Market Overview

| Study Period | 2021 - 2031 |

|---|---|

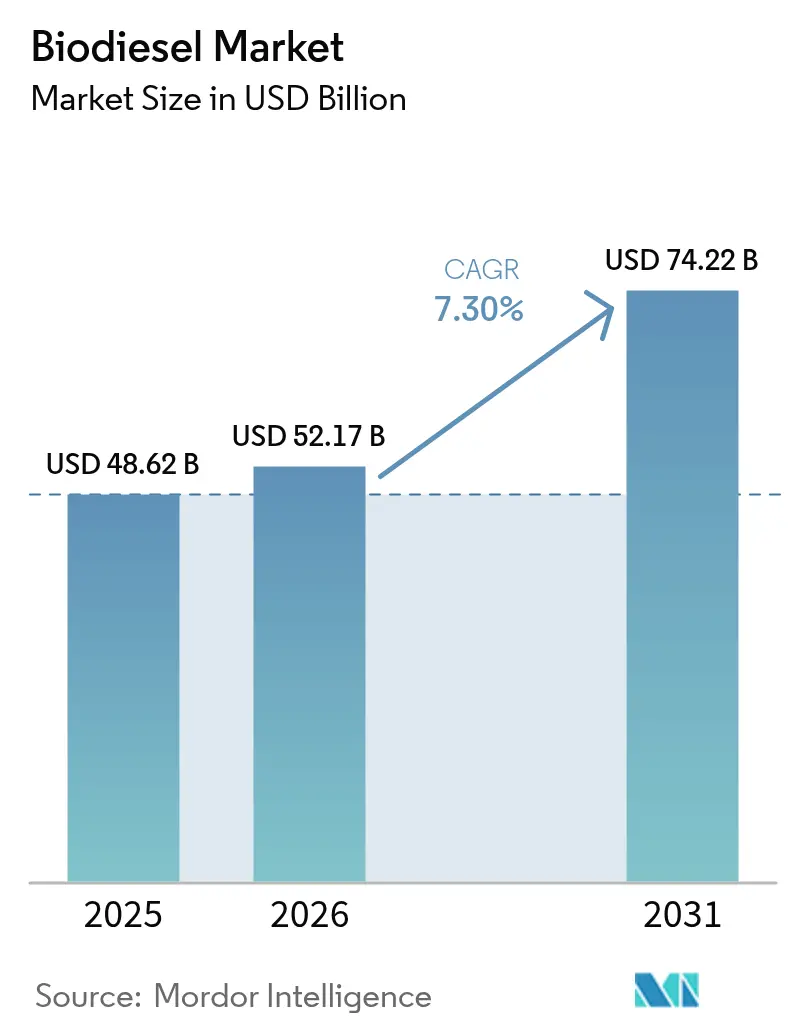

| Market Size (2026) | USD 52.17 Billion |

| Market Size (2031) | USD 74.22 Billion |

| Growth Rate (2026 - 2031) | 7.30% CAGR |

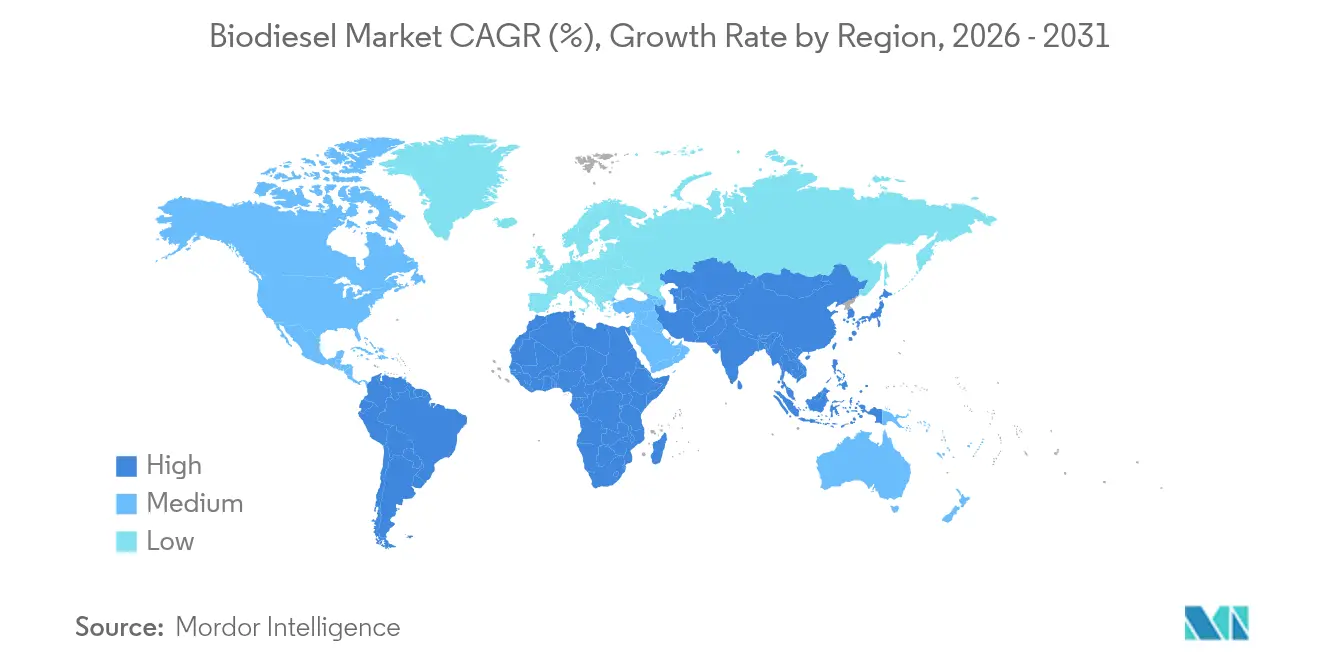

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biodiesel Market Analysis by Mordor Intelligence

The Biodiesel Market size was valued at USD 48.62 billion in 2025 and estimated to grow from USD 52.17 billion in 2026 to reach USD 74.22 billion by 2031, at a CAGR of 7.30% during the forecast period (2026-2031).

Demand is underpinned by tightening renewable-fuel blend mandates, oil-major investments in advanced hydro-treated vegetable-oil (HVO) capacity, and rising uptake across hard-to-abate industrial sectors. Europe anchors consumption through mature policy frameworks, while Asia-Pacific is expanding fastest as Indonesia, India, and China escalate national blend levels. Corporates are pursuing vertical integration to secure feedstock and optimise logistics, and the shift toward circular-economy waste inputs is reshaping cost structures and carbon-intensity profiles across the biodiesel market.

Key Report Takeaways

- By feedstock, vegetable oils led with 63.45% of the biodiesel market share in 2025; waste cooking oil and tallow are projected to post the fastest 10.15% CAGR through 2031.

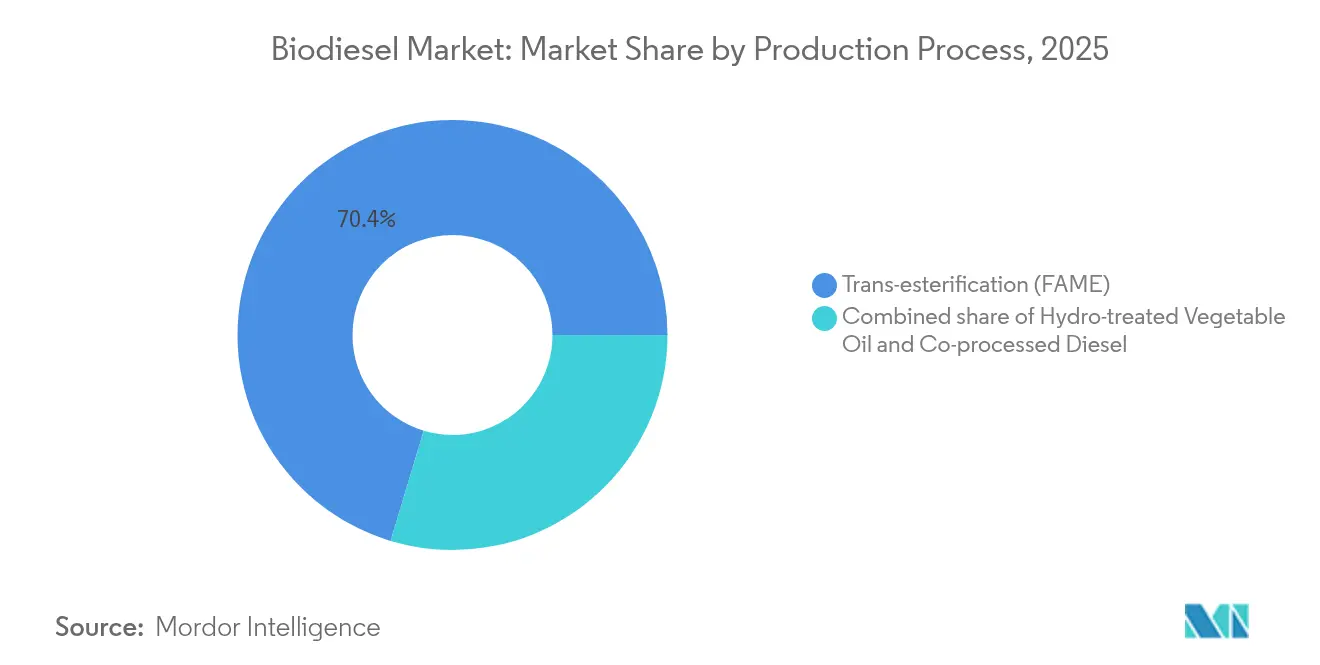

- By production process, trans-esterification accounted for 70.35% share of the biodiesel market size in 2025, while HVO is advancing at a 11.74% CAGR through 2031.

- By blend level, the B5 and below segment led with 47.58% biodiesel market share in 2025; B100 is forecast to expand at a 10.82% CAGR through 2031.

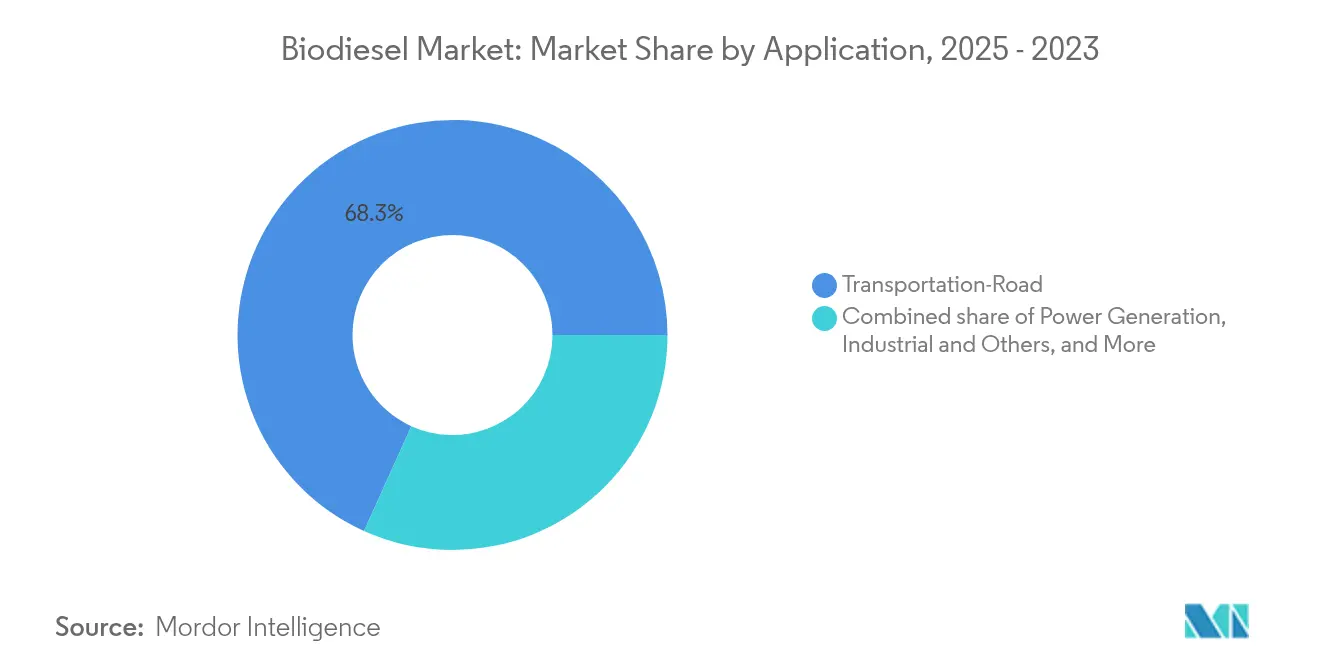

- By application, transportation-road retained a 68.25% share of the biodiesel market size in 2025, and industrial uses are expanding at a 12.58% CAGR through 2031.

- By geography, Europe commanded a 37.62% share of the biodiesel market in 2025; Asia-Pacific is registering the highest 10.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biodiesel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-fuel blend mandates expanding (B5 → B20) in U.S., Brazil, Indonesia, EU | 2.10% | North America, South America, APAC, Europe | Medium term (2-4 years) |

| Demand from hard-to-abate sectors (mining, marine, rail) seeking drop-in low-carbon fuels | 1.30% | Europe, North America with global spillover | Long term (≥ 4 years) |

| HVO/SAF capacity build-outs by oil majors lifting glycerin off-take | 1.80% | Europe, North America, emerging APAC | Medium term (2-4 years) |

| Waste- and residue-based feedstock credits (UCO, tallow) widening biodiesel-diesel margin | 1.20% | California, EU, Canada and other premium credit regions | Short term (≤ 2 years) |

| Co-processing technology lowering CAPEX via existing refineries | 0.90% | Refinery-dense regions worldwide | Medium term (2-4 years) |

| Carbon-intensity score premiums under LCFS & EU ETS | 0.70% | California, EU, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renewable-fuel Blend Mandates Expanding

National blend programmes are scaling rapidly, guaranteeing sizeable offtake volumes and underpinning long-term financing across the biodiesel market. Brazil’s Fuel-of-the-Future law raises the obligatory blend from B14 to B17 by 2027 and foresees B25 later in the decade, lifting domestic biodiesel use from 9.3 billion litres in 2024 to 12.3 billion litres by 2027.[1]D. Holt, “Brazil Fuel of the Future Law Boosts Biodiesel Blend,” agweb.com Indonesia is rolling out its B40 programme, while all EU member states must align with higher advanced biofuel quotas under RED-III. British Columbia now insists that 8% of diesel renewable content be produced domestically from April 2025, signalling how mandates increasingly favour local supply. Renewable Fuel Standard obligations remain in force in the United States and provide a dependable compliance baseline. These rules establish price floors, enabling producers to expand capacity and adopt efficiency-enhancing technologies.

Hard-to-Abate Sectors Seeking Drop-in Decarbonisation

Mining, marine, and rail operators' segments, where electrification lags, are adopting biodiesel blends to meet near-term carbon-reduction goals without infrastructure overhauls. Global mining firms spend roughly USD 7 billion annually on diesel equipment; switching to B20 or renewable diesel delivers 50–85% lifecycle emission cuts while lowering particulate outputs sharply.[2]Engine Technology Forum, “Biodiesel Reduces Mining Emissions,” engine-technology.org In Europe, Chevron Renewable Energy Group supplies EN 14214-grade fuel that cuts particulate matter in mines from 300-800 µg m³ to 50-200 µg m³. Marine uptake is growing through REG–Bunker Holding alliances to deploy B30, and freight rail trials show seamless engine compatibility. Willingness to pay decarbonisation premiums in these sectors supports higher-margin sales within the biodiesel market.

HVO and SAF Capacity Build-outs

Oil majors are investing heavily in HVO assets to harvest co-product value and create SAF supply chains, a trend reshaping competitive dynamics in the biodiesel industry. Neste lifted renewable aviation-fuel capacity to 1.5 million t pa in April 2025 and is enlarging its Rotterdam complex into the world’s largest renewable diesel and SAF facility by 2027.[3]Neste, “Annual Report 2025 – Renewable Products,” neste.com OMV’s EUR 200 million co-processing line at Schwechat converts 160,000 t of liquid biomass yearly, avoiding 360,000 t of fossil CO₂.[4]Euro-Petrole, “OMV Starts Schwechat Co-Processing Unit,” euro-petrole.com BP took full control of BP Bunge Bioenergia, yet shelved two greenfield SAF projects for portfolio optimisation. Premium-grade glycerin from HVO outputs further improves plant economics, reinforcing capital flows toward this pathway.

Waste- & Residue-based Feedstock Credits

Used cooking oil, tallow, and similar residues collect superior carbon credits under the Low Carbon Fuel Standards, widening the spread between biodiesel and fossil diesel margins. Imports of UCO into California rose markedly in 2024 as producers chased lower carbon-intensity scores, while waste inputs formed 88% of Neste’s renewable feedstock slate in Q2 2024. Brazil’s beef tallow exports jumped to 198,340 t in the first 11 months of 2023, doubling year-on-year, as overseas demand for low-CI feedstock increased. These incentives accelerate the biodiesel market pivot from edible oils toward circular-economy streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility (soy-oil, tallow) squeezes margins | −1.4% | Global, particularly high-output regions | Short term (≤ 2 years) |

| Land-use change scrutiny and EU RED-II food-crop cap | −0.8% | Europe with spillover to exporters | Medium term (2-4 years) |

| Oversupply of low-CI credits in U.S. LCFS | −0.6% | California and neighbouring states | Short term (≤ 2 years) |

| Electrification of light-duty fleets reducing diesel pool | −0.9% | Accelerating in mature markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

Soybean-oil quotations oscillated sharply through 2024 as Brazil’s higher blends drew more volumes, eroding producer margins and prompting output optimisation at several plants. UCO values approached virgin-oil parity once LCFS credits were incorporated, diluting expected cost advantages. Neste cited elevated feedstock costs as a principal factor behind depressed margins in 2024 despite flat diesel benchmarks. Climatic disruptions and ongoing food-versus-fuel tensions compound price uncertainty, compelling firms across the biodiesel market to diversify inputs or adopt hedging strategies where possible.

Land-use Change Scrutiny

EU RED-II caps traditional crop-based biofuels at 7% of transport energy and imposes strict land-use-change documentation, effectively narrowing the eligible pool of palm- and soy-derived esters for European customers. Compliance demands cradle-to-gate traceability, adding certification expense and limiting feedstock flexibility for exporters. Producers unable to verify low-ILUC status may face market exclusion, underscoring why waste-derived alternatives are gathering momentum inside the biodiesel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feedstock: Waste Streams Gathering Speed

Vegetable oils still delivered 63.45% of the 2025 supply, sustaining baseline volumes for the biodiesel market, yet their growth tempo is flattening as policymakers and buyers chase lower carbon-intensity scores. Palm oil dominates South-East Asia, whereas soybean oil prevails in the Americas, but each faces scrutiny over land-use risks.

Waste cooking oil and tallow are projected to expand at a 10.15% CAGR, well ahead of edible oils, thanks to premium LCFS credits and emerging advanced-biofuel quotas. Brazil’s beef-tallow exports, rising 144% year-on-year, signal widening global arbitrage. Algae-based oils and winter-canola pilots from the Neste–Bayer alliance illustrate the exploratory edge of feedstock R&D. Competition for residues is now sharpening, inserting new price volatility while steadily raising the sustainability bar across the biodiesel market.

By Production Process: HVO Ascendant

The familiar trans-esterification route retained 70.35% share of the biodiesel market size in 2025 by virtue of its comparatively light capital burden and well-established supply chain compatibility. It remains the mainstay for many small-to-mid producers, particularly in developing economies with limited refinery integration.

However, HVO capacity is forecast to clock a 11.74% CAGR as oil majors leverage existing hydrotreaters to create fungible diesel, SAF, and naphtha streams. The biodiesel market benefits because HVO commands infrastructure parity with fossil diesel, enabling B100 equivalents without cold-flow problems. Higher-value technical-grade glycerin and flexible feedstock windows further enhance plant returns, spurring a pipeline of conversions and greenfields across Europe, North America, and Asia-Pacific.

By Blend Level: High-Concentration Uptake Rising

B5-and-below products represented 47.58% of 2025 volumes, serving the mainstream automotive fleet with minimal infrastructure change. These blends underpin mass-market stability within the biodiesel market because almost all diesel vehicles can use them under manufacturer warranties.

Mandated jumps to B20 in markets such as Indonesia and niche B100 rollouts for mining and marine customers are pivoting growth toward higher blends. Pure biodiesel is set to climb at 10.82% CAGR through 2031. Operators adopting B30–B100 report lifecycle CO₂ reductions exceeding 80% and substantial particulate abatement, important metrics for ESG-oriented cargo owners and public procurement agencies.

By Application: Industrial Diversification Broadens Demand

Road transportation still commanded 68.25% of 2025 consumption, anchored by haulage and municipal fleet compliance rules. Electrification headwinds remain subdued in heavy freight, leaving a substantial diesel pool open for substitution.

Industrial, marine, rail, and power segments are forecast to increase at a 12.58% CAGR, signifying meaningful diversification of the biodiesel market. For instance, marine bunker suppliers in the Netherlands are now bunkering river-cruise fleets with B30 derived from waste oils. Remote mines are trialling B100 in gensets to reduce Scope 1 emissions without investing in grid upgrades. Such cross-sector adoption embeds biodiesel as a flexible decarbonisation lever beyond highway use.

Geography Analysis

Europe delivered 37.62% of global sales in 2025 and continues to reward low-carbon biodiesel through RED-III quotas, national carbon taxes, and subsidy schemes for waste-based feedstocks. Germany, France, and the United Kingdom each tightened blend obligations in 2025, and the Nordics are frontrunners in collecting municipal UCO for local processing, reinforcing regional circular-economy objectives. Sustainability certification remains stringent however, limiting feedstock choice and raising administrative overhead.

Asia-Pacific offers the fastest expansion path, showing a 10.02% CAGR projection to 2031 as Indonesia escalates toward B40, India allocates grants for capacity, and China integrates biodiesel into its dual-carbon roadmap. Accessible palm-oil supply, rising urban diesel demand, and supportive fiscal incentives make the region a strategic growth engine inside the biodiesel market. Nonetheless, export potential to Europe is checked by deforestation-linked rulings, compelling producers to upgrade traceability protocols.

North America holds mature infrastructure and policy stability via the U.S. Renewable Fuel Standard and an expanding patchwork of state-level Low Carbon Fuel Standards. Advanced credit trading deepens revenue pools, yet LCFS credit oversupply recently squeezed pricing. South America, led by Brazil’s trajectory toward B25, is simultaneously a feedstock powerhouse and a major internal market. Argentina’s producers navigate export tariffs but maintain competitiveness regionally through soybean-oil scale and established esterification expertise.

Competitive Landscape

Market concentration is increasing as integrated energy companies purchase specialist biodiesel firms and retrofit hydrotreaters for HVO output. Neste, Chevron Renewable Energy Group, and Archer Daniels Midland top the leaderboard through tight feedstock control, technology depth, and multi-regional distribution. Partnerships such as TotalEnergies with Cargill or Shell with Bunge create farm-to-fuel pipelines that hedge raw-material fluctuations.

Competitive advantage increasingly rests on lifecycle-emission credentials and flexibility to pivot between SAF, renewable diesel, and bio-naphtha depending on margin signals. Firms with refinery footprints fast-track co-processing to avoid greenfield CAPEX, whereas smaller independents carve niches in local waste-feedstock aggregations within the biodiesel market. Despite consolidation moves, new entrants continue to appear in emerging economies where domestic blends expand and local residue supply remains underutilised.

Intellectual-property development is centred on catalyst optimisation, glycerin valorisation, and pretreatment of high-FFA feedstocks. Licensing revenues and engineering-services contracts are now material profit streams for technology owners, adding layer to competitive dynamics.

Biodiesel Industry Leaders

Archer Daniels Midland Company

Wilmar International Ltd

Neste Oyj

Chevron Renewable Energy Group

Cargill

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Neste raised global SAF output capability to 1.5 million t pa and confirmed Rotterdam expansion to become the world’s largest renewable diesel and SAF site by 2027.

- April 2025: Aemetis India secured USD 31 million in biodiesel orders from state oil firms for delivery within 3 months, illustrating surging domestic demand.

- March 2025: British Columbia enforced a Canadian-content rule stipulating 8% domestically produced renewable diesel within the provincial blend mandate.

- January 2025: OMV inaugurated a EUR 200 million co-processing unit at Schwechat, converting 160,000 t pa of liquid biomass into HVO components.

Global Biodiesel Market Report Scope

Biodiesel is a renewable fuel from vegetable oils, animal fats, or cooking oils. It is produced through a chemical process called transesterification, which converts these feedstocks into a fuel that can be used in diesel engines without any modifications. Biodiesel is a cleaner-burning alternative to petroleum-based diesel fuel, as it produces lower emissions of greenhouse gases and air pollutants. It can be used independently or blended with petroleum diesel in varying proportions, depending on the desired properties and performance. Biodiesel is considered a sustainable and eco-friendly fuel option, as it reduces reliance on fossil fuels and helps decrease overall carbon emissions.

The biodiesel market is segmented by feedstock, application, and geography. By feedstock segment, the market is segmented into animal fat, vegetable oil, and other feedstocks. By application, the market is segmented into transportation, power generation, and other applications. The report also covers the market size and forecasts for the biodiesel market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Feedstock

| Vegetable Oils |

| Waste Cooking Oil and Tallow |

| Animal Fat |

| Algae and Novel Feedstocks |

By Production Process

| Trans-esterification (FAME) |

| Hydro-treated Vegetable Oil (HVO) |

| Co-processed/Co-refined Diesel |

By Blend Level

| B5 and Below |

| B6 to B20 |

| B100 |

By Application

| Transportation-Road |

| Transportation-Marine and Rail |

| Power Generation |

| Industrial and Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia & New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Feedstock | Vegetable Oils | |

| Waste Cooking Oil and Tallow | ||

| Animal Fat | ||

| Algae and Novel Feedstocks | ||

| By Production Process | Trans-esterification (FAME) | |

| Hydro-treated Vegetable Oil (HVO) | ||

| Co-processed/Co-refined Diesel | ||

| By Blend Level | B5 and Below | |

| B6 to B20 | ||

| B100 | ||

| By Application | Transportation-Road | |

| Transportation-Marine and Rail | ||

| Power Generation | ||

| Industrial and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia & New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the biodiesel market by 2031?

The biodiesel market size is forecast to reach USD 74.22 billion in 2031, expanding at a 7.30% CAGR over 2026-2031.

Which feedstock category is growing fastest?

Waste cooking oil and tallow are expected to post a 10.15% CAGR as low-carbon credit incentives make residue-based fuel more profitable.

Why is HVO production gaining momentum?

HVO offers drop-in compatibility with existing diesel infrastructure, yields high-value co-products, and is backed by major refiners investing in hydrotreatment upgrades.

How do blend mandates influence demand?

Mandatory B20 and higher programmes in markets such as Brazil and Indonesia guarantee long-term offtake volumes, underpinning capacity expansion and price stability.

What restrains biodiesel profitability?

Volatile soybean-oil prices, stringent EU land-use criteria, and oversupply of LCFS credits in California can compress margins for producers.

Which region presents the highest growth opportunity?

Asia-Pacific, led by Indonesia and India, is projected to register a 10.02% CAGR owing to expanding blend mandates and abundant regional feedstock.

Page last updated on: