Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

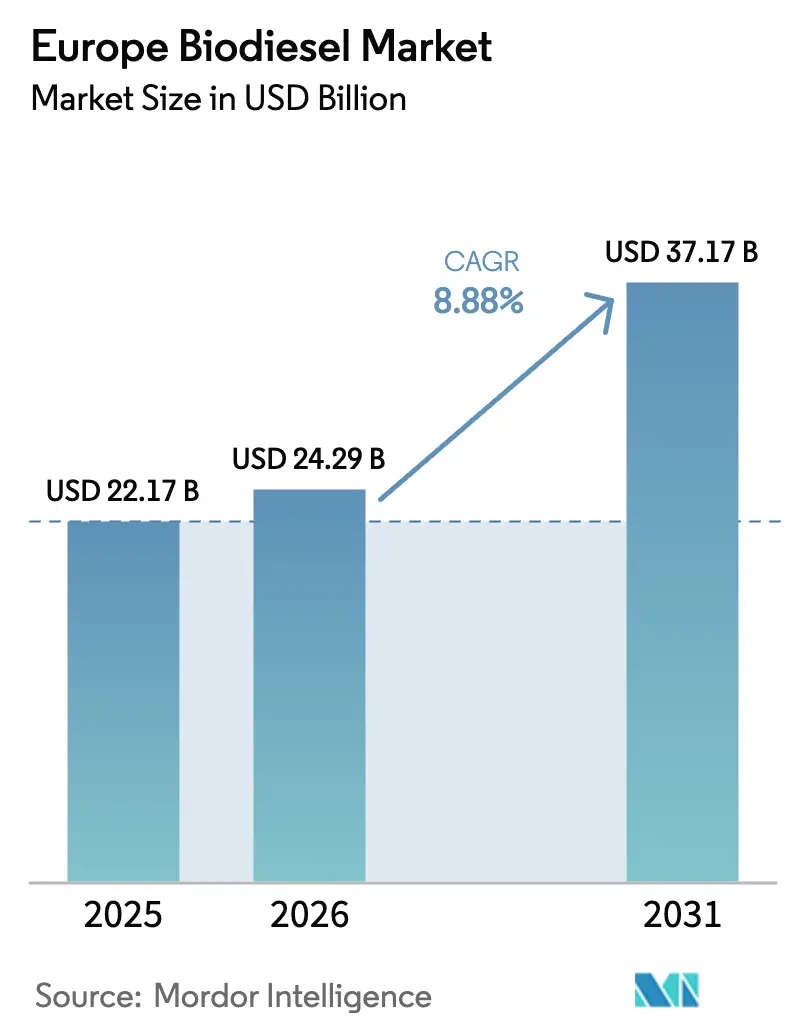

| Base Year Market Size (2025) | USD 22.17 Billion |

| Market Size (2026) | USD 24.29 Billion |

| Market Size (2031) | USD 37.17 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Biodiesel Market Analysis by Mordor Intelligence

The Europe Biodiesel Market size is expected to grow from USD 22.17 billion in 2025 to USD 24.29 billion in 2026 and is forecast to reach USD 37.17 billion by 2031 at 8.88% CAGR over 2026-2031.

Demand growth is anchored in the Renewable Energy Directive III, which double-counts waste oils, and in FuelEU Maritime rules that open a bunker-fuel outlet for FAME and HVO blends. Rapeseed oil continues to dominate feedstock selection because its well-established crushing base in Germany and France keeps delivering costs below imports of soybean and palm oils.[1]Bloomberg, “Energy Markets,” bloomberg.com At the same time, animal fats and used cooking oil (UCO) enjoy a regulatory premium that lifts their spot prices and draws new collection capacity, while OEM certifications for B30 and B100 engines are unlocking higher-blend demand from heavy-duty fleets.[2]European Automobile Manufacturers Association, “ACEA Position Papers,” acea.auto Competitive conditions are shifting as integrated refiners retrofit petroleum units for co-processing, compressing margins for standalone plants, and accelerating consolidation in the European biodiesel market.

Key Report Takeaways

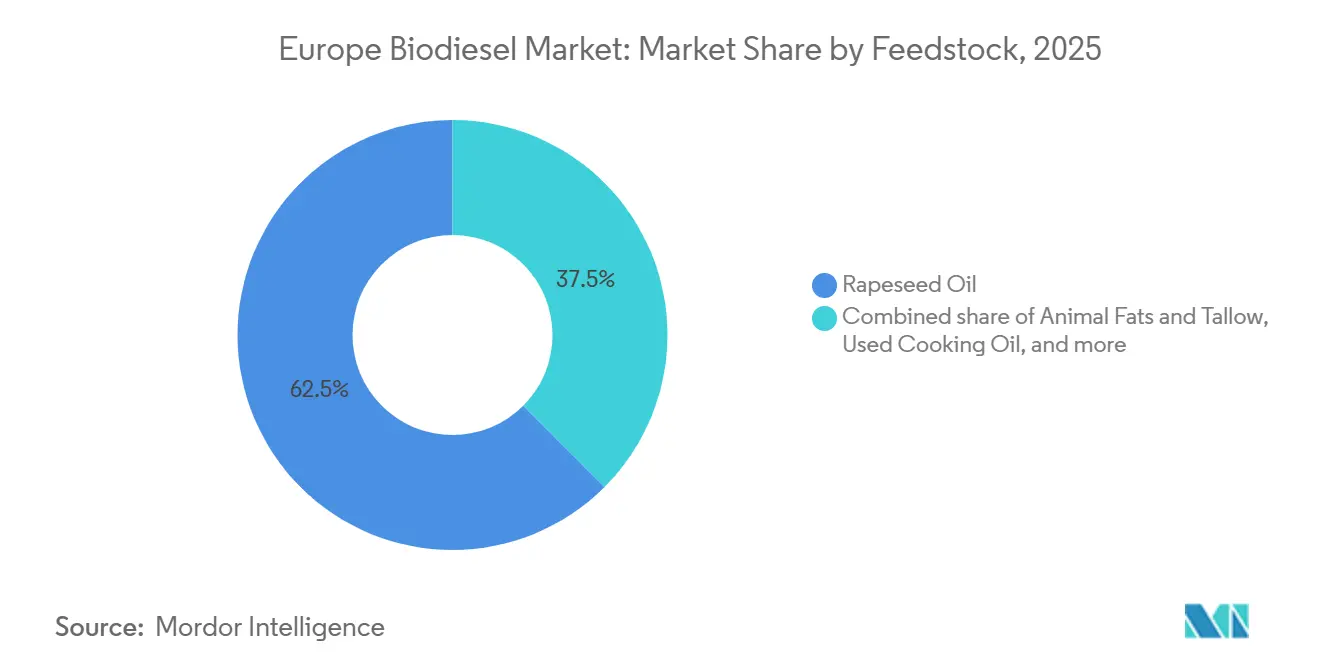

- By feedstock, rapeseed oil accounted for 62.5% of Europe's biodiesel market share in 2025, whereas animal fats and tallow are set to post the fastest expansion at a 12.5% CAGR through 2031.

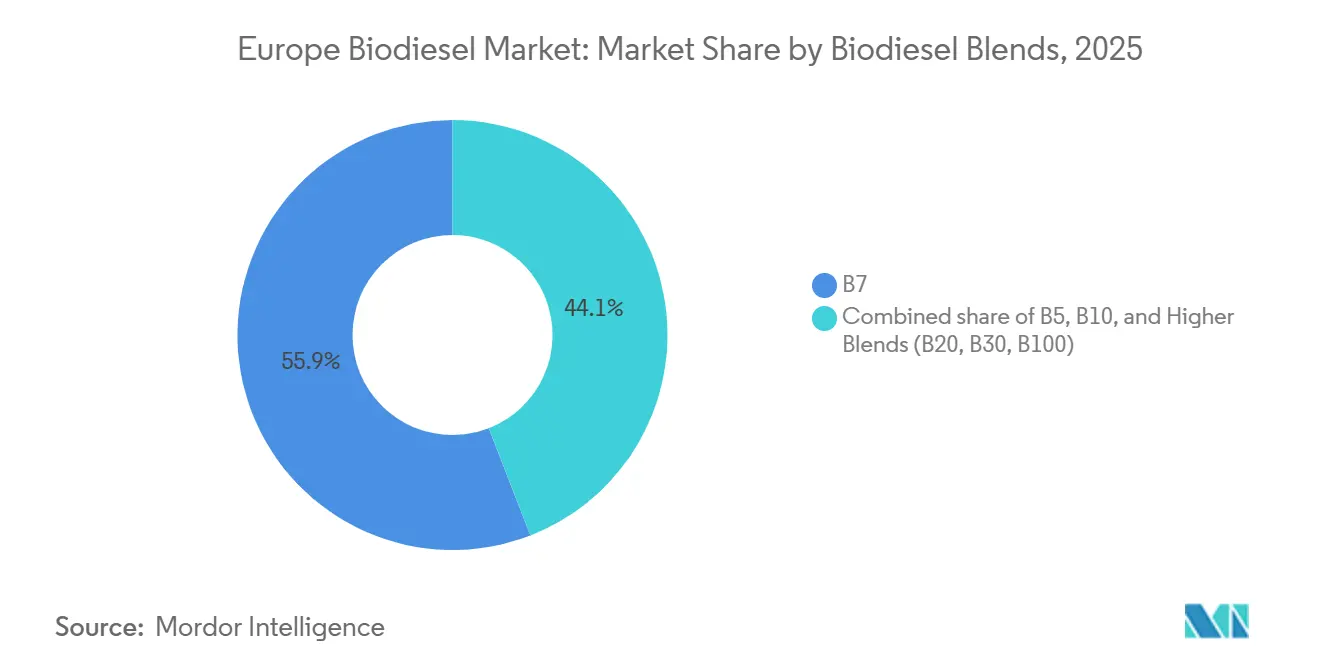

- By blend, B7 held 55.9% of consumption in 2025, but higher blends (B20, B30, B100) are forecast to rise at a 19.5% CAGR to 2031.

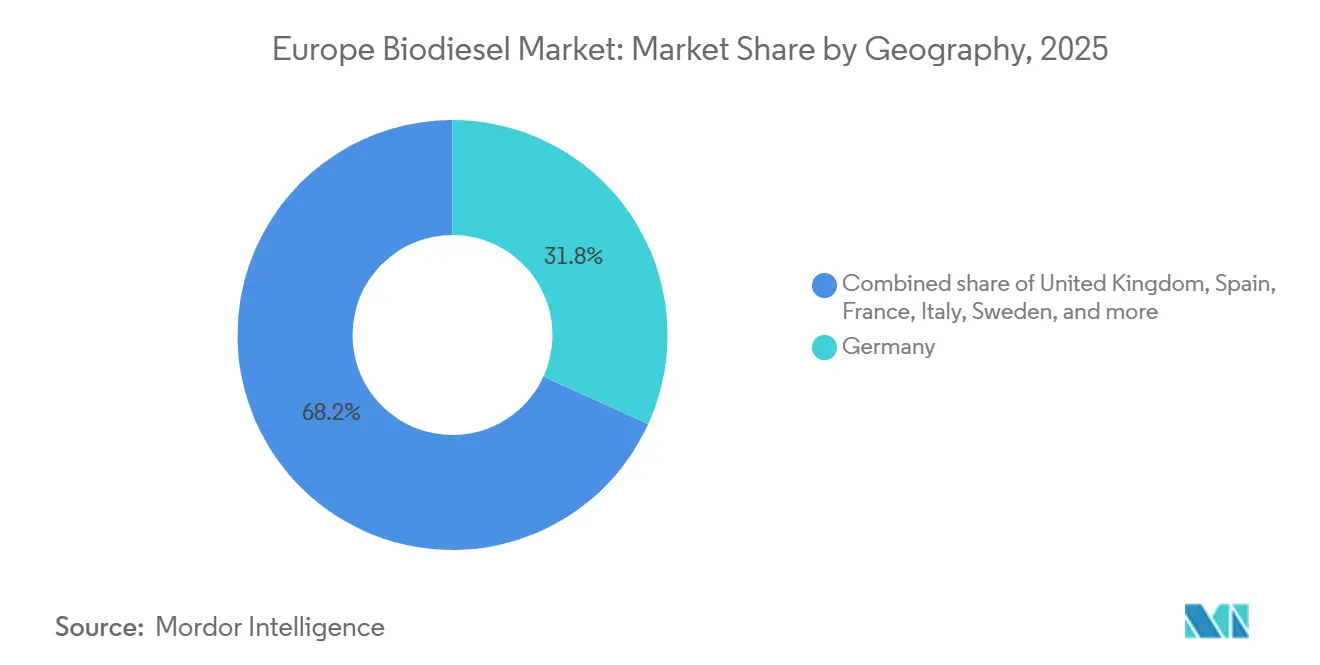

- By geography, Germany led with a 31.8% share in 2025, while the United Kingdom is projected to grow at a 14.1% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Biodiesel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapeseed-oil cost advantage versus competing low-carbon fuels | 1.20% | Germany, France, Poland, Central Europe | Medium term (2-4 years) |

| RED III double-counting that turbo-charges waste-oil demand | 2.10% | EU-wide, strongest in Netherlands, Spain, UK | Long term (≥ 4 years) |

| Record HVO capacity build-out across Spain, France & the Nordics | 1.80% | Spain, France, Finland, Sweden, Netherlands | Medium term (2-4 years) |

| Maritime FuelEU bunker demand for FAME/HVO blends | 0.90% | Netherlands, Spain, Italy, Greece | Long term (≥ 4 years) |

| Export arbitrage to the United States after the 2024 price crash | 0.60% | Germany, Netherlands, Belgium | Short term (≤ 2 years) |

| OEM pre-approval of B30/B100 truck engines for EU ETS-road compliance | 1.40% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapeseed-Oil Cost Advantage Versus Competing Low-Carbon Fuels

Rapeseed oil traded at EUR 580-620 per tonne in early 2026, a EUR 60-100 discount to landed soybean oil, giving refiners a structural edge when producing FAME that meets EN 14214 specs. Logistics from French and German farms to nearby plants keep freight low, and the feedstock avoids the deforestation risk premiums tied to palm-derived biodiesel under RED III.[3]European Commission, “FuelEU Maritime Initiative,” climate.ec.europa.eu The resulting cost cushion of EUR 0.08-0.12 per liter versus fossil diesel supports blending mandates without extra subsidies. Weather volatility narrowed that margin in 2024-2025, when drought and flooding cut yields below 3.2 tonnes per hectare and lifted rapeseed prices above EUR 620 per tonne, showing how agronomic shocks can rapidly erode a seemingly durable advantage. Refiners then turned to soybean oil, but higher carbon-intensity scores under FuelEU shrank profitability and reinforced the value of local rapeseed when harvests normalize.

RED III Double-Counting That Turbo-Charges Waste-Oil Demand

Since November 2023, waste oils and animal fats earn double compliance credits toward national transport targets, effectively doubling their economic value. Spot UCO prices climbed from EUR 850 per tonne in early 2024 to EUR 1,150 by mid-2025 as refiners competed for limited supply.[4]Reuters, “Commodities News,” reuters.com Investors responded by expanding collection networks across Spain, Italy, and Poland, regions previously underserved by structured pick-up systems. The incentive also spurred fraudulent imports, prompting mandatory ISCC PLUS audits on all non-EU waste-lipid cargoes from January 2026. While the rule accelerates feedstock diversification, it tightens supply for road biodiesel as aviation mandates rise, forcing producers to balance rapeseed reliance with compliance credit economics.

Record HVO Capacity Build-Out Across Spain, France & the Nordics

European HVO capacity grew from 3.2 million tpy in 2023 to 5.8 million tpy by end-2025, led by Neste, TotalEnergies, Cepsa, and Scandinavian refiners. HVO’s higher cetane number of 75-85 versus 51-55 for FAME makes it the preferred drop-in fuel for marine and aviation users, and its production economics improve when co-located with existing hydrogen and heat-recovery assets. Capital intensity averages EUR 150-200 million per 100,000 tpy, favoring integrated majors that retrofit petroleum units rather than build greenfield plants. By 2027, HVO facilities are expected to absorb 35-40% of Europe’s waste-lipid stream, up from 22% in 2024, shifting feedstock away from traditional FAME producers. This tilt alters pricing power in the European biodiesel market as standalone players scramble for supply or pivot toward specialty blends.

Maritime FuelEU Bunker Demand for FAME/HVO Blends

FuelEU Maritime imposed a 2% greenhouse-gas-intensity cut on fuels supplied to ships from January 2025, scaling to 6% by 2030. Roughly 11,000 European short-sea and ro-ro vessels lack the capital to switch to LNG or electricity, so operators have turned to bio-blends. Early contracts with Maersk, CMA CGM, and Stena Line secured 1.2 million tonnes of biodiesel bunkers for delivery by 2026. Storage hubs in Rotterdam, Antwerp, Barcelona, and Piraeus have installed dedicated bio-fuel lines to prevent contamination, broadening logistical reach. Because FuelEU’s well-to-wake accounting favors waste-derived inputs, UCO demand gains an independent anchor beyond road transport, adding a durable pull on limited feedstock pools in the European biodiesel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapeseed supply crunch from 2024-2026 harvest deficits | -0.80% | France, Germany, Poland, Romania | Short term (≤ 2 years) |

| Fraudulent UCO imports triggering tighter traceability audits | -0.50% | EU-wide, focus in Germany, Netherlands | Medium term (2-4 years) |

| Fast-tracking of battery-electric vans under AFIR | -0.40% | Germany, France, Netherlands, UK | Long term (≥ 4 years) |

| SAF mandates cannibalizing waste-lipid pools from 2027 | -1.10% | EU-wide, acute in France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapeseed Supply Crunch From 2024-2026 Harvest Deficits

Crop shortfalls cut European rapeseed output to 16.8 million tonnes in 2024-2025, versus 18.2 million tonnes two years earlier, lifting oil prices above EUR 620 per tonne. The squeeze forced refiners to import soybean oil that carries higher lifecycle emissions, reducing margin under RED III rules. Surpluses from Poland and Romania offset only part of the deficit. The episode underscored the need to diversify feedstocks and highlighted yield risk in a warming climate. Continued weather volatility is likely to keep rapeseed costs elevated into 2027, muting growth for the crop-based tier of the European biodiesel market.

SAF Mandates Cannibalizing Waste-Lipid Pools From 2027

The EU mandates a minimum 2% sustainable aviation fuel share in 2027, rising steeply thereafter, diverting an estimated 15-20% of waste-lipid volume away from road biodiesel. Airlines favor hydroprocessed esters that use the same UCO and tallow inputs prized by biodiesel refiners. Competition for feedstock is expected to widen price spreads and compress margins for road-fuel producers without captive supply. Refiners with integrated HVO capacity may pivot to aviation, while smaller FAME plants could face feedstock rationing. This redistribution is poised to reshape supply chains faster than refinery economics alone would suggest, adding volatility to the European biodiesel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Waste Lipids Gain Despite Rapeseed Dominance

Rapeseed retained 62.5% of the 2025 volume, equal to 13.8 million tonnes out of a 22 million tonne pool, underlining its entrenched position in the European biodiesel market for feedstocks. Yet animal fats and tallow are forecast to expand at a 12.5% CAGR through 2031, outpacing every other input. UCO sits second today but faces traceability scrutiny after customs uncovered adulterated imports in 2024. Soybean and palm oils together stay below 10% because carbon-intensity penalties and logistical costs blunt their appeal. Sunflower oil experienced a temporary bump during the rapeseed shortfall, though its high iodine number limits winter blending in northern Europe. Advanced lipids such as algae remain below 1%, confined to pilot plants that have yet to hit commercial scale.

Waste-lipid valuation has doubled since 2023 on RED III credits, sparking investment in collection fleets across southern and eastern Europe. However, the 2027 aviation mandate threatens to siphon 15-20% of that pool, tightening road-fuel supply and lifting volatility. Producers with vertically integrated waste-oil sourcing enjoy premium margins, while spot-market buyers face elevated credit risk. The tussle between rapeseed stability and waste-lipid incentives will determine the next phase of the European biodiesel market, with dual-feedstock flexibility emerging as a key competitive lever.

By Biodiesel Blends: Higher Concentrations Accelerate

B7 represented 55.9% of blended road diesel in 2025, maintaining its role as the standard tier within national mandates across much of the European biodiesel market size for blends. Higher blends (B20, B30, B100) are projected to rise at a 19.5% CAGR, powered by OEM warranties and looming EU ETS-road costs. Germany, France, and the Benelux region already support B10 retail pumps, and logistics firms such as DHL and DB Schenker have locked in B30 contracts to hedge carbon exposure.

OEM approvals issued in 2024-2025 eliminated warranty fears, enabling fleets to adopt B30 and, for captive depots, B100 that bypasses cold-flow constraints. FuelEU Maritime adds another outlet, with ro-ro operators choosing B20-B30 mixes to meet 2025 compliance at minimal capex. By 2028, higher blends could capture 20% of heavy-duty diesel demand, carving out a premium tier less sensitive to pump-price swings. This bifurcation splits the European biodiesel market into a commodity B7 segment and a value-added high-blend channel, each with distinct feedstock and pricing dynamics.

Geography Analysis

Germany captured 31.8% of the European biodiesel market in 2025, supported by 2.2 million tonnes of annual capacity and long-standing blending rules. Growth is slowing, though, because the crop-based cap nears its 7% ceiling and battery-electric vans erode B10 demand in cities. France and Spain are rising on the back of new HVO sites at La Mède and Huelva that serve both domestic mandates and export channels. Italy relies on Eni’s Venice and Gela co-processing hubs, which supply multi-feedstock diesel at lower cost than standalone FAME plants.

The United Kingdom is the fastest-growing market, heading for a 14.1% CAGR through 2031 as tighter RTFO rules boost demand for waste-based biodiesel and encourage investments in UCO import terminals at Immingham and Southampton. The Netherlands, while smaller, acts as Europe’s trading hub, with Rotterdam storing volumes that move into Germany, Belgium, and the UK. Poland’s rapeseed surplus underpins new crushing projects, while Sweden and Finland exploit forestry residues to produce tall-oil biodiesel that qualifies for RED III double-counting.

Diverging policy ambition is reshaping the map. Germany’s share may plateau as electrification in light vehicles advances, whereas the UK and Iberia could jointly rival Germany by 2030. Scandinavia, leveraging tall-oil and advanced feedstocks, supplies premium blends to marine and aviation users. Central and Eastern Europe grow in tandem with rapeseed yields and cross-border trade. Together, these shifts indicate a gradual diffusion of volume away from the historic German core toward a more balanced European biodiesel market.

Competitive Landscape

The top five suppliers, Neste, TotalEnergies, Eni, Repsol, and Cepsa, controlled roughly 40% of output in 2025, leaving the remaining 60% split among regional producers and trading houses. Integrated oil majors enjoy cost advantages by retrofitting existing hydrocrackers to co-process bio-feedstocks, reducing capital intensity to EUR 140 per tonne of annual capacity, about 30% below standalone builds. Neste’s 1.4 million tonne Rotterdam and Porvoo expansions typify this model, sharing hydrogen and utilities with adjacent fossil units for rapid scale-up.

Pure-play firms such as Verbio, Greenergy, and Argent Energy defend their share by signing long-term UCO contracts and adopting ISCC PLUS or REDcert systems to pass the stricter fraud audits introduced in 2026. Mid-tier players lacking feedstock integration face shrinking margins as waste-lipid prices rise and rapeseed supply tightens. White-space opportunities center on high-FFA pre-treatment, blockchain traceability, and modular HVO units licensed by technology houses like Honeywell UOP.

Patent filings in enzymatic transesterification and supercritical methanol rose 18% in 2024-2025, showing a race to improve yield and broaden feedstock options. Digital twins and AI-driven optimization help refiners tune processes to variable UCO quality, emerging as differentiators in a market where feedstock volatility is the chief risk. Consolidation is expected to continue as majors buy distressed assets or sign offtake contracts, further tightening the competitive field in the European biodiesel market.

Europe Biodiesel Industry Leaders

Neste Oyj

TotalEnergies SE

Eni S.p.A.

Greenergy International Ltd.

Verbio AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: TotalEnergies agreed to supply Maersk with 300,000 tonnes of FAME and HVO per year in a 10-year contract linked to Brent and UCO indices.

- March 2025: Eni and Saipem formed a JV to build a 200,000 tonne advanced biodiesel plant in Gela, using algal lipids and waste oils.

- March 2024: Neste announced a EUR 120 million program to add 400,000 tpy of renewable diesel at its Singapore site, with part of the output booked for Europe’s bunker market.

- February 2024: Cepsa commissioned a 500,000 tonne HVO unit in Huelva that draws UCO and tallow from Iberia and North Africa.

Europe Biodiesel Market Report Scope

Biodiesel is a renewable fuel derived from biomass sources, such as vegetable oils, animal fats, or recycled cooking oils. It is produced through transesterification, which involves chemically reacting the biomass feedstock with an alcohol (usually methanol or ethanol) in the presence of a catalyst, such as sodium hydroxide or potassium hydroxide.

Europe's biodiesel market is segmented by feedstock, biodiesel blends, and geography. By feedstock, the market is segmented into Coarse Grain, Sugar Crop, Vegetable Oil, and Others; by biodiesel blends, the market is segmented into B5, B20, B100, and higher blends. By geography, the market is segmented into Germany, France, Spain, the United Kingdom, Italy, the Netherlands, Poland, Sweden, Finland, and the Rest of Europe. The report also covers the market size and forecasts for the European biodiesel market across major regions.

By Feedstock

| Rapeseed Oil |

| Used Cooking Oil (UCO) |

| Soybean Oil |

| Palm Oil |

| Sunflower Oil |

| Animal Fats and Tallow |

| Algal and Other Advanced Feedstocks |

By Biodiesel Blends

| B5 |

| B7 |

| B10 |

| Higher Blends (B20, B30, B100) |

By Geography

| Germany |

| France |

| Spain |

| United Kingdom |

| Italy |

| Netherlands |

| Poland |

| Sweden |

| Finland |

| Rest of Europe |

| By Feedstock | Rapeseed Oil |

| Used Cooking Oil (UCO) | |

| Soybean Oil | |

| Palm Oil | |

| Sunflower Oil | |

| Animal Fats and Tallow | |

| Algal and Other Advanced Feedstocks | |

| By Biodiesel Blends | B5 |

| B7 | |

| B10 | |

| Higher Blends (B20, B30, B100) | |

| By Geography | Germany |

| France | |

| Spain | |

| United Kingdom | |

| Italy | |

| Netherlands | |

| Poland | |

| Sweden | |

| Finland | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe biodiesel market in 2026?

The market is valued at USD 24.29 billion in 2026, tracking the 8.88% growth path toward USD 37.17 billion by 2031.

Which feedstock leads production volumes?

Rapeseed oil supplies 62.5% of 2025 output, benefiting from local crop supply and established crushing assets.

What blend level is expanding the fastest?

Higher blends such as B20, B30, and B100 are rising at a 19.5% CAGR thanks to new OEM engine certifications.

Why is the United Kingdom the fastest-growing national market?

Post-Brexit tightening of the Renewable Transport Fuel Obligation and new waste-oil import terminals drive a 14.1% CAGR.

How are integrated oil majors gaining cost advantage?

They retrofit existing hydrocrackers to co-process bio-feedstocks, sharing hydrogen and utilities to cut capital intensity by roughly 30%.

What impact will SAF mandates have after 2027?

Sustainable aviation fuel rules will divert up to 20% of waste-lipid feedstock, tightening supply for road biodiesel refiners.

Page last updated on: