Bottled Water Processing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

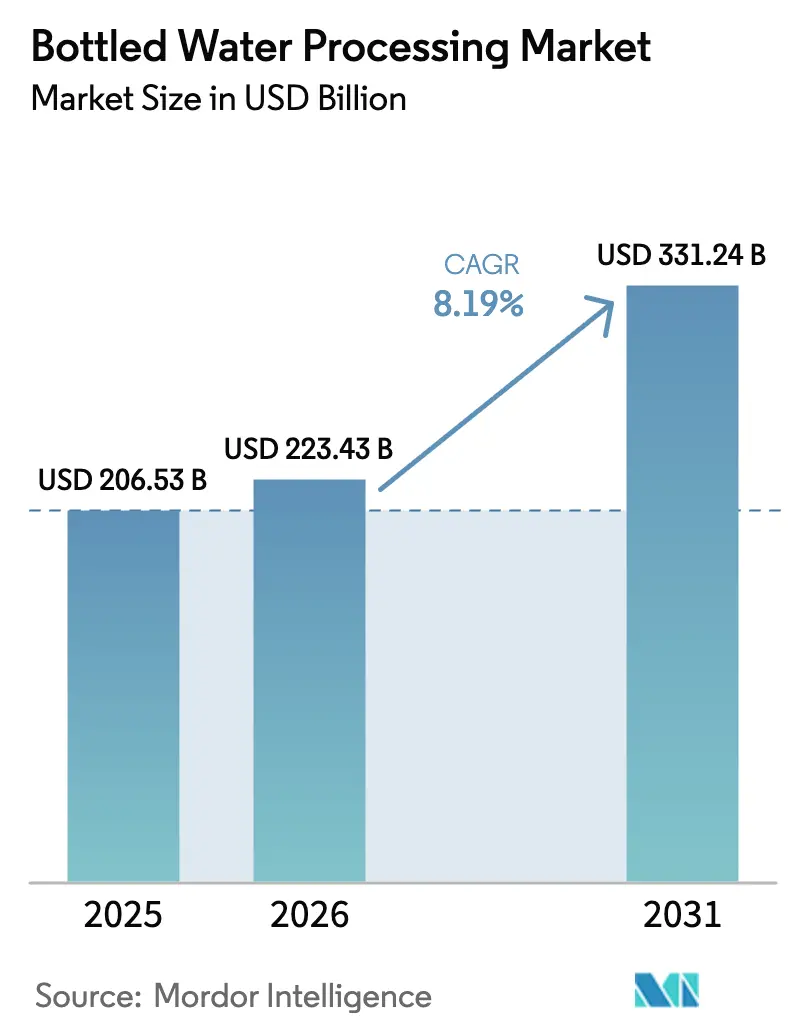

| Market Size (2026) | USD 223.43 Billion |

| Market Size (2031) | USD 331.24 Billion |

| Growth Rate (2026 - 2031) | 8.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bottled Water Processing Market Analysis by Mordor Intelligence

The bottled water processing market size was valued at USD 206.53 billion in 2025 and estimated to grow from USD 223.43 billion in 2026 to reach USD 331.24 billion by 2031, at a CAGR of 8.19% during the forecast period (2026-2031). Rapid urbanization, rising health awareness, and stricter potable-water regulations in both developed and developing regions underpin this expansion. Growing demand for AI-enabled real-time quality monitoring, wider use of mobile and modular bottling lines, and steady investments in energy-efficient membrane technologies further stimulate capital spending on new equipment. Companies continue to streamline operations through industry-4.0 integration, while sustainability mandates accelerate the shift toward recycled PET and emerging bioplastics. Asia–Pacific’s expanding middle class creates the largest volume upside, whereas North America and Europe drive premiumisation and compliance-driven upgrades.

Key Report Takeaways

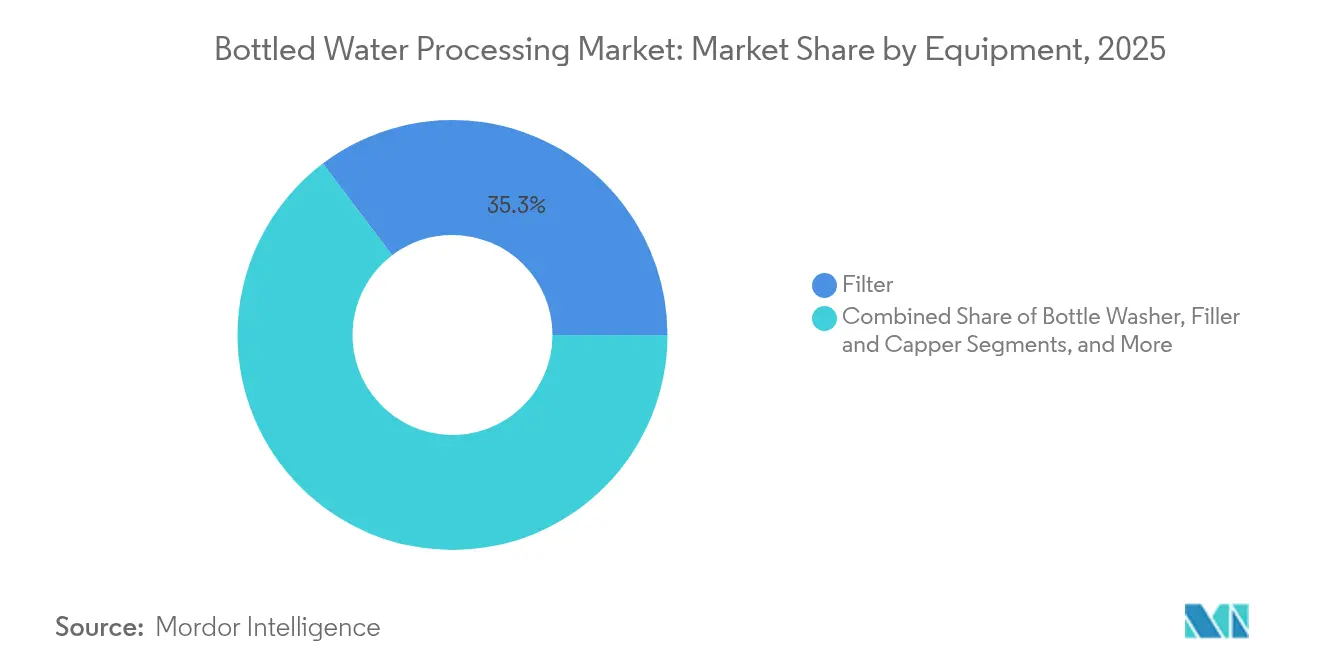

- By equipment, filters led with 35.31% revenue in 2025; shrink wrappers post the quickest 12.63% CAGR through 2031.

- By technology, reverse osmosis held 27.95% of the bottled water processing market share in 2025; microfiltration is projected to grow at 11.86% CAGR to 2031.

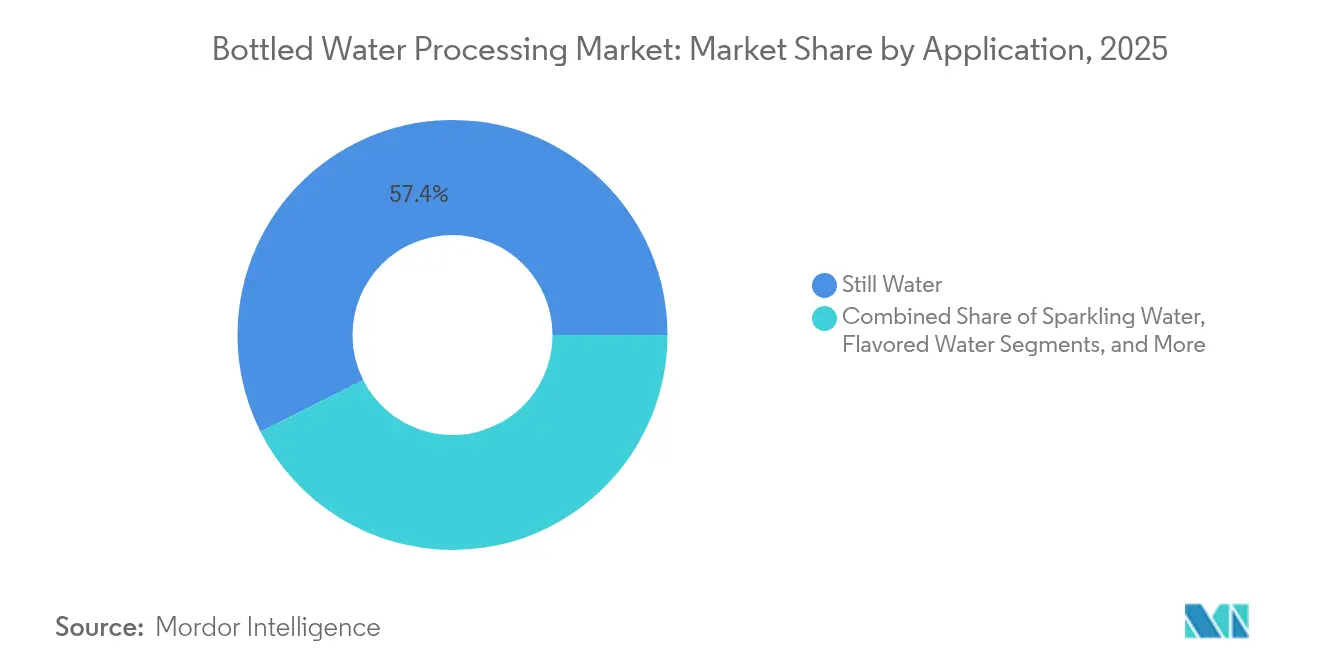

- By application, still water accounted for 57.42% share of the bottled water processing market size in 2025, whereas functional water advances at an 11.59% CAGR to 2031.

- By packaging material, PET dominated with 71.68% share in 2025; bioplastics adoption rises at 11.92% CAGR to 2031.

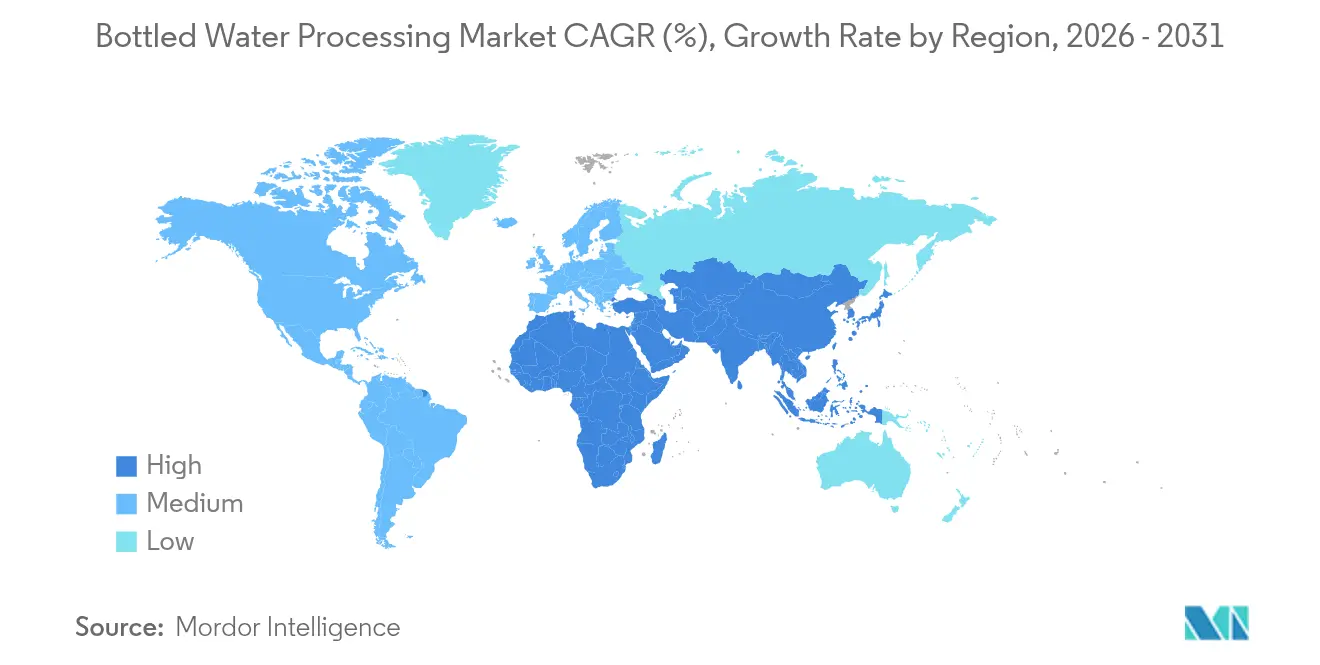

- By region, North America commanded 33.62% market share in 2025; Asia–Pacific expands fastest at 11.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bottled Water Processing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer health-consciousness | +2.1% | Global; strongest in North America & Europe | Medium term (2-4 years) |

| Urban middle-class expansion in emerging economies | +1.8% | Asia–Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Regulatory push for potable-water safety | +1.5% | Global; led by EU and North America | Short term (≤ 2 years) |

| Processing and packaging technology innovation | +1.3% | Global; concentrated in developed markets | Medium term (2-4 years) |

| AI-enabled real-time quality monitoring | +0.9% | Early adoption in North America & EU; APAC following | Long term (≥ 4 years) |

| Mobile & modular bottling lines for disaster relief | +0.6% | Priority in disaster-prone regions worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Health-Consciousness

Heightened focus on personal well-being pushes processors to adopt advanced purification and automated microbiological testing that complies with FDA 2024 rules on coliform and E. coli limits.[1]U.S. Food and Drug Administration, “Microbiological Testing and Corrective Measures for Bottled Water,” federalregister.gov Functional water fills a premium niche, requiring multi-stage membrane systems such as Pall’s SUPRAdisc II modules that raise throughput by 40%. AI-driven optical sensors now detect chemical oxygen demand variations with over 90% accuracy, ensuring consistent flavour and safety. Brands market mineral-rich, alkaline, or electrolyte-infused lines to health-centric consumers, adding equipment for precise nutrient dosing. These shifts reinforce demand for high-efficiency filtration, inspection, and clean-in-place systems across the bottled water processing market.

Urban Middle-Class Expansion in Emerging Economies

Asia–Pacific’s sizeable urban migration fuels spending on packaged beverages as modern retail gains reach. Indian joint ventures among Indorama, Dhunseri, and Varun Beverages are building 100 kiloton rPET capacity to support mandatory 30% recycled content targets for 2025-2026. Chinese PET producers such as Wankai scaled back output in late 2024 due to higher crude costs, creating room for energy-efficient equipment suppliers. Latin America sees Brazil and Chile use public-private partnerships to modernise water infrastructure, bringing new bids for mobile treatment plants. Middle-income households in these regions gravitate toward premium still and functional lines, lifting volume and complexity requirements for regional bottlers.

Regulatory Push for Potable-Water Safety

Policy makers tighten standards on contaminants, recycled content, and packaging chemistry. The EU Packaging and Packaging Waste Regulation enforces 30% rPET in beverage bottles by 2030 and bans PFAS from February 2025. The WHO 2025 call to action urges inclusive, climate-resilient water governance, influencing plant design worldwide. NSF/ANSI 53-2022 adds new reduction claims for point-of-use units, prompting wider deployment of specialised cartridges. Compliance now hinges on automated monitoring, digital documentation, and high-performance membranes, pushing the bottled water processing market toward upgraded installations.

Processing and Packaging Technology Innovation

Membrane breakthroughs include graphene-oxide layers with beta-cyclodextrin that capture short-chain PFAS more effectively than polyamide membranes. Electrochemical ozone generators achieve 99.8% bactericidal rates against E. coli without chemical residuals. Connected HMI and AI vision cut water and energy use by 30% in Krones lines. Packaging advances range from PHA bottles that compost within 90 days to lightweight glass and aluminium formats with full circularity programs. Continuous innovation sustains equipment sales as producers retrofit plants for higher speed, lower waste, and diverse containers across the bottled water processing market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic-waste sustainability pressures | -1.4% | Global; strongest in EU & other developed markets | Short term (≤ 2 years) |

| High capital expenditure for equipment | -1.1% | Global; greater impact in emerging markets | Medium term (2-4 years) |

| PET-resin price volatility | -0.8% | Worldwide with regional variations | Short term (≤ 2 years) |

| Municipal refill-station roll-outs | -0.5% | Urban centres in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic-Waste Sustainability Pressures

Europe’s BPA ban forces cooler suppliers to convert to PET alternatives by 2029, raising re-tooling costs for moulders. rPET remains USD 750-800 a tonne dearer than virgin PET, dampening adoption despite policy targets. China owns 66% of global PET capacity, undercutting European prices and heightening calls for trade remedies. Wood-based plastics now offer an alternative yet require new extrusion and blowing systems. The transition to circular packaging raises total plant investment and shifts demand toward equipment capable of handling higher recycled content across the bottled water processing market.

High Capital Expenditure for Equipment

Complex filling blocks, aseptic systems, and AI inspection modules command large outlays. Krones posted EUR 537.1 million EBITDA in 2024 partly on the Netstal acquisition for PET preform moulding. Danone spent USD 65 million on a Florida line that reduces bottle loss by 30% with novel moulding. Veolia’s emergency reverse-osmosis fleets illustrate high mobile-system costs and operator training needs. Smaller bottlers in emerging economies often delay upgrades, tempering the growth rate of the bottled water processing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Automation Drives Efficiency Gains

Filter assemblies retained 35.31% share in 2025 as multi-stage setups target microplastics and PFAS removal. Shrink wrappers register a 12.63% CAGR through 2031 because automated systems wrap 60-200 bottles per minute while lowering labour overhead. Integrated blow-moulder-filler blocks such as Krones ErgoBloc cut energy draw by optimising heating profiles.

Inspection technology evolves through augmented-reality service that speeds remote diagnostics and drops unplanned downtime to 0.1% in pilot sites. Conveyor systems embed AI vision to anticipate faults, which reduces idle time and boosts line utilisation. As plants target higher throughput, interest in modular conveyors and quick-changeover sleeve labelers widens the addressable base for equipment suppliers across the bottled water processing market.

By Technology: Membrane Innovation Accelerates

Reverse osmosis led with 27.95% share in 2025 thanks to ultrathin polyamide films that channel water up to eight times faster at lower pressure. Microfiltration’s 11.86% CAGR is propelled by hollow-fibre units achieving 98% recovery with minimal chemicals.

Ultrafiltration systems find favour in pre-treatment, easing fouling on downstream RO stages while keeping operating costs in check. Ion exchange sees renewed interest where selective resins strip hardness or heavy metals before bottling. UV LED arrays now provide 99.99% kill rates without mercury, supporting low-carbon operations. Electrochemical ozonation eliminates the need for separate oxygen concentrators, simplifying plant layouts. Such advances sustain the bottled water processing market as producers seek lower energy footprints and better contaminant control.

By Application: Functional Water Processing Expands

Still water remained the cornerstone with 57.42% of 2025 demand, produced on high-speed lines topping 80,000 bph. Functional water’s 11.59% CAGR stems from consumer appetite for vitamin, mineral, or electrolyte fortification, which needs precise micro-ingredient dosing under aseptic conditions.

Sparkling formats gain share as carbonation systems stabilise CO₂ dissolution while curbing gas loss. Flavoured waters rely on sterile dosing skids that avoid sugar crystallisation and aroma fade. Mineral water brands protect source integrity while applying UV and ozonation for microbiological safety. The resulting complexity enlarges the installation base for accurate mixing, sterile filling, and closed-loop monitoring across the bottled water processing market.

By Packaging Material: Sustainability Drives Innovation

PET secured 71.68% share in 2025, yet policy targets propel recycled content integration and alternative polymers. rPET food-grade quality demands advanced sorting, flake-washing, and solid-state polymerisation to remove impurities. Bioplastics post a 11.92% CAGR, led by PHA bottles approved for industrial composting within 90 days.

Lightweight glass, now 30% lighter, re-positions bottled water for premium audiences without major carbon penalties. Aluminium bottles benefit from high recycling value and on-the-go convenience. Processing lines shift toward flexible changeovers that handle multiple containers while maintaining sterility, a change that broadens the bottled water processing market size for turnkey integrators.

Geography Analysis

North America captured 33.62% market share in 2025, anchored by rigorous FDA microbiological protocols and early adoption of AI inspection. Regional bottlers benefit from established distribution and premium priced functional lines. Coca-Cola’s water stewardship programme and smartwater alkaline extensions illustrate category premiumisation, while PepsiCo pilots 100% recyclable paper bottles through Pulpex partnerships.Investment in AI-enabled maintenance keeps downtime low, reinforcing replacement demand within the bottled water processing market.

Asia–Pacific registers the fastest 11.07% CAGR. Urbanisation and rising disposable incomes support volume growth, and government mandates for recycled content spur equipment upgrades. India’s 100 kiloton rPET projects broaden feedstock for local bottlers. Chinese producers improve operational efficiency after capacity cutbacks caused by high feedstock costs, creating opportunities for advanced low-energy membrane suppliers. Modular and containerised bottling lines meet growing demand in disaster-prone areas, widening the bottled water processing market.

Europe maintains significant share under tightened environmental rules. The Packaging and Packaging Waste Regulation grants first mover advantage to plants capable of 30% rPET and PFAS-free designs. Middle East and Africa witness desalination investments like Metito’s 50,000 m³/day Kazakhstan plant that incorporates bottled output for remote regions. Latin America relies on private capital to upgrade plants in Brazil and Chile, bringing new bids for high-throughput filtration and filling lines.

Mordor Intelligence provides coverage of the bottled water processing market across other key regional markets, including Europe and North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The bottled water processing market exhibits fragmentation. Top suppliers combine equipment breadth, digital services, and after-sales networks to protect share. Krones booked EUR 5.29 billion revenue in 2024 and bought Netstal Maschinen for PET preform moulding, completing a closed-loop PET portfolio. Tetra Pak’s Factory Sustainable Solutions integrate nanofiltration, reverse osmosis, and heat recovery, helping plants cut energy and water costs by double-digit percentages.

Danone’s Partner for Growth programme signs 19 strategic suppliers, including SPX FLOW and Graphic Packaging, to lower resource use across its bottling network.[3]Danone, “Partner for Growth Program,” danone.com Sidel’s 80,000 bph Ghana hub shows emerging region investments that pair high speed filling with automated cleaning, giving local producers global-grade throughput.

Disruptors focus on precision membranes, electrochemical ozone, and AI diagnostics. Graphene-based filters outperform classical polymers on PFAS removal, while containerised systems by Kärcher Futuretech deliver 26,000 L/day in crisis zones. Such differentiation pressures incumbents to accelerate R&D, shaping the future trajectory of the bottled water processing market.

Bottled Water Processing Industry Leaders

Bisleri International Pvt. Ltd.

Danone S.A.

Gerolsteiner Brunnen GmbH & Co. KG

Nestle S.A.

Nongfu Spring (Yangshengtang Co. Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Krones closed the Netstal Maschinen AG acquisition, boosting PET preform and closure capabilities for closed-loop solutions.

- February 2025: Tetra Pak unveiled Factory Sustainable Solutions that merge nanofiltration, reverse osmosis, and heat recovery to lower resource use.

- January 2025: Sidel and Twellium opened Ghana’s fastest PET water line, running 80,000 bph with automated CIP.

- December 2024: Danone invested USD 65 million in a Florida line with bottle-moulding that cuts container loss by 30%.

Global Bottled Water Processing Market Report Scope

The bottled water processing industry refers to the sector involved in the production and processing of bottled water. It includes various stages, such as sourcing water from natural or treated sources, treating the water to meet quality standards, bottling, packaging, and distributing the final product to consumers. The industry ensures that the water is safe, clean, and meets regulatory requirements before it is packaged and sold to the public. Bottled water processing companies utilize advanced technologies and quality control measures to ensure the purity and safety of the water throughout the production process. The industry plays a significant role in providing consumers with convenient access to clean drinking water, especially in areas where tap water quality may be a concern or when individuals prefer the convenience of bottled water.

The bottled water processing market is segmented by equipment type: filter, bottle washer, filler and capper, blow molder, and other equipment types. By technology, the market is segmented by reverse osmosis (RO), ultrafiltration (UF), microfiltration (MF), chlorination and other technologies. By application, the market is segmented by still water, sparkling water, and flavored water. By region, the market is segmented by North America, Europe, Asia-Pacific, Middle East and Africa, and South America.

The market size and forecasts are provided in terms of (USD) for all the above segments.

| Filter |

| Bottle Washer |

| Filler and Capper |

| Blow Molder |

| Shrink Wrapper |

| Conveyor |

| Inspection System |

| Labeler |

| Other Equipment |

| Reverse Osmosis (RO) |

| Microfiltration (MF) |

| Ultrafiltration (UF) |

| Chlorination |

| Ion Exchange |

| UV Disinfection |

| Ozonation |

| Other Technology |

| Still Water |

| Sparkling Water |

| Flavored Water |

| Functional Water |

| Mineral Water |

| Plastic (PET) |

| Glass |

| Aluminum Cans |

| Bioplastics |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Equipment | Filter | ||

| Bottle Washer | |||

| Filler and Capper | |||

| Blow Molder | |||

| Shrink Wrapper | |||

| Conveyor | |||

| Inspection System | |||

| Labeler | |||

| Other Equipment | |||

| By Technology | Reverse Osmosis (RO) | ||

| Microfiltration (MF) | |||

| Ultrafiltration (UF) | |||

| Chlorination | |||

| Ion Exchange | |||

| UV Disinfection | |||

| Ozonation | |||

| Other Technology | |||

| By Application | Still Water | ||

| Sparkling Water | |||

| Flavored Water | |||

| Functional Water | |||

| Mineral Water | |||

| By Packaging Material | Plastic (PET) | ||

| Glass | |||

| Aluminum Cans | |||

| Bioplastics | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the bottled water processing market?

The market was valued at USD 223.43 billion in 2026.

How fast is the bottled water processing market expected to grow?

It is forecast to rise at an 8.19% CAGR, reaching USD 331.24 billion by 2031.

Which region will grow the fastest through 2031?

Asia–Pacific is projected to expand at an 11.07% CAGR, driven by urbanisation and middle-class income growth.

What equipment category holds the largest share?

Filter systems led with 35.31% revenue share in 2025.

Why are bioplastics gaining traction in water packaging?

Regulatory mandates and consumer pressure for sustainable packaging are driving bioplastic adoption, which now posts a 11.92% CAGR.

How does AI benefit bottled water processing plants?

AI vision and predictive maintenance cut downtime, optimise resource use, and ensure higher product consistency, improving plant profitability.

Page last updated on: