Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

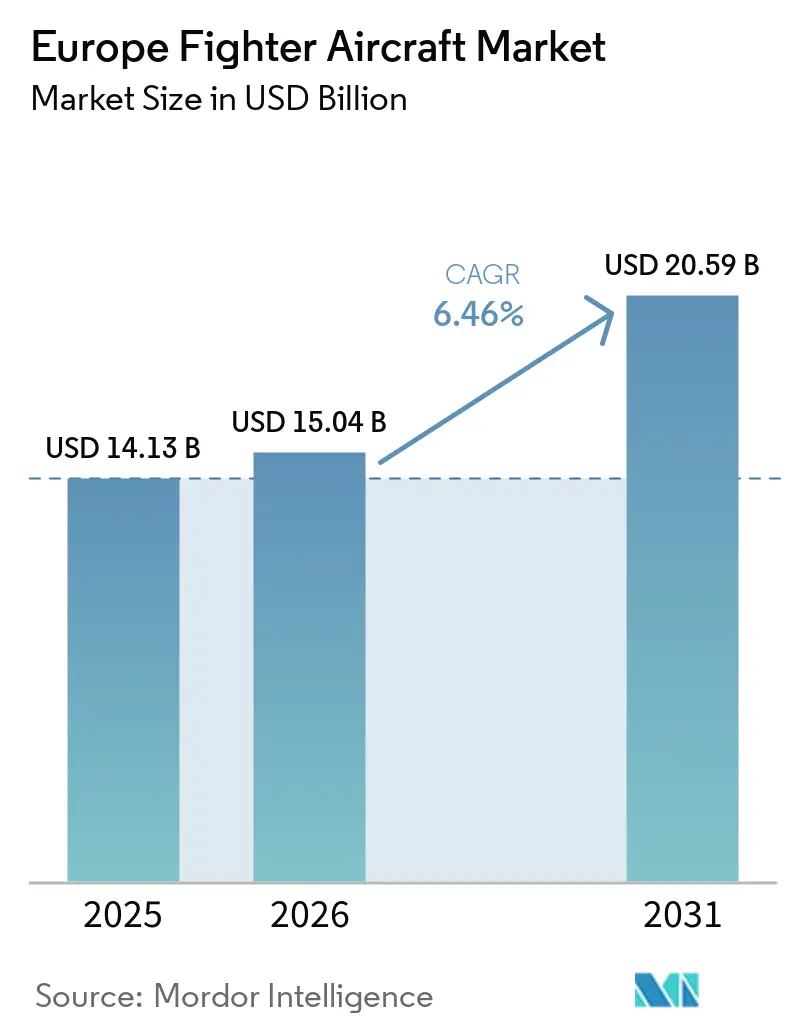

| Base Year Market Size (2025) | USD 14.13 Billion |

| Market Size (2026) | USD 15.04 Billion |

| Market Size (2031) | USD 20.59 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Fighter Aircraft Market Analysis by Mordor Intelligence

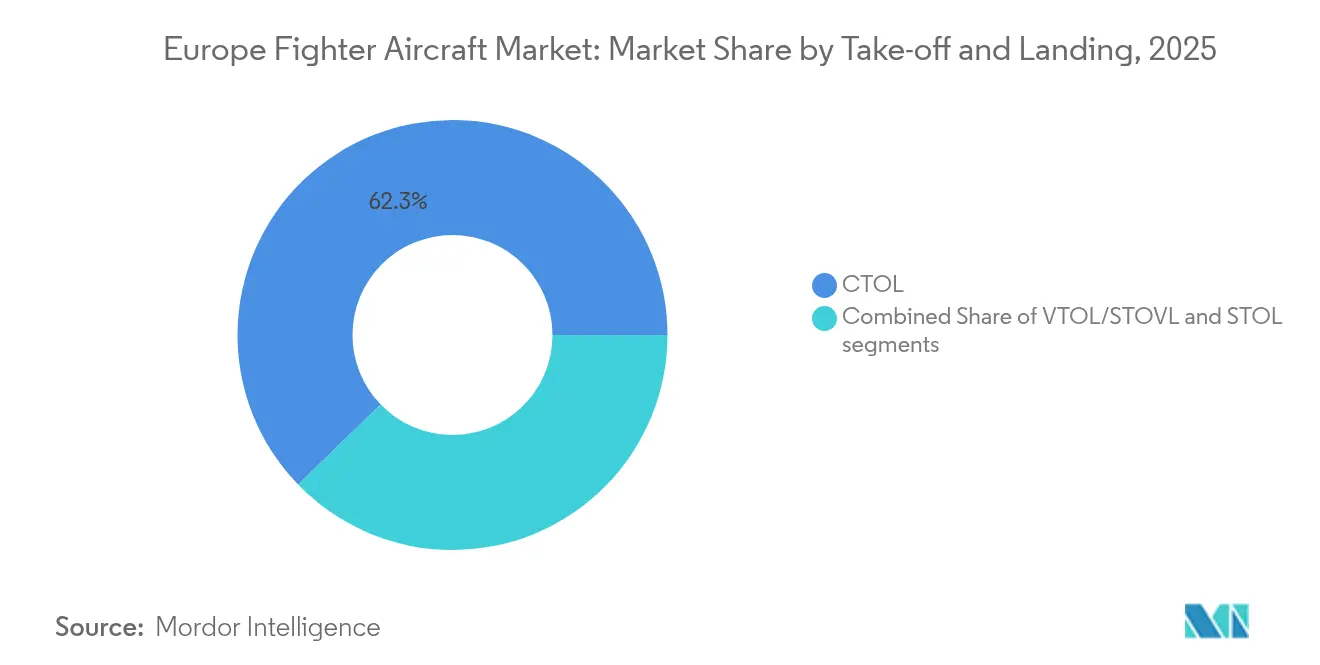

The Europe fighter aircraft market size was valued at USD 14.13 billion in 2025 and estimated to grow from USD 15.04 billion in 2026 to reach USD 20.59 billion by 2031, at a CAGR of 6.46% during the forecast period (2026-2031). Escalating security threats after Russia’s full-scale invasion of Ukraine, combined with the European Union’s EUR 150 billion (USD 175.85 billion) Security Action for Europe (SAFE) loan facility, have transformed procurement priorities and unlocked near-term funding for both 4th- and 5th-generation fleets. Germany’s decision to devote 5% of GDP to defense and the collective drive toward 6th-generation sovereignty amplify order backlogs, while industrial policies that privilege European content reshape supply chains and collaboration structures. Conventional take-off and landing (CTOL) aircraft currently command 62.87% of the European fighter aircraft market share, yet short- and vertical-take-off capabilities are gaining traction on the back of naval aviation modernization and austere-basing concepts.

Key Report Takeaways

- By take-off and landing, CTOL platforms captured 62.25% of the European fighter aircraft market share in 2025, while VTOL/STOVL platforms are projected to expand at a 7.54% CAGR to 2031.

- By fighter generation, 4.5th-generation aircraft held 43.12% of the European fighter aircraft market share in 2025; 6th-generation programs record the highest projected CAGR at 8.18% through 2031.

- By engine configuration, single-engine fighters accounted for 55.31% of the European fighter aircraft market in 2025, whereas twin-engine platforms are forecast to post a 6.81% CAGR between 2026 and 2031.

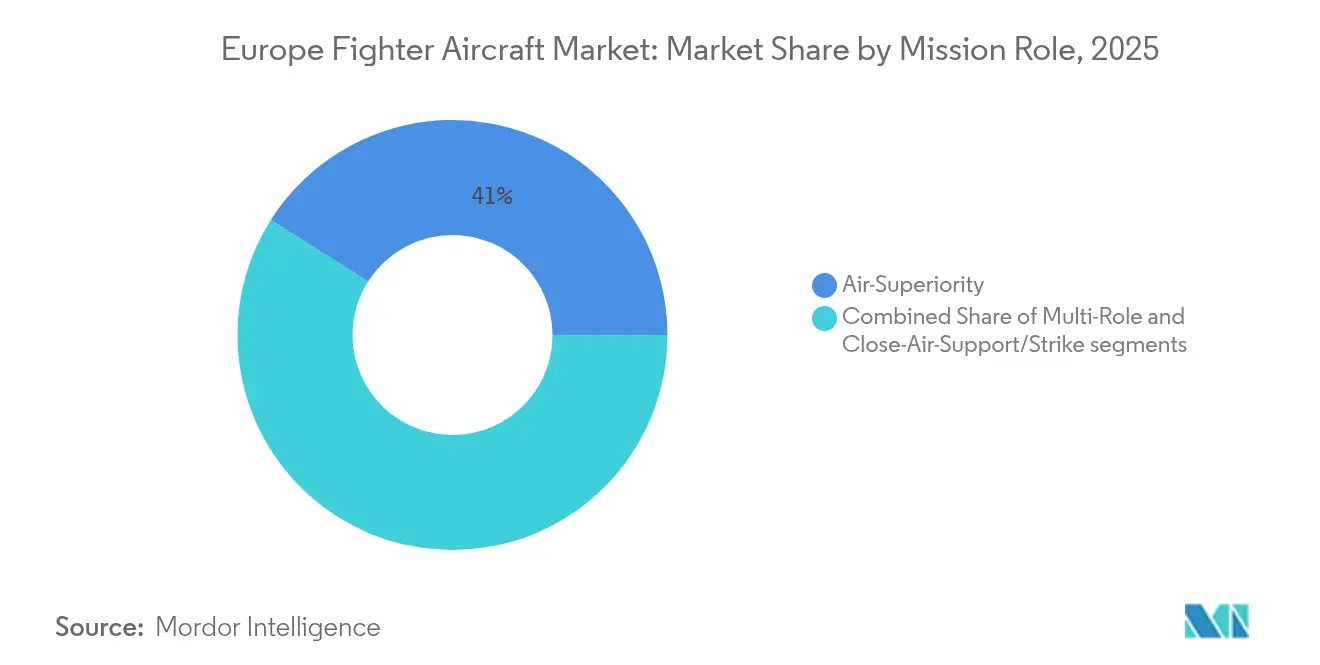

- By mission role, air-superiority platforms constituted 41.02% of the European fighter aircraft market size in 2025; multi-role platforms will advance at a 7.72% CAGR to 2031.

- By end user, air forces represented 52.45% of total demand in 2025, while naval aviation is the fastest-growing segment, with an 8.34% CAGR through 2031.

- By geography, France led with a 39.85% revenue share in 2025; Germany shows the strongest growth trajectory, with a 7.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Fighter Aircraft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Ukraine surge in European defense budgets | +1.80% | Eastern Europe, Germany | Short term (≤ 2 years) |

| Accelerated 5th-generation (F-35) procurements | +1.40% | Germany, Belgium, Czech Republic, Romania | Medium term (2–4 years) |

| Launch of 6th-generation programs (FCAS and GCAP) | +1.20% | France, Germany, Spain, UK, Italy, Japan | Long term (≥ 4 years) |

| Ageing legacy fleets reaching end of life | +1.00% | UK, Germany, Spain, Italy | Medium term (2–4 years) |

| EU joint-procurement mechanism unlocking scale buys | 0.8% | EU Member States, with spillover to EEA and Ukraine | Medium term (2-4 years) |

| Rise of manned–unmanned teaming requirements | 0.6% | Germany, France, UK, with early adoption in advanced air forces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Ukraine Surge in European Defense Budgets

The EU’s SAFE regulation unlocks EUR 150 billion (USD 175.85 billion) in loan guarantees dedicated to joint capability acquisition, marking the region’s most enormous peacetime spending wave since the Cold War.[1]Council of the European Union, “Council Regulation (EU) 2025/1106 establishing SAFE,” europa.eu Germany’s 5% of GDP pledge alone sends USD-level demand surging for new builds and sustainment across the Europe fighter aircraft market. National “escape-clause” budget mechanisms let Member States exceed fiscal rules by 1.5% of GDP through 2029, widening headroom for back-to-back orders. NATO’s 2024 capability review called air-superiority gaps critical, turning fighters into top-priority line items. Near-term disbursements, therefore, push the Europe fighter aircraft market toward a procurement super-cycle that extends at least through 2030.

Accelerated 5th-Generation F-35 Procurements

Germany’s 35-aircraft F-35A contract for nuclear-sharing roles anchors a regional commitment exceeding EUR 30 billion (USD 35.16 billion) to 2030. Belgium, Romania, and the Czech Republic follow with fleet conversions, valuing NATO interoperability over developmental risk. While US ITAR constraints raise sovereignty alarms, smaller forces accept dependency to secure near-term, 5th-generation capability envelopes. Resulting volume propels single-engine demand and reinforces a cost-per-flight-hour benchmark that influences future 6th-generation affordability discussions.

Launch of 6th-Generation Programs FCAS and GCAP

FCAS partners have earmarked over EUR 100 billion (USD 117.18 billion) through 2040, but Franco-German frictions over workshare and IP have brought schedule risks to the forefront. GCAP achieved EU regulatory clearance in June 2025, offering an alternative governance model for multilateral design authority and technology-sharing that sidesteps Brexit complexities. Flight-test activity under the STAR demonstrator validates manned-unmanned teaming concepts and sustains engineering workforces between production cycles. Although initial deliveries sit beyond 2035, the programs inject long-term demand visibility and anchor indigenous propulsion and sensor roadmaps critical to the European fighter aircraft market.

Ageing Legacy Fleets Approaching End of Life

The imminent retirement of Tornado, AMX, EF-18, and older F-16 variants drives overlapping replacement windows that exceed current assembly capacity. Structural-life exhaustion forces air forces to balance costly service-life extensions against new-build purchases, with many opting for mixed stop-gap and long-term fleets. More than 400 retirements will materialize before 2030, maintaining a high floor for the European fighter aircraft market demand.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring acquisition and life-cycle costs | −0.9% | Smaller European air forces | Long term (≥ 4 years) |

| Export-control/ITAR constraints on subsystems | −0.6% | EU Member States, UK, non-NATO Europe | Medium term (2–4 years) |

| Lengthy development and certification timelines | -0.5% | European nations developing indigenous platforms | Long term (≥ 4 years) |

| Engine-core production bottlenecks in Europe | -0.4% | Germany, UK, France, Spain (Eurojet consortium countries) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Soaring Acquisition and Life-Cycle Costs

F-35A unit prices exceed USD 80 million, while an upgraded Eurofighter approaches USD 120 million when development amortization is included.[2]European Parliament, “Financing the European Defence Industry,” europarl.europa.eu Sustainment typically accounts for 60–70% of total ownership, locking governments into multi-decade funding streams that squeeze other readiness accounts. The European Defence Agency (EDA) estimates that fragmented national buys add 20–30% to unit costs, yet political preferences for local workshare often trump economies of scale. Consequently, affordability pressures may moderate volumes after the current surge, tempering the long-run growth curve for the European fighter aircraft market.

Export-Control/ITAR Constraints on Subsystems

ITAR licensing remains a chokepoint for non-US content ambitions, as seen when US veto rights complicated Saab Gripen export talks in 2024.[3]Lexology, “Security Action for Europe,” lexology.com The EU now demands 65% European-origin subsystems for publicly financed defense programs, forcing indigenization of engines, avionics, and weapons interfaces. While the shift fosters sovereignty, it also inflates R&D outlays and extends timelines, suppressing near-term addressable demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Take-off and Landing: CTOL Pre-eminence Sustains, VTOL Gains Ground

CTOL aircraft accounted for 62.25% of the European fighter aircraft market in 2025, underpinned by well-established basing infrastructure and NATO STANAG-compliant runways. Fleet operators prize lower acquisition and sustainment costs versus STOVL peers, enabling broader force structure coverage. The European fighter aircraft market anticipates incremental CTOL orders from Germany, Spain, and Poland as life-extension deadlines converge.

VTOL/STOVL jets chart a 7.54% CAGR from a low base. Italy declared F-35B initial operating capability aboard the Cavour in 2024, validating integration pathways yet exposing deck-space and maintenance intensity challenges. The UK’s Queen Elizabeth-class carriers field the region’s largest STOVL air wing, but readiness rates below 65% spotlight sustainment burdens. Spain’s 2025 decision to forgo F-35B acquisitions underscores fiscal and operational trade-offs that could cap long-term penetration. Even so, carrier-based deterrence needs and dispersed-basing concepts keep VTOL demand visibly on the radar of the European fighter aircraft market.

By Fighter Generation: 4.5th-Gen Resilient Amid 6th-Gen Anticipation

4th- and 4.5th-generation aircraft make up more than 80% of active inventories; 4.5th-gen alone held 43.12% of Europe's fighter aircraft market share in 2025. Eurofighter Typhoon commands the most extensive installed base, and Italy's March 2025 EUR 2.8 billion (USD 3.28 billion) order for up to 24 additional units extends production through 2028.

6th-generation programs exhibit an 8.18% CAGR as FCAS and GCAP progress from concept stage to demonstrator testing. While timelines stretch beyond 2035, down-selects on common propulsion, adaptive engines, and collaborative combat sensors are already shaping supplier ecosystems. For the European fighter aircraft market, this creates a dual-track procurement landscape where 4th—and 5th-generation aircraft bridge capability gaps until 6th-generation units become operational.

By Engine Configuration: Cost-Focused Single-Engine Versus Capability-Led Twin-Engine

In 2025, single-engine designs represented 55.31% of the European fighter aircraft market, as the F-35A/B/C and Gripen families capitalized on cost-per-flight-hour advantages. High-thrust-to-weight ratios and proven safety records alleviate historical reliability concerns, making single-engine jets a preferred choice for smaller budgets.

Twin-engine fighters advance at a 6.81% CAGR, fueled by range, payload, and redundancy requirements integral to deterrence-oriented operations. Eurojet EJ200 production sustains Eurofighter fleets, but long lead times—now exceeding 36 months—expose capacity constraints. Strategic autonomy ambitions drive R&D for the European Combat Engine, which is anticipated to power 6th-generation prototypes and reduce reliance on US propulsion technology.

By Mission Role: Multi-Role Flexibility Sets the Pace

Air-superiority platforms captured 41.02% of the European fighter aircraft market share in 2025, yet growth momentum shifts toward multi-role variants posting a 7.72% CAGR through 2031. Combat lessons from Ukraine show that survivability and adaptability trump single-mission optimization. Eurofighter’s Phase 4 Enhancements package adds Storm Shadow and SPEAR 3, turning a pure fighter into a swing-role asset.

Close-air-support and dedicated strike aircraft fade as newer platforms integrate precision-strike and ISR payloads by design. For the European fighter aircraft market, multi-role dominance implies future procurements will prioritize digital avionics, data-link interoperability, and modular weapon stations over specialized airframes.

By End User: Air-Force Core, Naval Aviation Rising

Air Forces still account for 52.45% of overall demand, but Naval Aviation accelerates at 8.34% CAGR as France, Italy, and the UK elevate carrier airpower. The Charles de Gaulle refit and the Queen Elizabeth-class deployment cycles require sustained air wing onboarding and pilot qualification.

Marine/Army Aviation remains niche, focusing on light-attack and trainer derivatives rather than high-end fighters. Nevertheless, naval aviation's growth introduces new logistics streams—catapult/trap spares, corrosion protection, and shipborne support equipment—that broaden the European fighter aircraft industry's footprint.

Geography Analysis

France led the European fighter aircraft market in 2025 with 39.85% revenue share, buttressed by Dassault Rafale export wins and strategic use of state export-credit instruments. Domestic orders combine with overseas campaigns in the Indo-Pacific and Middle East, keeping production lines warm until FCAS milestones mature. Germany shows the highest growth at 7.11% CAGR through 2031 as Bundeswehr aviation shifts from Tornado to F-35A and reinvests in Airbus-led digital backbone solutions.

The UK remains a pivotal node despite post-Brexit regulatory changes. Typhoon upgrades, GCAP leadership, and a vibrant SME ecosystem sustain a robust home market. Italy balances Eurofighter and F-35 integration, leveraging Leonardo’s sensor and avionics strengths for domestic and export contracts. Spain navigates FCAS commitments amid budget ceilings, while Sweden’s Saab prioritizes Gripen E/F exports but wrestles with ITAR engine vetoes. Eastern European members—including Poland, Romania, and the Czech Republic—rapidly shift toward 5th-generation fleets to cement the interoperability of NATO. However, comparatively modest fleet sizes temper their aggregate effect on the European fighter aircraft market size. Across the bloc, emergent “Buy European” clauses and 60-day plant-approval rules should accelerate sovereign supply-chain projects and constrain extra-regional suppliers.

Competitive Landscape

The European fighter aircraft industry exhibits moderate concentration: Airbus, BAE Systems, Dassault, and Leonardo—often through joint ventures—control nearly 75% of capacity. Rising defense spending and 6th-generation programs reinforce incumbent dominance and invite software-centric entrants.

Strategic moves in 2025 signal consolidation around sovereign value chains. Airbus launched its Wingman concept under the STAR demonstrator to showcase human-machine teaming, while Dassault publicly asserted readiness to solo-develop a 6th-generation airframe if FCAS governance falters. BAE Systems converged combat cloud research with Leonardo’s ECRS Mk2 radar to streamline standard mission-data pipelines.

Law-firm briefs reveal that new EU readiness packages will privilege contractors meeting 65% European content, intensifying vertical-integration strategies. Technology disruptors such as Helsing pitch AI-enabled battle-management systems aimed at wingman drones, pressuring primes to quicken software release cycles. Despite these entrants, certification barriers and security-cleared labor pools continue to favor established aerospace groups within the European fighter aircraft market.

Europe Fighter Aircraft Industry Leaders

Saab AB

Airbus SE

BAE Systems plc

Lockheed Martin Corporation

Dassault Aviation SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EU cleared the UK-Italy-Japan GCAP joint venture for 6th-generation fighter development.

- December 2024: Italy ordered up to 24 additional Eurofighter Typhoon jets for EUR 2.8 billion (USD 3.28 billion).

Europe Fighter Aircraft Market Report Scope

A fighter aircraft is termed a high-speed aircraft equipped to carry out air-to-air combat operations and missions. Smaller size, ease of maneuvering, and high speed are some of the features of a fighter aircraft. It can carry heavy payloads, perform electronic warfare and air-to-air combat, and has ground attack capabilities.

The Europe fighter aircraft market is segmented by take-off, landing, and country. By take-off and landing, the market is segmented into conventional take-off and landing aircraft, short take-off and landing aircraft, and vertical take-off and landing aircraft. The market is segmented by country into the United Kingdom, Germany, France, Russia, Italy, and the Rest of Europe.

The market sizing and forecasts have been provided in value (USD billion) for all the above segments.

By Take-off and Landing

| Conventional Take-off and Landing (CTOL) |

| Short Take-off and Landing (STOL) |

| Vertical Take-off and Landing (VTOL/STOVL) |

By Fighter Generation

| 4th Generation |

| 4.5th Generation |

| 5th Generation |

| 6th Generation/NGAD |

By Engine Configuration

| Single-Engine |

| Twin-Engine |

By Mission Role

| Air-Superiority |

| Multi-Role |

| Close-Air-Support/Strike |

By End User

| Air Force |

| Naval Aviation |

| Marine/Army Aviation |

By Geography

| Germany |

| United Kingdom |

| France |

| Russia |

| Spain |

| Sweden |

| Austria |

| Rest of Europe |

| By Take-off and Landing | Conventional Take-off and Landing (CTOL) |

| Short Take-off and Landing (STOL) | |

| Vertical Take-off and Landing (VTOL/STOVL) | |

| By Fighter Generation | 4th Generation |

| 4.5th Generation | |

| 5th Generation | |

| 6th Generation/NGAD | |

| By Engine Configuration | Single-Engine |

| Twin-Engine | |

| By Mission Role | Air-Superiority |

| Multi-Role | |

| Close-Air-Support/Strike | |

| By End User | Air Force |

| Naval Aviation | |

| Marine/Army Aviation | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Sweden | |

| Austria | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe fighter aircraft market in 2026?

The Europe fighter aircraft market is valued at USD 15.04 billion in 2026.

Which country leads regional demand?

France commands 39.85% of 2025 revenue, thanks to Rafale exports and FCAS leadership.

What is the fastest-growing end-user segment?

Naval aviation shows the quickest rise with an 8.34% CAGR through 2031.

When will sixth-generation fighters enter European fleets?

FCAS and GCAP prototypes progress through the late 2020s, but operational squadrons are not expected before the mid-2030s.

Why are single-engine fighters popular in Europe?

F-35 procurement and lower life-cycle costs keep single-engine designs at 55.31% market share in 2025, serving budget-constrained forces.

What policy change most influences future orders?

The EU’s SAFE loan facility delivers EUR 150 billion of low-cost financing, accelerating procurement timelines through 2030.

Page last updated on: