Europe Bottled Water Processing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

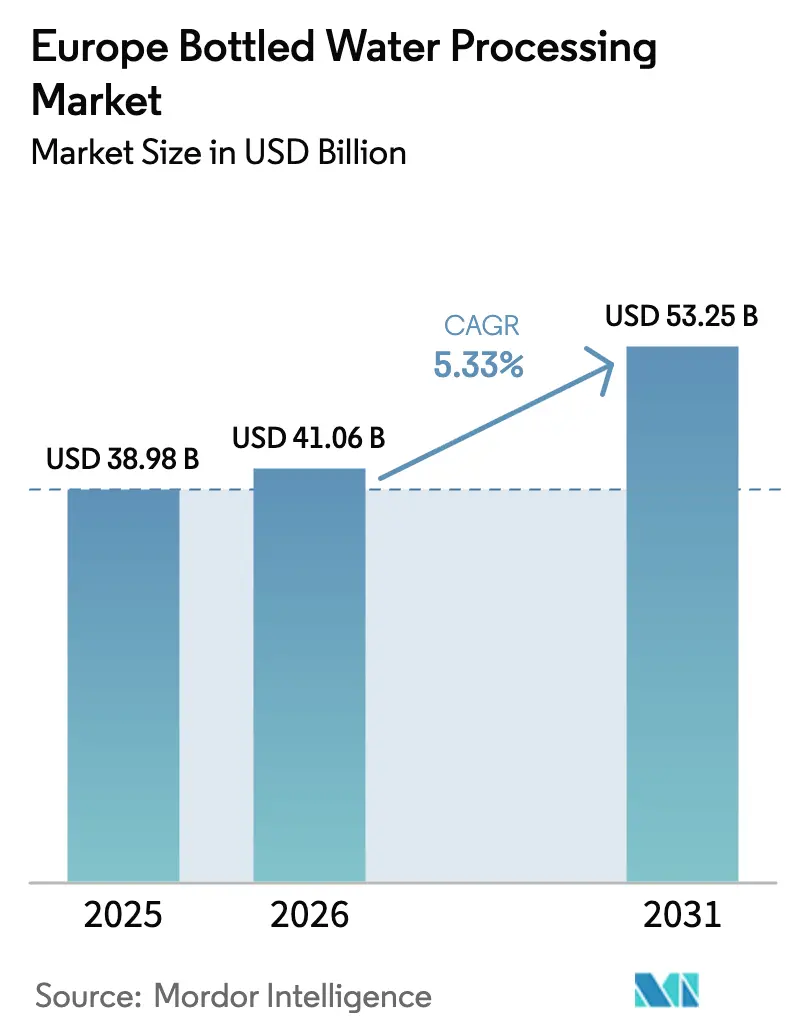

| Base Year Market Size (2025) | USD 38.98 Billion |

| Market Size (2026) | USD 41.06 Billion |

| Market Size (2031) | USD 53.25 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

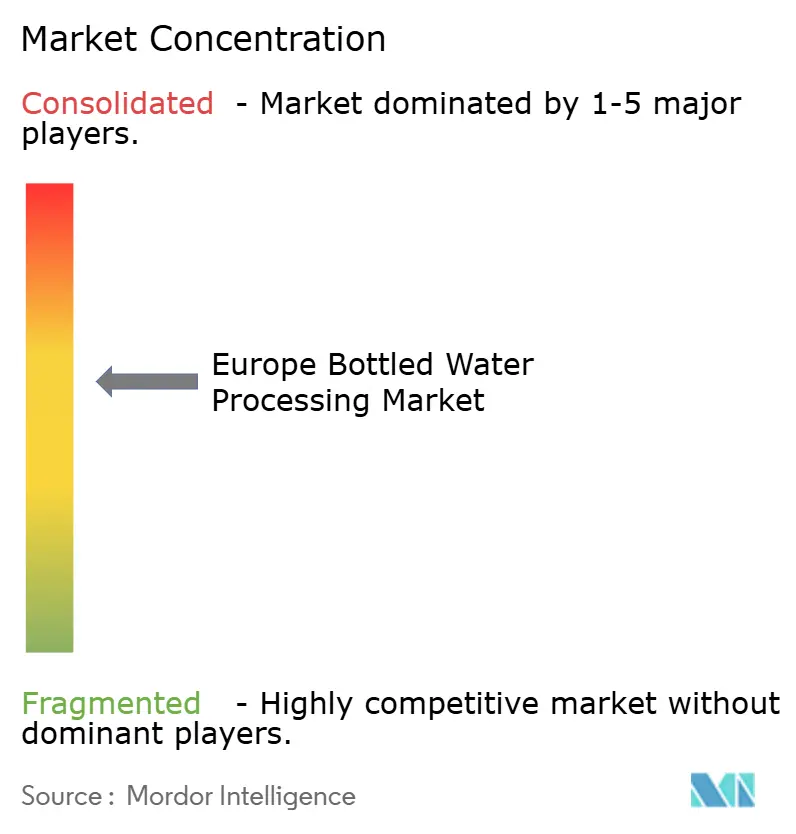

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Bottled Water Processing Market Analysis by Mordor Intelligence

The European bottled water processing market size in 2026 is estimated at USD 41.06 billion, growing from 2025 value of USD 38.98 billion with 2031 projections showing USD 53.25 billion, growing at 5.33% CAGR over 2026-2031. Robust retail demand, sharper EU sustainability mandates, and line-automation investments by scale players shape the current growth runway. Brand owners are tightening control of recycled-content supply chains, discount retailers are expanding private-label shelf space, and equipment makers are bundling predictive-maintenance contracts to lock in clients across the European bottled water processing market. Competitive dynamics favor vertically integrated brands in Germany and France; however, Spain’s tourism-driven volume rebound is spurring the development of greenfield capacity. Line modernization, particularly in areas such as blow molding, inspection, and UV systems, continues to redirect capital toward energy-efficient, rPET-compatible technology.

Key Report Takeaways

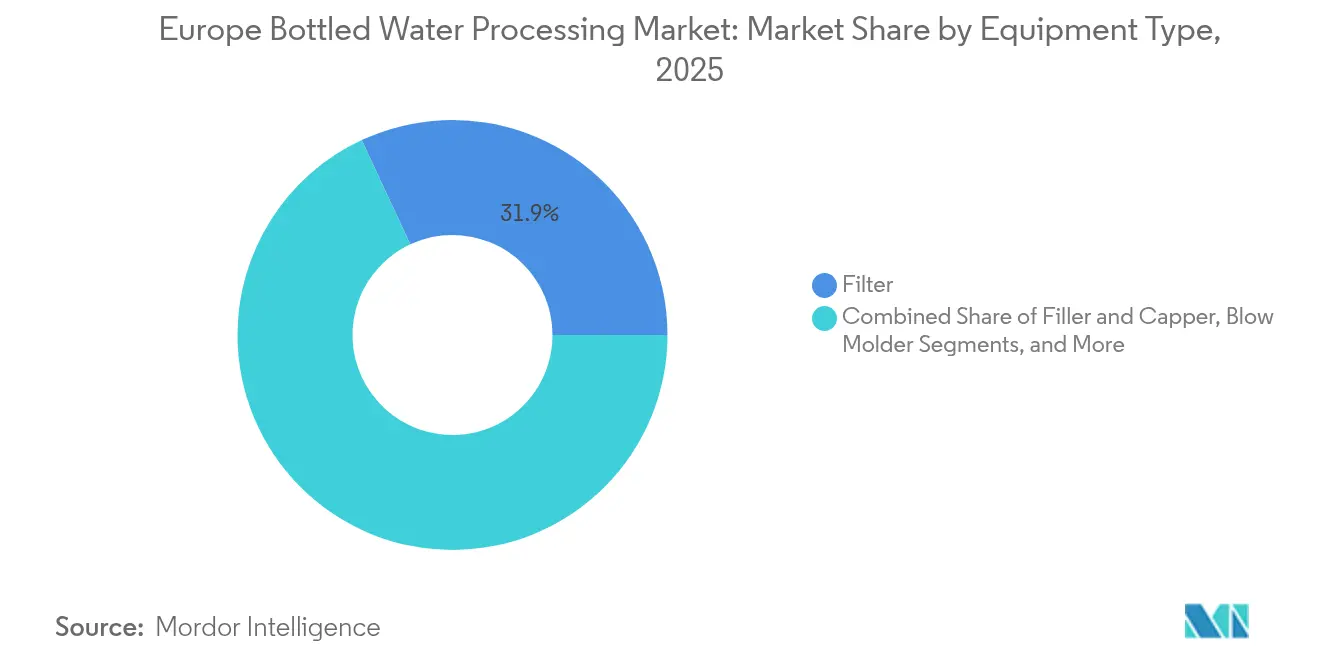

- By equipment type, filters led with 31.94% revenue share in 2025; blow molders are projected to expand at a 6.28% CAGR through 2031.

- By technology, reverse osmosis accounted for a 40.83% share in 2025, while UV disinfection is expected to grow at the fastest rate, with a 7.1% CAGR, from 2026 to 2031.

- By application, still water accounted for 63.43% of the European bottled water processing market size in 2025, and flavored water is expected to advance at a 7.36% CAGR through 2031.

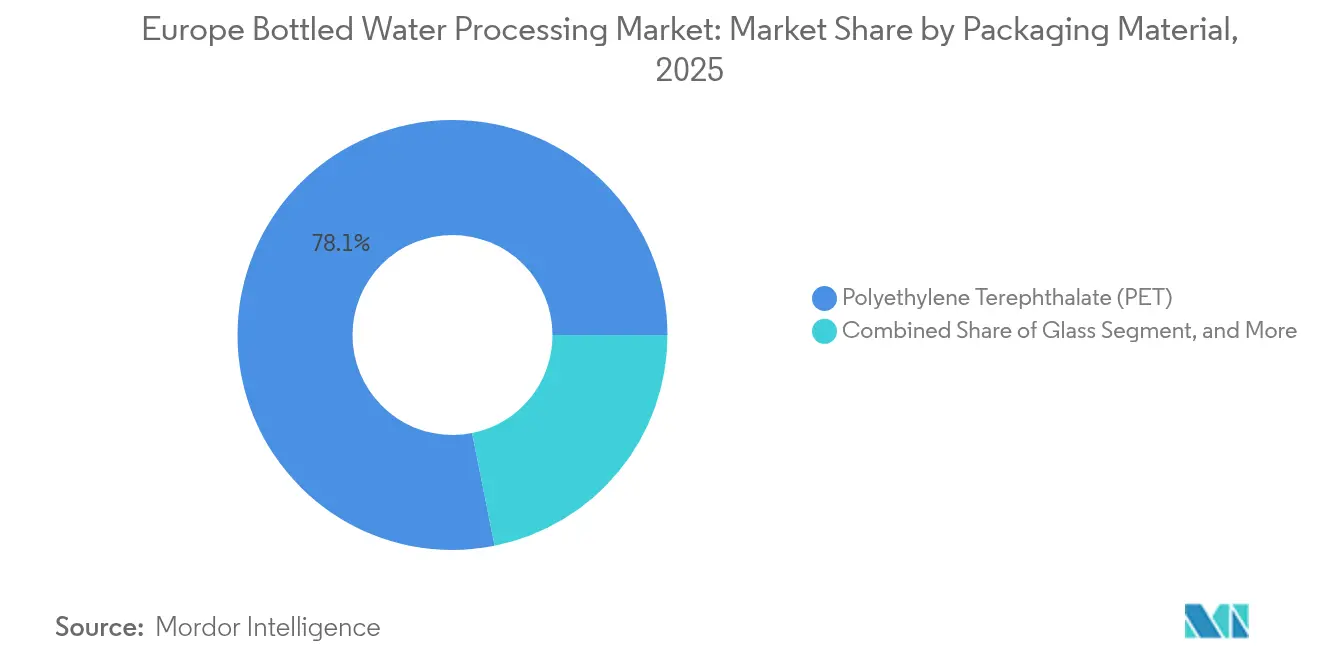

- By packaging material, polyethylene terephthalate dominated with a 78.14% share in 2025 and remains the fastest-growing substrate, with a 6.25% CAGR.

- By end user, integrated brands captured a 52.90% share in 2025; however, contract packagers are projected to record the highest forecast CAGR of 5.95% through 2031.

- By geography, Germany commanded a 38.25% share in 2025, whereas Spain is forecast to post the strongest growth rate of 7.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on bottled water processing market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Bottled Water Processing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health-conscious consumer base | +0.8% | Germany, France, the United Kingdom | Medium term (2-4 years) |

| Heightened stringency of the EU Drinking Water Directive | +1.2% | EU-27, stricter in Germany and France | Short term (≤ 2 years) |

| Growing Private Label penetration in discount retail | +1.0% | Netherlands, Spain, France | Medium term (2-4 years) |

| Rapid proliferation of on-the-go pack sizes | +0.7% | Urban centers across Germany, France, Spain, United Kingdom | Short term (≤ 2 years) |

| Shift toward rPET content mandates | +1.3% | EU-27, early compliance in Germany, France, the Netherlands | Long term (≥ 4 years) |

| Accelerated adoption of AI-enabled inline quality control | +0.5% | Germany, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Stringency of EU Drinking Water Directive

The revised directive tightens PFAS thresholds to 0.10 µg/L from January 2026, prompting bottlers to retrofit their ultrafiltration and activated-carbon stages, which increases greenfield line costs by 15-20%. Early enforcement in Germany favors vertically integrated brands that own protected spring sources over contract packagers reliant on municipal feedwater. Capital-expenditure pressure is therefore tilting the European bottled water processing market toward players capable of absorbing compliance spend. Material-contact clauses within the directive also accelerate the transition from legacy PVC tubing to stainless steel and FDA-grade polymers, thereby extending equipment replacement cycles.

Shift Toward rPET Content Mandates

The Packaging and Packaging Waste Regulation requires 30% recycled PET by 2030 and 65% by 2040, backed by extended producer responsibility fees that penalize virgin resin usage. Spot rPET shortages already push prices to parity with virgin resin, motivating Coca-Cola Europacific Partners to invest EUR 250 million (USD 275 million) in a Netherlands recycling facility that is set to come online in 2027. Secure rPET offtake is becoming a strategic differentiator across the European bottled water processing market, altering long-term supply contracts and favoring brands with closed-loop agreements.

Growing Private-Label Penetration in Discount Retail

Private-label bottled water achieved a 47% share in the Netherlands in 2024 and continues to rise as Aldi and Lidl deepen their partnerships with contract packagers.[1]Retail Detail, “Private Label Continues to Gain Ground in Europe,” retaildetail.eu. Retailer demand for agile molds, short lead-times, and rPET-verified packaging intensifies competition among co-packers, compressing margins for mid-tier branded bottlers. Spain and France follow the pattern, with Mercadona and Carrefour citing rPET milestones and on-shelf price gaps of 30-40% compared to national brands, which amplifies volume shifts in the European bottled water processing market.

Accelerated Adoption of AI-Enabled Inline Quality Control

AI vision systems, such as Krones Linatronic, reduce false rejects by 40% at 72,000 bph line rates, eliminating EUR 180,000 in annual waste for a typical still-water facility.[2]Krones AG, “Filling Technology and Inspection Systems,” krones.com. Predictive maintenance tie-ins from Tetra Pak’s Connected Packaging further curb unplanned downtime, widening the efficiency gap between AI-equipped factories and legacy plants. As insurers begin offering premium discounts for real-time monitoring, adoption is expected to accelerate among premium flavoured and functional water bottlers throughout the European bottled water processing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile virgin PET resin prices | -0.9% | EU-27, acute in Italy and Spain | Short term (≤ 2 years) |

| Rising municipal tap-water campaigns | -0.6% | Germany, France, United Kingdom urban centers | Medium term (2-4 years) |

| High CAPEX for aseptic filling lines | -0.7% | Premium-segment entrants across the EU-27 | Long term (≥ 4 years) |

| Scarcity of qualified maintenance personnel | -0.4% | Germany, France, and Italy's industrial belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Virgin PET Resin Prices

European virgin PET traded between EUR 1,100 and EUR 1,500 per ton in 2024, with 25% intra-year swings tied to energy and feedstock shocks. Still-water bottlers with quarterly retailer contracts have limited pass-through flexibility, so margin compression frequently erodes operating leverage. Italian mineral-water players experienced sharp Q3 2024 hits when Brent crude oil reached USD 95 per barrel, underscoring the raw-material exposure in the European bottled water processing market.[3]German Federal Ministry for the Environment, “Deposit Return System Performance Data,” bmu.de.

High CAPEX for Aseptic Filling Lines

Aseptic systems cost EUR 5 million - EUR 8 million (USD 5.5 million - USD 8.8 million) per line, including sterile air, peroxide sterilization, and ISO-class cleanrooms, keeping functional water production largely in the hands of deep-capital incumbents, such as Tetra Pak.[4]Tetra Pak, “Aseptic Processing Technology,” tetrapak.com. Contract packagers seeking to supply premium private-label SKUs encounter minimum-order and payback hurdles that hinder entry, limiting downstream innovation and hindering segment diversification in certain parts of the European bottled water processing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Blow Molders Gain as Lightweighting Meets rPET Compliance

Filters held the largest 31.94% share in the European bottled water processing market in 2025, reflecting the universal demand for particulate and microbial control. Both reverse-osmosis and ultrafiltration modules sustain recurring replacement revenue for suppliers, with membrane life cycles of 18-24 months ensuring stable aftermarket sales. Lightweighting pressures and retailer sustainability targets are, however, driving the acceleration of blow-molded installations. The Sidel Matrix platform reduces preform weight by 12% while maintaining 10 N top-load strength, resulting in material savings of approximately EUR 0.008 per bottle and a fast two-to-three-year payback. Integrated majors often couple blow-molders with high-speed fillers to optimize line balance, whereas contract packagers seek standalone modular units for multi-SKU runs.

The blow-molded CAGR of 6.28% through 2031 surpasses filters as brands pursue in-house preform-to-bottle control, a critical requirement for managing 30%–50% rPET blends. Fillers and capers remain essential, yet their growth tracks overall line buildouts rather than outpacing niche equipment. Bottle washers retain a limited share, mostly inside German glass-returnable operations. Secondary equipment, such as labelers, palletizers, and conveyors, adheres to price-competitive procurement, opening the door for Asian vendors in Southern and Eastern Europe. Technology suppliers respond with end-to-end service bundles, promising up-time guarantees that ease staffing gaps across the European bottled water processing market.

By Technology: UV Disinfection Gains on Energy Economics and Taste Neutrality

Reverse osmosis accounted for a 40.83% share in 2025, driven by its ability to remove dissolved solids and PFAS below detection limits. Energy draw, at 0.4–0.6 kWh per m³, and 20%–30% reject water, nevertheless drives operating cost debates. UV disinfection, which is expanding at a 7.1% CAGR, uses 70% less electricity than ozone and avoids the residual chlorine taste, appealing to premium still and flavored SKUs seeking clean-label cues. Pentair’s Sanitron units, with a throughput of 150 m³ per hour, deliver a 4-log Cryptosporidium reduction without forming disinfection byproducts, aligning with the European bottled water processing market's pivot toward taste integrity.

Support microfiltration, ultrafiltration, and chlorination, maintain midpoint shares, competing on plant-specific water chemistry and regulatory context. Ozone retains a role in sparkling-water lines for concurrent carbon dioxide scavenging, yet its share declines as UV systems integrate with AI-based quality monitoring. As energy tariffs climb and EU carbon-pricing deepens, ROI on UV retrofits strengthens, particularly in Spain and Italy, where kilowatt-hour costs outpace the EU average.

By Application: Flavored Water Rides Health-and-Wellness Tailwinds

Stillwater secured a 63.43% share of the European bottled water processing market in 2025, primarily through premiumization into larger pack sizes and mineral-rich variants. Volume adds trail value growth, signaling market maturity. Flavoured water, expanding at 7.36% CAGR, entices cola-leavers seeking low sugar and natural essences. Brands such as Vittel Infusions and Volvic Juicy employ aseptic filling to preserve delicate aromatics and use inline blending systems that maintain ±2% flavor dosing accuracy. Sparkling water, although smaller in scale, is gaining traction in export-oriented German mineral brands as consumers in Benelux and the United Kingdom trade up from cola.

Processing complexity scales with flavor diversification. Aseptic lines that combine high-shear blending, inline deaeration, and low-oxygen closures become standard for functional SKUs. Retail planograms reflect this migration, dedicating more shelf frontage to zero-calorie infused waters and electrolyte-enhanced sparkling lines. Contract packagers with the requisite aseptic infrastructure capture incremental private-label business, reinforcing the segmentation-led expansion of the European bottled water processing market.

By Packaging Material: PET Dominance Persists Despite Sustainability Headwinds

Polyethylene terephthalate commanded 78.14% of the packaging material share in 2025 within the European bottled water processing market and is projected to expand at a 6.25% CAGR through 2031, making it the fastest-growing substrate. This level gives PET the highest European bottled water processing market share by a wide margin. Its ascendancy rests on light weight, impact resistance, shelf appeal, and an extensive deposit-return network that keeps recycling rates high. Coca-Cola Europacific Partners highlighted these advantages in 2024 by introducing a 100% rPET still-water bottle that weighs 23 g, a 17% reduction from the 28 g of a virgin-PET equivalent, resulting in an 8% decrease in pallet transport emissions. Regulatory demands for 30% recycled content by 2030, rising on-the-go consumption of single-serve drinks, and advances in blow molding that trim wall thickness to 0.28 mm without sacrificing top-load strength keep PET on a strong growth path. Germany’s deposit-return system, which collected 93% of PET bottles in 2024, assures bottlers of steady rPET feedstock even when virgin resin prices swing.

By End User: Contract Packagers Gain as Brands Pursue Asset-Light Models

Integrated brands captured a 52.90% share in 2025 by controlling source, processing, and distribution economics within the European bottled water processing market. Yet their CAGR lags segment averages because capital is shifting toward marketing and route-to-market. Nestlé Waters outsourced an additional 80 million L to Niagara in 2025, signaling a pivot to asset-light tactics. Contract packagers, led by Refresco, are advancing 5.95% CAGR on the back of private-label demand and seasonal flex requirements. Scale allows them to absorb rPET surcharge risk and amortize aseptic lines across multiple SKUs.

Retail consolidation amplifies this model: the top five EU grocers now hold 38% of bottled-water volume, negotiating private-label exclusives that only large co-packers can supply. Smaller bottlers, caught between rPET compliance costs and price-led tenders, confront margin erosion. Investment, therefore, shifts to flexible lines capable of rapid mold and flavor changeovers, reinforcing the bifurcation trend across the European bottled water processing market.

Geography Analysis

Germany held a 38.25% share in 2025, underpinned by 530 registered mineral sources and a consumer preference for carbonated formats, which were priced 25-35% higher than still formats. Deposit-return systems capturing 93% PET collection supply rPET feedstock, prompting EUR 198 million in recycling investments since 2022. Domestic competition remains fragmented, with more than 200 bottlers defending regional proof of claims that resonate in the European bottled water processing market. High-line speeds and strict quality audits are pushing German plants toward AI-enabled inspection and blow-mold integration to maintain cost competitiveness.

Spain is projected to post the fastest growth rate of 7.95% through 2031. The tourism resurgence in coastal regions led to an 18% increase in bottled-water consumption in 2024, while export demand to North Africa and the Middle East gained momentum with the rise of halal certifications. Twelve new lines came online in 2024, mainly in Catalonia and Valencia, totaling EUR 104.5 million in investment. Spain’s 30% rPET mandate by 2027, three years ahead of EU targets, accelerates closed-loop initiatives, reinforcing local recycling ecosystems feeding the European bottled water processing market.

France, Italy, and the United Kingdom collectively account for 34.65% of the value. France excels in premium mineral exports; Italy dominates HORECA channels through regional brands; the United Kingdom faces headwinds from the installation of 1,800 public refill stations by 2024, which dampens single-serve PET growth. Yet private-label share in UK retailers tops 52%, steering co-packer capital toward lightweight PET alternatives for impulse channels.

Mordor Intelligence provides coverage of the bottled water processing market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The European bottled water processing market is characterized by moderate concentration, with the top five equipment suppliers, Krones, Sidel, GEA, Tetra Pak, and Alfa Laval, capturing roughly 62% of the 2024 installations. However, the top ten bottlers held only 48% of the retail value. Equipment firms differentiate through digital twins, financing, and predictive service contracts. Krones’ 2024 digital twin launch claims a 12% total cost-of-ownership reduction, deepening lock-in throughout the equipment's life cycle. Tetra Pak’s A3/Speed filler, unveiled in June 2025, reduces peroxide sterilization time to 4.2 seconds, lowering entry barriers for mid-tier flavoured-water launches.

Three archetypes shape bottler strategies. Integrated majors such as Danone and Nestlé invest in sustainability storytelling and premium SKUs. Regional specialists, such as Gerolsteiner, defend their home markets with mineral provenance and HORECA relationships. Contract packagers, exemplified by Refresco, scale across borders and retailer-specific programs. Horizontal consolidation inches forward: Alfa Laval’s 2024 membrane-filtration acquisition deepens turnkey capabilities, and Refresco’s 2025 Spanish plant buy bolsters Mediterranean reach.

Europe Bottled Water Processing Industry Leaders

Dow Chemical Co

Pall Corporation

Liquid Packaging Solutions Inc

Velocity Equipment Solutions Inc

Norland International Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Krones has enhanced its AI-driven inspectors, achieving a reliability rate exceeding 99.9%. Breweries have noted that this AI inspection software has significantly reduced bottle bursts at the filler, leading to improved stability in their production lines.

- June 2025: Tetra Pak launched the A3/Speed aseptic filler at 36,000 bph, with eleven early orders across Italy and Spain

- March 2025: Pentair released the UV Sanitron Pro system, confirming six European installs and 70% lower energy use than ozone.

- January 2025: Alfa Laval purchased a German membrane specialist, adding ultrafiltration depth to water-treatment offerings.

Europe Bottled Water Processing Market Report Scope

The Europe Bottled Water Processing Market refers to the industry involved in the treatment and packaging of bottled water, utilizing various equipment, technologies, and materials to ensure safety, quality, and compliance with regulatory standards. This market caters to diverse applications, including still, sparkling, and flavored water, and serves different end users such as integrated bottled water brands, contract packagers, and private label producers.

The Europe Bottled Water Processing Market Report is Segmented by Equipment Type (Filter, Filler and Capper, Blow Molder, Bottle Washer, Other Equipment Types), Technology (Reverse Osmosis, Microfiltration, Ultrafiltration, Chlorination, UV Disinfection, Other Technologies), Application (Still Water, Sparkling Water, Flavoured Water), Packaging Material (PET, Glass, High-Density Polyethylene, and Other Packaging Materials), End User (Integrated Bottled Water Brands, Contract Packagers, Private Label Producers), and Geography (United Kingdom, Germany, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Filter |

| Filler and Capper |

| Blow Molder |

| Bottle Washer |

| Other Equipment Types |

| Reverse Osmosis |

| Microfiltration |

| Ultrafiltration |

| Chlorination |

| UV Disinfection |

| Other Technologies |

| Still Water |

| Sparkling Water |

| Flavoured Water |

| Polyethylene Terephthalate (PET) |

| Glass |

| High-Density Polyethylene (HDPE) |

| Other Packaging Materials |

| Integrated Bottled Water Brands |

| Contract Packagers |

| Private Label Producers |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Equipment Type | Filter |

| Filler and Capper | |

| Blow Molder | |

| Bottle Washer | |

| Other Equipment Types | |

| By Technology | Reverse Osmosis |

| Microfiltration | |

| Ultrafiltration | |

| Chlorination | |

| UV Disinfection | |

| Other Technologies | |

| By Application | Still Water |

| Sparkling Water | |

| Flavoured Water | |

| By Packaging Material | Polyethylene Terephthalate (PET) |

| Glass | |

| High-Density Polyethylene (HDPE) | |

| Other Packaging Materials | |

| By End User | Integrated Bottled Water Brands |

| Contract Packagers | |

| Private Label Producers | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe bottled water processing market?

It is valued at USD 41.06 billion in 2026 with a 5.33% CAGR forecast to 2031.

Which equipment segment is expanding fastest?

Blow molders, advancing at a 6.28% CAGR as brands pursue lightweighting and rPET integration.

Why is UV disinfection gaining traction?

UV systems cut energy use by 70% versus ozone and avoid residual chlorine taste, supporting premium still and flavoured waters.

Which country leads regional market share?

Germany dominates with 38.25% share, supported by its extensive mineral-water tradition and recycling infrastructure.

How are private-label dynamics influencing processors?

Retailers in Spain, the Netherlands, and France raise private-label volumes, pushing contract packagers to invest in flexible, rPET-ready lines.

What limits entry into functional bottled water?

Aseptic filling lines cost EUR 5 million – EUR 8 million, a capital hurdle deterring smaller bottlers.

Page last updated on: