Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

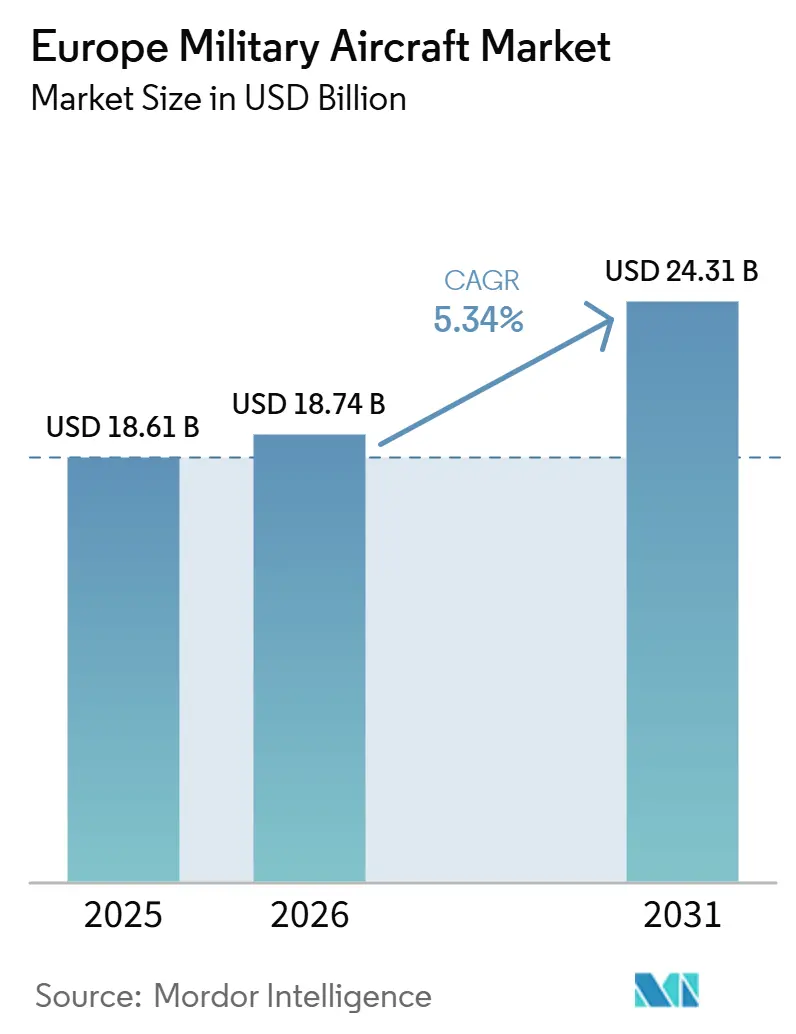

| Base Year Market Size (2025) | USD 18.61 Billion |

| Market Size (2026) | USD 18.74 Billion |

| Market Size (2031) | USD 24.31 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

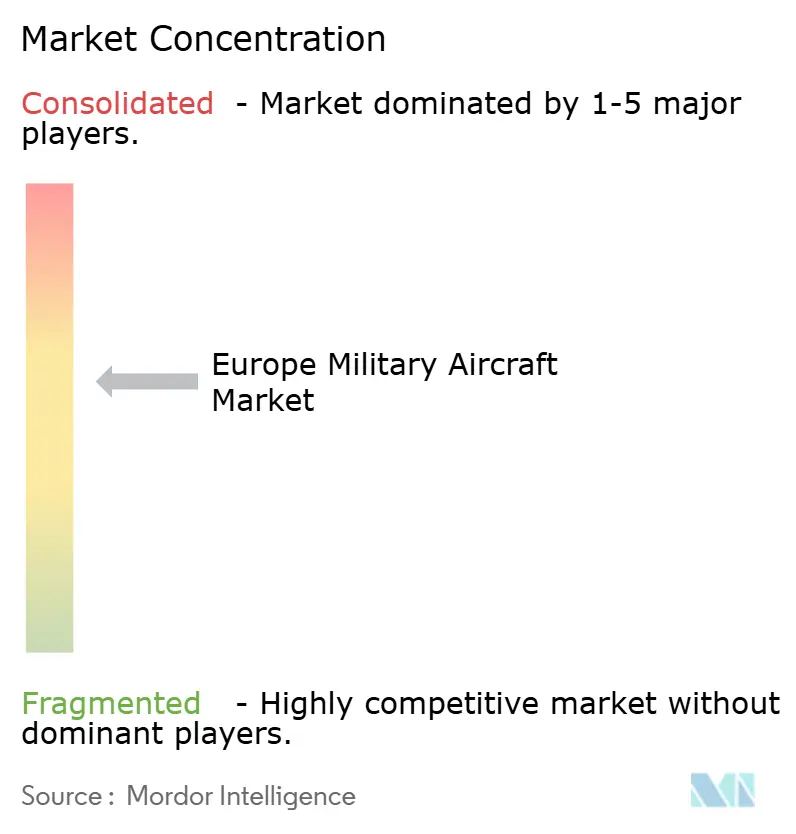

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Military Aircraft Market Analysis by Mordor Intelligence

The Europe military aircraft market size is expected to grow from USD 18.61 billion in 2025 to USD 18.74 billion in 2026, and is forecast to reach USD 24.31 billion by 2031, at a 5.34% CAGR over 2026-2031. The market is benefiting from a rearmament cycle that has pushed European military spending to USD 864 billion in 2025 and brought 22 European NATO members to the 2% of GDP threshold.[1]Source: SIPRI, “Global Military Spending Rise Continues as European and Asian Expenditures Surge,” Stockholm International Peace Research Institute, sipri.org EU member states also directed more capital toward equipment, with procurement expenditure surpassing EUR 100 billion (USD 114.31 billion) in 2025, keeping aircraft orders and upgrade work high in the spending mix. Program activity in 2026 shows that governments are backing both next-generation combat aircraft and shared support fleets, with GCAP funding advancing while NATO members also commit to joint airborne warning and transport capabilities. The Europe military aircraft market, therefore, combines strong state-backed demand with a moderate level of prime contractor concentration, in which a small group of large companies controls most platform programs across the region. Its main limits remain cost inflation, supply chain strain in propulsion and avionics, and certification schedules that can delay deliveries even when budgets are available.

Key Report Takeaways

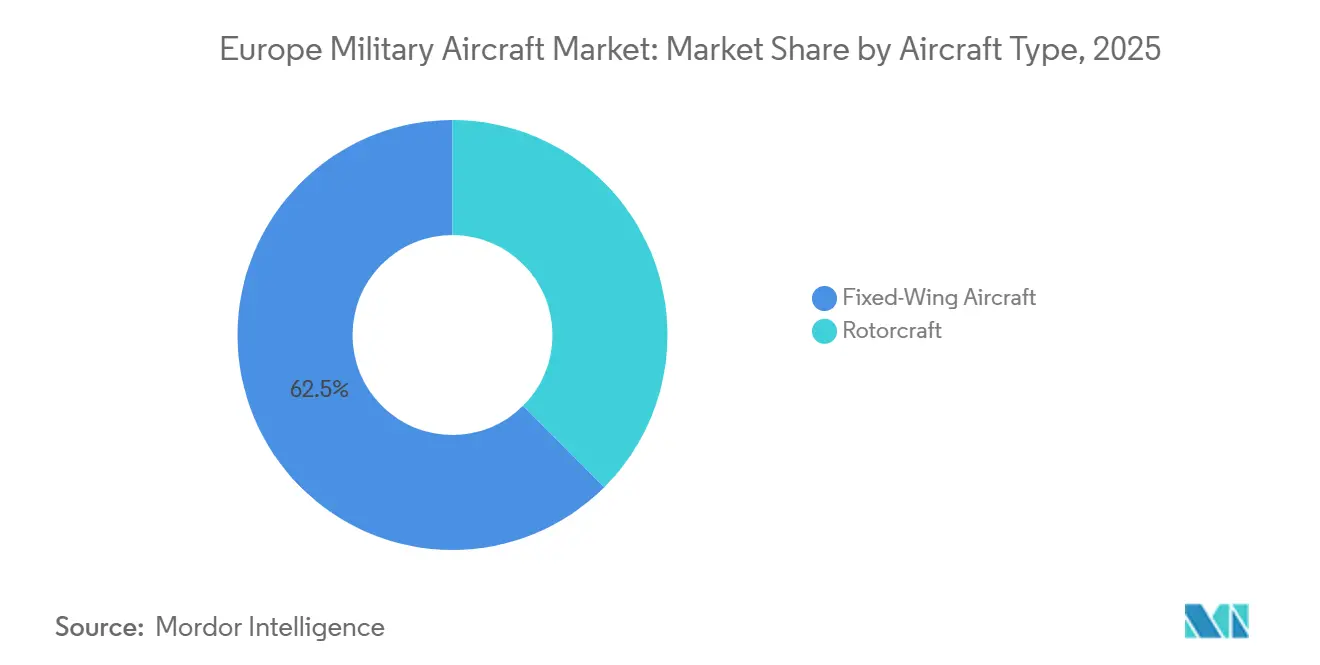

- By aircraft type, fixed-wing aircraft led with 62.48% share in 2025, while rotorcraft is forecast to grow at a 6.79% CAGR through 2031.

- By end-user service, Air Force operators held 74.39% of the Europe military aircraft market share in 2025, while Paramilitary and Coast Guard are projected to grow the fastest at a 7.10% CAGR through 2031.

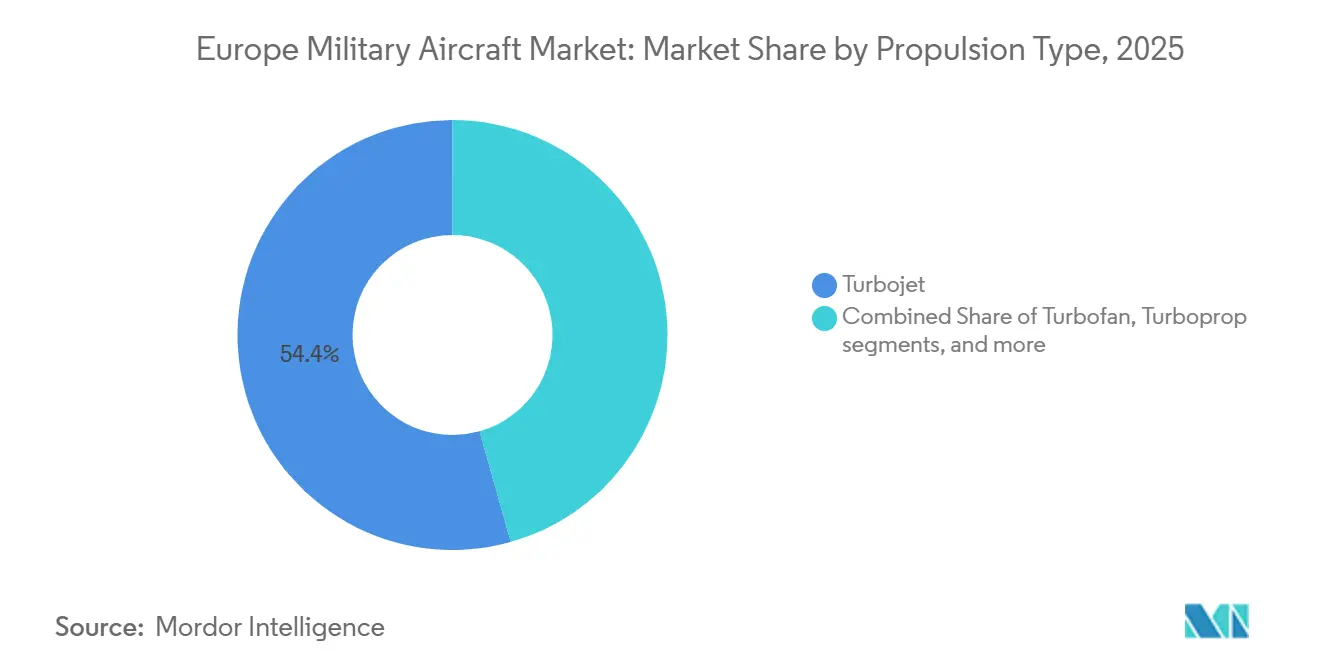

- By propulsion type, turbojet systems accounted for 54.36% of the Europe military aircraft market in 2025, while fully electric and hybrid-electric propulsion systems are projected to grow at a 7.34% CAGR through 2031.

- By geography, the UK led with 28.65% share in 2025, while Germany is forecast to grow at a 6.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Military Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NATO procurement rebuild after Ukraine | +1.80% | All European NATO members, with stronger impact in Eastern and Northern Europe | Short term (≤ 2 years) |

| Fleet ageing and upgrade-centric demand | +1.30% | Pan-European, especially Germany, the UK, France, and Italy | Medium term (2-4 years) |

| FCAS and GCAP industrial spillover | +0.90% | The UK and Italy through GCAP, Germany, France, and Spain through FCAS realignment | Long term (≥ 4 years) |

| Indigenous content rules favor European suppliers | +0.70% | EU-wide, especially France, Germany, Italy, and Spain | Medium term (2-4 years) |

| Software-defined mission systems raise retrofit scope | +0.50% | Broad European spillover, with concentration in the UK, Germany, and Italy | Medium term (2-4 years) |

| Carbon-constrained defense procurement nudges hybrid-electric development | +0.40% | Core EU markets, with early influence in Germany and the UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NATO Procurement Rebuild After Ukraine

The Ukraine conflict reset European defense budgeting at a speed not seen in decades, and the Europe military aircraft market is one of the clearest beneficiaries. The European military expenditure rose by 14% to USD 864 billion in 2025, the highest level recorded for the region. The spending mix also changed as governments shifted more money toward airpower and equipment procurement rather than simply raising baseline defense budgets. At the July 2026 NATO summit, allies moved to purchase up to 10 Saab GlobalEye aircraft, indicating a clear preference for a European platform in a collective program. That combination of higher budgets and shared procurement keeps near-term order visibility strong and supports the Europe military aircraft market beyond the current forecast window.

Fleet Ageing and Upgrade-Centric Demand

Fleet age is still forcing replacement and upgrade decisions across the Europe military aircraft market. Eurofighter partners plan to raise Typhoon production from 14 aircraft a year to 20 within 36 months, then to 30, while also pushing a mid-life upgrade to keep the platform relevant into the 2060s. Germany also approved a new Eurofighter Tranche 5 order and an SEAD upgrade package, which keeps retrofit demand moving alongside new-build demand. Germany is also taking delivery of F-35A aircraft in 2026 to replace Tornado jets, so procurement is occurring across two generations of combat aircraft simultaneously. That overlap supports fighter jets, avionics work, training assets, and support activities together rather than in separate cycles.

FCAS and GCAP Industrial Spillover

GCAP and the breakup of FCAS are reshaping long-term industrial positioning across the Europe military aircraft market. In July 2026, the UK, Italy, and Japan awarded a GBP 4.60 billion (USD 6.10 billion) contract to Edgewing for the next GCAP design phase. The UK also committed further multi-year funding, which removed a major budget question around the program's next stage. FCAS lost its manned fighter track in June 2026 following the industrial split between Airbus and Dassault, but that does not diminish future demand for combat air across Europe. Instead, it opens the way for workshare to shift toward GCAP, national alternatives, or additional Rafale and F-35 decisions, thereby keeping investment within the region's military aviation base.

Indigenous Content Rules Favor European Suppliers

New regulations are giving European suppliers a clearer advantage in the Europe military aircraft market. The EDIP regulation set a 35% ceiling on non-EU components for procurements that receive EU funding. The SAFE regulation also requires that contractors be established in the EU or the EEA for EU-backed common procurement. The broader readiness push inside Europe is also directing more defense sourcing toward regional suppliers, so sovereign content now matters more in contract design and workshare talks. This shift favors companies with established European manufacturing and can narrow the role of non-EU primes in jointly funded programs over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acquisition cost inflation and life-cycle burden | -1.40% | Pan-European, with sharper pressure in smaller NATO members with tighter budgets | Short term (≤ 2 years) |

| Engine-core and avionics supply bottlenecks | -1.00% | Pan-European, with concentration in the UK, Germany, and France | Medium term (2-4 years) |

| Certification delays for next-gen and retrofit platforms | -0.70% | EU and EASA jurisdictions across new platforms and mid-life upgrades | Medium term (2-4 years) |

| Skilled labor shortages in aerospace integration | -0.50% | Pan-European, especially Germany, France, the UK, and Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acquisition Cost Inflation and Life-Cycle Burden

Acquisition costs are rising fast enough to slow order sizes in the Europe military aircraft market. The GCAP design contract alone totals GBP 4.60 billion (USD 6.10 billion) for an 18-month phase, underscoring how expensive sixth-generation work has become. Support costs also rise because Eurofighter fleets still include Tranche 1, 2, and 3 aircraft with different avionics and software baselines. That pushes sustainment complexity higher and makes life-cycle planning harder for smaller NATO members with tighter budgets. The result is that some governments can fund capability upgrades but still struggle to buy the volumes they would prefer.

Engine-Core and Avionics Supply Bottlenecks

Propulsion and avionics supply constraints remain the most immediate execution risk for the Europe military aircraft market. Defense demand accelerated across Europe in 2025 and 2026, but production systems still face limited bandwidth after several years of uneven aerospace output. Avionics shortages, higher component costs, and geopolitical friction are still slowing delivery rates even as order books grow. The FCAS cancellation also created uncertainty for the MTU and Safran engine work that had supported next-generation sovereign propulsion development. When propulsion modules and mission systems are delayed, platform assembly schedules slip across both new-build and retrofit programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Fighter Jets and Rotorcraft Drive Parallel Growth Tracks

Fixed-wing aircraft accounted for 62.48% of the Europe military aircraft market in 2025, keeping this category well ahead of rotorcraft. Fighter jets remain the core demand driver inside fixed-wing, with Germany's F-35A deliveries, continuing Rafale output, and the Eurofighter production ramp all extending backlog visibility. Training aircraft are also gaining weight because new combat fleets need dedicated lead-in training capacity before frontline induction. Leonardo's December 2025 order for 12 M-346 F Block 20 aircraft from Austria showed that demand for advanced trainers is moving with combat fleet renewal rather than after it. Transport aircraft are also shifting toward pooled procurement, with 7 NATO allies launching a shared A400M fleet in July 2026, which could change how smaller states budget future airlift needs.

Rotorcraft is projected to expand at 6.79% CAGR through 2031, making it the fastest-growing aircraft type in the Europe military aircraft market. Spain's EUR 4.50 billion (USD 5.30 billion) order for 100 Airbus helicopters in December 2025 covered the H145M, NH90, H135, and H175M platforms, giving the segment a large multiyear production base. That order also shows a clear move toward fewer, more flexible military helicopters that can cover training, maritime, special operations, and light-attack needs within a single procurement plan. NAHEMA's April 2026 NH90 Block 2 study adds another layer of demand by covering both new-build and retrofit pathways across a 15-nation operator base.

By End-User Service: Air Forces Dominant, Paramilitary Demand Accelerates

Air Force operators held 74.39% share in 2025, making them the largest end-user group in the Europe military aircraft market. That lead came from high-value fighter jet and transport procurement across France, Germany, Italy, and Spain. Paramilitary and Coast Guard aviation remains the fastest-growing end-user group, with a 7.10% CAGR through 2031, as maritime surveillance and border security needs widen across southern and eastern Europe. Dual-use procurement rules also benefit this category, as platforms often require both civil and military certification paths to support coastal monitoring and patrol missions.

Army Aviation remains a stable growth segment because it absorbs much of the helicopter demand moving through the European military aircraft industry. Germany's H145M expansion shows how rotary-wing purchases are being split between the Bundeswehr and the Luftwaffe special forces rather than concentrated within a single service. Naval/Marine Corps Aviation end-users are adding targeted capacity in anti-submarine warfare (ASW), maritime patrol, and mission support rather than broad fleet expansion. Joint/Special Operations aviation is also gaining a clearer budget identity instead of being folded into larger Air Force or Army programs. The UK's March 2026 AW149 contract linked medium-lift helicopters to future autonomous teaming work, making this sub-segment more technology-led than replacement-led.

By Propulsion Type: Turbojet Incumbency Faces Emerging Disruption

Turbojet systems accounted for 54.36% of propulsion demand in 2025 and remained central to the combat fleet that defines much of the Europe military aircraft market. They remain essential for Typhoon and other combat aircraft, while turbofan engines support large transports and maritime patrol platforms. Turboprops still serve patrol and training roles, and turboshaft engines move with helicopter procurement across multi-mission fleets. Germany's H145M expansion and Spain's NH90 orders are directly lifting turboshaft demand across the region. The FCAS breakup, however, has introduced uncertainty into the next wave of sovereign European engine development tied to MTU and Safran.

Fully electric and hybrid-electric propulsion is forecast to grow at 7.34% CAGR through 2031, even though it starts from a small base in the Europe military aircraft market. The HECATE project validated a hybrid-electric power generation and distribution system exceeding 500 kW in late 2025 and linked that work to subsequent Clean Aviation programs. Near-term military use is focused on uncrewed logistics platforms rather than crewed combat aircraft. That keeps the technology tied to practical support missions and distributed operations rather than to symbolic fighter development programs.

Geography Analysis

The UK held 28.7% market share in the Europe military aircraft market in 2025 and remained the largest national market in the region. Its lead rests on GCAP leadership, Typhoon upgrades, and the March 2026 AW149 contract with Leonardo for 23 medium-lift helicopters. The country's upgrade spending is running alongside sixth-generation development, funding both current fleet relevance and long-term program control simultaneously.[2]Source: UK Defence Equipment & Support, “State-of-the-Art Radar Production Contract Secures 1,300 UK Defence Jobs,” Defence Equipment & Support, des.mod.uk France ranked second, supported by active Rafale deliveries and a large order backlog that still included 220 aircraft at the end of 2025. France is also keeping the Rafale F5 path funded, with work on the T-REX engine, new missile integration, and drone accompaniment, thereby protecting domestic capability after FCAS lost its manned fighter track.

Germany is forecast to grow at 6.90% CAGR through 2031, making it the fastest-growing country in the Europe military aircraft market. Its defense spending rose 24% to USD 114 billion in 2025, which was the largest absolute level among European NATO members. Germany is buying Eurofighter Tranche 5 aircraft, starting F-35A deliveries in 2026, and expanding the H145M fleet at the same time, so demand is spread across combat, rotorcraft, and support categories. Spain also accelerated sharply after raising defense spending 50% to USD 40.20 billion in 2025 and placing its 100-helicopter Airbus order. Italy stays in the middle tier on spending, but its equal position in Edgewing gives it a protected role in future sixth-generation workshare.

Turkey remains one of the most complex cases in the Europe military aircraft market, as it spent USD 30 billion on defense in 2025 while advancing its indigenous fifth-generation fighter program. TAI signed a procurement contract for 20 KAAN fighters in May 2026, and the US later notified Congress of a USD 700 million sale of F110 engines that support the program's propulsion base. The Netherlands continues to matter through F-35 supply links and participation in the NH90 program, while Russia remains outside the region's procurement ecosystem due to sanctions that impede normal market participation. Elsewhere, Belgium, Austria, and the Nordic countries are sustaining demand through helicopter deliveries, trainer orders, AWACS replacement work, and Gripen support activity.

Competitive Landscape

Innovation and Collaboration Drive Future Success

The Europe military aircraft market is moderately consolidated, with Airbus, BAE Systems, Dassault Aviation, Leonardo, and Saab controlling most large-platform programs across the region. Bruegel's March 2026 analysis showed that the top 10 contractors accounted for 67% to 90% of procurement value in Germany, Poland, and the UK, which limits room for new system-level entrants in the Europe military aircraft market. Even so, the field is broader at the subsystem level, where Thales, Safran, MTU Aero Engines, and Rheinmetall remain important in avionics, propulsion, and mission systems. This structure keeps bidding concentrated in major aircraft programs while leaving room for competition in integration, software, and specialist components.

The Edgewing joint venture is one of the clearest strategic moves now shaping the Europe military aircraft market because it concentrates GCAP design authority equally between BAE Systems, Leonardo, and JAIEC. That model can lock in current partners for decades if GCAP stays on schedule for service entry in 2035. Leonardo made another important move when its AW149 contract also established Yeovil as a center for autonomous rotary-wing development, tying a crewed platform award to future uncrewed capability. Saab also strengthened its position in 2026 by signing the Gripen E contract for Ukraine and by remaining central to the GlobalEye replacement discussion.[3]Source: Saab AB, “Saab Year-End Report 2025, Record Order Bookings, Building for Growth,” Saab AB, saab.com Dassault remains protected by Rafale production continuity and the funded F5 roadmap, which gives France a domestic combat-air path even without a shared FCAS fighter.

Competitive gaps are emerging at the intersection of manned aircraft programs and autonomy, electronic warfare, and sensor fusion. Mission-system software is becoming increasingly important because upgrades can generate recurring revenue even when the basic airframe remains unchanged. Smaller players can still enter through uncrewed logistics, ISR, and retrofit niches, but NATO interoperability and military airworthiness rules keep the threshold high for newcomers. As a result, the Europe military aircraft market is open enough for targeted specialists but still difficult to disrupt at the prime contractor level.

Europe Military Aircraft Industry Leaders

Airbus SE

BAE Systems plc

Leonardo S.p.A.

Dassault Aviation SA

Saab AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: The UK, Italy, and Japan awarded Edgewing a GBP 4.60 billion (USD 6.10 billion) 18-month development contract for the next design and assessment phase of the GCAP sixth-generation fighter, targeting a 2035 service entry.

- June 2026: Saab signed a contract with Sweden's Defense Materiel Administration for 16 new-build Gripen E fighters for Ukraine, valued at SEK 24.60 billion (USD 2.50 billion) and financed through an EU loan facility. Deliveries are scheduled for 2029 to 2030, and Sweden simultaneously committed 16 secondhand Gripen C/D aircraft as military aid deliverable in early 2027.

- June 2026: France and Germany formally abandoned the manned fighter component of the FCAS after industrial mediation between Airbus and Dassault Aviation collapsed in April 2026. The decision terminates the joint sixth-generation fighter, estimated at EUR 100.00 billion (USD 116.00 billion) over its intended life, but preserves development of the FCAS combat cloud and uncrewed drone elements.

- April 2026: NAHEMA contracted NHIndustries, a consortium of Airbus Helicopters, Leonardo, and GKN/Fokker, for a EUR 15.00 million (USD 17.60 million) NH90 Block 2 architecture study covering new-build and retrofit upgrade paths for the 15-nation NH90 operator base, extending the platform's commercial runway.

Europe Military Aircraft Market Report Scope

The Europe military aircraft market encompasses the procurement, production, modernization, maintenance, and lifecycle support of military aircraft operated by defense and security forces across the European region. The market includes fixed-wing aircraft and rotorcraft designed for defense, combat, transport, surveillance, reconnaissance, training, maritime security, special operations, and humanitarian missions. It also covers aircraft upgrades, mission system integration, propulsion systems, avionics, and aftermarket support services associated with military aviation platforms.

The Europe military aircraft market is segmented by aircraft type, end-user service, propulsion type, and geography. By aircraft type, the market is segmented into fixed-wing aircraft and rotorcraft. By end-user service, the market is segmented into Air Force, Army Aviation, Naval/Marine Corps Aviation, Joint/Special Operations, and Paramilitary and Coast Guard. By propulsion type, the market is segmented into turbofan, turbojet, turboprop, turboshaft, and fully electric/hybrid-electric. The report also covers the market sizes and forecasts for the Europe military aircraft market in six countries across the region. For each segment, the market size is provided in terms of value (USD).

By Aircraft Type

| Fixed-Wing Aircraft | Multi-Role Aircraft |

| Training Aircraft | |

| Transport Aircraft | |

| Others | |

| Rotorcraft | Multi-Mission Helicopters |

| Transport Helicopters | |

| Others |

By End-User Service

| Air Force |

| Army Aviation |

| Naval/Marine Corps Aviation |

| Joint/Special Operations |

| Paramilitary and Coast Guard |

By Propulsion Type

| Turbofan |

| Turbojet |

| Turboprop |

| Turboshaft |

| Fully Electric and Hybrid-Electric |

By Geography

| United Kingdom |

| France |

| Germany |

| Italy |

| Netherlands |

| Russia |

| Spain |

| Turkey |

| Rest of Europe |

| By Aircraft Type | Fixed-Wing Aircraft | Multi-Role Aircraft |

| Training Aircraft | ||

| Transport Aircraft | ||

| Others | ||

| Rotorcraft | Multi-Mission Helicopters | |

| Transport Helicopters | ||

| Others | ||

| By End-User Service | Air Force | |

| Army Aviation | ||

| Naval/Marine Corps Aviation | ||

| Joint/Special Operations | ||

| Paramilitary and Coast Guard | ||

| By Propulsion Type | Turbofan | |

| Turbojet | ||

| Turboprop | ||

| Turboshaft | ||

| Fully Electric and Hybrid-Electric | ||

| By Geography | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| Rest of Europe | ||

Market Definition

- Aircraft Type - All the military aircraft and rotorcraft which are used for various applications are included in this study.

- Sub-Aircraft Type - For this study, sub-aircraft types such as fixed-wing aircraft and rotorcraft based on their application are considered.

- Body Type - Multi-Role Aircraft, Transport, Training Aircraft, Bombers, Reconnaissance Aircraft, Multi-Mission Helicopters, Transport Helicopters and various other aircraft and rotorcraft are considered in this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms