Bread Improvers Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 1.8 Billion |

| Market Size (2030) | USD 2.47 Billion |

| Growth Rate (2025 - 2030) | 6.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

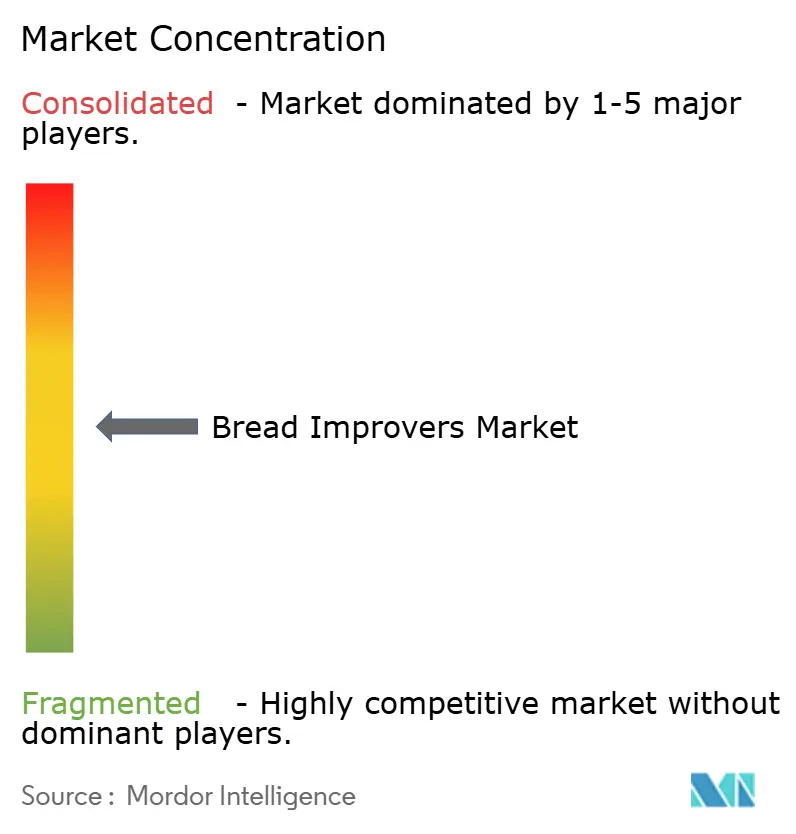

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bread Improvers Market Analysis by Mordor Intelligence

The bread improvers market size stands at USD 1.80 billion in 2025 and is on track to reach USD 2.47 billion by 2030, advancing at a 6.55% CAGR. This steady rise reflects how large bakeries and small craft operations alike rely on advanced blends to achieve consistent volume, texture, and shelf stability while meeting clean-label rules. Industrial automation, urban demand for premium convenience foods, and the spread of frozen dough technologies are widening the addressable customer base. Europe anchors global demand through its mature bakery infrastructure, but Asia-Pacific is attracting capacity expansion as disposable incomes rise and Western-style baked goods penetrate mass retail. Across ingredient categories, enzymes outpace emulsifiers in growth as biotechnology opens label-friendly routes to dough strengthening, freshness protection, and flavor enhancement. Meanwhile, precision liquid formats gain momentum in automated plants, and artisanal bakers adopt professional-grade systems that once belonged only in industrial lines.

Key Report Takeaways

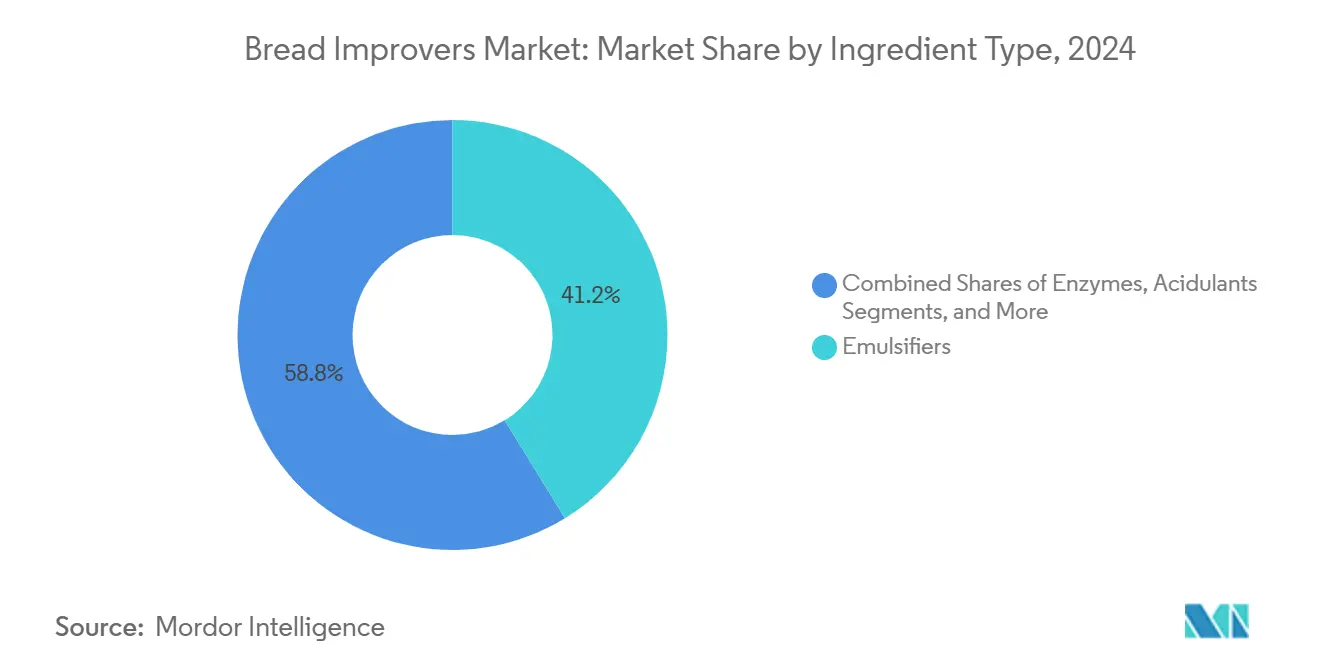

- By ingredient type, emulsifiers led with 41.23% of bread improvers market share in 2024, while enzymes are forecast to grow at a 7.23% CAGR to 2030.

- By form, powder products captured 55.46% market share in 2024; liquid formulations are projected to expand at a 6.89% CAGR through 2030.

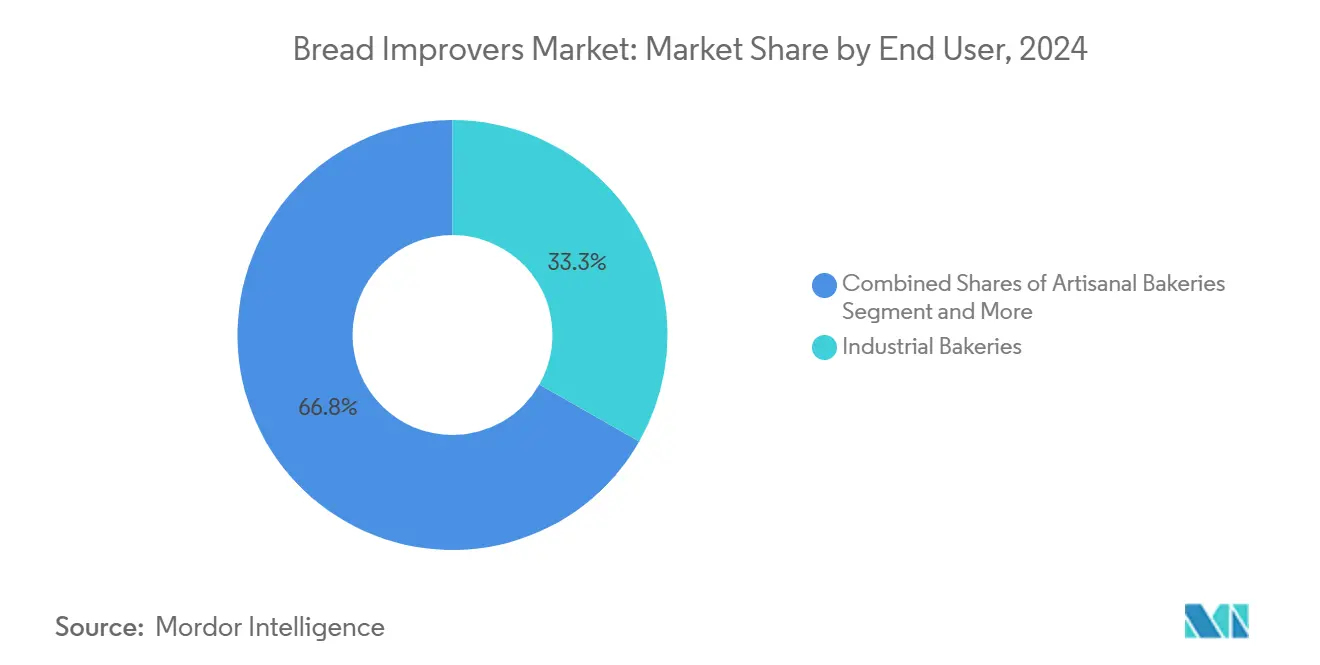

- By end user, industrial bakeries held 33.25% share of the bread improvers market in 2024, whereas artisanal bakeries are set to rise at a 7.23% CAGR over the forecast period.

- By application, bread accounted for 52.34% of the bread improvers market share in 2024, and pizza bases and flatbreads are advancing at a 7.45% CAGR to 2030.

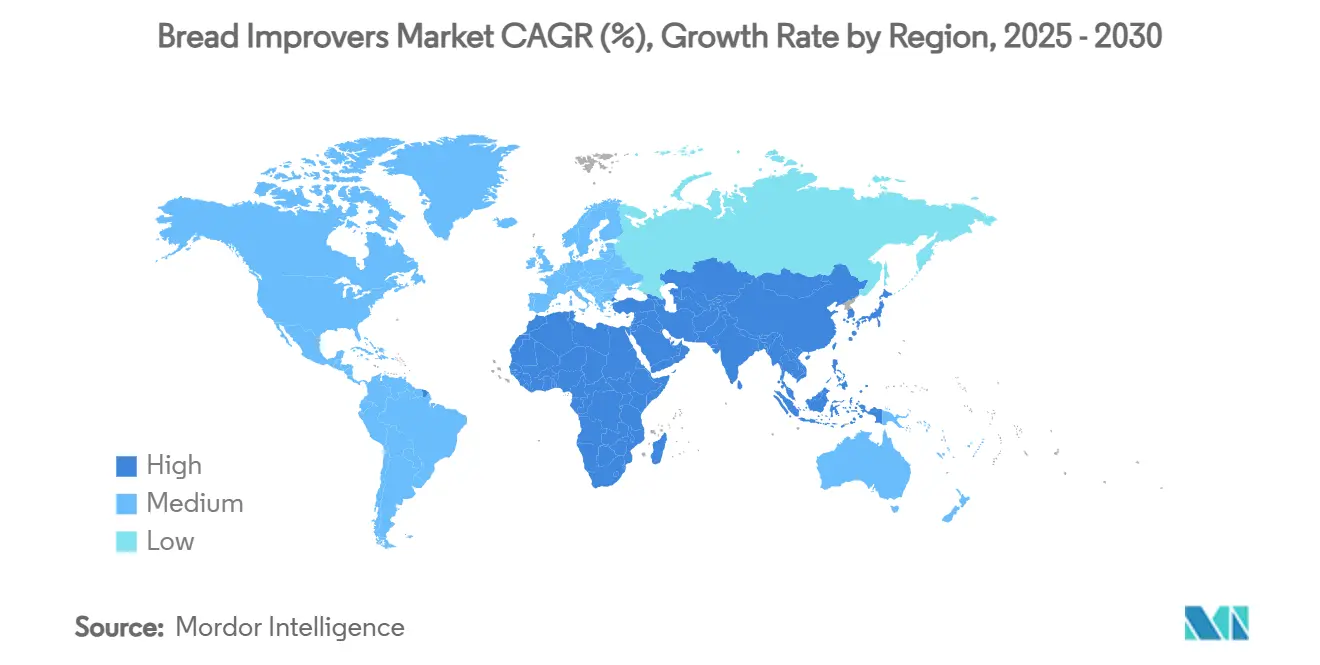

- By geography, Europe dominated with 35.67% share in 2024; Asia-Pacific is the fastest-growing region at a 7.78% CAGR to 2030.

Global Bread Improvers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience & premium bakery products | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing preference for clean-label, natural improvers | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Expansion of industrial-scale artisanal bread lines | +0.9% | Global, led by Europe & North America | Medium term (2-4 years) |

| Shelf-life extension needs in global bread supply chains | +1.1% | Global, critical in emerging markets | Short term (≤ 2 years) |

| Algorithm-driven on-demand improver formulation | +0.7% | Developed markets, gradual APAC adoption | Long term (≥ 4 years) |

| Adoption of heat-stable maltogenic amylase in frozen dough trade | +0.6% | Global, particularly North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenience & Premium Bakery Products

In 2024, 84% of bakery operators are set to invest in capacity, responding to a surge in demand for artisanal-quality products. This demand, however, presents a challenge: consumers want the authenticity of handcrafted goods but also seek consistent availability and a longer shelf life. The answer lies in advanced improver formulations that mimic traditional fermentation while ensuring industrial efficiency. These bread improvers allow manufacturers to capture the intricate flavors and textures of artisanal bread, sidestepping the time and variability challenges of traditional methods. Urban markets are witnessing pronounced growth in the premium segment, driven by consumers' readiness to pay more for perceived quality and convenience. As urbanization and the rise of dual-income households continue, this trend is poised for medium-term growth, emphasizing convenience without sacrificing quality.

Growing Preference for Clean-Label, Natural Improvers

Consumer research reveals that a significant 85% of US consumers now actively seek out products with recognizable ingredients, marking the clean-label movement's transition from a niche preference to a mainstream necessity. This consumer shift has spurred innovations in enzyme-based and fermentation-derived improvers, offering alternatives to synthetic additives without compromising performance. The European Union[1]European Commission, “Regulation (EC) No 1333/2008 on Food Additives,” ec.europa.eu, through its Regulation (EC) No 1333/2008, has intensified the push for natural alternatives. Companies, as highlighted by the European Commission, are pouring investments into biotechnology solutions that align with both regulatory mandates and consumer desires. As manufacturers aim to replace artificial preservatives while ensuring shelf stability, cultured dextrose and fermentation-based preservatives are emerging as popular choices. The clean-label trend wields significant influence in developed markets, bolstered by supportive regulatory frameworks and a consumer base well-versed in making informed choices. This momentum signifies a profound structural shift, poised to redefine product development and market strategies in the years to come.

Expansion of Industrial-Scale Artisanal Bread Lines

In 2024, 53% of bakery operators anticipate significant revenue boosts from premium product lines, highlighting a lucrative opportunity in the industrial scaling of artisanal bread production. Achieving this growth demands advanced improver systems that uphold the sensory traits of traditional methods while ensuring the consistency and efficiency of large-scale operations. Manufacturers are turning to advanced enzyme technologies, like maltogenic amylases and xylanases, to mimic the intricate biochemical processes of prolonged fermentation in a fraction of the time. The real challenge? Retaining the genuine flavor and texture that epitomize artisanal quality, all while satisfying the demands of industrial distribution in terms of volume and consistency. A testament to this trend is Puratos' S500 multipurpose bread improver, which harnesses enzyme technology for uniform baking results across varied production settings. As competition intensifies, this momentum is poised to continue, with manufacturers channeling investments into premium lines for enhanced margins and distinct market positioning.

Shelf-Life Extension Needs in Global Bread Supply Chains

As global supply chains grow more complex, the need for shelf-life extension technologies has become paramount. Bread manufacturers, in particular, grapple with the challenge of preserving product quality amidst extended distribution networks and fluctuating storage conditions. This challenge is heightened in emerging markets, where underdeveloped cold chain infrastructures present hurdles. However, this gap also opens doors for improvers that can ensure freshness and safety without the need for refrigeration. Novozymes' Novamyl® BestBite solution showcases the promise of enzyme-based shelf-life extensions. Studies reveal that consumers perceive bread treated with this product to be just as appealing after 15 days as it is when fresh. Furthermore, the rise of the frozen dough trade has led to the development of freeze-thaw stable starches via enzymatic modification. This advancement allows manufacturers to centralize production while ensuring consistent quality across varied retail settings. As supply chain disruptions persist, pushing manufacturers to seek technological solutions, these advancements in shelf-life extension technologies emerge as a significant growth catalyst.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile pricing of emulsifier & enzyme raw materials | -0.4% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Stringent additive regulations in US & EU | -0.3% | North America & Europe, with spillover effects globally | Medium term (2-4 years) |

| Sourdough fermentation as "label-free" improver substitute | -0.2% | Developed markets, premium segments | Long term (≥ 4 years) |

| Supply chain fragility for specialty enzyme cofactors | -0.1% | Global, concentrated in biotechnology hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Pricing of Emulsifier & Enzyme Raw Materials

Market growth faces a significant hurdle due to raw material price volatility. Key ingredients are witnessing unprecedented price swings, straining manufacturer margins and complicating long-term planning. The American Bakers Association highlighted a 45% surge in canola oil prices and a 67% jump in soybean oil prices over the past year, attributing these spikes to supply chain disruptions and volatility in the agricultural commodity market, as reported by Baking Business. Such price hikes have a direct bearing on emulsifier production costs, given that vegetable oils are the primary feedstocks for essential emulsifying agents like mono- and diglycerides and lecithins. Enzyme production isn't immune either; specialty cofactors and fermentation substrates face supply constraints and price volatility, significantly influencing production economics. This challenge is magnified in emerging markets, where currency fluctuations intensify the effects of rising commodity prices, potentially curtailing market penetration and growth prospects. In response, manufacturers are diversifying their supplier bases and exploring alternative raw material sources. However, these strategies demand time for implementation and might not entirely alleviate immediate price pressures.

Stringent Additive Regulations in US & EU

Manufacturers face mounting challenges as evolving clean-label requirements push them to reformulate products with approved natural alternatives, which may not match the functionality of traditional improver formulations. Continuous re-evaluation of food additives by the European Food Safety Authority introduces uncertainty for manufacturers, especially with the looming threat of restrictions on currently approved substances, jeopardizing established product lines. Smaller manufacturers and newcomers, often lacking the resources to navigate intricate approval processes, find these regulatory burdens particularly daunting, which could stifle innovation and dampen market competition. Furthermore, these regulatory challenges resonate in global markets, as multinational manufacturers tend to adopt the strictest standards across their operations, aiming for consistency and a streamlined approach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Enzymes Drive Innovation Despite Emulsifier Dominance

In 2024, emulsifiers dominate the market with a 41.23% share, underscoring their pivotal role in enhancing dough texture across various bakery applications. Meanwhile, enzymes are emerging as the fastest-growing segment, projected to expand at a 7.23% CAGR from 2025 to 2030. This surge is largely fueled by the clean-label movement and advancements in bioactive formulations. Notably, the enzyme segment's ascent is bolstered by regulatory perks: enzyme-based solutions often get the nod as processing aids rather than additives, easing labeling challenges and boosting consumer trust. Innovative research, like the exploration of Antarctic α-amylase from Geomyces pannorum, highlights the promise of specialized enzymes. Such enzymes have been linked to a 26% uptick in bread volume and a 14.5% enhancement in cohesiveness over traditional methods, as noted in BMC Biotechnology.

Oxidizing and reducing agents hold steady market positions, playing vital roles in dough development and optimizing the gluten network. Acidulants, on the other hand, are key players in pH control and flavor enhancement. This segmentation underscores the industry's shift towards multifunctional solutions, adept at tackling multiple baking challenges. In response to the rising competition from enzymes, emulsifier manufacturers are innovating hybrid formulations. These new products meld traditional emulsifying traits with enzymatic benefits, effectively bridging the divide between conventional methods and biotechnological advancements. Given the declining costs of biotechnology and a regulatory tilt favoring natural over synthetic additives, the market dynamics hint at a sustained shift towards enzyme-centric solutions.

By Form: Liquid Formulations Gain Traction in Automated Systems

In 2024, the powder form segment leads the market with a 55.46% share, thanks to its established distribution channels, longer shelf life, and easier storage. These advantages resonate with manufacturers of all sizes. However, liquid formulations are on the rise, boasting a 6.89% CAGR through 2030. This surge is largely attributed to the automation trends in industrial bakeries and the precise dosing that liquid systems offer. The industry's pivot towards liquid formulations underscores a broader trend: a move towards automated mixing and dosing systems that promise consistency, reduced labor, and minimized human error. Meanwhile, paste formulations carve out a unique niche, delivering concentrated benefits for specific applications where powders or liquids might fall short.

Regional preferences and operational needs shape the dynamics of form segmentation. European manufacturers, equipped with advanced automation, are leaning more towards liquid systems. In contrast, emerging markets still gravitate towards powders, valuing their simplicity and cost-effectiveness. The liquid segment's expansion is bolstered by technological strides in stabilization and preservation, which have not only extended shelf life but also enhanced handling, alleviating past concerns. To cater to varied customer needs, manufacturers are embracing dual-format capabilities. Some are even innovating concentrated liquid systems that, when reconstituted at the point of use, merge the stability of powders with the precision of liquids.

By End User: Artisanal Segment Disrupts Industrial Dominance

In 2024, industrial bakeries, commanding a 33.25% market share, continue to dominate the bread improvers market. Their scale advantages and established supply relationships fuel this volume growth. This dominance underscores the economics of large-scale bread production, where consistent quality and operational efficiency amplify the value derived from improver investments. Meanwhile, artisanal bakeries are emerging as the fastest-growing segment, projected to expand at a 7.23% CAGR from 2025 to 2030. This surge is propelled by trends of consumer premiumization and the widespread adoption of professional-grade improver technologies. These advancements empower smaller operators to achieve results once reserved for their larger counterparts. Such a trajectory signals a notable shift in market dynamics, with artisanal producers now accessing sophisticated improver formulations that were previously the domain of industrial giants.

While retail/in-store bakeries and foodservice channels play pivotal roles, they occupy smaller segments of the market, each catering to distinct operational needs and consumer interactions. Owing to the rising tourism and eating-out culture, the consumption of out og home bakery products is increasing in the market, driving the growth. According to the Office for National Statistics[2]Office for National Statistics Data, "Number of overseas resident visits to the United Kingdom", www.ons.gov data from 2023, 38 million overseas tourists visited the United Kingdom. The growth of the artisanal segment is noteworthy, emphasizing a quality-over-quantity philosophy. This approach not only commands premium pricing but also yields higher margins. It opens avenues for specialized improver formulations that prioritize sensory attributes over mere cost savings. These dynamics resonate with broader consumer inclinations towards authenticity and craftsmanship. Artisanal bakeries, leveraging advanced improvers, strive to uphold traditional characteristics while ensuring the consistency vital for commercial success. This endeavor is bolstered by the rise of clean-label improver options, harmonizing with the artisanal ethos while delivering essential operational benefits.

By Application: Pizza Bases Drive Convenience Food Expansion

In 2024, bread applications command a dominant 52.34% market share, underscoring the pivotal role of bread improvers in traditional bread production. This segment's established supply relationships and technical requirements further bolster its leadership. The bread segment's prominence is attributed to the wide array of bread types and production methods, each necessitating specialized improver formulations, ranging from industrial white bread to artisanal sourdough. Meanwhile, pizza bases and flatbreads are emerging as the fastest-growing application segment, boasting a 7.45% CAGR through 2030. This surge is driven by global trends favoring convenience foods and advancements in frozen dough technologies, which facilitate centralized production and widespread baking. Such growth mirrors shifting consumer preferences towards convenient meal solutions and the worldwide embrace of pizza and flatbread.

Cookies, biscuits, buns, and rolls hold steady market positions, catering to unique demands for texture, shelf life, and processing traits distinct from traditional bread. The pizza and flatbread segment's expansion stands out, merging convenience food trends with age-old baking techniques. This fusion opens avenues for specialized improver formulations, ensuring quality is upheld even through freeze-thaw cycles and prolonged storage. The industry's application segmentation showcases its responsiveness to evolving consumption trends. Manufacturers are not only crafting solutions for new food formats but are also reinforcing their support for time-honored bread applications. As food manufacturers strive to set their offerings apart, the segment dynamics hint at a future of continued diversification, driven by innovative product formats and enhanced convenience features.

Geography Analysis

In 2024, Europe commands a dominant 35.67% market share, leveraging its well-established bakery infrastructure, robust regulatory framework, and discerning consumer base that increasingly favors premium improver formulations. Europe's market supremacy is underscored by its rich history of bread consumption, cutting-edge baking technologies, and a regulatory landscape that champions innovation while upholding stringent safety standards. According to the Average purchase per person per week of bread in the United Kingdom[3]Department for Environment, Food & Rural Affairs, "Average purchase per person per week of bread in the United Kingdom", www.gov.uk data from 2023, average purchase per person per week of bread in the United Kingdom was 465 grams.

In contrast, the Asia-Pacific region emerges as the fastest-growing market, projected to expand at a 7.78% CAGR from 2025 to 2030. This growth is fueled by urbanization, rising disposable incomes, and a burgeoning appetite for Western-style bakery products, which in turn, necessitate advanced improver technologies. Such disparities in regional growth underscore the shifting demographic and economic currents reshaping global food consumption. North America, with its penchant for convenience foods and cutting-edge automation technologies, plays a pivotal role in the market, driving demand for specialized improver formulations. The region's market landscape is further shaped by regulatory pushes for clean-label products and the innovative strides of major food manufacturers in improver technologies.

Meanwhile, South America and the Middle East & Africa emerge as promising frontiers, with their burgeoning urban populations and evolving retail infrastructures spurring a demand for enhanced bakery products. This geographic segmentation not only underscores the universal appeal of bread but also illuminates the regional nuances in consumer tastes, regulatory landscapes, and technological advancements that shape the demand for improvers. Asia-Pacific's upward trajectory is further bolstered by Corbion's strategic move to acquire Novotech's bread improver business in India, a testament to the region's allure for global players.

Competitive Landscape

The bread improvers market if fragmented with regional and global players dominating the market. The 2024 creation of Novonesis via the Novozymes-Chr. Hansen merger bulked up one of the world’s largest enzyme portfolios, deepening R&D pipelines spanning maltogenic amylase to xylanase. DSM-Firmenich exited direct yeast extract operations, selling to Lesaffre to streamline focus on specialty lipids and vitamins. Such moves redraw boundaries between classical yeast houses and biotech-forward enzyme specialists.

Regional champions defend share by tailoring blends to local flours and baking styles. Puratos leverages its Bakery Schools program to entrench technology alongside up-skilling initiatives, reinforcing brand trust across emerging markets. Corbion, through its Lactic Acid heritage, emphasizes clean preservation, whereas Angel Yeast scales yeast-plus-enzyme complexes in China’s extensive industrial bread lines. Patent filings cluster around thermostable amylase mutations and synergistic enzyme cocktails, suggesting long-term competition will revolve around intellectual property and application know-how rather than commodity emulsifier volumes.

Partnerships with equipment makers also intensify: dosing pump vendors integrate supplier-validated libraries that auto-adjust improver levels to flour protein shifts measured in real time. The model locks in proprietary formulations and positions ingredient firms as digital service providers, not just commodity suppliers. Meanwhile, sustainability pledges push firms to source palm-free emulsifiers and cut fermentation carbon footprints, adding new differentiation axes.

Bread Improvers Industry Leaders

-

Lesaffre International

-

Puratos group

-

Corbion N.V

-

Archer Daniels Midland Company

-

Kerry Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Aditya Birla Group, through its subsidiary Aditya Birla Chemicals (USA) Inc., strategically entered the United States chemicals market by acquiring Cargill's specialty chemical manufacturing facility in Dalton, Georgia. This acquisition aligns with the group's objective to strengthen its presence in the US manufacturing landscape.

- May 2025: Caitlyn India Pvt Ltd (CIPL) unveiled plans for a Rs 400 crore investment to set up a phosphoric acid plant in India, targeting an annual output of 50,000 tonnes. This initiative seeks to curtail import reliance and enhance the nation's fertiliser self-sufficiency. Strategically located in a port-accessible industrial zone in southern India, the plant will harness hemihydrate–dihydrate (HH-DH) technology, ensuring high-purity phosphoric acid and cleaner gypsum by-products.

- December 2024: Tate and Lyle have entered into a partnership with BioHarvest Sciences to leverage Botanical Synthesis technology for the development of next-generation plant-based ingredients, focusing on sustainable sweeteners and acidulants that optimize land and water usage.

- November 2024: Tate and Lyle has completed its USD 1.8 billion acquisition of CP Kelco, significantly enhancing its portfolio of nature-based ingredients. These include pectin and citrus fiber, which are essential for applications such as food preservation and texture modification. This strategic acquisition strengthens Tate and Lyle's ability to address the growing demand in the clean-label market and highlights the industry's focus on bio-based ingredient solutions.

Global Bread Improvers Market Report Scope

| Emulsifiers |

| Enzymes |

| Oxidizing Agents |

| Reducing Agents |

| Acidulants |

| Powder |

| Liquid |

| Pastes |

| Industrial Bakeries |

| Artisanal Bakeries |

| Retail/In-Store Bakeries |

| Foodservice channels |

| Bread |

| Cookies and Biscuits |

| Buns and Rolls |

| Pizza Bases and Flatbreads |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Ingredient Type | Emulsifiers | |

| Enzymes | ||

| Oxidizing Agents | ||

| Reducing Agents | ||

| Acidulants | ||

| Form | Powder | |

| Liquid | ||

| Pastes | ||

| End User | Industrial Bakeries | |

| Artisanal Bakeries | ||

| Retail/In-Store Bakeries | ||

| Foodservice channels | ||

| Application | Bread | |

| Cookies and Biscuits | ||

| Buns and Rolls | ||

| Pizza Bases and Flatbreads | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the bread improvers market and how fast is it growing?

The bread improvers market size is USD 1.80 billion in 2025 and is projected to reach USD 2.47 billion by 2030, reflecting a 6.55% CAGR.

Which ingredient category is expanding the fastest?

Enzymes lead growth at a 7.23% CAGR because they enable clean-label claims while improving dough strength and freshness.

Why are liquid bread improver formats gaining popularity?

Liquid systems integrate easily with automated dosing equipment, delivering precise dispersion and reducing manual handling errors, which drives a 6.89% CAGR for this form.

Which region shows the highest growth potential for bread improvers?

Asia-Pacific records the fastest regional CAGR at 7.78% as urbanization and disposable income boost demand for Western-style bakery products.

Page last updated on: