Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.49 Billion |

| Market Size (2026) | USD 10.75 Billion |

| Market Size (2031) | USD 12.43 Billion |

| Growth Rate (2026 - 2031) | 2.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Carpets and Rugs Market Analysis by Mordor Intelligence

The Europe Carpets and Rugs Market size is projected to expand from USD 10.49 billion in 2025 and USD 10.75 billion in 2026 to USD 12.43 billion by 2031, registering a CAGR of 2.94% between 2026 and 2031. Renovation programs tied to European building-efficiency mandates continue to refresh installed floors in residential and commercial spaces, while hybrid work norms keep demand for sound-absorbing and comfort-oriented textile flooring steady in selective zones. Hospitality upgrades in Mediterranean destinations sustain commercial ordering patterns for custom-woven and modular specifications aligned to brand standards. At the same time, regulatory shifts on PFAS and end-of-life accountability push manufacturers toward recycled fibers, take-back systems, and digital traceability. Input-cost pressure and installer shortages increase project lead times, so producers emphasize modularity, compliant chemistry, and closed-loop designs to defend margin and specification wins. The digital product passport framework, come into force in 2026, is also guiding procurement teams toward verifiable recycled content and material declarations across the European carpet and rugs market[1]European Commission, “Digital Product Passport for Sustainable Products,” European Commission, commission.europa.eu.

Key Report Takeaways

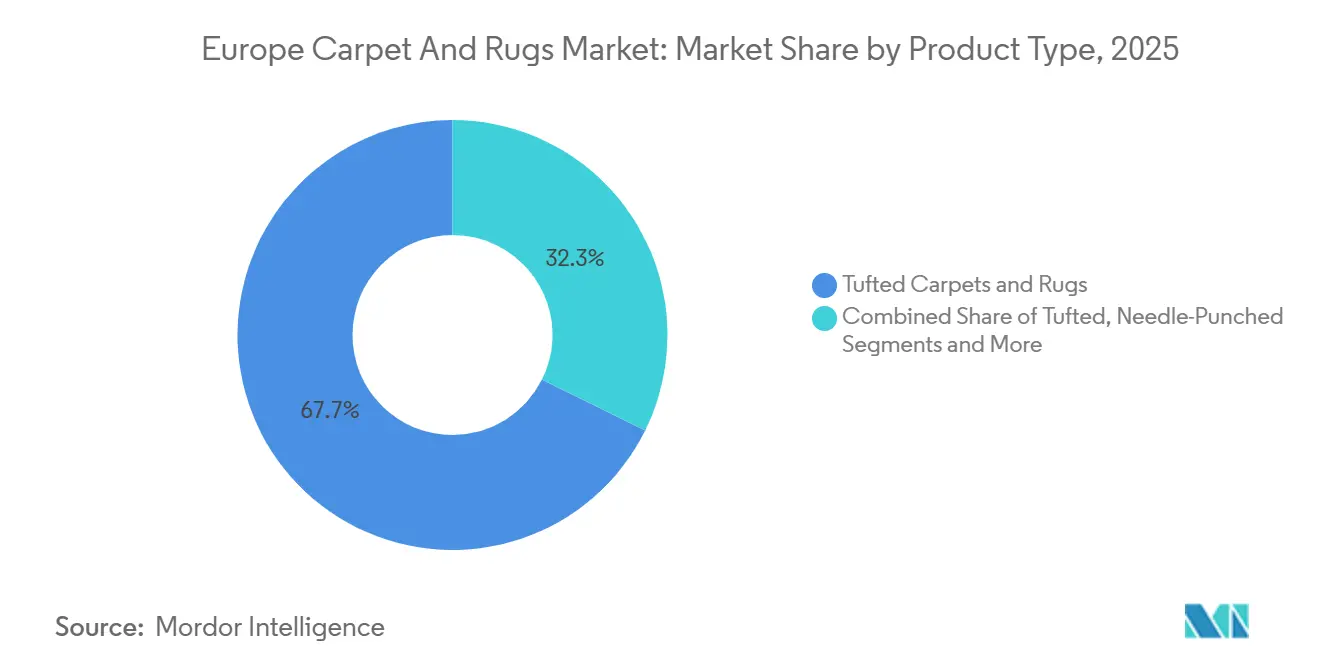

- By product type, tufted carpets led with 67.68% revenue share in 2025 in the Europe Carpets and Rugs Market, while woven is projected to expand at a 3.85% CAGR during 2026–2031.

- By material, polypropylene accounted for 35.45% in 2025 in the Europe Carpets and Rugs Market, and recycled and bio-based fibers are forecast to grow at an 8.41% CAGR through 2031.

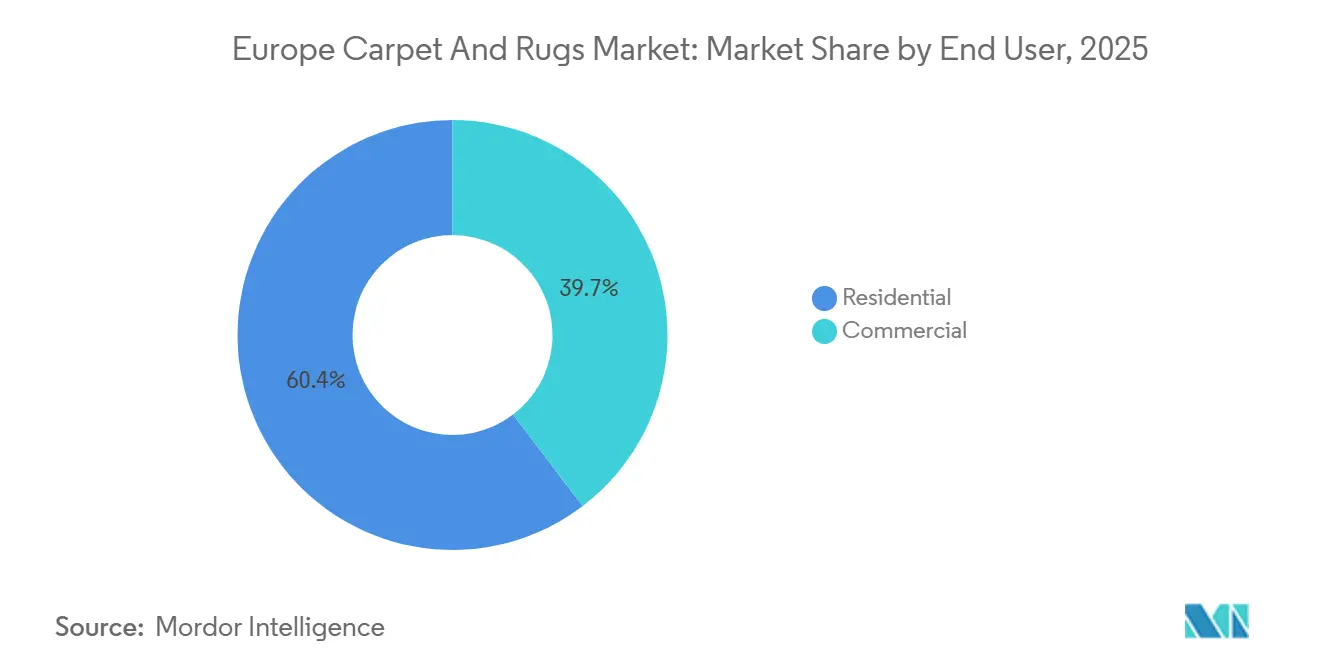

- By end user, residential captured 60.35% in 2025 and is expected to post the fastest growth at a 3.45% CAGR over 2026–2031.

- By distribution channel, B2C retail held 64.87% in 2025 in the Europe Carpets and Rugs Market, while B2B direct is set to advance at a 5.54% CAGR through 2031.

- By geography, Germany accounted for 23.60% in 2025 in the Europe Carpets and Rugs Market, and Spain is projected to register the highest growth at a 6.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Carpets and Rugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation Wave And EPBD-Driven Building Upgrades Accelerate Flooring Replacement Cycles | +1.8% | National, with concentrated impact in Germany, France, Nordics | Medium term (2-4 years) |

| Hospitality Pipeline And Brand Conversions Spur Room And Corridor Re-Carpeting | +1.2% | Mediterranean core in Spain, Italy, Greece, with spill-over to Portugal and Southern France | Short term (≤ 2 years) |

| France's EPR And The European Union's EPR Expansion Catalyze The Recycled And Bio-Based Fibers | +1.1% | France is immediate, the Netherlands and Latvia are active, broader European Union roll-out by 2028 | Medium term (2-4 years) |

| Office Fit-Out And Refit Programs Boost Modular Carpet Tiles | +0.9% | European core, with early gains in Frankfurt, Amsterdam, and London corporate hubs | Medium term (2-4 years) |

| Rising Demand For Certified Low-VOC And Recycled-Content Textile Flooring | +0.7% | National, skewed to Northern Europe, including Germany, the Nordics, and Benelux | Long term (≥ 4 years) |

| PFAS Phase-Outs In Textiles Pivot Demand To PFAS-Free Stain Protection And Wool Or PET | +0.6% | France immediate mover, Denmark early mover, European Union-wide proposal is expected by end-2026 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renovation Wave and EPBD-driven building upgrades accelerate flooring replacement cycles

The European Commission’s Renovation Wave targets an upgrade of 35 million buildings by 2030, which supports a steady cadence of flooring replacement during energy retrofits and deep-renovation projects that bundle insulation, acoustics, and interior surfaces into single scopes. Implementation of the recast Energy Performance of Buildings Directive in Member States brings forward national plans and compliance schedules that catalyze procurement as deadlines approach, lifting orders for modular carpet tiles in residential and public buildings where acoustic performance is required. Rail-station modernization programs in continental Europe favor modular carpet tiles for high-traffic concourses, with vendors highlighting ease of phased installation and targeted replacement that aligns with busy facility schedules[2]Tarkett, “Modular Carpet for Transport and Public Venues,” Tarkett, tarkett.com . The shift toward upgrading the least efficient buildings first increases the likelihood that older wall-to-wall broadlooms are replaced with higher-performing modular and tufted options that contribute to thermal and acoustic targets in rebuilt envelopes. In Germany, access to public-sector renovations requires adherence to external product certifications and VOC testing regimes, which pushes manufacturers to sustain rigorous audits and documentation, strengthening entry barriers in tender-led projects[3]Viacor, “TÜV-PROFiCERT and VOC Requirements,” Viacor, viacor.de .

Hospitality pipeline and brand conversions spur room and corridor re-carpeting

Operators in Mediterranean resort destinations continue to refresh soft finishes as part of brand upgrades, which support custom-woven corridors and modular guestroom tiles that meet acoustic and durability requirements under high occupancy. Conversion-led projects tend to compress timelines compared with new-build development, which concentrates purchasing into shorter windows and elevates order volumes in single quarters as hotels push to reopen on-season. Public and private tenders increasingly weigh eco-criteria, including low emissions and recycled content, suppliers position Ecolabel-qualified tiles and disclose cradle-to-gate carbon footprints to secure inclusion on bidder lists. Premium and upper-upscale properties emphasize cohesive brand identity through colorways and patterning, which maintains demand for woven formats in selected zones while modular tiles support room turnover efficiency and targeted maintenance. This pattern sustains specification opportunities across Spain, Italy, and Greece as tourism infrastructure is upgraded for throughput and design refresh cycles tied to brand standards.

France's EPR and the European Union's EPR expansion catalyze the recycled and bio-based fibers

Extended Producer Responsibility for building-related textiles in France applies eco-modulated fees and collection obligations, which reward designs with recycled content and take-back pathways while penalizing virgin-only formulations through higher contributions. Producers with recycled content above set thresholds gain fee reductions that shift the total-cost-of-ownership calculus in favor of circular products over typical lifespans, encouraging design for disassembly and secondary-market reuse that can satisfy local reuse quotas. Manufacturers have expanded take-back and reuse programs for carpet tiles in markets with active EPR, which supports closed-loop models where backing and yarn re-enter production streams with verified recycled shares. European Union measures to standardize textile EPR and promote circular design criteria across Member States increase the predictability of demand for recycled fibers and transparent end-of-life schemes over the medium term. Initiatives from industry foundations have reinforced the strategic rationale for circular procurement in flooring, strengthening alignment between recyclate investments and regulatory trajectories in France, the Netherlands, and other early adopters.

Office fit-out and refit programs boost modular carpet tiles

Workplace strategies that prioritize acoustics and flexible layouts favor modular tiles over broadloom because tiles enable targeted zoning for meeting rooms and collaboration areas while simplifying reconfiguration as headcounts change. Installer communities and facility teams cite modular formats as faster to lift and relay, reducing disruption to tenants during weekend or overnight changeouts compared with full-roll replacements. Vendors offer collections that target air-quality performance while managing airborne dust and allergens in busy office environments, which supports compliance with low-emitting material policies and wellness targets. Corporate projects seeking green-building ratings select tiles and backings that carry recognized certifications or contribute to acoustic comfort credits, which consolidates demand among suppliers with documented low-VOC and recycled-content options in their catalogs. Workplace and education specifications continue to value sound absorption and visual comfort, and suppliers position product lines that link acoustic claims to productivity and experience outcomes in open-plan spaces.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resilient or Lvt Substitution In Commercial Spaces | -1.4% | Northern Europe in the United Kingdom, Germany, and the Nordics, where the hard-surface share is elevated | Medium term (2-4 years) |

| Petrochemical Feedstock Volatility Inflates Carpet Costs | -1.0% | National exposure with higher sensitivity in Belgium, the Netherlands, and Germany | Short term (≤ 2 years) |

| Compliance Costs From Chemical Restrictions and Ecolabel Criteria | -0.8% | National, with a heavier burden on SMEs and mid-tier manufacturers in France, Germany, and Benelux | Long term (≥ 4 years) |

| Installer Shortages and Reinstatement Obligations Raise Costs and Timelines | -0.6% | Germany, the Netherlands, and the Nordics, with spillover to France and the United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Resilient or LVT substitution in commercial spaces

The shift to hard-surface alternatives in reception, corridor, and clinical areas constrains broadloom volumes as facility managers emphasize cleanability and minimalist design in high-traffic zones. Healthy-building narratives also shape demand, so product categories perceived as easy to sanitize can displace carpet in sensitive applications, while carpet remains relevant in administrative and sound-critical areas. Project specifications often mix surfaces, which reduces total square meters allocated to carpet on a per-project basis, even as modular tiles retain a role in acoustic spaces. In healthcare, infection-control guidance has steered clinical environments away from textile flooring, while administrative zones continue to utilize modular tiles for comfort, sound, and aesthetics. This mixed-material trend is most apparent in Northern European commercial interiors, where open-plan layouts utilize hard surfaces for circulation and textiles for collaboration spaces.

Petrochemical feedstock volatility inflates carpet costs

Cost swings in polypropylene and polyamide value chains challenge pricing stability for mid-market products, especially where producers rely on external resin sourcing. Elevated energy inputs and logistics variability compound feedstock effects, which can compress margins if price pass-through is delayed in contracts. Some integrated players reduce exposure by aligning yarn production with carpet manufacturing, while others hedge and adjust product mixes to maintain competitiveness. European Union mechanisms that add carbon accountability to imports present an additional layer of input-cost sensitivity that companies must manage in procurement planning. The net effect has greater emphasis on modular formats and value-engineered constructions to balance cost-to-performance until input markets stabilize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tufted carpets dominate, woven accelerates in luxury hospitality

Tufted carpets and rugs accounted for 67.68% in 2025, giving the category a clear lead in the Europe Carpets and Rugs Market due to high-speed production and broad design flexibility. Woven formats are smaller in share yet post the fastest growth at a 3.85% CAGR over 2026–2031, supported by premium hospitality specifications that prioritize pattern clarity and durability in corridors and ballrooms. Modular tile penetration continues to rise within tufted volumes as specifiers standardize on 50×50 cm formats for targeted acoustic zones and simplified replacement. Product development focuses on low-emission chemistry and allergen-sensitive features, responding to stricter building and wellness requirements in education and office interiors. The Europe Carpets and Rugs Market benefits from these format dynamics because they align with renovation-led projects that value short lead times and minimized disruption.

Modularization within tufted products also changes how portfolios are merchandised, with suppliers curating visual families that coordinate across open offices, meeting rooms, and circulation paths. Suppliers’ woven offerings hold their ground in upper-upscale properties and high-end residential settings where brand identity needs and luxury positioning remain decisive. Needle-punched solutions fill a performance niche in transportation, public access, and certain industrial settings where toughness and maintenance ease drive specification. Across formats, compliance with low-VOC and PFAS-free requirements has become table stakes in tender-led segments, reinforcing the need for verified chemistry and traceable inputs. These product shifts collectively support stable mix and margin contributions in the Europe Carpets and Rugs Market.

By Material: Polypropylene leads, recycled fibers surge on EPR incentives

Polypropylene commanded 35.45% share in 2025 on moisture resistance and ease of maintenance in healthcare and hospitality zones, anchoring the material’s position across mid-market installations in the Europe Carpets and Rugs Market. Recycled and bio-based fibers are forecast to grow at an 8.41% CAGR through 2031, propelled by EPR fee structures and eco-label incentives that tilt procurement toward circular content. Backing innovations integrate recycled constituents and bio-based tackifiers that reduce embodied carbon while maintaining performance targets for comfort and durability. Regenerated nylon produced from post-consumer streams is now standard in multiple commercial tile collections, aligning with green-building criteria that value documented recycled shares. These developments build resilience into supply chains and position compliant products for preferred access to EPR-governed tenders in France and other early movers.

Nylons remain the performance benchmark in high-traffic settings where resilience and stain resistance anchor lifecycle value propositions, while polyester variants that incorporate recycled bottle content offer compelling options in residential and light-commercial applications. Natural fibers such as wool keep a stable niche in luxury residential and boutique hospitality based on inherent flame resistance and sensory comfort. Suppliers navigating recycled PET supplies compete for consistent flake streams and emphasize material contracts to manage availability risk, while diversifying recycled inputs in backup to sustain circularity goals. As material portfolios shift, European tender frameworks that favor recycled content and PFAS-free formulations continue to steer product design in the Europe Carpets and Rugs Market.

By End User: Residential dominates, commercial accelerates on office refits

Residential applications captured 60.35% of demand in 2025, reflecting occupants’ preference for warmth, sound absorption, and underfoot comfort in bedrooms and living spaces across the Europe Carpets and Rugs Market. Residential is also projected to record the fastest growth at 3.45% CAGR through 2031 as energy-efficiency incentives and renovation programs continue to upgrade building envelopes and interior finishes. Hybrid work arrangements support elevated attention to acoustics and wellness at home, which sustains modular tile adoption in study and workspace zones within residences. Cleaner chemistries and low-VOC claims help drive preference for brands with verifiable product data, especially in homes with children or allergy sensitivities. These dynamics help residential remain a steady anchor of the Europe Carpets and Rugs Market.

Commercial applications span hospitality and leisure, corporate offices, retail, healthcare, and education, with each subsegment responding to different performance needs and procurement frameworks. Corporate offices emphasize modularity, acoustics, and reconfiguration, which keep tile-based specifications resilient even as circulation spaces make room for hard-surface alternatives. Education and certain public buildings place strict weight on reverberation and air-quality standards, elevating modular tiles that couple acoustic control with low-emission certification. In healthcare, procurement often channels textile flooring toward administrative zones due to infection-control protocols, which constraint use in clinical spaces while preserving specialized roles elsewhere. Overall, project-level priorities for comfort, acoustics, and compliance sustain a balanced but selective growth path for commercial volumes in the Europe Carpets and Rugs Market.

By Distribution Channel: B2C retail leads, B2B direct gains on project efficiency

B2C retail accounted for 64.87% of market share in 2025, reflecting the continued importance of physical showrooms for tactile evaluation, color matching, and installation services in the Europe Carpets and Rugs Market. Specialty flooring stores integrate installation quotes at the point of sale and retain local installer networks, which improves conversion and supports higher average order values. Home-improvement chains and furniture retailers cross-sell area rugs as add-ons to larger ticket furniture purchases, while online channels expand through visualization tools and mailed samples that reduce uncertainty for remote buyers. Return rates remain online higher than in-store due to lighting and color variance at home, which challenges pure-play e-commerce models even as digital engagement complements showroom-first journeys[4]CBI, “Consumer Buying Behavior and Online Channels,” CBI, cbi.eu. These multichannel realities keep B2C dominant in aggregate across the European carpet and rugs market.

B2B direct, which accounted for 35.13% market share in 2025, is expected to outpace other channels with a projected 5.54% CAGR through 2031 as commercial buyers streamline tendering and shorten lead times through direct supplier coordination. Direct programs often bundle co-design services and logistics support, which reduces project risk for large room-count refurbishments in hospitality and corporate settings. Manufacturers also have pilot service-based models with take-back and reuse provisions to align with circularity targets and simplify lifecycle management for corporate portfolios. Brand-owned design studios and experience centers blur B2B and B2C by serving both professional specifiers and premium consumers, preserving control over product storytelling and technical documentation. Trade shows, architect libraries, and installer networks continue to influence commercial specifications even when not transacting directly, giving brands multiple touchpoints across the European carpet and rugs market.

Geography Analysis

Germany held 23.60% of the Europe Carpets and Rugs Market share in 2025 on the strength of corporate office refits in Munich, Frankfurt, and Hamburg, and the continued focus on acoustic and wellness objectives in workplace interiors. Public and private renovations tied to efficiency subsidies have historically boosted interior upgrade packages that include flooring refreshes alongside insulation and glazing improvements. Regulations that emphasize indoor environmental quality and sound attenuation have maintained a clear role for modular tiles in open-plan work settings, particularly for meeting rooms and focus areas. Procurement rigor in public-sector projects has reinforced the importance of low-emission chemistry and audited product claims, shaped supplier eligibility, and favored incumbents that maintain multiple certifications. These conditions position Germany as a reliable anchor of the Europe Carpets and Rugs Market.

Spain is projected to post the fastest growth at a 6.23% CAGR through 2031 as hospitality-driven upgrades return to schedule in Mediterranean cities and resort areas. Commercial specifications in Iberia continue to favor custom-woven corridors in upscale properties, while modular tiles accelerate room maintenance and reconfiguration cycles. This mix supports steady ordering for performance-driven nylon and PET constructions with stain and wear treatments aligned to high-occupancy environments. In France, EPR obligations have pushed municipal and educational tenders toward higher recycled-content thresholds, which elevates suppliers that can prove circular inputs and take-back pathways in carpet tiles. Backing systems that combine recycled materials with bio-based constituents extend the appeal of tiles in public procurement, where environmental-cost labels and LCA scores are now part of consumer-facing transparency.

Benelux remains a pivotal production hub and a leader in circular carpet-tile capabilities, supported by established recycling lines and proximity to Northern European demand clusters. Nordic countries prioritize sustainability leadership and indoor-environment quality, which sustains modular tile roles in education and office settings even as broader residential preferences diversify across surfaces. The United Kingdom navigates supply-chain adjustments that affect landed costs and lead times, prompting retailers and project owners to deepen local installer coordination and inventory planning. Italy preserves a strong premium and design orientation across interior finish categories, which supports woven and bespoke offerings in high-end residential and boutique hospitality showrooms. Across the rest of Europe, manufacturing capabilities and craft traditions in neighboring markets continue to supply both commodity and artisanal segments, with regional sourcing used to speed logistics and support rapid renovation schedules in the Europe Carpets and Rugs Market.

Competitive Landscape

Competition remains balanced among several mid-to-large suppliers and a wide tail of regional specialists, with product breadth, compliance, and circularity credentials now central to bids and tender access in the Europe Carpets and Rugs Market. Manufacturers leverage vertical integration and supplier partnerships to mitigate feedstock and energy uncertainty while sustaining service levels across commercial programs. In this environment, leaders differentiate through backing systems with higher recycled content, traceability features embedded in product labels, and take-back networks that enable closed-loop flows of tiles and yarn. Portfolio strategies increasingly pair modular collections for office and hospitality with woven formats for premium spaces, preserving high-value roles for both. These strategic pivots are reinforced by demand for verified low-VOC performance and PFAS-free chemistry options that comply with national and European Union-level restrictions.

Examples of targeted moves highlight this direction. Tarkett updated its circular EcoBase carpet-tile backing to incorporate bio-based pine rosin, lowering fossil-derived content and cutting per-tile carbon footprints while maintaining high recycled content in the system. Victoria PLC relocated woven-rug production from Belgium to Turkey while retaining European design centers, with the transition intended to normalize margins as new capacity stabilizes through 2026. Interface expanded its Scherpenzeel capabilities to scale carpet-tile recycling at the European level, integrating recovered material into new products and supporting carbon-negative backing strategies that align with corporate climate targets. These investments align with regulatory expectations for digital product passports and documentation of recycled content and chemistry disclosures across the European carpet and rugs market.

Specialists continue to command premium segments where heritage, pattern control, and color nuance secure brand-led specifications in hospitality and luxury residential. Needle-felt expertise and PFAS-free performance treatments have become more prominent differentiators as national restrictions expand, strengthening portfolios that deliver stain protection without fluorochemicals. Traceability innovation, including watermarked tiles that carry scannable identifiers, helps facility managers verify materials and align end-of-use take-back with internal sustainability reporting. Across the supplier landscape, European Union Ecolabel participation remains a gateway to public tenders in Scandinavia and Germany, which further concentrates opportunity among companies with complete and well-documented catalogs. The net effect is intensifying differentiation around circular content, declared chemistry, and proven take-back systems in the European carpet and rugs market.

Europe Carpets and Rugs Industry Leaders

Victoria PLC

Condor Group

Tarkett

Interface (EMEA)

Associated Weavers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Victoria PLC completed the relocation of Belgian woven-rugs production to Uşak, Turkey, while retaining European design centers, with the company expecting margin normalization as operations stabilize in 2026.

- December 2024: Condor Group acquired FINDEISEN in Germany, integrating the needle-felt specialist into its portfolio and positioning for PFAS-free performance in high-wear environments.

- September 2025: Tarkett’s Scherpenzeel facility launched a large-scale carpet-tile recycling line in Europe, targeting post-consumer EcoBase-backed tiles and aiming to reach high recovered-material content in new tiles by 2027.

Europe Carpets and Rugs Market Report Scope

Carpets and rugs are floor covering used to improve aesthetics of the house/office spaces and provide comfort and warmth. The yarn typically made from woven fabric such as wool, cotton, silk and jute. Rug is used to cover a specific area of the floor while carpet is used for covering wall-to-wall or are fixed-to-the-floor. A complete background analysis of the European carpet and rug market, which includes an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview, is covered in the report. The report also features a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across key points in the industry's value chain.

The European carpet and rugs market is segmented by type (wall-to-wall tufted carpets, wall-to-wall woven carpets, and rugs), application (residential and commercial), distribution channel (contractors, retail, other distribution channels), and country (Germany, the United Kingdom, France, Spain, and Rest of Europe). The report offers market size and forecasts for the European carpet and rug market in value (USD billion) for all the above segments.

By Product Type

| Tufted |

| Woven |

| Needle-Punched |

| Knotted / Hand-Knotted |

| Others (Flat-weave, Hooked, Braided) |

By Material

| Nylon |

| Polyester (PET & PTT) |

| Polypropylene |

| Wool |

| Other Natural Fibres (Jute, Sisal, Cotton, Silk) |

| Recycled & Bio-based Fibres |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Corporate Offices | |

| Retail | |

| Healthcare & Educational Institutions | |

| Other Commercial Facilities |

By Distribution Channel

| B2B/Direct from the Manufacturers | |

| B2C/Retail | Home-Improvement & DIY Stores |

| Specialty Flooring Stores (includes exclusive brand outlets) | |

| Furniture & Furnishing Stores | |

| Online | |

| Other Distribution Channels |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Product Type | Tufted | |

| Woven | ||

| Needle-Punched | ||

| Knotted / Hand-Knotted | ||

| Others (Flat-weave, Hooked, Braided) | ||

| By Material | Nylon | |

| Polyester (PET & PTT) | ||

| Polypropylene | ||

| Wool | ||

| Other Natural Fibres (Jute, Sisal, Cotton, Silk) | ||

| Recycled & Bio-based Fibres | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Corporate Offices | ||

| Retail | ||

| Healthcare & Educational Institutions | ||

| Other Commercial Facilities | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail | Home-Improvement & DIY Stores | |

| Specialty Flooring Stores (includes exclusive brand outlets) | ||

| Furniture & Furnishing Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe Carpets and Rugs Market?

The Europe Carpets and Rugs Market size is projected at USD 10.75 billion in 2026 and is forecast to reach USD 12.43 billion by 2031 at a 2.94% CAGR, supported by renovation programs and selective commercial upgrades.

Which product types lead to demand across Europe?

Tufted carpets and rugs lead by a wide margin with 67.68% in 2025 due to fast production and flexible design options, while woven formats grow faster in premium hospitality corridors and ballrooms at a 3.85% CAGR to 2031.

Which materials and sustainability features are gaining traction?

Polypropylene leads to 35.45% and recycled and bio-based content grow quickly on EPR incentives and tender criteria, with suppliers expanding circular backings and regenerated nylon to meet eco-label expectations.

What geographies are most important for growth?

Germany remains the anchor with 23.60% in 2025, and Spain is the fastest-growing through 2031 at 6.23% CAGR, driven by hospitality upgrades and modular tile adoption in high-traffic spaces.

How are regulations influencing product choices?

PFAS restrictions and low-VOC requirements are accelerating PFAS-free finishes and verified emissions testing, while EPR frameworks push recycled content and take-back schemes that favor circular carpet tiles.

Page last updated on: