Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.15 Billion |

| Market Size (2026) | USD 1.25 Billion |

| Market Size (2031) | USD 1.89 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Water Enhancer Market Analysis by Mordor Intelligence

The Europe water enhancer market size was valued at USD 1.15 billion in 2025 and estimated to grow from USD 1.25 billion in 2026 to reach USD 1.89 billion by 2031, at a CAGR of 8.62% during the forecast period (2026-2031). The market landscape is characterized by significant regional variations across European countries, with Western Europe maintaining a dominant market position. Consumer behavior analysis indicates a pronounced shift toward health-conscious beverage choices, particularly among urban populations. The market's fundamental growth drivers include increasing health awareness, demand for sugar-free alternatives, and the convenience factor associated with portable water enhancement solutions. Additionally, the market benefits from technological advancements in flavor development and preservation techniques, enabling manufacturers to offer diverse product portfolios. The competitive environment features both established beverage companies and emerging specialized manufacturers, contributing to product innovation and market expansion through various distribution channels.

Key Report Takeaways

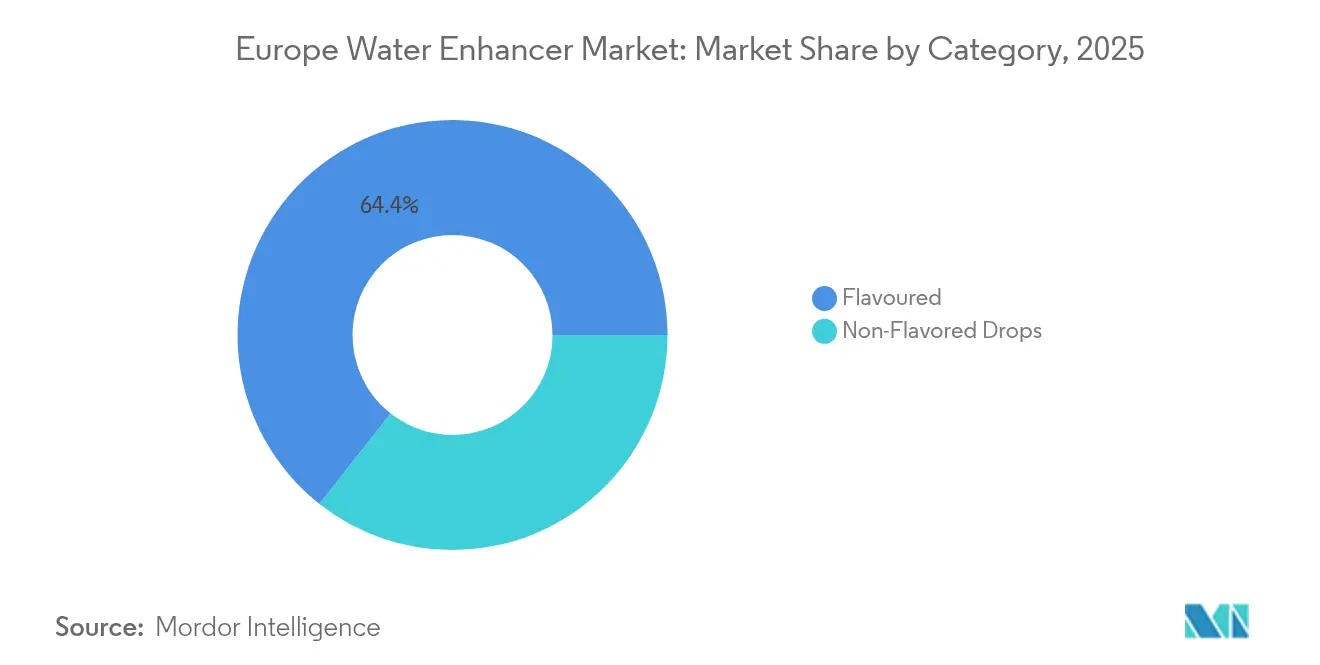

- By category, flavoured led with 64.38% revenue share in 2025; non-flavoured drops are projected to expand at a 10.41% CAGR through 2031.

- By ingredient source, artificial/synthetic ingredients held 59.88% of the European water enhancer market share in 2025, while natural/organic ingredients are set to advance at an 11.05% CAGR.

- By sweetener type, without sugar variants commanded 69.92% share of the European water enhancer market size in 2025; with sugar options are forecast to grow at a 9.34% CAGR.

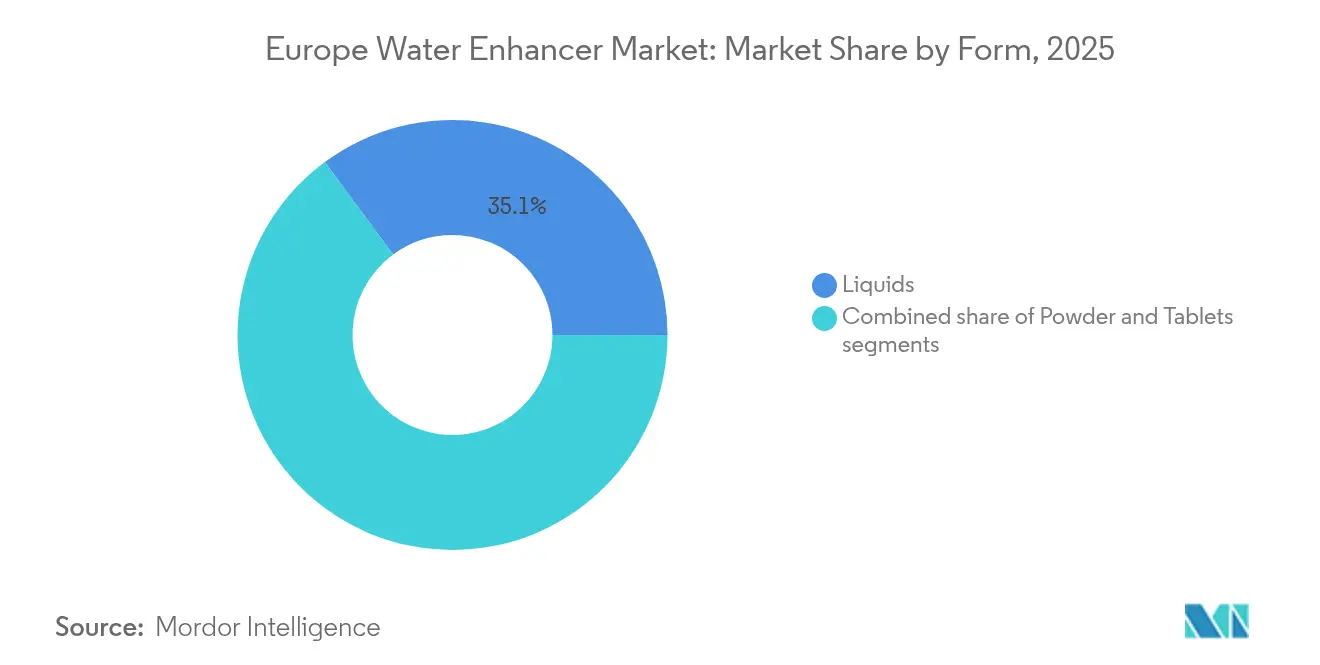

- By form, liquids led with 35.12% revenue share of Europe water enhancer in 2025; tablets are forecasted to grow at a CAGR of 9.92%.

- By distribution channel, supermarkets/hypermarkets accounted for 54.72% of 2025 revenues; online retail stores are forecast to post the fastest 13.41% CAGR.

- By geography, Germany captured 24.86% of the European water enhancer market share in 2025 and is projected to grow at a 10.11% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Water Enhancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness boosts demand for low-calorie and sugar-free beverage alternatives | +2.5% | Germany, the United Kingdom, France, Netherlands, Sweden | Medium term (2-4 years) |

| Increasing preference for convenient, on-the-go hydration solutions supports market growth | +2.1% | Pan-European, with stronger impact in urban centers | Short term (≤ 2 years) |

| Strong marketing and product innovation by major beverage companies drive consumer interest | +1.8% | Germany, the United Kingdom, France, Spain, Italy | Medium term (2-4 years) |

| Partnerships between beverage brands and fitness/wellness influencers enhance market traction | +1.2% | United Kingdom, Germany, Sweden, Netherlands | Short term (≤ 2 years) |

| Expanding retail distribution channels improve product accessibility across europe | +1.7% | Eastern Europe, Spain, Italy | Medium term (2-4 years) |

| Rising popularity of fitness and wellness trends increases use of electrolyte-boosting enhancers | +1.3% | Germany, the United Kingdom, France, Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness Boosts Demand for Low-Calorie and Sugar-Free Beverage Alternatives

The European Water Enhancer Market is undergoing a substantial transformation driven by increasing health-conscious consumption patterns and consumer demand for low and zero-calorie alternatives. The Union of European Beverage Associations' (UNESDA) strategic initiative to reduce added sugars in soft drinks by 10% between 2019 and 2025 has generated significant market opportunities for water enhancers as healthier alternatives to conventional sweetened beverages. Consumer preferences have evolved considerably, moving beyond basic hydration requirements to products delivering comprehensive functional benefits, including essential vitamins, minerals, and electrolytes. In response to this market demand, manufacturers are implementing advanced product development strategies that incorporate specific formulations of magnesium and B vitamins to enhance mental clarity and stress reduction, targeting a diverse consumer base comprising students and professionals seeking sophisticated functional hydration solutions.

Increasing Preference for Convenient, On-The-Go Hydration Solutions Supports Market Growth

Water enhancers are experiencing significant growth across Europe due to their portable and customizable nature. Their compact format strongly appeals to urban professionals and active consumers who seek efficient ways to flavor water without carrying multiple beverage containers. The market expansion is propelled by continuous innovations in packaging, particularly squeeze bottles and single-dose formats that maximize convenience and user experience. Waterdrop, a prominent player in this segment, has successfully expanded its microdrinks presence to over 30 countries, serving more than 2 million customers. The versatility of water enhancers has transformed beverage consumption patterns, extending their usage from homes to workplaces, fitness centers, and travel locations, establishing them as an integral part of modern consumers' daily hydration routines. The growing emphasis on personalized hydration experiences and the increasing adoption of portable beverage solutions continue to drive market momentum across European regions.

Strong Marketing and Product Innovation by Major Beverage Companies Drive Consumer Interest

Major beverage companies are driving growth in the European water enhancer market through strategic marketing initiatives and systematic product innovation. The increasing consumer focus on health and demand for functional, personalized hydration solutions has prompted these companies to utilize their brand strength, distribution networks, and Research and development capabilities. They are developing water enhancers with features like zero sugar, natural ingredients, added vitamins, and electrolytes in convenient formats. These products appeal to diverse consumer groups, including fitness enthusiasts, busy professionals, and families seeking alternatives to sugary beverages. The companies' investments in multi-channel marketing, encompassing digital campaigns, influencer partnerships, and in-store promotions, enhance brand visibility and product adoption across European markets. In the European water enhancer market, Kraft Heinz Company's Mio brand exemplifies this strategic approach through its product portfolio expansion and substantial marketing investments. The company's advertising expenditure of approximately USD 1,031 million in 2024 demonstrates its commitment to strengthening its market presence in Europe.

Rising Popularity of Fitness and Wellness Trends Increases Use Of Electrolyte-Boosting Enhancers

The expanding fitness and wellness trends across the European water enhancer market demonstrate significant growth potential, driven by consumer demand for functional hydration solutions that complement active lifestyles. The increased participation in physical activities such as gym workouts, yoga, cycling, and running has heightened awareness about maintaining proper electrolyte balance to prevent dehydration, fatigue, and muscle cramps. This market development extends beyond athletes to include general consumers focused on their well-being. According to Sport England, gym participation in England increased between November 2023 and November 2024, with 5.9 million people attending gym sessions in 2024 [1]Source: Sport England, "Number of people participating in gym sessions in England", www.sportengland.org . Moreover, the market demand for low-sugar, portable, and vitamin-enriched water enhancer products aligns with consumer requirements for convenient hydration solutions. Europe's aging population further strengthens market growth, as older consumers seek hydration products for improved energy levels and recovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent European Union food and beverage regulations slow product development and approvals | -1.2% | European Union-wide, with particular impact in Germany, France | Medium term (2-4 years) |

| Limited consumer awareness in certain european regions restricts market penetration | -0.9% | Eastern Europe, Southern Europe | Short term (≤ 2 years) |

| High competition from flavoured bottled water and soft drinks limits market share | -0.8% | Pan-European | Medium term (2-4 years) |

| High price points compared to traditional beverages reduce mass appeal | -0.6% | Eastern Europe, Southern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent EU Food and Beverage Regulations Slow Product Development and Approvals.

The European regulatory framework for food additives, particularly EU Regulation EC 1333/2008, requires manufacturers of water enhancers to conduct extensive safety assessments and provide technological justification for ingredients. These regulatory requirements create barriers for smaller market entrants and startups, who often lack the resources to complete complex approval processes. The varying interpretations and implementation of European Union directives across member states create additional compliance challenges, increasing costs and time-to-market for new product formulations. The Austrian Agency for Health and Food Safety mandates that additives must be safe, technologically necessary, and not misleading to consumers, with the European Food Safety Authority (EFSA) conducting regular safety assessments. These regulations have prompted manufacturers to shift toward natural ingredients and clean-label formulations, which typically face reduced regulatory scrutiny but may affect product flavor profiles and shelf stability.

Limited Consumer Awareness in Certain European Regions Restricts Market Penetration

The European water enhancer market faces significant restraints due to limited consumer awareness, particularly pronounced in regions with deeply embedded traditional beverage preferences. This market impediment necessitates substantial capital investment in consumer education programs to communicate product functionality and consumption occasions effectively. The category's complex positioning across multiple beverage segments - soft drinks, functional waters, and nutritional supplements - creates market fragmentation and consumer uncertainty regarding product differentiation. Flavored water consumption patterns indicate distinct demographic barriers, with younger demographics gravitating toward flavor variety and sweetness profiles, while older consumer segments demonstrate preferences for functional attributes with reduced sweetness levels. These divergent consumer preferences necessitate segmented marketing approaches, presenting additional challenges for market penetration, especially in regions where category recognition remains minimal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Flavor Innovation Drives Category Growth

Flavored holds a 64.38% share of the European Water Enhancer Market in 2025, as consumers seek options to enhance plain water while avoiding calories and sugar. The segment's success comes from delivering familiar tastes that meet both flavor preferences and health requirements. Companies such as Kraft Heinz's MiO and Coca-Cola's Dasani Drops have introduced diverse flavor options, ranging from Lemonade, Berry Blast, and Orange Tangerine to refined taste profiles that match European preferences. Advances in flavor technology have improved taste authenticity and longevity in water applications.

Non-Flavored Drops are expected to grow at a CAGR of 10.41% from 2026-2031, driven by demand for functional hydration benefits. This segment provides specific nutritional elements such as electrolytes, vitamins, and minerals, appealing to health-focused consumers and active individuals. The growth reflects consumer interest in beverages with quantifiable functional benefits. Improvements in ingredient technology have enhanced the solubility and stability of functional components in water, allowing better delivery of active ingredients while maintaining product quality.

By Ingredient Source: Natural Formulations Gain Momentum

Despite the rise of natural options, artificial and synthetic ingredients held a 59.88% market share in 2025 due to their advantages in flavor intensity, stability, and cost efficiency. This segment benefits from established supply chains and consistent quality. However, advancements in natural ingredient technology are narrowing the gap with synthetic options. In Germany, sugar alternatives like inulin, carob, and natural syrups are gaining traction, while ingredients such as Palatinose and Fibersol are increasingly used in beverages for their health benefits. These shifts in preferences are creating opportunities for product differentiation through natural formulations that deliver both sensory appeal and wellness benefits.

From 2026 to 2031, the natural and organic ingredients segment in the European water enhancer market is projected to grow at a CAGR of 11.05%, outpacing the overall market. This growth is driven by consumers' focus on ingredient transparency and preference for plant-based components over synthetic ones. The trend aligns with the European food and beverage sector's shift toward clean-label products. Manufacturers are responding by creating water enhancers with botanical extracts, fruit essences, and natural sweeteners for authentic flavors without artificial additives. Data from the German Organic Food Industry Association (BÖLW) shows German consumers spent EUR 16.99 billion on organic products in 2024, highlighting strong demand for natural offerings .

By Sweetener Type: Sugar-Free Options Dominate Market Share

Without sugar variants held a 69.92% share of the European water enhancer market in 2025, reflecting consumer preferences for healthier hydration options. This dominant position stems from increasing demand for zero-calorie alternatives that support weight management and reduced sugar consumption. The segment's growth is supported by improved sweetener technologies that deliver better taste profiles without calories, overcoming previous flavor-related barriers. The European regulatory framework provides clear guidelines for sweeteners, with ingredients like sucralose and acesulfame potassium receiving approval from the European Food Safety Authority, enabling stable product development in the sugar-free segment.

From 2026 to 2031, with sugar options are projected to expand at a CAGR of 9.34%. This surge is fueled by a rising consumer appetite for natural formulations boasting moderate sweetness. There's a discernible shift among consumers favoring products with naturally sourced sugars, distancing themselves from artificial sweeteners. This preference stems from a belief that natural and minimally processed ingredients signify superior quality and enhanced health benefits, even when sugar content is moderate. Manufacturers are increasingly innovating to meet this demand by introducing products with clean-label claims. Additionally, regulatory support for natural sugar alternatives is further propelling market growth.

By Form: Liquid Dominance Faces Tablet Innovation

In 2025, the liquid segment commands a dominant 35.12% share of the European water enhancer market. This leadership stems from consumers' preference for the convenience of ready-to-use formats that deliver immediate flavor. The segment's supremacy is rooted in its operational simplicity and efficient flavor distribution. Leveraging advanced formulation technologies, liquid enhancers guarantee consistent flavor distribution and product stability. Their compact packaging aligns with on-the-go consumption trends. Furthermore, the segment's robust performance is bolstered by streamlined manufacturing processes and a supply chain infrastructure that ensures competitive pricing and widespread retail distribution.

Meanwhile, the tablet segment is on an upward trajectory, forecasting a CAGR of 9.92% from 2026 to 2031. This growth is fueled by innovations catering to consumers' desires for precise dosage and functional benefits. Tablets not only ensure accurate delivery of essential nutrients like vitamins, minerals, and electrolytes but also boast superior portability and stability over their liquid counterparts. This format appeals especially to health-conscious consumers who value measured nutrient intake and minimal packaging. Powder formulations, while holding a smaller market share, primarily cater to institutions and budget-conscious consumers seeking cost-effective hydration solutions.

By Distribution Channel: Digital Commerce Accelerates Growth

Supermarkets and hypermarkets led the market in 2025 with a 54.72% share, leveraging their physical presence and high foot traffic to boost visibility. By placing water enhancers near bottled water and sports drinks, they create natural purchase links. Grocery retailers are adapting to diverse consumer needs, with high-income shoppers favoring health-conscious, premium, and sustainable products, while price sensitivity shapes lower-income choices. This segmentation allows brands to offer products at varied price points. Convenience stores and pharmacies, and health stores are key secondary channels, with pharmacies effectively positioning functional water enhancers alongside wellness products.

Online retail stores are driving the European water enhancer market, projected to grow at a CAGR of 13.41% from 2026 to 2031. This growth is fueled by consumers increasingly purchasing health and wellness products online due to convenience, variety, and personalized experiences. E-commerce enables water enhancer manufacturers to adopt direct-to-consumer (DTC) strategies, bypassing traditional retail intermediaries. Companies leverage platforms like Ocado and Amazon, along with their online stores, using subscription services, promotional bundles, and wellness-focused campaigns. In 2024, 94% of EU citizens aged 16-74 used the internet, and 77% made online purchases, highlighting strong digital infrastructure supporting online sales .

Geography Analysis

Germany dominates the European water enhancers market, holding a 24.86% market share in 2025 and is expected to grow at a CAGR of 10.11% from 2026-2031. The country's market leadership is attributed to its extensive retail infrastructure, high consumer awareness of functional beverages, and focus on health and wellness. German consumers readily embrace innovative beverage solutions that support active lifestyles and health objectives. The Bundesamt für Verbraucherschutz und Lebensmittelsicherheit (Federal Office for Consumer Protection and Food Safety) enforces strict regulatory standards for food additives. While these regulations create market entry challenges, they ensure high product quality standards that enhance consumer confidence.

The United Kingdom represents a key market for water enhancers, supported by robust distribution networks and strong consumer awareness. Major international brands, including Kraft Heinz's MiO and PepsiCo's products, maintain significant market presence. British consumers favor products offering functional benefits such as vitamins, minerals, and performance-enhancing ingredients that complement active lifestyle trends. The market features continuous product innovation, with manufacturers regularly introducing new flavors and functional formulations to sustain consumer interest and market growth.

Southern European countries, including Italy, Spain, and France, offer substantial growth potential for water enhancers, despite current lower market penetration compared to Northern Europe. These markets are developing due to increasing consumer interest in hydration and growing awareness of beverage alternatives. The region's warm climate creates inherent demand for refreshing beverages, while cultural preferences for taste and quality drive consumer expectations for premium water enhancer products.

Competitive Landscape

The European water enhancer market maintains a moderate consolidation, with major multinational beverage corporations, including The Kraft Heinz Company, The Coca-Cola Company, PepsiCo Inc., and Eau Exquise, holding significant market positions through their extensive distribution networks and established brand equity. The market presents substantial opportunities for product development in wellness-oriented hydration solutions, particularly addressing European consumer preferences for stress management, immune system support, and cognitive performance enhancement.

Market dynamics indicate increasing participation from smaller enterprises through strategic product launches and innovations. Manchester Drinks Co. exemplified this trend in March 2023 by introducing Strawberry and Blue Raspberry water enhancers under the Slush Puppie brand, strategically positioning these products to capitalize on the expanding market segment for drink and coffee enhancers. This development demonstrates the market's receptiveness to new entrants who can effectively differentiate their product offerings.

In response to evolving market demands, companies are implementing advanced technological solutions to strengthen their competitive positions. These initiatives encompass digital consumer engagement platforms, algorithmic product recommendations, and subscription-based distribution models. PepsiCo's introduction of Gatorade Hydration Booster represents a strategic product development approach, illustrating how established market participants are adapting their portfolios to address changing consumer preferences and maintain market relevance.

Europe Water Enhancer Industry Leaders

-

The Kraft Heinz Company

-

The Coca-Cola Company

-

PepsiCo Inc.

-

Dyla LLC

-

Eau Exquise

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kraft Heinz introduced MiO Unwind, a functional water enhancer containing magnesium and B vitamins, to address the increasing consumer demand for stress-relief beverages.

- April 2025: Phizz introduced its new product, Phizz Daily Energy, formulated to enhance energy levels and maintain hydration during summer months. The product contains seven electrolytes, a multivitamin blend, and a concentrated B-vitamin complex, along with 75mg of guarana-derived caffeine.

- March 2025: Myprotein launched Impact Hydrate, a new hydration product. The lemon and lime-flavored drink contains 600mg of electrolytes and no added sugar, packaged in a 25-serving tub.

- May 2024: Precision Fuel and Hydration formed a partnership with Ironman Europe, offering Precision Hydration 1000 electrolyte tablets. These tablets contain 1,000mg of sodium per 34 ounces.

Europe Water Enhancer Market Report Scope

A water enhancer is a mixture of functional ingredients, such as vitamins, minerals, and electrolytes, that can be mixed with regular drinking water to enhance its nutritional value.

The European water enhancer market is segmented by distribution channel and geography. By distribution channel, the market is divided into pharmacy/drug stores, convenience stores, hypermarkets/supermarkets, online channels, and other distribution channels. By geography, the market is divided into Spain, the United Kingdom, Germany, France, Italy, Russia, and the Rest of Europe.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Category

| Flavoured |

| Non-Flavored Drops |

By Form

| Powder |

| Tablets |

| Liquids |

By Ingredient Source

| Natural/Organic |

| Artificial/Synthetic |

By Sweetener Type

| With Sugar |

| Without Sugar |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Pharmacy and Health Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Category | Flavoured |

| Non-Flavored Drops | |

| By Form | Powder |

| Tablets | |

| Liquids | |

| By Ingredient Source | Natural/Organic |

| Artificial/Synthetic | |

| By Sweetener Type | With Sugar |

| Without Sugar | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Pharmacy and Health Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the European water enhancer market?

The market is valued at USD 1.25 billion in 2026.

How fast is the market growing?

It is expected to post a 8.62% CAGR, reaching USD 1.89 billion by 2031.

Which country leads consumption?

Germany accounts for 24.86% of 2025 sales and is projected to remain the largest as well as the fastest-growing national market.

What product type holds the biggest share?

Flavour Drops dominate with 64.38% of revenue, driven by taste familiarity and zero-calorie positioning.

Page last updated on: