Ethylene Vinyl Acetate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

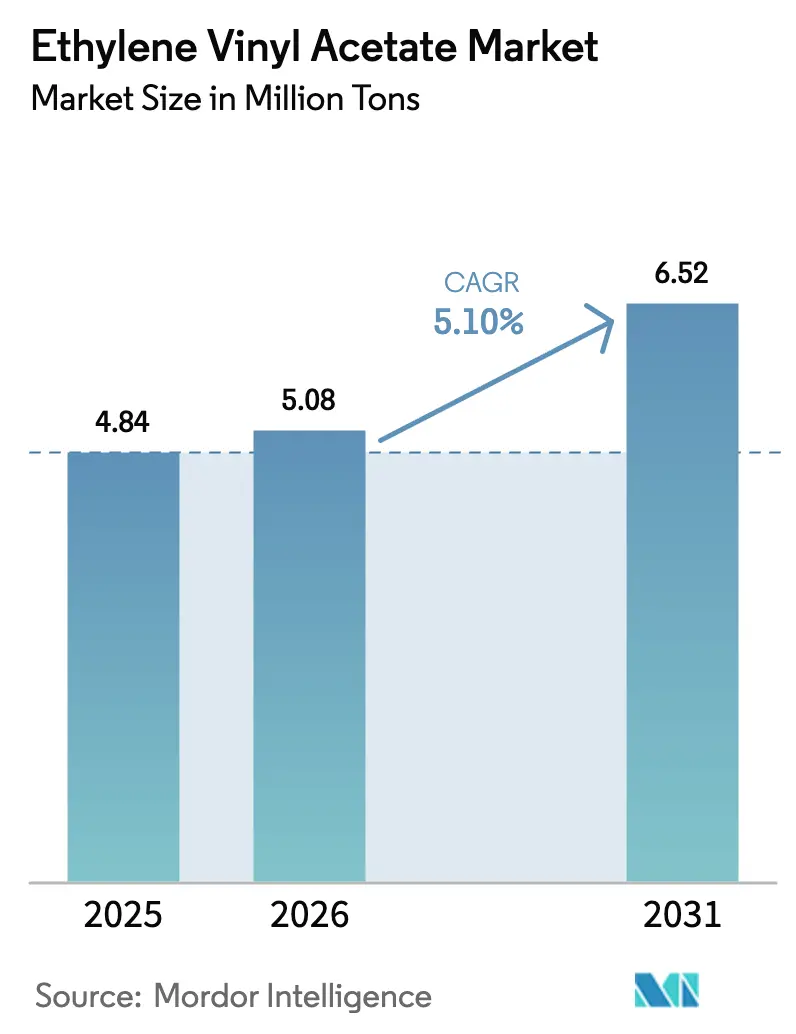

| Market Volume (2026) | 5.08 Million tons |

| Market Volume (2031) | 6.52 Million tons |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

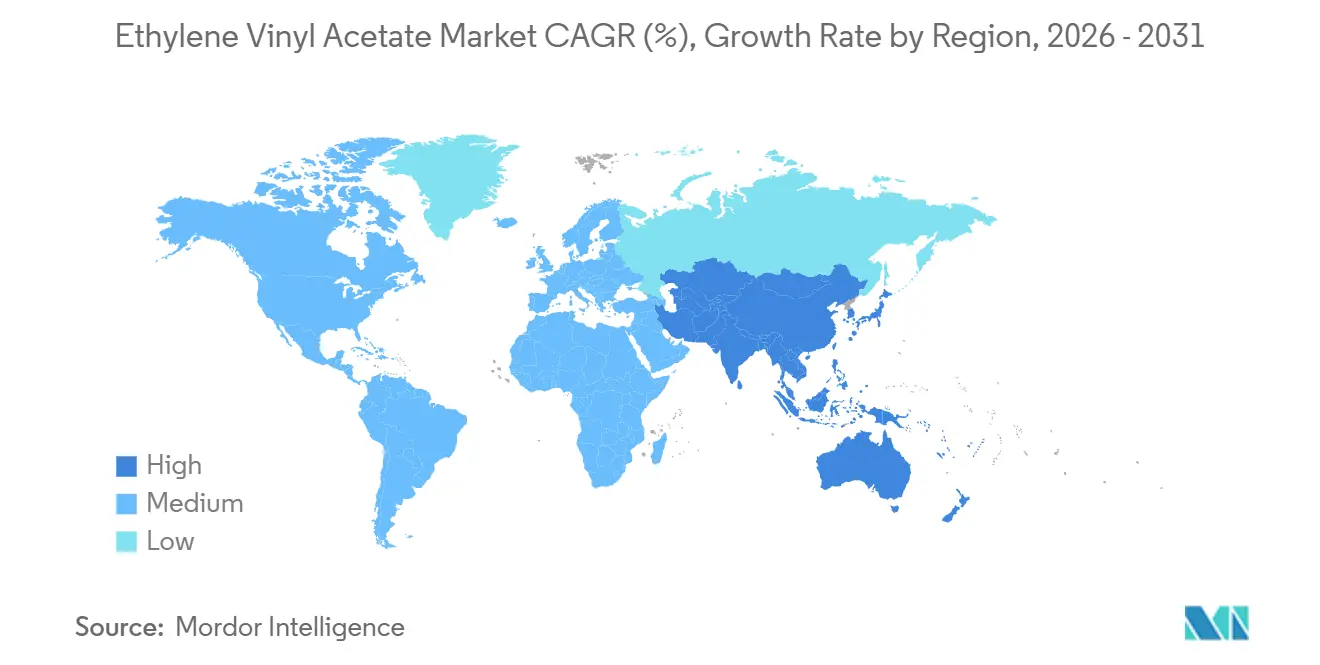

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

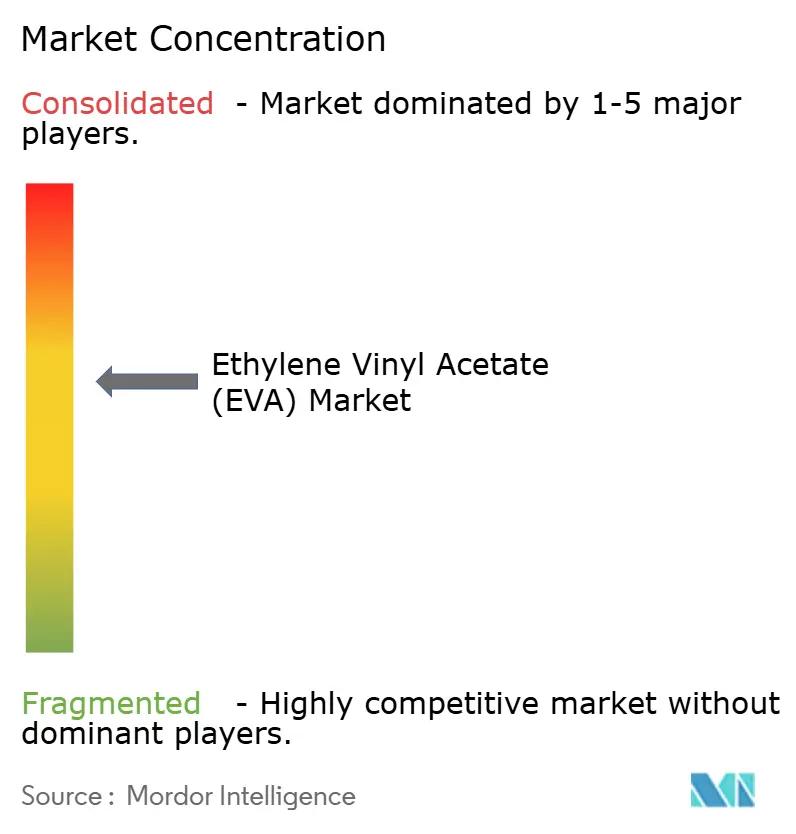

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethylene Vinyl Acetate Market Analysis by Mordor Intelligence

The Ethylene Vinyl Acetate Market size was valued at 4.84 million tons in 2025 and is estimated to grow from 5.08 million tons in 2026 to reach 6.52 million tons by 2031, at a CAGR of 5.10% during the forecast period (2026-2031). Persistent growth stems from solar‐photovoltaic encapsulants, Asian footwear foam production, and the migration of e-commerce packaging toward recyclable multilayer films. However, the industry wrestles with feedstock swings in ethylene and vinyl acetate monomer (VAM), as well as substitution threats from polyolefin elastomers (POE) and thermoplastic polyurethanes (TPU). Integrated petrochemical groups maintain margin resilience by backward integrating into ethylene and VAM, while smaller converters face intense competition from rising Korean and Chinese capacities. Bio‐based and recycled grades, meanwhile, create premium niches as regulators demand circular content.

Key Report Takeaways

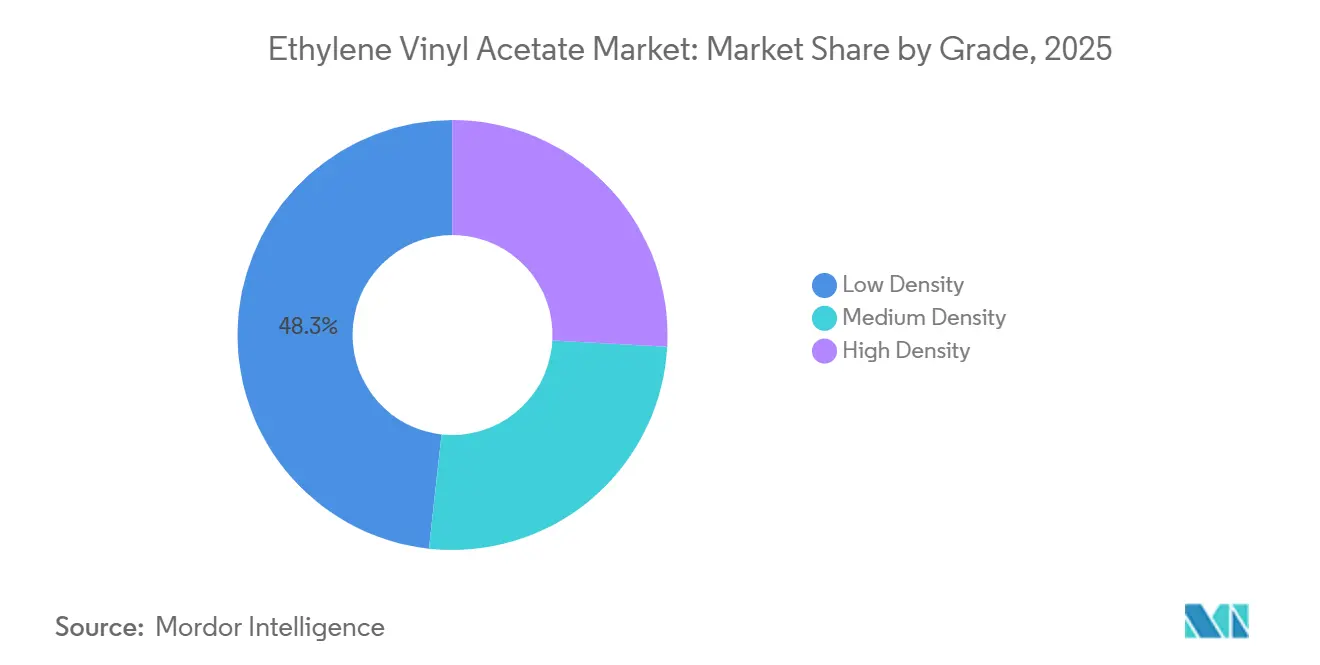

- By grade, low-density EVA held 48.25% of the ethylene vinyl acetate market share in 2025; high-density grades are forecast to grow at a 6.46% CAGR through 2031.

- By application, films accounted for 44.90% of the ethylene vinyl acetate market size in 2025, while solar cell encapsulation is set to expand at a 7.01% CAGR to 2031.

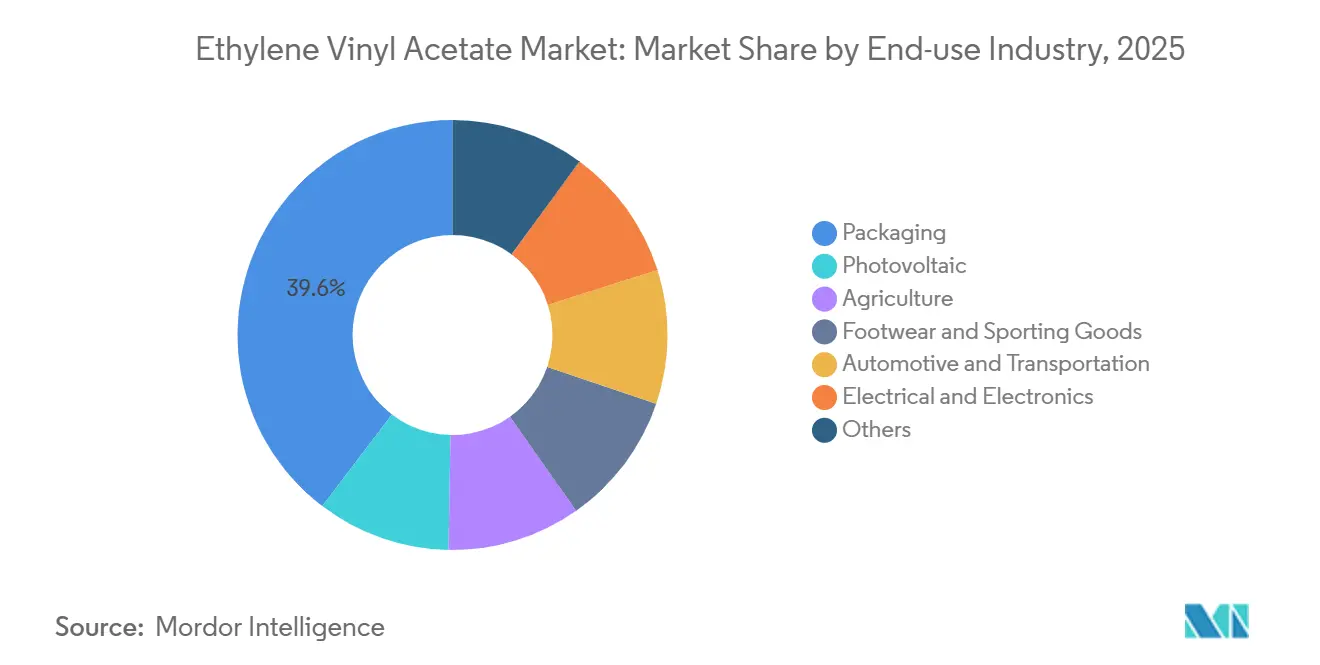

- By end-use, packaging led with 39.64% revenue share in 2025; photovoltaic applications will post the fastest 6.59% CAGR between 2026 and 2031.

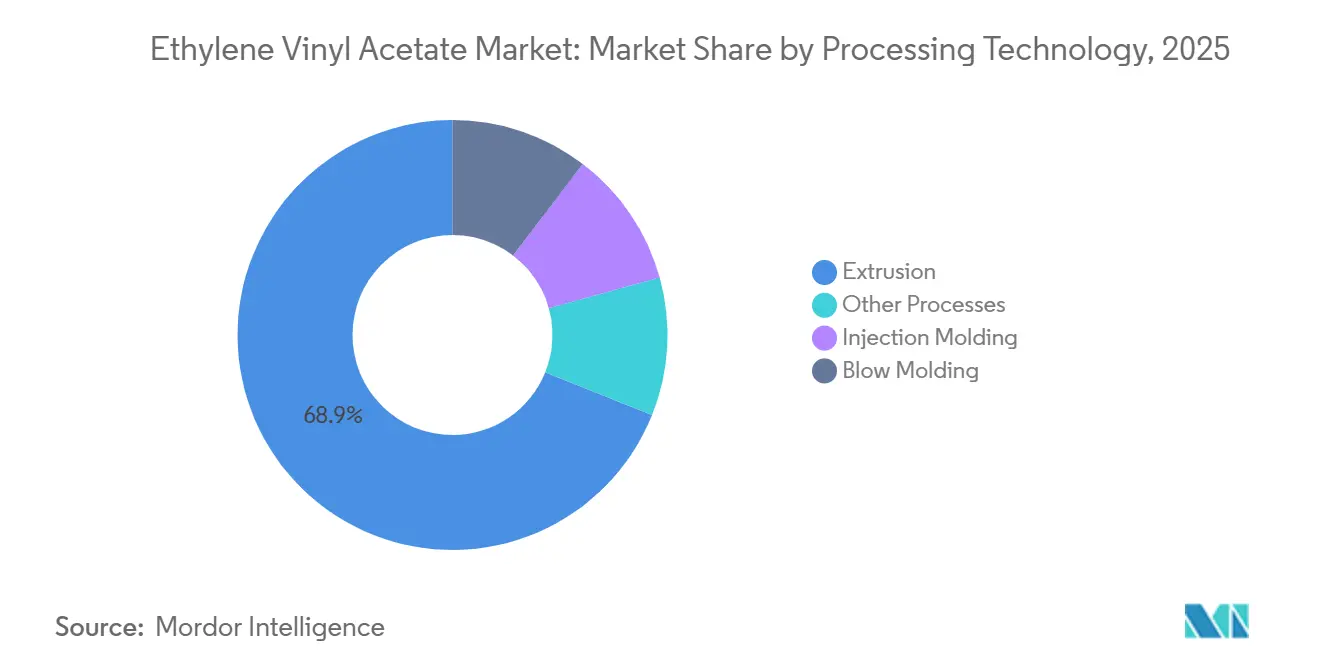

- By processing technology, extrusion captured 68.94% share of the ethylene vinyl acetate market size in 2025 and is advancing at a 6.18% CAGR through 2031.

- Asia-Pacific commanded 63.11% of the ethylene vinyl acetate market share in 2025 and is projected to grow at a 6.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ethylene Vinyl Acetate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Asian footwear output based on lightweight EVA foams | +1.2% | APAC core (India, Vietnam, China), spill-over to Southeast Asia | Medium term (2-4 years) |

| Packaging shift to recyclable multilayer EVA films in North America | +0.8% | North America and EU | Long term (≥ 4 years) |

| Rapid solar-PV build-out boosting high-VA EVA encapsulants | +1.9% | Global, with concentration in APAC, Middle East, Southern Europe | Short term (≤ 2 years) |

| APAC e-commerce explosion driving demand for EVA hot-melt adhesives | +0.7% | APAC core, emerging in Latin America | Medium term (2-4 years) |

| Autoclave-route EVA capacity expansions lowering unit costs | +0.5% | Global, led by China, Middle East, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Asian Footwear Output Based on Lightweight EVA Foams

India’s footwear sector consumes roughly 55% of domestic EVA, dominated by injection-molded soles and lightweight sandals that reduce shipping costs and improve comfort. Contract manufacturing is shifting from China’s coastal hubs to Vietnam and Indonesia, lifting regional demand for compression-molded EVA foams. Patent filings in 2024–2025 document multi-hardness formulations that lower shrinkage and enable tighter tolerances for automated assembly lines[1]Chinese National Intellectual Property Administration, “EVA Sole Patents,” cnipa.gov.cn. ISO 9001-certified plants achieve consistent density profiles essential for robotic footwear insertion. Yet TPU midsoles are encroaching on premium running shoes because they deliver higher energy return and can be reground, aligning with circular-economy mandates[2]BASF, “Polyurethane Footwear Solutions,” basf.com. Producers able to deliver ultra-light, high-rebound EVA grades at competitive prices will protect their share in the mass-market segment.

Packaging Shift to Recyclable Multilayer EVA Films in North America

Extended producer responsibility laws in California, Colorado, Maine, and Oregon levy fees on non-recyclable packaging, prompting converters to redesign multilayer films around recyclable structures that retain EVA tie-layers below 5 wt%. The European Union’s Packaging and Packaging Waste Regulation 2025/40 ramps recycled-content requirements to 35% by 2030 and 65% by 2040. Dow and Valoregen’s circular-feedstock deal will supply 15,000 t per year of certified content, while Mura Technology targets 600,000 t of advanced-recycling output by 2030. Celanese lifted Edmonton capacity by 35% in 2023 to meet recyclable-film demand. Brand owners paying eco-modulated fees favor resins that carry ISCC PLUS certificates, ensuring traceable circular attribution.

Rapid Solar-PV Build-Out Boosting High-VA EVA Encapsulants

Solar levelized costs below USD 0.03/kWh in high-irradiance regions are inducing multi-GW procurement pipelines. China produced 800 GW of modules in 2024, yet Longi Green Energy posted a RMB 5.26 billion loss on a 60% price collapse, showing that volume growth does not equate to profitability. High-VA EVA (28%–33% VA) remains the dominant encapsulant at 42% share, prized for optical clarity and adhesion. However, Dow’s ENGAGE POE limits power loss to 0.3% over 25 years versus 35% for conventional EVA, expanding POE share to 11%–14%. India’s antidumping duties of USD 537–1,559/ton on EVA imports fragment supply chains and underscore security-of-supply risk. Suppliers investing in autoclave capacity and localized feedstocks can ride the solar wave while defending margins.

APAC E-Commerce Explosion Driving Demand for EVA Hot-Melt Adhesives

China shipped more than 120 billion parcels in 2024, and India’s e-commerce parcel count is rising at double digits as digital payments proliferate. EVA hot-melt bonds recycled carton board at conveyor speeds above 1,000 boxes per hour without solvents, suiting automated warehouses. Nevertheless, polyolefin-based adhesives offer superior heat resistance in tropical hubs that regularly exceed 40 °C. Celanese expanded its Nanjing vinyl-acetate-ethylene line by 70,000 t in April 2024 to feed Southeast Asian hot-melt formulators. Multinationals now audit suppliers for ISO 14001 compliance, making environmental certification a qualifying hurdle.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethylene and VAM feedstock price volatility | -0.9% | Global, acute in import-dependent regions (Europe, Southeast Asia) | Short term (≤ 2 years) |

| EU and US single-use-plastic crackdowns | -0.6% | EU, North America, spill-over to export-oriented Asian producers | Medium term (2-4 years) |

| POE and TPU gaining share in solar and footwear | -0.7% | Global, concentrated in premium segments (high-efficiency modules, athletic footwear) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ethylene and VAM Feedstock Price Volatility

Spot ethylene averaged USD 835-845/t CFR Southeast Asia in September 2025, down 15% year-on-year as new crackers came online in China and the Middle East. VAM tracks acetic acid and ethylene, creating dual exposure that strains non-integrated EVA players. Korean majors cut more than 3.66 million t of ethylene output in December 2025, pushing operating rates below 70% and idling crackers at LG Chem, Lotte Chemical, and Hanwha Solutions. Europe faces added cost from the Carbon Border Adjustment Mechanism in 2026, punishing fossil-based feedstocks. Dow’s Fort Saskatchewan net-zero ethylene project aims to decouple margins from fossil volatility by 2029. Long-term ethane or bio-naphtha contracts will differentiate cost leaders from spot buyers.

EU and US Single-Use-Plastic Crack-Downs

The EU Single-Use Plastics Directive bans several disposable items and requires 90% bottle-collection rates by 2029, creating a cost pass-through to resin producers. The new Packaging and Packaging Waste Regulation grades films for recyclability and demands 35% recycled content by 2030, penalizing multilayer laminates lacking circular design. California SB 54 similarly obliges brand owners to finance collection schemes, raising non-recyclable formats’ unit cost by up to USD 0.05. REACH preregistration for VAM adds laboratory and dossier expenses that smaller EVA producers struggle to absorb. Firms forging chemical-recycling partnerships secure certified circular feedstock that satisfies regulators and unlocks premium pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Premium Solar Needs Lift High-Density EVA

High-density EVA achieved a 6.46% CAGR outlook through 2031 as bifacial and heterojunction solar modules require 28%–33% VA content to guarantee optical transmission and adhesion across 25 years, placing the segment ahead of overall ethylene vinyl acetate market growth. Low-density resin, dominant at 48.25% in 2025, underpins commodity films and mass-market footwear that value melt-flow indices above 20 g/10 min for fast cycle times. Tubular reactors supply these grades at lower capital cost, maintaining competitiveness in price-sensitive packaging. Medium-density EVA bridges hot-melt adhesives and wire-cable jacketing, where flow and cohesive strength must balance. ISCC PLUS-certified biomass EVA from Dow-Mitsui, launched in September 2024, offers a drop-in replacement across density tiers for brand owners disclosing Scope 3 emissions. Compliance with US FDA 21 CFR 177.1350 and EU Reg 10/2011 caps VA content at 50% and sets migration limits, forcing solar-grade suppliers to validate low residual monomer levels.

Localization plays heavily in China, which hit 70% solar-grade self-sufficiency in 2023 and pursues 85% by 2030, cutting import reliance on South Korean and Japanese producers subject to Indian antidumping duties. BASF-YPC plans a 300,000 ton expansion in Nanjing, leveraging LyondellBasell tubular technology to service both domestic solar and export customers. Low-density resin faces substitution from TPU midsoles in high-performance sports shoes but retains primacy in cost-driven markets. Agricultural greenhouse films continue to specify medium-density EVA with UV stabilizers to extend service life beyond five seasons in Mediterranean climates.

By Application: Solar Encapsulation Surges Past Films

Solar encapsulation will accelerate at 7.01% through 2031, overtaking flat film volume as global photovoltaic installations surpass 400 GW annually. The ethylene vinyl acetate market size for films remains significant at 44.90% in 2025, serving snack packaging, greenhouse covers, and laminated safety glass, yet its trajectory slows under single-use-plastic restrictions. Adhesives capture logistics tailwinds from e-commerce, although POE systems are winning share where heat resistance is vital. Foams for sandals, yoga mats, and buoyancy aids remain a mature arena; innovation now focuses on multi-color injection molding and anti-shrinkage additives. Other uses, including photovoltaic cables and LCD protective sheets, depend on evolving IEC and ISO standards that favor low-VOC resins.

Films intended for EU markets must incorporate 35% recycled content by 2030 and meet design-for-recycling Grade A, motivating converters to adopt mono-material polyethylene structures with EVA tie-layers kept below 5 wt%. Hot-melt formulators are purging phthalates in line with the ZDHC Restricted Substances List, pushing EVA producers to certify low-migration additive packages. Foam suppliers in athletic footwear are now balancing density reduction against rebound energy to compete with TPU’s 60% return benchmark.

By End-Use Industry: Photovoltaics Redraw Demand Mix

Photovoltaic installations will post a 6.59% CAGR, making them the fastest-growing end-use and reshaping the ethylene vinyl acetate market. Packaging still led at 39.64% in 2025, but extended producer responsibility fees are dampening growth. Agriculture leverages EVA greenhouse films that maintain photosynthetically active radiation transmission while filtering UV, extending crop cycles in Spain, Turkey, and Morocco. Footwear and sporting goods continue to buy EVA for lightness, though TPU captures premium niches requiring high energy return and recyclability. Automotive wire harnesses adopt EVA insulation compliant with IEC 62930 for rooftop PV cables, while electronics manufacturers specify clean-room-produced EVA for LCD protection films.

China’s 800 GW module output in 2024 signaled solar scale, yet Longi’s loss proved that volume does not guarantee profit. Indian antidumping measures raise localized resin prices, prompting domestic capacity expansion. Packaging converters tracking EU rules are negotiating long-term supply of certified circular EVA to avoid surcharges. Footwear brands now audit supplier factories for ISO 14001, consolidating orders among plants demonstrating low VOC emissions and tight density control.

By Processing Technology: Extrusion Remains Unassailable

Extrusion captured 68.94% of 2025 volume and will rise at 6.18% CAGR, reflecting high-throughput production of films and foams. Injection molding remains important for footwear soles and thin-wall parts but demands higher mold investment. Blow molding is confined to buoyancy aids and toys due to EVA’s melt viscosity, while compression molding continues in thick sheet foams. Celanese’s Edmonton debottleneck in 2023 added extrusion-grade capacity tailored to recyclable film converters. BASF-YPC’s forthcoming line will use tubular extrusion to supply medium- and high-density solar encapsulant resin. ISCC PLUS biomass EVA now offers processors a drop-in option without altering extruder screws or temperature profiles. Injection molders target melt-flow index optimization to shorten cycles, and Chinese patents reveal anti-shrinkage agents enabling multi-color soles with consistent dimensions. Industry 4.0 retrofits—melt-pressure sensors and AI-driven predictive maintenance—help converters cut scrap, lower energy use, and pull ahead of legacy plants.

Geography Analysis

Asia-Pacific contributed 63.11% of global ethylene vinyl acetate market volume in 2025 and will grow at 6.51% through 2031, buoyed by Chinese solar dominance and Indian footwear manufacturing. China operated 2.45 million tons of annual EVA capacity at 90.66% utilization in December 2023, yet still imported high-VA grades, prompting northwest coal-to-olefins investments. Zhenhai’s 1.5 million t ethylene expansion in 2024 and the Gulei Phase 2 cracker slated for 2025 reinforce upstream integration. South Korean players slashed 3.66 million t ethylene in 2025 due to oversupply, pressuring operating rates. Japanese producers such as Dow-Mitsui and Tosoh specialize in high-purity solar resin for export to Southeast Asia. India’s antidumping tariffs protect domestic EVA capacity but raise module production costs, accelerating interest in local autoclave projects.

North America held a mid-teens share in 2025. Celanese’s 35% Edmonton lift readied supply for recyclable film makers navigating new state EPR laws. Dow’s net-zero Fort Saskatchewan ethylene facility, planned for 2029 start-up, aims to shield margins from carbon taxes. Braskem’s USD 800 million Rio de Janeiro expansion will add 220,000 tons of ethylene by 2028 but hinges on financing stability. Mexico’s proximity to U.S. OEMs anchors automotive wiring demand, while greenhouse film consumption rises in high-value horticulture.

Europe’s share remains in the low double digits, constrained by strict waste and carbon rules. The Packaging and Packaging Waste Regulation demands 35% recycled content and could classify non-recyclable films as Grade C, triggering penalties. REACH dossiers for VAM drive compliance overhead. Germany and Italy still use EVA in rooftop solar and agriculture, but processors must certify low migration for food packaging. The Middle East is building integrated chains, exemplified by ADNOC’s Ruwais expansion and Saudi Aramco’s Jafurah field, preparing export barrels for Asia. South America experiences episodic growth, with Brazil’s agriculture films offsetting economic volatility; Argentine inflation curbs import capability despite greenhouse demand.

Value Chain Analysis

The EVA value chain starts with upstream ethylene and vinyl acetate monomer (VAM) production, typically located in integrated petrochemical and acetyl chains that can absorb feedstock swings and keep polymer units supplied. These monomers then move into high-pressure polymerization, with tubular routes used for commodity film and foam grades and autoclave routes used for tighter-molecular-weight solar encapsulant grades. After polymerization, compounding and formulation convert the base resin into application-specific packages, including hot-melt adhesives, foams, films, and encapsulant formulations, which are then turned into end products through conversion processes such as extrusion, injection, and lamination for packaging, photovoltaics, and footwear.

Key bottlenecks and leverage points are concentrated at large cracker-acetyl hubs and shaped by maintenance cycles and rationalization decisions. Those upstream events flow through to EVA availability and pricing, particularly for import-dependent regions. In Europe, supply tightness has been linked to asset downtime and rationalization, including an extended shutdown at TotalEnergies Gonfreville (offline since February 2025) and the closure of Versalis Dunkirk (since April 2025), underscoring how a limited number of large upstream complexes influence downstream supply. Downstream, mass-balance circularity is increasingly built into the chain without requiring segregated physical streams, illustrated by Celanese (May 2026) working with SharpCell Oy to incorporate CCU-derived building blocks into VAE binder systems using mass-balance at its Clear Lake, Texas facility, supporting converters and brand owners that need traceable circular attribution.

Competitive Landscape

The ethylene vinyl acetate market is moderately consolidated. Integrated groups enjoy feedstock control and global distribution, while regional Chinese companies erode price through capacity additions. Strategic moves revolve around low-cost geography expansions (northwest China coal-to-olefins, Middle East ethane-rich sites), certified circular feedstock agreements (Dow–Valoregen, Dow–Mura), and high-VA solar encapsulant innovation to mitigate POE substitution. Bio-based and recycled grades command 10%–15% premiums and help producers penetrate regulated packaging and footwear niches. Technology focus splits between tubular reactors for commodity films and autoclave units for narrow-MW solar grades. ISO 9001 and ISO 14001 certification, plus REACH VAM registration, form the license to operate in global value chains. Industry 4.0 controls cut defect rates, favoring producers who retrofit legacy lines before smaller rivals can match costs.

Ethylene Vinyl Acetate Industry Leaders

Exxon Mobil Corporation

Sinopec Yanshan Petrochemical Company

LOTTE Chemical Corporation

Dow

LG Chem

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is forming where converters need EVA solutions that meet circularity procurement requirements without changing line performance. The shift shows up in brand-owner and converter pull for certified content in packaging and adhesives, alongside supplier efforts to introduce mass-balance approaches, including Celanese using mass-balance accounting for CCU-derived building blocks in VAE binder systems at Clear Lake in May 2026. This expands the practical demand for EVA grades and tie-layer solutions that fit recyclability-oriented multilayer structures, for example by limiting EVA content in those films, while also providing certificates and documentation that help customers manage EPR-style fee modulation and recycled-content requirements.

In photovoltaics, the opportunity is less about incremental volume and more about encapsulation architectures and qualification standards. Tier-1 module makers are increasingly referencing harsh reliability testing, notably 85 degrees C/85% RH damp-heat performance, while discussions around multi-layer encapsulation films that can replace or augment standard monolayer EVA create a pathway for differentiated high-VA and specialty-film formulations. At the same time, new supply additions raise the weight of cost and regional security of supply: Sipchem awarded USD 187 million EPC contracts in June 2024 to expand its EVA plant in Saudi Arabia by 70,000 tons, and H&G Chemical commissioned a 300,000 tpa EVA plant in Yeosu in September 2025. Together, these investments push buyers to revisit sourcing mixes and drive producers to compete on consistency, qualification support, and integration with upstream ethylene and VAM.

Recent Industry Developments

- May 2026: ExxonMobil commercialized an ionomer-free vacuum skin packaging material for food that uses ExxonMobil EVA 06519FL polymer alongside Exceed performance polyethylene resins. This positions EVA as a functional replacement for ionomer-based structures in premium food packaging, with an emphasis on cost and supply-chain simplification while maintaining seal performance.

- September 2025: H&G Chemical commissioned a 300,000 ton per year EVA plant in Yeosu, South Korea. This added large-scale regional supply and increased competitive pressure on pricing and contract terms, particularly for converters sourcing solar and packaging grades in Asia.

- June 2024: Sipchem awarded USD 187 million EPC contracts to expand International Polymers Companys EVA plant in Saudi Arabia by 70,000 tons. The project strengthens Middle East integration into EVA exports and provides an additional supply base for customers seeking diversified sourcing beyond Northeast Asia.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers ethylene vinyl acetate (EVA) copolymer resin that is produced and sold as a material, and then used by converters in products such as films, foams, wire and cable compounds, hot-melt adhesives, and solar encapsulant layers.

Scope exclusions: Finished goods that contain EVA (for example, shoes or laminated items) are excluded to avoid double counting value that already sits in downstream product markets.

Segmentation Overview

- By Grade

- Low Density

- Medium Density

- High Density

- By Application

- Films

- Adhesives

- Foams

- Solar Cell Encapsulation

- Other Applications

- By End-use Industry

- Packaging

- Photovoltaic

- Agriculture

- Footwear and Sporting Goods

- Automotive and Transportation

- Electrical and Electronics

- Others

- By Processing Technology

- Extrusion

- Injection Molding

- Blow Molding

- Other Processes

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on EVA supply, demand, and pricing, so the model does not rely on one single data series. We use public and official sources such as the US International Trade Commission trade statistics, UN Comtrade, the International Energy Agency for macro energy and industry signals, and the US Geological Survey where relevant for petrochemical feedstock context. We also review customs and tariff schedules where EVA and close copolymers appear, along with peer-reviewed polymer and materials journals to confirm typical vinyl acetate content ranges, density behavior, and major use patterns.

Alongside public data, we use sources like company annual reports, investor presentations, and credible press to track capacity additions, maintenance cycles, and regional demand commentary. When needed, paid subscriptions are used for company financials and intelligence, shipment level import and export tracking, and patent databases to cross-check technology movement in PV encapsulants and specialty grades. This list is not exhaustive, and other sources were referred to during data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to sanity check what desk sources cannot fully confirm, especially grade splits, typical contract versus spot pricing behavior, and regional mix by application. We speak with a balanced set of stakeholders across resin producers, compounders, converters, distributors, and large end users in packaging, footwear components, and solar supply chains, and then reconcile differences by region so assumptions stay consistent. For a global market like EVA, inputs are validated across APAC, EMEA, and the Americas, since trade flows and pricing cycles can vary by hub.

The goal of the interviews is practical, not just directional: we confirm how much of reported sales is tied to EVA resin used in each converter application, and we use the same guidance to set shares when specialty grades are sold through distributors.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 18% | APAC: 45% |

| Mid tier: 43% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 19% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where production, capacity, operating rate signals, and trade movements are used to reconstruct regional resin availability, which is then mapped to consumption by major converter-driven applications. The numbers are corroborated with selective bottom-up approximations, such as sampled supplier revenue splits, channel checks on resin selling prices, and volume cross-checks using typical kg-per-unit needs in foams and solar encapsulant usage. Where a direct read is missing, for example specialty grades sold through distributors, the gap is handled by applying validated shares from interviews and then stress testing the result against import patterns.

Key inputs include ethylene and vinyl acetate feedstock price trends, new capacity and debottleneck announcements, operating rate cycles, average selling price ranges by VA content and end use, and demand signals from packaging film output, footwear midsole production, and solar module installations. Forecasts are generated using scenario analysis supported by short run regression checks, where drivers like solar buildout rates and packaging consumption are varied within realistic bands agreed with industry respondents. Forecast outputs are therefore easier to interpret and update when a driver shifts.

Data Validation & Update Cycle

All model outputs are checked against independent signals, including trade balances, capacity change timelines, and whether implied prices fall within the ranges validated in interviews. Outliers are reviewed in a second analyst pass, and assumptions are revisited when a region shows a sudden jump that cannot be explained by demand drivers or known supply events. If large variances remain, respondents are re-contacted to confirm whether the shift is temporary, such as a turnaround, or structural.

Reports are refreshed annually, and interim updates are made when material events occur, such as large plant additions, extended outages, or sharp feedstock moves that affect resin pricing. Before delivery, a final review is completed so the published view reflects the latest available public data and the most recent validation checks.

Mordor Intelligence's Ethylene Vinyl Acetate Market Size Compared Against Other Published Estimates

Published EVA market values can look far apart because groups do not always count the same unit, and some blend resin value with downstream product value. Differences also come from the year used for pricing, how trade is treated, and whether the estimate is anchored more on capacity signals or on end use demand.

By tracking feedstock-linked resin ASP movements and refreshing scope boundaries, Mordor Intelligence keeps the valuation tied to EVA resin sold into conversion uses rather than finished goods that simply contain the material, which is a key reason the spread shows up in the table.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.07 B (2024) | |

| Global Consultancy A | USD 11.65 B (2024) | Often blends resin and downstream value in selected applications, and it uses a broader grade mapping that can pull in adjacent copolymers, which lifts or shifts totals depending on region. |

| Industry Publisher B | USD 7.19 B (2024) | Uses a narrower application boundary and more conservative price realization for higher VA content grades, and it can understate value when solar encapsulant demand is treated as a smaller share. |

Taken together, the gap is mostly explained by what is counted as the market unit (resin versus downstream), and by how prices are normalized across grades and regions for the same year. Our approach stays traceable because each step links back to clear demand pools, trade checks, and price ranges that can be re-tested when new capacity or end use momentum changes.

Key Questions Answered in the Report

How large is the ethylene vinyl acetate market in 2026?

It is estimated at 5.08 million tons in 2026 and is forecast to climb to 6.52 million tons by 2031.

Which segment grows fastest within EVA applications?

Solar cell encapsulation is projected to expand at a 7.01% CAGR through 2031 as global PV installations soar.

What region dominates EVA demand?

Asia-Pacific controls 63.11% of global volume, led by China’s solar module output and India’s footwear industry.

Why is EVA facing substitution in solar modules?

POE encapsulants eliminate acetic-acid-induced degradation, reducing 25-year power loss from 35% to 0.3% in field trials.

How are regulations shaping EVA packaging demand?

By 2030, EU and U.S. EPR laws mandate recycled content, pushing converters to embrace circular EVA grades.

What drives EVA price volatility?

Fluctuating ethylene and VAM feedstock costs, amplified by regional oversupply and new carbon levies in Europe.

Page last updated on: