Europe Blueberry Market Analysis by Mordor Intelligence

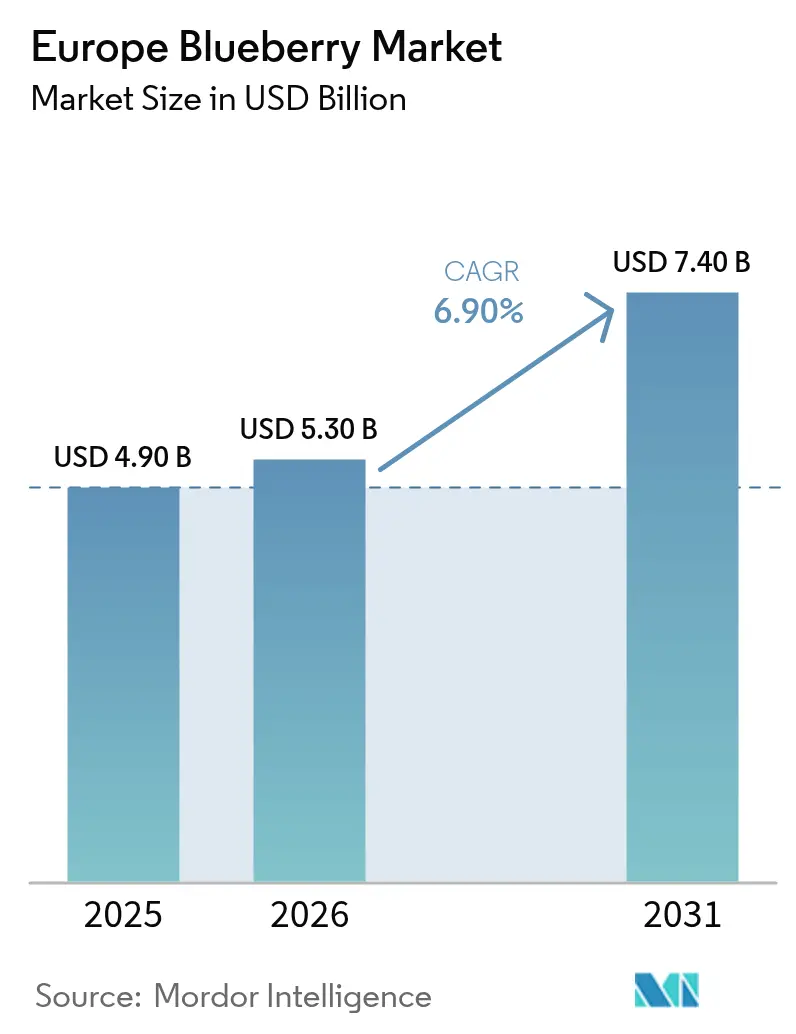

The Europe blueberry market size is projected to expand from USD 4.9 billion in 2025 and USD 5.3 billion in 2026 to USD 7.4 billion by 2031, registering a CAGR of 6.9% between 2026 and 2031. Robust consumer demand for nutrient-dense snacks, multi-year sourcing contracts that shift retail risk onto growers, and rapid tunnel adoption that lengthens the harvest season underpin this trajectory. Spain maintains its leadership in supply because Huelva province harvests premium fruit in December when wholesale prices peak. Germany anchors consumption as retailers position blueberries as convenient functional food, while Poland posts double-digit production gains by coupling tunnel systems with mechanical harvesters. Ongoing consolidation among packers and breeders strengthens their negotiating power with supermarkets, yet moderate concentration leaves room for regional cooperatives to scale proprietary cultivars and capture margins.

Key Report Takeaways

- By geography, Germany commanded a 24.8% share of the Europe blueberry market size in 2025 and is advancing at a 9.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Blueberry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of controlled-environment agriculture | +1.8% | Spain, the Netherlands, Poland, Germany, the United Kingdom, France, and Italy | Medium term (2-4 years) |

| Expansion of mechanized harvesting technologies | +1.2% | Poland, Spain, the Netherlands, and Germany | Medium term (2-4 years) |

| Growing demand for antioxidant-rich snack ingredients | +1.5% | Europe with the strongest pull in Germany and the United Kingdom | Long term (≥ 4 years) |

| European Union specialty-crop financial support programs | +1.3% | All member states, strongest uptake in Spain and Poland | Long term (≥ 4 years) |

| Retail-chain private-label grower contracts | +1.4% | Western Europe retail hubs | Medium term (2-4 years) |

| Blueberry inclusion in nationally funded school-meal standards | +0.9% | Germany, Poland, the United Kingdom, France, Spain, Italy, the Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Controlled-Environment Agriculture

High‑tunnel systems in Huelva enable a December blueberry harvest, allowing growers to secure pre‑holiday premiums, and in 2026, blueberries covered approximately 3,800 hectares. Severe February storms damaged infrastructure and caused up to 50% early strawberry losses. Daifressh is expanding blueberry tunnels in Poland from 10 hectares in 2024 to 100 hectares by 2030, showcasing profitability in marginal climates through protected cultivation. Dutch producers have adopted advanced substrate systems, which have tripled strawberry yields. In 2025, around 591 hectares are under protected cultivation, while open-field production is around 724 hectares[1]Source: Statistics Netherlands Staff, “Agricultural and Horticultural Production Statistics,” Statistics Netherlands, cbs.nl . Tunnel culture reduces fungicide sprays by lowering leaf wetness, aligning with European pesticide-reduction targets. Retailers reward this consistency with multi-year contracts that smaller open-field farms struggle to secure.

Expansion of Mechanized Harvesting Technologies

Mechanized harvesting directly shapes the Europe blueberry market by easing the region’s most acute constraint, seasonal labor. Over-the-row pickers reduce harvesting labor from 120 person-hours to 15 machine-hours per hectare, helping growers in Poland, Spain, and Italy stabilize costs and stay competitive despite wage inflation within the Jagoda Jps. European growers are using mechanical harvesters with soft-robotic grippers from the International Federation of Adapted Physical Activity (IFAPA) and vibration-tuned models from the University of Turin, reducing damage rates to 4.5% and meeting private-label standards for the fresh market. Nurseries such as Fall Creek now breed uniform-ripening cultivars for one-pass mechanical picking, a shift that raises pack-out efficiency, extends shelf life, and trims shrink, all of which bolster growers’ margins in a market where retailers negotiate on delivered cost per clamshell fallcreeknursery.com. As mechanization scales across flat Polish farms and gradually penetrates Spain’s sloped Huelva orchards, labor-related volatility eases, reinforcing the supply reliability that European supermarkets demand and underpinning continued regional output growth.

Growing Demand for Antioxidant-Rich Snack Ingredients

German shoppers consumed 1.2 kilograms per capita in 2025 as retailers marketed blueberries as cognitive and cardiovascular aids[2]Source: Eurostat Data Team, “Crops and Livestock Database,” Eurostat, ec.europa.eu . Food manufacturers have reformulated yogurt, cereal bars, and smoothie packs to include natural anthocyanins, with processed blueberry ingredients anticipated to comprise 22% of the European market value by 2025. United Kingdom campaigns linked daily portions to science-backed benefits, lifting household penetration to a trend of 60%. I Fresh-market distributors increasingly prioritize varieties with extended shelf life and strong visual appeal, strengthening year‑round programs with retailers. Although seasonal price fluctuations remain, growers value the reliable retail programs that provide a stable demand baseline and greater planning security.

European Union Specialty-Crop Financial Support Programs

Under the 2023–2027 Common Agricultural Policy (CAP), eco-schemes allocate EUR 8.9 billion (USD 10.47 billion) annually to support sustainable practices like drip irrigation and integrated pest management. High-value crops, such as blueberries, attract significant investment to meet European Union (EU) Green Deal objective[3]Source: Directorate-General for Agriculture and Rural Development, “Food, Farming and Fisheries Portal,” European Commission, ec.europa.eu. The Junta de Andalucía allocated subsidies covering 40% of capital costs for tunnel modernization across a designated 1,200 hectares in 2024. These subsidies are conditional upon farms obtaining LEAF or Global Good Agricultural Practices GlobalG.A.P. certification to comply with European Union (EU) sustainability requirements. Poland has allocated a significant portion of its EUR 823 million (USD 967.88 million) Common Agricultural Policy (CAP) processing budget and Knowledge Process Outsourcing (KPO) funds to modernize cold storage and harvesting equipment, boosting its record exports to Germany, which exceeded EUR 8 billion (USD 9.41 billion) in the first half of 2025. France backed varietal nurseries to double national output by 2030. Compliance costs for water audits and biodiversity buffers squeeze smallholders, pushing acreage toward firms with administrative scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages during peak harvest windows | -1.1% | United Kingdom, Poland, Spain, Germany, France, Italy, and the Netherlands | Short term (≤ 2 years) |

| Rising incidence of mummy-berry and scorch virus | -0.7% | Poland, Germany, the Netherlands, Italy, Switzerland, Spain, and France | Medium term (2-4 years) |

| Farm-gate price volatility from off-season import surges | -0.9% | Spain, the Netherlands, Germany, the United Kingdom, France, Italy, and Poland | Short term (≤ 2 years) |

| Stricter water-use regulations in southern Europe | -0.6% | Spain, Italy, and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages During Peak Harvest Windows

Irregular border crossings into the European Union (EU) dropped by 22% in 2025, but the agricultural sector still faces a labor shortage. Consequently, Italy and the United Kingdom have raised seasonal worker quotas to record levels to sustain harvest productivity. In 2024, United Kingdom farms left 12% of their fruit unharvested due to 8,500 unfilled seasonal worker vacancies, prompting 71% of growers to invest in automation and Agri-Tech despite high initial costs. Poland relied on Ukrainian workers, whose numbers dropped sharply after wartime mobilization, while German vegetables lured pickers with higher hourly pay. Moroccan visa delays for the early 2026 harvest led some Huelva producers to offer premiums of up to EUR 12 (USD 14.11) per hour, reducing profit margins by an estimated 18%.

Rising Incidence of Mummy-Berry and Scorch Virus

Blueberry scorch virus is a key phytosanitary concern in Poland. The industry focuses on vector control and testing resistant varieties to sustain its 12,500-hectare production through 2026. Germany documented outbreaks in Lower Saxony and Bavaria that prompted neonicotinoid-free aphid programs, increasing operating costs. The mummy-berry fungus threatens blueberry production in the United Kingdom, France, and the Netherlands, with fungicide applications costing GBP 450 (USD 608) per hectare to prevent yield losses of up to 50%. Italian research showed infection peaks during bloom, but many small farms lack weather stations for precise sprays. Retail audits penalize orchards with repeat infections, jeopardizing long-term contracts and accelerating exits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Germany remains the consumption engine, accounting for a 24.8% share in the Europe blueberry market size, and is anticipated to register the fastest growth at 9.5% CAGR by 2031. The growing import accounting for around 34,600 metric tons to satisfy demand for functional snacking, while domestic acreage stabilizes under 8,500 hectares. Spain retained leadership with 31.2% production share in 2025, and harvests of 66,600 metric tons that feed winter exports, yet strict irrigation caps on the Doñana aquifer threaten expansion and raise compliance costs. Poland leads European blueberry production, with annual growth of 25% over the past few years. The industry focuses on covered cultivation and mechanization across 13,000 hectares to boost exports to Germany and the United Kingdom. The Netherlands, Europe’s primary logistics hub, imports over 87,000 metric tons of blueberries, projected to reach 114,000 metric tons by 2026. Of this, 88% is re-exported, shaping regional price signals and supply chains.

France pursues subsidy-driven plans to double output by 2030 and leans on organic niches to win shelf space. The United Kingdom’s reliance on Spanish and Polish fruit persists as local labor shortages curb acreage growth despite retailer backing. Italy adds capacity in Piedmont and Veneto, but yields decline due to water caps and drought stress along the Po River. Portugal and Romania offer low-cost expansion sites for integrated groups and breeders targeting Central Europe.

Northern regions benefit from ample rainfall and fewer irrigation rules, drawing investment away from drought-prone southern Spain and Italy. Eastern Europe gains traction as supply chain diversification hedges import volatility from Southern Hemisphere origins. Logistics corridors anchored in Rotterdam and Hamburg shorten lead times, enabling retailers to better calibrate supply to weekly promotions. Over the forecast, acreage migrates northward while southern leaders protect share through premium genetics and organic certification.

Competitive Landscape

The combined top five account for the majority of Europe blueberry market share, leaving ample room for cooperatives that specialize in niche varieties or organic premiums. Driscoll’s led the Europe blueberry market with a significant revenue share in 2025 by coupling Iberian and Dutch packhouses with its 2022 purchase of Berry Gardens United Kingdom, which added local grower alliances and new export routes. Hortifrut followed, with its acquisition of Atlantic Blue for EUR 241 million (USD 254 million), lifting regional volume by 25% in 2024 and supporting the NaturAll on-the-branch launch targeting premium retailers. Together, the two giants secure direct-retailer contracts and integrate breeding, farming, packing, and marketing to protect margins.

The September 2024 merger of Agroberries and BerryWorld, backed by Continental Grain, created the second-largest global berry supplier with 150,000 metric tons throughput and 3,000 hectares under management. Surexport assembled 1,600 hectares across Spain, Portugal, and Morocco through three 2023 deals and built an automated Huelva facility to chase private-label growth. BayWa and Nufri formed a joint venture to commercialize VentureFruit genetics on 120 hectares that aim for December harvests before Peruvian volumes arrive. MerrryBerry in Romania expanded capacity and sorting capability to supply Central European supermarkets.

Companies expand their geographic footprints to hedge weather risk and secure year-round supply, while investments in renewable energy and water audits support retailer sustainability scorecards. Breeding programs focus on machine-harvest traits and flavor stability, leveraging genotyping advances from the United States Department of Agriculture Research Service that cut development cycles to seven years. Capital inflows from pension funds such as PSP Investments, now holding 62.04% of Hortifrut, signal confidence in scale players that tie genetics to distribution.

Recent Industry Developments

- January 2026: The newly formed Ukrainian Blueberry Growers Association united 40 producers cultivating 1,700 hectares to standardize quality and boost exports. Collective marketing and certification efforts position Ukraine to supply larger contract volumes into the European winter window, increasing supply diversity and price competition.

- May 2025: Sant'Orsola unveiled Residuo Zero-certified blackberries alongside premium blueberry and raspberry packs at Macfrut 2025’s Berry Area. The expanded product mix and pesticide-free label raise the competitive bar in Italy’s fresh segment and should stimulate retail shelf space for high-value berries.

- January 2025: Romania’s Agricrafters announced plans to scale a premium Sekoya blueberry farm from 62 hectares to 1,000 hectares through new genetics and pot cultivation systems. This acreage surge could lift Romania’s export capacity by 1,500 metric tons within five years and intensify regional supply during the July–August peak.

Europe Blueberry Market Report Scope

Blueberry is a small, pulpy, edible fruit that is bright-colored and sweet and sour in taste. It comes from the genus Vaccinium (family Ericaceae). Blueberries are a good source of fiber, antioxidants, vitamin C, vitamin K, iron, and manganese.

The European blueberry market is segmented by geography (Spain, Poland, Germany, Netherlands, United Kingdom, France, and Italy). The report offers an analysis of production (volume), consumption (value and volume), import (value and volume), export (value and volume), and price trend analysis. The report offers the market size and forecasts in terms of value (USD) and volume (metric tons) for all the above segments.

By Geography

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Poland | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| France | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis |

| By Geography | Spain | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Poland | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Netherlands | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

Key Questions Answered in the Report

What is the projected value of the Europe blueberry market in 2031?

The Europe blueberry market is forecast to reach USD 5.3 billion by 2031.

Which country consumes the most blueberries in Europe?

Germany leads consumption, accounting for 24.8% of regional volume in 2025.

Why are tunnel systems important for European blueberry growers?

Tunnels extend harvest from May to November, protect against weather, and help secure premium winter pricing.

How severe are labor shortages for European blueberry farms?

In 2024, farms across Europe lacked thousands of seasonal workers, leaving up to 12% of fruit unharvested in the United Kingdom.

Which segment of demand is growing fastest?

Industrial users in yogurt, cereal, and smoothie applications are increasing purchases at a 9.5% annual rate.

What is the key restraint on Spanish production growth?

Stricter water-use rules on the Doñana aquifer have cut irrigation allowances by 15% and could remove 800 hectares by 2028.

Page last updated on: