Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

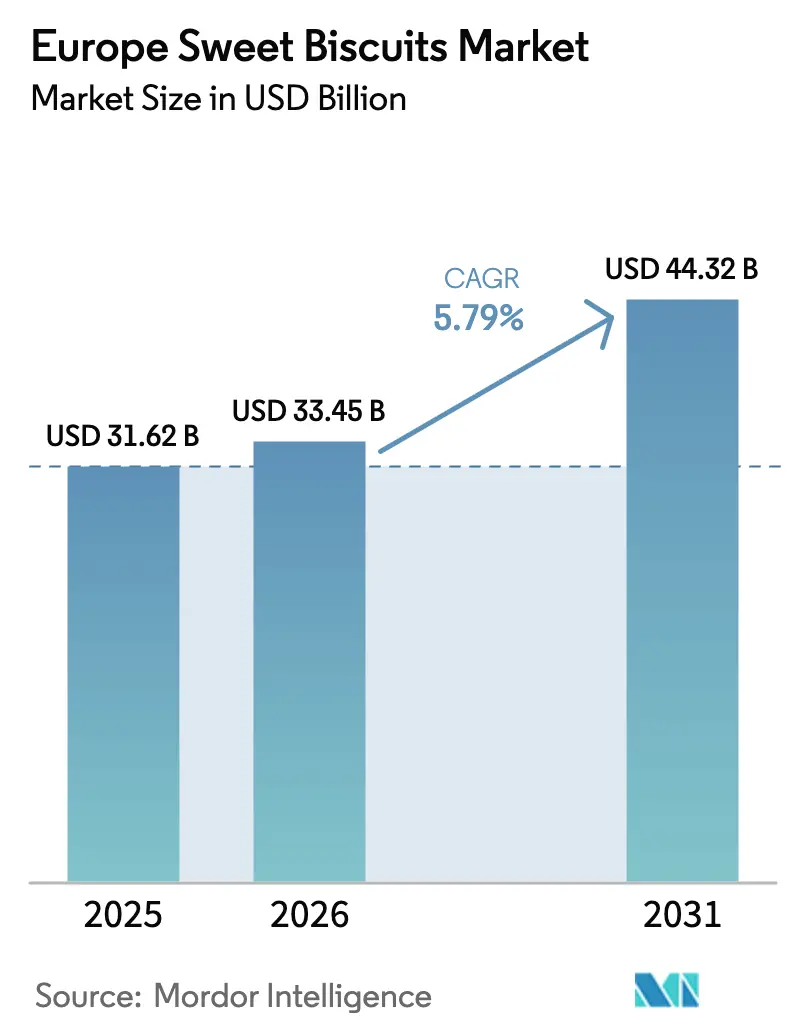

| Base Year Market Size (2025) | USD 31.62 Billion |

| Market Size (2026) | USD 33.45 Billion |

| Market Size (2031) | USD 44.32 Billion |

| Growth Rate (2026 - 2031) | 5.79% CAGR |

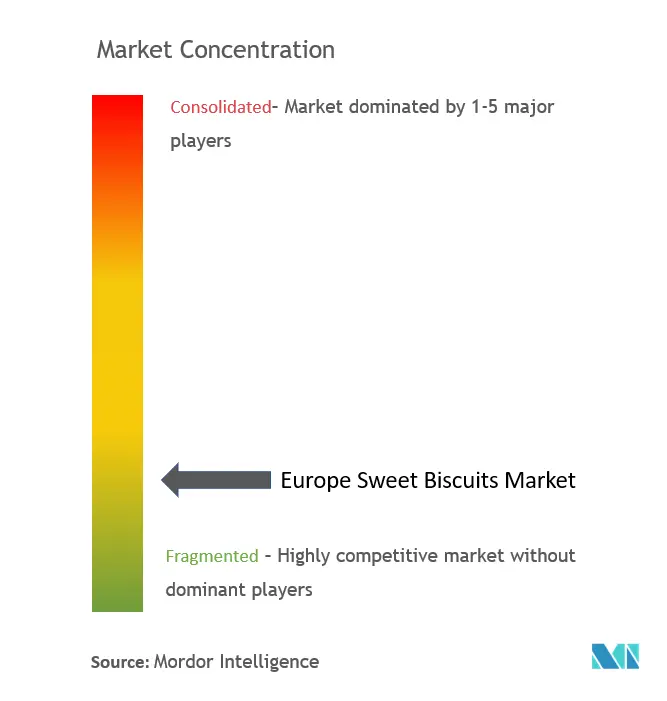

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Sweet Biscuits Market Analysis by Mordor Intelligence

The Europe Sweet Biscuits market size is expected to grow from USD 31.62 billion in 2025 to USD 33.45 billion in 2026 and is forecast to reach USD 44.32 billion by 2031 at 5.79% CAGR over 2026-2031. The European Sweet Biscuits Market reached USD 31.62 billion in 2025 and is projected to grow at a compound annual growth rate of 5.86% to reach USD 42.03 billion by 2030. This robust expansion reflects the sector's resilience amid evolving consumer preferences and the strategic adaptations of major manufacturers to capture emerging opportunities across diverse European markets. Macro forces driving this growth include the sustained demand for indulgent snacking occasions, accelerated by post-pandemic lifestyle changes that favor convenient, portion-controlled treats. The UK commands the largest regional market share at 26.18% in 2024, leveraging its strong biscuit heritage and established retail infrastructure, while Spain emerges as the fastest-growing market with a 7.94% CAGR, driven by expanding modern retail channels and increasing disposable incomes [1]Source: Eurostat, "Agricultural prices increase in Q4 2024", ec.europa.eu. Premiumization in chocolate-coated varieties, the fast adoption of online grocery, and a rebound in tourism across Southern Europe all reinforce demand. At the same time, manufacturers are balancing affordability with portion-controlled packs that help maintain price accessibility even as raw-material costs fluctuate. Technology investments in automation and data-driven product development further widen the gap between agile leaders and slower followers, creating opportunities for share gains in both mature and emerging European channels.

Key Report Takeaways

- By product type, plain biscuits led with 29.78% of the European sweet biscuits market size in 2025; chocolate-coated variants are set to grow the quickest at 6.02% CAGR to 2031.

- By packaging, plastic packets and pouches held 56.86% revenue share in 2025, but boxes are forecast to register a 6.18% CAGR through 2031.

- By flavor profile, plain varieties represented 85.10% volume share in 2025; flavored options are on track for a 7.12% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 64.92% sales in 2025, whereas online retail will expand at a 6.24% CAGR to 2031.

- By geography, the United Kingdom commanded 25.87% of the European sweet biscuits market share in 2025, while Spain is projected to post the fastest 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Sweet Biscuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Indulgent Snack Occasions | +1.2% | Global, with stronger impact in Northern Europe | Medium term (2-4 years) |

| Product Innovation and Flavor Varieties | +0.9% | Western Europe core, expanding to Eastern Europe | Long term (≥ 4 years) |

| Gifting Culture Boosts Demand for Sweet Biscuits | +0.7% | Germany, United Kingdom, France with seasonal concentration | Short term (≤ 2 years) |

| Convenient Portion Packs and Affordability | +0.8% | Pan-European with urban concentration | Medium term (2-4 years) |

| Technological Advancements in Manufacturing and Packaging | +0.6% | Manufacturing hubs in Germany, Netherlands, Italy | Long term (≥ 4 years) |

| Growth of Modern and Online Retail Channels | +1.1% | Western Europe leading, rapid adoption in Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Indulgent Snack Occasions

The fundamental shift toward snacking as meal replacement has accelerated European sweet biscuits consumption, with indulgent occasions increasingly replacing traditional structured eating patterns. Consumer behavior analysis reveals that 34% of nutrition experts identify increased snacking as a rising trend, driven by flexible work arrangements and urbanization. This transformation creates opportunities for manufacturers to position biscuits as premium snacking solutions rather than mere accompaniments to beverages. The trend particularly benefits chocolate-coated and filled biscuit segments, which command higher margins and align with consumers' desire for affordable luxury experiences. European consumers increasingly seek "everyday luxuries" that provide emotional satisfaction without significant financial commitment, positioning sweet biscuits as accessible indulgence options. The regulatory environment supports this shift through the EU's focus on portion control labeling, enabling manufacturers to market single-serve formats as mindful indulgence options.

Product Innovation and Flavor Varieties

Innovation velocity in European sweet biscuits has intensified as manufacturers leverage consumer insights and rapid development cycles to introduce differentiated products that command premium pricing. The sector benefits from accelerated product development timelines, with retailers achieving 6-12 week innovation cycles compared to traditional 12–18-month CPG timelines, enabling faster response to emerging flavor trends and seasonal preferences. Mondelēz International exemplifies this approach through its AI-powered marketing platform partnership with Accenture, reducing creative development time from weeks to hours while enabling real-time consumer preference analysis. Strategic partnerships between major brands are creating novel product categories, as demonstrated by the Mondelēz-Lotus Bakeries collaboration launching Cadbury+Biscoff in the UK and Milka+Biscoff across Europe in early 2025. The innovation imperative extends beyond flavor to include functional ingredients, with growing demand for gut-health supporting prebiotics and blood-sugar friendly formulations reflecting broader wellness trends. European food safety regulations, particularly those governing novel ingredients and health claims, provide a structured framework for innovation while ensuring consumer protection.

Gifting Culture Boosts Demand for Sweet Biscuits

Seasonal consumption patterns across Europe demonstrate the enduring strength of gifting traditions, with sweet biscuits experiencing pronounced demand spikes during key cultural celebrations that drive both volume and premium product sales. German retail scanner data reveals the magnitude of seasonal variation, with sweet consumption including biscuits surging 42.4% above annual averages in December before contracting 59.6% in January, illustrating both the opportunity and challenge of seasonal dependency [2]Source: Federal Statistical Office of Germany, "Dry January: 50% less alcohol bought in January 2024 than in December 2023", destatis.de. This pattern reflects deep-rooted European traditions where premium biscuits serve as essential components of holiday celebrations, corporate gifts, and social occasions. Manufacturers capitalize on this seasonality through limited-edition packaging, premium ingredient formulations, and strategic retail placement during peak gifting periods. The trend particularly benefits tin packaging formats, which achieved the fastest growth rate of 6.27% CAGR within packaging segments, as consumers associate metal containers with gift-worthy presentation and extended shelf life. Cross-border gifting within the European Union amplifies this effect, with regional specialties like Belgian cookies and German lebkuchen gaining broader European distribution through e-commerce channels.

Convenient Portion Packs and Affordability

The intersection of convenience and value consciousness has elevated portion-controlled packaging as a critical success factor, enabling manufacturers to address diverse consumer needs while optimizing price points across economic segments. Plastic packets and pouches dominate the packaging landscape with 57.43% market share in 2024, reflecting their cost efficiency and convenience attributes that resonate with budget-conscious consumers facing persistent inflation pressures [3]Source: European Central Bank, "What were the drivers of euro area food price inflation over the last two years?", ecb.europa.eu. The affordability imperative has intensified as European food inflation, while moderating from 2023 peaks, continues to influence purchasing decisions, with private-label biscuits gaining market share as consumers seek value without compromising quality perception. Strategic pack sizing enables manufacturers to maintain accessibility across income segments, with Mondelēz implementing pack-size laddering in Europe to offer price points ranging from EUR 1 to EUR 5 with adjusted gram weights to preserve affordability. This approach proves particularly effective in Eastern European markets where price sensitivity remains elevated, allowing global brands to compete with local value offerings while maintaining margin integrity. The EU's upcoming Packaging and Packaging Waste Regulation will influence portion pack strategies, requiring manufacturers to balance convenience with sustainability mandates including recyclability targets and empty space limitations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and Nutrition Concerns About High Sugar Content | -0.8% | United Kingdom leading, spreading across Western Europe | Medium term (2-4 years) |

| Rising Raw Material Costs | -1.1% | Global impact with regional variations | Short term (≤ 2 years) |

| Competition from Traditional Savory Snacks | -0.4% | Northern Europe primarily | Long term (≥ 4 years) |

| Regulatory challenges | -0.3% | EU-wide with national variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health and Nutrition Concerns About High Sugar Content

The European sweet biscuits sector faces mounting pressure from health-conscious consumers and regulatory initiatives targeting sugar reduction, creating both challenges and opportunities for reformulation strategies that maintain taste appeal while addressing wellness concerns. German government data reveals a structural shift in sugar consumption, with per-capita intake declining to 30.4 kg in 2024 from 33.9 kg previously, representing a 10% decrease in domestic sugar utilization. This trend reflects broader European nutrition priorities, with 51% of nutrition experts identifying blood-sugar friendly diets as a rising consumer preference, while 59% highlight gut-focused nutrition as an emerging demand driver. UK regulatory measures exemplify the intensifying policy environment, with High Fat, Salt, Sugar (HFSS) prominence rules implemented in October 2022 reducing visibility of indulgent products, while planned promotion restrictions scheduled for October 2025 threaten impulse purchase dynamics. Manufacturers are responding through alternative sweetener adoption, portion size optimization, and functional ingredient integration, with opportunities emerging in reduced-sugar formulations that leverage natural sweeteners like tapioca syrup and inulin to maintain consumer acceptance while addressing health positioning requirements.

Rising Raw Material Costs

Commodity price volatility continues to pressure European sweet biscuits manufacturers, with key ingredients experiencing significant cost inflation that challenges margin preservation while maintaining competitive pricing in price-sensitive consumer markets. Wheat and cereal prices, fundamental to biscuit production, have shown persistent elevation with EU cereal production estimated at 260.9 million tonnes in 2024/25, representing a 7% decline below five-year averages and the lowest production in a decade. Sugar market dynamics present mixed signals, with EU sugar production expected to increase by up to 1 million tonnes versus the prior year, potentially providing cost relief, while cocoa prices have reached record levels requiring strategic pricing and formulation adjustments. Energy costs remain a structural challenge for baking operations, with European food sector analysis revealing that energy-intensive processes faced electricity price increases of 145% and oil price rises of 43% during the 2022 inflationary period, creating lasting impacts on operational economics. Manufacturers are implementing multi-pronged cost management strategies including ingredient substitution, supply chain optimization, and strategic pricing, with Mondelēz demonstrating industry leadership through pack-size adjustments and premium mix optimization to offset cocoa cost pressures while preserving consumer accessibility. The EU's dependency on imported inputs, particularly soya-based ingredients and certain minerals, creates additional vulnerability to geopolitical disruptions and currency fluctuations that compound raw material cost pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plain Biscuits Anchor Market Despite Premium Innovation

Plain biscuits maintain market leadership with 29.78% share in 2025, reflecting their versatility as both standalone snacks and accompaniments to beverages, while chocolate-coated variants drive category premiumization with the highest growth rate of 6.02% CAGR through 2031. The enduring appeal of plain biscuits stems from their affordability, extended shelf life, and broad demographic acceptance, making them essential SKUs for retailers seeking to capture price-conscious consumers amid ongoing economic pressures. Sandwich biscuits represent a significant growth opportunity, combining the comfort of familiar formats with innovative filling varieties that enable premium positioning and higher margins per unit. Cookies continue expanding their European footprint through American-style formats and artisanal positioning, while the "Others" category, encompassing filled biscuits and wafer varieties, benefits from texture innovation and exotic flavor introductions.

Chocolate-coated biscuits' superior growth trajectory reflects successful premiumization strategies that leverage cocoa's indulgence associations despite raw material cost pressures, with manufacturers implementing sophisticated supply chain management to maintain accessibility. The segment benefits from strategic partnerships like the Mondelēz-Lotus collaboration, which combines established biscuit expertise with premium chocolate brands to create differentiated offerings that command higher price points. Innovation velocity in chocolate-coated varieties enables rapid response to seasonal trends and limited-edition opportunities that drive both volume and value growth. European food safety regulations provide a robust framework for chocolate-coating processes, ensuring consistent quality standards while enabling cross-border distribution efficiency. The segment's growth potential remains substantial as manufacturers explore functional chocolate coatings incorporating probiotics, plant-based alternatives, and reduced-sugar formulations that address evolving consumer wellness priorities.

By Packaging Type: Plastic Dominance Faces Sustainability Pressures

Plastic packets and pouches command 56.86% market share in 2025 due to their cost efficiency, barrier properties, and consumer convenience, while boxes experience the fastest growth at 6.18% CAGR driven by premiumization trends and sustainability positioning. The plastic packaging dominance reflects fundamental economics favoring flexible formats that minimize material usage, optimize shelf space, and provide superior product protection during distribution. However, the EU's Packaging and Packaging Waste Regulation (PPWR), entering force in February 2025, will fundamentally reshape packaging strategies through mandatory recyclability targets, recycled content requirements, and restrictions on certain single-use formats.

Box packaging growth reflects consumer premiumization preferences and gifting applications, with rigid formats conveying quality perception and enabling sophisticated graphics that enhance shelf appeal and brand differentiation. The regulatory environment increasingly favors paper-based solutions, with PPWR requiring 75% recyclability for paper and cardboard packaging by 2025, compared to more stringent requirements for plastic alternatives. Manufacturers are investing in sustainable packaging innovations, exemplified by Mondelēz's partnership with Saica to develop paper-based food packaging solutions that maintain product integrity while meeting environmental objectives. The "Others" category, including tins and jars, benefits from reusability positioning and premium gift applications, particularly during seasonal periods when presentation value drives purchasing decisions. PFAS restrictions in food-contact packaging, limiting concentrations to 25 ppb for targeted substances, require reformulation of barrier coatings and adhesives across all packaging formats, creating opportunities for innovative material suppliers and potential cost implications for manufacturers.

By Flavor Profile: Plain Varieties Dominate While Flavored Options Drive Growth

Plain biscuits maintain overwhelming dominance with 85.10% market share in 2025, reflecting European consumers' preference for versatile, familiar flavors that complement diverse consumption occasions, while flavored varieties achieve the highest growth rate of 7.12% CAGR as manufacturers pursue differentiation and premium positioning strategies. The plain segment's strength derives from its broad appeal across age groups, cultural preferences, and consumption contexts, making it an essential category for retailers seeking to maximize inventory turnover and consumer satisfaction. Flavored biscuits represent the industry's innovation frontier, enabling manufacturers to respond rapidly to emerging taste trends, seasonal preferences, and cultural celebrations that drive premium pricing and brand loyalty.

The flavored segment benefits from accelerated product development cycles and consumer willingness to experiment with novel taste experiences, particularly among younger demographics who demonstrate reduced brand loyalty and increased openness to premium offerings. Strategic flavor innovation leverages regional preferences and seasonal associations, with manufacturers introducing limited-edition varieties that create urgency and social media engagement. The growth trajectory reflects successful premiumization strategies that position flavored biscuits as affordable luxury items, enabling higher margins while maintaining accessibility for mainstream consumers. European regulatory frameworks support flavor innovation through established approval processes for natural and artificial flavoring substances, while geographical indication protections create opportunities for regional specialties to gain broader market recognition. The segment's expansion potential remains significant as manufacturers explore functional flavoring that incorporates wellness benefits, plant-based alternatives, and exotic ingredients that differentiate products in increasingly competitive retail environments.

By Distribution Channel: Traditional Retail Leads While Digital Transforms Access

Supermarkets and hypermarkets retain commanding market leadership with 64.92% share in 2025, leveraging their extensive reach, promotional capabilities, and consumer shopping habits, while online retail channels achieve the fastest growth at 6.24% CAGR as digital transformation reshapes consumer purchasing behavior and enables direct brand engagement. The traditional retail dominance reflects established consumer patterns favoring physical product evaluation, immediate gratification, and integrated shopping experiences that combine biscuits with complementary purchases. However, the digital channel's rapid expansion demonstrates fundamental shifts in consumer behavior, particularly among urban demographics and younger consumers who prioritize convenience and product discovery through digital platforms.

Online retail growth benefits from improved logistics infrastructure, expanded product assortments, and personalized marketing capabilities that enable targeted consumer engagement and premium product positioning. Convenience stores maintain steady performance through their proximity advantages and impulse purchase opportunities, while specialty and gourmet stores capture premium segments seeking artisanal and imported varieties that command higher margins. The "Other Distribution Channels" category encompasses vending machines, foodservice outlets, and institutional sales that provide consistent volume opportunities with different margin structures. European e-grocery market dynamics show projected growth rates of 7-9% annually through 2027, with efficiency-focused players outperforming through automated fulfillment centers and optimized delivery networks. The distribution landscape evolution requires manufacturers to develop omnichannel strategies that leverage both traditional retail relationships and direct-to-consumer capabilities, while regulatory compliance across multiple channels creates complexity in labeling, promotion restrictions, and consumer protection requirements.

Geography Analysis

The United Kingdom maintains market leadership with 25.87% share in 2025, capitalizing on its deep-rooted biscuit culture, established retail infrastructure, and strong brand heritage that resonates with both domestic and international consumers. British biscuit consumption patterns reflect cultural traditions where tea-time occasions drive consistent demand, while the market's maturity enables premium positioning and innovation acceptance. However, the UK faces headwinds from health-conscious regulations, including HFSS prominence rules and planned promotion restrictions that may dampen impulse purchases and require strategic reformulation to maintain growth momentum. Italy represents a significant market opportunity through its large packaged food sector valued at USD 99.2 billion in 2023, with sweet biscuits identified as a high-growth category benefiting from tourism recovery and consumer receptivity to innovative products.

Spain emerges as the fastest-growing market with 7.78% CAGR, driven by expanding modern retail channels, rising disposable incomes, and increasing urbanization that favors convenient snacking formats. The Spanish market benefits from strong tourism recovery, changing consumption patterns toward premium and international brands, and retail modernization that improves product accessibility and variety. France demonstrates steady performance through its sophisticated food culture and premium positioning opportunities, while Germany's large consumer base provides volume stability despite health-conscious trends that favor reduced-sugar and organic alternatives. The Netherlands and Belgium leverage their strategic locations as European distribution hubs and strong confectionery heritage to maintain competitive positions, while Poland represents Eastern Europe's growth potential through rapid retail modernization and increasing consumer purchasing power.

Regional consumption patterns vary significantly, with Northern European markets showing preference for plain and traditional varieties, while Southern European consumers demonstrate greater openness to flavored innovations and premium positioning. The European Union's regulatory harmonization facilitates cross-border distribution efficiency, while individual country preferences for packaging formats, portion sizes, and flavor profiles require localized marketing strategies. Sweden's market dynamics reflect Nordic preferences for organic and sustainable products, creating opportunities for manufacturers with strong environmental credentials and transparent supply chains. The "Rest of Europe" category encompasses emerging markets in Eastern Europe where retail modernization, urbanization, and rising incomes create substantial growth opportunities for both international brands and local manufacturers seeking to expand their geographic footprint.

Competitive Landscape

Influence of Social Media & Beauty Influencers

The European sweet biscuits market exhibits moderate fragmentation with a concentration score, creating opportunities for both established multinational corporations and agile regional players to capture market share through differentiated strategies and targeted consumer positioning. Market leadership remains contested among major players including Mondelēz International, Pladis (United Biscuits/McVitie's), Bahlsen, Lotus Bakeries, and Nestlé, each leveraging distinct competitive advantages ranging from global distribution networks to heritage brand equity and innovation capabilities.

Strategic patterns emphasize portfolio diversification, premium positioning, and geographic expansion, with successful players investing heavily in consumer insights, rapid product development, and omnichannel distribution to maintain relevance in evolving market conditions. Consolidation activity continues reshaping the competitive landscape, exemplified by Valeo Foods Group's EUR 200 million acquisition of I.D.C. Holding to strengthen Eastern European presence and expand sweet snacking capabilities. European food safety regulations provide a level competitive playing field while enabling quality differentiation, with companies investing in certifications, traceability systems, and supply chain transparency to build consumer trust and regulatory compliance.

Technology adoption drives competitive differentiation, with leaders like Mondelēz implementing AI-powered marketing platforms to accelerate creative development and enable real-time consumer preference analysis, while manufacturing automation enhances efficiency and quality consistency. White-space opportunities exist in functional biscuits targeting specific health benefits, sustainable packaging solutions that exceed regulatory requirements, and regional flavor innovations that leverage geographical indication protections to create differentiated premium offerings.

Europe Sweet Biscuits Industry Leaders

-

Kellanova

-

Mondelēz International

-

Britannia Industries

-

Parle

-

ITC Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nestlé Confectionery launched a new bakery-inspired range in the UK, featuring popular chocolate brands Aero, Milkybar and Munchies. This product line tapped into the growing consumer demand for indulgent snacks that combined the flavours of baked goods with traditional confectionery. The range included three distinct flavours: Aero Double Choc Brownie Flavour, Milkybar Crispy Cookie, and Munchies Vanilla Cheesecake Flavour.

- July 2025: Healthier snacking biscuit challenger, Good Guys Bakehouse, moved into Sweet Biscuits with a new duo of Sweet Crispy Biscuits, made for sofa grazing. The launch into Sweet Biscuits was a new move for the brand, which had established itself as a key player in the Savoury Biscuits space, with its Cheddar, Pepper and Paprika Biscuits Melts over-indexing on younger, health-conscious shoppers at Sainsbury's and Ocado in the UK and Tesco in Ireland.

- July 2025: Manchester-based Hill Biscuits unveiled Simply Savoury by Hill Biscuits, working in partnership with Cerealto UK, launching its first-ever savoury product in the company's 170-year history. Manchester-based Hill Biscuits introduced a classic cream cracker to the market in direct response to growing consumer demand for quality, value-for-money savoury options and an evolving snacking market. The company recognized an opportunity to diversify its product range as Cerealto UK already manufactured a wide range of sweet biscuits and savoury products.

Europe Sweet Biscuits Market Report Scope

A sweet biscuit is a small flat cake that is crisp and usually sweet. The Europe Sweet Biscuits market is segmented by type, distribution channel, and geography. By type, the market is segmented into cookies, sandwich biscuits, chocolate coated, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and others. By geography, the market is segmented into the United Kingdom, France, Germany, Italy, Spain, Russia, and the Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Plain Biscuits |

| Cookies |

| Sandwich Biscuits |

| Chocolate-Coated Biscuits |

| Others |

By Packaging Type

| Boxes |

| Plastic Packets/Pouches |

| Others |

By Flavor Profile

| Plain |

| Flavored |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty and Gourmet Stores |

| Online Retail |

| Other Distribution Channels |

By Geography

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Plain Biscuits |

| Cookies | |

| Sandwich Biscuits | |

| Chocolate-Coated Biscuits | |

| Others | |

| By Packaging Type | Boxes |

| Plastic Packets/Pouches | |

| Others | |

| By Flavor Profile | Plain |

| Flavored | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty and Gourmet Stores | |

| Online Retail | |

| Other Distribution Channels | |

| By Geography | United Kingdom |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the European sweet biscuits market in 2026?

It reached USD 33.45 billion in 2026 and is forecast to hit USD 44.32 billion by 2031, reflecting a 5.79% CAGR.

Which country leads regional sales?

The United Kingdom leads with 25.87% share, supported by strong tea-time traditions and extensive retail coverage.

Which product segment is growing fastest?

Chocolate-coated biscuits are projected for a 6.02% CAGR through 2031 as consumers seek premium indulgence.

Why is online retail significant for biscuit sales?

E-commerce enables direct engagement, personalized promotions, and convenient home delivery, driving a 6.24% CAGR in digital channels through 2031.

Page last updated on: