-derived and animal-derived. The market is segmented by application into bakery, dairy, and frozen desserts, confectionery, meat, poultry, and seafood, beverages, sauces, dressings, and spreads, and plant-based meat and dairy alternatives. The market is segmented by geography into Germany, the United Kingdom, Italy, France, Spain, the Netherlands, and the Rest of Europe. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Mono-, Di-glycerides, and Derivatives |

| Lecithin |

| Sorbitan Esters |

| Polyglycerol Esters |

| Others |

By Source

| Plant-derived |

| Animal-derived |

By Application

| Bakery |

| Dairy and Frozen Desserts |

| Confectionery |

| Meat, Poultry and Seafood |

| Beverages |

| Sauces, Dressings and Spreads |

| Plant-based Meat and Dairy Alternatives |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Rest of Europe |

| By Product Type | Mono-, Di-glycerides, and Derivatives |

| Lecithin | |

| Sorbitan Esters | |

| Polyglycerol Esters | |

| Others | |

| By Source | Plant-derived |

| Animal-derived | |

| By Application | Bakery |

| Dairy and Frozen Desserts | |

| Confectionery | |

| Meat, Poultry and Seafood | |

| Beverages | |

| Sauces, Dressings and Spreads | |

| Plant-based Meat and Dairy Alternatives | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the forecast value of the Europe food emulsifiers market by 2031?

The market is projected to reach USD 1.53 billion by 2031, growing at a 4.28% CAGR.

Which segment holds the largest Europe food emulsifiers market share by product type?

Lecithin led with 33.02% revenue share in 2025.

Which application is expanding the fastest for emulsifiers in Europe?

Plant-based meat and dairy alternatives are growing at an 7.65% CAGR through 2031.

Why are plant-derived emulsifiers gaining ground in Europe?

Vegan diets, allergen avoidance, and retailer sustainability mandates are pushing plant origins to 59.58% share in 2025 with a 6.84% CAGR outlook.

Page last updated on: