Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

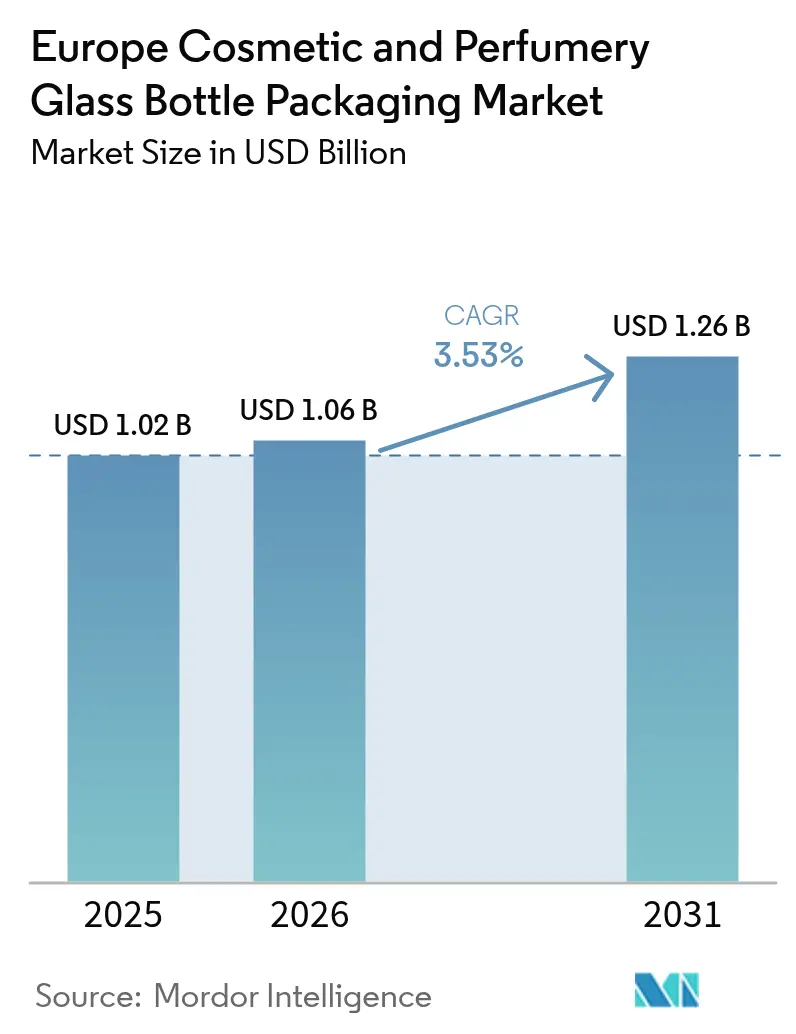

| Base Year Market Size (2025) | USD 1.02 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 3.53% CAGR |

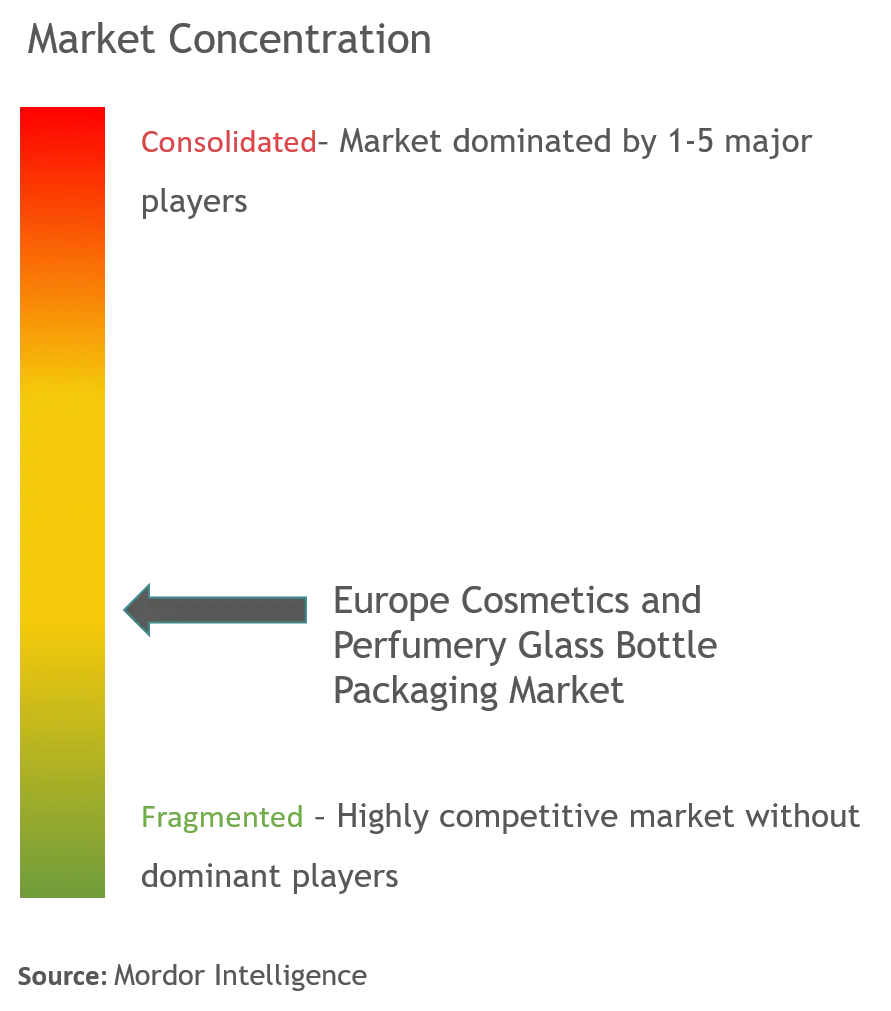

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cosmetic And Perfumery Glass Bottle Packaging Market Analysis by Mordor Intelligence

The Europe cosmetic and perfumery glass bottle packaging market size was valued at USD 1.02 billion in 2025 and estimated to grow from USD 1.06 billion in 2026 to reach USD 1.26 billion by 2031, at a CAGR of 3.53% during the forecast period (2026-2031). This moderate headline growth masks a shift toward high-PCR compositions, furnace electrification, and refillable formats, which are reshaping capital spending, supplier selection, and bottle design. Luxury houses are incorporating minimum recycled-glass thresholds into their specifications, while specialty converters are installing hybrid methane-electric furnaces that promise double-digit gas savings but require multimillion-euro investments. Cost inflation is therefore migrating from energy to equipment, and producers able to amortize these investments across food, spirits, and pharmaceutical lines are better positioned to defend margins. At the same time, niche beauty labels are utilizing stock amber vials and digital decoration to compete on sustainability narratives, rather than relying on bespoke molds, thereby enlarging the addressable customer base for mid-size converters.

Key Report Takeaways

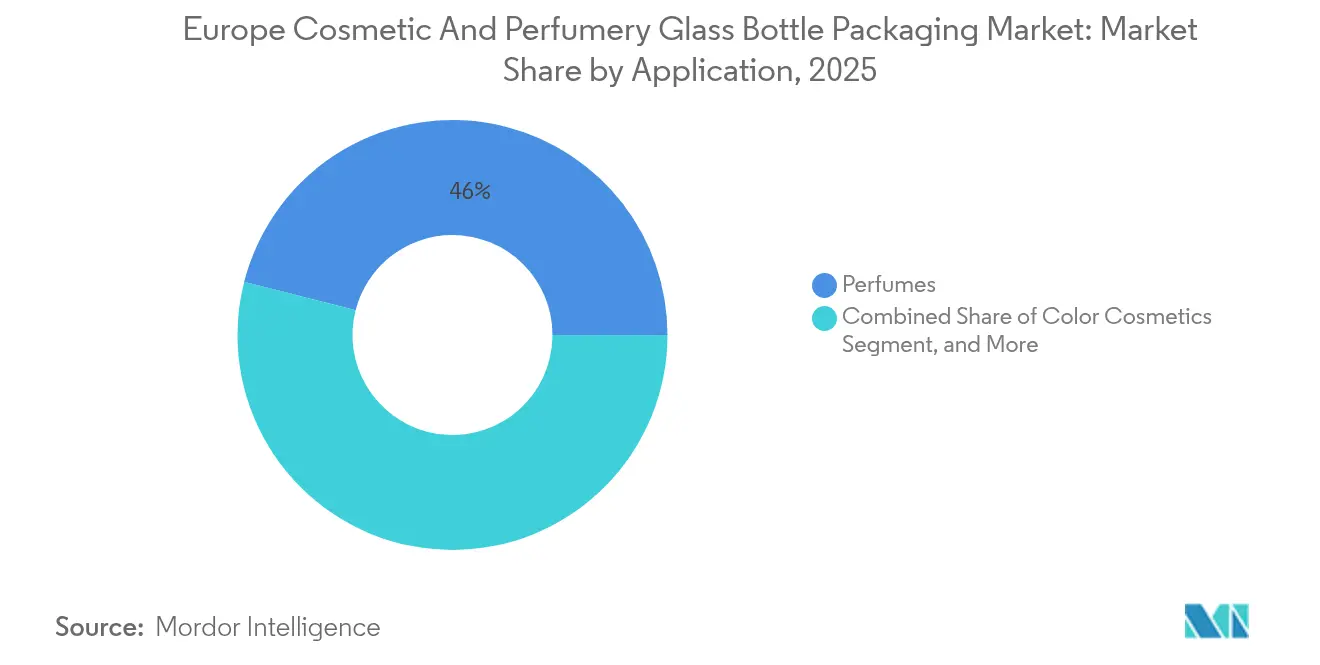

- By application, perfumes led the Europe cosmetic and perfumery glass bottle packaging market with a 46.02% share in 2025; skin care is expected to expand at a 4.56% CAGR through 2031.

- By capacity, the 50-100 ml segment captured 42.10% of the Europe cosmetic and perfumery glass bottle packaging market share in 2025, while the 100-150 ml segment is forecast to post the fastest growth, with a 5.49% CAGR through 2031.

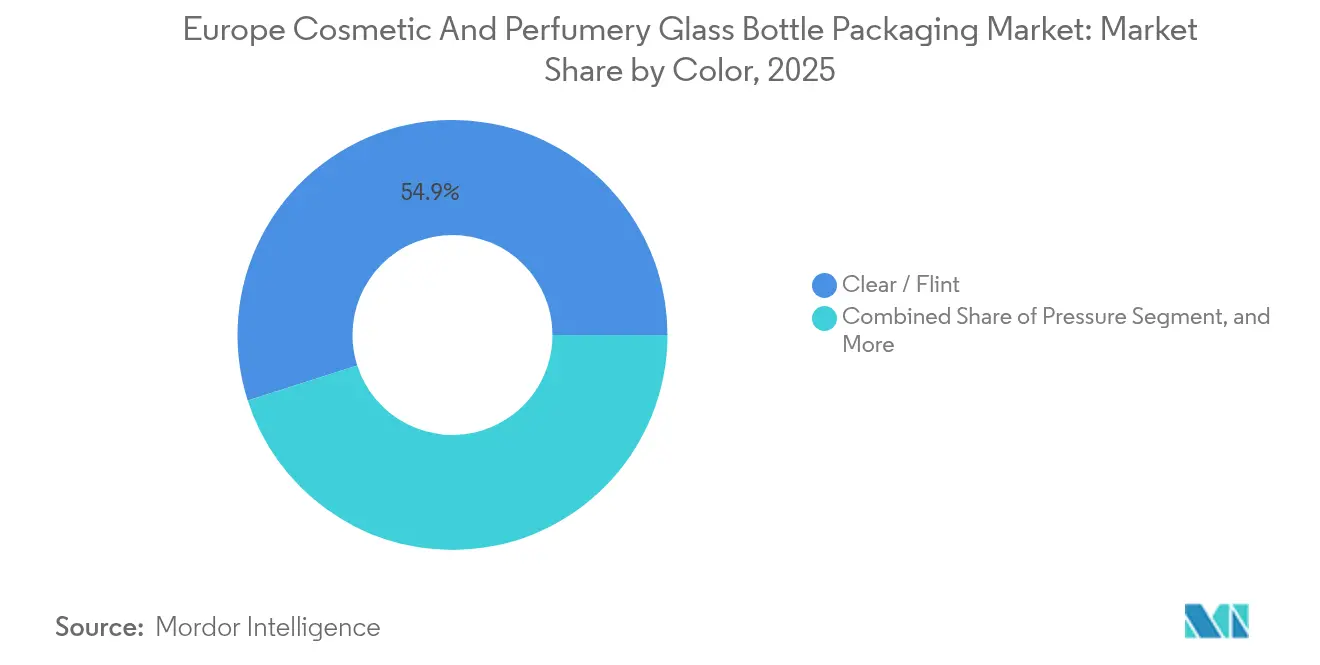

- By color, clear glass accounted for 54.92% of the Europe cosmetic and perfumery glass bottle packaging market share in 2025; amber glass is projected to advance at a 4.81% CAGR over 2026-2031.

- By end-user, luxury brands retained 47.70% of the Europe cosmetic and perfumery glass bottle packaging market share in 2025; indie and private-label brands are set to grow at a 5.17% CAGR to 2031.

- By country, Germany dominated the Europe cosmetic and perfumery glass bottle packaging market with a 22.35% share in 2025, whereas Spain is poised to achieve the highest 5.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Cosmetic And Perfumery Glass Bottle Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Dropper Bottles | +0.6% | Germany, France, Benelux (serum-intensive markets) | Medium term (2-4 years) |

| Increased Emphasis on Packaging for Product Differentiation | +0.5% | Global, with premium concentration in France, UK, Italy | Long term (≥ 4 years) |

| Premiumization of European Fragrance and Skin Care Segments | +0.8% | France, Germany, UK, Italy (luxury hubs) | Long term (≥ 4 years) |

| EU Packaging and Packaging Waste Regulation Accelerating High-PCR Glass Adoption | +0.9% | EU-27 (regulatory mandate) | Short term (≤ 2 years) |

| Expansion of Refillable and Returnable Glass Systems Across Luxury Beauty | +0.5% | France, Germany, Benelux (early-adopter luxury brands) | Medium term (2-4 years) |

| Automation Investments Driven by Skilled-Glassmaker Shortages | +0.3% | Germany, Italy, France (high-wage manufacturing hubs) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Dropper Bottles

Formulators seeking high-potency serums are championing glass droppers because the format signals precision dosing, enhances perceived efficacy, and commands price premiums of 15-25% over screw-cap bottles.[1]Virospack, “Tubular Vial Launch,” virospack.com Virospack’s 2024 rollout of tubular vials with Blowback and Antirotation patents underscores that dimensional repeatability, not furnace output, is the gating factor, nudging converters to co-engineer neck finishes with closure suppliers. As the Europe cosmetic and perfumery glass bottle packaging market deepens its focus on actives, bottles below 50ml are capturing new formulations that rely on dropper caps to meter retinol, niacinamide, and microbiome cultures. German and Dutch fillers, many operating at pharmaceutical-grade clean-room standards, are exploiting their QC credentials to win turnkey contracts from clinical-beauty startups that lack in-house filling lines. The net result is a shift toward small-batch, high-margin orders that reward converters with rapid changeover capability and digitally enabled decoration.

Increased Emphasis on Packaging for Product Differentiation

Luxury and premium mass labels alike are upgrading their decorations to convey exclusivity while preserving recyclability. Bormioli Luigi opened a vacuum sputtering unit in 2024 that metallizes entire bottles without lacquers, allowing converters to keep the container in the clear-glass recycling stream.[2]Packaging Connections, “Bormioli Luigi Introduces Hybrid Furnace,” packagingconnections.com Baralan then introduced 3D relief technology in 2025, embedding raised logos directly in the mold so that tactile branding replaces secondary labels. These capabilities accelerate time to market because decoration is integral, not post-process, reducing cycle times for limited runs that indie brands demand. Converters that can bundle design, molding, and decoration are therefore capturing a higher wallet share, a trend visible in France and Italy, where integrated glassworks can deliver full-service prototypes in under eight weeks. The Europe cosmetic and perfumery glass bottle packaging market is benefiting as brand managers allocate incremental budget from digital advertising back toward physical differentiation, reviving value growth even as unit sales flatten.

Premiumization of European Fragrance and Skin Care Segments

Fragrances priced above EUR 100 (USD 109) per 75ml are growing faster than the total fragrance market, and the aesthetic of heavy, thick-walled flint glass remains central to the perceived luxury.[3]Formes de Luxe, “Investment Consortium to Acquire Verescence,” formesdeluxe.com Verescence, which supplies LVMH, Puig, and L’Oréal, produces over 600 million bottles annually and operates five dedicated decoration plants, demonstrating how production scale and artistry coexist in the top tier. In skin care, premium jars weighing 150-200g are replacing plastic in the EUR 50-plus bracket because consumers associate glass with product purity and inertness. German specialty retailers report that facial serums in amber glass outsell those in plastic droppers by double-digit margins, despite higher shelf prices. Private-equity interest reinforces the momentum that the 2025 sale of Verescence to a Movendo Capital-led consortium signals, indicating that investors see headroom in premium glass, rather than commoditized beverage grades. The Europe cosmetic and perfumery glass bottle packaging market, therefore, skews toward value per tonne, not volume, insulating converters from the cyclical lows seen in mass beverages.

EU PPWR Accelerating High-PCR Glass Adoption

Regulation (EU) 2023/1545 mandates tiered recycled-content thresholds, encouraging cosmetic brands to adopt verified PCR supply. Each 10% PCR increment reduces CO₂ emissions roughly 5%, aligning with corporate net-zero pledges. Verescence’s Infini 20 and Infini 40 lines already exceed the regulation and recorded a 77% PCR integration in 2023, positioning the firm as the supplier of choice for brands seeking scope 3 carbon reductions. Yet PCR introduces color tints and defect risk, so converters are installing optical-sorting cullet systems and investing in advanced forehearth controls to stabilize melt. In Spain and France, regional governments co-fund cullet-processing centers, thereby reducing the length of reverse logistics loops and increasing bottle-to-bottle yields. The Europe cosmetic and perfumery glass bottle packaging market is thus moving toward closed-loop procurement contracts where brand, filler, and converter share PCR-quality KPIs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Plastic Packaging as a Substitute for Glass Bottles | -0.4% | Mass-market segments across Europe (price-sensitive retail) | Medium term (2-4 years) |

| High Energy Costs and Carbon Footprint of Glass Production | -0.6% | Germany, Italy, France (energy-intensive manufacturing) | Short term (≤ 2 years) |

| Freight-Surcharges for E-commerce Fragile Goods | -0.2% | UK, Germany, Benelux (high e-commerce penetration) | Short term (≤ 2 years) |

| Soda-Ash Supply Volatility Disrupting Furnace Scheduling | -0.3% | EU-27 (import-dependent supply chains) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Plastic Packaging as a Substitute for Glass Bottles

Below EUR 20 price points, PET and monomaterial PP are eroding glass's share because freight, breakage, and dangerous-goods surcharges add 25-40% to the cost during e-commerce fulfillment. Quadpack’s 2025 Lola PET jar targets this sensitivity by offering a single-polymer pack that sidesteps glass weight penalties. DHL’s cosmetics sector guide highlights that alcohol-rich perfumes in glass face hazmat classification, raising compliance overhead for small web merchants. However, the EU’s 2027 microplastics ban will prohibit certain plastic additives, aluminum, and bio-PET, and offer medium-term relief for cost-driven brands. Converters respond by lightweighting flint bottles, but acceptance varies: mass drugstores calculate total landed cost without assigning monetary value to sustainability claims, so glass loses out unless a supplier can prove parity on grams per dose.

High Energy Costs and Carbon Footprint of Glass Production

Furnace fuel remains the highest variable cost. Natural-gas prices, while below the 2022 spike, still average 50-70% above 2019 levels, and electricity remains volatile as nuclear shutdowns squeeze supply. O-I Glass invested EUR 95 million (USD 103 million) to install oxy-fuel-assisted furnaces in France, claiming 18% CO₂ cuts. Bormioli Luigi’s 2024 hybrid furnace, co-funded by the EU Innovation Fund, mixes methane with electric boosting to trim gas usage by 30%. Financing these rebuilds is challenging against a 3.58% CAGR topline, so converters with diversified beverage or pharma exposure cross-subsidize cosmetics capacity. Meanwhile, contract terms index glass-price surcharges to the German Day-Ahead Power Price, directly passing energy volatility to brand customers and making packaging budgets harder to forecast.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Perfumes Anchor Value, Skin Care Unlocks Incremental Growth

Perfumes maintained a 46.02% share in 2025, underscoring the importance of scent preservation and brand storytelling, which rely on inert, fragrance-impermeable glass. EDP and extrait concentrations require thick-wall bottles to prevent evaporation and oxidation, and leading houses allocate up to 15% of ex-factory cost to primary packaging, well above the cosmetics average. Within Europe, flagship SKUs such as Lancôme La Vie Est Belle and Dior Sauvage each sell over 3 million units annually in flint bottles that act as quasi-collectibles. The Europe cosmetic and perfumery glass bottle packaging market benefits because refill pods use the same high-spec ratios to fit existing bottle geometries, embedding a base load of replacement demand.

Skin care, which accounts for only 33% of the volume, is expanding at a 4.56% CAGR as clinical-grade serums proliferate. Airless pumps built into glass barrels now meet ISO 15378 pharma-pack standards, letting cosmeceutical brands validate 36-month stability for retinoids and peptides. Dropper bottles account for nearly half of new skin-care treatment launches in France and the Netherlands, where dermocosmetics often capture dermatologist recommendations. Indie brands often prefer amber glass droppers under 30ml to reinforce apothecary cues and minimize UV degradation. In both strands, the Europe cosmetic and perfumery glass bottle packaging industry leverages pharmaceutical know-how, clean-room molding, EO sterilization, and tamper bands to upsell value-added services that plastic cannot match.

By Capacity: Mid-Range Dominates, Large Formats Accelerate

Bottles between 50 ml and 100 ml held a 42.10% share of the Europe cosmetic and perfumery glass bottle packaging market in 2025, as they align with the portability of handbags and customs duty-free limits. The 75 ml size remains flagship for prestige fragrances, driving economies of scale in mold cavitation and carton sizes. Yet the 100-150 ml bracket will clock a 5.49% CAGR on the back of “value jar” night creams and premium body oils that justify pantry-size packs. Vetropack’s upcoming thermally hardened lightweight technology promises 30% lighter glass in that range without sacrificing drop resistance, a breakthrough that could unlock mass-premium adoption.

Formats under 30 ml thrive in booster concentrates and discovery sets, where lower fill volumes support retail pricing of EUR 1 per milliliter. However, for ampoules below 10 ml, plastic and aluminum blister sticks compete aggressively due to airline carry-on rules and the weight of secondary packaging. At the opposite extreme, formats exceeding 150 ml remain niche but are gaining traction in bath elixirs and spa oils sold through direct-to-consumer channels. These tend to use flint or coated black bottles to emphasize ritual and aesthetics, reinforcing the experiential pull that glass confers. For converters, the capacity mix dictates furnace scheduling: small formats demand narrow-neck press-and-blow, while jars require wide-mouth presses, so multi-IS lines rotate molds weekly to balance changeover losses with inventory risk.

By Color: Clear Leads, Amber Gains Momentum

Clear or flint glass accounted for 54.92% of the 2025 volume, primarily because transparency showcases the hue of juice in fragrances and reveals texture gradients in skin creams. Decoration can then add color via internal lacquers or external metallization without sacrificing the base raw material. Yet amber glass is the fastest climber, with a 4.81% CAGR, because “clean beauty” and probiotic serums often tout UV protection and apothecary aesthetics. Notably, vitamin C serums degrade 50% slower in amber versus flint, according to supplier stability tests, allowing brands to extend shelf-life guarantees to 24 months.

Color segmentation also plays a role in refill systems, where translucent shells with inner PET cartridges allow consumers to monitor the fill level while the structural outer bottle remains pristine. Mixing cullet streams, however, complicates recycling as color impurities downgrade flint batches. Germany’s dual-stream system mandates color-sorted returns, providing its converters with superior cullet purity and thereby a cost advantage over flint melts. Southern markets with single-stream collection struggle to supply color-sorted PCR, forcing converters to import high-grade cullet at premium prices, a logistics cost now amplified by fuel surcharges.

By End-User: Luxury Retains Scale, Indie Brands Deliver Growth

Luxury conglomerates, including LVMH, Estée Lauder, and Chanel, held a 47.70% share in 2025, deploying multi-year framework agreements that guarantee furnace utilization for suppliers such as Verescence and Stoelzle. These contracts often bundle exclusivity on mold ownership, preventing converters from reselling unused capacity, but provide long-run visibility essential for financing furnace rebuilds. Upmarket brands also demand ISO 50001 certification and full scope-3 carbon accounting, raising the barrier to entry for smaller glassworks.

Indie and private-label players are advancing at a 5.17% CAGR by using contract packers such as Quadpack and Lumson. Minimum order quantities of 5,000 units permit test-and-learn product drops without inventory obsolescence. Digital inkjet decoration supports a 10-day turnaround, crucial for social-commerce flash sales. While unit economics are lean, indie brands pay 30% more per bottle than their luxury peers; they offset this by leveraging direct-to-consumer margins and crowdfunding. For converters, the challenge is operational flexibility: short runs risk idle furnace time, so AI-driven batch planning tools schedule independent orders as fillers between luxury campaigns, maximizing tonnage per day.

Geography Analysis

Germany contributed 22.35% of 2025 demand, driven by a USD 24.0 billion (EUR 22.0 billion) domestic beauty spend and a network of precision glassmakers concentrated in Bavaria and Thuringia. Gerresheimer’s Lohr am Main plant underwent a hybrid furnace retrofit, which reduced gas use by 15% and lowered CO₂ emissions by 40%, solidifying Germany’s position as a leading pilot for decarbonized melting on the continent. The market also benefits from pharmacy-channel dermocosmetics, where regulatory traceability favors glass over plastic. Germany’s dual-stream recycling system collects 85% of container glass, feeding high-quality cullet back into the cosmetic loop and lowering the effective cost per tonne.

Spain, although with only 12% of the current volume, will post the region’s top 5.86% CAGR through 2031. A 5.30% expansion in domestic beauty spending, a USD 7.8 billion (EUR 7.2 billion) export engine, and Verescence’s La Granja investment are mutually reinforcing tailwinds. Catalonia’s government subsidizes cullet-processing plants, accelerating closed-loop PCR supply that aligns with EU PPWR. Spanish fragrance leader Puig channels local bottle supply into its brands and third-party fill contracts, anchoring furnace utilization. Tourism rebound fuels duty-free perfume traffic through Barcelona and Madrid airports, boosting demand for high-unit-value bottles.

France remains the export powerhouse, with USD 25.4 billion (EUR 23.3 billion) in cosmetics shipments in 2024, sustaining a vast capacity in Normandy and the Loire Valley. The PFAS ban, effective January 2026, and allergen-label expansion in 2026 push formulators toward stable, inert containers, favoring thick-walled glass. Verescence, Pochet, and SGD Pharma share a deep understanding of decorative know-how, enabling French brands to iterate on bottle design without importing capacity. Meanwhile, state-backed green-loan schemes fund hybridization of legacy furnaces, closing the gap between sustainability ambition and capex constraints.

Italy and the United Kingdom round out the major blocs, each with mature yet premium-oriented spend. Italy’s Bormioli Luigi and Zignago Vetro lead the way in lightweight jars, while UK converters cater to heritage fragrance houses navigating post-Brexit border frictions. Benelux, although small, houses logistics hubs and Verescence’s decoration site in Belgium, which distributes amber serum bottles across Northern Europe overnight. Central and Eastern Europe exhibit pockets of 4-5% growth as rising incomes drive beauty spending; however, the glass supply there still imports molds and decorations from Western Europe, limiting local bottle diversity.

Competitive Landscape

Consolidation defines the Europe cosmetic and perfumery glass bottle packaging market. Gerresheimer’s EUR 800 million (USD 872 million) purchase of Bormioli Pharma in 2024 added nine plants and significant closure capacity, unlocking one-stop supply for jars, vials, and droppers. Verallia’s EUR 230 million (USD 251 million) acquisition of Vidrala’s Italian arm strengthened cross-category scalability, letting it shuttle molds between food and beauty orders. Private-equity capital poured in when Movendo Capital and Draycott acquired Verescence in 2025, signaling that investors value luxury-skewed portfolios insulated from fluctuations in beverage volume.

Strategically, players are focusing on three key levers: furnace hybridization, automation, and the design of refill systems. Stoelzle’s AI process control reduces scrap by 8%, resulting in a direct EBIT uplift as scrap melts consume unbillable energy. Bovone’s 7-axis robotic polishing reduces manual defects, elevating A-grade output critical for the clarity of fragrance flacons. On decarbonization, O-I’s oxy-fuel furnaces and Bormioli Luigi’s methane-electric hybrids set benchmarks that regulators may codify into best practices. Hemorrhaging skilled labor accelerates the adoption of robotics, with Vetropack’s automated Italian warehouse eliminating 3-5% of handling losses and enabling 24-hour dispatch windows.

White-space innovation lies in refillable architecture and advanced PCR formulations. Lumson’s Slim 50 ml jar features a twist-off cup, allowing only the inner pod to be replenished, which cuts the lifecycle glass mass by 60%. Techniplast’s RT-Lift technology enables vertical cartridge swaps without unscrewing entire assemblies, making it ideal for eye-cream jars where torque can induce stress cracks. Smaller disruptors that master these mechanics can punch above their weight by licensing IP to major brands. Industry certifications have become table stakes: ISO 9001 and 22716 guarantee cosmetics GMP, ISO 14001 attests to environmental governance, and the forthcoming ISO 23969 will govern PCR traceability, reinforcing the compliance moat for incumbents.

Europe Cosmetic And Perfumery Glass Bottle Packaging Industry Leaders

Verescence France SASU

Vitro S.A.B. de C.V.

Zignago Vetro SpA

Piramal Glass Private Limited

Pragati Glass Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vetropack’s thermally hardened lightweight reusable glass bottle concept won the World Packaging Organisation WorldStar Award, highlighting a 30% weight reduction while preserving structural integrity.

- March 2025: Baralan unveiled its new 3D decoration technology alongside the Re-Charge refillable glass system, delivering raised logo designs and reusable containers for emerging beauty brands.

- February 2025: Verescence entered exclusive negotiations for a change of ownership as Oaktree Capital Management agreed to sell its stake to a Movendo Capital and Draycott led consortium, paving the way for continued investment in sustainable glass capacity.

- January 2025: TricorBraun announced the acquisition of Euroglas in Germany and Glaspack in Austria, broadening its distribution reach across the DACH region.

Europe Cosmetic And Perfumery Glass Bottle Packaging Market Report Scope

The Europe cosmetic and perfumery glass bottle packaging market refers to the industry focused on the production, distribution, and utilization of glass bottles specifically designed for packaging cosmetics and perfumery products. These bottles are valued for their durability, aesthetic appeal, and ability to preserve the quality of the contents.

The Europe Cosmetic and Perfumery Glass Bottle Packaging Market Report is Segmented by Application (Perfumes, Skin Care, Color Cosmetics, Other Applications), Capacity (Up to 50 ml, 50–100 ml, 100–150 ml, Above 150 ml), Color (Clear/Flint, Amber, Other Colors), End-User (Luxury Brands, Premium Mass, Mass Market, Indie/Private Label), and Country (Germany, United Kingdom, France, Italy, Spain, Benelux, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD) Only.

By Application

| Perfumes |

| Skin Care |

| Color Cosmetics |

| Other Applications |

By Capacity

| Up to 50 ml |

| 50 – 100 ml |

| 100 – 150 ml |

| Above 150 ml |

By Color

| Clear / Flint |

| Amber |

| Other Colors |

By End-User

| Luxury Brands |

| Premium Mass |

| Mass Market |

| Indie / Private Label |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Benelux |

| Rest of Europe |

| By Application | Perfumes |

| Skin Care | |

| Color Cosmetics | |

| Other Applications | |

| By Capacity | Up to 50 ml |

| 50 – 100 ml | |

| 100 – 150 ml | |

| Above 150 ml | |

| By Color | Clear / Flint |

| Amber | |

| Other Colors | |

| By End-User | Luxury Brands |

| Premium Mass | |

| Mass Market | |

| Indie / Private Label | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Benelux | |

| Rest of Europe |

Key Questions Answered in the Report

What is the value of Europe’s cosmetic and perfumery glass bottle packaging segment in 2026?

The segment is valued at USD 1.06 billion in 2026 and is projected to hit USD 1.26 billion by 2031.

How quickly is high-PCR glass adoption advancing under the EU Packaging and Packaging Waste Regulation?

PCR integration is rising sharply, with leading suppliers already embedding 20-40% recycled content and reporting 77% of total 2023 output produced with PCR glass.

Why are skincare brands shifting to glass dropper bottles?

Dropper formats signal precision dosing, justify 15-25% price premiums, and protect high-potency actives, making them a preferred choice for serums and treatment concentrates.

Which European geography is forecast to record the fastest growth in cosmetic glass packaging to 2031?

Spain is set to grow at a 5.86% CAGR, buoyed by export-oriented fragrance houses and rapid e-commerce expansion.

How are high energy costs shaping production strategies for glass containers?

Producers are investing in hybrid methane-electric furnaces and oxy-fuel technology to cut gas use 15-30% and lower on-site CO₂ emissions by up to 18%.

What innovation enables lighter cosmetic glass bottles without sacrificing durability?

Thermally hardened lightweight bottles, slated for industrial roll-out in 2026, reduce weight by about 30% while maintaining the structural strength required for refill cycles.

Page last updated on: