Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 21.04 Billion |

| Market Size (2026) | USD 21.76 Billion |

| Market Size (2031) | USD 25.76 Billion |

| Growth Rate (2026 - 2031) | 3.43% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Bacon Market Analysis by Mordor Intelligence

The Europe bacon market size was valued at USD 21.04 billion in 2025 and estimated to grow from USD 21.76 billion in 2026 to reach USD 25.76 billion by 2031, at a CAGR of 3.43% during the forecast period (2026-2031). The market's expansion is supported by the increasing incorporation of bacon into convenience-focused eating habits and rising demand from foodservice operators and quick-service formats, where bacon serves as a versatile, flavor-enhancing ingredient. Manufacturers are responding to evolving consumer preferences by introducing new flavors, formats, and cleaner-label options, including premium artisanal cuts and naturally cured or nitrate-free products. However, health concerns related to processed meat and the growing popularity of plant-based and flexitarian diets pose challenges. To address these, the industry is focusing on healthier or reformulated products and exploring opportunities such as halal-certified offerings and sustainable sourcing practices.

Key Report Takeaways

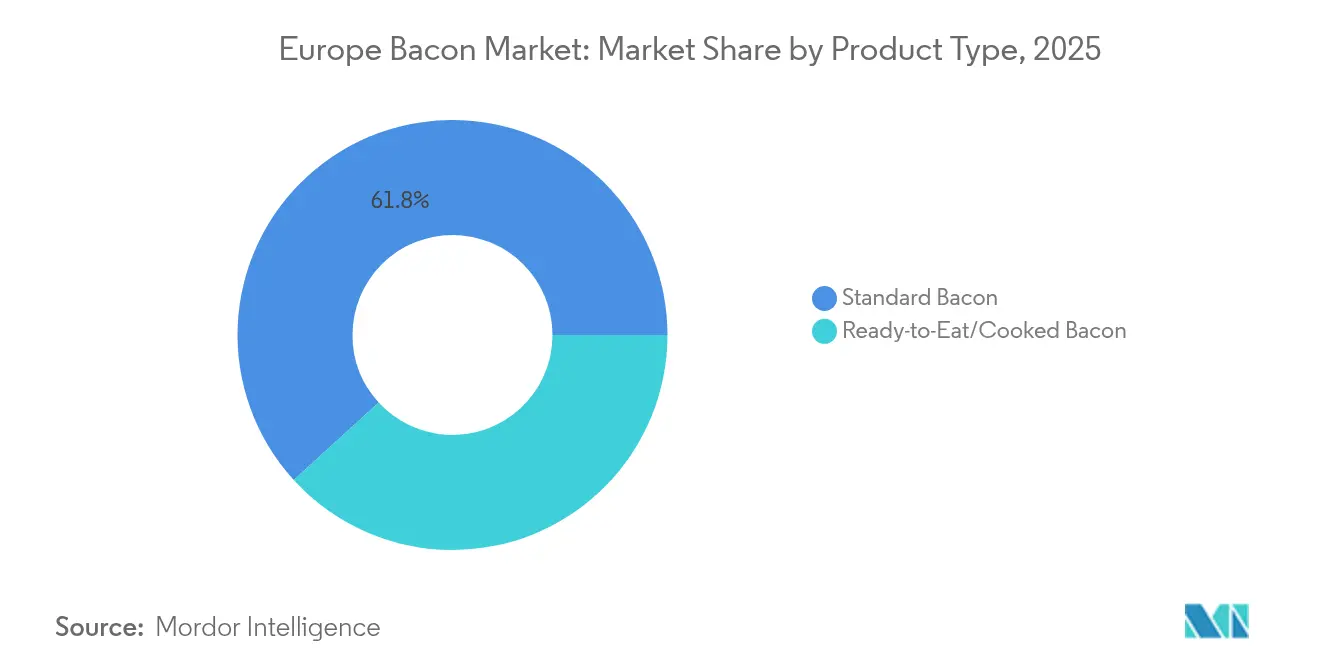

- By product type, standard bacon led with 61.78% revenue share in 2025, whereas ready-to-eat formats are forecast to expand at a 3.47% CAGR to 2031.

- By meat type, pork held 88.45% of the Europe bacon market share in 2025, while beef bacon is set to grow at a 3.58% CAGR through 2031.

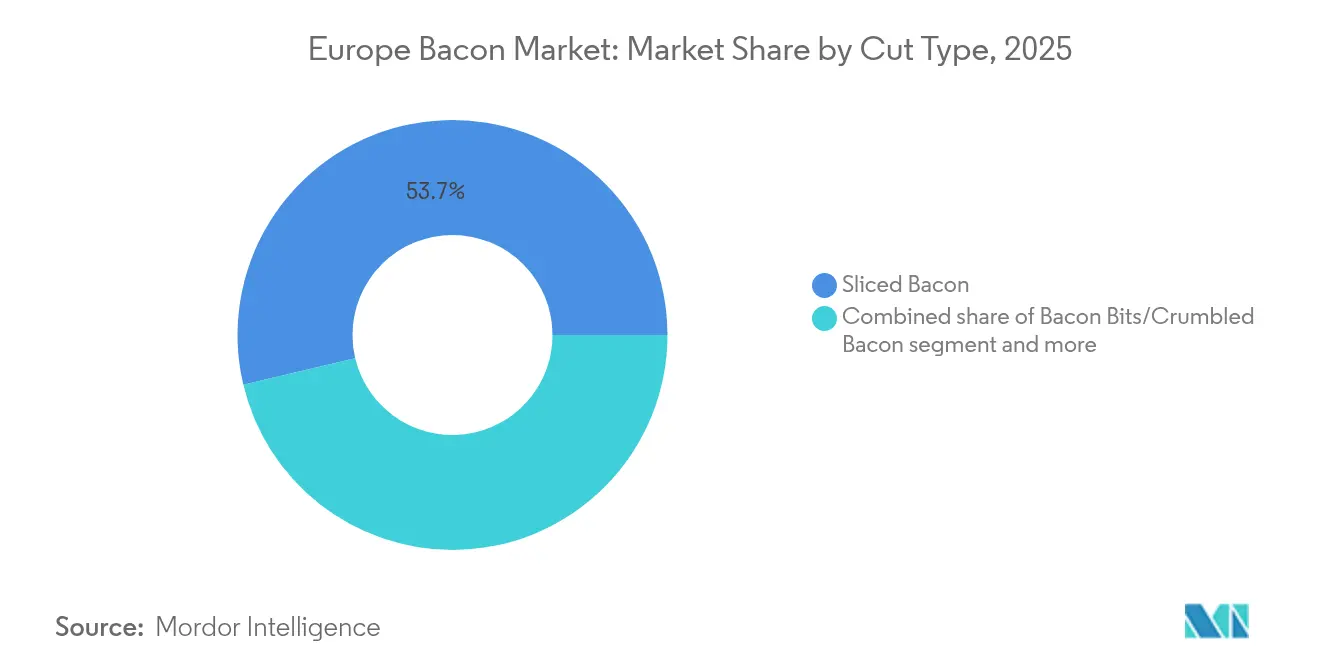

- By cut type, sliced bacon accounted for 53.72% of the Europe bacon market size in 2025, and pre-cooked bacon shows the fastest rise at a 4.17% CAGR.

- By distribution channel, retail dominated with 62.64% share in 2025, yet foodservice is projected to post a 4.21% CAGR to 2031.

- By geography, Germany led with a 19.12% share in 2025, while Spain is expected to advance at a 4.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Bacon Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High protein diet trends | +0.6% | Germany, the United Kingdom, Italy, Netherlands | Medium term (2-4 years) |

| Regional food tourism and culinary exposure | +0.3% | Spain, France, Italy, Belgium | Long term (≥ 4 years) |

| Growth of foodservice and quick-service restaurants | +0.8% | Germany, the United Kingdom, France, Spain, Poland | Short term (≤ 2 years) |

| Innovation in flavors and formats | +0.5% | United Kingdom, Germany, Netherlands, France | Medium term (2-4 years) |

| Rising focus on clean label products | +0.4% | United Kingdom, Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Rise of gourmet and premiumization trends | +0.7% | Spain, Italy, France, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High protein diet trends

High-protein diet trends are significantly driving demand in the Europe bacon market by transforming its perception from an indulgent, fatty meat to a convenient and versatile source of concentrated animal protein. This shift aligns with the growing popularity of protein-centric eating patterns. Across Europe, consumers are increasingly prioritizing foods that support satiety, weight management, muscle maintenance, and active lifestyles. Protein is one of the most valued macronutrients in this context, with surveys showing that a rising number of consumers, particularly younger demographics, view protein content as a critical indicator of a healthy product. These consumers actively seek products that prominently highlight their intrinsic or added protein content on packaging. This evolving mindset creates substantial opportunities for bacon in high-protein breakfasts, low-carb or keto-style diets where carbohydrates are restricted but protein and fat are embraced, and snack occasions where small portions of cooked or ready-to-eat bacon provide a convenient and savory protein boost.

Growth of foodservice and quick-service restaurants

The rapid expansion of foodservice and quick-service restaurants (QSRs) across Europe is a significant driver of the Europe bacon market, reshaping consumption patterns and boosting demand for convenient, protein-rich ingredients. As urbanization accelerates and lifestyles become increasingly fast-paced, more consumers are opting for dining out, take-away, and ready-to-eat meals, creating a steady and growing channel for bacon consumption. For instance, consumer spending in the Italian quick-service restaurant industry totaled approximately EUR 25.44 billion in 2024, underscoring the scale and importance of quick-service formats in European food culture, according to data from the National Council of Shopping Centers [1]Source: National Council of Shopping Centers (CNCC), "Consumer spending in the quick service restaurant (QSR) industry", cncc.it. Bacon, known for its versatility and quick preparation, is widely used across quick-service restaurant menus in items such as burgers, sandwiches, pizzas, salads, and breakfast offerings. Its ability to enhance flavor and provide protein content makes it a staple ingredient for operators aiming to meet consumer preferences effectively.

Innovation in flavors and formats

Innovation in bacon flavors and product formats is emerging as a transformative driver of growth in the Europe bacon market, as consumers increasingly seek distinctive, convenient, and premium eating experiences. Traditional salted or smoked varieties are being replaced by bold, gourmet, and globally inspired flavor profiles that turn everyday meals into exceptional culinary moments. Retailers are at the forefront of this shift, introducing creative and indulgent options to meet evolving consumer preferences. For example, Sainsbury’s offers Candied Maple Streaky Bacon in a 200 g pack, showcasing how mainstream retail channels are embracing sweet-savory, specialty-style bacon to captivate adventurous consumers and carve out a unique position in the market. These innovations not only reignite consumer interest but also redefine bacon as a versatile and essential ingredient that seamlessly integrates with contemporary culinary trends, such as the rising popularity of brunch culture and fusion cuisine.

Rising focus on clean label products

The increasing emphasis on clean-label products is a significant driver of the Europe bacon market, as consumers prioritize transparency, natural ingredients, and minimal processing in their food choices. Consumers across the region are increasingly seeking products free from artificial preservatives, synthetic additives, and unnecessary chemicals, which has led manufacturers to reformulate bacon products with simpler and more recognizable ingredient lists. This trend is particularly evident among health-conscious consumers and families who are actively seeking assurance that their everyday foods align with broader wellness and sustainability values. In response, producers are introducing nitrate-free, reduced-additive, and naturally cured bacon varieties, often labeled with terms such as no artificial preservatives, naturally smoked, and made with simple ingredients. Additionally, companies are expanding their portfolios to include a wider range of clean-label meat products, reflecting the growing demand and consumers' willingness to pay a premium for products perceived as higher in quality, safety, and alignment with their values.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over processed meat consumption | -0.9% | Germany, United Kingdom, France, Netherlands, Nordics | Long term (≥ 4 years) |

| Rising vegan and plant-based diets | -0.5% | United Kingdom, Germany, Netherlands, Sweden, Spain | Medium term (2-4 years) |

| Strict regulations on food safety | -0.3% | EU-wide, Denmark (stricter) | Short term (≤ 2 years) |

| Animal welfare standards complicating production | -0.2% | Germany, Denmark, Netherlands, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over processed meat consumption

Health concerns regarding processed meat consumption pose a significant restraint on the Europe bacon market. Increasing awareness of the potential health risks associated with processed meats, including links to heart disease, obesity, and certain cancers, has led many consumers to reduce or reconsider their intake. Reports from health organizations and heightened media focus on the adverse effects of high sodium, saturated fat, and preservatives such as nitrates and nitrites have amplified public scrutiny. This has driven a notable portion of the population, particularly younger, health-conscious consumers, to adopt moderation or seek alternatives. These trends are especially evident among individuals following flexitarian, plant-forward, or low-processed diets, which emphasize fresh, minimally processed protein sources over traditional cured meats like bacon. Additionally, government bodies and nutrition advocates across Europe are actively promoting dietary guidelines that recommend limiting processed meat consumption, further pressuring the category.

Rising vegan and plant-based diets

The increasing adoption of vegan, vegetarian, and plant-based diets is emerging as a significant restraint on the Europe bacon market. Consumers are progressively shifting away from traditional meat products toward alternatives perceived as healthier, more ethical, and environmentally sustainable. This trend is particularly evident in countries like Germany, where plant-based eating is becoming mainstream. According to EIT Food’s Nutrition Trend Report 2025, 82% of German nutrition experts expect continued growth in plant-based and flexitarian eating, underscoring the momentum behind reduced-meat lifestyles. As more Europeans adopt flexitarian habits, reducing meat consumption without eliminating it, the demand for processed meats, including bacon, is declining. Furthermore, the growing availability, enhanced nutritional profiles, and improved taste and texture of plant-based meat substitutes are intensifying this restraint. These alternatives directly compete with bacon by offering comparable flavors and textures while addressing consumer concerns related to health, ethics, and environmental sustainability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready-to-Eat Formats Capture Foodservice Shift

Standard bacon accounted for 61.78% of the product-type share in 2025, underscoring its continued dominance and central role in the Europe bacon market. This strong position is driven by entrenched consumer preferences, its culinary adaptability, and well-established supply chain networks, making it a staple in households and foodservice channels. Standard bacon provides consumers with the flexibility to control cooking methods, texture, and flavor intensity, enabling its use in a variety of traditional European dishes, including classic breakfasts, sandwiches, pastas, salads, and gourmet recipes. Its market leadership is further supported by longstanding production processes and economies of scale achieved by European pork processors, ensuring widespread availability and competitive pricing in retail channels.

The ready-to-eat and cooked bacon segment is projected to grow at a CAGR of approximately 3.47% from 2026 to 2031, indicating a notable shift in the Europe bacon market toward convenience-focused consumption. This segment's growth is fueled by evolving consumer lifestyles, increased urbanization, and rising demand for quick, easy-to-prepare meal solutions requiring minimal cooking effort. Unlike standard bacon, which requires preparation and cooking, ready-to-eat and pre-cooked bacon offers convenience, consistent quality, portion-controlled packaging, and versatility for use in breakfasts, sandwiches, salads, and other quick meals. These attributes make it particularly appealing to busy households and time-conscious professionals.

By Meat Type: Beef Bacon Gains Traction in Halal and Health Segments

Pork bacon leads the European bacon market, holding an 88.45% share in 2025. This dominance is attributed to its widespread availability, traditional consumption patterns, and strong consumer preference for its taste and versatility. Established supply chains and large-scale pork production across Europe ensure consistent quality, competitive pricing, and year-round availability, further reinforcing its market position. Pork bacon's flavor profile and adaptability to various dishes, including classic breakfasts, sandwiches, salads, and gourmet recipes, make it a staple in both households and foodservice operations, sustaining its high market share. Data from the Agriculture and Horticulture Development Board highlights that pork is the most consumed red meat in Europe, with an average per capita consumption of 28.1 kg per person based on the 2022–2024 three-year average . This high consumption reflects entrenched cultural habits, affordability, and the integration of pork into European cuisine, directly contributing to the dominance of pork-based bacon over alternatives such as beef or specialty meats.

Beef bacon, while still a niche compared to pork, is emerging as one of the fastest-growing segments in the European bacon market, with an estimated CAGR of 3.58% through 2031. This growth is driven by shifting consumer preferences. Some consumers seek bacon-like flavor and versatility while moderating pork intake due to religious, cultural, or personal reasons, making beef bacon a suitable alternative for flexitarian or pork-restricted diets. Additionally, beef-based processed meats are often perceived as more premium, associated with higher protein content and indulgent taste. This perception enhances beef bacon's appeal for gourmet burgers, sandwiches, and foodservice innovations. Furthermore, the increasing availability of beef bacon in retail and foodservice channels, coupled with marketing efforts highlighting its unique attributes, is expanding its consumer base. The segment is also benefiting from the growing trend of high-protein diets and the rising demand for alternative meat options, which align with evolving dietary preferences and lifestyle choices across Europe.

By Cut Type: Pre-Cooked Bacon Leads Growth Amid Labor Shortages

Sliced bacon is projected to hold a 53.72% share of the cut-type segment in 2025, highlighting the strong preference of European consumers and foodservice operators for convenience, portion control, and versatility in processed meat products. Sliced packs align with everyday cooking practices, enabling households to prepare consistent portions without the need for trimming or additional preparation. The standardized thickness of slices ensures even cooking and a predictable texture, encouraging repeat purchases. Retailers favor sliced bacon due to its effective merchandising in chill cabinets, adaptability to various pack sizes ranging from single-serve to family and club formats, and suitability for private-label development and frequent promotions.

Pre-cooked bacon is emerging as one of the most dynamic cut types in the European bacon market, with a projected growth rate of approximately 4.17% CAGR for 2026–2031, outpacing the overall category. This growth is driven by time-constrained consumers and foodservice operators seeking the flavor and versatility of bacon without the preparation time, splatter, or food-safety concerns associated with raw meat. Pre-cooked strips and pieces can be reheated in seconds using a pan, oven, or microwave and are ready to be incorporated into breakfast dishes, burgers, salads, pizzas, and prepared meals. The increasing presence of quick-service restaurants, café chains, and delivery-focused formats across Europe further boosts demand for pre-cooked bacon. It reduces back-of-house labor, simplifies staff training, and ensures consistent portion sizes and crispness across outlets. These attributes are essential for standardized menu items and rapid service, making pre-cooked bacon a preferred choice in the foodservice industry.

By Distribution Channel: Foodservice Outpaces Retail Post-Pandemic

Retail is expected to account for 62.64% of the European bacon market in 2025, highlighting the strong association of bacon with at-home consumption and the structure of modern grocery trade across the region. Supermarkets and hypermarkets allocate significant chilled shelf space to bacon, often dedicating entire sections to private-label and branded products. These offerings provide consumers with a wide range of options, including standard, smoked, flavored, lean, organic, and ready-to-eat variants in convenient sliced and pre-cooked formats. These formats align with weekly shopping habits and family stocking patterns. As consumers increasingly prepare breakfast, brunch, and simple evening meals at home, retail channels cater to this demand through multipacks, resealable packs, and portion-controlled formats. These packaging solutions extend shelf life, reduce waste, and make bacon a reliable, planned, and top-up purchase across large chains, discounters, and convenience stores.

Foodservice distribution is projected to grow at a compound annual growth rate (CAGR) of 4.21% through 2031, making it the fastest-growing channel for bacon in Europe. This growth is driven by the steady rebound and diversification of eating-out occasions and on-premise consumption. Quick-service restaurants, cafés, burger chains, and casual dining establishments increasingly use bacon as a versatile ingredient in breakfast plates, burgers, pizzas, salads, and small plates. This allows operators to enhance menu offerings, increase ticket values, and meet consumer demand for indulgent, protein-rich dishes. According to IfD Allensbach data reported by Statista, eating out is deeply ingrained in German leisure culture, with nearly 51.06 million people in Germany indicating they sometimes eat out in their free time in 2025 . This data underscores the significant customer base available to foodservice operators in one of Europe’s largest bacon-consuming markets, reinforcing the growth potential for bacon-containing dishes in the foodservice channel.

Geography Analysis

Germany accounted for 19.12% of Europe’s bacon market share in 2025, making it the largest national market in the region. This position is supported by a strong pork consumption culture, extensive retail distribution networks, and a well-established meat-processing industry. German consumers have a long-standing preference for pork-based products, with bacon being a staple in both household meals and foodservice channels. Despite the rise of flexitarian trends, the scale of domestic production and the maturity of the meat-processing sector sustain Germany’s leading position. Additionally, the country’s regulatory focus on quality, traceability, and animal welfare influences market dynamics, encouraging producers to innovate with cleaner-label and premium bacon varieties to meet evolving consumer preferences.

Spain is projected to be the fastest-growing geography in Europe’s bacon market, with a CAGR of 4.86% between 2026 and 2031. This growth is driven by increasing demand for convenience foods, the expansion of foodservice channels, and a rising interest in international and fusion cuisines that often feature bacon. The Spanish foodservice sector, particularly quick-service and casual dining formats, has increasingly incorporated bacon-based menu items. Meanwhile, modern retail chains are broadening their offerings of flavored, artisanal, and premium-cut bacon. This combination of culinary adaptability and convenience-driven consumption positions Spain as a dynamic growth center in the European bacon market.

The United Kingdom, France, Italy, the Netherlands, Poland, Belgium, and Sweden collectively contribute to the remainder of Europe’s bacon market share, each influenced by unique consumption habits, regulatory frameworks, and production capacities. The United Kingdom remains one of Europe’s most developed pork and bacon markets, supported by a strong domestic production base. According to the Agriculture and Horticulture Development Board, the United Kingdom produced 960,800 tonnes of pig meat in 2024, marking a year-on-year increase of nearly 4%, which reinforces its robust supply capabilities. France and Italy maintain stable demand due to their culinary traditions and strong retail networks. The Netherlands and Poland play significant roles as major pork producers and exporters within Europe, further shaping the region’s bacon market dynamics.

Competitive Landscape

The European bacon market exhibits a moderately concentrated competitive landscape, dominated by large multinational processors such as WH Group Ltd., JBS S.A., and Sofina Foods. These companies leverage extensive supply chains, diversified product portfolios, and robust distribution networks to maintain a significant presence across multiple European countries. Their advantages include economies of scale, established brand recognition, and long-standing partnerships with retailers. However, the market is not fully consolidated, as regional processors, private-label manufacturers, and artisanal producers hold notable positions in individual countries or niche segments. This balance between multinational leaders and strong local competitors creates a dynamic yet moderately concentrated market structure.

There are emerging opportunities in the clean-label and halal-certified bacon segments. As consumer demand grows for natural, minimally processed, and transparently sourced products, clean-label bacon is gaining popularity. However, many established players face challenges in reformulating products and adapting operations due to traditional processing methods and entrenched brand identities. Similarly, the halal-certified bacon segment remains underdeveloped in much of Europe, leaving room for new entrants or agile regional producers to address unmet demand among Muslim consumers. These opportunities provide a platform for disruptors, including startups and mid-sized processors, to differentiate themselves through product purity, ethical positioning, or culturally tailored offerings that larger incumbents have been slower to adopt.

Competitive intensity varies significantly across Europe. It is highest in Germany and the United Kingdom, where saturated retail environments, strong discount chains, and a growing premium artisanal segment exert pressure on mid-market processors. These conditions force companies to innovate or compete aggressively on pricing. In contrast, competition is lower in Southern and Eastern Europe, where fragmented supply chains, lower per-capita incomes, and a stronger reliance on regional producers reduce the dominance of multinational brands. In these regions, local taste preferences, traditional production methods, and cost sensitivity support smaller players and limit competitive overlap. This geographic diversity influences manufacturers' strategic priorities, shaping decisions on product positioning, market entry, and investment focus across Europe.

Europe Bacon Industry Leaders

-

WH Group Ltd (Smithfield)

-

JBS SA (Tulip Ltd)

-

Danish Crown A/S

-

Sofina Foods

-

OSI Group (Gelderland)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Finnebrogue announced two new additions to its Guinness product range: Guinness Unsmoked Back Bacon and Guinness Premium Pork Sausages. The Guinness Unsmoked Back Bacon is produced without nitrites and features a rich, deep color derived from its Guinness infusion.

- July 2025: HKFoods has announced that it will retain ownership of its bacon production plant in Swinoujście, Poland, reversing earlier discussions regarding a potential sale. The company intends to focus on strengthening its core business operations in Finland and Poland.

- October 2024: Simon Howie has introduced an alternative to traditional pork bacon with its new Streaky Beef Bacon packs. These packs are available in two variants: Premium Dry-Cured Smoked Streaky Beef Bacon and Premium Dry-Cured Unsmoked Streaky Beef Bacon.

- March 2024: Pork Farms has launched a range of ready-to-eat snacks, including Pork Farms Maple Bacon, designed as an alternative to existing smoked cooked bacon products in the market. Sweetened with maple syrup, the product can be consumed cold or heated.

Europe Bacon Market Report Scope

The European bacon market is segmented by type into standard bacon and ready-to-eat bacon. Based on the distribution channel, the market studied segmented into foodservice channels and retail. . Retail channels are further classified into supermarkets/hypermarkets, specialty stores, online stores, and other retail channels. The report further analyses the regional scenario of the market, which includes detail analysis on Spain, Germany, United Kingdom, France, Italy, Russia, and Rest of Europe.

By Product Type

| Standard Bacon |

| Ready-to-Eat/Cooked Bacon |

By Meat Type

| Pork |

| Beef |

| Other Meat Types |

By Cut Type

| Sliced Bacon |

| Bacon Bits/Crumbled Bacon |

| Bacon Rashers/Whole Slabs |

| Pre-Cooked Bacon |

By Distribution Channel

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty and Butcher Shops | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Foodservice |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Standard Bacon | |

| Ready-to-Eat/Cooked Bacon | ||

| By Meat Type | Pork | |

| Beef | ||

| Other Meat Types | ||

| By Cut Type | Sliced Bacon | |

| Bacon Bits/Crumbled Bacon | ||

| Bacon Rashers/Whole Slabs | ||

| Pre-Cooked Bacon | ||

| By Distribution Channel | Retail | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Specialty and Butcher Shops | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Foodservice | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the Europe bacon market in 2026 and how fast is it growing?

The market stands at USD 21.76 billion in 2026 and is forecast to rise to USD 25.76 billion by 2031, reflecting a 3.43% CAGR.

Which country leads regional demand?

Germany accounts for 19.12% of 2025 sales, driven by strong retail and foodservice networks despite recent volume softening.

Which segment is expanding the fastest?

Pre-cooked bacon, favored by quick-service restaurants, is projected to grow at a 4.17% CAGR through 2031.

Why is beef bacon gaining traction?

Halal certification and lower saturated-fat content help beef strips appeal to Muslim and health-conscious consumers, supporting a 3.58% CAGR outlook.

Page last updated on: